Since its introduction, the British Virgin Islands' annual financial reporting regime has entered its mature operational phase. Over 350,000 active BVI companies now operate under established BVI annual returns compliance requirements. Companies with December 31, 2024, financial year-ends recently passed their September 30, 2025, deadline, with attention now turning to the upcoming September 30, 2026, deadline for 2025 financial year returns.

The framework introduced through the BVI Business Companies Act amendments, effective January 2023, has stabilized into predictable compliance routines. Initial implementation phases, including extended deadlines, concluded June 30, 2025.

Companies now face standardized nine-month filing requirements. Understanding these BVI annual return obligations is critical for maintaining good standing and avoiding regulatory complications.

The Established Framework: Where BVI Annual Return Compliance Stands Today

Section 98A of the BVI Business Companies Act has operated fully since January 2023. The standard nine-month filing rule governs all BVI annual financial return submissions. The VIRRGIN system serves as the BVI financial account reporting system, operational since July 1, 2025, and provides registered agents with a standardized infrastructure for reporting non-compliance within 30 days of missed deadlines.

| Element | Current Position (December 2025) |

|---|---|

| Applicable Entities | All BVI Business Companies (unless exempt) |

| Filing Deadline | 9 months from financial year-end |

| 2024 Returns (Dec 31 FYE) | Due September 30, 2025 (passed) |

| 2025 Returns (Dec 31 FYE) | Due September 30, 2026 (upcoming) |

| Notification System | VIRRGIN (operational since July 2025) |

The regulatory framework rests on the BVI Business Companies (Financial Return) Order, 2023, establishing standardized templates and reporting formats.

This requirement exists independently of beneficial ownership reporting and government fee payments. The BVI annual returns supplement rather than replace other compliance obligations.

Core Components: What Constitutes an Annual Return

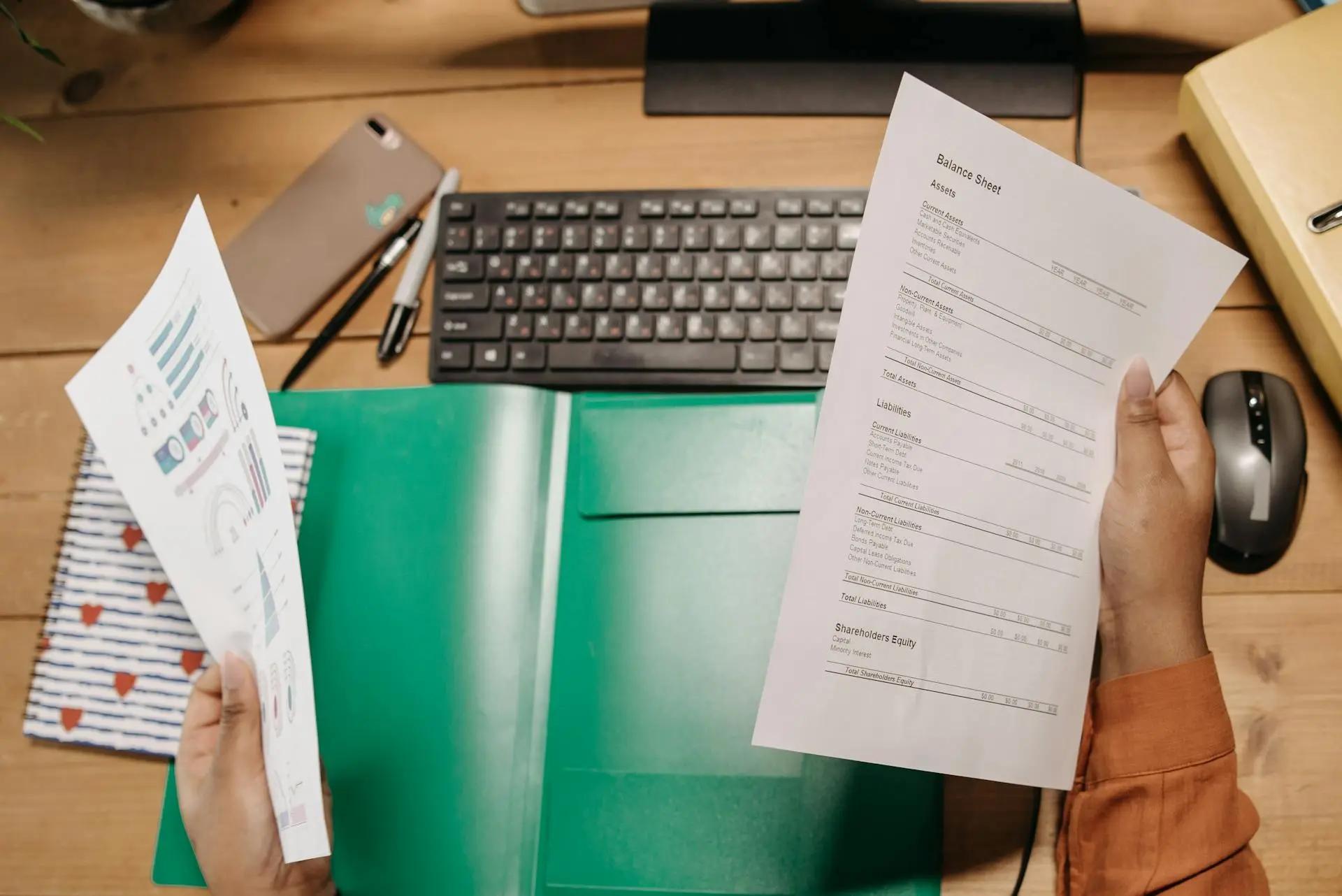

The annual return BVI consists of two fundamental documents: a Statement of Financial Position (balance sheet) and an Income Statement. This simplified structure provides high-level financial snapshots without requiring full IFRS-compliant financial statements or audit certification.

The BVI Financial Services Commission (FSC) imposes no mandatory accounting standards. While many companies adopt IFRS for consistency, any recognized accounting framework works, provided it produces reasonable financial accuracy. Directors bear statutory duties under Section 98A to ensure financial position accuracy. This creates personal accountability.

Currency flexibility extends across all major currencies. Companies may present their annual financial return in US dollars, pounds, euros, or any functional currency used in their accounting records. The official template appears in the Schedule to the BVI Business Companies (Financial Return) Order, 2023.

Understanding the Official Template Format

The BVI annual financial return template published by the FSC provides a standardized format that all companies must follow. The official BVI annual return form consists of two distinct sections with prescribed line items.

Balance Sheet/Statement of Financial Position

Assets:

- Cash and cash equivalents

- Loans and receivables

- Investments and other financial assets

- Tangible fixed assets

- Intangible assets

- Other assets

- Total Assets

Liabilities:

- Accounts payable

- Long-term debts

- Other Liabilities

- Total Liabilities

Shareholder's Equity:

- Single line item representing total equity

Income Statement

Revenue:

- Top-line sales or income

Cost of Sales:

- Direct costs producing revenue

Gross Profit:

- Calculated field (Revenue minus Cost of Sales)

Expenses:

- Operating expenses

- Other expenses

- Income tax expense

- Total Expenses

Net Income:

- Bottom line (Gross Profit minus Total Expenses)

You can download the BVI annual financial return template form at https://www.bvifsc.vg/sites/default/files/bvi_business_companies_financial_return_order_2023.pdf

Companies may add supplementary line items within these categories if needed for accurate presentation, but cannot omit prescribed items.

The template accommodates both active trading companies with revenues and expenses, and dormant holding companies showing primarily investments and equity with minimal operational activity.

Companies access the official template through the BVI FSC website or directly from their registered agents, who typically provide pre-formatted versions integrated into their submission platforms.

Mandatory Filing Obligations and Recognized Exemptions

Do BVI companies file annual returns? Yes, every BVI business company must file its BVI financial annual return annually.

However, four specific BVI annual return exemption categories exist:

- Listed companies whose securities trade on recognized stock exchanges enjoy exemption, reflecting existing public disclosure obligations under securities regulations. These entities already provide extensive financial reporting to securities regulators, making additional returns unnecessary.

- BVI-regulated entities filing financial statements with the FSC pursuant to financial services legislation receive an exemption. This encompasses regulated mutual funds, private investment funds, approved managers, and other financial services businesses already submitting comprehensive information under sector-specific frameworks.

- Companies submitting annual tax returns accompanied by financial statements to the BVI Inland Revenue qualify for exemption. While BVI imposes no corporate income tax on offshore companies, certain entities conducting business within the BVI file tax returns with supporting financial statements.

- Companies in liquidation receive a conditional exemption based on timing. If the annual return became due before liquidation commenced, filing remains mandatory. Only if liquidation began before the due date does the exemption apply.

Deadline Calculation: Determining Your Compliance Timeline

The universal nine-month window from the financial year-end determines all annual financial return BVI deadlines. Companies must understand their financial year structure—either the default calendar year or a board-adopted 12-month period.

Companies with December 31, 2024 financial year-ends faced their BVI annual returns deadline on September 30, 2025, which recently passed. These entities now prepare for 2025 returns due September 30, 2026. Non-calendar year companies calculate respective windows from adopted financial periods.

| 2025 Year-End | Filing Window Opens | 2026 Filing Deadline |

|---|---|---|

| December 31 | January 1, 2026 | September 30, 2026 |

| March 31 | April 1, 2025 | December 31, 2025 |

| June 30 | July 1, 2025 | March 31, 2026 |

A company with a March 31, 2025, year-end filed between April 1, 2025, and December 31, 2025. Its March 31, 2026, year-end return will be due December 31, 2026, using the same nine-month calculation.

Companies incorporated mid-year or never formally establishing annual financial return BVI periods default to calendar year structures unless directors execute board resolutions adopting alternative periods.

The Act does not permit extended first periods—a company incorporated on December 1, 2025, cannot extend its first period through December 31, 2026.

Submission Mechanics: The Registered Agent's Central Role

All BVI annual return submissions are routed exclusively through BVI registered agents, never directly to the Registry. This keeps returns confidential but allows regulatory oversight. Returns remain private and non-public.

Registered agents maintain custody for a minimum of five years at their BVI offices. Electronic or paper formats gain acceptance at the agent's discretion.

The VIRRGIN system handles non-filing notifications. Agents must report non-compliance within 30 days through this centralized infrastructure.

Only BVI competent authorities—the Financial Services Commission, International Tax Authority, Financial Investigation Agency, and Attorney General—possess statutory authority to request copies under specific circumstances. Standard company searches do not reveal return contents. This maintains corporate privacy but preserves regulatory access.

Post-Submission Process: Once submitted, registered agents review returns for completeness and formatting compliance before accepting them as filed. Companies receive written confirmation from their registered agent acknowledging receipt and confirming the filing date. This confirmation provides proof of compliance and should be retained in corporate records.

If a registered agent loses filed records through system failure, office damage, or other circumstances, the company bears responsibility for providing replacement copies. Companies must maintain independent archives of all submitted returns and confirmation receipts throughout the retention period.

Extension Requests and Special Circumstances

The BVI Business Companies (Amendment) Act, 2024 grants the Financial Services Commission authority to extend filing deadlines under Section 98A(2A). Companies facing genuine difficulties producing complete statements within nine months—such as ongoing audit processes, complex consolidations, or data access issues—may request extensions before deadlines expire.

Extension applications require submission to the FSC explaining specific circumstances preventing timely filing. The FSC evaluates requests individually, granting relief where justified.

Extensions granted apply to specific companies rather than industry-wide relief. This differs from the broad initial implementation extensions that expired June 30, 2025.

Companies should apply for extensions proactively rather than waiting until deadlines pass.

Penalties do not apply during granted extension periods. However, the FSC provides no guarantee of approval, making extension requests strategic decisions requiring careful timing and justification. Registered agents typically handle extension applications on behalf of companies.

Financial Penalties and Operational Impact

The BVI Business Companies Act establishes a statutory penalty framework for late filing under Section 98A. Companies failing to meet their filing deadlines become subject to financial penalties imposed by the Registrar of Corporate Affairs.

Statutory Penalty Structure:

- First month (or partial month): USD 300

- Each subsequent month: USD 200

- Maximum cumulative penalty: USD 5,000

The penalty regime operates progressively. Upon missing deadlines, companies become liable for USD 300 for the first month or partial month. Each subsequent month adds USD 200 until reaching the USD 5,000 maximum. A company three months overdue would face USD 700 in cumulative penalties (USD 300 + USD 200 + USD 200).

In September 2024, the BVI FSC announced it would not impose penalties on initial annual return filings "until further notice." The initial implementation extension period ended June 30, 2025, and the VIRRGIN notification system became operational July 1, 2025, for registered agents to report non-compliance.

Once maximum penalties apply with ongoing non-compliance, the Registrar holds discretionary authority to strike companies off the register entirely, effectively terminating legal existence. Struck-off companies lose all legal capacity to contract, hold assets, or maintain business relationships. Restoration is complex, costly, and not guaranteed.

Given the evolving regulatory environment, companies should prioritize timely filing regardless of penalty enforcement status. Loss of good standing alone creates substantial operational problems, making compliance the prudent course regardless of monetary consequences.

Effective Preparation: Documentation and Timing Strategies

Section 98A imposes duties on directors to exercise reasonable care in ensuring the company's financial position accuracy. This personal accountability exists independent of audit requirements.

Essential Documentation Checklist:

- Complete bank statements covering the full financial period

- All income invoices and receipts documenting revenue

- Expense documentation and supporting records

- Investment account statements and valuations

- Asset acquisition and disposal documentation

- Inter-company transaction records and agreements

- Foreign currency transaction details

The nine-month window compresses rapidly for complex structures. Companies should implement contemporaneous record-keeping throughout the year. Beginning documentation assembly 60-90 days before deadlines allows adequate time for registered agent coordination and data verification.

If a company has multi-currency operations, consolidated structures, or entities with limited in-house capabilities, it is recommended to engage accounting firms familiar with BVI annual report requirements, ensuring accuracy and deadline compliance.

Common Challenges and Solutions

Record Maintenance Issues

Companies lacking systematic record-keeping throughout financial years trigger last-minute reconstruction. The solution: implement quarterly bookkeeping reviews, monthly bank reconciliations, and continuous document scanning.

Financial Year Uncertainty

Companies sometimes lack formal documentation of their financial year. The default calendar year applies unless directors adopt alternatives via board resolution.

Companies should execute resolutions formally adopting chosen periods and communicate these to registered agents.

Dormant Company Assumptions

Dormant companies often assume exemptions apply. However, the BVI annual financial return mandate applies regardless of activity levels. Dormant entities must file returns reflecting nil operations. Inactivity is not an exemption criterion.

Multi-Currency Complexity

Operations across multiple currencies require converting to a single presentation currency. The regulations permit any major currency presentation. Companies should select their functional currency for presentation, and modern accounting software handles multi-currency bookkeeping efficiently.

Best Practices for Sustainable Compliance

- Implement Year-Round Records: Maintain organized digital systems capturing transactions contemporaneously for for BVI company annual return rather than reconstructing annually. This reduces preparation burden.

- Establish 60-Day Advance Timelines: Begin preparation minimum two months before deadlines. This creates buffers for complications and registered agent coordination.

- Document Financial Year Formally: Execute board resolutions clearly establishing financial periods, particularly for non-calendar years. This prevents confusion.

- Annual Exemption Reviews: Assess exemption qualification annually since business changes may affect eligibility.

- Monitor FSC Communications: Subscribe to BVI FSC circulars, receiving authoritative updates on deadline modifications or procedural changes.

- Engage Specialized Professionals: Retain accounting firms with demonstrated BVI annual return expertise for complex situations or when internal resources lack technical depth.

Frequently Asked Questions

If your financial year ended December 31, 2025, file your BVI annual financial return by September 30, 2026. Non-calendar year companies calculate nine months from their specific year-end. March 31, 2026, year-ends require filing by December 31, 2026.

No. The BVI annual return requirement applies regardless of activity levels unless specific statutory exemptions exist. Dormant companies must file returns reflecting nil operations. Inactivity does not constitute exemption criteria under Section 98A.

Annual returns remain private with registered agents. Only BVI competent authorities—FSC, International Tax Authority, Financial Investigation Agency, and Attorney General—can request copies under specific circumstances. Standard company searches do not reveal contents.

The BVI Business Companies Act establishes statutory penalties: USD 300 for the first month, then USD 200 per subsequent month (maximum USD 5,000). However, as of December 2025, companies should consult their registered agents about current enforcement policies. Regardless of monetary penalties, companies immediately lose Certificate of Good Standing status upon non-compliance, impacting banking relationships and commercial operations. At maximum penalties, the Registrar may strike companies off the register.

No. The BVI financial annual return does not require audit certification. Directors must exercise reasonable care, ensuring accuracy, but no audit mandate exists. Companies may use any recognized accounting standard.

These are separate obligations. Annual fees maintain registration status and are paid to the Registry. The BVI annual return provides financial information to your registered agent under Section 98A. Both exist independently—paying fees does not eliminate filing obligations.

Companies may prepare returns internally if directors possess adequate accounting knowledge and maintain accurate records. However, directors bear statutory responsibility for accuracy. Many engage professionals for complex structures or international operations.

Conclusion

In December 2025, the BVI annual return regime will be fully operational with established procedures. Approximately 356,675 active BVI companies navigate annual filing obligations that have become part of standard corporate governance. The upcoming September 30, 2026, deadline represents the third annual cycle for calendar-year companies.

Proactive preparation, systematic record-keeping, and timely registered agent engagement remain critical for success. The nine-month filing window provides adequate time when approached systematically.

Companies now treat annual return preparation as routine corporate governance rather than as an exceptional administrative burden.

We can manage your BVI company’s annual return filing for you, 100% remotely and online. For more details on how we can help you stay compliant, please visit our BVI Annual Return Filing service page.

Sources & References

- https://www.bvifsc.vg/news/industry-updates/industry-circular-26-2025-filing-initial-annual-returns

- https://www.bvifsc.vg/news/industry-updates/industry-circular-9-2025-bvi-fsc-extends-time-filing-initial-annual-returns

- https://www.bvifsc.vg/news/industry-updates/industry-circular-34-2024-filing-annual-returns

- https://www.bvifsc.vg/sites/default/files/bvi_business_companies_financial_return_order_2023.pdf

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.