Key Takeaways

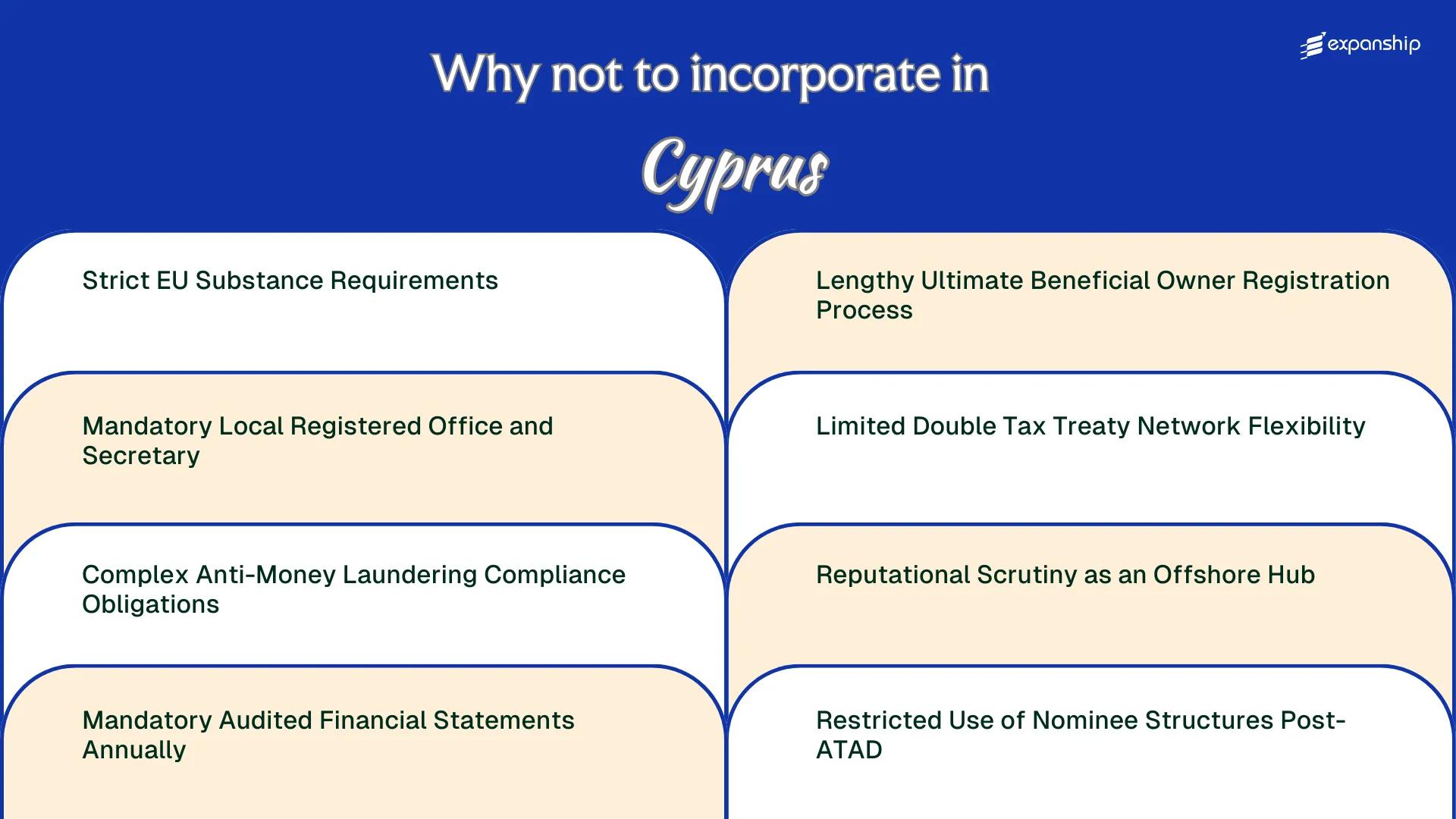

- Under the Companies Law, Cap. 113 and EU Anti-Tax Avoidance Directives, Cyprus companies must now demonstrate genuine economic substance, which creates ongoing staffing, office, and operational costs that hollow holding structures can no longer avoid.

- Cyprus imposes a mandatory annual audit requirement on all companies regardless of size or turnover, adding accounting and professional fees that jurisdictions with simplified reporting thresholds do not impose on smaller entities.

- Despite access to over 60 double tax treaties, Cyprus's network offers limited flexibility for certain routing structures following post-ATAD restrictions on nominee arrangements and increased scrutiny of passive income flows.

- Foreign investors face a multi-step Ultimate Beneficial Owner registration process through the Cyprus Registrar of Companies that introduces delays and ongoing disclosure obligations not present in less regulated offshore jurisdictions.

Cyprus operates under a heavily regulated corporate framework, shaped by its obligations as a European Union member state and its adherence to directives from bodies including the Cyprus Securities and Exchange Commission and the Institute of Certified Public Accountants of Cyprus. The disadvantages of incorporating in Cyprus span compliance burdens, structural restrictions, and reputational factors that affect how foreign-owned entities are perceived and administered.

Not every business will encounter these disadvantages equally. The specific challenges your firm faces depend significantly on its industry, ownership structure, and intended commercial activity.

This article is most relevant to non-EU investors and foreign entrepreneurs setting up holding companies, investment vehicles, or trading entities through Cyprus. Primary corporate governance obligations derive from the Companies Law, Cap. 113, which governs the formation and ongoing conduct of Cyprus-registered companies.

Strict EU Substance Requirements

Cyprus EU substance requirements risks are among the most operationally demanding aspects of maintaining a compliant holding or trading entity on the island. Meeting these requirements is not a formality; it carries measurable recurring costs.

What Genuine Economic Substance Actually Demands

Under the OECD BEPS framework and the EU's anti-avoidance directives, including ATAD and the Parent-Subsidiary Directive as applied through Cyprus tax law, your company must demonstrate genuine local management and control. This means resident directors making real decisions on the island, board meetings held locally, and core income-generating activities conducted from within the jurisdiction. For a foreign business owner managing operations remotely, this translates into either relocating key personnel or hiring qualified local directors at significant annual expense.

Why Tax Authorities Are Looking Harder

The EU's Code of Conduct Group and the OECD's Inclusive Framework have intensified scrutiny on Cyprus holding company substance restrictions, particularly for IP holdings and intra-group financing structures. Failing to satisfy substance tests risks reclassification of income in your home jurisdiction, denial of treaty benefits, or transfer pricing adjustments. A single adverse determination can eliminate the tax efficiency the structure was built to achieve.

If your company cannot evidence local management control through documented board decisions made in Cyprus, tax authorities in your home country may disregard the entity entirely for treaty or exemption purposes.

Mandatory Local Registered Office and Secretary

One of the more tangible Cyprus registered office requirements drawbacks is the obligation to maintain a physical registered address within the country at all times. Under the Cyprus Companies Law, Cap. 113, every company incorporated under that statute must have a registered office to which all official correspondence, regulatory notices, and legal service documents are directed.

This is not a formality you can satisfy with a virtual mailbox abroad. The address must be a genuine, locally maintained office, and any change must be formally notified to the Registrar of Companies.

Beyond the address, your firm must also appoint a company secretary who is typically Cyprus-resident and operationally accessible. That requirement creates ongoing costs even when the business conducts no activity locally.

For a foreign owner running operations entirely outside the island, these obligations translate into recurring friction:

- You pay annual retainer fees to a local provider for an address you never physically use

- Any lapse in maintaining the registered address can trigger compliance notices from the Registrar of Companies

- The mandatory local secretary Cyprus company rules mean you need a trusted third party with legal knowledge, not just a mailing contact

- Switching providers mid-year still requires formal filings, adding administrative time and cost

Cyprus Company Incorporation

Understand the full compliance structure before you incorporate, including registered office and secretary obligations under Cap. 113.

Complex Anti-Money Laundering Compliance Obligations

Cyprus AML compliance challenges are among the most demanding operational burdens a foreign business owner will encounter after incorporation. The primary legislation, the Prevention and Suppression of Money Laundering Activities Law of 2007 (as amended), along with directives transposed from the EU's Fourth and Fifth Anti-Money Laundering Directives, creates a layered set of obligations that require continuous legal attention, not just at setup.

Your company will likely qualify as an obliged entity under this framework, triggering mandatory KYC requirements for clients, counterparties, and sometimes shareholders. Collecting, verifying, and periodically updating that documentation is an ongoing administrative task that typically requires retaining a qualified compliance officer or outsourcing to a licensed AML service provider, both of which carry recurring costs.

| Requirement | Detail | Practical Burden |

|---|---|---|

| AML Compliance Officer | Mandatory for obliged entities | Additional staffing or outsourcing cost |

| Customer Due Diligence (CDD) | Required at onboarding and on material change | Ongoing documentation and review cycles |

| MOKAS Reporting | Suspicious activity must be reported to MOKAS | Legal exposure if thresholds are misapplied |

| Internal AML Policy | Written procedures required by law | Must be updated with each regulatory amendment |

MOKAS, the Unit for Combating Money Laundering, has authority to investigate and issue compliance directives. Failure to file a suspicious activity report, even where intent is absent, can trigger regulatory sanctions.

Foreign directors unfamiliar with EU AML standards often underestimate how frequently these policies must be reviewed. Each new EU directive amendment requires corresponding updates to internal procedures, creating a compliance cycle with no fixed endpoint.

Mandatory Audited Financial Statements Annually

All Cyprus-registered companies, regardless of size or activity level, are legally required to prepare and submit audited accounts each financial year under the Companies Law, Cap. 113. This is one of the more cited Cyprus mandatory audit requirements cons for foreign owners who are accustomed to jurisdictions where small or dormant entities are exempt from full statutory audit.

The audit must be conducted by a licensed auditor registered with the Institute of Certified Public Accountants of Cyprus (ICPAC). That restriction alone limits your choice of auditors and introduces a recurring professional fee that exists regardless of whether your company generated any revenue.

Even a dormant entity cannot simply file a nil return. The obligation to maintain IFRS-compliant financial statements and have them independently verified creates an annual cost floor that many foreign owners underestimate when projecting operational expenses.

- Annual audited financial statements are mandatory under Cap. 113 with no small-company exemption equivalent to UK or EU thresholds

- Auditors must hold a current ICPAC licence; foreign-licensed auditors cannot fulfil this requirement

- Audited accounts must be submitted to the Registrar of Companies as part of the annual return

- Dormant companies remain subject to the audit obligation, not just active trading entities

- Failure to file compliant accounts can result in striking-off proceedings by the Registrar

Unlike many EU member states that exempt micro-entities from statutory audit, Cyprus applies the full audit requirement to virtually all registered companies with no turnover-based threshold that triggers an exemption.

Lengthy Ultimate Beneficial Owner Registration Process

The Cyprus UBO registration process problems begin before your company can fully operate. Under the Prevention and Suppression of Money Laundering Activities Law (Law 188(I)/2007, as amended), all Cyprus companies must register their ultimate beneficial owners in the UBO Register maintained by the Registrar of Companies, and gaps in that process carry direct legal consequences.

Structural Delays in Registration

Submissions to the UBO Register require detailed documentation on each beneficial owner holding 25% or more of shares or voting rights, including certified identity documents and proof of address. Any inconsistency or missing field triggers rejection, forcing resubmission cycles that can extend the process by weeks, particularly for foreign nationals whose documents require notarisation and apostille.

Consequences for Foreign-Owned Entities

Failure to register accurately within the statutory timeframe exposes the firm to administrative fines. Beyond penalties, a company without a valid UBO registration may face restrictions when opening corporate bank accounts or satisfying due diligence requests from financial institutions, creating an operational bottleneck that disproportionately affects foreign-owned entities managing ownership structures across multiple jurisdictions.

Support for UBO Registration and Compliance Challenges in Cyprus

If your company's UBO registration is creating delays or exposing you to compliance risk, our Cyprus specialists can manage the process and documentation requirements on your behalf.

Limited Double Tax Treaty Network Flexibility

Cyprus double tax treaty limitations create measurable structural problems when your holding company depends on treaty access to reduce withholding taxes on dividends, interest, or royalties flowing from specific source countries.

- The DTT network covers around 65 treaties, but several high-growth markets your business may target — including Brazil, most of Sub-Saharan Africa, and parts of Southeast Asia — have no bilateral agreement in place, leaving distributions subject to full domestic withholding rates in those source countries.

- Treaties that do exist vary significantly in their withholding rate reductions, and some older agreements have not been updated to reflect current OECD standards, creating uncertainty around their practical application.

- Under the OECD Base Erosion and Profit Shifting framework, treaty access increasingly requires demonstrating genuine economic substance, which limits the ability to claim benefits under Cyprus DTT network restrictions without incurring real operational costs.

- Source countries applying Principal Purpose Tests under their domestic anti-avoidance rules can deny treaty benefits entirely, even where a valid agreement exists.

Reputational Scrutiny as an Offshore Hub

Cyprus offshore reputation risks are not hypothetical. The jurisdiction spent years on the EU's radar for enabling aggressive tax planning, and the reputational residue of that history still affects how banks, investors, and counterparties perceive entities registered there.

The European Commission's repeated scrutiny of the IP Box regime and the post-2013 bail-in crisis damaged confidence in Cypriot structures among international financial institutions. Some EU and US banks apply enhanced due diligence automatically to companies with a registered address in Nicosia or Limassol, regardless of actual business activity.

For your business, this translates into slower account opening, additional documentation demands, and, in some cases, outright rejection by correspondent banks. The offshore perception problem is not resolved by substance alone.

- Certain payment processors categorise Cyprus-registered entities under elevated-risk policies

- Some institutional investors require additional legal opinions before accepting a Cypriot entity as a counterparty

- EU state aid investigations into past tax rulings have increased scrutiny on Cypriot holding structures

A foreign-owned Cyprus holding company seeking to open a euro account with a Western European bank may be required to produce notarised director identification, a detailed source-of-funds declaration, and a legal opinion on corporate substance — a process that can cost upward of EUR 3,000 in professional fees before a single account is approved.

Restricted Use of Nominee Structures Post-ATAD

Cyprus nominee structure restrictions under ATAD have significantly narrowed how foreign owners can separate legal from beneficial control. The EU Anti-Tax Avoidance Directives, transposed into Cyprus law through amendments to the Income Tax Law and the Assessment and Collection of Taxes Law, require that arrangements must reflect genuine economic substance, not just formal legal form.

Under the General Anti-Avoidance Rule (GAAR) now embedded in Cyprus tax legislation, arrangements deemed to lack commercial reality can be disregarded by the Tax Commissioner. If your nominee structure exists primarily to obscure beneficial ownership or shift income without corresponding substance, it is exposed to re-characterisation, back-taxes, and penalties.

Nominee shareholding arrangements also intersect with UBO disclosure obligations under the Prevention and Suppression of Money Laundering Law, meaning the concealment benefit that historically attracted such structures is legally compromised regardless of ATAD.

The practical cost is not just legal risk. Maintaining a defensible nominee arrangement now requires documented evidence of economic rationale, which demands ongoing legal oversight and increases annual compliance expenditure.

If your structure relies on nominee arrangements without demonstrable economic substance in Cyprus, the Tax Commissioner holds statutory authority to disregard it entirely under the GAAR provisions, triggering full tax liability at the beneficial owner level.

Mitigating These Incorporation Challenges

Overcoming Cyprus incorporation challenges requires structural preparation before registration, not reactive adjustments after the fact.

- Register your entity's ultimate beneficial owners through the UBO Register maintained by the Registrar of Companies and Official Receiver, allowing sufficient lead time for verification delays.

- Appoint a Cyprus-resident company secretary and establish a locally registered office address prior to submission of incorporation documents.

- Engage a Cyprus-licensed auditor from incorporation, given that audited financial statements are a statutory requirement under the Companies Law, Cap. 113.

- Build a documented substance profile covering local directorship, decision-making records, and physical presence to satisfy EU ATAD and OECD BEPS compliance thresholds.

- Conduct an AML risk assessment aligned with the Anti-Money Laundering Law of 2021, ensuring your business falls within the correct due diligence tier before operations begin.

- Review available double tax treaty provisions specific to your target markets early, since the network's bilateral scope may require supplementary structuring at the holding level.

These steps address obligations set across multiple regulatory layers, including directives transposed into Cypriot law and requirements enforced by the Cyprus Securities and Exchange Commission and the Tax Department. Taken together, they reflect the density of the compliance framework any foreign business must account for when operating through a Cypriot entity.

Cyprus Still a Viable Business Destination

Despite the compliance demands covered throughout this blog, Cyprus company formation remains a credible option for businesses that can satisfy its structural and regulatory requirements. The jurisdiction holds EU membership, a 12.5% corporate tax rate, and an established legal system rooted in English common law, factors that continue to attract international capital.

| Pros | Cons |

|---|---|

| 12.5% corporate tax rate, one of the lowest within the EU | Annual audited financial statements are mandatory regardless of company size |

| EU membership provides access to EU directives and cross-border recognition | UBO registration through the Registrar of Companies involves procedural delays |

| Legal system based on English common law, familiar to common law practitioners | Substance requirements under EU ATAD directives limit the use of shell structures |

| Participation exemption on dividends and capital gains on share disposal | AML obligations under the Prevention and Suppression of Money Laundering Law demand ongoing compliance resources |

| Access to EU Parent-Subsidiary and Interest and Royalties Directives | Reputational scrutiny from international bodies affects banking access and counterparty perception |

Weighing the risks of Cyprus incorporation ultimately depends on whether your business can maintain genuine economic substance and absorb recurring compliance costs. For firms structured to meet those conditions, the challenges are predictable and manageable within established legal frameworks.

Compliance Services for Companies in Cyprus

Annual filing, AML obligations, UBO registration, and ongoing statutory requirements for Cyprus-registered entities.

Conclusion

A Cyprus incorporation drawbacks summary requires honest accounting of what the jurisdiction demands operationally. Substance requirements under EU directives, the annual mandatory audit obligation, and the UBO registration process through the Registrar of Companies each impose real administrative and financial costs on a business. These are structural features of the regime, not incidental friction. Your firm's exposure to these obligations begins from the moment of incorporation and continues for the entity's lifetime. Specialist guidance on local compliance frameworks is what determines whether those obligations are met efficiently or become a source of regulatory risk.

Expanship's Cyprus Company Formation Support

Expanship works with businesses facing the specific compliance demands that Cyprus incorporation carries, from satisfying the Cyprus Securities and Exchange Commission's substance expectations to meeting the Registrar of Companies' UBO filing obligations and annual audit requirements under the Cyprus Companies Law, Cap. 113. Cyprus company formation compliance support is where that operational burden sits, and Expanship's role is to reduce it to a manageable workload rather than suggest it disappears.

Beyond that, our services cover the full incorporation and post-incorporation cycle:

- Your company registration and document preparation are handled from the outset, covering all filings with the Registrar of Companies.

- A local registered agent and office address are provided to satisfy Cyprus's mandatory residency requirements.

- Liaising with government bodies and regulatory authorities on your behalf is part of the standard engagement.

- Ongoing compliance management keeps your entity in good standing after incorporation.

- Banking introduction assistance connects your business with suitable financial institutions operating in Cyprus.

- Tax registration and liaison with the Tax Department of Cyprus are included to support your compliance obligations.

Speak with Expanship Cyprus to discuss your specific situation.

Frequently Asked Questions (FAQ)

Substance requirements apply broadly, but the threshold varies by activity. Cyprus tax residency requires that management and control be exercised locally, and entities claiming treaty benefits or the 2.5% IP Box rate face heightened scrutiny under BEPS Action 5 and the EU Anti-Tax Avoidance Directives. A pure trading subsidiary with local staff and operations faces less pressure than a holding or royalty company relying on preferential rates.

Non-submission of audited accounts to the Registrar of Companies under the Cyprus Companies Law, Cap. 113, results in administrative penalties and can trigger strike-off proceedings. The audit requirement cannot be waived regardless of company size or turnover, which distinguishes Cyprus from jurisdictions like the UK where small companies qualify for audit exemptions. Persistent non-compliance also creates downstream issues with tax filings and UBO registry obligations.

The cost depends on the level of activity, but a realistic baseline for a holding entity with a local director, registered office, secretary, and bookkeeping runs from EUR 8,000 to EUR 20,000 per year before audit fees. Audit costs for a mid-sized Cyprus company typically range from EUR 2,500 to EUR 6,000 annually depending on transaction volume and complexity. These figures make Cyprus materially more expensive to maintain than an equivalent structure in a non-EU low-substance jurisdiction.

Failure to register or update beneficial ownership information in the UBO Registry maintained by the Registrar of Companies can result in fines of up to EUR 20,000 per officer under the Prevention and Suppression of Money Laundering Law (188(I)/2007 as amended). The process itself is administratively demanding, requiring detailed documentation for each beneficial owner holding 25% or more of shares or voting rights. Delays are common where ownership chains pass through multiple foreign holding entities requiring notarised and apostilled supporting documents.

It is not an outright prohibition, but the practical utility of nominee shareholding for tax structuring purposes has been significantly curtailed. Under the EU Anti-Tax Avoidance Directive and its Cyprus transposition, arrangements lacking economic substance or designed primarily to obtain treaty or directive benefits can be disregarded. Nominee directors specifically raise management-and-control concerns that directly threaten Cyprus tax residency status, making their use in anything beyond administrative functions legally risky.

Cyprus has around 65 active double tax treaties, which is a reasonable number but includes notable gaps and ageing agreements that predate modern OECD standards. For businesses with significant operations in Southeast Asia, several key jurisdictions such as Vietnam and Indonesia are not covered by a Cyprus treaty, limiting withholding tax relief on dividends and royalties. Ireland and the Netherlands offer broader and more recently updated treaty networks for Asian-facing structures, which is a concrete disadvantage for Cyprus in that context.

No. Cyprus law does not provide a small company audit exemption. Every Cyprus private limited company must file audited financial statements regardless of turnover, balance sheet size, or number of employees, which is a direct consequence of Cap. 113. This contrasts with jurisdictions such as the UK, where companies meeting two of three thresholds — turnover below GBP 10.2 million, assets below GBP 5.1 million, fewer than 50 employees — qualify for an audit exemption.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.