Key Takeaways

- Cyprus applies a 12.5% corporate tax rate — one of the lowest among EU member states — which applies to a broadly defined taxable base, giving foreign-owned companies a structurally low effective tax burden rather than a nominal headline figure.

- Under the Non-Domicile Regime, foreign shareholders who qualify are exempt from the Special Defence Contribution, meaning dividends and passive interest can be received without the additional layer of taxation that would otherwise apply under Cypriot domestic law.

- Because Cyprus company law derives from English common law, international investors benefit from a legal framework built on precedent, contractual enforceability, and corporate governance conventions that are widely understood across common law jurisdictions.

- Registration through the Department of Registrar of Companies and Official Receiver grants access to EU Single Market passporting rights, enabling a Cyprus-incorporated entity to operate and provide services across member states without establishing separate legal entities in each country.

Cyprus is an independent EU member state positioned at the eastern edge of the Mediterranean, with direct access to European, Middle Eastern, and North African markets. Company registration falls under the jurisdiction of the Registrar of Companies, which operates under the Department of Registrar of Companies and Official Receiver. Foreign businesses most commonly establish a Private Company Limited by Shares when structuring their presence here.

The tax posture is treaty-based and low-tax, shaped by a combination of domestic legislation and an extensive network of bilateral agreements. Ownership of a Cyprus-registered entity carries no restrictions on foreign nationals — non-residents can hold 100% of shares across virtually all sectors, and the regulatory framework actively accommodates foreign direct investment.

The benefits of incorporating in Cyprus extend across tax efficiency, regulatory access, and legal infrastructure. This article examines those advantages in detail, drawing on the specific provisions and frameworks that distinguish Cyprus company formation from structures available elsewhere in the EU.

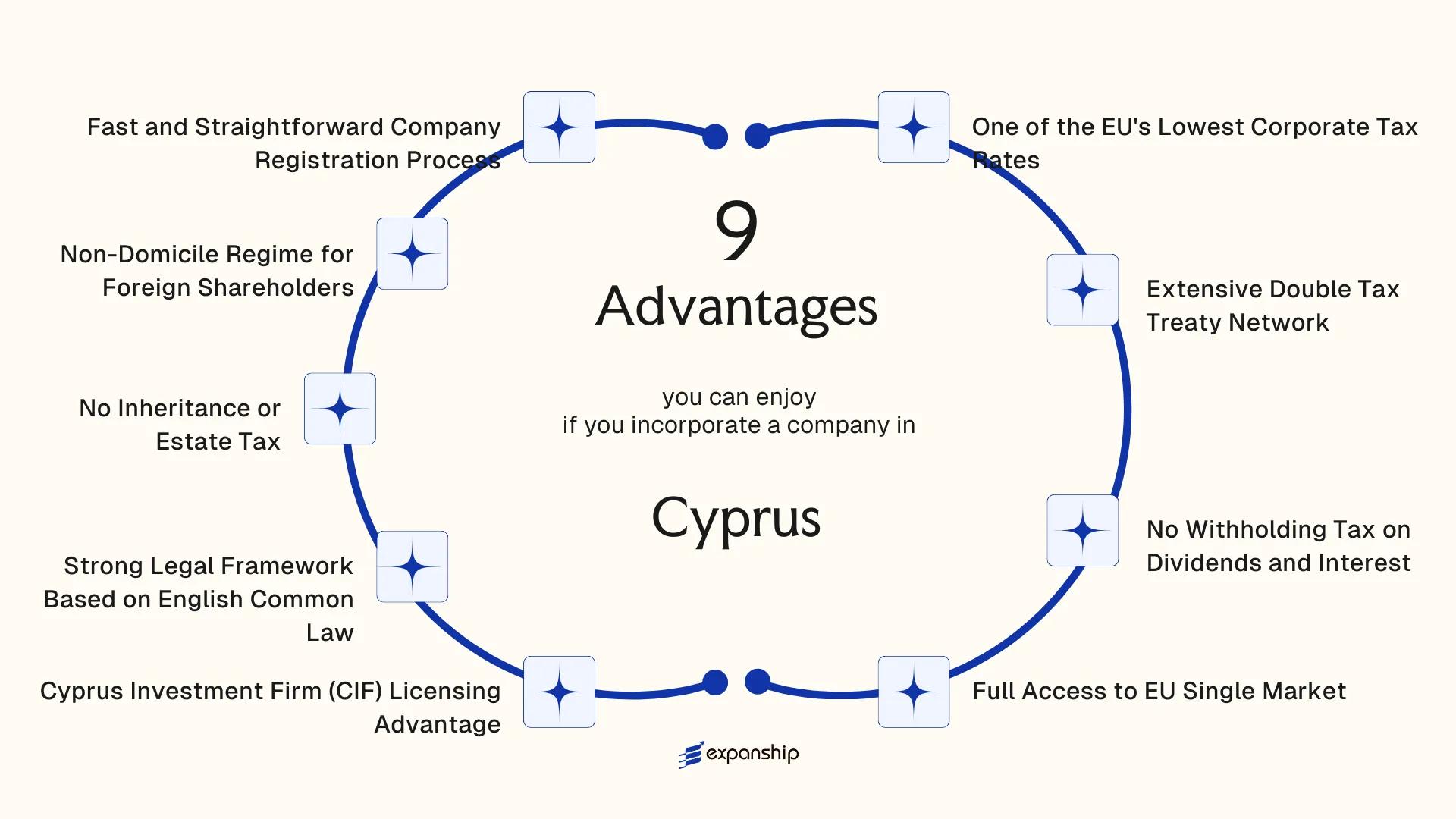

One of the EU's Lowest Corporate Tax Rates

Cyprus applies a standard corporate income tax rate of 12.5% on taxable profits, one of the lowest headline rates among EU member states. The EU average sits closer to 21%, which means companies incorporated in Cyprus retain a materially larger share of their earnings before any additional planning is applied.

What the Rate Actually Covers

Under the Income Tax Law (Law 118(I)/2002), taxable income is calculated after deducting allowable business expenses, which keeps the effective rate for many trading companies well below the nominal 12.5%. For businesses with significant intellectual property income, the Notional Interest Deduction and the IP Box regime can reduce the effective rate further, to as low as 2.5% on qualifying profits.

Why the Structure Matters for Foreign-Owned Entities

A foreign shareholder owning a Cyprus-registered company is subject to this rate on profits generated through the entity, not on worldwide income at their home country rate — provided the company has genuine substance and management in Cyprus. This separation is what makes the rate a functional advantage rather than a nominal one.

Your Cyprus entity can retain significantly more post-tax profit for reinvestment compared to operating through a higher-rate EU jurisdiction.

Extensive Double Tax Treaty Network

Cyprus has concluded over 65 double tax treaties with countries spanning Europe, the Middle East, Asia, and beyond. This network directly reduces or eliminates withholding taxes on dividends, interest, and royalties paid between treaty partners — meaning your business retains more of its cross-border income rather than losing portions of it to foreign tax authorities.

The practical effect is significant for holding structures. When a Cyprus-resident company receives dividends from a subsidiary in a treaty country, the applicable withholding rate is often reduced to 5% or even 0%, depending on the specific agreement. Without treaty protection, your firm could face standard statutory withholding rates that vary widely by country.

Treaty benefits also apply to capital gains in certain cases. Under several of these agreements, gains on the disposal of shares are taxable only in the country of residence — which, for a Cyprus-resident entity, means exposure to the 12.5% corporate tax rate rather than a potentially higher rate in the source country.

The treaties that make this possible include:

- Agreements with major trading partners such as Germany, France, the UAE, India, and China, giving your business access to reduced rates in high-volume commercial corridors

- Treaty terms negotiated broadly in line with the OECD Model Tax Convention, which creates predictability when structuring cross-border transactions

- Coverage of income categories including dividends, interest, royalties, and in many cases capital gains, reducing the risk of double taxation across multiple income streams

To access these treaty benefits, your company must qualify as a tax resident of Cyprus, which requires that central management and control be exercised from within the country.

Company Incorporation in Cyprus

Incorporate a tax-resident Cyprus company and access one of Europe's most extensive double tax treaty networks.

No Withholding Tax on Dividends and Interest

Cyprus imposes no withholding tax on dividends paid to non-resident shareholders. This rule applies regardless of the shareholder's country of residence and without requiring a double tax treaty to be in place. For foreign investors extracting profits from a Cyprus-registered entity, the full dividend amount reaches them without deduction at source.

The practical consequence is direct: profit repatriation to a holding company in another jurisdiction, or to an individual shareholder abroad, does not trigger any additional tax layer at the point of distribution. Many jurisdictions impose withholding rates of 15% to 25% on outbound dividends, meaning the absence of such a charge materially affects after-tax returns.

| Payment Type | Rate Applicable | Condition |

|---|---|---|

| Dividends to non-residents | 0% | No treaty requirement |

| Interest to non-residents | 0% | General rule under domestic law |

| Royalties to non-residents | 0% | Subject to anti-avoidance provisions |

Interest payments made to non-resident lenders are equally exempt from withholding tax under domestic law. This matters for group financing structures where a parent entity or related company provides intercompany loans; interest can flow out without retention.

Royalty payments also carry a zero rate in most circumstances, though specific anti-avoidance rules under the Income Tax Law (Law 118(I)/2002, as amended) may apply depending on the arrangement's substance. Confirming eligibility against that framework before structuring your flow is advisable.

Full Access to EU Single Market

Cyprus EU single market access benefits flow directly from its accession to the European Union in 2004 under the Treaty of Accession. A company incorporated there operates under EU law, meaning it can sell goods, supply services, and establish branches across all 27 member states without separate incorporation in each country.

This access is grounded in the four fundamental freedoms of the EU: free movement of goods, services, capital, and people. For a foreign business owner, this means a single corporate structure can address an entire continental market of over 440 million consumers.

Passporting rights extend this further for regulated entities. A firm licensed in one EU member state can passport that license into other member states under EU directives, removing the cost and delay of obtaining parallel authorizations jurisdiction by jurisdiction.

EU membership also grants your business access to EU public procurement frameworks, structural funds, and cross-border VAT arrangements governed by EU VAT directives.

Keep these points in mind:

- EU single market access applies to entities genuinely established and managed from Cyprus

- Passporting rights depend on the specific directive governing your regulated activity

- Free movement of capital allows profit repatriation across EU borders without restriction

- Substance requirements must be met; a dormant shell entity does not qualify for passporting

Cyprus transposed EU directives into domestic law using its English common law legislative tradition, which means many EU regulations are interpreted through case law principles familiar to UK-trained legal practitioners.

Cyprus Investment Firm (CIF) Licensing Advantage

Obtaining Cyprus Investment Firm CIF licensing benefits from a regulatory structure that is directly transposed from EU directives, primarily MiFID II, into national law through the Investment Services and Activities and Regulated Markets Law of 2017 (Law 87(I)/2017). The Cyprus Securities and Exchange Commission (CySEC) is the competent authority that supervises CIFs, and its regulatory framework is fully harmonised with EU standards, meaning a CIF licence carries credibility across all 27 member states.

EU Passporting Without Redundant Licensing

A CIF authorised by CySEC can passport its services across the entire EU and EEA under MiFID II provisions, without obtaining a separate licence in each target jurisdiction. For a firm seeking to serve clients in Germany, France, or the Netherlands, this eliminates the cost and delay of multiple national licensing processes. A single CySEC-regulated firm authorisation therefore opens a far wider addressable market than the size of the domestic economy would otherwise suggest.

Operational Cost Efficiency Through CySEC Oversight

CySEC's fee structure and minimum capital requirements are generally lower than those imposed by regulators in larger EU jurisdictions such as Germany's BaFin or France's AMF, while still meeting EU baseline standards. This means your firm can achieve full regulatory standing at a lower operational cost. The specific capital threshold depends on the category of investment services your entity is authorised to provide under Law 87(I)/2017.

Structure Your CIF Licence in Cyprus

Get guidance on CySEC authorisation requirements, capital thresholds, and passporting your investment services across the EU.

Strong Legal Framework Based on English Common Law

Cyprus adopted English common law as the foundation of its legal system following British colonial administration, and that inheritance shapes how your business operates there today. The Cyprus English common law legal framework benefits foreign businesses directly because contracts, corporate structures, and dispute resolution all follow principles familiar to investors from the UK, Australia, Hong Kong, and other common law jurisdictions.

- Companies Law, Cap. 113 governs company formation and operation. Modelled closely on the UK Companies Act, it defines director duties, shareholder rights, and corporate governance in terms that foreign counsel and investors can interpret without significant translation effort.

- Contract law follows common law doctrine, meaning precedent-based interpretation applies. For cross-border commercial agreements, this reduces ambiguity compared to civil law systems where codified statutes may override contractual intent.

- Cyprus courts apply equitable principles, including trust law, which has direct relevance for holding structures and asset protection arrangements used by international groups.

- English remains an official working language of the legal and judicial system, so corporate documents, court filings, and legal opinions are routinely produced in English without requiring certified translation.

- Judgments from Cyprus courts are enforceable across EU member states under EU Regulation No. 1215/2012, giving your entity's legal position practical reach beyond the island's borders.

No Inheritance or Estate Tax

Cyprus abolished inheritance tax in 2000. No estate duty, succession tax, or wealth transfer tax applies to assets held through a Cypriot company or to shares in such an entity upon the death of a shareholder. This gives the Cyprus no inheritance tax advantage a clear structural value for foreign investors planning multigenerational wealth transfer.

For a business owner holding shares in a Cyprus-registered entity, ownership can pass to heirs without triggering a tax liability at the point of transfer. In jurisdictions such as Germany or France, estate taxes can reach 30–50% on inherited business assets, depending on the value and relationship of beneficiaries. Structuring ownership through a Cypriot holding company removes that exposure entirely.

The exemption is not conditional on the shareholder's residency status or domicile. Whether the deceased was a non-resident or a local tax resident, no inheritance or estate charge arises on the Cypriot entity itself.

A foreign investor holds shares worth €5,000,000 in a Cyprus holding company. Upon death, those shares transfer to designated heirs with zero estate or inheritance tax applied in Cyprus, preserving the full value of the holding for the next generation.

Non-Domicile Regime for Foreign Shareholders

Cyprus non-domicile regime benefits apply to individuals who qualify as tax residents but are not domiciled in the country under the provisions of the Special Defence Contribution (SDC) Law. Non-domicile status is typically acquired by individuals who have not been Cyprus tax residents for at least 17 of the preceding 20 years.

Under this regime, qualifying individuals are fully exempt from SDC, which is otherwise levied on dividend income at 17% and on interest income at 30%. For a foreign shareholder receiving distributions from a Cyprus-registered company, this exemption means dividend income can be received without any additional Cyprus-level taxation beyond the corporate rate.

The non-domicile SDC exemption for non-domicile benefits applies regardless of whether the dividend originates from local or foreign-source income, provided the individual holds non-dom status at the time of distribution. This makes the structure particularly relevant for foreign investors who relocate to Cyprus and draw income from their shareholdings.

- Exempt from 17% SDC on dividends

- Exempt from 30% SDC on passive interest income

- No minimum dividend amount threshold to qualify for the exemption

Non-domicile status requires you to formally establish Cyprus tax residency, which carries its own conditions, including the 60-day rule under the Income Tax Law.

Fast and Straightforward Company Registration Process

One of the Cyprus fast company registration advantages is the timeline itself. The Registrar of Companies, operating under the Department of the Registrar of Companies and Official Receiver, can process a standard private limited company (Ltd) incorporation within five to seven working days. For straightforward applications with complete documentation, same-day or next-day registration is available through an expedited service.

That speed has a direct commercial consequence. Your business can open bank accounts, enter contracts, and begin operating within the same week the decision to incorporate is made, rather than waiting weeks or months as is common in several other EU member states.

The legal framework governing incorporation is the Companies Law, Cap. 113, which sets out clear, predictable requirements for private limited companies. The documentation required is standard:

- Memorandum and Articles of Association

- Details of directors and shareholders

- Registered office address in Cyprus

- Consent forms from directors and the company secretary

No minimum paid-up capital is required for a private company under Cap. 113, which removes a common upfront barrier that exists in other EU jurisdictions such as Austria or Poland, where minimum capital thresholds apply.

Filings and submissions to the Registrar are conducted through the e-filing portal, reducing the need for physical presence. A foreign business owner can complete the process entirely through a local authorized representative, making physical travel to the island unnecessary for the incorporation itself.

Why Cyprus Stands Out Among European Jurisdictions

Businesses evaluating European incorporation options most frequently compare Cyprus against Ireland, the Netherlands, and Luxembourg. These jurisdictions compete for the same profile of foreign investor: holding company structures, fund vehicles, and internationally mobile entrepreneurs seeking EU residency and market access. The comparison is instructive because it isolates where Cyprus delivers structurally distinct outcomes rather than marginal differences.

What the comparison reveals is that the combination of a 12.5% corporate tax rate, zero withholding taxes on outbound dividends and interest, English common law courts, and the Non-Domicile regime sits within a single jurisdiction in a way that competing locations do not replicate in full. Ireland matches on the corporate rate but imposes conditions on dividend exemptions that Cyprus does not. Luxembourg and the Netherlands offer mature treaty networks but carry higher compliance costs and greater regulatory scrutiny on substance requirements for holding entities.

| Parameter | Cyprus | Ireland | Netherlands | Luxembourg |

|---|---|---|---|---|

| Corporate Tax Rate | 12.5% | 12.5% | 25.8% | 17% (up to €200k: 15%) |

| Withholding Tax on Outbound Dividends | 0% | 25% (subject to exemptions) | 0% (subject to conditions) | 15% (subject to exemptions) |

| Withholding Tax on Outbound Interest | 0% | 20% (subject to exemptions) | 0% | 0% |

| Inheritance / Estate Tax | None | None | None | None |

| Non-Domicile Tax Regime | Yes | No | No | No |

| Legal System | English Common Law | English Common Law | Civil Law | Civil Law |

| EU Member | Yes | Yes | Yes | Yes |

Compliance Services for Companies in Cyprus

Maintain your Cyprus company's good standing with registered office management, annual return filing, and ongoing regulatory support.

Conclusion

Cyprus presents a coherent case for foreign business owners: a 12.5% corporate tax rate applied to a genuinely broad taxable base, a non-domicile regime that removes the Special Defence Contribution on dividends and passive interest, and an English common law legal system that governs contracts and corporate structures in terms familiar to most international investors. These are not isolated features; they form an interconnected framework where tax efficiency, legal predictability, and EU market access reinforce one another.

The benefits of incorporating in Cyprus are real, but their relevance depends on your specific circumstances. A financial services firm will weigh the Cyprus Securities and Exchange Commission licensing pathway differently than a holding company structured around treaty-protected dividend flows. Industry, residency status, and ownership structure all determine which advantages apply with full effect.

For businesses where the combination of EU passporting rights, treaty network access, and low effective tax burden aligns with operational needs, Cyprus company formation offers a structurally sound foundation. Understanding how these elements interact within your specific setup is the step that determines whether the jurisdiction fits your objectives.

Start Your Cyprus Company with Expanship Today

To incorporate a Cyprus company with Expanship, your engagement is handled by specialists who work directly with the relevant authorities and regulatory processes discussed throughout this blog, including company registration at the Registrar of Companies and Official Receiver, CIF licensing coordination with the Cyprus Securities and Exchange Commission, and ongoing compliance under the Income Tax Law (Cap. 297) and the Special Defence Contribution framework. Every engagement is scoped to the actual structure you are forming, not a generic package.

Expanship Cyprus company formation services cover the full administrative lifecycle of establishing and maintaining a private limited company (Ltd) or other eligible entity under Cyprus law:

- Preparation and legalization of incorporation documents, including the Memorandum and Articles of Association

- Registered agent and registered office provision as required under the Companies Law, Cap. 113

- Liaison with the Registrar of Companies for name reservation, filing, and certificate issuance

- Post-incorporation compliance management, including annual return filings and statutory record maintenance

- Corporate bank account introduction assistance with local and international banking institutions

- Director and secretary appointment support where nominee arrangements are required

Expanship Cyprus is available to discuss your specific incorporation requirements and advise on the structure that fits your operational and tax objectives.

Frequently Asked Questions (FAQ)

Yes, foreign nationals can own 100% of a Cyprus private limited company (Ltd) without any local shareholder requirement. There are no restrictions on foreign ownership under the Companies Law, Cap. 113, which governs company formation on the island. Certain regulated activities, such as obtaining a Cyprus Investment Firm licence from the Cyprus Securities and Exchange Commission, may carry their own fit-and-proper requirements, but those relate to licensing rather than ownership eligibility.

The standard corporate income tax rate is 12.5%, applied to net taxable profits as defined under the Income Tax Law of 2002. This rate applies uniformly to resident companies and to non-resident companies deriving income through a permanent establishment in Cyprus. There is no minimum corporate tax or alternative minimum tax that applies to dormant or low-profit entities under general law.

Foreign shareholders who qualify as non-domiciled tax residents are exempt from the Special Defence Contribution (SDC), which is the levy that would otherwise apply to dividend income at a rate of 17%. To qualify, an individual must have been a tax resident for fewer than 17 of the last 20 years prior to the relevant tax year. This exemption is governed by the Special Defence Contribution Law and effectively means qualifying non-domiciled shareholders receive dividend distributions free of any Cyprus-level withholding or SDC charge.

No withholding tax applies to interest payments made to non-resident companies under the current tax framework. Royalty payments made in respect of rights used outside Cyprus are also generally exempt from withholding tax, though royalties for rights used within the jurisdiction may be subject to withholding at rates that vary depending on the applicable double tax treaty. Where a relevant treaty exists, the treaty rate takes precedence over domestic rules.

Standard incorporation through the Department of Registrar of Companies and Official Receiver typically takes between five and ten working days once all required documents are submitted in proper form. An expedited service is available that can reduce processing to one to three working days for an additional fee. The timeline assumes no objections to the proposed company name and that the memorandum and articles of association conform to the requirements under Companies Law, Cap. 113.

Dividends received by a Cyprus-resident company from a foreign subsidiary are generally exempt from corporate income tax under the participation exemption provisions of the Income Tax Law of 2002. The exemption is subject to conditions: the paying company must not be engaged in more than 50% passive income-generating activities, and it must not be subject to a substantially lower tax rate than the Cyprus rate. Where those conditions are not met, the income is taxable at the standard 12.5% rate, though a credit for foreign tax paid is typically available.

The legal system is grounded in English common law principles inherited through the colonial period and codified through legislation such as the Contract Law, Cap. 149. This means core concepts around offer, acceptance, consideration, and breach align closely with those used in the United Kingdom, Hong Kong, Singapore, and other common law jurisdictions. In practice, this reduces the interpretive friction when drafting cross-border agreements or enforcing judgments, though recognition of foreign judgments still depends on bilateral arrangements or EU regulations where applicable.

There is no inheritance tax or estate duty in Cyprus, meaning shares in a Cyprus company that pass to a beneficiary upon the death of a shareholder carry no tax charge at the point of transfer. This has been the position since estate duty was abolished, and no equivalent levy has been reintroduced in subsequent tax legislation. The beneficiary assumes ownership of the shares without any Cyprus-level tax cost, though their home jurisdiction may impose its own succession or inheritance tax rules independently.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.