Key Takeaways

- Cyprus business structures are governed primarily by the Companies Law, Cap. 113 and the Partnership Law, Cap. 116, with registration administered by the Registrar of Companies and Official Receiver under the Ministry of Energy, Commerce and Industry.

- The private limited company (Ltd) is the most commonly registered entity in Cyprus, favoured for its liability protection and compatibility with both holding and trading structures.

- Branch offices and representative offices allow foreign companies to establish a local presence in Cyprus without forming a separate legal person under Cap. 113.

- Beneficial ownership reporting under Cyprus's UBO register framework reflects the jurisdiction's continued alignment with EU transparency directives, affecting compliance obligations across all entity types.

Introduction to Entity Types in Cyprus

Cyprus is a sovereign republic and EU member state situated in the eastern Mediterranean, south of Turkey and west of Lebanon. Company registration is administered by the Registrar of Companies and Official Receiver, which operates under the Ministry of Energy, Commerce and Industry. The primary legislation governing corporate structures is the Companies Law, Cap. 113, supplemented by the Partnership Law, Cap. 116.

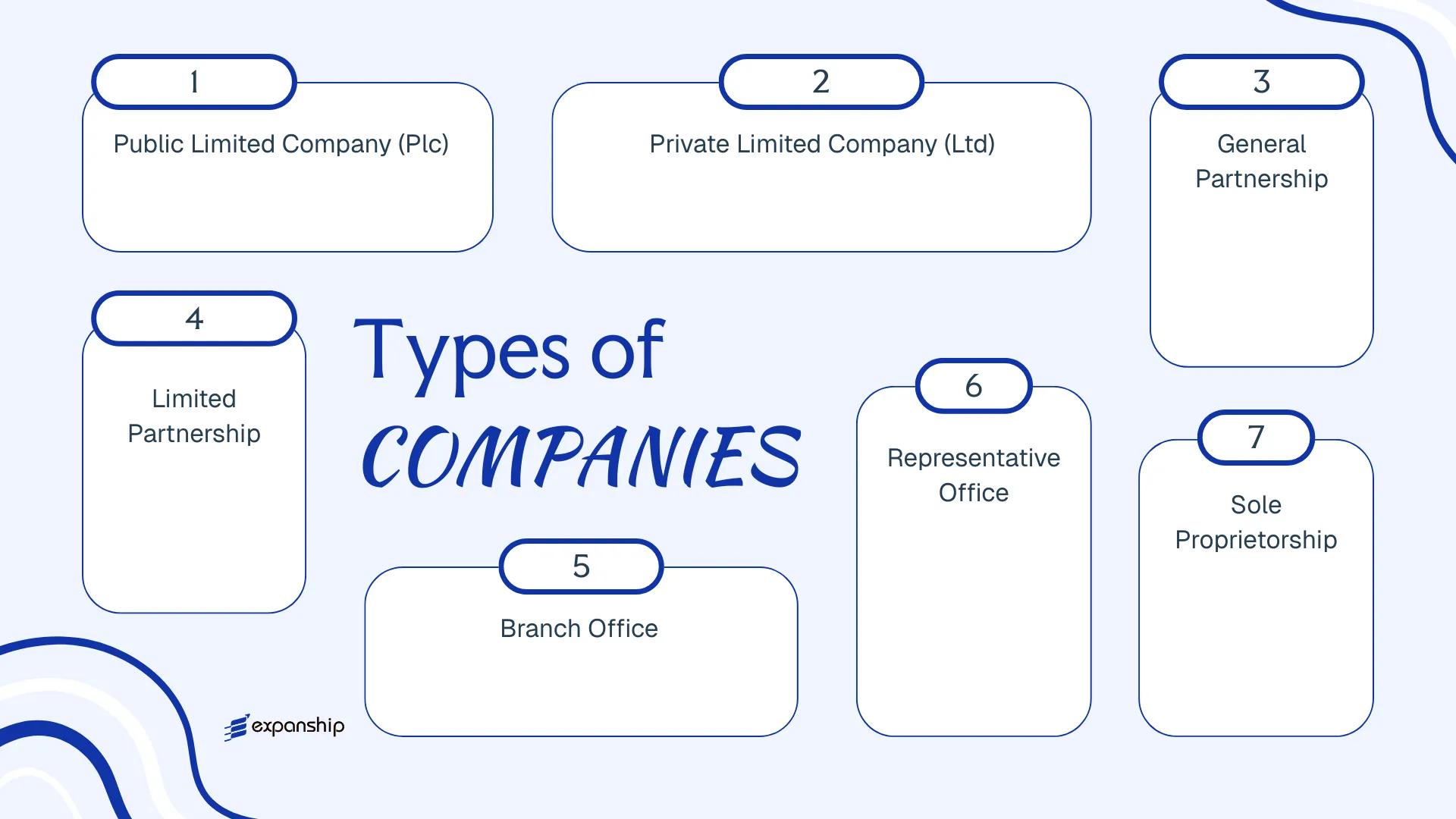

Structurally, the types of business entities in Cyprus span several distinct legal forms: the Private Limited Company (Ltd), the Public Limited Company (Plc), the General Partnership, the Limited Partnership, the Branch Office, the Representative Office, and the Sole Proprietorship.

Cyprus applies a low-tax corporate regime, with access to an extensive double tax treaty network and EU directives on dividends, interest, and royalties. Each legal entity type carries different implications for liability, taxation, governance, and regulatory obligations. This article examines each structure in turn — covering formation requirements, compliance obligations, and the conditions under which each form is most commonly used.

An Overview of Business Structures in Cyprus

Under the Cyprus Companies Law, Cap. 113, and supplementary legislation including the Partnerships and Business Names Law, Cap. 116, businesses can be structured across six distinct legal forms. Each form carries different implications for liability, taxation, membership, and permitted activities. The sections that follow examine each structure in detail.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Public Limited Company (Plc) | Incorporated company | Limited to shares | Taxable | Permitted | 7 shareholders | Registrar of Companies | Cap. 113 |

| Private Limited Company (Ltd) | Incorporated company | Limited to shares | Taxable | Permitted | 1 shareholder | Registrar of Companies | Cap. 113 |

| General Partnership | Unincorporated firm | Unlimited, joint | Taxable | Permitted | 2 partners | Registrar of Companies | Cap. 116 |

| Limited Partnership | Unincorporated firm | Mixed (general/limited) | Taxable | Permitted | 2 partners | Registrar of Companies | Cap. 116 |

| Branch Office | Extension of foreign entity | Parent bears liability | Taxable on local income | Permitted | N/A | Registrar of Companies | Cap. 113 |

| Representative Office | Non-trading presence | Parent bears liability | Generally exempt | Not permitted | N/A | Registrar of Companies | Cap. 113 |

| Sole Proprietorship | Individual trader | Unlimited, personal | Taxable | Permitted | 1 individual | Registrar of Companies | Cap. 116 |

Each of these structures is examined in full in the sections below.

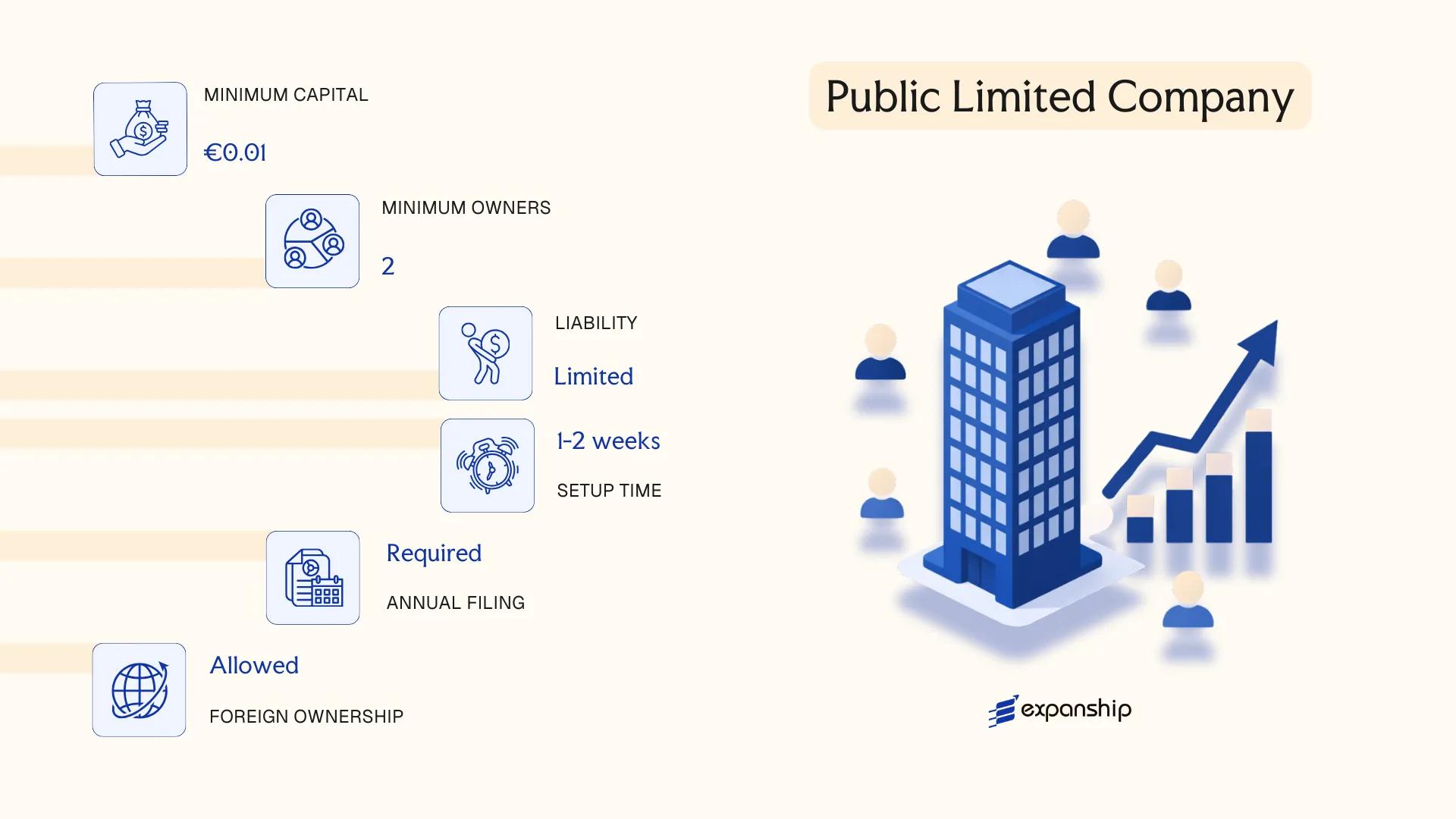

Public Limited Company (Plc) under the Cyprus Companies Law, Cap. 113

Governed by the Cyprus Companies Law, Cap. 113, a Cyprus Public Limited Company Plc formation results in a separate legal entity with limited liability for its shareholders. The structure sits at the more regulated end of the corporate spectrum, designed for businesses that intend to offer shares to the public or seek a listing on a recognised stock exchange.

Unlike its private counterpart, a Plc is not restricted from inviting public subscription to its shares. This openness to public capital markets comes with correspondingly stricter disclosure and governance obligations under Cap. 113.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Public Limited Company (Plc) | Separate legal personality; shareholders' liability limited to unpaid share capital |

| Members | Shareholders: minimum 7, no maximum | Directors: minimum 2; Company Secretary required |

| Local Presence | Registered office in Cyprus; local company secretary | Registered address must be maintained at all times |

| Share Capital | Minimum authorised capital: EUR 25,629 (CYP 15,000 equivalent); at least 25% paid-up on registration | Shares may be listed; public subscription permitted |

| Privacy | Shareholder register and accounts filed publicly with the Registrar of Companies | Beneficial ownership disclosed to the UBO Register |

Focus Points

- Taxation: Subject to 12.5% corporate income tax on worldwide profits; VAT registration required above the statutory threshold; dividend distributions generally exempt from withholding tax for non-resident shareholders; stamp duty applies to certain instruments.

- Economic Substance: No formal substance legislation equivalent to some other jurisdictions, but demonstrable management and control in Cyprus strengthens tax residency claims.

- Annual Compliance: Audited financial statements required; annual return filed with the Registrar of Companies; AGM must be held within 15 months of the preceding AGM.

- Treaty Access: Qualifies for benefits under Cyprus's network of double tax treaties, provided tax residency is established through management and control.

- Conversion: A Plc may be re-registered as a private limited company under Cap. 113 by special resolution and Registrar approval, subject to meeting private company criteria.

Closing

A Plc is suited to businesses seeking public capital, preparing for a stock exchange listing, or requiring a structure that signals institutional credibility to investors. The primary advantage is unrestricted access to public equity markets; the principal limitation is the administrative burden, including mandatory audit, higher minimum capital, and continuous disclosure requirements.

A Cyprus Plc is most appropriate for businesses with public fundraising intentions or listed-company ambitions, not for closely held or SME structures.

Company Incorporation in Cyprus

Incorporate a Public Limited Company or other business structure in Cyprus with end-to-end support from Expanship.

Private Limited Company (Ltd) under the Cyprus Companies Law, Cap. 113

The Private Limited Company is the most widely used corporate structure for Cyprus Private Limited Company Ltd registration. Governed by the Cyprus Companies Law, Cap. 113, it carries separate legal personality distinct from its shareholders, meaning the entity can own assets, enter contracts, and incur liabilities in its own name.

Liability is capped at each member's shareholding, and shares are not freely transferable to the public. This structural restriction distinguishes it from its public counterpart and makes it the default choice for closely held commercial operations.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private Limited Company by shares | Incorporated under Cap. 113; "Limited" or "Ltd" suffix required |

| Members | Min. 1 shareholder, max. 50 | Corporate or individual; nominee shareholders permitted |

| Directors | Min. 1 director | Corporate directors allowed; no nationality requirement, though tax residency affects substance |

| Local Presence | Registered office address in Cyprus required | Must be a physical address; a P.O. box alone does not suffice |

| Share Capital | No statutory minimum; commonly EUR 1,000 | Denominated in any currency; shares must be fully or partly paid |

| Privacy | Shareholder and director details on public register | Beneficial ownership disclosed to the UBO Register (not fully public) |

Focus Points

- Taxation: Subject to 12.5% corporate income tax on worldwide profits for tax-resident companies; 19% VAT applies to taxable supplies; no withholding tax on dividends paid to non-residents; stamp duty applies to certain agreements at nominal rates.

- Economic Substance: Tax residency is determined by management and control; majority of directors should be Cyprus-resident to avoid residency challenges by foreign tax authorities.

- Annual Compliance: Annual return filed with the Registrar of Companies; audited financial statements required regardless of size; income tax return submitted to the Tax Department.

- Treaty Access: Cyprus-resident companies access an extensive double tax treaty network and EU Directives, including the Parent-Subsidiary and Interest and Royalties Directives.

- Conversion: A private company may be re-registered as a public company under Cap. 113 procedures, subject to meeting the relevant thresholds.

Closing

Cyprus Ltd companies are routinely used for trading, holding, IP ownership, and fund management structures given the combination of EU membership, a low corporate tax rate, and treaty access. The primary limitation is that annual audit is mandatory, adding a fixed compliance cost regardless of revenue.

This entity suits non-resident founders and international businesses seeking an EU-based, tax-efficient structure with full foreign ownership and no minimum capital threshold.

Partnerships in Cyprus [General Partnership, Limited Partnership]

Governed by the Partnerships and Business Names Law, Cap. 116, partnerships in Cyprus do not carry separate legal personality distinct from their partners. Partnership registration in Cyprus is administered through the Registrar of Companies and Official Receiver, and the process differs meaningfully depending on whether the structure is a general or limited form.

Liability exposure is the defining variable between the two types. In a general partnership, every partner bears unlimited personal liability for the firm's debts. A limited partnership, by contrast, permits certain partners to cap their liability to the amount contributed, provided at least one general partner retains unlimited liability.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Partnership (no separate legal personality) | Partners are collectively the business |

| Members | Partners; minimum 2, maximum 20 | At least 1 general partner required in a limited partnership |

| Local Presence | Registered office address in Cyprus required | Must be maintained for official correspondence |

| Capital | No statutory minimum; contributions in cash or kind | Terms governed by the partnership agreement |

| Privacy | Partner names disclosed on public register | No option for nominee partners |

Focus Points

- Taxation: Partnerships are generally treated as tax-transparent; income is taxed at the partner level under personal income tax rates, though VAT registration obligations apply if turnover thresholds are met.

- Annual Compliance: Annual returns must be filed with the Registrar; no audit requirement comparable to limited companies.

- Treaty Access: As pass-through entities without separate legal personality, partnerships do not independently access Cyprus's double tax treaty network.

- Conversion: A partnership may convert to a limited company under Cap. 113, subject to standard incorporation requirements.

- Restrictions: Partnerships are barred from engaging in banking or insurance activities.

Sub-Types

General Partnership

All partners hold equal management rights and unlimited liability unless the partnership agreement specifies otherwise. This structure suits small professional practices or family-run trading operations where partners operate with mutual trust.

Limited Partnership

One or more limited partners contribute capital but are excluded from management; participation in day-to-day decisions can void their liability protection. The structure is sometimes used for investment holding arrangements or fund-like vehicles where passive investors are involved.

Closing

Partnerships suit smaller commercial ventures, professional services firms, or arrangements where two or more parties wish to operate with minimal formality and shared management. The absence of a minimum capital requirement reduces the setup barrier, but the unlimited liability exposure for general partners is a material structural risk that warrants careful consideration before proceeding.

Cyprus partnerships are most appropriate for small professional firms or closely-held ventures where the partners have an established relationship and accept the associated liability implications.

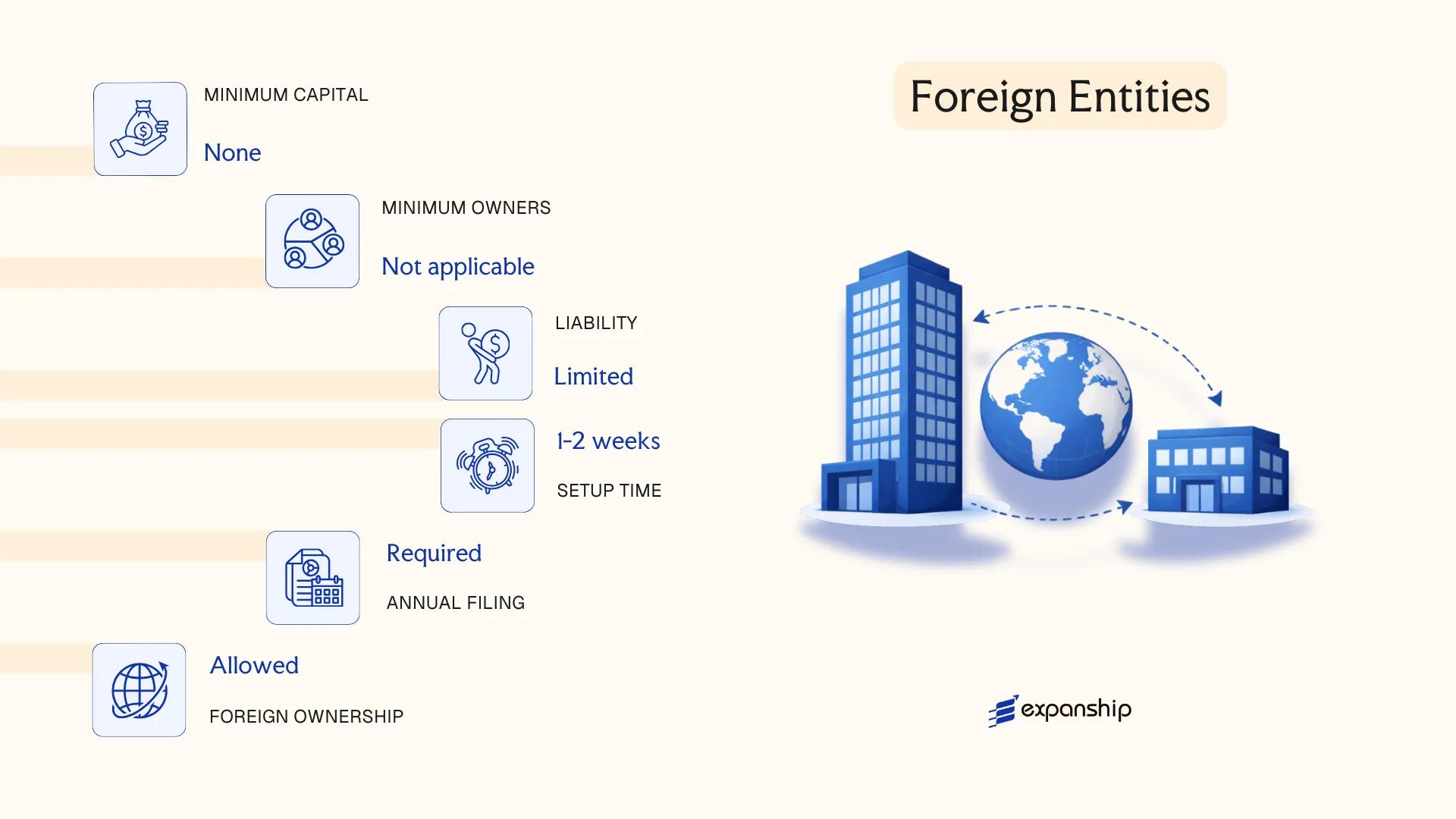

Foreign Entities in Cyprus [Branch Office, Representative Office]

A foreign company branch office Cyprus registration is governed by Part XI of the Companies Law, Cap. 113, which applies to overseas companies establishing a place of business within the Republic. Unlike a subsidiary, a branch does not constitute a separate legal entity — it is an extension of the parent company, which retains full legal and financial liability for the branch's operations.

Registration must be completed with the Registrar of Companies within one month of the branch commencing operations. The required documentation includes certified copies of the parent company's constitutional documents, a list of directors, and the appointment of a local authorised representative.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Extension of foreign parent; no separate legal personality | Parent bears unlimited liability for branch obligations |

| Authorised Representative | Minimum one individual resident in Cyprus | Must be named in the registration filing |

| Registered Office | Physical address required in Cyprus | Cannot be a P.O. box |

| Capital | No minimum capital requirement | Branch does not issue shares |

| Privacy | Parent company documents become public record upon filing | Includes constitutional documents and director details |

| Trade Name | May operate under parent's name or a registered trade name | Subject to Registrar approval if name differs |

Focus Points

- Taxation: Branch profits are subject to the standard 12.5% corporate income tax; VAT registration is required if taxable turnover exceeds the statutory threshold; withholding tax may apply to royalties or interest paid abroad depending on applicable tax treaties.

- Economic Substance: No statutory substance requirements specific to branches, but the parent's tax residency status may affect how profits are attributed and taxed.

- Annual Compliance: Branches must file annual returns and audited financial statements of the parent company with the Registrar of Companies.

- Treaty Access: Access to Cyprus's double tax treaty network depends on the tax residency of the parent, not the branch itself.

- Restrictions: A branch cannot engage in activities outside the scope permitted to the parent entity under its own constitutional documents.

Sub-Types

Branch Office

Registered under Part XI of Cap. 113, a branch office may conduct full commercial activities in Cyprus on behalf of the parent. It generates taxable income locally and must maintain accounting records within the Republic.

Representative Office

A representative office is a lighter-presence structure used strictly for non-commercial activities such as market research, liaison, or promotional functions. It cannot conclude contracts or generate revenue in Cyprus; any income-producing activity would require re-classification as a branch.

Closing

Foreign groups use branches primarily for direct market entry without creating a separate subsidiary, though the absence of liability separation between parent and branch is a material structural limitation. This structure suits established overseas companies that require an operational presence without the administrative overhead of incorporating a new entity.

Foreign companies seeking a direct operational foothold in Cyprus without incorporating a new legal entity, provided the parent is prepared to assume full liability for local activities.

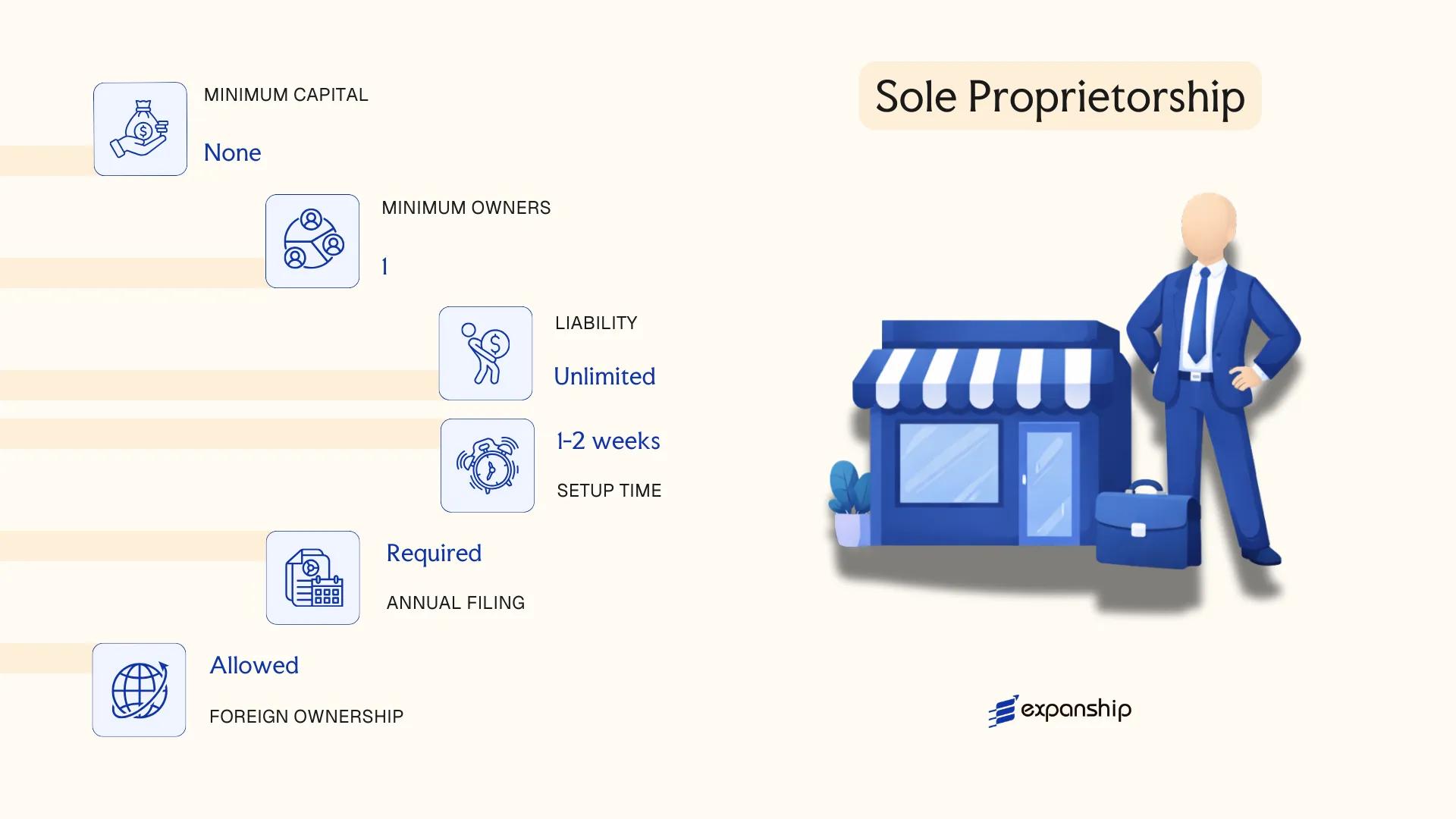

Sole Proprietorship in Cyprus

Sole proprietorship registration Cyprus follows a straightforward administrative process, but the structure itself carries significant legal implications that business owners must understand before proceeding. Governed primarily by general commercial law rather than a dedicated statute like the Companies Law, Cap. 113, a sole proprietorship has no separate legal personality — the individual and the business are, in law, the same person.

Registration is handled through the Tax Department (for tax identification) and the Registrar of Companies and Official Receiver for trade name registration where a trading name other than the proprietor's own name is used. Self-employed registration Cyprus is processed concurrently through the Social Insurance Services, where mandatory contributions apply from the outset.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated sole trader | No separate legal personality; proprietor bears full personal liability |

| Members | Single proprietor | No minimum capital or co-ownership permitted |

| Local Presence | Physical address required | Must be registered with the Tax Department and Social Insurance Services |

| Capital | No statutory minimum | No prescribed currency or paid-up capital requirement |

| Privacy | Proprietor's details on public record | Trade name registered with the Registrar if different from proprietor's name |

| Liability | Unlimited personal liability | Personal assets are exposed to business creditors |

Focus Points

- Taxation: Subject to personal income tax (progressive rates up to 35%); VAT registration mandatory if annual turnover exceeds the statutory threshold (currently €15,600); no corporate tax applies; stamp duty may apply to certain agreements.

- Social Insurance: Mandatory contributions to the Social Insurance Fund as a self-employed person, calculated on declared income.

- Annual Compliance: Annual income tax return required; no separate company annual return or financial statements filed with the Registrar.

- Treaty Access: No access to Cyprus's double tax treaty network, which applies only to tax-resident companies and individuals under specific conditions.

- Conversion: Can be converted into a private limited company under Cap. 113, though this requires full incorporation as a new entity rather than a structural conversion.

Closing

Cyprus sole trader setup suits freelancers, consultants, and small-scale operators who require a low-cost, low-administration structure for domestic activity. The primary limitation is unlimited personal liability, which makes this form unsuitable for ventures carrying meaningful commercial or financial risk.

Local service providers and self-employed professionals operating individually with limited liability exposure and no requirement for foreign investment or corporate structuring.

How to Choose the Right Entity Type in Cyprus

Selecting the correct structure from the outset determines your tax position, regulatory obligations, and operational flexibility for the life of the business — getting this decision wrong has concrete consequences.

Why Your Entity Choice Matters

- Choosing a tax-exempt entity when you require access to Cyprus's double tax treaty network means withholding tax reductions available under those treaties cannot be claimed in counterpart countries.

- Registering a branch of a foreign company when you intend to trade independently within Cyprus can expose the parent entity to local liabilities that a separately incorporated firm would have contained.

- Selecting a private limited company when a single-person consultancy is all that is needed subjects your business to mandatory audit requirements under the Companies Law, Cap. 113, adding recurring professional fees that a sole proprietorship would not trigger.

- Forming a company when your primary objective is asset protection or succession planning locks you into annual shareholder obligations and disclosure requirements that do not apply to trust arrangements.

Key Factors to Consider

- Business Activity: Active trading, passive asset-holding, and regulated activities such as investment funds each require a distinct structure under Cyprus law.

- Tax Objectives: Your need for full tax residency, treaty access, or eligibility for the Intellectual Property Box regime will determine which entity qualifies.

- Substance Capacity: If you cannot maintain employees, a physical office, and local decision-making in Cyprus, your chosen structure must not carry substance requirements that trigger reporting failures.

- Ownership and Management: Multi-party ventures with governance requirements point toward a private limited company, while flexible arrangements may suit a limited partnership registered under the Partnership Law, Cap. 116.

- Privacy Requirements: Directors and shareholders of companies incorporated under Cap. 113 appear on the public register maintained by the Registrar of Companies; nominee structures are permissible but add compliance layers.

- Exit Strategy: Not all entity types permit redomiciliation or conversion — confirm this before formation if a future structural change is anticipated.

The full text of the Cyprus Companies Law, Cap. 113 is available on the official Cyprus Law Database.

Corporate Compliance Services in Cyprus

Ongoing compliance support for Cyprus-registered entities, including annual returns, audit coordination, and regulatory filings with the Registrar of Companies.

Conclusion

Selecting the right structure is the first binding decision in any Cyprus company formation summary guide, and each entity type under Cap. 113 or the relevant partnership legislation serves a distinct purpose. The private limited company (Ltd) remains the most commonly registered form, favoured for its liability protection and compatibility with holding and trading structures. Public limited companies suit businesses seeking capital markets access or listing requirements. General and limited partnerships are used where pass-through arrangements and shared management are required. Branch offices and representative offices give foreign firms a local presence without creating a separate legal person. Sole proprietorships carry the lightest administrative burden but offer no liability separation.

Regulatory oversight by the Registrar of Companies and the continuous alignment with EU directives signal a trajectory toward greater transparency, including beneficial ownership reporting under the UBO register framework. Your choice of entity will shape tax treatment, governance obligations, and future structuring options.

How Expanship Can Assist You

Expanship's Cyprus company incorporation services cover the full process of registering a business with the Registrar of Companies and Official Receiver — the authority responsible for incorporating private and public limited companies, partnerships, and other entities under the Cyprus Companies Law, Cap. 113. Your specific structure determines the filings required, and our team works through each step accordingly.

From document preparation to post-incorporation obligations, our Cyprus company registration assistance includes:

- Preparation and legalization of incorporation documents

- Registered agent and registered office provision in Cyprus

- Filing and liaison with the Registrar of Companies and Official Receiver

- Post-incorporation compliance management, including annual returns and director registers

- Banking introduction assistance for corporate account setup

- Ongoing corporate secretarial support

Reach out to our team directly through Expanship Cyprus to discuss your structure and next steps.

Frequently Asked Questions (FAQ)

The Private Limited Company (Ltd) is the most frequently registered structure under Cap. 113. Its combination of limited liability, a single-shareholder minimum, and access to the EU parent-subsidiary directive makes it the default choice for both resident and non-resident founders.

A Private Ltd restricts share transfers and cannot offer shares to the public, whereas a Public Limited Company (Plc) may list on a stock exchange and must maintain a minimum share capital of €25,629. Compliance requirements for a Plc are substantially heavier, including mandatory audited accounts filed with the Registrar of Companies and stricter governance rules.

A Private Limited Company using nominee shareholders and directors provides the greatest degree of confidentiality. The beneficial owner's details are not disclosed on the public register, though registration with the Ultimate Beneficial Owner (UBO) Register maintained by the Department of Registrar of Companies and Intellectual Property is required under the Prevention and Suppression of Money Laundering Law.

A sole proprietorship and a Private Ltd can each be formed by one individual. General and Limited Partnerships require a minimum of two partners, making single-person formation legally unavailable for those structures.

Non-EU nationals may register a Private Ltd, branch office, or sole proprietorship without restrictions under Cap. 113. For sole proprietorship specifically, non-EU founders may need to satisfy additional conditions relating to residency permits, so consulting the Civil Registry and Migration Department beforehand is advisable.

Cap. 113 permits a Private Ltd to re-register as a Public Limited Company, and vice versa, subject to meeting the applicable capital and shareholder requirements. Conversion between fundamentally different structures, such as a partnership transforming into a limited company, generally requires dissolution of the existing entity and fresh incorporation rather than a statutory continuation.

Private and Public Limited Companies hold full separate legal personality under Cap. 113. General and Limited Partnerships, as well as sole proprietorships, do not — meaning personal assets of the owner or partners remain exposed to business liabilities.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.