Key Takeaways

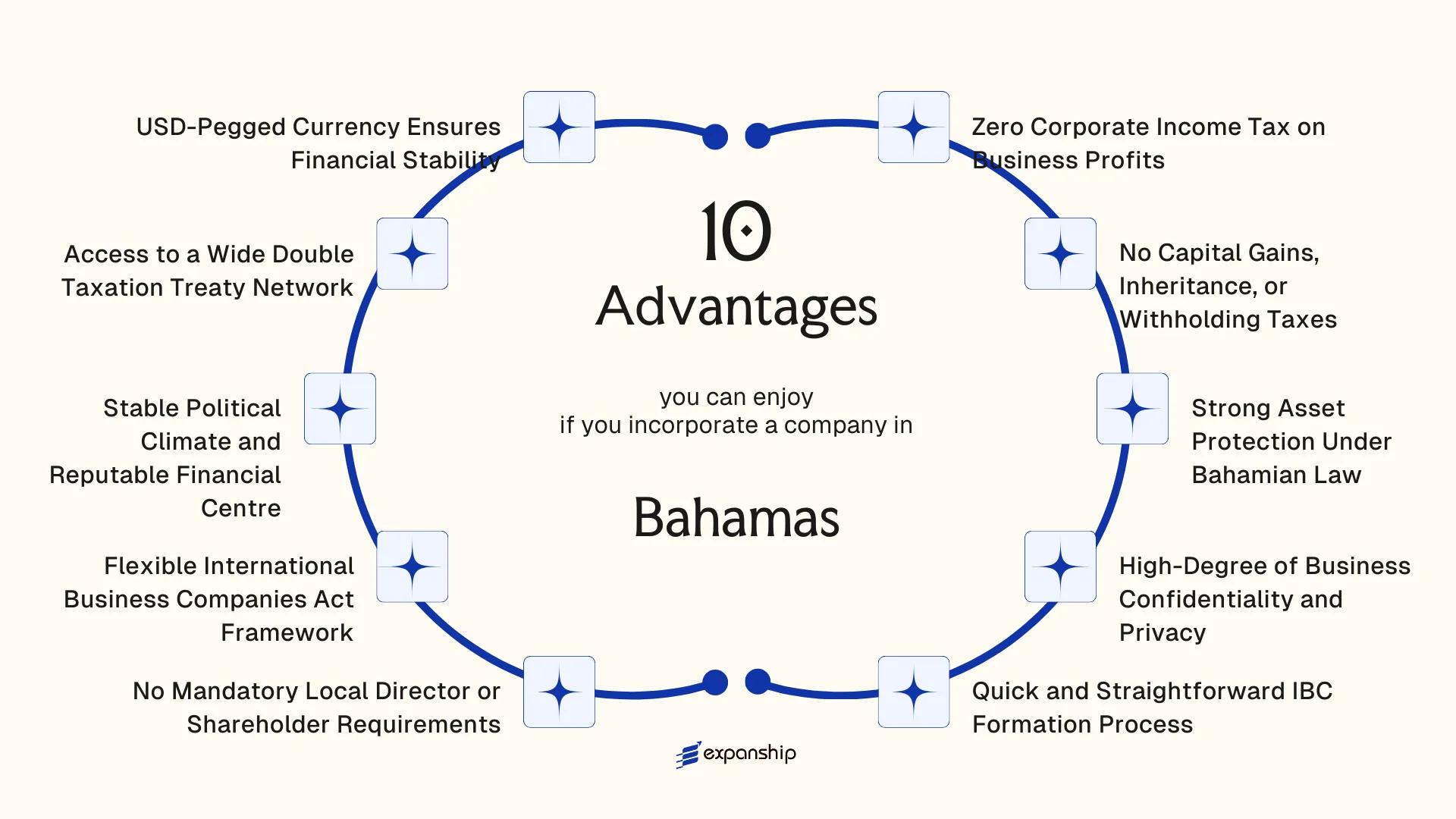

- Businesses incorporated under the Bahamas' International Business Companies Act pay zero corporate income tax on profits, eliminating one of the most significant cost burdens for internationally structured entities.

- The absence of capital gains, inheritance, and withholding taxes at the entity level means that wealth accumulation and cross-border distributions are not subject to the layered fiscal drag common in higher-tax jurisdictions.

- Because the Bahamian dollar is pegged 1:1 to the USD, companies operating in dollar-denominated markets carry no currency conversion risk from their jurisdiction of incorporation.

- Oversight by established bodies — including the Securities Commission of the Bahamas and the Registrar General's Department — provides a defined regulatory framework that supports entity credibility without imposing the compliance burdens typically associated with onshore financial centres.

Located in the northwestern Caribbean, the Bahamas is an independent sovereign nation and a member of the Commonwealth. Company registration falls under the authority of the Registrar General's Department, the official body responsible for business incorporation and related filings. Foreign investors most commonly use the International Business Company as their legal vehicle of choice. The jurisdiction operates on a zero-tax basis for most internationally oriented businesses, with no corporate income tax, capital gains tax, or inheritance tax applied at the entity level.

Foreign ownership faces no structural restrictions — your business can be wholly owned by non-resident individuals or corporate shareholders without triggering any mandatory local participation requirements. This openness reflects a broader policy posture that has made the benefits of incorporating in the Bahamas a subject of consistent interest among international entrepreneurs, holding company structures, and asset management vehicles alike.

This article outlines the primary advantages that the Bahamian legal and regulatory framework offers to foreign businesses considering formation here.

Zero Corporate Income Tax on Business Profits

The Bahamas zero corporate income tax advantage is one of the most commercially significant features of its offshore framework. Under Bahamian law, International Business Companies pay no tax on profits earned outside the territory.

What the Zero-Tax Rule Actually Covers

The International Business Companies Act establishes that an IBC conducting business internationally is not subject to corporate income tax on its earnings. This directly increases after-tax returns, since profit generated through foreign operations remains entirely within the business rather than being reduced by a domestic tax liability.

Rates in comparable jurisdictions such as Singapore sit at 17%, while Hong Kong applies up to 16.5%. For a foreign-owned entity routing international revenues through a Bahamian IBC, the differential in retained earnings compounds meaningfully over time.

The Statutory Basis and Its Practical Scope

The tax-exempt status is not a discretionary concession granted case-by-case; it is a structural feature encoded in the legislative framework governing IBCs. Your firm's tax position is therefore predictable and legally grounded, rather than subject to administrative interpretation.

This certainty allows for reliable financial planning without annual uncertainty over applicable rates or qualifying conditions.

All profits your IBC earns from international operations are retained in full, with no corporate income tax deducted at the Bahamian level.

No Capital Gains, Inheritance, or Withholding Taxes

Under the International Business Companies Act, 2000, International Business Companies (IBCs) registered in the Bahamas are exempt from capital gains tax. No capital gains tax on Bahamas company transactions means that profits generated from the sale of shares, securities, or other capital assets held outside the country are not subject to any domestic tax charge. For investors structuring exits, asset sales, or portfolio disposals through an IBC, this directly preserves the full value of those transactions.

Inherited assets held through an IBC are equally unencumbered. There is no inheritance or estate tax applicable to such structures, which matters for succession planning across generations or between business partners.

Dividend distributions from an IBC to non-resident shareholders attract no withholding tax. This is a structural feature confirmed under the IBC framework, not a discretionary exemption, meaning your business can distribute profits without a percentage being deducted at source before funds reach foreign shareholders.

Several factors make these exemptions practically significant:

- Retained capital is not reduced by exit or transfer taxes, preserving full reinvestment capacity

- Succession arrangements can be structured without triggering domestic tax at the point of transfer

- Profit repatriation to foreign shareholders requires no withholding calculation or local filing at the distribution stage

These exemptions apply to qualifying IBCs conducting business outside the jurisdiction.

Incorporate a Company in the Bahamas

Set up a Bahamas IBC and access a tax-neutral structure with no capital gains, inheritance, or withholding taxes on qualifying international business.

Strong Asset Protection Under Bahamian Law

Bahamas asset protection for businesses is grounded in a well-established statutory framework, primarily the International Business Companies Act, 2000. Under this legislation, an IBC's assets are legally separated from the personal liabilities of its shareholders, meaning creditors pursuing an individual shareholder generally cannot reach the company's holdings. That structural separation is not incidental; it is codified protection with direct consequences for how foreign investors structure their international holdings.

| Feature | Legal Basis | Practical Effect |

|---|---|---|

| Shareholder liability limitation | International Business Companies Act, 2000 | Personal assets of shareholders are shielded from corporate creditors |

| Statutory asset segregation | IBC Act, s. 130+ | Company assets held separately from member interests |

| Foreign judgment enforcement | Common law principles | Foreign judgments require re-litigation; not automatically enforceable |

Foreign court judgments are not automatically recognized and enforced in the jurisdiction. A creditor seeking to enforce a judgment issued abroad must relitigate the claim before local courts, which introduces a meaningful procedural barrier. For business owners facing litigation risk in their home country, this feature gives the corporate structure a degree of insulation that purely domestic entities cannot provide.

Charges and security interests over IBC assets can also be registered under the Companies (Charges) Register, creating transparent priority rules that protect secured creditors while maintaining orderly claims resolution. This makes the entity suitable not just for protection against unforeseen claims, but also for structured financing arrangements where asset security is explicitly required.

High-Degree of Business Confidentiality and Privacy

Bahamas business confidentiality and privacy protections are codified under the International Business Companies Act, which governs the formation and operation of IBCs. Under this legislation, the names of shareholders and directors are not required to be filed in any public register. That means beneficial ownership details remain outside the reach of public searches, which is a direct structural protection — not merely a policy preference.

Registered agents hold company records locally, but third parties have no general right of access to those documents. For business owners who want to separate their personal identity from their corporate activities, this architecture makes it possible without relying on nominee arrangements as a workaround.

The Financial Intelligence Unit of the Bahamas enforces anti-money laundering compliance, and registered agents are obligated to collect beneficial ownership data. That information is held privately by the agent, not published in a central public database accessible to competitors or outside parties.

Keep these points in mind:

- Shareholder and director details are not part of any public registry filing

- Beneficial ownership records are held by the registered agent, not disclosed publicly

- The IBC Act permits bearer shares to be held by an approved custodian, adding a further ownership privacy layer

- Disclosure to authorities is required under lawful order or regulatory investigation

Unlike many offshore jurisdictions that have moved to fully public beneficial ownership registers under international pressure, the Bahamas has maintained a private registry model accessible only to competent authorities.

Quick and Straightforward IBC Formation Process

The Bahamas IBC formation process benefits foreign business owners primarily through speed and low administrative friction. Under the International Business Companies Act, 2000, a new entity can typically be registered within one to two business days once documentation is in order, meaning your company can be legally operational before most jurisdictions have finished processing the initial paperwork.

Registration Requirements Are Minimal by Design

Forming an IBC requires a registered agent licensed under Bahamian law, a registered office address in the country, and a Memorandum and Articles of Association filed with the Registrar General's Department. No minimum share capital is prescribed for most standard IBC structures, which removes a common barrier that delays formation in higher-threshold jurisdictions.

Fast Bahamas company registration advantages extend beyond speed alone. Because the Registrar General's Department processes filings centrally and the documentation requirements are standardised, your formation costs remain predictable and the process does not depend on lengthy back-and-forth with multiple government bodies.

Annual Maintenance Obligations Are Light

Once registered, an IBC's ongoing compliance obligations are comparatively limited. The entity must maintain a registered agent and office, pay its annual government fee, and keep records sufficient to satisfy the Companies (Amendment) Act, 2018 requirements on beneficial ownership and financial records.

This structure means your administrative burden after incorporation does not escalate significantly year over year, allowing the business to allocate resources toward operations rather than regulatory maintenance.

Maximise Your Bahamas IBC Benefits with Expert Guidance

Speak with our corporate services team about setting up and maintaining a compliant Bahamas IBC tailored to your business objectives.

No Mandatory Local Director or Shareholder Requirements

Under the International Business Companies Act, 2000, an IBC registered in the Bahamas is not required to appoint a local director or resident shareholder. Full ownership and directorship can be held by foreign nationals, with no minimum local participation mandated. This is the Bahamas no local director requirement advantage that distinguishes the jurisdiction from many onshore regimes where foreign ownership must be diluted by local nominees.

- Your company can be 100% foreign-owned. No portion of equity is required to flow to a Bahamian resident or citizen, meaning you retain complete control over dividends, governance decisions, and exit strategy.

- There is no residency requirement for directors. You can appoint individuals from any country, which allows the board to reflect your actual decision-making structure rather than an artificial local arrangement created solely for compliance.

- Corporate directors are permitted. A foreign company can serve as the director of a Bahamian IBC, which is useful for group structures where a holding entity exercises board-level authority.

- Nominee arrangements remain optional. Where privacy is the objective, nominees can be used, but they are not a structural requirement imposed by law.

This flexibility means the legal ownership structure of your IBC can mirror your commercial reality without adjustments made to satisfy local-content rules.

Flexible International Business Companies Act Framework

The International Business Companies Act, 2000 (as amended) is the governing statute for IBCs registered in the Bahamas. One of the primary Bahamas International Business Companies Act advantages is the degree of structural latitude the legislation grants to incorporators, which is unusual even by offshore standards.

Under the Act, an IBC can be structured with a single class of shares or multiple classes carrying different rights, including voting, dividend, and liquidation preferences. These rights are defined in the company's articles of incorporation, giving shareholders the ability to engineer economic arrangements without being constrained by a rigid statutory default. No minimum share capital is prescribed, which removes a common barrier for newly formed entities.

The Act also permits a company to hold its own shares, reduce its share capital, and pay dividends from capital, subject to a solvency test. For business owners structuring holding companies, joint ventures, or investment vehicles, this flexibility allows the entity to be tailored to the transaction rather than the other way around.

A foreign investor incorporating an IBC with 1,000,000 authorized shares at a nominal par value of $0.001 per share incurs no statutory minimum capital requirement. The full economic structure, including preferred returns, carried interest, and redemption rights, can be encoded directly into the articles of incorporation at formation, without court approval or regulatory pre-clearance.

Stable Political Climate and Reputable Financial Centre

The Bahamas stable political climate for business stems from a long-standing constitutional democracy that has maintained uninterrupted civilian governance since independence in 1973. That institutional continuity means predictable regulatory conditions for foreign-owned entities. Your company operates under a legal framework that does not shift dramatically between administrations.

The Securities Commission of the Bahamas and the Financial Intelligence Unit operate under internationally recognized compliance standards, including alignment with Financial Action Task Force (FATF) recommendations. This regulatory posture matters because it affects how correspondent banks and institutional counterparties assess your entity's risk profile.

Membership in CARICOM and observer status with the Organisation of American States places the jurisdiction within recognized multilateral frameworks, which can reduce friction when dealing with counterparts who scrutinize the legitimacy of an offshore structure.

- The country is not listed on the EU's list of non-cooperative jurisdictions for tax purposes, a distinction that affects whether European business partners treat your structure with added scrutiny.

- The Bahamas Financial Services Board actively promotes the jurisdiction's compliance credentials to institutional audiences globally.

FATF compliance standards and international listing status can change; verify the Bahamas' current standing on relevant watchlists before finalizing your structure.

Access to a Wide Double Taxation Treaty Network

The phrase "Bahamas double taxation treaty benefits" requires careful framing. Unlike many offshore centers, the Bahamas has not pursued an extensive bilateral tax treaty network. It is not a party to a broad set of double taxation agreements (DTAs) in the traditional sense. For foreign investors, understanding what this means in practice is more useful than assuming treaty coverage that does not exist.

What the Bahamas Has Signed

The jurisdiction has entered into a series of Tax Information Exchange Agreements (TIEAs) rather than comprehensive income tax treaties. These agreements, negotiated under frameworks endorsed by the OECD, cover information sharing on tax matters with counterpart jurisdictions including the United States, Canada, the United Kingdom, and several EU member states. TIEAs are distinct from DTAs; they do not eliminate withholding taxes or allocate taxing rights between countries.

Why This Still Benefits Your Business Structure

Because the Bahamas imposes no corporate income tax, capital gains tax, or withholding tax domestically, the absence of a wide DTA network carries less structural weight than it would for a high-tax jurisdiction. A business incorporated here has no domestic tax liability against which a treaty reduction would apply. The practical advantage is that your entity already operates from a zero-tax base, which removes the primary problem that double taxation treaties are designed to solve.

- TIEA partners include the US, Canada, UK, France, and Germany, among others

- TIEA compliance supports the entity's credibility with foreign regulators and banking institutions

- Bahamas-incorporated firms benefit from OECD-aligned transparency standards without domestic tax exposure

USD-Pegged Currency Ensures Financial Stability

The Bahamian dollar has maintained a fixed 1:1 peg to the US dollar since 1966, administered by the Central Bank of the Bahamas under the Central Bank of the Bahamas Act. This peg is the primary Bahamas USD-pegged currency stability advantage for foreign business owners: transactions, contracts, and account balances denominated in BSD carry no conversion risk against the world's primary reserve currency.

For offshore structures, this arrangement removes a layer of financial uncertainty that exists in many other jurisdictions. Since IBCs incorporated under the International Business Companies Act 2000 routinely conduct business in USD, the peg means pricing, invoicing, and profit repatriation all operate without exposure to exchange rate fluctuations between the local and functional currency.

Practical implications for your business include:

- USD accounts and BSD accounts are interchangeable at par, meaning treasury management carries no cross-currency reconciliation burden.

- Contracts priced in USD require no hedging instruments to offset currency movement between execution and settlement.

- Foreign investors reviewing financial statements avoid the distortion that currency depreciation introduces in jurisdictions with floating or managed-float regimes.

- Banking relationships with institutions licensed under the Banks and Trust Companies Regulation Act 2020 can be maintained in USD without conversion friction.

The Central Bank holds foreign currency reserves to support the peg, which underpins the operational reliability of this arrangement over decades. For a firm holding assets or processing receipts in US dollars, this fixed-rate environment translates directly into predictable cash flow and reduced administrative overhead in cross-border financial management.

Why the Bahamas Stands Out Among Offshore Jurisdictions

Compared against other Caribbean and Atlantic offshore centres, the Bahamas offers a combination of structural features that few jurisdictions in the region match simultaneously. Cayman Islands, BVI, and Bermuda are the competitors most foreign incorporators genuinely weigh against a Bahamian IBC, given their shared target market of wealth management clients, holding structures, and international trading companies.

What the comparison reveals is not simply that tax rates differ, but that the regulatory and operational profile of a Bahamian entity sits at a distinct intersection: no corporate income tax, no mandatory local directorship, a USD-pegged currency, and IBC formation governed by a well-established statutory framework without the higher cost base associated with Cayman or Bermuda. BVI offers similar tax neutrality, but its annual fees and compliance obligations have increased substantially in recent years. Bermuda carries a stronger reputational premium but also a significantly higher cost of incorporation and maintenance, which affects smaller businesses and holding entities disproportionately.

| Parameter | Bahamas | Cayman Islands | BVI | Bermuda |

|---|---|---|---|---|

| Corporate Income Tax | 0% | 0% | 0% | 0% |

| Capital Gains Tax | None | None | None | None |

| Local Director Required | No | No | No | No |

| USD-Pegged Currency | Yes | Yes (CI$) | Yes (USD) | No (BMD, pegged) |

| Annual Government Fee (IBC) | Low–moderate | High | Moderate–high | High |

| Privacy / Confidentiality | Strong | Moderate | Moderate | Moderate |

| FATF Status | Compliant | Compliant | Compliant | Compliant |

| Main Regulatory Body | SCB | CIMA | FSC | BMA |

Compliance Services for Bahamas Companies

Maintain good standing under Bahamian law with ongoing compliance support, including annual filings, registered agent obligations, and regulatory reporting.

Conclusion

The benefits of incorporating in the Bahamas rest on a combination of structural features that are difficult to replicate elsewhere: zero corporate income tax under the International Business Companies Act, a high degree of statutory privacy, and a USD-pegged currency that eliminates exchange rate exposure for businesses operating in dollar-denominated markets.

Not every structure fits every situation. The IBC framework suits businesses with international operations and non-resident ownership, but the applicable advantages depend on your industry, where your clients are based, and how your entity generates income. Understanding that fit matters more than the general case for any jurisdiction.

For businesses that do qualify, the legal and fiscal framework is well-defined and backed by a stable regulatory environment overseen by the Securities Commission of the Bahamas and the Registrar General's Department. The path forward begins with confirming that your business model aligns with the IBC structure and that your compliance obligations are properly mapped before formation.

Start Your Bahamas Company with Expanship Today

Expanship supports the full formation and ongoing compliance lifecycle for Bahamas International Business Companies registered under the International Business Companies Act, 2000. From preparing your incorporation documents to liaising with the Registrar General's Department on your behalf, the firm handles each stage of the process directly. Every engagement accounts for the specific obligations that apply to your entity type, including annual renewal filings and economic substance declarations where relevant.

Expanship's service scope for Bahamas company formation covers the following:

- Preparation and legalization of incorporation documents, including the Memorandum and Articles of Association

- Provision of a registered agent and registered office address, as required under the IBC Act

- Government filing and direct liaison with the Registrar General's Department

- Post-incorporation compliance management, including annual filings and record-keeping obligations

- Banking introduction assistance to support your business account setup with regional and international institutions

To incorporate in the Bahamas with Expanship, or to request further information about Expanship Bahamas company formation services, contact the team directly through the Expanship Bahamas enquiry page.

Frequently Asked Questions (FAQ)

An IBC incorporated under the International Business Companies Act is not subject to corporate income tax on business profits. The Bahamas imposes no income tax at the corporate level, and this applies regardless of the volume or source of profits generated outside the jurisdiction. There is also no capital gains tax, withholding tax on dividends, or inheritance tax applicable to the entity or its shareholders.

Incorporation can generally be completed within one to two business days once all required documentation is submitted to the Registrar General's Department. The process involves reserving a company name, filing the Memorandum and Articles of Association, and paying the applicable government fees. Timelines may extend slightly if additional due diligence documentation is required.

Under the International Business Companies Act, an IBC requires a minimum of one director and one shareholder, both of whom may be the same individual. There is no obligation for either to be a Bahamian resident or national. Corporate directors and corporate shareholders are both permitted under the Act.

An IBC that conducts business within the Bahamas or with Bahamian residents loses the specific exemptions afforded under the International Business Companies Act framework. Such activity requires separate licensing and brings the entity within the scope of domestic tax and regulatory obligations. The IBC structure is designed for international operations conducted outside the jurisdiction.

The Bahamian dollar maintains a fixed 1:1 peg with the US dollar, which has been in place for decades and is administered through the Central Bank of the Bahamas. This peg eliminates exchange rate risk between the two currencies and provides predictability for businesses denominating contracts or holding assets in USD. The arrangement is backed by the Central Bank's reserve management policy.

The Bahamas has a limited treaty network compared to jurisdictions such as the Netherlands or Luxembourg, and this is a relevant consideration for structures where treaty access is a priority. The jurisdiction has signed Tax Information Exchange Agreements (TIEAs) with a number of countries, which affects its international standing but does not function as a double taxation treaty. Shareholders should assess their own country's domestic rules regarding controlled foreign corporations and foreign income inclusion before relying on Bahamian structuring for treaty purposes.

The Financial Intelligence Unit (FIU) of the Bahamas has authority to access beneficial ownership and financial information as part of anti-money laundering and counter-financing of terrorism obligations. While the IBC framework provides confidentiality from public disclosure, it does not shield information from lawful requests by the FIU or competent foreign authorities under mutual legal assistance arrangements. Confidentiality under Bahamian law applies to public registries and third parties, not to regulatory and law enforcement access.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.