Key Takeaways

- Samoa's business entities fall under two separate regulatory bodies: the Samoa International Finance Authority (SIFA) for international structures and the Ministry of Commerce, Industry and Labour (MCIL) for domestic registrations.

- International Companies incorporated under the International Companies Act 1988 operate under a zero-tax regime on foreign-sourced income, making them the most commonly registered structure among non-resident entrepreneurs.

- Each of Samoa's nine available entity types — ranging from the International Company to the Sole Trader — carries distinct liability profiles, registration requirements, and operational restrictions under separate legislative instruments.

- Beneficial ownership requirements introduced through Samoa's regulatory framework have increased transparency obligations across entity types, affecting reporting duties at the point of formation.

Introduction to Entity Types in Samoa (WS)

Located in the South Pacific Ocean, Samoa is an independent sovereign nation situated approximately midway between Hawaii and New Zealand, within the wider Polynesian island group. The country operates under a stable parliamentary system and maintains a distinct legal identity from American Samoa, its neighbouring territory to the east.

Company registration falls under the jurisdiction of the Samoa International Finance Authority (SIFA), which administers the incorporation and ongoing compliance of business entities operating within the country's legal framework. Domestic registrations are handled through the Ministry of Commerce, Industry and Labour (MCIL). The types of business entities in Samoa span both resident and non-resident structures, each governed by separate legislative instruments.

From a tax perspective, certain entity types — particularly those incorporated under the International Companies Act 1988 — operate under a zero-tax regime on foreign-sourced income, while locally operating firms are subject to domestic tax obligations.

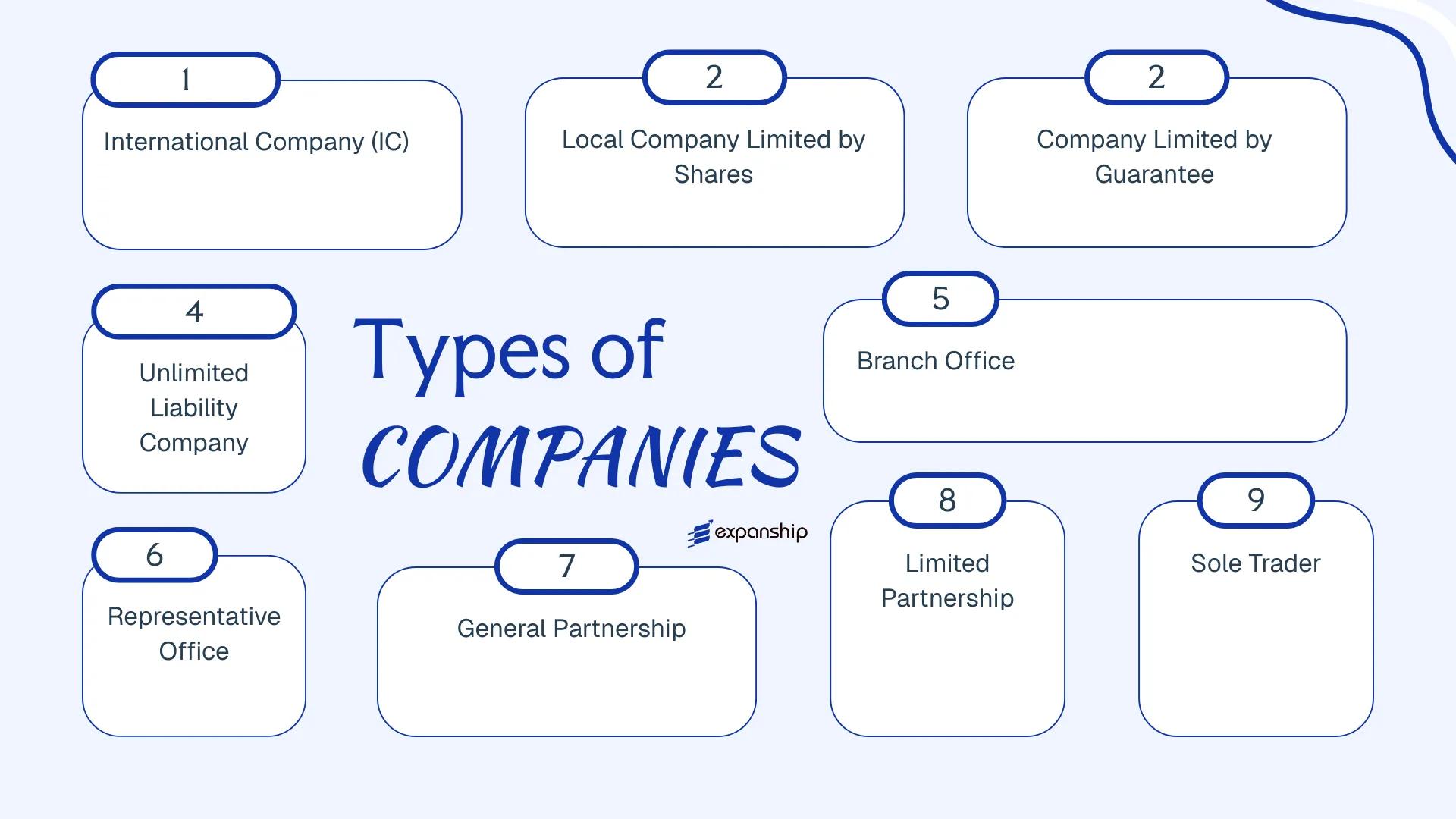

Available Samoa WS company structures include:

- International Company (IC)

- Local Company Limited by Shares

- Company Limited by Guarantee

- Unlimited Liability Company

- Branch Office

- Representative Office

- General Partnership

- Limited Partnership

- Sole Trader

Each of these Samoa corporate entity types carries distinct registration requirements, liability implications, and operational restrictions, all of which are examined in the sections that follow.

An Overview of Business Structures in Samoa (WS)

Samoa's corporate framework provides several distinct entity types, each governed primarily by the Companies Act 2001 for domestic structures and the International Companies Act 1987 for offshore formations. The Samoa International Finance Authority (SIFA) and the Registrar of Companies administer registration and ongoing compliance. Each structure carries different implications for liability, taxation, and permitted activities.

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| International Company (IC) | Incorporated company | Limited | Exempt | No | 1 shareholder | SIFA | International Companies Act 1987 |

| Local Company Limited by Shares | Incorporated company | Limited | Taxed | Yes | 1 shareholder | Registrar of Companies | Companies Act 2001 |

| Company Limited by Guarantee | Incorporated company | Limited | Taxed | Yes | 1 member | Registrar of Companies | Companies Act 2001 |

| Unlimited Liability Company | Incorporated company | Unlimited | Taxed | Yes | 1 shareholder | Registrar of Companies | Companies Act 2001 |

| Branch Office | Foreign entity | Parent liable | Taxed | Yes | N/A | Registrar of Companies | Companies Act 2001 |

| Representative Office | Foreign entity | Parent liable | Generally exempt | No | N/A | Registrar of Companies | Companies Act 2001 |

| General Partnership | Unincorporated | Unlimited | Taxed | Yes | 2 partners | Registrar of Companies | Partnership Act 1975 |

| Limited Partnership | Unincorporated | Mixed | Taxed | Yes | 2 partners | Registrar of Companies | Partnership Act 1975 |

| Sole Trader | Unincorporated | Unlimited | Taxed | Yes | 1 person | Registrar of Companies | Business Licenses Act |

Each of these structures is examined in full in the sections below.

International Company (IC)

Samoa International Company IC registration is governed by the International Companies Act 1987 (as amended), administered through the Samoa International Finance Authority (SIFA). An IC is a distinct legal entity, separate from its members, carrying limited liability by default. Structurally, it functions as a hybrid offshore vehicle — capable of holding assets, entering contracts, and conducting business outside the jurisdiction under a single incorporated form.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | International Company (IC) | Incorporated under the International Companies Act 1987 |

| Members | Shareholders (minimum 1, no maximum) | Corporate shareholders permitted; bearer shares abolished |

| Directors | Minimum 1 director (individual or corporate) | No residency requirement for directors |

| Local Presence | Registered Agent required; no registered office obligation beyond agent's address | Registered Agent must be SIFA-licensed |

| Capital | No minimum share capital; WST or any foreign currency | Shares may be issued at par or no-par value |

| Privacy | Beneficial ownership not on public record | Register of members held by Registered Agent |

Focus Points

- Taxation: ICs are exempt from Samoan income tax, withholding tax, and stamp duty on income sourced outside Samoa; no VAT obligations apply to offshore activities.

- Economic Substance: Samoa does not currently impose economic substance requirements on ICs, unlike many competing offshore jurisdictions.

- Annual Compliance: Annual renewal fees are payable to SIFA; no requirement to file financial statements or audited accounts.

- Treaty Access: Samoa has a limited tax treaty network; ICs generally cannot access treaty benefits, as they are not tax residents.

- Restrictions: ICs are prohibited from conducting business with Samoan residents, owning local real estate, or operating as a bank or insurance company without separate licensing.

Closing

An IC suits holding structures, IP ownership, and international trading operations where activity occurs entirely outside Samoa. The absence of minimum capital and accounting filing requirements reduces administrative overhead, though the limited treaty network restricts its utility for structures requiring double taxation relief.

Best suited for non-resident investors seeking a low-compliance offshore holding or trading vehicle with full foreign ownership and no local operational footprint.

Company Incorporation in Samoa

Register an International Company (IC) in Samoa with end-to-end support from entity setup to Registered Agent appointment.

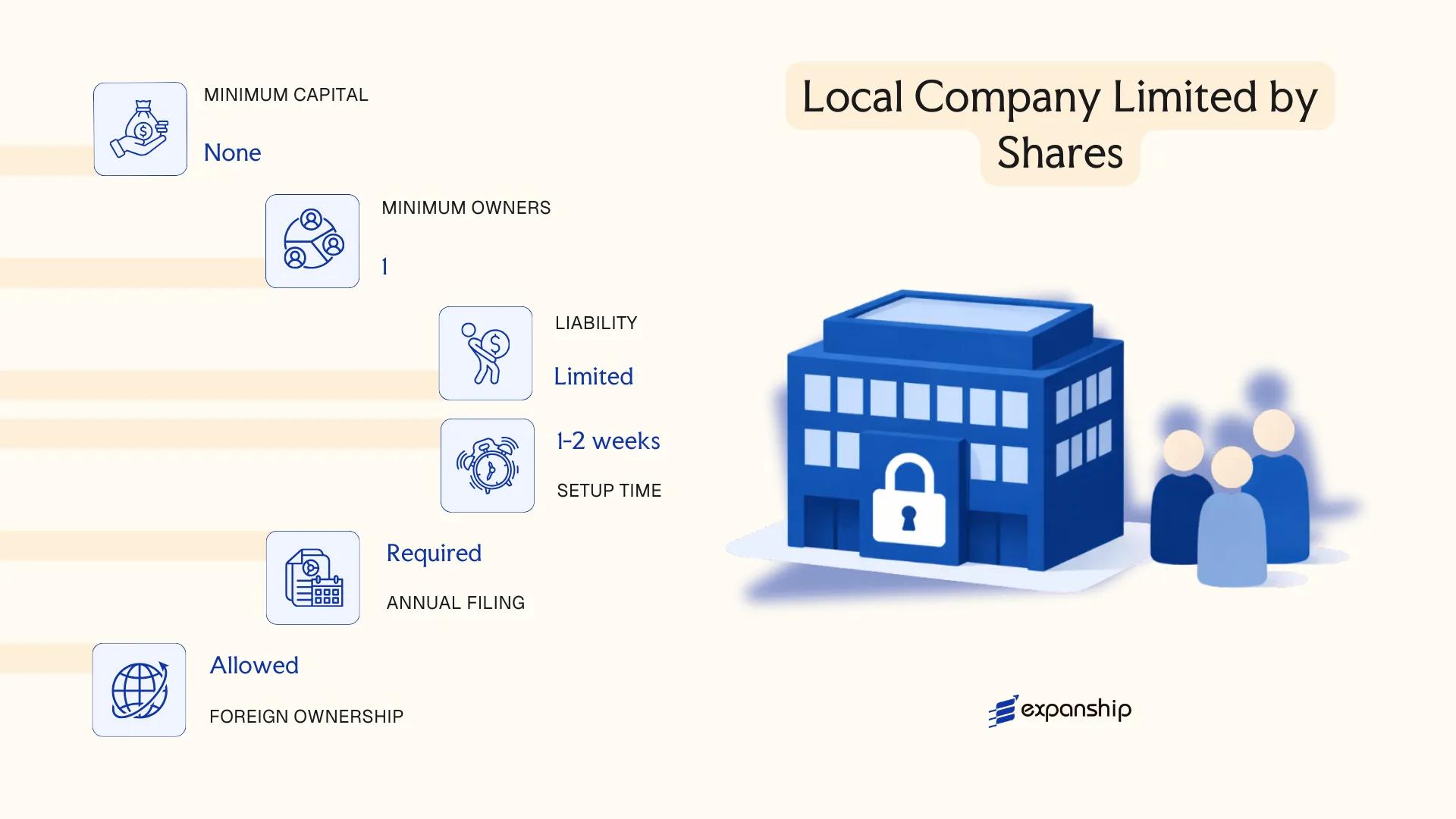

Local Company Limited by Shares

A Samoa local company limited by shares is incorporated under the Companies Act 2001 and is governed domestically, making it distinct from the offshore International Company structure. The entity holds separate legal personality, meaning it can own assets, enter contracts, and incur liabilities independently of its shareholders, whose financial exposure is capped at the unpaid amount on their shares.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Company Limited by Shares | Incorporated under the Companies Act 2001 |

| Members | Shareholders and Directors; min. 1 each; no statutory maximum | A sole director-shareholder structure is permitted |

| Local Presence | Registered office in Samoa required | Must be a physical address; a PO Box alone is not sufficient |

| Capital | No minimum share capital prescribed; denomination in any currency | Shares must be issued at a fixed or no-par value |

| Privacy | Shareholder and director details filed with the Samoa Registry of Companies | Register is publicly accessible |

Focus Points

- Taxation: Subject to corporate income tax on Samoa-sourced income; VAT may apply depending on turnover thresholds; dividend withholding tax applies to distributions to non-residents.

- Annual Compliance: Annual returns and financial statements must be filed with the Registrar of Companies.

- Economic Substance: No formal economic substance regime applies to local companies at present.

- Treaty Access: May benefit from tax treaties Samoa has entered into, subject to residency conditions.

- Conversion: Can be converted to a different company structure under the Companies Act 2001 by special resolution and regulatory approval.

Closing

This structure suits businesses conducting trade, providing services, or operating commercially within the domestic market. The capped shareholder liability is a practical advantage, though the public disclosure of ownership information limits confidentiality compared to offshore alternatives.

Best suited for entrepreneurs and businesses targeting the local Samoan market or requiring a domestically recognised legal entity for licensing, contracting, or government engagement.

Company Limited by Guarantee

A Samoa company limited by guarantee (CLG) is governed by the Companies Act 2001, administered by the Samoa Ministry of Commerce, Industry and Labour (MCIL). Unlike a share-based company, members contribute a fixed guaranteed sum upon winding up rather than purchasing equity. The entity holds separate legal personality, meaning it can contract, sue, and hold assets in its own name.

This structure is typically associated with non-profit activity, though the legislation does not restrict CLGs exclusively to non-commercial purposes. For organisations seeking the Samoa WS guarantee company structure without distributing profits to members, this form provides a recognised legal vehicle.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Company Limited by Guarantee | Incorporated under the Companies Act 2001 |

| Members | Minimum 1; no statutory maximum | Called "members"; no shareholders |

| Directors | Minimum 1; no residency requirement | Corporate directors permitted |

| Local Presence | Registered office in Samoa required | Must maintain a local registered address |

| Guarantee Amount | Defined in the constitution | Each member's liability capped at their pledged sum |

| Privacy | Beneficial ownership subject to MCIL records | No public share register; constitutionon file |

Focus Points

- Taxation: CLGs engaged in non-profit activity may qualify for exemption from income tax; commercial income could attract standard corporate tax; GST and withholding tax obligations depend on the nature of activities conducted.

- Annual Compliance: Annual returns must be filed with MCIL; financial statements may be required depending on the scale of operations.

- Economic Substance: No specific economic substance regime applies to CLGs under current Samoa legislation.

- Conversion: Conversion from a CLG to a share-based company is not straightforwardly provided for under the Companies Act 2001; restructuring typically requires dissolution and re-incorporation.

- Restrictions: Profit distribution to members is generally prohibited; any surplus must be applied toward the organisation's stated objects.

Closing

A CLG suits membership associations, charitable bodies, and industry groups requiring a formal legal structure without equity ownership. The absence of share capital simplifies governance, though the restriction on profit distribution makes this unsuitable for any venture with commercial return objectives.

Best suited for non-profit organisations, foundations, and member-based associations seeking a legally recognised entity in Samoa without a profit-sharing mechanism.

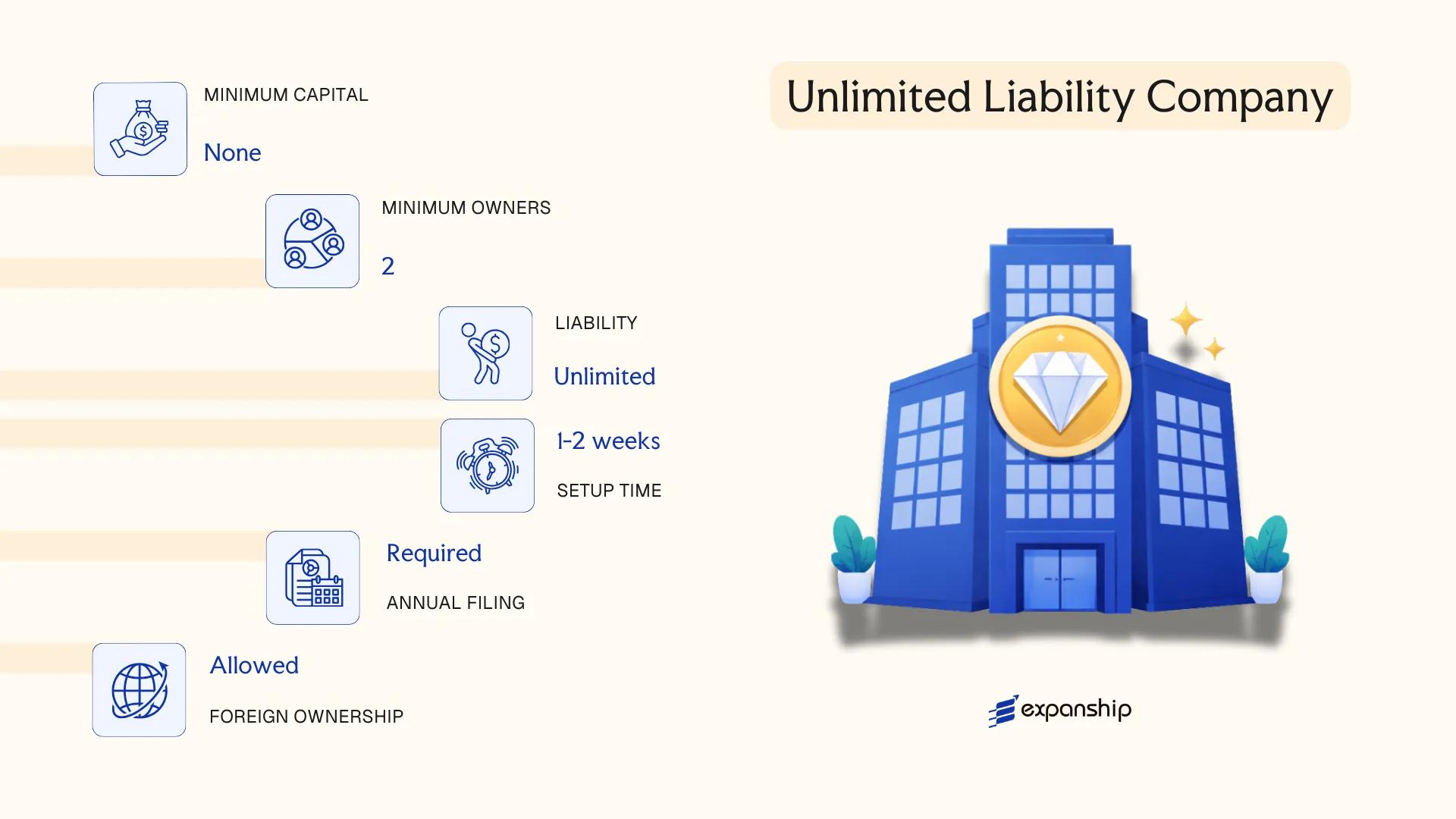

Unlimited Liability Company

Samoa unlimited liability company registration is governed by the Companies Act 2001, administered by the Samoa Ministry of Commerce, Industry and Labour (MCIL). Unlike most corporate structures, an unlimited liability company carries separate legal personality but removes the liability shield — members remain personally responsible for the company's debts without any cap.

This structure is uncommon in practice and generally pursued in narrow circumstances where the absence of limited liability is either legally required or commercially accepted by the parties involved.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unlimited liability company with separate legal personality | Members bear full personal liability for company debts |

| Members | Minimum 1 shareholder; no maximum | Shareholders can be natural persons or corporate entities |

| Directors | Minimum 1 director | No residency requirement specified under the Companies Act 2001 |

| Local Presence | Registered office in Samoa required | Must maintain a physical registered address within the jurisdiction |

| Share Capital | No statutory minimum; denominated in WST or foreign currency | Shares may or may not have par value |

| Privacy | Register of members filed with MCIL | Beneficial ownership information subject to disclosure rules |

Focus Points

- Taxation: Subject to standard corporate income tax; VAT obligations apply if turnover thresholds are met; no specific exemptions tied to entity structure alone.

- Annual Compliance: Annual returns must be filed with MCIL; financial records must be maintained.

- Conversion: Conversion to a limited liability structure is possible under the Companies Act 2001, subject to MCIL approval.

- Restrictions: Not eligible for the offshore benefits available to International Companies under the International Companies Act 1987.

Closing

An unlimited liability company suits restructuring scenarios or group arrangements where one entity within a corporate group absorbs liability by design. The primary drawback is unambiguous — personal exposure for shareholders creates material financial risk that most commercial operators will not accept.

Best suited for intra-group holding arrangements where a parent entity is willing to assume unlimited liability as part of a deliberate corporate structure.

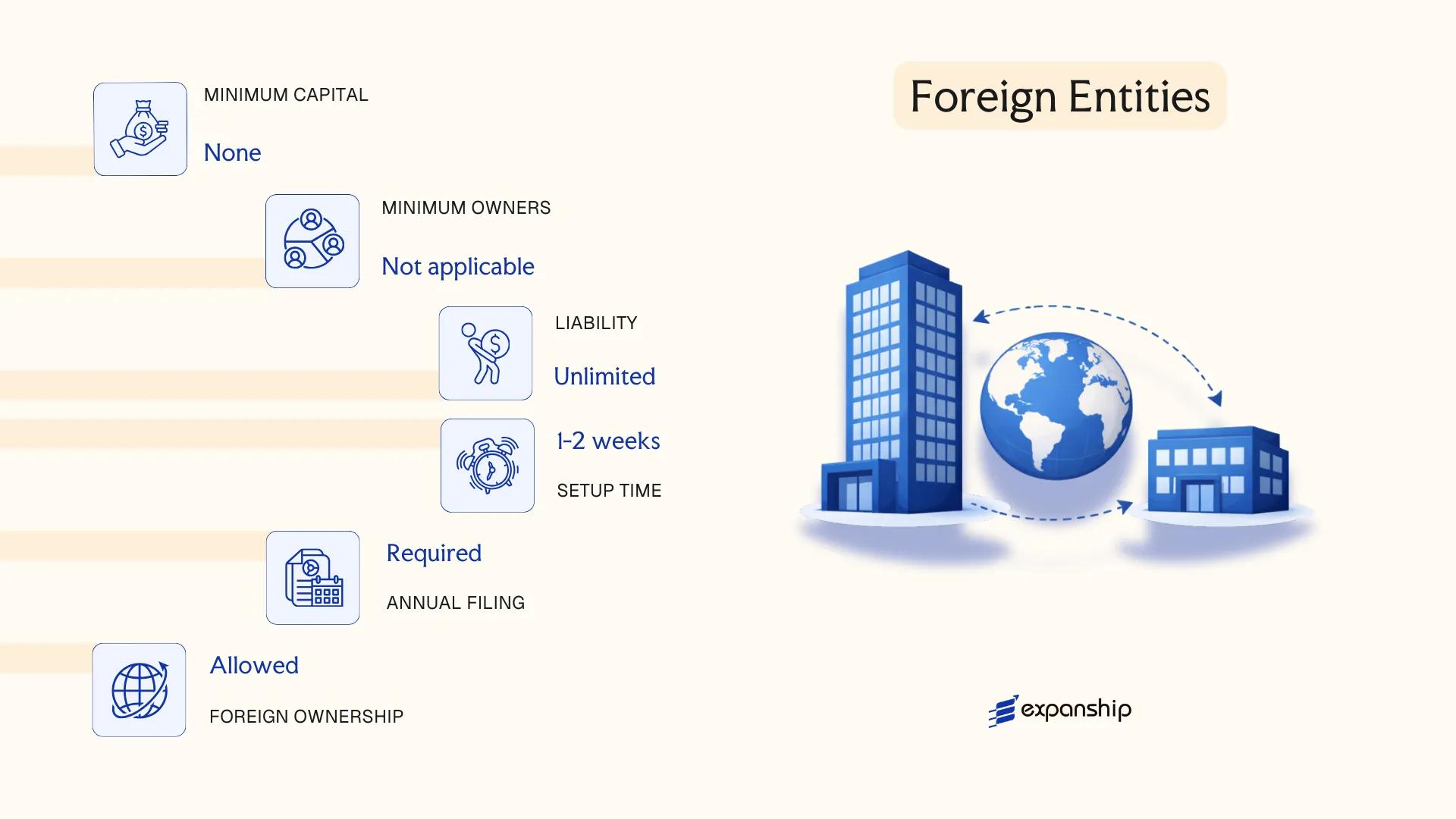

Foreign Entities [Branch Office, Representative Office]

A foreign company branch office in Samoa (WS) is governed by the Companies Act 2001, which requires overseas companies to register with the Samoa Ministry of Commerce, Industry and Labour (MCIL) before conducting business within the territory. A branch does not constitute a separate legal entity — it remains an extension of the parent company, which bears full liability for the branch's obligations.

A representative office occupies a more restricted position. Rather than conducting revenue-generating activities, it is permitted to carry out market research, liaison functions, and promotional activities on behalf of the parent firm.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Branch: extension of parent; Representative: non-trading presence | Neither form has separate legal personality |

| Liability | Parent company bears full liability | No liability shield at the local level |

| Local Presence | Registered agent and registered office in Samoa required | MCIL registration mandatory |

| Directors / Officers | At least one local authorized representative | Must be appointed for service of process |

| Capital | No prescribed minimum capital | Parent's financial statements must be filed |

| Privacy | Parent company details are publicly disclosed | Filed documents accessible via MCIL |

Focus Points

- Taxation: Branch profits are subject to corporate income tax; withholding tax may apply on remittances to the parent; no separate VAT registration threshold applies to branch turnover.

- Compliance: Annual filing of the parent company's audited financial statements with MCIL is required.

- Restrictions: Representative offices are prohibited from generating local revenue or entering commercial contracts.

- Conversion: A branch may be converted into a locally incorporated entity, though this involves a separate registration process.

A branch suits foreign firms testing the local market or executing specific contracts without establishing an independent subsidiary; the key limitation is unrestricted parental liability exposure.

Best suited for established foreign companies seeking a direct operational presence without the administrative overhead of incorporating a standalone local subsidiary.

Partnerships [General Partnership, Limited Partnership]

Samoa limited partnership registration WS falls under the Partnership Act 1975, the primary legislation governing both general and limited partnerships in the jurisdiction. Neither structure carries separate legal personality — the business and its partners remain legally indistinguishable, which has direct implications for liability exposure and asset protection.

General partnerships bind all partners jointly and severally for the firm's debts and obligations. A limited partnership introduces a two-tier structure: at least one general partner bears unlimited liability for the entity's obligations, while limited partners are liable only to the extent of their contributed capital.

Key Characteristics

| Requirement | General Partnership | Limited Partnership |

|---|---|---|

| Legal Form | Unincorporated; no separate legal personality | Unincorporated; no separate legal personality |

| Members | Partners (minimum 2, no statutory maximum) | Min. 1 general partner + 1 limited partner |

| Liability | All partners: unlimited, joint and several | General partner: unlimited; limited partner: capped at capital contribution |

| Local Presence | No statutory registered agent requirement, but a local address is advisable | Same as general partnership |

| Capital | No minimum capital requirement; WST or foreign currency accepted | No minimum; limited partner's contribution must be defined in the partnership agreement |

| Privacy | Partnership agreements are not publicly filed; partner details have limited public disclosure | Same as general partnership |

Focus Points

- Taxation: Partnerships are treated as pass-through structures — income is taxed at the individual partner level under Samoa's Income Tax Act 1974; no corporate-level tax applies, and no VAT or withholding tax obligations arise at the entity level for most structures.

- Annual Compliance: No statutory annual return filing is required for unregistered partnerships, though tax obligations to the Samoa Revenue Authority remain.

- Economic Substance: No formal economic substance regime applies to partnerships under current Samoan law.

- Treaty Access: Partnerships generally do not qualify as residents under double tax agreements, as they lack separate legal personality and are fiscally transparent.

- Restrictions: Limited partners who participate in active management risk losing their limited liability protection under the Partnership Act.

Closing

Partnerships suit smaller commercial ventures, professional services arrangements, or joint investment projects where partners are comfortable with the liability implications. The pass-through tax treatment is a functional advantage, though the absence of liability protection for general partners is a structural constraint that warrants careful consideration.

General partnerships are best suited for closely held professional or trading arrangements between trusted parties; limited partnerships are more appropriate where passive investors require defined liability exposure.

Sole Trader

Sole trader registration in Samoa WS falls under the Business Licenses Act 1998, which requires all persons conducting business to obtain the appropriate licence before commencing trade. Unlike incorporated entities, a sole trader has no separate legal personality — the individual and the business are legally the same, meaning personal assets are fully exposed to business liabilities.

Registration is handled through the Ministry of Commerce, Industry and Labour (MCIL). The process is straightforward, though operating without limited liability protection means your personal finances remain at direct risk from any business debts or legal claims.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated sole proprietorship | No separate legal personality from the owner |

| Proprietor | Single individual only | One owner; cannot have co-owners or partners |

| Local Presence | Physical business address required | No registered agent requirement, but a local address must be stated on the licence |

| Capital | No minimum capital requirement | Denominated in Samoan Tālā (WST) by default |

| Privacy | Owner's name is publicly associated with the business | No beneficial ownership register separation |

| Liability | Unlimited personal liability | Personal assets at risk for all business obligations |

Focus Points

- Taxation: Subject to personal income tax under the Income Tax Act 2012; no separate corporate tax applies; GST registration is required if annual turnover exceeds the applicable threshold.

- Annual Compliance: Business licence renewal is required annually through MCIL; no separate financial statements are required for filing purposes.

- Economic Substance: No formal substance requirements apply to this structure.

- Treaty Access: As an unincorporated individual, access to double tax agreements depends on personal tax residency status.

- Conversion: A sole trader can transition to a registered company under the Companies Act 2001, though this requires fresh incorporation.

Closing Paragraph

A sole trader setup suits resident individuals providing services or running small local operations where administrative simplicity is the priority. The absence of a minimum capital requirement and the low compliance burden make it accessible, but unlimited personal liability is a material drawback for any business carrying financial or legal risk.

Samoan resident individuals operating small-scale, low-risk service businesses who do not require asset protection or external investment.

How to Choose the Right Entity Type in Samoa (WS)

Selecting how to choose a business entity in Samoa requires matching your operational profile to the legal and regulatory framework that governs each structure under Samoan law.

Why Your Entity Choice Matters

The structure you register has direct legal and financial consequences.

- Registering an International Company while conducting local trade in Samoa violates the International Companies Act 1988, which prohibits ICs from doing business with Samoan residents — and can result in deregistration or penalties.

- Choosing a tax-exempt entity, such as an IC, when treaty-based withholding tax reductions are needed disqualifies your business from claiming relief under any double tax agreement, as exempt entities typically fall outside treaty scope.

- Selecting a structure without substance capacity when economic substance obligations apply can trigger reporting failures and associated regulatory sanctions.

- Forming a company when a trust or foundation would serve asset protection or succession objectives locks you into annual shareholder maintenance obligations that do not apply to those alternatives.

Key Factors to Consider

- Business Activity: Active trading, passive asset holding, and regulated sectors such as banking or insurance each require a distinct structure.

- Local vs. Offshore Operations: Transacting with Samoan residents requires a locally registered company; purely external operations may qualify for an IC.

- Tax Objectives: Whether your priority is full exemption, treaty access, or a specific domestic tax regime determines which entities are eligible.

- Privacy Requirements: If public disclosure of directors or shareholders is a concern, nominee structures or entities with confidentiality provisions may be relevant.

- Substance Capacity: If you cannot maintain staff or decision-making functions in the jurisdiction, choose an entity type with lower or no substance thresholds.

- Exit Strategy: Not all Samoan entities permit redomiciliation or conversion — confirm this before formation if flexibility is a priority.

Compliance Services for Companies in Samoa

Ongoing compliance support for Samoan entities, including annual returns, registered agent obligations, and regulatory filings.

Conclusion

Incorporating a company in Samoa WS means selecting from a defined set of structures, each governed under distinct legislation with its own liability profile and operational scope. The International Company remains the most registered entity type, favored by non-resident entrepreneurs for its tax-exempt status on foreign-sourced income. Local Companies Limited by Shares suit resident-owned trading operations, while Companies Limited by Guarantee serve non-commercial purposes such as associations. Unlimited Liability Companies are rare in practice, and foreign branch offices function as extensions of an existing legal person rather than separate entities. Partnerships and sole trader arrangements address smaller-scale or professional activity.

Samoa's regulatory framework, administered by the Ministry of Commerce, Industry and Labour, has trended toward greater transparency through beneficial ownership requirements. Selecting the correct structure from the outset determines your reporting obligations, liability exposure, and long-term operational flexibility. Expanship's team works directly with these considerations during the formation process.

How Expanship Can Assist You

Expanship's Samoa company formation services cover every stage of the process, from selecting the right structure under the International Companies Act 1987 or the Companies Act 2001 to filing with the Samoa Ministry of Commerce, Industry and Labour (MCIL). Each entity type discussed in this blog — from the International Company to the local company limited by shares — carries distinct registration requirements and ongoing obligations that vary in scope and timing.

Expanship manages the full lifecycle of your entity in Samoa:

- Document preparation and notarization or apostille legalization

- Registered agent and registered office provision in Samoa

- Filing and liaison with MCIL and the Samoa Companies Registry

- Post-incorporation compliance management, including annual returns

- Banking introduction assistance for corporate account setup

Our corporate services in Samoa are available across all entity classes registered in the jurisdiction.

To discuss your specific requirements, contact Expanship Samoa directly.

Frequently Asked Questions (FAQ)

The International Company (IC), governed by the International Companies Act 1987, is by far the most frequently incorporated structure. Its exemption from local taxation on foreign-sourced income and minimal reporting requirements make it the default choice for non-resident entrepreneurs pursuing offshore holding or asset-protection arrangements.

An IC is barred from conducting business with Samoa residents or owning local real estate, whereas a Local Company Limited by Shares may trade domestically without restriction. The IC pays no corporate tax on foreign income, while the local company is subject to standard Samoan corporate tax rates. Compliance obligations also diverge significantly — ICs face lighter annual filing requirements compared to domestic firms registered under the Companies Act 2001.

The International Company provides the highest degree of confidentiality. Beneficial ownership details, shareholder registers, and financial accounts are not filed on any public record. Nominee directors and shareholders are permitted under the International Companies Act 1987.

An IC requires only one director and one shareholder, both of which a single person can fulfill. A General Partnership, by contrast, requires a minimum of two partners. A Company Limited by Guarantee also requires members, so sole formation is not possible for every structure.

Foreign nationals may incorporate an International Company without restriction — no local director or shareholder is mandated by statute. Registering a Local Company Limited by Shares or a foreign branch is also permitted, though branch offices must appoint a local registered agent and file constitutional documents with the Samoa Companies Office. Sole Trader registration is generally limited to individuals with legal residency.

Samoa's Companies Act 2001 provides a mechanism for re-registration and continuation, allowing domestic companies to convert between certain structures. An IC may also re-domicile into or out of Samoa under continuance provisions in the International Companies Act 1987. Conversion between fundamentally different legal forms — such as from a partnership to a limited company — typically requires dissolution and fresh incorporation rather than a direct conversion.

International Companies, Local Companies Limited by Shares, Companies Limited by Guarantee, and Unlimited Liability Companies all hold distinct legal personality separate from their members. General Partnerships do not — partners remain personally liable for firm obligations. Limited Partnerships occupy a middle ground, where limited partners are shielded from personal liability while the general partner retains unlimited exposure.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.