Key Takeaways

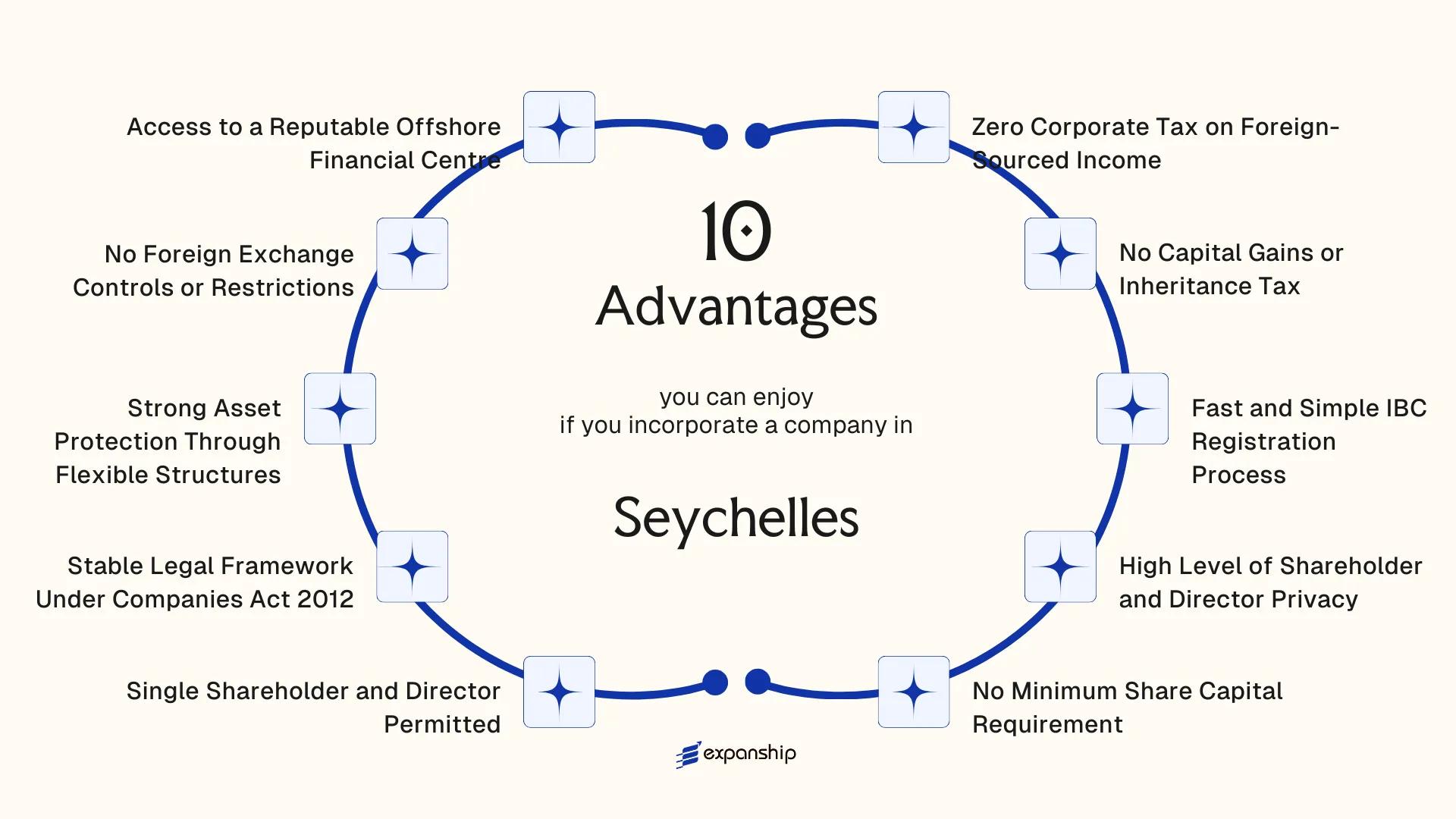

- Seychelles IBCs incorporated under the International Business Companies Act 2016 owe no corporate tax on foreign-sourced income, eliminating a recurring cost that would otherwise compound across every international transaction the entity processes.

- Because the Financial Services Authority permits a single individual to serve simultaneously as sole shareholder and sole director, solo operators can maintain a fully compliant Seychelles structure without assembling a separate board or nominee arrangement.

- The absence of both a minimum share capital requirement and capital gains tax means an IBC can be formed and held at minimal financial exposure, with no penalisation when appreciated assets are disposed of.

- Seychelles' territorial tax basis, enforced through the framework established under the Companies Act 2012 and the IBC Act 2016, provides foreign business owners with a legally defined separation between offshore earnings and local tax liability — a distinction that is explicit in statute rather than dependent on administrative discretion.

Seychelles is an independent island nation in the western Indian Ocean, governed as a republic and recognized internationally as an established offshore financial centre. Company registration falls under the authority of the FSA, the Financial Services Authority, which oversees the licensing and regulation of corporate entities incorporated under local law. The most common vehicle used by foreign businesses is the International Business Company.

From a tax posture, the jurisdiction operates on a territorial basis, meaning income generated outside the country is generally not subject to local corporate tax. Foreign ownership is broadly permitted across most sectors, and there are no general restrictions preventing non-residents from holding full ownership of a locally incorporated entity. This article examines the principal benefits of incorporating in Seychelles and what they mean in practical terms for your business. The Seychelles company formation advantages covered here span tax treatment, privacy, capital requirements, and the legal framework that underpins the entire structure.

Zero Corporate Tax on Foreign-Sourced Income

Under the International Business Companies Act 2016, a Seychelles IBC that derives income exclusively from outside the country pays zero corporate tax on those earnings. This is the foundational principle behind the Seychelles zero tax on foreign income framework, and it has direct financial consequences for how an offshore company retains and deploys its profits.

How the Exemption Is Structured

The IBC regime legally separates domestic and foreign income. Profits generated from activities conducted entirely outside Seychelles are not subject to any corporate income tax at the entity level, meaning your company retains the full margin on international transactions rather than surrendering a portion to the Seychelles Revenue Commission.

What This Means for Cross-Border Operations

For a trading, consulting, or holding entity operating across multiple foreign markets, the absence of corporate tax on foreign-sourced income can materially alter net returns compared to jurisdictions where such income is taxed at standard rates. The exemption applies provided the IBC does not conduct business with Seychelles residents or hold immovable property locally, which are the primary conditions that would bring the entity within the scope of domestic taxation.

Foreign-sourced profits earned through your Seychelles IBC are retained in full at the corporate level, with no tax liability owed to the Seychelles Revenue Commission.

No Capital Gains or Inheritance Tax

Under the International Business Companies Act 2016, an IBC registered in Seychelles is not subject to capital gains tax on any profits derived from the disposal of assets. No capital gains tax Seychelles IBC structures face means that when your company sells shares, real estate held abroad, or other investments, the full proceeds remain within the entity without a portion being clawed back by the tax authority.

For investors who regularly restructure holdings or exit positions, this has direct financial consequences. A company domiciled in a jurisdiction that levies capital gains at 20% or higher would erode returns on every disposal event. Here, that erosion does not occur.

Inheritance tax is equally absent. Assets held through a Seychelles IBC do not attract succession duties when ownership transfers between generations or between parties, which makes the structure suitable for long-term wealth planning across family groups.

The exemptions apply specifically to income and gains sourced outside the jurisdiction. A few reasons this framework works in your favour:

- No tax event is triggered on the sale of foreign shareholdings

- Cross-border asset transfers within group structures avoid locally imposed exit charges

- Succession of ownership does not require advance tax provisioning

- Investment returns accumulate without annual capital gains assessment

Seychelles IBC Formation

Register your International Business Company in Seychelles and benefit from the jurisdiction's capital gains and inheritance tax exemptions.

Fast and Simple IBC Registration Process

Seychelles IBC fast registration advantages stem directly from how the regulatory framework is structured for international business companies. Under the International Business Companies Act 2016, a new IBC can typically be incorporated within 24 to 48 hours of submitting the required documentation through a licensed registered agent. For a foreign entrepreneur who needs an operational entity quickly, that timeline removes weeks of waiting that other jurisdictions routinely impose.

The registered agent requirement is not a bureaucratic obstacle. Licensed agents, regulated by the Financial Services Authority (FSA), handle the filing on your behalf, which means you are not required to be physically present at any point during the incorporation process. Your company can be formed remotely, with documents executed and submitted electronically.

| Parameter | Detail |

|---|---|

| Typical Incorporation Time | 24 to 48 hours |

| Physical Presence Required | No |

| Governing Legislation | International Business Companies Act 2016 |

| Regulatory Body | Financial Services Authority (FSA) |

| Filing Agent Requirement | Licensed registered agent mandatory |

The documentation requirements are limited in scope. A standard IBC formation generally requires the Memorandum and Articles of Association, identification documents for directors and shareholders, and proof of address. There are no mandatory government audits or pre-registration approvals from foreign investment authorities, which eliminates procedural delays common in onshore jurisdictions. The result is that your business structure is legally constituted and ready to operate within a very short window after initiating the process.

High Level of Shareholder and Director Privacy

Under the International Business Companies Act 2016, IBCs registered in Seychelles are not required to file shareholder or director information on any publicly accessible register. This is one of the most significant Seychelles shareholder privacy benefits for foreign owners: your name, ownership percentage, and role within the company are not visible to third parties through routine registry searches.

The Financial Services Authority (FSA) is the supervisory body for IBCs, but the disclosure requirements it enforces apply internally, not publicly. Registered agents hold the beneficial ownership and officer records, which means that corporate information stays within a defined, confidential channel rather than appearing in open databases.

Statutory registers — including the register of members and directors — are maintained at the registered agent's office, not at the FSA. Access to those records requires either a court order or the company's own authorization.

Keep these points in mind to maintain your privacy protections:

- Appoint a licensed registered agent based in Seychelles; they are legally responsible for maintaining your confidential records.

- Ensure your beneficial ownership information is accurately filed with your registered agent, as required under anti-money laundering obligations.

- Understand that privacy is procedural, not absolute; a court order can compel disclosure.

- Do not confuse confidentiality with anonymity; Seychelles IBCs still comply with FATF standards.

Despite its strong privacy framework, Seychelles shares beneficial ownership information with foreign authorities through bilateral exchange mechanisms, meaning the privacy protections are structural, not a shield from legitimate legal processes.

No Minimum Share Capital Requirement

Seychelles imposes no minimum share capital requirement on International Business Companies registered under the International Business Companies Act 2016. Your company can be incorporated with a single share of any denomination, in any currency. That structural flexibility means capital is not a barrier to registration, which directly reduces the financial commitment required to establish a legal entity.

What the Law Actually Permits

Under the IBC Act 2016, the default authorised share capital is USD 100,000, but this figure carries no obligation to deposit or pay up any portion of it. Shares can be issued as par value or no-par-value, giving you control over how the capital structure is presented to counterparties, banks, or partners.

Authorised capital and paid-up capital are treated as entirely separate matters. This means you can maintain a nominal issued capital while still operating a fully functional entity with accounts, contracts, and international commercial relationships.

Why This Matters for Foreign Business Owners

For foreign founders structuring a holding company, a trading entity, or an SPV, not being required to lock up capital at incorporation preserves liquidity from day one. Funds that would otherwise sit idle in a statutory capital account remain available for operations, investment, or deployment elsewhere.

This feature is particularly relevant when the IBC is used as an intermediate holding structure, where the economic substance of the business resides elsewhere and tying up capital at the entity level would serve no commercial purpose.

Structure Your Seychelles IBC Capital Framework

Speak with our corporate specialists to understand how Seychelles share capital rules apply to your specific entity structure and incorporation goals.

Single Shareholder and Director Permitted

Under the Seychelles International Business Companies Act 2010, as amended, an IBC can be formed and operated by a single individual who holds both the shareholder and director roles simultaneously. No second person is required at any stage, whether at incorporation or during ongoing operations.

The practical significance of this for a foreign business owner is direct:

- A sole founder can establish and control the entity without appointing nominee directors or co-shareholders to satisfy a minimum headcount. This eliminates a layer of structural complexity that many jurisdictions impose.

- Because one person holds both roles, decision-making authority is consolidated. Resolutions can be passed by a single signatory, which reduces administrative overhead for small or single-owner businesses operating across time zones.

- There is no statutory requirement to hold formal board meetings or general meetings with multiple attendees. A one-person company structure can fulfill its compliance obligations without coordinating schedules among several parties.

- The Seychelles single shareholder company advantage is especially relevant for consultants, holding structures, and special-purpose vehicles where concentrated ownership is a design requirement, not a limitation.

The register of directors and shareholders is maintained with the registered agent but is not publicly accessible, so the single-owner structure does not create additional disclosure exposure under the current regulatory framework.

Stable Legal Framework Under Companies Act 2012

The Seychelles Companies Act 2012 stable framework governs International Business Companies (IBCs) under a codified, modern statute that replaced the earlier IBC Act of 1994. Enacted by the National Assembly and administered by the Seychelles Financial Services Authority (FSA), the Act consolidates corporate governance rules into a single, predictable legislative instrument.

Statutory predictability matters for foreign business owners because it reduces legal risk. When the rules governing your company's formation, share structure, and director obligations are written into primary legislation rather than governed by administrative discretion, you operate with enforceable certainty. The FSA's regulatory oversight further ensures that licensed registered agents operate within defined compliance boundaries, adding procedural consistency to legal certainty.

The Act also aligns with international standards recognised by bodies such as the Financial Action Task Force (FATF), which means your entity is formed under a framework that has been assessed against global compliance benchmarks. For businesses that need to open bank accounts, enter contracts, or transact across borders, this international recognition carries practical weight.

Under Section 4 of the Companies Act 2012, an IBC is defined as a company incorporated under this Act that is authorised to carry on all lawful business, subject to the restrictions set out in section 5 — providing a statutory foundation that delineates permitted activities with legislative clarity rather than regulatory interpretation.

Strong Asset Protection Through Flexible Structures

A Seychelles asset protection offshore structure derives much of its strength from the International Business Companies Act 2024 (which consolidated and updated the earlier IBC framework), which permits considerable structural flexibility in how ownership and control are arranged.

Seychelles IBCs can issue multiple classes of shares with differentiated voting rights, dividend entitlements, and redemption terms. This means you can separate economic interest from control, a feature particularly useful for estate planning, joint ventures, or ring-fencing specific asset pools within a single entity.

The law also permits nominee arrangements, layered holding structures, and the appointment of a protector in trust-linked setups. Each layer introduces a distinct legal boundary between your personal assets and operational or liability-bearing entities.

- Shares can be held in certificated or uncertificated form, reducing exposure through bearer-style structural design

- No requirement to publicly disclose beneficial ownership on the company registry, limiting third-party visibility into the ownership chain

- Assets held by an IBC are legally distinct from the shareholder's personal estate under Seychelles company law

For businesses structured as Seychelles offshore company wealth protection vehicles, this legal separation is the operative mechanism, not a contractual arrangement but a statutory one.

Asset protection structures must be established before a claim or liability arises; courts may disregard transfers made with the intent to defraud existing creditors.

No Foreign Exchange Controls or Restrictions

Seychelles IBCs are not subject to foreign exchange controls, which is a direct consequence of the country's open capital account policy. For a business operating across multiple currencies or jurisdictions, this means funds can move in and out without regulatory pre-approval, conversion mandates, or reporting thresholds tied to currency flows.

Under the International Business Companies Act 2016, an IBC may hold accounts in any currency and conduct transactions denominated in foreign currencies without restriction. There is no requirement to repatriate earnings or convert foreign currency receipts into the Seychellois Rupee. Practically, this means your firm can receive client payments in USD, EUR, GBP, or any other currency and distribute those funds to shareholders or settle invoices abroad without triggering a compliance process specific to the currency itself.

This freedom is particularly relevant for structures used in international trade, investment holding, or digital service businesses where payment flows cross multiple jurisdictions in short timeframes. Delays caused by currency controls can disrupt settlement cycles and increase transaction costs. The absence of those controls removes an entire layer of operational friction.

- No mandatory conversion of foreign currency receipts

- No central bank approval required for cross-border transfers from an IBC

- No caps on the value of outbound or inbound currency transactions at the entity level

- Accounts may be denominated and maintained in any major international currency

This policy applies to IBCs engaged exclusively in international business, which is the standard classification for most offshore structures formed in this jurisdiction.

Access to a Reputable Offshore Financial Centre

Seychelles carries genuine standing as a reputable offshore financial centre, which translates into practical credibility for businesses incorporated there. The jurisdiction is regulated by the Financial Services Authority (FSA), established under the Financial Services Authority Act 2013, which oversees International Business Companies, securities, insurance, and other non-bank financial services. That regulatory oversight gives your entity a verifiable compliance framework to point to, rather than an absence of governance.

Membership in international standard-setting bodies reinforces that standing. The FSA cooperates with the Eastern and Southern Africa Anti-Money Laundering Group (ESAAMLG), meaning AML and CFT standards applied to Seychelles-registered firms align with FATF-equivalent requirements. For a foreign business owner, this matters when opening corporate bank accounts or satisfying counterparty due diligence, since correspondent banks and institutional partners routinely assess whether the incorporating jurisdiction maintains credible oversight.

The practical benefits of this standing include:

- Access to banking relationships in jurisdictions that screen for FATF-compliant incorporation origins

- Reduced counterparty friction when engaging European, Asian, or Gulf-based institutional partners

- A compliance baseline that satisfies many standard KYC and AML documentation requests without requiring additional legal opinions

Seychelles was removed from the EU list of non-cooperative jurisdictions in 2022 after implementing agreed tax transparency reforms, including economic substance requirements under the Economic Substance Act. Removal from that list has direct consequences for European business relationships, as EU-regulated entities face restrictions when dealing with firms incorporated in listed territories. Your company therefore operates from a jurisdiction whose regulatory posture has been validated through an external review process, not simply asserted by domestic authorities alone.

Why Seychelles Stands Out Among Offshore Jurisdictions

Compared to other offshore centres competing for the same incorporation business, the Seychelles IBC structure holds a measurable position across several parameters that matter to foreign investors: formation speed, tax treatment, privacy protections, and structural flexibility. The jurisdictions most directly comparable are the British Virgin Islands, Mauritius, and Panama, each targeting a similar profile of international business owner and offering broadly analogous IBC-type vehicles. What the comparison reveals is not that any single jurisdiction dominates across every parameter, but that Seychelles advantages over other offshore jurisdictions tend to cluster around low operational friction and cost-efficiency, particularly for smaller international structures that do not require treaty access.

Mauritius, for instance, offers a tax treaty network that Seychelles cannot match, but that benefit carries a compliance burden, including substance requirements and audit obligations, that many straightforward holding or trading structures do not need. The BVI remains a recognised name, though its annual fees and regulatory costs have risen considerably. Panama offers strong privacy protections but operates under a different legal tradition, which affects how structures are interpreted across common law jurisdictions. Seychelles operates under a Companies Act 2012 framework that is codified, predictable, and administered by the Financial Services Authority.

| Parameter | Seychelles | British Virgin Islands | Mauritius | Panama |

|---|---|---|---|---|

| Corporate Tax on Foreign Income | 0% | 0% | 0% (GBL) / 15% (domestic) | 0% (foreign-sourced) |

| Capital Gains Tax | None | None | None | None |

| Annual Government Fee | Low | Moderate to High | Moderate | Low to Moderate |

| Minimum Share Capital | None | None | None | None |

| Single Shareholder Permitted | Yes | Yes | Yes | Yes |

| Director Privacy | High | Moderate | Moderate | High |

| Tax Treaty Access | Limited | None | Extensive | Limited |

| Substance Requirements | Minimal | Minimal | Required for GBL | Minimal |

| Legal Framework | Common Law (Companies Act 2012) | Common Law (BCA 2004) | Common Law (Companies Act 2001) | Civil Law |

| Regulatory Body | FSA Seychelles | BVI FSC | FSC Mauritius | Superintendencia |

Compliance Services for Seychelles Companies

Maintain your Seychelles IBC in good standing with annual filings, registered agent obligations, and ongoing regulatory support.

Conclusion

The core case for the benefits of incorporating in Seychelles rests on a combination of structural efficiency and fiscal clarity that few offshore jurisdictions deliver as consistently. A company formed under the International Business Companies Act 2016 faces no tax on foreign-sourced income, no capital gains exposure, and no minimum capital threshold — conditions that reduce both the cost of formation and the ongoing compliance burden for foreign business owners.

Privacy provisions under the same Act, along with the single-director and single-shareholder structure, mean that smaller enterprises and solo operators are not forced into governance arrangements designed for larger organisations. The practical effect is a structure that can be maintained without excessive administrative overhead.

Whether this framework suits your business depends on where you generate revenue, how you hold assets, and what your home jurisdiction requires in terms of controlled foreign corporation rules or substance obligations. The Seychelles IBC benefits for businesses are most material when the entity operates internationally and maintains clear separation from local trading activity. A properly formed and maintained entity — one that accounts for your specific corporate structure and filing obligations — positions your business to use this framework as intended under Seychelles law. Getting that formation right from the outset determines how effectively those advantages hold over time.

Let Expanship Handle Your Seychelles Company Formation

Expanship manages the full incorporation process for International Business Companies registered under the Seychelles Companies Act 2012, including all filings with the Registrar of Companies at the Financial Services Authority (FSA). From structuring your entity to maintaining statutory compliance, the firm handles the administrative and regulatory requirements that foreign owners would otherwise need to coordinate across multiple service providers.

Engaging Expanship for your Seychelles company formation with Expanship means the following services are covered directly:

- Preparation and legalization of incorporation documents, including the Memorandum and Articles of Association

- Provision of a registered agent and registered office address, both mandatory under the Companies Act 2012

- Liaison with the FSA Registrar of Companies for filing and certificate issuance

- Post-incorporation compliance management, including annual renewal and statutory record upkeep

- Banking introduction assistance for corporate account opening with institutions active in the jurisdiction

- Director and shareholder nominee services where structural privacy is required

For foreign owners who are not resident in the Seychelles, these requirements cannot be self-managed without local representation. Expanship provides that representation directly, removing the need to source a registered agent, a compliance manager, and a banking contact separately.

Reach out to Expanship Seychelles to begin your IBC incorporation.

Frequently Asked Questions (FAQ)

The Companies Act 2012 does not require shareholder or director details to be filed on any public register. Beneficial ownership information is maintained by the licensed registered agent and disclosed only to the Financial Intelligence Unit or relevant authorities upon a lawful request, meaning ownership details are not accessible through routine public searches.

A Seychelles IBC pays zero corporate tax on income derived from activities conducted entirely outside the jurisdiction. This exemption applies as long as the entity does not trade locally or derive income sourced within Seychelles, in which case standard domestic tax rules would apply instead.

No minimum paid-up capital is required under the IBC framework. Shares may be issued at any par value or without par value, and the company does not need to deposit or demonstrate any capital amount prior to or following registration.

Incorporation is generally completed within one to two business days once all required documentation is submitted to the Registrar of Companies through a licensed registered agent. The timeline assumes no discrepancies in the submitted documents; additional due diligence requirements from the registered agent can extend this marginally.

Currently, Seychelles imposes no foreign exchange controls on IBCs, allowing unrestricted movement of funds across borders. Should the legislative environment change, existing companies would be subject to any new rules enacted, as no statutory grandfather protection is built into the current framework for this specific area.

Seychelles does not levy capital gains tax at all, and this applies to gains realised on the disposal of foreign assets held through an IBC. The absence of capital gains tax is a feature of the broader tax regime rather than a specific IBC concession, so it applies regardless of the asset class or the jurisdiction in which the underlying asset is located.

Seychelles has at various times appeared on and been removed from EU and FATF monitoring lists, and its status can change following periodic reviews. An IBC remains a validly incorporated entity regardless of listing status, but counterparties in certain jurisdictions may apply enhanced due diligence or impose restrictions on transactions involving Seychelles-registered entities, which is a practical consideration for banking and cross-border contracting.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.