Key Takeaways

- Seychelles offers nine distinct business entity types, ranging from the International Business Company (IBC) to the Sole Proprietorship, each governed by specific statutory parameters under the Companies Act and regulated by the Financial Services Authority (FSA).

- The IBC is the most commonly registered entity in Seychelles, primarily chosen by non-resident entrepreneurs for its tax-neutral treatment of foreign-sourced income under the jurisdiction's territorial tax system.

- Businesses requiring access to Seychelles' tax treaty network must register as a Special License Company (CSL), which operates under a licensed framework distinct from the standard IBC structure.

- Non-commercial and member-based organisations are directed toward the Company Limited by Guarantee, while investment vehicles seeking pass-through tax treatment are better served by the Limited Partnership (LP).

Introduction to Entity Types in Seychelles

Seychelles is an archipelago of 115 islands situated in the western Indian Ocean, northeast of Madagascar and east of mainland Africa. It is an independent republic and a member of the Commonwealth. Company registration falls under the jurisdiction of the Seychelles Financial Services Authority (FSA), the statutory body responsible for licensing and supervising non-bank financial services, including the incorporation and ongoing regulation of business entities.

The jurisdiction operates a territorial tax system, meaning foreign-sourced income is generally not subject to domestic taxation for qualifying structures.

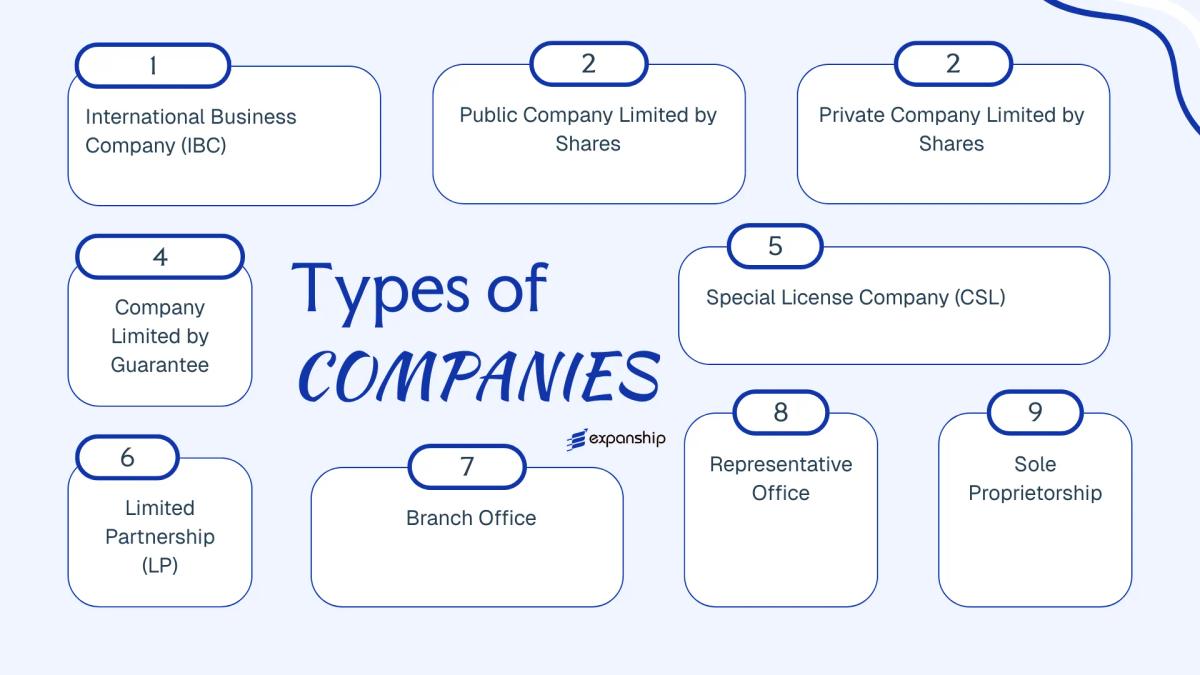

Several types of companies in Seychelles are available to both residents and non-residents: the International Business Company (IBC), the Public Company Limited by Shares, the Private Company Limited by Shares, the Company Limited by Guarantee, the Special License Company (CSL), the Limited Partnership (LP), the Branch Office, the Representative Office, and the Sole Proprietorship.

Each structure carries distinct legal characteristics, ownership rules, and regulatory obligations. This article examines each Seychelles business entity type in turn, covering formation requirements, governance, liability, and applicable use cases.

An Overview of Business Structures in Seychelles

Seychelles business structures overview spans several distinct entity types, each governed primarily by the Companies Act 1972 (as amended) and supplementary legislation such as the International Business Companies Act 1994 and the Limited Partnerships Act 2003. Responsibility for registering and supervising these entities sits with the Registrar of Companies, operating under the Financial Services Authority (FSA). Each structure carries different rules on liability, taxation, membership, and permitted activities.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| IBC | Private Company | Limited | Exempt | Not permitted | 1 shareholder | FSA / Registrar | IBC Act 1994 |

| Public Company | Public Company | Limited | Taxed | Permitted | 2 shareholders | Registrar of Companies | Companies Act 1972 |

| Private Company | Private Company | Limited | Taxed | Permitted | 1 shareholder | Registrar of Companies | Companies Act 1972 |

| Company Limited by Guarantee | Non-profit entity | Limited | Taxed | Restricted | 1 member | Registrar of Companies | Companies Act 1972 |

| CSL (Special License) | Private Company | Limited | Reduced rate (1.5%) | Permitted | 1 shareholder | FSA | CSL Act 2003 |

| Limited Partnership | Partnership | General / Limited | Taxed | Permitted | 2 partners | FSA / Registrar | Limited Partnerships Act 2003 |

| Branch Office | Foreign entity extension | Unlimited (parent) | Taxed | Permitted | N/A | Registrar of Companies | Companies Act 1972 |

| Representative Office | Foreign entity extension | Unlimited (parent) | Exempt | Not permitted | N/A | Registrar of Companies | Companies Act 1972 |

| Sole Proprietorship | Unincorporated | Unlimited | Taxed | Permitted | 1 owner | Registrar of Companies | Business Tax Act |

Each of these structures is examined in full in the sections below.

International Business Company (IBC)

The International Business Company is the most widely registered structure for Seychelles IBC registration requirements, governed by the International Business Companies Act 2016, which repealed and replaced the original 1994 legislation. The entity carries separate legal personality distinct from its shareholders, and members' liability is limited to their unpaid share capital.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Company limited by shares (or guarantee, or both) | Can also be incorporated with unlimited liability |

| Members | Shareholders and Directors | Minimum 1 shareholder, 1 director; no maximum; both roles can be held by the same person |

| Local Presence | Registered Agent required | Physical registered office address in Seychelles mandatory; no requirement for local directors or employees |

| Share Capital | No minimum capital; any currency permitted | Bearer shares are prohibited under the 2016 Act |

| Privacy | Register of directors and shareholders not publicly accessible | Held by the Registered Agent; disclosed to the Registrar but not open to public inspection |

Focus Points

- Taxation: IBCs are exempt from Seychelles income tax, withholding tax, capital gains tax, and stamp duty on income sourced outside the country; no VAT obligation applies to offshore activities.

- Economic Substance: IBCs conducting relevant activities (banking, insurance, fund management, etc.) must satisfy substance requirements under the Economic Substance Act 2021.

- Annual Compliance: Annual renewal fee payable to the Registrar of Companies; no requirement to file audited accounts unless the entity opts into a regulated regime.

- Treaty Access: Seychelles has a limited tax treaty network; IBCs generally do not qualify as tax residents and therefore cannot access treaty benefits.

- Restrictions: An IBC may not conduct business with Seychelles residents, own immovable property locally, or carry on banking, insurance, or trust business without a specific licence.

Closing

The Seychelles IBC offshore company structure is commonly used for international holding, IP ownership, trading, and investment activity. The primary advantage is the low incorporation cost combined with full tax exemption on foreign-sourced income; the principal limitation is that expanded substance requirements now apply to certain financial activities, which increases the operational burden for those sectors.

This entity suits non-resident entrepreneurs and investors seeking a cost-efficient vehicle for cross-border holding or trading activities that generate no income within Seychelles.

Company Incorporation in Seychelles

Register a Seychelles IBC with full compliance support, registered agent services, and ongoing maintenance.

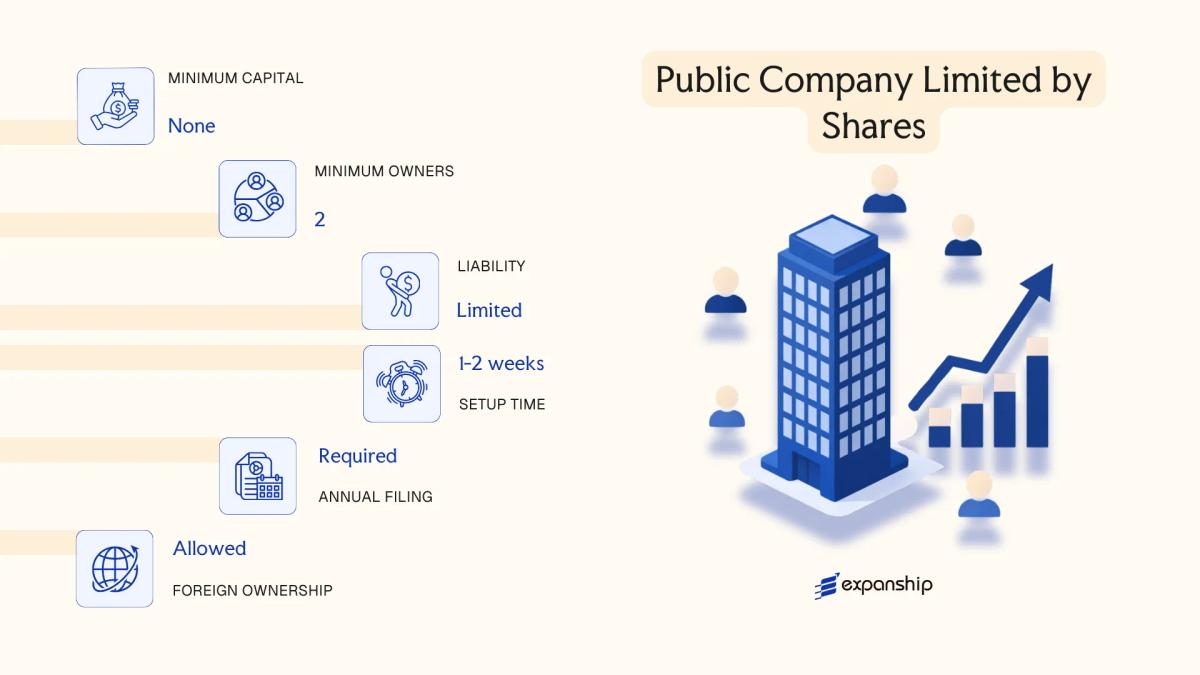

Public Company Limited by Shares

A Seychelles public company limited by shares is governed by the Companies Act, 2021, which consolidates and modernises the earlier legislative framework. Like its private counterpart, it carries separate legal personality and limits shareholder liability to the amount unpaid on their shares, but its defining distinction is the ability to offer shares to the general public and, subject to regulatory approval, seek a listing on a recognised exchange.

Listing on the Seychelles Stock Exchange (MERJ Exchange) requires compliance with MERJ's listing rules and oversight from the Financial Services Authority (FSA), which supervises non-bank financial services in the jurisdiction.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Public company limited by shares | Carries separate legal personality; shareholders not liable beyond unpaid share capital |

| Members | Shareholders: minimum 2, no maximum | Directors: minimum 3; a company secretary is required |

| Local Presence | Registered agent and registered office required | Must maintain a physical registered address in Seychelles |

| Share Capital | No statutory minimum; shares denominated in any currency | Must produce a prospectus when offering shares to the public |

| Privacy | Directors and shareholders appear on public record | Less privacy than private structures |

| Transferability | Shares freely transferable | No restriction on share transfer, unlike a private company |

Focus Points

- Taxation: Subject to the Seychelles Business Tax at 15% on taxable income; VAT applies if turnover exceeds the registration threshold; no withholding tax on dividends under domestic law; stamp duty may apply to certain instruments.

- Economic Substance: If conducting relevant activities, the entity must meet substance requirements under the Economic Substance Act, 2021.

- Annual Compliance: Annual return and financial statements must be filed with the Registrar of Companies; listed entities face additional continuous disclosure obligations under MERJ rules.

- Conversion: A public company may be re-registered as a private company under the Companies Act, 2021, subject to shareholder approval and Registrar consent.

- Restrictions: Cannot commence business until a trading certificate is issued by the Registrar; public fundraising is subject to FSA prospectus requirements.

Closing

A public company limited by shares suits businesses seeking access to public capital markets or planning a stock exchange listing, though the associated compliance burden, public disclosure requirements, and multi-member governance structure make it a structurally demanding option compared to most other entity types available in Seychelles.

This structure is most appropriate for established businesses pursuing a public listing on MERJ Exchange or those requiring broad-based equity fundraising from the general public.

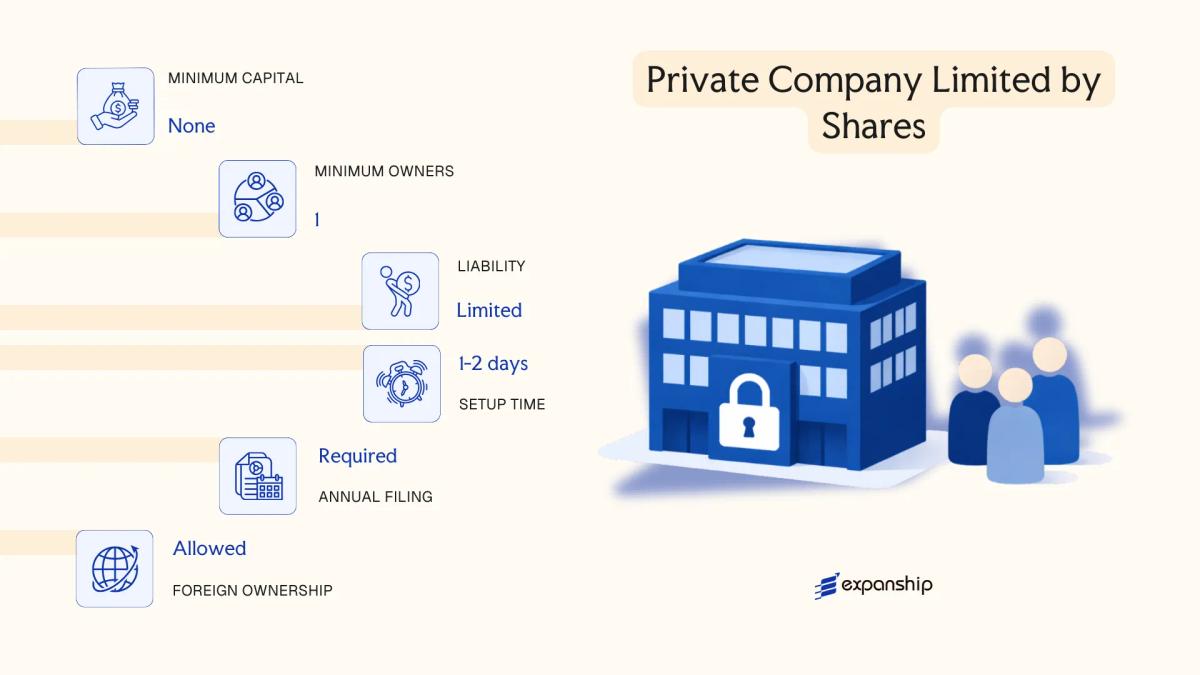

Private Company Limited by Shares

A Seychelles private company limited by shares is governed by the Companies Act, 1972, as amended, and falls under the regulatory oversight of the Registrar of Companies within the Financial Services Authority (FSA). It constitutes a separate legal entity, meaning the company holds rights and obligations distinct from those of its shareholders.

Liability of each shareholder is capped at the amount unpaid on their shares. This structure suits businesses seeking a domestic legal presence rather than an offshore vehicle, making it appropriate for locally operating enterprises or regionally anchored holding arrangements.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private Company Limited by Shares | Separate legal personality; governed by Companies Act, 1972 |

| Members | Shareholders: min. 1, max. 50 | Transfer of shares is restricted by the articles |

| Management | Directors: min. 1 | No residency requirement for directors |

| Local Presence | Registered office in Seychelles required | Must maintain a physical registered address locally |

| Share Capital | No statutory minimum; denominated in any currency | Shares may or may not carry par value |

| Privacy | Shareholder and director details on public record | Less privacy than an IBC structure |

Focus Points

- Taxation: Subject to Seychelles Business Tax on locally sourced income; VAT applies if annual turnover exceeds the registration threshold; no withholding tax on dividends to non-residents under general rules.

- Economic Substance: Not subject to the same economic substance obligations as CSL entities, but locally active businesses must demonstrate genuine operations.

- Annual Compliance: Annual return and audited financial statements must be filed with the Registrar; failure attracts penalties under the Companies Act.

- Restrictions: Cannot offer shares to the public or list on a stock exchange; shareholder count capped at 50.

- Conversion: May be converted to a public company by altering its articles and meeting the requirements set out under the Companies Act.

Closing

This structure suits entrepreneurs and investors establishing a trading, services, or holding business with a genuine local or regional presence. The primary advantage is full legal recognition under domestic law with straightforward governance; the principal limitation is the public disclosure of ownership and directorship information.

Resident or regionally active businesses requiring a domestically recognised legal entity with limited liability and a conventional corporate structure.

Company Limited by Guarantee

A Seychelles company limited by guarantee is incorporated under the Companies Act 1972, which remains the principal legislation governing this structure. Unlike share-based companies, members commit to contributing a fixed sum toward the entity's liabilities upon winding up, rather than subscribing to shares. This gives the structure a distinct legal character: it carries separate legal personality and limited liability, yet functions without share capital.

Registered with the Registrar of Companies under the Financial Services Authority (FSA), this entity type is most commonly associated with non-profit purposes, though the Act does not restrict it exclusively to such activities.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Company Limited by Guarantee (CLG) | Governed by the Companies Act 1972 |

| Members | Minimum 1; no statutory maximum | Referred to as members, not shareholders |

| Governance | Minimum 1 director | Directors manage operations; members provide guarantee |

| Local Presence | Registered office and registered agent required | Must maintain a physical address in Seychelles |

| Share Capital | None | Guarantee amount defined in the Memorandum |

| Privacy | Directors and members on public record | Limited privacy compared to an IBC |

Focus Points

- Taxation: No corporate income tax on foreign-sourced income; domestic income may be subject to standard corporate tax; VAT and withholding tax obligations depend on activity type.

- Economic Substance: CLGs engaged in relevant activities must satisfy substance requirements under the Economic Substance Act 2021.

- Annual Compliance: Annual return filing required with the FSA; financial statements may be required depending on activity.

- Restrictions: Cannot distribute profits to members; any surplus must be applied toward the entity's stated objectives.

- Treaty Access: Not typically structured to access double tax treaties, which are limited in scope for Seychelles entities generally.

Closing Paragraph

Guarantee company registration in Seychelles suits organisations pursuing charitable, civic, or professional association purposes, where the absence of profit distribution is a structural requirement rather than a limitation. The primary advantage is the liability protection afforded to members; the main drawback is the restriction on profit distribution, which limits its utility for commercial ventures.

This structure is best suited for non-profit organisations, professional associations, charities, and regulatory or membership bodies that require legal personality without share capital.

Special License Company (CSL)

The Seychelles Special License Company, commonly referred to as a CSL, is governed by the Companies (Special Licenses) Act, 2003. It occupies a hybrid position in Seychelles corporate law, combining the domestic company framework with an international business orientation, making it structurally distinct from both standard onshore companies and IBCs.

As a separate legal entity with limited liability, the CSL holds its own assets, enters contracts, and incurs obligations independently of its shareholders. Its hybrid character means it is treated as a resident company for tax treaty purposes while retaining access to certain offshore operating flexibilities.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Company limited by shares | Incorporated under the Companies (Special Licenses) Act, 2003 |

| Members | Shareholders and Directors; minimum 1 shareholder, 1 director; no maximum | Directors may be corporate; no mandatory residency requirement for directors |

| Local Presence | Registered agent and registered office required | Must also maintain a physical presence or substance in Seychelles |

| Capital | No statutory minimum share capital; denominated in any currency | Shares may be issued at par or no par value |

| Tax Rate | Corporate tax levied at 1.5% on net income | The defining feature distinguishing CSL from an IBC |

| Privacy | Beneficial ownership disclosed to the FSA; not on public record | Seychelles Financial Services Authority holds regulatory oversight |

Focus Points

- Taxation: Subject to a concessionary corporate tax rate of 1.5% on net profits; exempt from withholding tax on dividends paid to non-resident shareholders; VAT and stamp duty obligations generally do not apply to qualifying CSL activities.

- Economic Substance: CSLs are expected to demonstrate genuine substance in Seychelles, including management and control, which influences treaty eligibility.

- Annual Compliance: Required to file audited financial statements and an annual return with the Financial Services Authority (FSA).

- Treaty Access: Because the CSL is treated as a tax-resident entity, it can access Seychelles' double taxation agreements, which an IBC cannot.

- Restrictions: CSLs cannot conduct business with Seychelles residents and are subject to FSA licensing conditions that restrict operational scope.

Closing

The CSL suits holding structures, international trading operations, and IP ownership arrangements where treaty access is a material consideration. Its 1.5% tax rate and treaty eligibility give it a clear functional advantage over an IBC, though the substance requirements and FSA oversight add compliance costs that may not suit lean or dormant structures.

Businesses requiring access to Seychelles' double taxation treaty network while maintaining a tax-efficient, internationally oriented corporate structure.

Limited Partnership (LP)

Seychelles limited partnership registration is governed by the Limited Partnerships Act, 2003. An LP formed under this legislation carries a separate legal personality, distinguishing it from general partnerships in most other jurisdictions. The structure combines limited liability for passive investors with the operational flexibility typically associated with partnership arrangements.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Separate legal entity | Distinct from partners' personal assets |

| Members | Min. 1 general partner + 1 limited partner; no maximum | General partners bear unlimited liability; limited partners' liability is capped at their contributed capital |

| Local Presence | Registered agent required | Physical office not mandatory |

| Capital | No statutory minimum; contributions may be cash or in-kind | Denomination is flexible |

| Privacy | Partner details not on public register | Maintained in internal records held by the registered agent |

Focus Points

- Taxation: LPs are generally treated as tax-transparent; no corporate income tax, withholding tax, VAT, or capital gains tax applies at the entity level, with tax obligations falling to partners in their home jurisdictions.

- Economic Substance: LPs conducting relevant activities may be subject to economic substance obligations under the Economic Substance Act, 2021.

- Annual Compliance: Annual renewal fees apply; no audited financial statements are typically required for non-regulated LPs.

- Treaty Access: LPs generally do not benefit from double tax treaties as stand-alone entities.

- Restrictions: Limited partners must not participate in management; doing so risks losing limited liability protection.

Closing

An LP suits fund structures, joint ventures, and asset-holding arrangements where separation between active management and passive investment is required. The tax-transparent treatment is a clear structural advantage, though unlimited liability for the general partner remains a material exposure that warrants careful consideration.

This structure is best suited for private equity funds, investment vehicles, and joint ventures where investors require liability protection without direct management involvement.

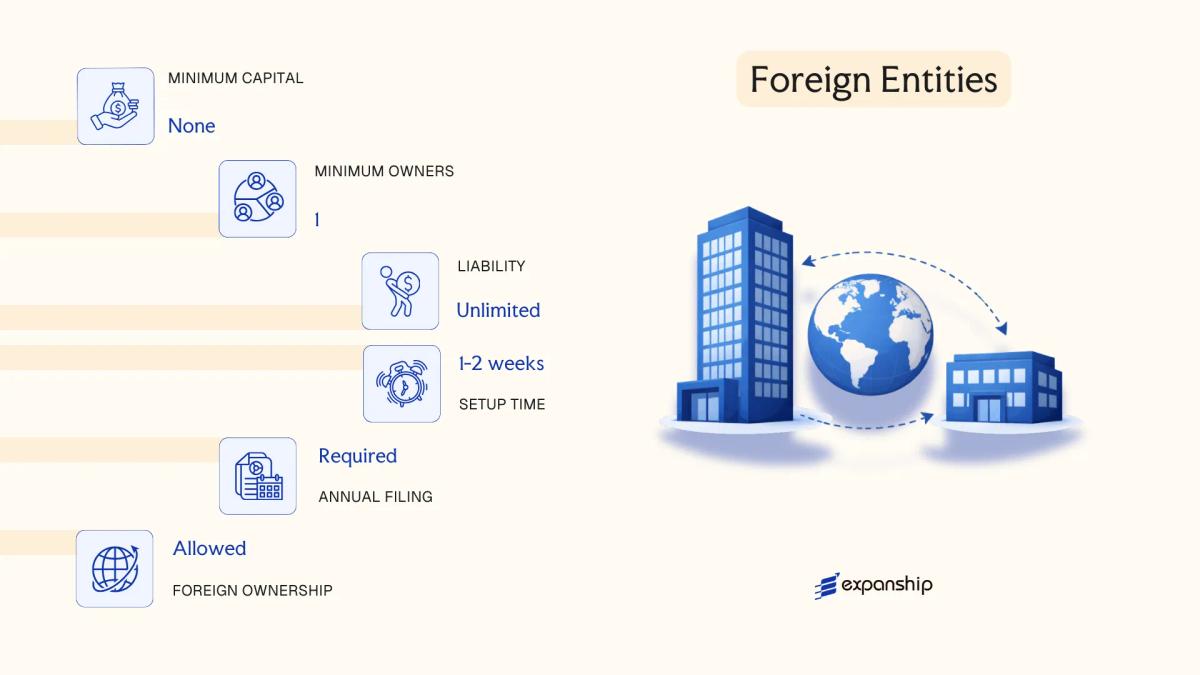

Foreign Entities in Seychelles [Branch Office, Representative Office]

Foreign companies seeking a local presence without incorporating a new entity have two recognised options: a branch office or a representative office. Seychelles branch office registration for a foreign company is governed by the Companies Act 1972, which requires the overseas firm to register with the Registrar of Companies under Part XI of that Act.

A branch is not a separate legal entity — it remains an extension of the parent company, which retains full liability for the branch's obligations. A representative office is more restricted in scope; it may not engage in revenue-generating activities and is typically used for market research or liaison functions only.

Key Characteristics

| Requirement | Branch Office | Representative Office |

|---|---|---|

| Legal Form | Extension of foreign parent; no separate legal personality | Extension of foreign parent; no separate legal personality |

| Registered Agent | Required | Required |

| Local Office | Registered address in Seychelles required | Registered address required |

| Capital | No minimum capital requirement | No minimum capital requirement |

| Commercial Activity | Permitted | Not permitted |

| Privacy | Parent company details filed publicly with Registrar | Parent company details filed publicly |

Focus Points

- Taxation: The branch is subject to Seychelles Business Tax on locally sourced income; no corporate tax on foreign-sourced income; VAT may apply to local transactions if turnover thresholds are met.

- Annual Compliance: Annual returns and financial statements of the parent must be filed with the Registrar of Companies.

- Economic Substance: Substance obligations may apply depending on the nature of activities conducted locally.

- Treaty Access: Access to Seychelles' tax treaties depends on the parent entity's residency status, not the branch registration itself.

- Restrictions: A representative office cannot invoice clients, execute sales contracts, or generate revenue in any form.

Closing

A branch office suits foreign businesses testing the local market or managing regional operations without the administrative overhead of a standalone subsidiary. The primary limitation is that the parent company bears unlimited liability for all branch obligations.

Best suited for established foreign corporations that require an operational foothold in Seychelles while keeping group structure consolidated under the parent entity.

Sole Proprietorship

Sole proprietorship registration Seychelles falls under the Business Registration Act 2013, administered by the Seychelles Financial Intelligence Unit (FIU) and processed through the Registrar of Businesses. Unlike incorporated entities, a sole proprietorship carries no separate legal personality — the business and the individual owner are treated as one, meaning personal assets are fully exposed to business liabilities.

Registration is straightforward for residents, though non-residents face restrictions on operating locally without additional licensing. The structure suits self-employed individuals running small-scale or service-based operations under a trading name.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated sole trader | No separate legal personality from owner |

| Members | Single proprietor | One individual only; no partners or shareholders |

| Local Presence | Registered business address required | Must maintain a local address on public record |

| Capital | No statutory minimum | No prescribed currency or paid-up capital requirement |

| Privacy | Proprietor's name on public register | Limited privacy; owner identity is publicly disclosed |

| Eligibility | Seychelles residents primarily | Non-residents may face restrictions under local licensing rules |

Focus Points

- Taxation: Subject to the Business Tax Act; standard business tax rates apply on net income; no corporate tax distinction from personal income; VAT registration required if turnover exceeds the statutory threshold.

- Annual Compliance: Annual renewal of business registration required with the Registrar of Businesses.

- Economic Substance: No economic substance obligations apply to sole proprietorships.

- Conversion: Can be converted into a Private Company Limited by Shares if the business scales.

- Restrictions: Cannot issue shares, raise equity, or limit personal liability.

Closing

A sole proprietorship suits resident individuals operating small local businesses or providing freelance services where administrative simplicity outweighs the need for liability protection. The absence of incorporation formalities reduces setup costs, but unlimited personal liability remains a significant structural constraint.

Seychelles-resident self-employed individuals running low-risk, small-scale service or trading operations who do not require liability separation or external investment.

How to Choose the Right Entity Type in Seychelles

Knowing how to choose a business structure in Seychelles requires more than comparing registration fees — the wrong choice produces concrete legal and financial consequences that are difficult to reverse.

Why Your Entity Choice Matters

- Registering an International Business Company and then trading with Seychelles residents puts you in breach of the Companies Act, which can result in administrative penalties or striking off by the Registrar of Companies.

- Selecting a tax-exempt entity such as an IBC forfeits access to any tax treaty benefits, since exemption from domestic tax typically disqualifies the entity from treaty protection under standard limitation-on-benefits clauses.

- Choosing a structure without substance capacity when the firm is subject to the Seychelles' economic substance requirements can trigger reporting failures and regulatory fines.

- Forming a standard share company when your objectives are estate planning or asset protection locks you into ongoing shareholder obligations — annual returns, share registers, and director filings — that a foundation would not require.

Key Factors to Consider

- Business Activity: Passive asset-holding, active trading, and regulated sectors each fall under different legislative frameworks, pointing toward the IBC, a private company, or a CSL respectively.

- Local vs. Offshore Operations: Transacting with Seychelles residents requires a locally licensed structure; purely offshore activity does not.

- Tax Objectives: If treaty access matters, a tax-exempt entity will not serve that purpose — a Special License Company or a standard resident company is more appropriate.

- Privacy Requirements: Director and shareholder details for IBCs are not held on a public register, whereas public companies face broader disclosure obligations under the Companies Act, 2021.

- Substance Capacity: If you cannot maintain staff, office space, or local decision-making, your entity type must either fall outside substance requirements or meet a lower threshold.

- Exit Strategy: Not all Seychelles structures permit redomiciliation or conversion — confirm these options before formation if future restructuring is likely.

Corporate Compliance Services in Seychelles

Maintain good standing with the Registrar of Companies through annual return filing, registered agent requirements, and ongoing regulatory obligations.

Conclusion

Seychelles company formation guide summary: each structure under the Companies Act 2972, as amended, serves a distinct commercial purpose. The IBC remains the most registered entity type, favoured by non-resident entrepreneurs for its tax-neutral holding and trading arrangements. Private companies limited by shares suit small to medium-sized businesses with local operational ties, while the CSL addresses those requiring treaty access under a licensed framework. Companies limited by guarantee fit non-commercial and member-based organisations. The LP offers pass-through structuring for investment vehicles, and branch registrations serve foreign firms testing operational presence without separate incorporation.

Regulatory oversight by the Financial Services Authority continues to evolve, with ongoing updates to beneficial ownership reporting and AML compliance obligations. Choosing the right structure involves aligning your operational profile with the entity's statutory parameters. Expanship's team works directly with this framework.

How Expanship Can Assist You

Expanship's Seychelles company incorporation services cover the full range of entities discussed in this guide — from IBCs registered under the International Business Companies Act 2016 to CSLs, Limited Partnerships, and locally oriented private companies. Our team works directly with the Seychelles Financial Services Authority (FSA) and the Registrar of Companies to keep your incorporation process accurate and on schedule.

Across each engagement, we handle the practical and regulatory steps so your business can move forward without administrative delays:

- Document preparation, notarization, and apostille legalization

- Registered agent and registered office provision in Seychelles

- Government filing and Registrar of Companies liaison

- Post-incorporation compliance management, including annual returns and UBO declarations

- Corporate bank account introduction support

Reach out to our team through Expanship Seychelles to discuss which structure fits your situation and what the next steps look like.

Frequently Asked Questions (FAQ)

The International Business Company (IBC), governed by the International Business Companies Act 2016, is the most frequently incorporated entity in the jurisdiction. Its appeal stems from a zero-tax position on foreign-sourced income and a straightforward incorporation process administered by the Registrar of Companies.

An IBC is restricted from trading with Seychelles residents or owning local real estate, whereas a Private Company Limited by Shares can conduct business domestically. The IBC carries minimal compliance obligations, with no audit or annual return requirement, while the Private Company faces more structured ongoing requirements under the Companies Act 1972. Tax treatment also differs: IBCs are exempt from local income tax on offshore earnings, while domestic companies are subject to the Business Tax Act.

The IBC provides the highest level of privacy. Shareholder and director details are not part of the public register, and nominee directors and shareholders are permitted under the Act. Beneficial ownership information is held by the registered agent but is not publicly accessible.

An IBC and a Private Company Limited by Shares can each be formed by one director and one shareholder. A Limited Partnership, however, requires at least two partners — a general partner and one limited partner. A Company Limited by Guarantee requires at least one member, but its structure is typically unsuited to single-person commercial ventures.

Foreign nationals can incorporate an IBC, a Special License Company (CSL), a Private Company Limited by Shares, a Company Limited by Guarantee, and register a Limited Partnership without residency requirements. A CSL requires a physical presence and a local registered office, and is subject to Financial Services Authority licensing. Branch offices of foreign companies are also available to non-residents under a formal registration process.

Conversion between certain entity types is permissible under Seychelles law. An IBC can be continued into or out of the jurisdiction under the International Business Companies Act 2016, and re-domiciliation of foreign companies is supported. Conversion between an IBC and a domestic company structure requires regulatory review and is not automatic.

The IBC carries the lightest compliance burden among all available structures. There is no requirement to file annual returns, audited accounts, or financial statements with the Registrar, provided the company maintains records at its registered agent's office. By contrast, a CSL must meet ongoing FSA reporting standards, and domestic companies are subject to annual filing requirements.

IBCs, Private Companies Limited by Shares, Public Companies, Companies Limited by Guarantee, and CSLs all have separate legal personality from their members. A Limited Partnership does not confer separate legal personality by default, meaning the general partner retains personal liability for partnership obligations. Sole proprietorships carry no legal separation between the owner and the business.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.