Key Takeaways

- The Sociedad Anónima, governed by Law 32 of 1927, remains Panama's most widely registered entity type and is particularly favored by holding companies, international traders, and non-resident entrepreneurs.

- Panama's territorial tax system means income generated outside the country is generally not subject to local income tax, a factor that directly influences entity selection for internationally operating businesses.

- All legal entities in Panama are incorporated and maintained through the Public Registry of Panama (Registro Público de Panamá), the sole government body with jurisdiction over company formation records.

- Ongoing FATF engagement and expanding automatic exchange of information agreements have progressively increased Panama's transparency requirements, making compliance a continuous obligation rather than a one-time registration exercise.

Introduction to Entity Types in Panama

Panama sits at the southern tip of Central America, bordering Colombia to the southeast and Costa Rica to the northwest, with coastlines on both the Pacific Ocean and the Caribbean Sea. It is an independent republic, and company formation falls under the jurisdiction of the Public Registry of Panama (Registro Público de Panamá), the government body responsible for incorporating and maintaining records of legal entities. The country operates a territorial tax system, meaning income generated outside Panama is generally not subject to local income tax.

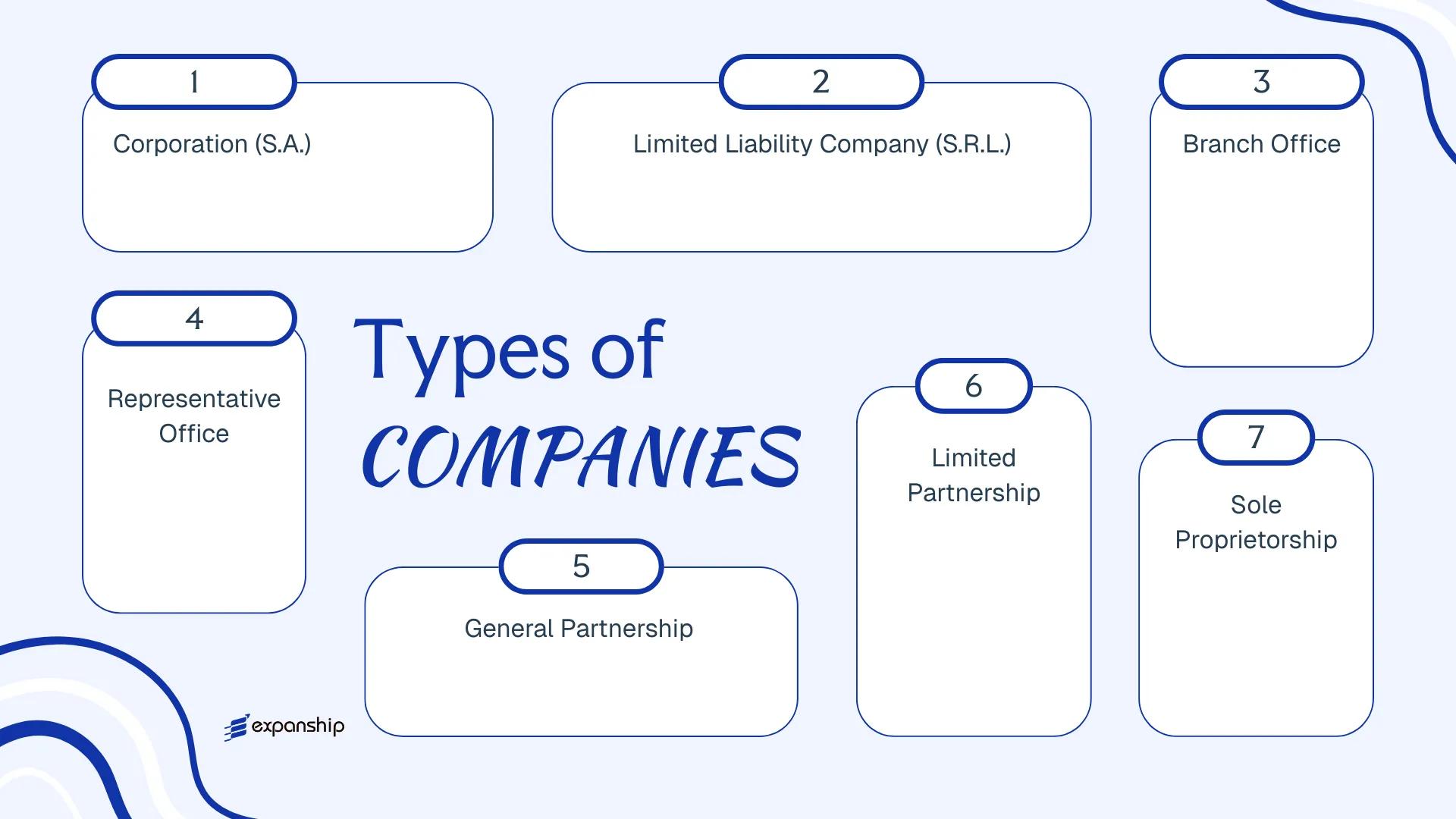

Several types of business entities in Panama are available to both residents and foreign nationals. These include the Sociedad Anónima (S.A.), the Sociedad de Responsabilidad Limitada (S.R.L.), the branch office, the representative office, the general partnership, the limited partnership, and the sole proprietorship.

Each structure carries distinct implications for liability, governance, and tax treatment. This article examines each Panamanian corporate structure in detail, covering registration requirements, ownership rules, and practical considerations to help you determine which legal form suits your business objectives.

An Overview of Business Structures in Panama

Panamanian company law offers several distinct entity types, each governed primarily by the Commercial Code (Código de Comercio) and, for corporations specifically, by Law 32 of 1927. Certain structures also fall under more recent legislation, including Law 4 of 2009, which regulates limited liability companies. Each form carries different implications for liability, taxation, and permitted commercial activity.

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Sociedad Anónima (S.A.) | Corporation | Limited to shareholding | Taxed on local income | Permitted | 3 directors, 1+ shareholder | Public Registry | Law 32 of 1927 |

| S.R.L. | LLC | Limited to capital contribution | Taxed on local income | Permitted | 2–20 members | Public Registry | Law 4 of 2009 |

| Branch Office | Foreign entity extension | Parent bears full liability | Taxed on local income | Permitted | N/A (parent company) | Public Registry | Commercial Code |

| Representative Office | Non-trading presence | Parent bears full liability | Generally exempt | Not permitted | N/A (parent company) | Public Registry | Commercial Code |

| General Partnership | Sociedad Colectiva | Unlimited, joint | Taxed on local income | Permitted | 2+ partners | Public Registry | Commercial Code |

| Limited Partnership | Sociedad en Comandita | Mixed (general/limited) | Taxed on local income | Permitted | 1 general, 1 limited | Public Registry | Commercial Code |

| Sole Proprietorship | Individual trader | Unlimited, personal | Taxed on local income | Permitted | 1 owner | Municipal authority | Commercial Code |

Each of these structures is examined in full in the sections below.

Sociedad Anónima (S.A.) — The Panamanian Corporation

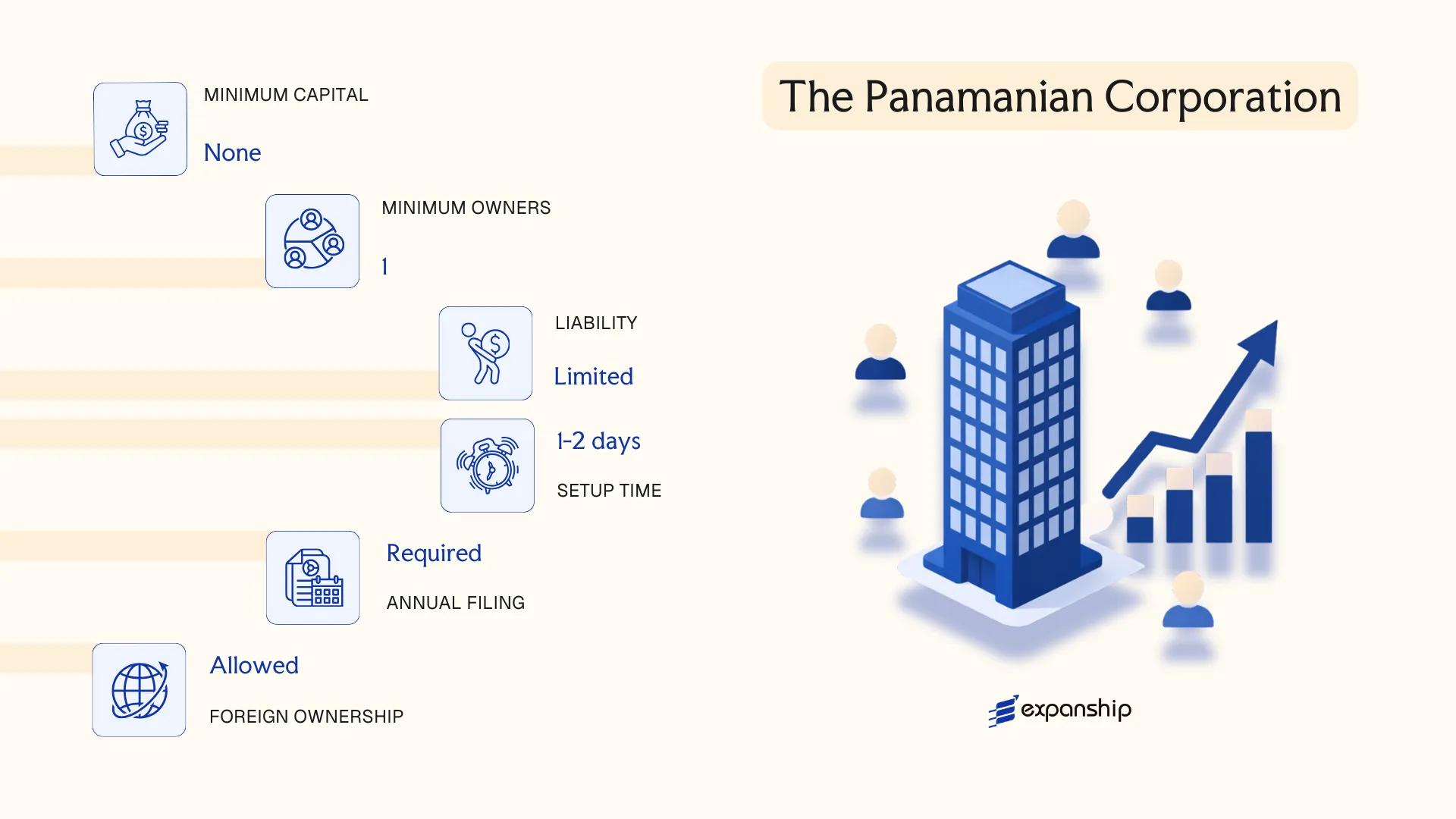

Governed by Law 32 of 1927, the Sociedad Anónima is the most widely used corporate structure for Panama Sociedad Anónima SA formation. The legislation has remained largely intact for nearly a century, which gives the structure a degree of legal predictability uncommon in many comparable jurisdictions.

The S.A. carries separate legal personality, meaning the entity holds rights and obligations independently of its shareholders. Liability is limited to each shareholder's capital contribution, and the structure accommodates both resident and non-resident ownership without restriction.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Corporation (Sociedad Anónima) | Separate legal personality from shareholders |

| Members | Shareholders (min. 1, no maximum); Directors (min. 3, no maximum) | Directors and shareholders may be the same individuals; corporate directors permitted |

| Local Presence | Registered Agent required (must be a Panamanian attorney or law firm) | No requirement for a local director or physical office |

| Capital | No minimum capital requirement; denominated in any currency; shares may have no par value | Capital structure is highly flexible |

| Privacy | Bearer shares abolished since 2015; registered shares now required; shareholder register held by registered agent | Beneficial ownership information submitted to a Centralised Depository |

Focus Points

- Taxation: Foreign-sourced income is exempt from corporate income tax under Panama's territorial tax system; locally sourced income is taxed at 25%. No VAT applies to offshore transactions; withholding tax on dividends paid from foreign-source income is 5%, and 10% on locally sourced income. Stamp duty applies to certain documents executed locally. Visit the Dirección General de Ingresos (DGI) for current rates.

- Economic Substance: No economic substance requirements for holding or offshore-operating S.A.s, provided income remains foreign-sourced.

- Annual Compliance: Annual franchise tax (currently USD 300) payable to the Public Registry; annual registered agent fee required to maintain good standing.

- Treaty Access: Panama has a limited but growing network of double taxation treaties; access depends on residency status and the nature of income.

- Conversion: An S.A. may be converted into an S.R.L. or merged with another entity through a formal notarial process registered with the Public Registry of Panama.

Closing

The S.A. suits holding structures, international trading companies, and IP ownership vehicles where foreign-source income is the primary revenue stream. Its flexibility in capital structure is a practical advantage, though the three-director minimum adds an administrative layer that smaller operations may find disproportionate.

Best suited for international investors and multinational groups seeking a flexible holding or trading vehicle with foreign-source income and no requirement for local operational presence.

Company Incorporation in Panama

Incorporate a Sociedad Anónima or other entity type in Panama with full registered agent support and Public Registry filing.

Limited Liability Company (S.R.L.) — Sociedad de Responsabilidad Limitada

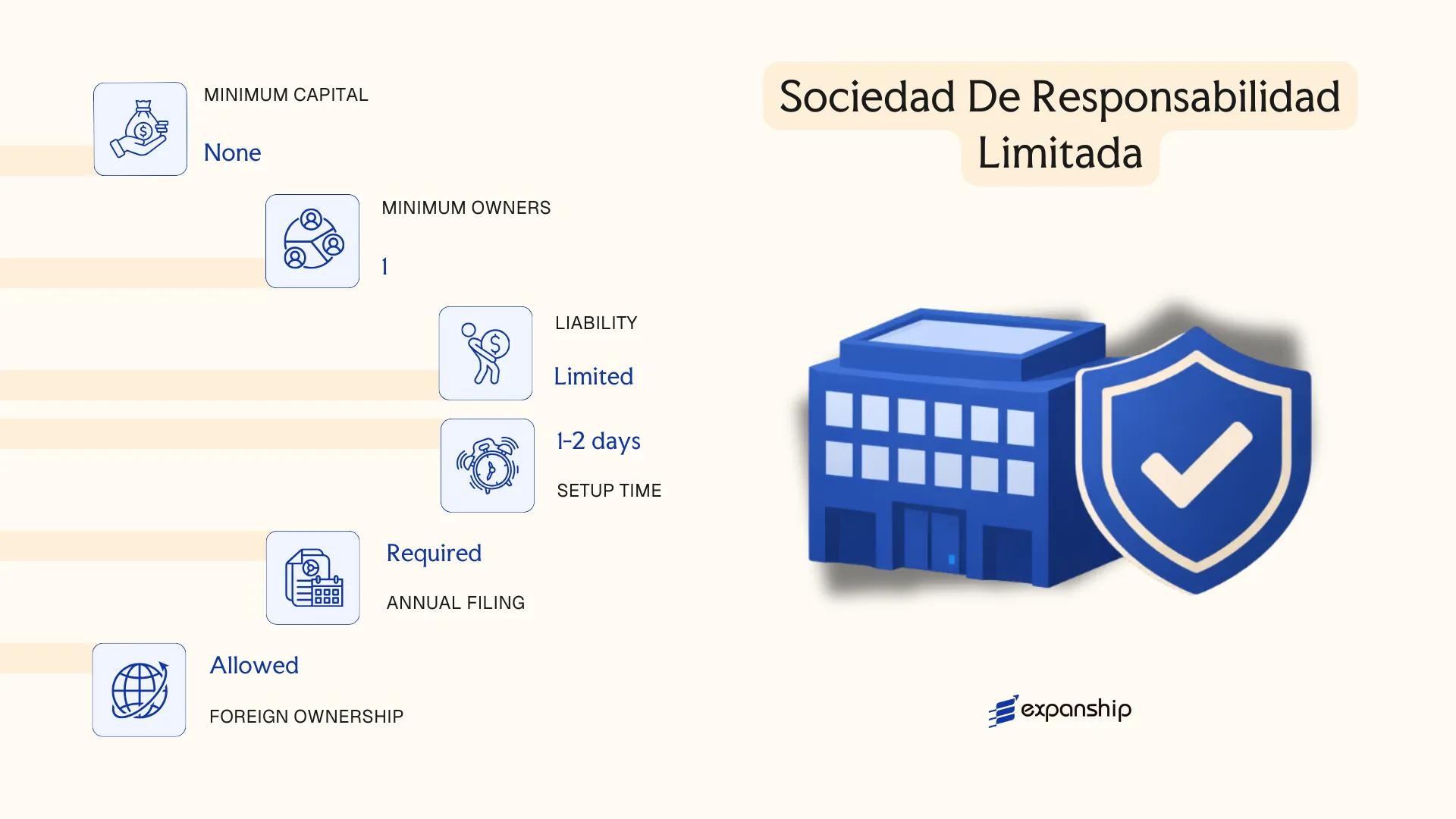

Governed by the Commercial Code of Panama and further shaped by Law 24 of 1966, the Sociedad de Responsabilidad Limitada is a hybrid structure that combines corporate limited liability with partnership-style governance. For Panama SRL limited liability company registration, the entity is recognised as a separate legal person, meaning its debts and obligations remain distinct from those of its members.

Ownership is divided into quotas rather than freely transferable shares, which restricts how interests can be assigned. Transfers generally require the consent of the other members, making the S.R.L. a closer-knit structure by design.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sociedad de Responsabilidad Limitada (S.R.L.) | Separate legal personality; liability limited to capital contribution |

| Members | 2–20 members (quotaholders) | No single-member S.R.L. permitted; 20-member cap distinguishes it from the S.A. |

| Management | One or more managers (Gerentes) | Need not be members; no board structure required |

| Local Presence | Registered agent (must be a licensed Panamanian attorney or law firm) | Physical office not mandatory; registered agent address suffices |

| Capital | No statutory minimum; denominated in any currency | Divided into quotas, not shares; quota transfers require member consent |

| Privacy | Member names filed in the Public Registry | Less privacy than an S.A.; quota transfers are also registered publicly |

Focus Points

- Taxation: Foreign-sourced income is exempt from Panamanian corporate income tax under the territorial tax system; domestic income is taxed at the standard corporate rate of 25%. No VAT applies to purely passive or offshore activities, though the 7% ITBMS (Impuesto de Transferencia de Bienes Muebles y Servicios) applies to qualifying domestic transactions.

- Annual Compliance: An annual franchise tax (tasa única) is payable to the Public Registry; financial statements are required but not publicly filed.

- Economic Substance: No specific economic substance regime currently applies to S.R.Ls. engaged solely in offshore activities, though this may change as Panama responds to FATF and OECD guidance.

- Conversion: An S.R.L. may be converted into an S.A. through a formal notarial process and re-registration with the Public Registry.

- Restrictions: The 20-member cap and mandatory consent for quota transfers make this structure unsuitable for entities anticipating broad investor participation or future public offerings.

Closing

The S.R.L. suits closely held family businesses, joint ventures with a fixed group of partners, and domestic trading operations where ownership control takes priority. The built-in transfer restrictions offer a structural safeguard against unwanted ownership changes, though that same rigidity limits scalability.

The Sociedad de Responsabilidad Limitada is most appropriate for small to mid-sized ventures with a defined, stable group of owners who require limited liability without the administrative overhead of a full corporate structure.

Foreign Entities in Panama [Branch Office, Representative Office]

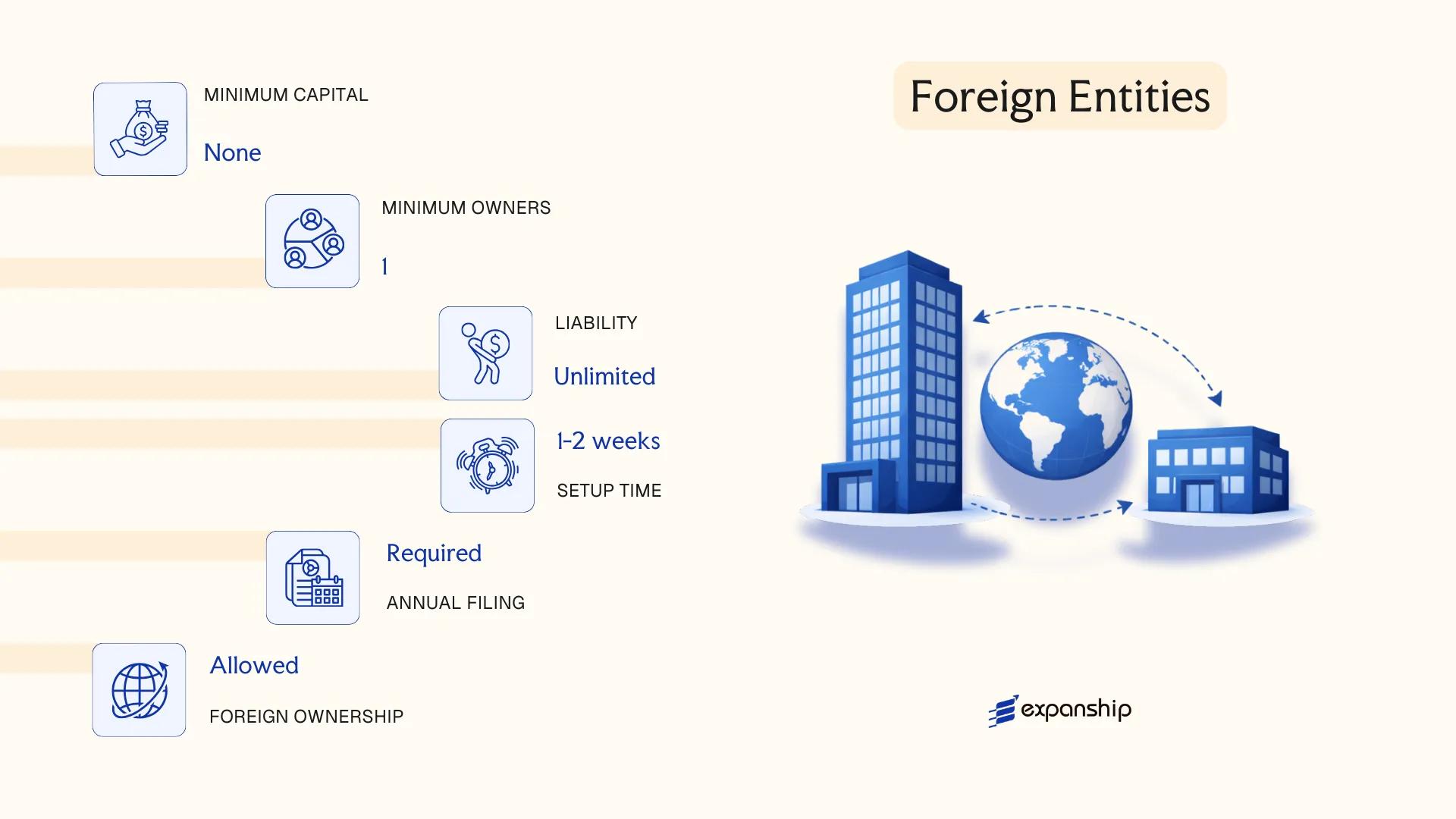

Registering a foreign company branch office in Panama is governed by the Commercial Code of Panama and Cabinet Decree No. 247 of 1970, which together establish the conditions under which a foreign entity may conduct business in the country. A branch office is not a legally separate entity from its parent company — it carries the same legal personality and exposes the parent to full liability for obligations incurred locally.

A representative office, by contrast, is restricted from generating revenue in the local market. Its activities are limited to promotional or liaison functions on behalf of the foreign parent.

Key Characteristics

| Requirement | Branch Office | Representative Office |

|---|---|---|

| Legal Form | Extension of foreign parent; no separate legal personality | Extension of foreign parent; no separate legal personality |

| Authorized Representative | Locally appointed legal representative (apoderado) | Locally appointed legal representative |

| Registered Agent | Required (licensed Panamanian attorney) | Required (licensed Panamanian attorney) |

| Local Office | Required | Required |

| Capital Requirement | No statutory minimum; parent's capital applies | None |

| Commercial Activity | Permitted | Prohibited |

| Privacy | Parent company's registration documents become public record upon filing | Same as branch |

Focus Points

- Taxation: Branch profits remitted abroad are subject to a 10% dividend withholding tax on locally sourced income; territorial tax rules mean foreign-sourced income is exempt from corporate income tax; ITBMS (Panama's VAT equivalent at 7%) applies to taxable local transactions.

- Registration: Both structures must register with the Public Registry of Panama and obtain a business license (aviso de operación) from the Ministry of Commerce and Industries (MICI).

- Annual Compliance: Branches must file annual tax returns with the Dirección General de Ingresos (DGI) and maintain local accounting records.

- Restrictions: A representative office cannot issue invoices, sign commercial contracts for its own account, or receive payment for services locally.

- Economic Substance: Foreign entities with Panama operations may fall under substance requirements if they engage in relevant activities, particularly under OECD-aligned reforms adopted after 2018.

Recommendations

A branch office suits foreign companies seeking direct operational presence without incorporating a separate local entity, though the absence of liability separation is a significant structural drawback. A representative office is appropriate for market-entry purposes where commercial activity is not yet intended.

Branch offices are best suited for established foreign companies that require an operational foothold without creating a subsidiary, while representative offices fit businesses in an exploratory or pre-commercial phase.

Partnerships in Panama [General Partnership, Limited Partnership]

Governed by the Código de Comercio (Commercial Code) of Panama, partnership structures occupy a distinct space in the country's corporate framework. Panama limited partnership registration follows rules established under the same code, which recognises two primary partnership forms: the Sociedad Colectiva (general partnership) and the Sociedad en Comandita (limited partnership).

Neither structure carries separate legal personality in the same way a Sociedad Anónima does. Partners in a general partnership bear unlimited joint liability for business obligations, while the Sociedad en Comandita Panama model introduces a two-tier membership structure that separates active management from passive investment.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sociedad Colectiva / Sociedad en Comandita | Registered via public deed before a Notary Public |

| Members | General partners: minimum 2, no statutory maximum; Limited partnership adds at least 1 silent partner | Silent partners in S. en Comandita have liability capped at their capital contribution |

| Registered Agent | Mandatory licensed Panamanian registered agent | Required for all registered entities under Panamanian law |

| Capital | No statutory minimum; denomination in any currency | Capital contributions defined in the partnership deed |

| Liability | General partners: unlimited; Silent partners: limited to contribution | Key structural distinction between the two forms |

| Privacy | Partner names appear in public deed registered with the Public Registry | Lower privacy than an S.A. structure |

Focus Points

- Taxation: Partnerships are generally taxed on Panama-source income at the standard corporate rate of 25%; foreign-source income is exempt under the territorial tax system; VAT (ITBMS) at 7% applies to taxable supplies; no specific withholding exemption applies to partner distributions.

- Annual Compliance: Obligatory filing of financial records and renewal of the registered agent; commercial licence renewal required for active trading businesses.

- Economic Substance: Panama's substance requirements apply primarily to entities with foreign-source income; partnerships operating domestically should assess applicability under current regulations.

- Treaty Access: Panama's double taxation treaty network is limited; partnership structures may face restricted access depending on the treaty and whether the entity qualifies as a resident person.

- Conversion: General partnership Panama formation does not automatically allow conversion to a corporation without dissolution and re-incorporation under a new deed.

Sub-Types

Sociedad Colectiva (General Partnership)

All partners hold unlimited personal liability and participate in management. This form is uncommon for commercial ventures of scale due to the absence of liability protection.

Sociedad en Comandita (Limited Partnership)

At least one general partner manages the business and bears unlimited liability, while one or more silent (comanditario) partners contribute capital with liability confined to that contribution. This structure is occasionally used for family business arrangements or private investment vehicles.

Closing Paragraph

General partnership Panama formation suits closely-held domestic businesses where all participants accept personal liability, while the Sociedad en Comandita is more applicable to private investment arrangements requiring a distinction between capital contributors and active managers. The principal limitation of both forms is the exposure of at least one partner to unlimited liability, which restricts their use in higher-risk commercial activities.

These structures are best suited for small domestic businesses or private family arrangements where the partners have a high degree of mutual trust and limited exposure to third-party commercial risk.

Sole Proprietorship in Panama

Sole proprietorship Panama registration falls under the general commercial framework governed by the Código de Comercio (Commercial Code) of Panama, originally enacted in 1916 and subsequently amended. Unlike corporations or limited liability companies, a sole proprietorship does not constitute a separate legal entity — the individual owner and the business are legally the same person.

This structure is referred to locally as an empresa individual or negocio de persona natural. Registration is handled through the Ministerio de Comercio e Industrias (MICI), with the business formally recorded in the Registro Público under the owner's name.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated individual business | No separate legal personality from the owner |

| Owner | Proprietor (persona natural) | One individual only; no co-owners permitted |

| Liability | Unlimited personal liability | Owner's personal assets are exposed to business debts |

| Local Presence | Registered address in Panama required | Must maintain a local commercial address for MICI registration |

| Capital | No statutory minimum | Declared at registration; no prescribed currency requirement |

| Privacy | Owner's name appears in public registry | Limited privacy; full name publicly associated with the business |

Focus Points

- Taxation: Subject to personal income tax under Panama's territorial tax system; income sourced outside Panama is exempt. ITBMS (VAT at 7%) applies if annual revenue exceeds the registration threshold. No separate corporate tax applies.

- Annual Compliance: Annual municipal tax (tasa única) and renewal of the commercial licence through MICI are required.

- Social Security: Self-employed owners must register with the Caja de Seguro Social (CSS) and contribute independently.

- Treaty Access: As an unincorporated individual business, access to Panama's double tax treaty network is limited compared to corporate structures.

- Conversion: Converting to an S.A. or S.R.L. requires a separate incorporation process; there is no automatic conversion mechanism.

Closing Paragraph

A sole proprietorship suits self-employed professionals, freelancers, and small traders conducting locally focused operations with low liability exposure. The primary advantage is minimal setup cost and administrative simplicity; the significant drawback is unlimited personal liability, which leaves the owner's private assets fully at risk.

This structure is most appropriate for individual service providers or micro-businesses operating exclusively within Panama who do not require liability protection or investor participation.

How to Choose the Right Entity Type in Panama

Knowing how to choose a business entity in Panama before you register saves time, money, and potential legal exposure later.

Why Your Entity Choice Matters

The structure you select has concrete legal and financial consequences.

- Registering an offshore S.A. when you intend to conduct commercial activity with Panamanian residents places you in breach of local trading rules, which can result in penalties or cancellation of registration.

- Selecting a tax-exempt entity when your business requires access to double taxation agreements means you cannot claim withholding reductions in counterpart countries, since treaty eligibility typically requires full tax residency status.

- Forming a corporation when a private interest foundation would better serve asset protection or succession objectives locks you into annual board and shareholder obligations that foundations are not subject to under Law 25 of 1995.

- Choosing a structure that requires audited financial statements when your operation is a single-person consultancy introduces recurring compliance costs that a simpler structure would not trigger.

Key Factors to Consider

- Business Activity: Active trading, passive asset-holding, and regulated sectors such as banking or insurance each require a distinct structure under Panamanian law.

- Local vs. Offshore Operations: Transacting with Panamanian residents requires a locally registered, tax-active entity rather than an offshore-structured company.

- Ownership and Management: Single-owner operations may prefer the S.R.L. for its flexible management structure, while multi-party ventures may require a formal board under the S.A. framework.

- Tax Objectives: Your need for full exemption, territorial tax treatment, or treaty access will determine which entity qualifies.

- Privacy Requirements: The Public Registry discloses directors of corporations; nominee arrangements or foundation structures offer greater confidentiality where that is a priority.

- Exit Strategy: Not all Panamanian entity types permit redomiciliation or conversion; confirm this before incorporation if an exit or restructuring is foreseeable.

Panama's primary company formation law, Law 32 of 1927, governs the S.A. and remains the foundational legislative reference for corporate structuring decisions.

Compliance Services for Companies in Panama

Maintain good standing, meet annual obligations, and stay aligned with Panama's regulatory requirements for your entity type.

Conclusion

Selecting the right structure is the first substantive decision in any incorporating a company in Panama guide, and that choice has direct consequences for taxation, governance, and operational flexibility. The Sociedad Anónima remains the most registered entity type in the country, favored by holding companies, international traders, and non-resident entrepreneurs for its bearer-share history and broad statutory flexibility under Law 32 of 1927. The S.R.L. suits smaller, closely held businesses where member identity and transfer restrictions matter. Branch offices serve foreign companies extending existing operations, while representative offices fit non-commercial presences. Partnerships remain uncommon outside specific professional or family arrangements.

Regulatorily, Panama has moved steadily toward greater transparency through FATF engagement and expanded automatic exchange of information agreements. That trajectory affects entity selection and ongoing compliance obligations, making your Panama business registration overview a living exercise rather than a one-time decision.

How Expanship Can Assist You

Expanship's Panama company formation services are built around the specific structures and requirements covered in this guide. From incorporating a Sociedad Anónima under the Corporations Law (Law 32 of 1927) to registering a Sociedad de Responsabilidad Limitada, our team handles filings directly with the Public Registry of Panama and coordinates with the Ministry of Commerce and Industries where required.

Beyond initial registration, Expanship supports your business across its full lifecycle in Panama:

- Document preparation, notarization, and apostille legalization

- Registered agent and registered office provision, as required by Panamanian law

- Government filing and Public Registry liaison

- Post-incorporation compliance management, including annual reporting obligations

- Corporate secretarial services

- Banking introduction assistance with Panamanian financial institutions

Reach out to Expanship Panama to discuss which structure fits your objectives.

Frequently Asked Questions (FAQ)

The Sociedad Anónima (S.A.) is by far the most frequently incorporated structure, governed by Law 32 of 1927. Its flexible shareholder rules, bearer-share history, and broad acceptance in international transactions have made it the default choice for both resident and non-resident founders.

The S.A. can have an unlimited number of shareholders and its shares are transferable without amending the corporate charter, whereas an S.R.L. caps membership and requires quota-transfer formalities. For tax purposes, neither entity is taxed on foreign-source income under Panama's territorial tax system. Compliance obligations for the S.R.L. are generally lighter, but its structural rigidity makes it less attractive for multi-investor arrangements.

The Sociedad Anónima offers the highest degree of privacy. Shareholder names are not recorded in the Public Registry; only the directors and the registered agent appear in public filings. Nominee director and nominee shareholder services are legally available and widely used.

A single individual can form an S.A. or an S.R.L., as both permit sole ownership. General and limited partnerships, however, require at least two partners by definition. A sole proprietorship is, by nature, a single-person structure with no minimum capital requirement.

All principal entity types — S.A., S.R.L., branch office, and partnerships — are open to foreign nationals without residency requirements. Panama imposes no nationality restrictions on directors or shareholders of a corporation. Foreign founders should note that branch offices require a locally appointed attorney-in-fact registered with the Public Registry.

Panamanian corporate law does not provide a straightforward statutory conversion mechanism between entity types. Restructuring typically involves dissolving one entity and incorporating another, or executing a merger under Law 32 of 1927. Legal counsel should review the specific assets, liabilities, and tax implications before any such restructuring.

The S.A., S.R.L., and branch office each hold separate legal personality under Panamanian law. General partnerships do not automatically confer limited liability or full legal separation from their partners. A limited partnership provides separation only for limited partners; the general partner retains personal liability.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.