Key Takeaways

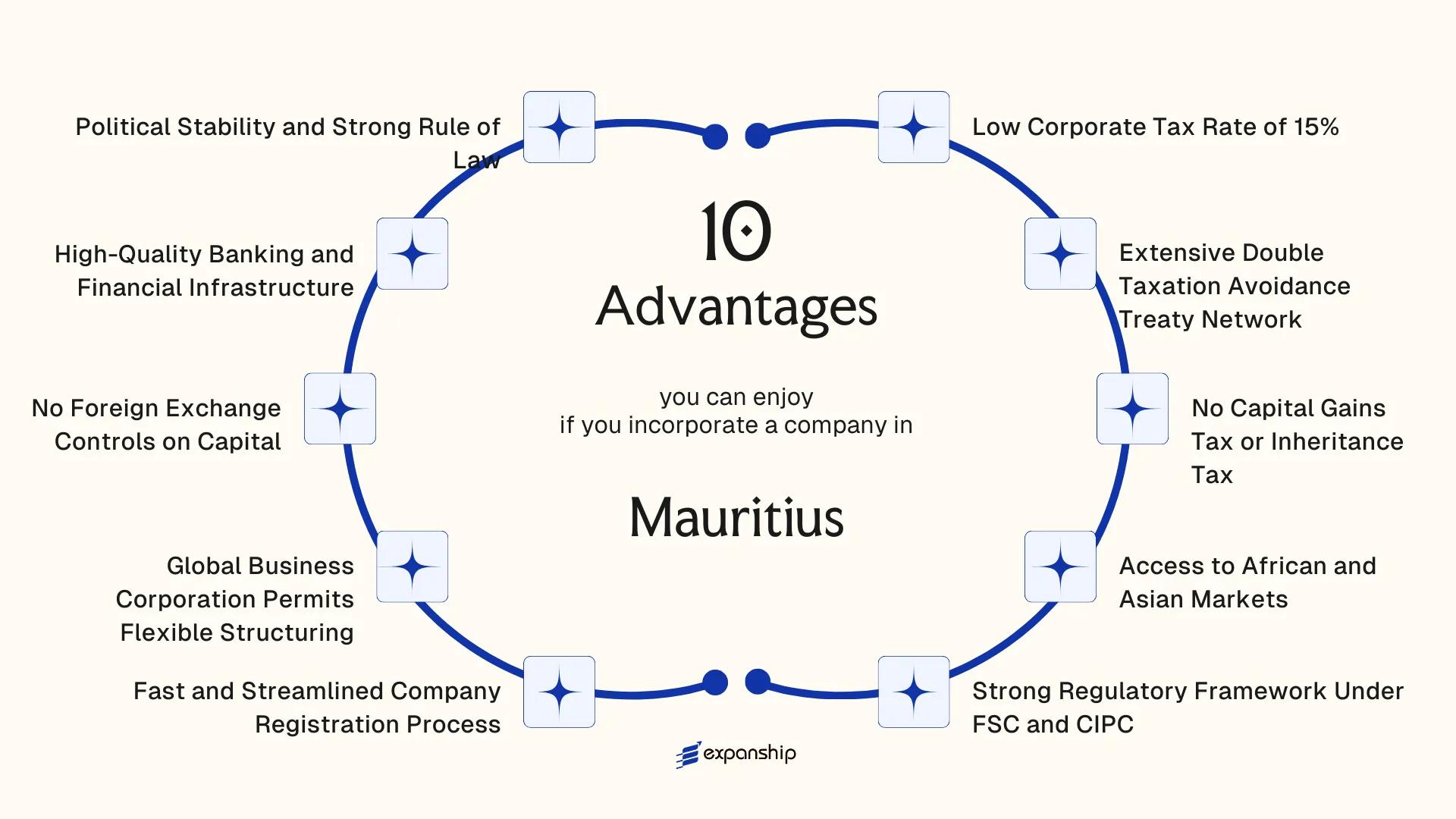

- Mauritius imposes corporate tax at a flat 15% rate under the Income Tax Act 1995, with no capital gains tax or inheritance tax, meaning investors can retain and repatriate profits without facing additional layers of taxation on asset appreciation or wealth transfer.

- The Global Business Corporation licence, issued under the Financial Services Act 2007, enables foreign-owned entities to access Mauritius's double taxation avoidance treaty network while structuring cross-border operations with flexible ownership arrangements and no mandatory local shareholding.

- Businesses oriented toward Africa or Asia gain a structural advantage from Mauritius's treaty coverage, which reduces or eliminates withholding taxes on dividends, interest, and royalties flowing through the jurisdiction across key regional economies.

- Because the Financial Services Commission and the Corporate and Business Registration Department govern different aspects of compliance depending on entity type, the regulatory obligations a company faces are determined by its licence category and activity — not by a single uniform framework applied to all registrations.

Mauritius is an independent island nation in the Indian Ocean, situated at the intersection of African and Asian trade corridors, and operates as a politically stable republic with a well-established legal system rooted in both common law and civil law traditions. Company registration falls under the oversight of the Corporate and Business Registration Department, the statutory body responsible for incorporating and maintaining business entities on the island. Foreign investors most commonly establish a Global Business Corporation when structuring cross-border operations through the jurisdiction.

The tax regime is treaty-based and low-tax by design, with foreign ownership permitted across most sectors without mandatory local shareholding requirements. This openness to foreign direct investment has made the jurisdiction a consistent destination for holding structures, investment funds, and regional operating companies alike.

This article examines the concrete advantages your business gains by choosing Mauritius company formation — from its regulatory environment to its financial infrastructure and treaty access.

Low Corporate Tax Rate of 15%

Mauritius low corporate tax rate benefits are defined by a single flat rate of 15%, which applies uniformly to both resident and non-resident companies under the Income Tax Act 1995.

What the Rate Actually Means in Practice

At 15%, the corporate tax burden sits well below the OECD average of approximately 23%. For a foreign-owned entity generating profits through a Mauritius-registered company, that gap directly increases after-tax retained earnings available for reinvestment or distribution.

How the Structure Reinforces the Rate

Global Business Companies licensed under the Financial Services Act 2007 may access further relief through foreign tax credits, effectively reducing their tax liability on foreign-sourced income. The 15% headline rate functions as a ceiling, not a floor, for qualifying structures.

Eligibility for these credits depends on demonstrating foreign tax paid, which requires maintaining adequate substance and documentation within the jurisdiction. This is a compliance condition, not an administrative formality, and should be factored into your corporate structuring from the outset.

A properly structured Mauritius entity can retain a materially higher share of profits compared to operating through a higher-tax domicile, without relying on opacity or artificial arrangements.

Extensive Double Taxation Avoidance Treaty Network

Mauritius has signed over 45 double taxation avoidance agreements, covering major economies across Africa, Asia, Europe, and the Gulf. This treaty network is a structural advantage for foreign businesses that route cross-border income through a Mauritian entity, as it directly reduces withholding tax on dividends, interest, and royalties paid between treaty partners.

For investors targeting Africa, the treaties with countries such as India, South Africa, Rwanda, and Mozambique create a measurable tax cost reduction at the point of income repatriation. India, historically one of the primary treaty relationships, has been renegotiated and updated, so your structure must be reviewed against current provisions under the amended India-Mauritius treaty to confirm applicable rates and conditions.

Treaty eligibility generally depends on your entity holding a valid Global Business Licence issued under the Financial Services Act 2007, along with demonstrating genuine economic substance in the jurisdiction.

Why this matters in practice:

- Withholding tax rates on dividends can fall to 0-5% under treaty terms, versus standard domestic rates of 10-20% in many partner countries

- Treaty protection reduces the risk of double taxation on the same income stream in two jurisdictions simultaneously

- The network covers jurisdictions across multiple continents, reducing the need to establish multiple holding entities in different regions

- Treaty provisions often extend to capital gains in certain partner jurisdictions, providing additional tax certainty for exit planning

Incorporate a Company in Mauritius

Set up a Mauritian company and access one of the most extensive treaty networks available to holding and investment structures.

No Capital Gains Tax or Inheritance Tax

Mauritius imposes no capital gains tax, a structural feature of its tax code that directly benefits foreign business owners and investors. Gains realised from the disposal of securities, real estate, or business assets are not subject to tax at the corporate or individual level. For a holding company or investment vehicle, this means exit proceeds flow back to shareholders without a domestic tax charge reducing the return.

| Tax Type | Position in Mauritius | Governing Reference |

|---|---|---|

| Capital Gains Tax | Not imposed | Income Tax Act 1995 |

| Inheritance Tax | Abolished | Finance Act 1981 |

| Estate Duty | Not applicable | Abolished concurrent with inheritance tax |

| Withholding Tax on Dividends | 0% (resident companies) | Income Tax Act 1995 |

The zero inheritance tax position carries practical weight for succession planning. Ownership stakes in a Mauritian entity can transfer between generations or to beneficiaries without a domestic tax event triggering on the transfer itself. For family offices or founder-owned structures, this reduces the cost and complexity of long-term ownership transitions.

Both exemptions apply regardless of where the underlying assets or beneficiaries are located, subject to the terms of any applicable tax treaty and your home jurisdiction's rules on foreign-sourced gains. Your own country's controlled foreign corporation rules or exit tax provisions remain relevant, so the domestic tax position in Mauritius is one variable within a broader structuring analysis.

Access to African and Asian Markets

Mauritius sits at the geographic midpoint between the African continent and the Indian subcontinent, a position that directly shapes its commercial utility. As a Mauritius gateway to African Asian markets, companies registered here can access two of the world's fastest-growing economic regions from a single base, without maintaining separate legal entities in each.

The African Continental Free Trade Area (AfCFTA) connection is particularly relevant. Mauritius is a signatory, which gives incorporated entities preferential access to a trade bloc covering 54 countries and a combined GDP exceeding USD 3 trillion. For businesses targeting Sub-Saharan Africa, this reduces tariff friction that would otherwise apply to goods and services originating from outside the bloc.

On the Asian side, the country's strong bilateral ties with India, further reinforced by the Comprehensive Economic Cooperation and Partnership Agreement, allow Mauritius-incorporated firms to serve Indian markets under structured preferential terms. Similar frameworks extend toward China and Southeast Asia.

Keep these points in mind:

- AfCFTA membership confers preferential tariff treatment, but specific product schedules still apply

- CECPA benefits are available to qualifying entities under defined rules of origin

- Your firm's substance in Mauritius affects treaty and trade agreement eligibility

- Trade agreement benefits are not automatic; confirm that your business activity falls within covered sectors

Mauritius is one of the few small-island nations that holds active investment promotion agreements with both India and multiple African Development Bank member states simultaneously.

Strong Regulatory Framework Under FSC and CIPC

The Mauritius FSC regulatory framework advantages extend well beyond formal compliance. The Financial Services Commission, established under the Financial Services Act 2007, supervises all financial services activities, while the Companies and Intellectual Property Commission handles corporate registrations and statutory filings. Having two distinct, specialized bodies means oversight is targeted rather than generic, which reduces bureaucratic overlap and gives your business a clearer regulatory counterpart to deal with.

Regulatory Credibility That Travels

Holding a license or registration under FSC supervision signals to banks, institutional partners, and counterparties in other jurisdictions that your entity operates under a regulated, audited framework. The FSC enforces Anti-Money Laundering and Combating the Financing of Terrorism requirements aligned with FATF standards, which directly affects how correspondent banks and overseas regulators assess your firm's risk profile. That external credibility is difficult to obtain from an unregulated offshore structure.

Structured Flexibility for Different Business Types

The FSC issues specific licenses across categories including Global Business Licenses, investment dealer authorizations, and fund administration permits, each with defined capital requirements and conduct obligations under the Financial Services Act 2007. This tiered licensing structure means your business operates under rules proportionate to its actual activities rather than a one-size framework. CIPC's online filing system also maintains a public register of companies, which supports the due diligence requirements that many institutional investors and foreign banks impose before entering a commercial relationship.

Maximize Your Regulatory Advantages in Mauritius

Speak with our corporate services team to identify the right license category, registration structure, and compliance obligations for your business under the FSC and CIPC frameworks.

Fast and Streamlined Company Registration Process

Mauritius fast company registration advantages are not merely procedural — the speed at which a business becomes legally operational has a direct bearing on when it can open bank accounts, sign contracts, and begin generating revenue.

- Under the Companies Act 2001, a private company can typically be incorporated within one to two business days once all required documents are submitted to the Registrar of Companies.

- The online registration portal operated by the Corporate and Business Registration Department (CBRD) accepts applications digitally, removing the requirement for physical presence during the filing process.

- There is no minimum paid-up capital requirement for a standard private company, which means your entity can be formed and registered without first moving funds into the jurisdiction.

- A company secretary must be appointed, but this role can be fulfilled by a licensed management company, which removes the administrative burden from the applicant.

- For regulated activities requiring a Financial Services Commission licence, processing timelines are longer, but the standard corporate registration itself remains decoupled from that process, so the legal entity exists independently while licensing proceeds.

For foreign investors accustomed to multi-week registration timelines in other jurisdictions, the ability to have a legally constituted company within days materially reduces the cost of entry and time-to-market.

Global Business Corporation Permits Flexible Structuring

A Mauritius Global Business Corporation advantages stems partly from the structural latitude the GBC license provides. Under the Financial Services Act 2007 and administered by the Financial Services Commission (FSC), a GBC can be incorporated as a company, trust, partnership, or protected cell company, giving foreign business owners meaningful choice over how their entity is constituted.

That flexibility has direct implications for holding structures, fund vehicles, and operating companies seeking to channel cross-border income. A GBC can hold shares in foreign subsidiaries, act as an investment holding entity, or serve as a regional headquarters, without being locked into a single corporate form dictated by the jurisdiction.

Ownership is also unrestricted. Foreign nationals can hold 100% of a GBC without a local partner, and there is no mandatory minimum paid-up capital requirement under the Companies Act 2001 for most GBC structures.

A foreign investor establishes a GBC holding company with USD 1 in paid-up capital, holds 100% of four African operating subsidiaries through it, and repatriates dividends upward with no withholding tax at the GBC level, an outcome not replicable under comparable holding regimes in Singapore or the Netherlands without substantially higher capitalization or local director requirements.

No Foreign Exchange Controls on Capital

Mauritius imposes no foreign exchange controls, meaning your business can move capital in and out of the country without restriction. This applies to dividends, loan repayments, royalties, and the full repatriation of profits. For a foreign investor, this removes a structuring constraint that is common in many African and emerging market jurisdictions.

The absence of restrictions is grounded in the Exchange Control Act, which was repealed in 1994. Since that repeal, transactions in foreign currency have been freely conducted without prior approval from the Bank of Mauritius or any other regulatory authority.

Practical benefits for foreign-owned entities include:

- Dividends can be remitted to a parent company abroad without withholding restrictions tied to currency approval

- Loan proceeds and repayments between related entities in different jurisdictions face no capital movement ceilings

- Proceeds from asset sales or business exits can be transferred out in full

Free capital repatriation means your treasury and group financing arrangements are not distorted by local currency rules, which reduces both administrative overhead and hedging costs.

Global Business Companies must conduct their banking through a Category 1 bank licensed by the Bank of Mauritius, which determines which institutions can facilitate your cross-border transfers.

High-Quality Banking and Financial Infrastructure

Mauritius banking infrastructure advantages for businesses are grounded in a well-supervised financial system that supports multi-currency operations, cross-border transactions, and institutional-grade services without the friction common in many emerging market jurisdictions.

Licensed Banks with International Capabilities

The Bank of Mauritius, established under the Bank of Mauritius Act 2004, licenses and supervises commercial banks operating on the island. Most major banks licensed here offer multi-currency accounts, trade finance facilities, and correspondent banking relationships with institutions in Europe, Asia, and North America. For a foreign-owned entity conducting cross-border business, this means your operating accounts can hold and transact in USD, EUR, GBP, and other major currencies from a single local banking relationship.

Account Access for International Structures

Foreign-incorporated entities, including Global Business Companies licensed under the Financial Services Act 2007, can open corporate bank accounts with licensed local banks. Account opening requirements vary by institution but generally include KYC documentation, proof of business activity, and corporate records. This accessibility removes a common barrier that foreign investors face in jurisdictions where account opening is restricted to resident-owned firms.

Payment Infrastructure and Financial Services Depth

Beyond banking, the financial services ecosystem includes licensed fund administrators, custodians, insurance companies, and capital markets intermediaries regulated by the Financial Services Commission. This concentration of licensed service providers means your business can access fund management, structured finance, and payment processing within the same jurisdiction, reducing the need to operate across multiple regulatory environments.

Political Stability and Strong Rule of Law

Mauritius political stability business advantages are, in practical terms, a form of structural risk reduction. The country has maintained uninterrupted democratic governance since independence in 1968, with regular peaceful transfers of power. For a foreign business owner, this continuity means your corporate structure, tax position, and regulatory relationships are not subject to abrupt policy reversals.

The legal system is grounded in a dual tradition: English common law governs commercial matters, while civil law principles derived from the French Napoleonic Code apply to certain areas such as property. This mixed framework gives both common law and civil law jurisdictions a recognisable foundation to work from. Courts apply established precedent, and the Companies Act 2001 provides a codified basis for corporate rights and obligations.

Ranked consistently among the top performers in Africa on rule of law indicators by the World Bank's Worldwide Governance Indicators, the country's legal institutions carry real credibility with counterparties and financiers. Contracts are enforceable through independent courts, and the judiciary operates without direct executive interference under the Constitution. That independence matters when you are structuring cross-border transactions that may eventually require dispute resolution.

Key institutional factors that support investor security include:

- The Constitution of Mauritius guarantees protection of property rights and prohibits arbitrary expropriation without fair compensation

- The Supreme Court serves as the apex civil and commercial court, with appeals available to the Judicial Committee of the Privy Council in London

- The Financial Intelligence and Anti-Money Laundering Act (FIAMLA) and associated AML frameworks align the jurisdiction with FATF standards, which supports correspondent banking relationships

Why Mauritius Stands Out Against Competing Jurisdictions

Assessing how Mauritius compares on Mauritius vs competing jurisdictions advantages requires choosing rivals that target the same investor profile. Singapore, Seychelles, and Cyprus each appeal to internationally minded business owners seeking tax efficiency, treaty access, or offshore structuring, making them the most relevant benchmarks for this analysis.

Where Mauritius distinguishes itself is not through any single feature but through the combination of treaty depth, dual-market access, and regulated credibility at a cost base that neither Singapore nor Cyprus can consistently match. Singapore carries higher substance and operational costs; Cyprus, post-2013, operates under greater EU regulatory pressure; Seychelles offers lighter compliance but a significantly thinner treaty network and limited banking infrastructure. For a firm routing investment into Africa or South Asia, the treaty network underpinned by Mauritius's bilateral agreements carries direct commercial weight that these alternatives cannot replicate.

| Parameter | Mauritius | Singapore | Seychelles | Cyprus |

|---|---|---|---|---|

| Standard Corporate Tax Rate | 15% | 17% | 15% | 12.5% |

| Double Tax Treaties | 45+ | 90+ | ~30 | 65+ |

| Capital Gains Tax | None | None | None | None |

| Africa-Focused Treaty Access | Strong | Limited | Minimal | Minimal |

| FSC-Regulated Fund Structures | Yes | Yes | Limited | Yes |

| Foreign Exchange Controls | None | None | None | None |

| FATF Status | Compliant | Compliant | Monitored | Compliant |

Compliance Services for Companies in Mauritius

Stay aligned with FSC and CIPC requirements through structured compliance support tailored to Mauritius-registered entities.

Conclusion

Mauritius presents a well-defined case for foreign incorporation: a 15% corporate tax rate applied under the Income Tax Act 1995, an extensive network of double taxation avoidance agreements covering key African and Asian economies, and the absence of capital gains tax combine to produce a jurisdiction where the structural tax position is clear from the outset. These are not incidental features but codified rules that directly affect how profits are retained, distributed, and repatriated.

That case is strongest for businesses with a genuine operational or investment nexus to Africa or Asia. The treaty network and the Global Business Corporation licence structure under the Financial Services Act 2007 are designed with cross-border activity in mind, and the benefits of incorporating in Mauritius are most material when that geographic orientation exists.

Your specific industry, ownership structure, and activity type will determine how much of this framework applies. A holding company, a fund, and an operating subsidiary each interact with the Financial Services Commission and the Companies and Intellectual Property Commission in different ways, and the applicable obligations differ accordingly. The next step is assessing which entity type and licence category align with your business objectives, and ensuring the structure is set up correctly under the relevant regulatory requirements from the start.

Start Your Mauritius Company with Expanship Today

Mauritius company formation with Expanship covers the full incorporation lifecycle, from selecting between a domestic company and a Global Business Corporation under the Companies Act 2001 to meeting the ongoing obligations set by the Registrar of Companies and the Financial Services Commission. The services are structured to match the specific requirements each entity type carries under Mauritian law.

Expanship's support across this process includes:

- Preparation and legalization of constitutional documents, including the constitution or model articles where applicable

- Provision of a registered agent and local registered office address as required under the Companies Act 2001

- Filing with the Registrar of Companies and, where required, submission of applications to the Financial Services Commission

- Post-incorporation compliance management, including annual return filings and maintenance of statutory registers

- Coordination of corporate secretary services to satisfy residency and governance requirements

- Banking introduction assistance to support account opening with local financial institutions

To discuss your incorporation requirements, contact Expanship Mauritius.

Frequently Asked Questions (FAQ)

A GBC is subject to corporate income tax at a flat rate of 15% under the Income Tax Act 1995. Dividends distributed to non-resident shareholders are exempt from withholding tax in Mauritius, and since there is no capital gains tax, profits from asset disposals or share transfers are not subject to further taxation at the corporate or shareholder level.

The Financial Services Commission (FSC) licenses and supervises GBCs under the Financial Services Act 2007. Failure to meet ongoing compliance obligations, including substance requirements and annual fee payments, can result in suspension or revocation of the GBC licence. Revocation removes the entity's access to treaty benefits and its authorization to conduct cross-border financial activities.

No restrictions apply to the repatriation of profits, dividends, or capital by foreign investors. The Exchange Control Act was repealed, and Mauritius operates without foreign exchange controls, meaning funds can be transferred across borders freely without prior approval from the Bank of Mauritius or any other authority.

Incorporating a standard private company under the Companies Act 2001 can be completed within one to two business days through the Corporate and Business Registration Department (CBRD). Obtaining the GBC licence from the FSC takes longer, typically two to four weeks, depending on the completeness of the application and the nature of the proposed business activities.

For investments directed into Sub-Saharan Africa, Mauritius holds a structural advantage due to its treaty network with over 45 countries, many of which are African states with no equivalent treaty relationship with Singapore or the Netherlands. The India-Mauritius tax treaty, though amended in 2016, still provides a framework for Indian-facing structures. The comparative advantage depends on the specific target countries and treaty provisions relevant to your investment structure.

The FSC requires a GBC to demonstrate economic substance in Mauritius, which includes having qualified resident directors, maintaining accounting records locally, holding board meetings on the island, and conducting core income-generating activities from within the jurisdiction. These requirements align with the OECD's Base Erosion and Profit Shifting (BEPS) standards and were formalized through amendments to the Financial Services Act. Entities that fail to establish genuine substance risk being denied treaty benefits by foreign tax authorities.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.