Key Takeaways

- Mauritius operates a dual regulatory framework in which the Registrar of Companies governs entities under the Companies Act 2001 and the Financial Services Commission oversees global business and financial services activities.

- The Global Business Company is the most registered entity type among international investors, primarily used for cross-border holding and investment activity under the Income Tax Act.

- Among the ten recognised legal structures, the Private Company Limited by Shares serves as the standard vehicle for domestic trade, while the Authorised Company is designed for non-resident businesses that conduct no local dealings.

- Mauritius draws its legal system from both English common law and the Napoleonic Code, a duality that directly shapes how business entities are structured and governed across all available forms.

Introduction to Entity Types in Mauritius

Mauritius is an island nation in the southwestern Indian Ocean, situated east of Madagascar and part of the Mascarene archipelago. As an independent republic and member of the Commonwealth, it maintains a legal system that draws from both English common law and the Napoleonic Code — a duality that shapes how business entities are structured and governed.

Company registration and ongoing compliance fall under the authority of the Registrar of Companies, which operates under the Companies Act 2001. The Financial Services Commission (FSC) regulates entities engaged in global business and financial services activities. Together, these two bodies govern the full spectrum of legal entity structures available to domestic and foreign investors.

The tax regime is treaty-based and generally low-rate, with Mauritius holding an extensive network of double taxation agreements that affect how different entity types are taxed on cross-border income.

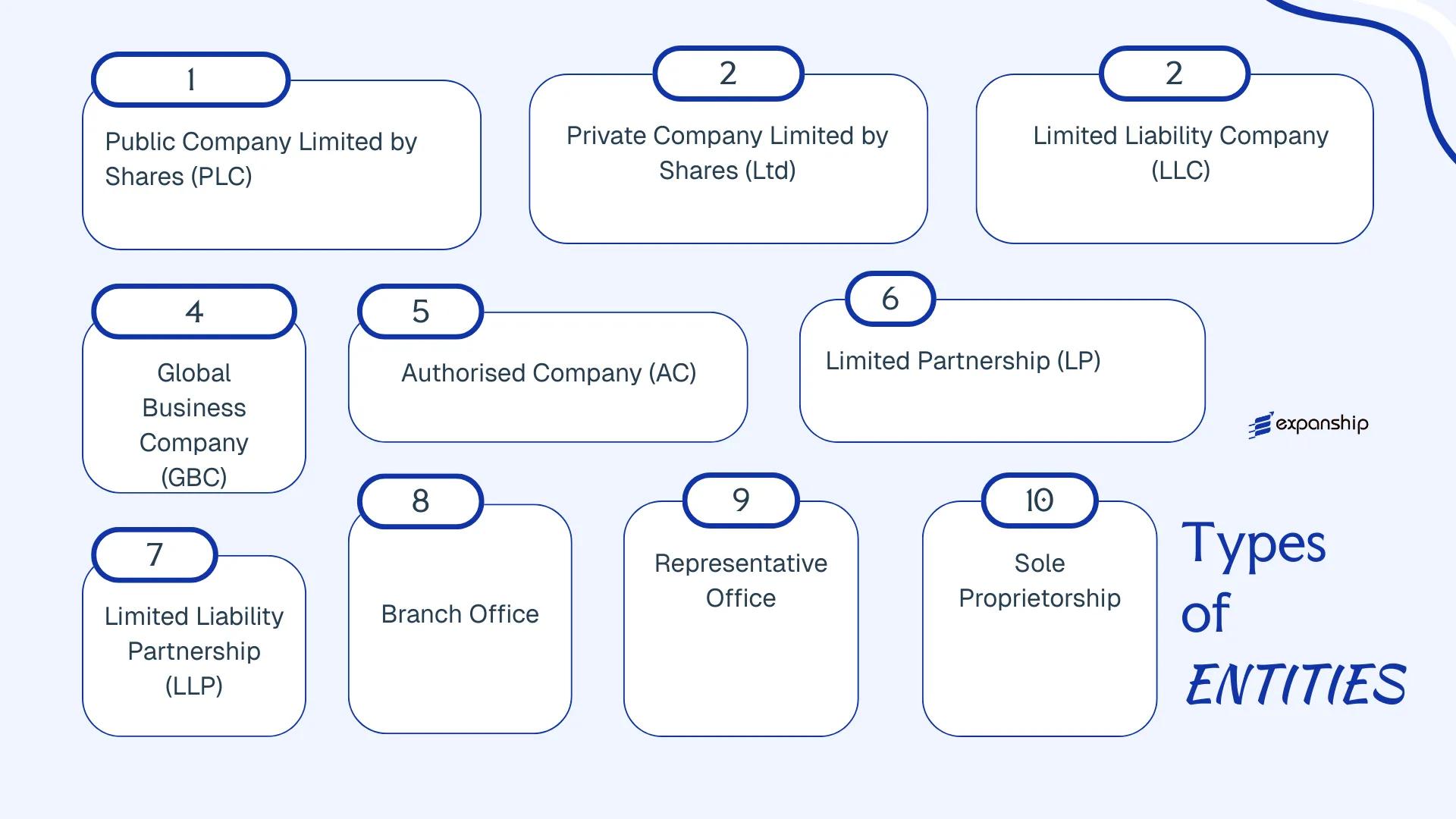

The types of business entities in Mauritius available under the current legal framework include:

- Public Company Limited by Shares (PLC)

- Private Company Limited by Shares (Ltd)

- Limited Liability Company (LLC)

- Global Business Company (GBC)

- Authorised Company (AC)

- Limited Partnership (LP)

- Limited Liability Partnership (LLP)

- Branch Office

- Representative Office

- Sole Proprietorship

Each structure carries distinct requirements around ownership, liability, taxation, and regulatory oversight, all of which this article examines in detail.

An Overview of Business Structures in Mauritius

Mauritius offers multiple business structures under two primary legislative instruments: the Companies Act 2001 and the Financial Services Act 2007. Each structure carries distinct characteristics in terms of liability, tax treatment, trading permissions, and regulatory oversight, and the sections that follow examine each in full detail.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Public Company (PLC) | Incorporated company | Limited to shares | Taxed | Yes | 7 shareholders | Registrar of Companies | Companies Act 2001 |

| Private Company (Ltd) | Incorporated company | Limited to shares | Taxed | Yes | 1 shareholder | Registrar of Companies | Companies Act 2001 |

| Limited Liability Company (LLC) | Hybrid entity | Limited | Taxed | Yes | 1 member | Registrar of Companies | Companies Act 2001 |

| Global Business Company (GBC) | Incorporated company | Limited | Taxed (15% CIT) | Restricted | 1 shareholder | Financial Services Commission | Financial Services Act 2007 |

| Authorised Company (AC) | Incorporated company | Limited | Exempt | No | 1 shareholder | Financial Services Commission | Financial Services Act 2007 |

| Limited Partnership (LP) | Partnership | Mixed | Taxed / Pass-through | Yes | 2 partners | Registrar of Companies | Limited Partnerships Act 2011 |

| Limited Liability Partnership (LLP) | Partnership | Limited | Pass-through | Yes | 2 partners | Registrar of Companies | Limited Liability Partnerships Act 2016 |

| Branch Office | Foreign branch | Unlimited (parent) | Taxed | Yes | N/A | Registrar of Companies | Companies Act 2001 |

| Representative Office | Non-trading presence | Unlimited (parent) | Exempt | No | N/A | Registrar of Companies | Companies Act 2001 |

| Sole Proprietorship | Unincorporated | Unlimited | Taxed | Yes | 1 owner | Registrar of Businesses | Business Registration Act 2002 |

Each of these structures is examined in full in the sections below.

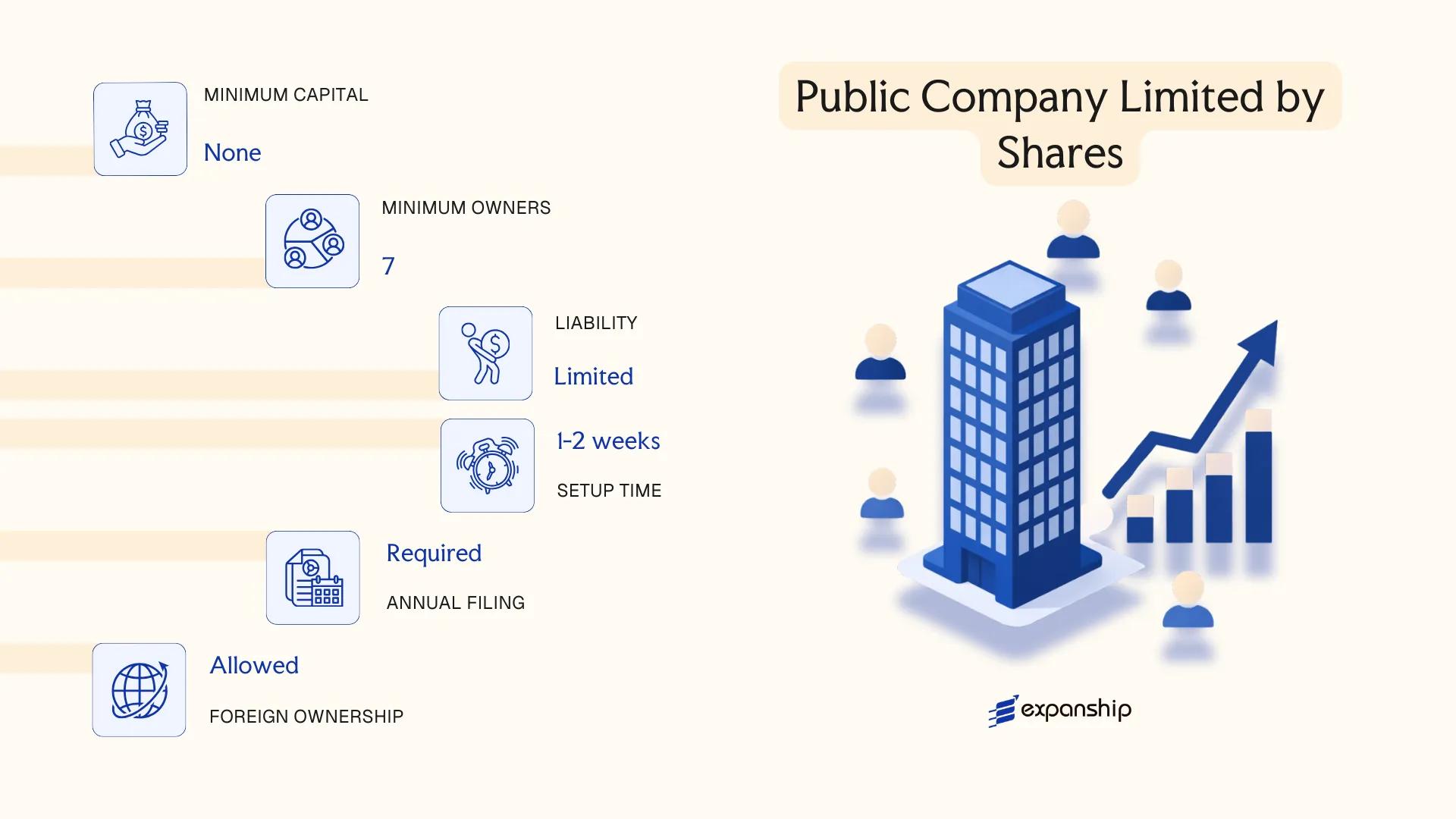

Public Company Limited by Shares (PLC)

A Mauritius public company limited by shares is governed by the Companies Act 2001 and exists as a separate legal entity from its shareholders. Liability is limited to the amount unpaid on each member's shares. Unlike private companies, a PLC may offer its shares to the public and, if listed, is subject to additional oversight by the Financial Services Commission (FSC) and the Stock Exchange of Mauritius (SEM).

Listing on the SEM is not mandatory. An entity may be incorporated as a public company and remain unlisted, though it must still meet the structural requirements applicable to this form under the Companies Act 2001.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Public Company Limited by Shares | Separate legal personality; shareholders not personally liable beyond unpaid share capital |

| Members | Min. 2 shareholders; no upper limit | Shares may be offered to the public; bearer shares are not permitted |

| Directors | Min. 2 directors | At least 2 must be individuals; corporate directors permitted alongside individual directors |

| Local Presence | Registered office in Mauritius required | No mandatory resident director requirement for domestic PLCs, though governance best practice applies |

| Share Capital | No statutory minimum; denominated in MUR or any currency | Must have an authorised share capital; par value or no-par value shares permitted |

| Privacy | Register of shareholders is a public document | Directors and officers are publicly disclosed via the Registrar of Companies |

Focus Points

- Taxation: Subject to a 15% corporate income tax rate; an 8% alternative minimum tax applies on turnover where tax payable falls below threshold; VAT registration required if turnover exceeds MUR 6 million annually; dividends distributed to non-resident shareholders are generally exempt from withholding tax under domestic law.

- Annual Compliance: Must file audited financial statements and an annual report with the Registrar of Companies; listed PLCs are subject to continuous disclosure obligations under SEM Listing Rules.

- Economic Substance: No formal economic substance regime applies to domestic PLCs; however, listed entities must meet SEM governance requirements including board composition and audit committee standards.

- Conversion: A private company may be converted to a public company by special resolution and re-registration under the Companies Act 2001, subject to meeting the structural requirements.

- Restrictions: May not restrict the transfer of shares in its constitution; offering shares to the public without a prospectus is prohibited.

Closing

A PLC is suited to businesses seeking access to public capital markets or planning a future listing on the SEM, though the associated compliance burden — audited accounts, public disclosure, and ongoing regulatory reporting — makes it a structurally heavier vehicle than most private alternatives.

Established businesses or groups planning a public listing on the Stock Exchange of Mauritius, or those requiring a publicly recognised corporate structure to attract institutional investors.

Company Incorporation in Mauritius

Incorporate a public or private company in Mauritius with end-to-end support from entity selection to post-incorporation compliance.

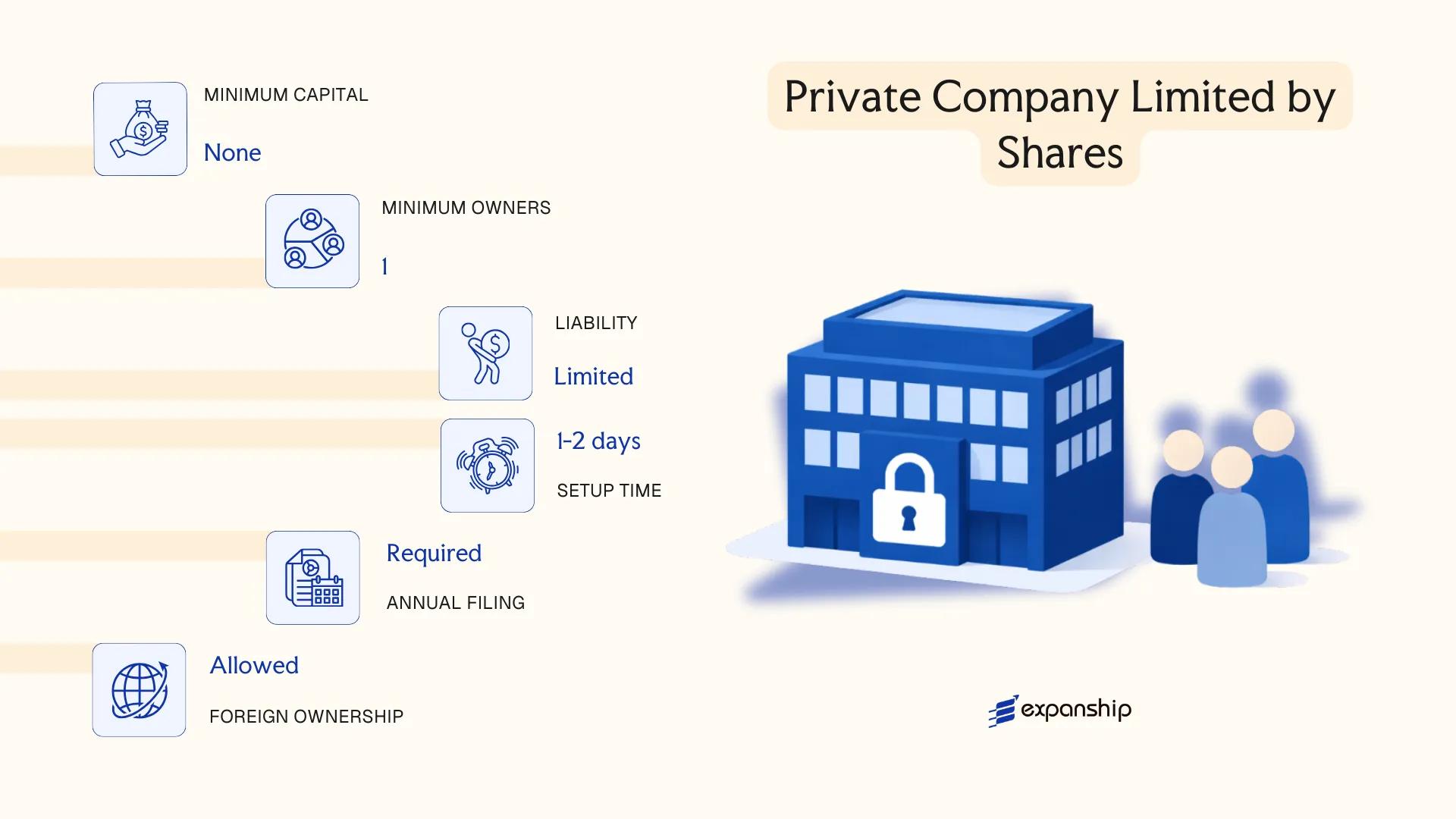

Private Company Limited by Shares (Ltd)

A Mauritius private company limited by shares (Ltd) is governed by the Companies Act 2001, administered by the Registrar of Companies under the Corporate and Business Registration Department (CBRD). The entity carries a separate legal personality, meaning its debts and obligations are distinct from those of its shareholders.

Shares in a private company cannot be offered to the public and are subject to transfer restrictions set out in the company's constitution. This structure suits closely held businesses where ownership control is a priority.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private Company Limited by Shares | Governed by Companies Act 2001 |

| Members | Shareholders (1–25) and Directors (minimum 1) | No corporate director restriction; one person can hold both roles |

| Local Presence | Registered office address in Mauritius required | Must be maintained at all times with the CBRD |

| Capital | No minimum share capital; MUR or foreign currency permitted | Shares must have a par value or be no-par-value shares |

| Privacy | Constitution and shareholder details filed with CBRD | Beneficial ownership disclosures required under FAIA 2012 |

Focus Points

- Taxation: Subject to 15% corporate income tax; 15% VAT registration threshold applies; dividends paid to non-residents may attract 0% withholding tax under domestic law or applicable tax treaties.

- Annual Compliance: Annual return and audited financial statements must be filed with the CBRD; audit is mandatory unless exempt under the Act.

- Economic Substance: No formal economic substance obligation applies to domestic Ltd entities, unlike Global Business Companies.

- Treaty Access: Does not automatically qualify for Mauritius's tax treaty network; treaty benefits depend on tax residency and substance.

- Conversion: Can be converted to a public company or other permitted structure under the Companies Act 2001 through a formal CBRD process.

Closing

A private Ltd is commonly used for local trading operations, domestic holding structures, and family-owned enterprises where restricted share transferability is desirable. The absence of a minimum capital requirement lowers the entry barrier, though the 25-shareholder cap limits scalability for businesses seeking broader investor participation.

This structure suits small to mid-sized businesses, joint ventures, and family groups requiring straightforward domestic incorporation with defined ownership boundaries.

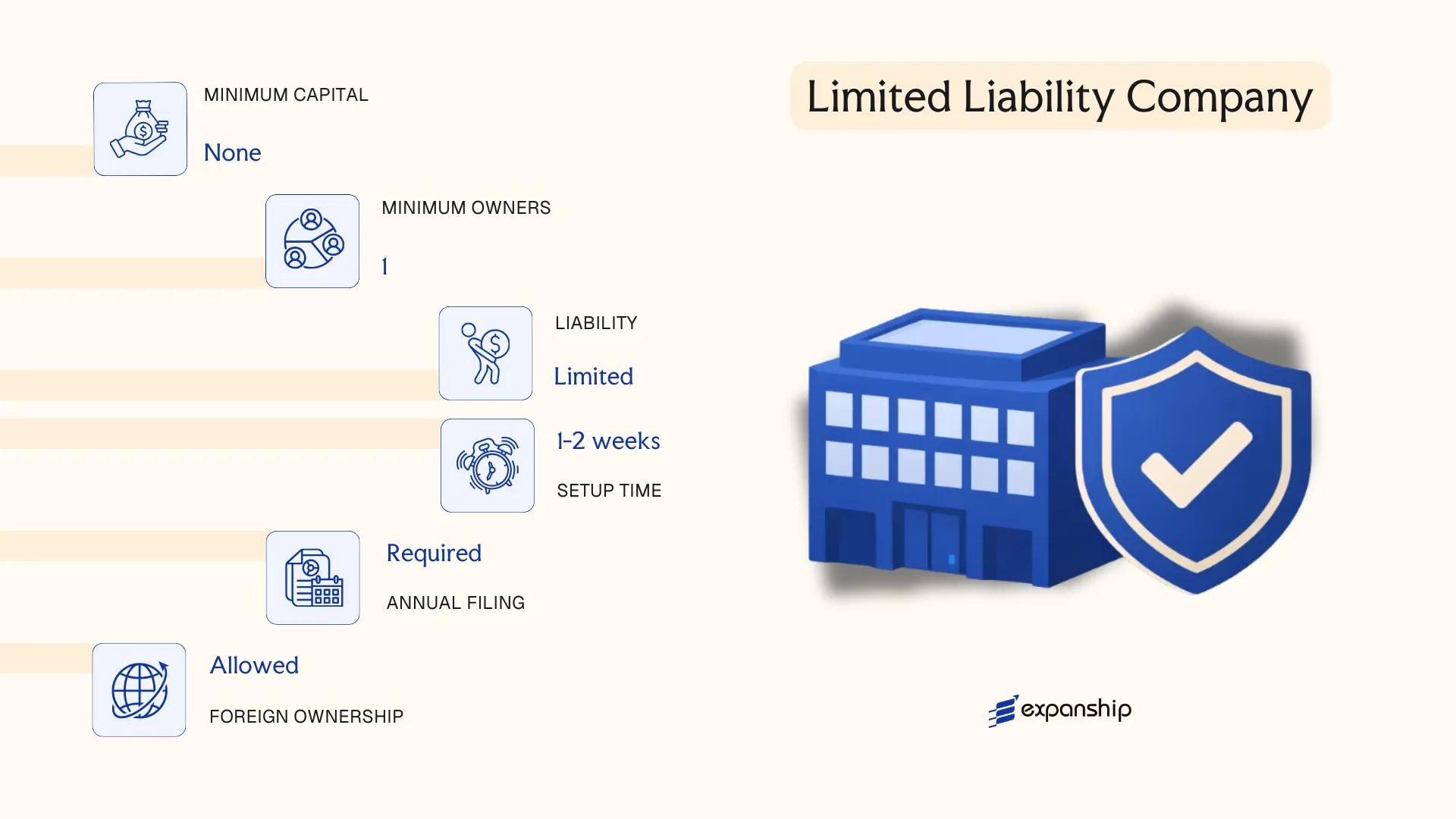

Limited Liability Company (LLC)

Mauritius does not recognise the LLC as a distinct statutory form under the Companies Act 2001. The legislation provides for companies limited by shares, companies limited by guarantee, and unlimited companies — but not a standalone LLC category in the American or Caribbean sense. What practitioners informally call a "Mauritius LLC structure" typically refers to a private company limited by shares configured with member-managed governance, which produces a functionally similar result.

Mauritius limited liability company formation discussions often arise because foreign investors seek a hybrid structure combining pass-through-style flexibility with corporate liability protection. Under the Companies Act 2001, the private limited company is the closest equivalent, offering separate legal personality and capped member liability while allowing considerable contractual freedom in the company's constitution.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private Company Limited by Shares | Governed by Companies Act 2001 |

| Members / Roles | Shareholders and Directors | Minimum 1 shareholder; minimum 1 director; maximum 25 shareholders |

| Local Presence | Registered Agent and Registered Office | Must maintain a physical registered address in Mauritius |

| Share Capital | No statutory minimum; MUR or foreign currency permitted | Shares must be issued at incorporation |

| Privacy | Beneficial ownership disclosed to the Registrar of Companies | Not publicly searchable in all cases; subject to AML obligations |

Focus Points

- Taxation: Corporate tax applies at 15% on net income; an 8% partial exemption may apply on certain foreign-source income; standard VAT rate is 15%; no capital gains tax; withholding tax rates vary by income type and applicable tax treaty.

- Economic Substance: Domestic companies without GBC status are not subject to OECD-driven substance requirements, though substance remains relevant for treaty access.

- Annual Compliance: Annual return and audited financial statements must be filed with the Registrar; audit is mandatory regardless of size for companies limited by shares.

- Restrictions: The 25-shareholder cap and prohibition on public share offerings distinguish this structure from a public company.

- Conversion: A private company may be converted to a public company or re-registered as a GBC under the Financial Services Act 2007 if qualifying conditions are met.

Closing

This structure suits domestic trading, holding arrangements, and small-to-medium enterprises where owners require liability protection without the administrative burden of a public listing. The main constraint is the 25-shareholder ceiling, which limits equity distribution for businesses planning broader investor participation.

Founders and small investor groups seeking liability protection within a flexible governance framework, without needing to access international tax treaty networks.

Global Business Company (GBC)

A Mauritius Global Business Company is governed by the Companies Act 2001 and the Financial Services Act 2007, with licensing administered by the Financial Services Commission (FSC). It carries separate legal personality and limited liability, and functions as a hybrid structure designed for cross-border activities rather than domestic trade.

Resident in Mauritius for tax purposes, a GBC can access the country's network of Double Taxation Agreements (DTAs) — provided it meets substance requirements. This distinguishes it structurally from an Authorised Company, which is treated as non-resident.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private company limited by shares | Incorporated under the Companies Act 2001; FSC-licensed |

| Members | Min. 1 shareholder; no maximum | Shareholders can be individuals or corporate entities; nominee shareholding permitted |

| Directors | Min. 2 directors, majority must be resident in Mauritius | At least 2 resident directors required to satisfy substance |

| Local Presence | Registered office + licensed Management Company | Must be administered by an FSC-licensed Management Company |

| Capital | No statutory minimum; any currency | Shares may be issued in foreign currency |

| Privacy | Beneficial ownership disclosed to FSC; not on public register | Register of directors is filed but not fully public |

Focus Points

- Taxation: Corporate tax rate of 15% on net income; an 80% partial exemption may apply to qualifying income streams (dividends, interest, royalties), reducing the effective rate to 3%; standard VAT and withholding tax rules apply with possible treaty relief.

- Economic Substance: Must demonstrate core income-generating activities in Mauritius, maintain adequate employees or expenditure, and hold board meetings locally.

- Annual Compliance: Annual return, audited financial statements, and renewal of FSC licence required each year.

- Treaty Access: Eligible for Mauritius's DTA network, subject to satisfying substance and residency conditions under each treaty.

- Restrictions: Cannot conduct business with Mauritius residents or own immovable property locally.

Closing

A GBC suits holding structures, investment funds, regional headquarters, and IP-owning entities that require tax residency and treaty access. The 80% partial exemption on qualifying income is a material advantage; however, the mandatory substance requirements add ongoing operational costs that lighter offshore structures do not carry.

A GBC is best suited for internationally active businesses seeking Mauritius tax residency, treaty benefits, and a credible substance footprint for cross-border investment or holding activity.

Authorised Company (AC)

Mauritius Authorised Company registration falls under the Companies Act 2001, governed by the Financial Services Commission (FSC). Unlike the GBC, this structure is designed specifically for businesses that conduct activities and derive income entirely outside Mauritius. It holds separate legal personality, with liability limited to members' contributions.

Classified as a resident entity for Companies Act purposes but treated as non-resident for tax purposes, the AC occupies a distinct position in the corporate framework. This tax treatment means it falls outside the standard income tax net applicable to domestic companies.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Body corporate with separate legal personality | Limited liability applies |

| Members | Shareholders; minimum 1, no maximum | Corporate shareholders permitted |

| Directors | Minimum 1; no residency requirement | No maximum prescribed |

| Local Presence | Registered agent required; no physical office mandatory | Registered agent must be FSC-licensed |

| Capital | No minimum share capital; any currency permitted | Shares may be par or no-par value |

| Privacy | Beneficial ownership filed with FSC; not on public register | Register of members not publicly accessible |

Focus Points

- Taxation: Treated as non-resident for tax purposes; exempt from income tax on foreign-sourced income, not subject to VAT registration obligations, and no withholding tax on distributions to non-residents.

- Tax Treaties: No access to Mauritius's double taxation agreements, as the AC holds non-resident tax status.

- Economic Substance: No economic substance requirements apply, given income is derived entirely outside the jurisdiction.

- Annual Compliance: Annual return and financial summary must be filed with the FSC; full audited accounts are not required unless the FSC directs otherwise.

- Restrictions: Prohibited from conducting business with Mauritius residents or transacting in Mauritian rupees.

Recommendations

The AC suits holding structures, asset-holding vehicles, and businesses with no operational or client nexus to Mauritius, though the absence of treaty access limits its utility for tax planning relative to the GBC.

The Authorised Company is most appropriate for non-resident founders seeking a low-cost, administratively simple offshore vehicle with no requirement for local substance.

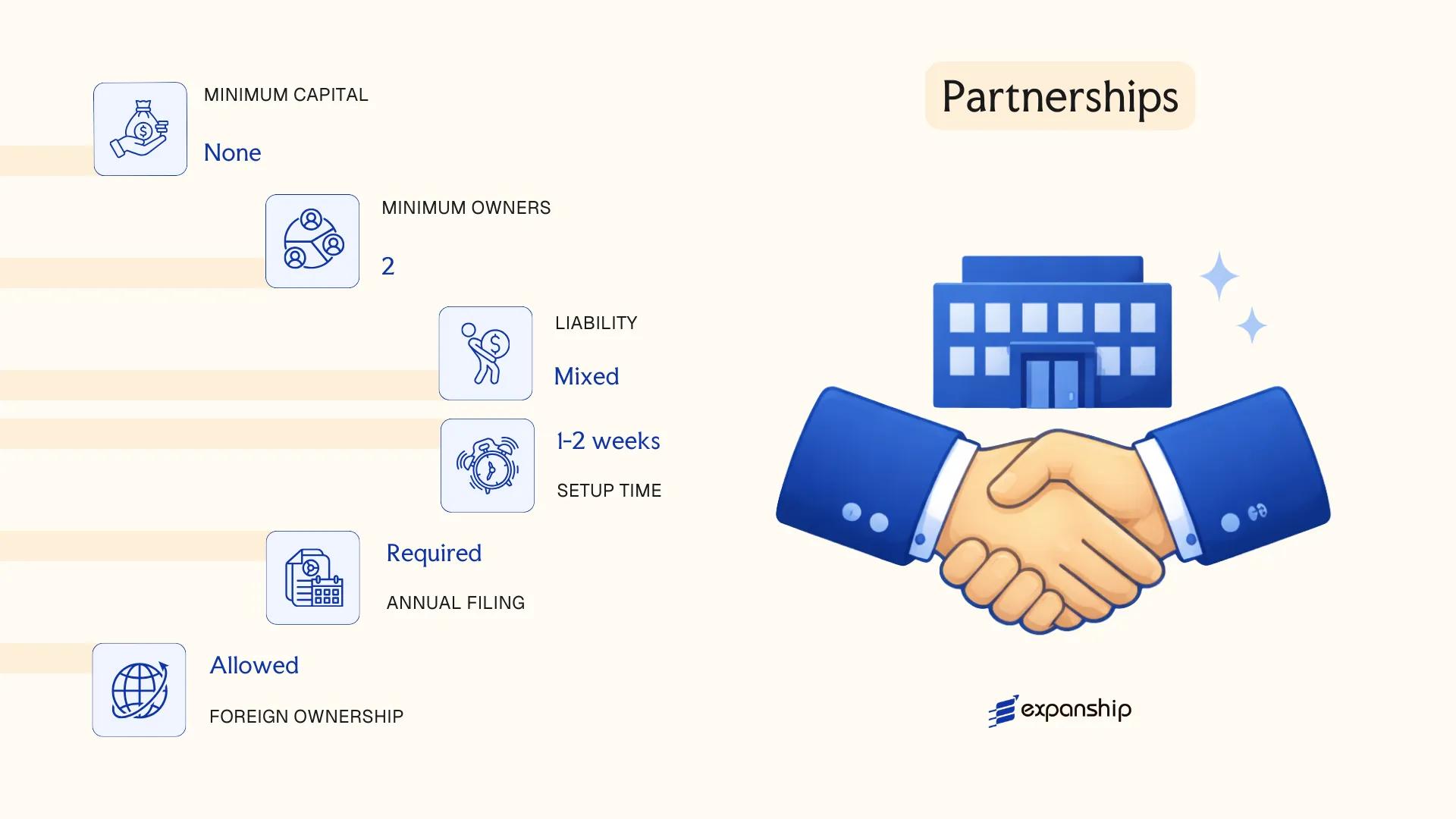

Partnerships [Limited Partnership, Limited Liability Partnership]

Mauritius limited partnership registration is governed by the Limited Partnerships Act 2011, which provides a framework distinct from general partnership law. A limited partnership (LP) is not a separate legal person under Mauritian law; it is a contractual arrangement between at least one general partner bearing unlimited liability and one or more limited partners whose exposure is capped at their contributed capital.

The Limited Liability Partnership Act 2016 introduced the LLP as a separate category, granting it full legal personality. This makes the LP vs LLP Mauritius distinction consequential: an LLP can hold assets, enter contracts, and sue in its own name, whereas an LP cannot. Both structures are registered with and regulated by the Registrar of Companies.

Key Characteristics

| Requirement | Limited Partnership (LP) | Limited Liability Partnership (LLP) |

|---|---|---|

| Legal Personality | None — contractual arrangement | Separate legal person |

| Partners / Members | Min. 1 general partner + 1 limited partner; no statutory maximum | Min. 2 partners (individuals or bodies corporate); no maximum |

| Liability | General partner: unlimited; Limited partner: capped at contribution | All partners: limited to agreed contribution |

| Local Presence | Registered agent and registered office required | Registered office and a resident manager required |

| Capital | No minimum; contributions can be cash or in-kind | No minimum prescribed |

| Privacy | Partnership agreement not publicly filed; partner details filed with Registrar | Partner details and manager details on public record |

Focus Points

- Taxation: Both LPs and LLPs are treated as tax transparent by default — income is assessed at the partner level; however, an LP may elect to be taxed as a company, triggering the standard 15% corporate tax rate; VAT registration obligations follow the same thresholds as other business forms.

- Economic Substance: Neither structure automatically triggers substance obligations, but partners holding a Global Business Licence introduce substance requirements at that licence level.

- Annual Compliance: Both structures must file an annual return with the Registrar; LLPs additionally must maintain and file financial statements.

- Treaty Access: LPs and LLPs do not independently access Mauritius's tax treaty network; treaty benefits depend on the residence and status of the individual partners.

- Restrictions: A limited partner in an LP who participates in management loses limited liability protection under the 2011 Act.

Sub-Types

Limited Partnership

Formed under the Limited Partnerships Act 2011, this structure operates without legal personality. It is used primarily as an investment vehicle or fund structure where the general partner manages assets and limited partners contribute capital passively.

Limited Liability Partnership

Established under the Limited Liability Partnership Act 2016, the LLP carries full legal personality and offers mutual limited liability to all partners. Professional services firms and joint ventures commonly use this form where shared management and liability protection for all participants are both required.

When to Use Partnership Structures

Partnership structures in Mauritius suit fund vehicles, professional practices, and joint ventures where pass-through tax treatment or flexible profit-sharing is a priority. The principal advantage of both forms is structural flexibility in profit allocation without mandatory share capital requirements. The key limitation is restricted treaty access — income flowing through these entities does not automatically qualify for Mauritius's double taxation agreements.

LPs are most appropriate for private equity and fund structures with passive investors; LLPs suit professional partnerships or joint ventures where all participants require limited liability.

Foreign Business Structures [Branch Office, Representative Office]

Mauritius branch office registration for a foreign company is governed by the Companies Act 2001, specifically the provisions applicable to foreign companies operating within the jurisdiction. A branch is not a separate legal entity — it is an extension of the parent company, which retains full liability for the branch's obligations. A representative office operates under similar principles but is structurally more restricted in what activities it may conduct.

Registration of a foreign company branch requires filing with the Registrar of Companies, including the parent company's constitutional documents, details of local agents, and a certified copy of the parent's financial statements.

Key Characteristics

| Requirement | Branch Office | Representative Office |

|---|---|---|

| Legal Form | Extension of foreign parent; no separate legal personality | Extension of foreign parent; no separate legal personality |

| Authorised Activities | Full commercial and trading operations permitted | Limited to liaison, marketing, and promotional activities; no revenue-generating activity |

| Local Presence | Must appoint a local agent resident in Mauritius; registered address required | Registered local address required |

| Capital | No prescribed minimum capital | No prescribed minimum capital |

| Financial Reporting | Parent's audited financials must be filed with the Registrar | Generally mirrors branch obligations |

| Privacy | Directors and agent details are on public record | Similar public disclosure applies |

Focus Points

- Taxation: The branch is taxed on Mauritius-sourced income at the standard corporate rate of 15%; VAT registration may apply depending on turnover thresholds; no separate withholding tax regime applies to branch profit remittances under domestic law, though treaty provisions may vary.

- Economic Substance: No formal substance requirement applies to branches in the same manner as GBCs, but the parent remains responsible for all liabilities incurred.

- Annual Compliance: Annual return and updated financial documents of the parent must be filed with the Registrar of Companies.

- Treaty Access: Branches generally do not qualify for treaty benefits under Mauritius's double taxation agreements, as treaty access typically requires resident entity status.

- Restrictions: A representative office cannot invoice clients, earn revenue, or enter into commercial contracts on its own account.

Closing Paragraph

A branch is commonly used by foreign firms seeking a direct operational presence without incorporating a new entity, while a representative office suits businesses in early market exploration phases. The primary advantage of both structures is speed and simplicity of setup; the key limitation is the absence of limited liability protection, leaving the parent fully exposed.

Best suited for established foreign companies testing the Mauritius market or managing regional operations directly through their parent entity.

Sole Proprietorship

Sole proprietorship registration in Mauritius is governed by the Business Registration Act 2002, administered by the Registrar of Businesses. Unlike incorporated entities, a sole proprietorship has no separate legal personality — the business and its owner are legally the same person, meaning personal assets are exposed to business liabilities without limit.

Registration is completed through the Business Registration Office, which issues a Business Registration Number (BRN). The process is relatively straightforward and carries low setup costs, making it a common entry point for self-employed individuals and micro-businesses operating domestically.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated business | No separate legal personality from the owner |

| Owner | Sole Proprietor | One individual only; no co-owners permitted |

| Local Presence | Registered business address required | Must maintain a physical address in Mauritius |

| Capital | No minimum capital requirement | Owner funds the business directly |

| Privacy | BRN and owner name on public register | Limited privacy; proprietor identity is disclosed |

| Liability | Unlimited personal liability | Personal assets at risk for all business debts |

Focus Points

- Taxation: Business income is taxed as personal income under the Income Tax Act; standard rates apply, with VAT registration required once annual turnover exceeds MUR 6 million; no separate corporate tax applies.

- Annual Compliance: Annual return filing with the Registrar of Businesses and tax return submission to the Mauritius Revenue Authority (MRA) are required.

- Conversion: A sole proprietorship can be converted into a private limited company, though the process requires fresh incorporation and does not carry over legal continuity automatically.

- Restrictions: Foreign nationals face restrictions operating as sole traders; this structure is generally reserved for Mauritian citizens and residents.

- Treaty Access: No access to double taxation agreements, as those apply to corporate entities, not unincorporated businesses.

Closing

A sole proprietorship suits local service providers, freelancers, and small-scale traders operating with minimal capital and low liability exposure. The absence of incorporation formalities reduces administrative burden, but unlimited personal liability remains a significant structural constraint.

Local sole traders, freelancers, and self-employed individuals conducting low-risk, domestic business activities with no plans for external investment.

How to Choose the Right Entity Type in Mauritius

Selecting the wrong structure under the Companies Act 2001 carries consequences that affect your tax position, regulatory standing, and operational capacity from day one — not just at the margins.

Why Your Entity Choice Matters

The structure you register shapes every compliance obligation that follows. Choosing incorrectly has concrete, documented consequences:

- Registering an Authorised Company or Global Business Company when your actual business activity targets local residents places you in breach of the Companies Act 2001, exposing the entity to striking off by the Registrar of Companies.

- Selecting a tax-exempt structure — such as an Authorised Company — disqualifies you from claiming withholding tax reductions under any of Mauritius's double taxation agreements, since treaty access requires tax residency.

- Operating through a structure subject to substance requirements without maintaining genuine local presence, employees, or board meetings triggers reporting failures and potential penalties under the Financial Services Act 2007.

- Using a share-based company structure for estate or succession planning binds you to annual shareholder obligations and statutory meetings that would not apply under a foundation or trust arrangement.

Key Factors to Consider

- Business Activity: Active trading, passive asset holding, and regulated sectors such as banking or collective investment schemes each fall under different licensing and structural requirements administered by the Financial Services Commission.

- Local vs. Offshore Operations: Transacting with Mauritius residents requires a domestic entity; purely cross-border operations may qualify for the GBC or AC regime.

- Tax Objectives: Your need for full exemption, treaty network access, or a specific partial exemption rate under the Income Tax Act 1995 will narrow your options to a small subset of entity types.

- Substance Capacity: If you cannot realistically maintain a registered office, local directors, and decision-making functions within the jurisdiction, you must select an entity type whose regulatory threshold matches that operational reality.

- Ownership and Management: Single-owner operations and multi-party joint ventures impose different governance requirements — a limited partnership or LLC offers management flexibility that a company structure does not.

- Exit Strategy: Redomiciliation, conversion between entity types, and voluntary winding-up procedures are not uniformly available across all structures registered with the Registrar of Companies.

Compliance Services for Companies in Mauritius

Ongoing compliance support for Mauritius-registered entities, including annual filings, statutory obligations, and Financial Services Commission requirements.

Conclusion

Mauritius offers a defined set of entity types, each designed for a specific commercial or administrative purpose. Setting up a company in Mauritius guide decisions typically begin with understanding this structure: the Global Business Company suits cross-border holding and investment activity under the Income Tax Act, while the Authorised Company serves non-resident businesses with no local dealings. Private companies limited by shares remain the standard vehicle for domestic trade, and limited partnerships provide flexibility for fund structures. The GBC is consistently the most registered entity type among international investors.

Regulation sits with the Financial Services Commission and the Registrar of Companies. Mauritius continues to expand its tax treaty network and align with OECD compliance standards, reinforcing its position as a mid-shore jurisdiction of substance. Your choice of structure will shape everything from tax residency to directorship obligations, making the Mauritius company formation summary a practical starting point for any cross-border planning exercise.

How Expanship Can Assist You

Expanship's Mauritius company incorporation services cover the full process — from selecting the right entity under the Companies Act 2001 to completing registration with the Registrar of Companies. Whether your goal is a Global Business Company regulated by the Financial Services Commission or a straightforward private company for domestic operations, your setup is handled by specialists who know the local framework.

From the first document to post-incorporation obligations, your business has support at every stage:

- Document preparation and notarization/legalization

- Registered agent and registered office provision

- Filing with the Registrar of Companies and FSC liaison where applicable

- Post-incorporation compliance management, including annual returns

- Corporate secretary services

- Banking introduction assistance

Ready to move forward? Reach out to Expanship Mauritius to discuss your requirements directly.

Frequently Asked Questions (FAQ)

The Private Company Limited by Shares (Ltd) is the most frequently incorporated structure. Its relatively low share capital requirements, flexible governance rules, and ability to trade locally make it the default choice for resident entrepreneurs and foreign investors operating domestically.

A GBC holds a licence issued by the Financial Services Commission and is designed for cross-border business, granting access to Mauritius's double tax treaty network. A private Ltd company is incorporated under the Companies Act 2001 and trades domestically without FSC licensing requirements. The compliance burden for a GBC is notably higher, including substance requirements and ongoing FSC reporting.

The Authorised Company (AC) offers the greatest degree of confidentiality, as its beneficial ownership details are not part of the public register. Nominee directors and shareholders are permitted. The AC is restricted from trading with Mauritius residents and must file an annual return with the Registrar of Companies, but financial statements are not publicly disclosed.

A sole proprietorship and a GBC each require only one individual to establish. Partnerships, by definition, require at least two partners under the Limited Partnerships Act 2011. Private and public companies have distinct minimum shareholder thresholds, with a public company requiring a minimum of seven shareholders.

Foreign nationals may incorporate most structures, including a GBC, AC, or private Ltd company, without a local residency requirement. A GBC requires FSC licensing and a registered agent holding a Management Company licence. For structures involving local trading, foreign investors must comply with the Non-Citizens (Employment Restriction) Act where employment of directors is concerned.

The Companies Act 2001 permits re-registration between certain company types, such as converting a private company to a public company. Conversion from a GBC to an AC, or vice versa, involves surrendering the existing FSC licence and applying for the new category. Not all conversions are straightforward, and tax treatment may change upon re-registration.

A private Ltd company, a public company, and sole proprietorships are all permitted to transact with local residents. A GBC and an AC are explicitly restricted from conducting business with residents or holding immovable property in Mauritius, under their respective FSC licence conditions.

A sole proprietorship carries the lightest compliance burden, requiring registration under the Business Registration Act 2002 but no annual financial statements filed with a regulatory body. Among incorporated structures, the private Ltd company with fewer than 25 shareholders is exempt from audit requirements under certain thresholds specified in the Companies Act 2001.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.