Key Takeaways

- St. Kitts and Nevis operates dual legislative tracks for company formation, with Nevis-specific entities governed by separate island ordinances including the Nevis Business Corporation Ordinance and the Nevis Limited Liability Company Ordinance.

- The Financial Services Regulatory Commission (FSRC) holds authority over corporate activity across the federation, while Nevis Island Administration ordinances create a parallel regulatory framework for offshore structures.

- Nevis offshore incorporation attracts the highest volume of international registrations within the federation, largely due to asset protection provisions unique to Nevis legislation.

- Neither capital gains tax nor inheritance tax is imposed at the federation level, with international business entities generally subject to favorable or zero-rate treatment on foreign-sourced income.

Introduction to Entity Types in St. Kitts and Nevis

St. Kitts and Nevis is a two-island federation in the eastern Caribbean, situated in the Lesser Antilles between Antigua and Barbuda to the southeast and Sint Eustatius to the northwest. It is an independent sovereign nation and a member of the Commonwealth, with each island operating distinct company legislation — a structural feature that directly shapes the available business entity types in St. Kitts and Nevis.

Company registration falls under the authority of the Financial Services Regulatory Commission (FSRC), which oversees corporate activity across the federation. Nevis-specific entities are additionally governed under Nevis Island Administration ordinances, creating a parallel but separate legal track for offshore structures.

From a tax standpoint, the federation imposes no capital gains tax and no inheritance tax, with international business entities generally subject to favorable or zero-rate treatment on foreign-sourced income.

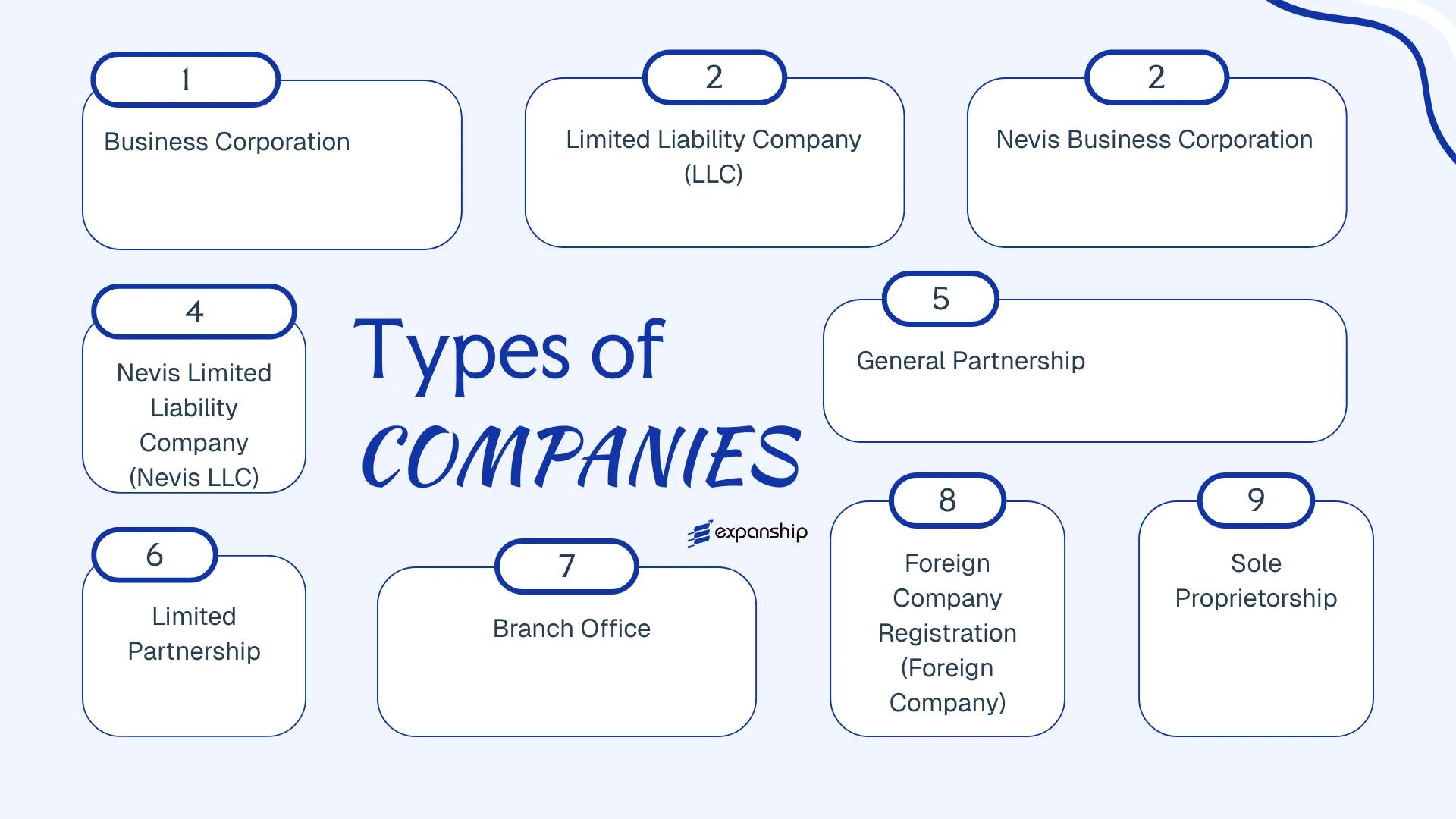

Businesses can be structured as one of the following:

- Business Corporation (Companies Act)

- Limited Liability Company

- Nevis Business Corporation

- Nevis Limited Liability Company

- General Partnership

- Limited Partnership

- Branch Office or Foreign Company Registration

- Sole Proprietorship

Each structure carries distinct formation requirements, liability treatments, and applicable legislation, all of which this article examines in turn.

An Overview of Business Structures in St. Kitts and Nevis

St. Kitts and Nevis offers multiple distinct entity types under two separate legislative frameworks — one governing Saint Kitts and the other specific to the island of Nevis. The primary federal statutes include the Companies Act (Cap 21.03) for Saint Kitts, while Nevis operates its own ordinances, notably the Nevis Business Corporation Ordinance and the Nevis Limited Liability Company Ordinance. Each structure carries different implications for liability, taxation, ownership, and permitted activities.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Business Corporation (St. Kitts) | Incorporated company | Limited | Taxed | Yes | 1 shareholder | Financial Services Regulatory Commission | Companies Act (Cap 21.03) |

| LLC (St. Kitts) | Limited liability company | Limited | Taxed | Yes | 1 member | Financial Services Regulatory Commission | LLC Act |

| Nevis Business Corporation | Incorporated company | Limited | Exempt (offshore) | No | 1 shareholder | Nevis Island Administration | Nevis Business Corporation Ordinance |

| Nevis LLC | Limited liability company | Limited | Exempt (offshore) | No | 1 member | Nevis Island Administration | Nevis LLC Ordinance |

| General Partnership | Unincorporated | Unlimited | Taxed | Yes | 2 partners | Registrar of Companies | Partnership Act |

| Limited Partnership | Hybrid | Mixed | Taxed | Yes | 1 GP + 1 LP | Registrar of Companies | Partnership Act |

| Branch Office | Extension of foreign entity | Parent liable | Taxed | Yes | N/A | Financial Services Regulatory Commission | Companies Act (Cap 21.03) |

| Sole Proprietorship | Unincorporated | Unlimited | Taxed | Yes | 1 person | Registrar of Companies | Business Names Act |

Each of these structures is examined in full in the sections below.

Business Corporation under the Companies Act

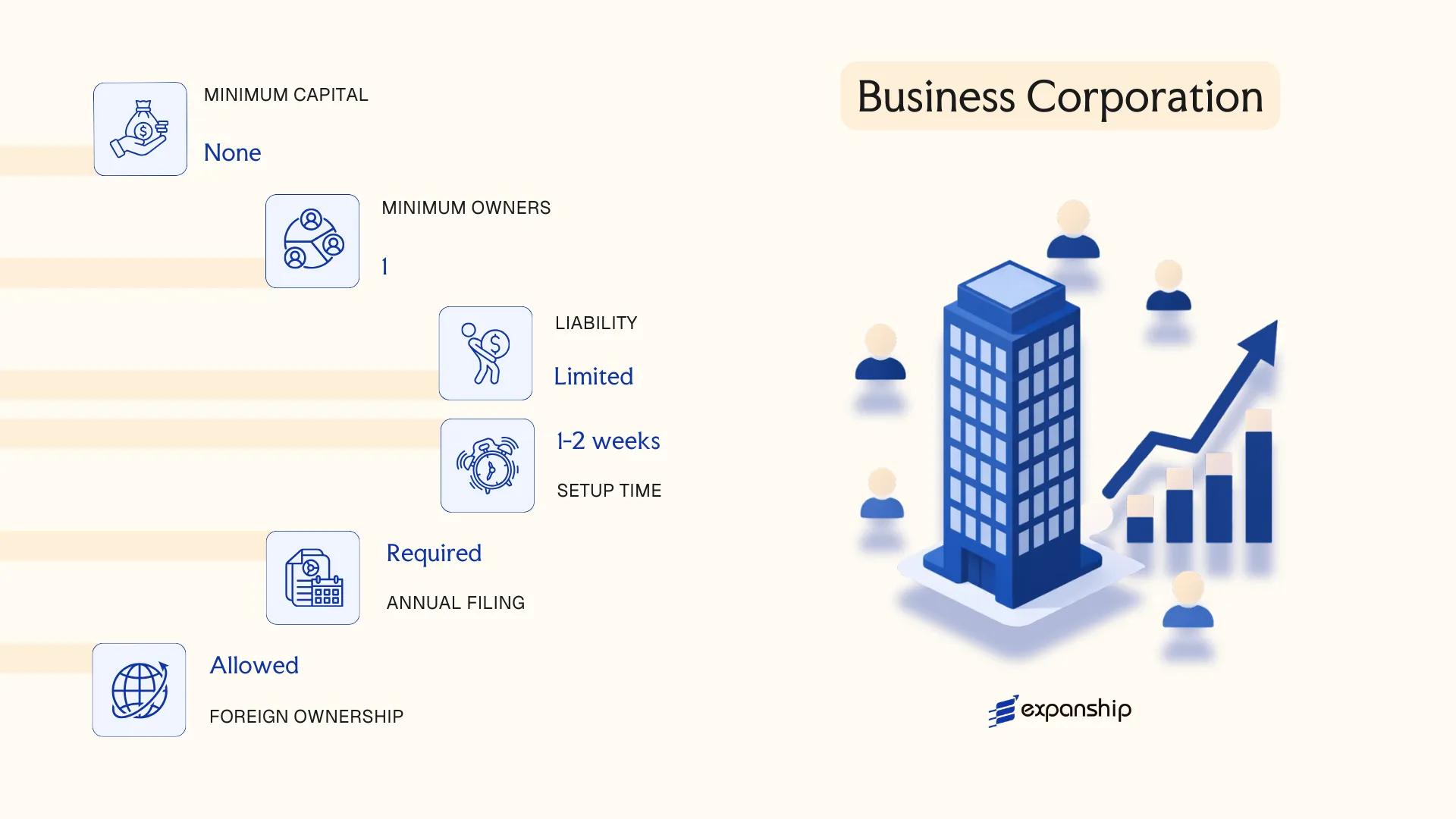

A St. Kitts Companies Act business corporation is governed by the Companies Act, Cap. 21.03, which applies to the island of Saint Kitts. Incorporated under this federal legislation, the entity carries separate legal personality distinct from its shareholders, meaning the company can own assets, enter contracts, and bear liabilities in its own name.

Limited liability extends to shareholders, whose exposure is confined to their unpaid share capital. This structure suits businesses seeking a domestically recognised legal form with full legal capacity under Saint Kitts law.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Incorporated company with separate legal personality | Governed by the Companies Act, Cap. 21.03 |

| Governance | Directors (min. 1) and Shareholders (min. 1, no maximum) | Directors and shareholders may be the same person |

| Local Presence | Registered office on Saint Kitts required | Registered agent appointment also required |

| Share Capital | No statutory minimum; denominated in Eastern Caribbean Dollar (XCD) or any currency | Shares may be issued with or without par value |

| Privacy | Director and shareholder names appear on public registry | No bearer shares permitted |

Focus Points

- Taxation: Saint Kitts does not impose corporate income tax, capital gains tax, or inheritance tax; however, certain business activities may attract other levies — consult the Inland Revenue Department for current obligations.

- Annual Compliance: Companies must file an annual return and maintain statutory registers; failure to comply can result in striking off.

- Economic Substance: Domestic companies conducting relevant activities may be subject to economic substance requirements under federal regulations.

- Treaty Access: Saint Kitts and Nevis has a limited network of double taxation agreements; treaty benefits should be verified before structuring any cross-border arrangements.

- Restrictions: Foreign ownership is generally permitted, though certain regulated sectors may impose local ownership or licensing conditions.

Closing

A Companies Act business corporation is suited to trading operations, domestic market activity, and holding structures where a locally incorporated entity is operationally or contractually required. One key advantage is full domestic legal recognition; the primary limitation is the reduced privacy compared to Nevis-based structures, given public registry disclosure.

Local or regionally focused businesses that require a federally incorporated entity with full domestic legal standing on Saint Kitts.

Company Incorporation in St. Kitts and Nevis

Incorporate a business corporation or other entity type in St. Kitts and Nevis with Expanship's end-to-end incorporation service.

Limited Liability Company (LLC)

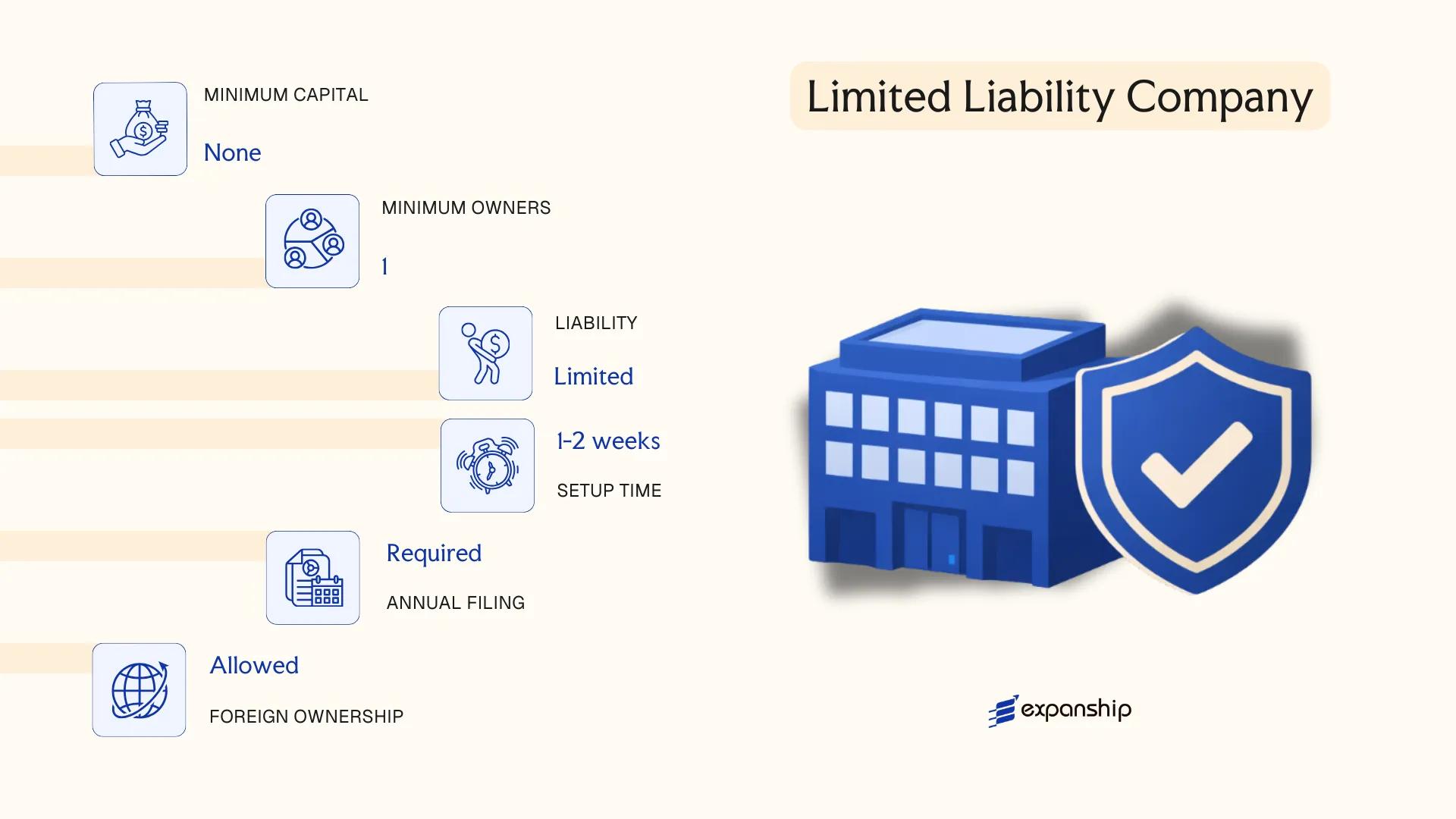

St. Kitts and Nevis LLC formation at the federal level is governed by the Companies Act of St. Kitts and Nevis, though the more internationally recognised LLC structure is administered at the island level under Nevis legislation. The LLC on the St. Kitts side functions as a hybrid entity, combining limited liability protection for its members with operational flexibility not typically available in a standard corporation.

Membership interests replace shares, and the entity maintains a separate legal personality distinct from its members. Management can vest in the members directly or be delegated to appointed managers, depending on how the operating agreement is structured.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Limited Liability Company | Separate legal personality; hybrid of corporate and partnership features |

| Members | Minimum 1; no statutory maximum | Members hold interests, not shares |

| Management | Member-managed or manager-managed | Defined in the operating agreement |

| Local Presence | Registered agent and registered office required | Must be maintained continuously |

| Capital | No mandatory minimum capital; Eastern Caribbean Dollar (XCD) | Capital contributions defined in the operating agreement |

| Privacy | Member details not required on public register | Operating agreement is a private document |

Focus Points

- Taxation: No corporate income tax, withholding tax, capital gains tax, or VAT applies to qualifying LLCs; stamp duty may apply to certain transactions.

- Economic Substance: Entities engaged in relevant activities must satisfy economic substance requirements under applicable legislation.

- Annual Compliance: Annual filing obligations apply, including renewal fees and maintenance of the registered agent.

- Treaty Access: St. Kitts and Nevis has a limited tax treaty network; confirm treaty eligibility before structuring cross-border arrangements.

- Conversion: Conversion from an LLC to another entity type is possible but requires regulatory approval and appropriate filings.

Closing

The LLC structure suits holding arrangements, family asset protection, and investment vehicles where pass-through treatment or flexible profit distribution is a priority. Its primary limitation is that the more developed and internationally recognised LLC framework resides under Nevis legislation rather than the federal St. Kitts framework, which can cause jurisdictional ambiguity for counterparties unfamiliar with the distinction.

This entity type works well for private investors and family offices seeking asset protection with flexible governance and no mandatory share capital requirement.

Nevis Business Corporation under the Nevis Business Corporation Ordinance

Governed by the Nevis Business Corporation Ordinance (NBCO), initially enacted in 1984 and subsequently amended, the Nevis Business Corporation (NBC) is one of the oldest offshore corporate structures in the Caribbean. The entity carries separate legal personality, meaning it can own assets, enter contracts, and incur liabilities in its own name, entirely distinct from its shareholders.

Nevis IBC formation under this ordinance is administered through a licensed registered agent based on the island of Nevis, as no direct filing with a government office is required from the incorporating party. The NBC Nevis offshore corporation structure is designed primarily for international business activity rather than domestic trade within the federation.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Corporation (separate legal entity) | Governed by the NBCO |

| Members / Officers | Shareholders, Directors, Officers | Minimum 1 shareholder, 1 director; no maximum; same person may hold all roles |

| Local Presence | Licensed Registered Agent and Registered Office on Nevis | Both mandatory; agent must be NBCO-licensed |

| Capital | No minimum share capital; denominated in any currency | Bearer shares are not permitted |

| Privacy | Shareholder and director details not on public record | Names do not appear in publicly accessible registries |

Focus Points

- Taxation: NBCs are exempt from corporate income tax, withholding tax, capital gains tax, and stamp duty on foreign-source income; no VAT applies to offshore activities.

- Annual Compliance: An annual fee is payable to maintain good standing; no requirement to file financial statements publicly.

- Economic Substance: NBCs engaged in relevant activities may be subject to economic substance obligations under the federation's substance legislation.

- Treaty Access: The federation has a limited tax treaty network; NBCs should not be assumed to qualify for treaty benefits without separate analysis.

- Conversion: An NBC may be continued, merged, or re-domiciled to or from another jurisdiction under provisions in the ordinance.

Closing

The NBC suits holding structures, international trading, and IP ownership arrangements where privacy and offshore income exemption are the primary requirements; the principal limitation is restricted treaty access and the growing application of substance rules to relevant activities.

Best suited for internationally active founders or investors seeking an established offshore corporate vehicle with asset protection features and no public disclosure of beneficial ownership.

Nevis Limited Liability Company (Nevis LLC) under the Nevis Limited Liability Company Ordinance

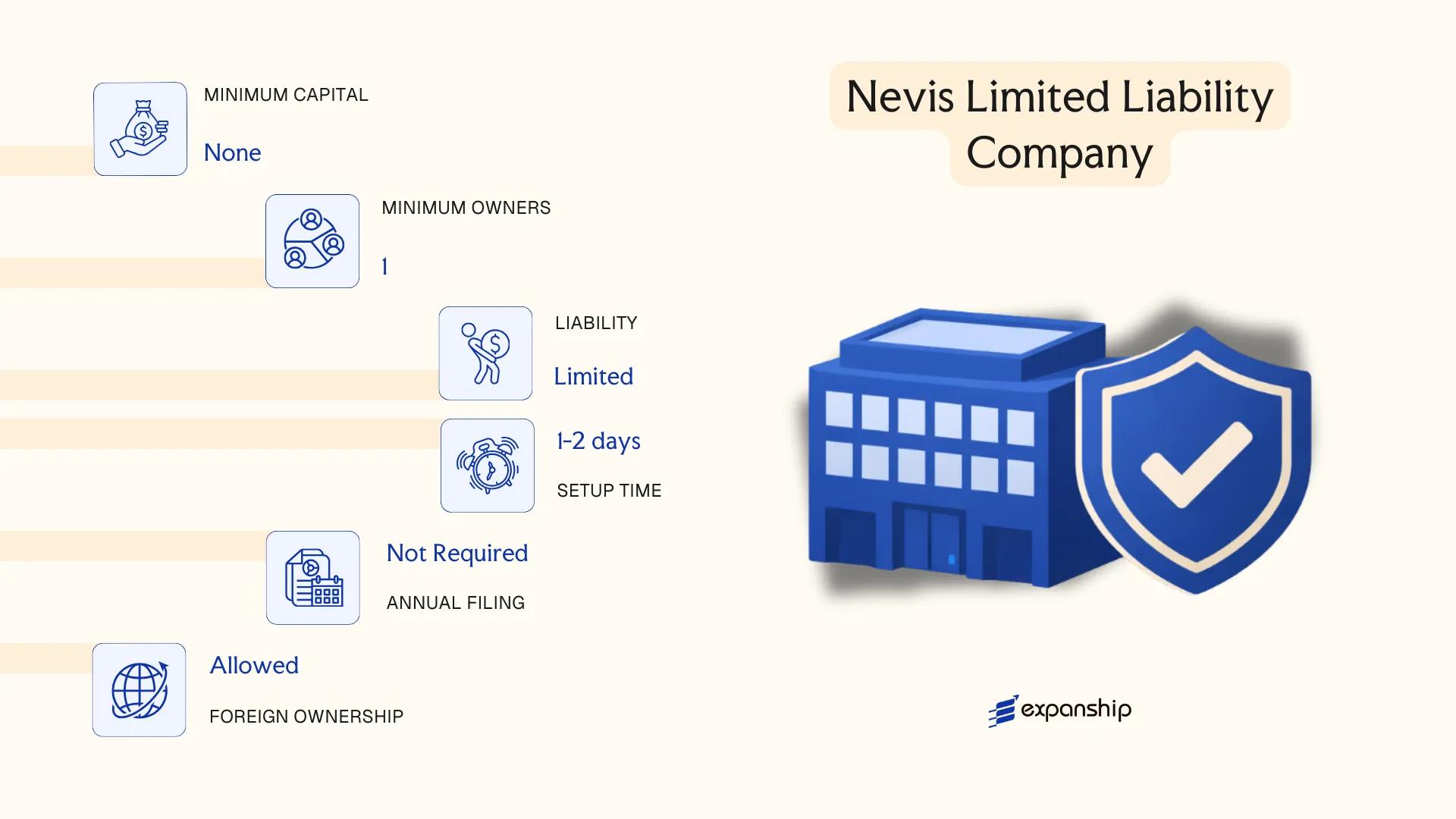

Governed by the Nevis LLC Ordinance limited liability company framework — formally, the Nevis Limited Liability Company Ordinance of 1995, as amended — the Nevis LLC is a hybrid entity that combines the limited liability protections of a corporation with the operational flexibility of a partnership. It holds separate legal personality, meaning it can own assets, enter contracts, and incur obligations in its own name.

Membership interests are not considered corporate stock, and the entity is not bound by the rigid governance requirements that apply to corporations. This structural distinction makes it a formation of choice for Nevis LLC offshore formation purposes, particularly for asset-holding and investment structures.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Limited Liability Company | Separate legal personality; hybrid structure under the Nevis Limited Liability Company Ordinance |

| Members | Referred to as Members; minimum 1, no maximum | Can be individuals or legal entities; no residency requirement |

| Managers | Optional; can be member-managed or manager-managed | Managers need not be members or residents |

| Local Presence | Registered Agent required in Nevis | No requirement for a local office beyond the registered agent |

| Capital | No minimum capital requirement; no specified currency | Contributions may be cash, property, or services |

| Privacy | Member and manager names are not filed in any public register | Confidentiality is a structural feature of the ordinance |

Focus Points

- Taxation: No corporate income tax, withholding tax, capital gains tax, or VAT applies to a Nevis LLC conducting business outside the island federation; stamp duty obligations are minimal.

- Economic Substance: Entities not conducting relevant activities as defined under CARICOM-aligned substance rules are generally not subject to substance requirements, but professional advice should be confirmed per activity type.

- Annual Compliance: An annual fee is payable to maintain good standing; no public financial statements are required.

- Charging Order Protection: Under the ordinance, a creditor of a member is limited to a charging order against distributions, not direct seizure of LLC assets — a key Nevis LLC asset protection feature.

- Conversion: The ordinance permits continuation and domestication of foreign entities into a Nevis LLC structure.

Closing

The Nevis LLC is used predominantly for holding assets, investment vehicles, IP ownership, and estate planning structures where confidentiality and creditor protection are priorities. Its primary limitation is that some counterparties and financial institutions in high-regulation jurisdictions may apply additional scrutiny to entities incorporated in Nevis.

The Nevis LLC suits non-resident individuals and holding structures requiring strong statutory asset protection and operational privacy without ongoing public disclosure obligations.

Partnerships (General Partnership, Limited Partnership)

St. Kitts and Nevis limited partnership registration falls under separate legislative frameworks depending on which island's law governs the entity. On the federal side, the Companies Act Cap 21.03 addresses general partnerships, while Nevis administers limited partnerships through the Nevis Limited Partnership Ordinance.

General partnerships carry no separate legal personality — partners bear unlimited joint and several liability for the firm's obligations. A Nevis limited partnership, by contrast, provides liability protection for limited partners, restricting their exposure to the amount of their capital contribution.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Partnership (contractual) | General partnership has no separate legal personality; Nevis LP does |

| Members | General partners (unlimited liability); limited partners (LP only) | Minimum one general partner required in an LP; no statutory cap on limited partners |

| Local Presence | Registered Agent and Registered Office required | Must be maintained on Nevis for Nevis LP |

| Capital | No statutory minimum; no prescribed currency | Capital contributions defined in the partnership agreement |

| Privacy | Partner names not on public register for Nevis LP | General partnership partners may be more exposed depending on registration filings |

Focus Points

- Taxation: No corporate income tax, capital gains tax, withholding tax, or VAT applies to qualifying partnerships; tax treatment flows through to partners individually.

- Annual Compliance: Nevis LPs must maintain a registered agent and file annual renewal fees; no public financial statements required.

- Economic Substance: Partnerships engaged in relevant activities may be subject to economic substance obligations under applicable regulations.

- Conversion: Nevis LP legislation generally permits conversion to other Nevis entity types, subject to Registrar approval.

- Restrictions: A general partner in a Nevis LP retains unlimited liability; appointing a corporation as general partner is a common structural mitigation.

Sub-Types

General Partnership

All partners participate in management and carry unlimited personal liability. This structure suits smaller domestic arrangements where partners accept shared responsibility without a formal corporate shield.

Nevis Limited Partnership

At least one general partner manages the firm while limited partners remain passive investors protected from liability beyond their contributed capital. This structure is commonly used for investment funds, family wealth vehicles, and asset-holding arrangements.

Closing

Nevis LP formation requirements make the structure particularly suited to investment holding and private fund arrangements where investor liability protection is required, though the mandatory general partner with unlimited liability remains a structural constraint that requires deliberate planning.

Nevis limited partnerships are best suited to private investment structures, family offices, and fund vehicles where passive investors require statutory liability protection.

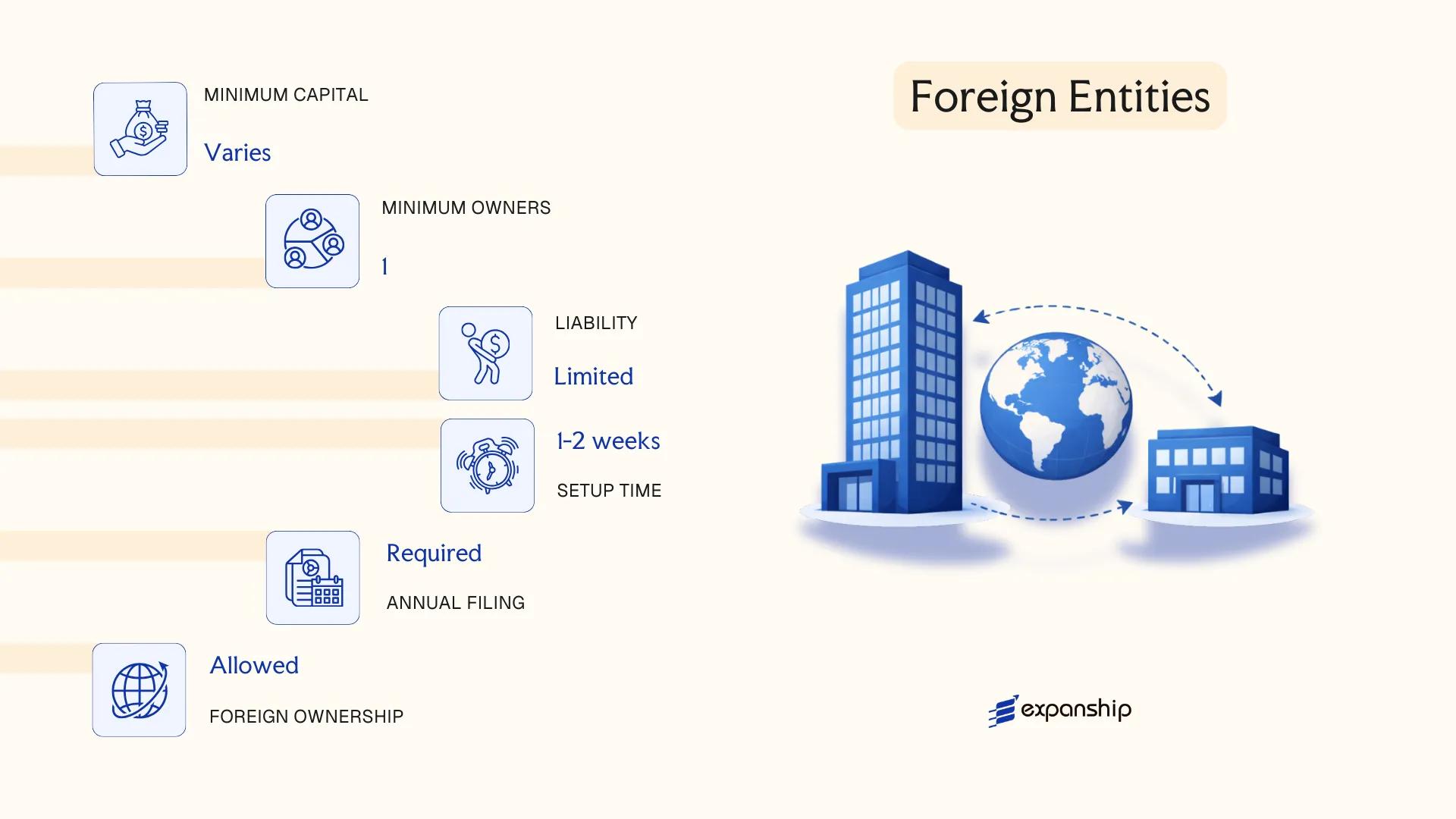

Foreign Entities (Branch Office, Foreign Company Registration)

Foreign company registration in St. Kitts and Nevis is governed primarily by the Companies Act Cap 21.03 for entities registering on the island of St. Kitts, while the Nevis Business Corporation Ordinance and related Nevis legislation govern overseas companies operating under Nevis jurisdiction. A foreign entity does not form a new legal person distinct from its parent — it remains an extension of the parent company, which retains full legal liability for the branch's obligations.

Registering an overseas company in Nevis or St. Kitts requires the foreign firm to file certified constitutional documents from its home jurisdiction along with particulars of its directors and a designated registered agent locally.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Branch / Registered Foreign Company | Not a separate legal entity; parent bears full liability |

| Representatives | Authorised Agent or Local Representative | Must be appointed to accept service of process |

| Local Presence | Registered Agent and Registered Office required | Mandatory under both St. Kitts and Nevis frameworks |

| Capital | No separate minimum capital requirement | Parent company's capitalisation applies |

| Privacy | Directors of parent company disclosed on registration | Home jurisdiction documents become part of local filing |

Focus Points

- Taxation: No corporate income tax, capital gains tax, or withholding tax applies locally; the branch's tax exposure is generally determined by the parent's home jurisdiction obligations.

- Annual Compliance: Annual renewal filings and maintenance of a registered agent are required to keep the registration in good standing.

- Economic Substance: Trading branches of foreign entities may be subject to substance considerations depending on the nature of activities conducted locally.

- Treaty Access: The federation's limited tax treaty network means foreign branches should not assume automatic treaty benefits from the parent's home country treaties.

- Restrictions: Certain regulated sectors (banking, insurance, financial services) require additional licensing beyond basic foreign company registration.

Closing

A registered foreign company structure suits businesses that need a formal local presence for contracting or operational purposes without establishing a separate subsidiary. The primary advantage is administrative simplicity; the clear drawback is that the parent entity remains fully exposed to liabilities incurred by the branch.

Foreign businesses requiring a local operational footprint or contractual standing in the federation without restructuring their existing corporate group.

Sole Proprietorship

A sole proprietorship in St. Kitts and Nevis is the simplest business structure available to individual operators. Registration is governed by the Business Names Registration Act, which requires any person trading under a name other than their own legal name to register that business name with the Registrar of Companies.

Unlike incorporated entities, a sole proprietorship carries no separate legal personality. The owner and the business are treated as one and the same in law, meaning personal assets remain fully exposed to business liabilities.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated | No separate legal personality from the owner |

| Owner Title | Proprietor | Single individual; no partners or shareholders |

| Liability | Unlimited personal liability | Personal assets are directly at risk |

| Local Presence | Registered business address required | Registration filed with the Registrar of Companies |

| Capital | No minimum requirement | Denominated in Eastern Caribbean Dollars (XCD) |

| Privacy | Business name publicly registered | Owner's identity linked to the registration |

Focus Points

- Taxation: No separate corporate tax applies; income is assessed as personal income of the proprietor. No VAT registration is required below the statutory threshold.

- Annual Compliance: Business name registration must be renewed periodically with the Registrar; failure to renew can result in deregistration.

- Economic Substance: No economic substance obligations apply to sole proprietorships.

- Conversion: A sole proprietorship can be converted into an incorporated entity, though the process requires new registration rather than a structural amendment.

- Treaty Access: This structure does not access tax treaty benefits available to corporate entities.

Recommendations

A sole proprietorship suits small-scale, locally focused operations where simplicity and low administrative cost take priority over liability protection. The primary drawback is unlimited personal liability, which makes this structure unsuitable for any activity carrying meaningful financial or legal risk.

Local sole traders and self-employed individuals conducting low-risk, single-person operations in St. Kitts and Nevis.

How to Choose the Right Entity Type in St. Kitts and Nevis

Knowing how to choose a business entity in Nevis or St. Kitts requires more than comparing registration fees. The structure you select has direct legal, tax, and operational consequences that are difficult to reverse once the entity is active.

Why Your Entity Choice Matters

- Registering a Nevis Business Corporation or Nevis LLC as an offshore, tax-exempt entity while conducting trade with local residents places the company in breach of the applicable Ordinance and exposes it to penalties or striking off.

- Opting for a tax-exempt structure to avoid local taxation also disqualifies the entity from claiming benefits under any double taxation arrangement St. Kitts and Nevis holds, since exempt entities are generally excluded from treaty eligibility.

- Forming a standard company when a trust or foundation structure would serve asset protection goals binds you to annual shareholder meeting obligations, director filings, and register maintenance requirements that do not apply to those alternative structures.

Key Factors to Consider

- Business Activity: Passive asset-holding, active trading, and regulated sectors such as banking or insurance each require a distinct structure under the applicable Companies Act or Nevis Ordinance.

- Local vs. Offshore Operations: Transacting with residents of the Federation requires a locally registered entity; operating exclusively outside it opens eligibility for offshore structures under the Nevis Business Corporation Ordinance or the Nevis Limited Liability Company Ordinance.

- Tax Objectives: Full exemption, territorial taxation, and treaty access are mutually exclusive in certain structures, so your tax position must align with the entity type from the outset.

- Privacy Requirements: Nevis offshore structures permit greater confidentiality than entities registered on the St. Kitts public register, particularly where nominee arrangements are used.

- Substance Capacity: If you cannot maintain physical presence, staff, or decision-making within the jurisdiction, choose a structure that does not trigger substance requirements under applicable reporting frameworks.

- Exit Strategy: Redomiciliation and conversion rights differ across entity types; the Nevis Business Corporation Ordinance permits continuance out of the jurisdiction, whereas other structures may not.

Corporate Compliance Services in St. Kitts and Nevis

Maintain good standing, meet annual filing obligations, and satisfy regulatory requirements for your entity under the applicable St. Kitts and Nevis legislation.

Conclusion

St. Kitts and Nevis offers a well-defined set of structures for incorporating in St. Kitts and Nevis, each serving distinct purposes. The Nevis Business Corporation suits non-resident shareholders seeking asset protection under the Nevis Business Corporation Ordinance. A Nevis LLC, governed by the Nevis Limited Liability Company Ordinance, appeals to those prioritizing flexible membership arrangements and charging order protections. Domestic companies under the Companies Act serve resident-facing commercial activity. Partnerships and sole proprietorships remain appropriate for smaller, locally oriented operations. Branch registrations allow foreign firms to establish a presence without forming a separate legal entity.

Nevis offshore incorporation continues to attract the highest volume of international registrations within the federation, driven primarily by the asset protection provisions specific to that island's legislation.

Regulatory oversight has trended toward greater transparency in recent years, with ongoing updates to beneficial ownership requirements shaping how structures are maintained. Expanship's team works directly within these frameworks to guide your formation decisions.

How Expanship Can Assist You

Expanship company formation St. Kitts and Nevis covers every structure discussed in this blog — from a Nevis LLC formed under the Nevis Limited Liability Company Ordinance to a domestic business corporation registered with the Registrar of Companies. Each entity type carries distinct filing requirements, and working with a knowledgeable service provider reduces the risk of procedural delays or non-compliance from the outset.

Expanship's service scope across both islands includes:

- Document preparation and notarization or apostille legalization

- Registered agent and registered office provision

- Filing and liaison with the Registrar of Companies or the Nevis Island Administration

- Post-incorporation compliance management, including annual returns

- Banking introduction assistance

Reach out through Expanship KN to discuss which structure fits your business objectives.

Frequently Asked Questions (FAQ)

The Nevis LLC, formed under the Nevis Limited Liability Company Ordinance, is among the most frequently registered structures, largely due to its flexible membership rules and the absence of a corporate tax at the entity level for non-resident business. Its combination of liability protection and minimal mandatory filings makes it a practical default for international operators.

A Nevis LLC is not required to pay local corporate tax on foreign-sourced income, whereas a St. Kitts Business Corporation incorporated under the Companies Act is subject to domestic tax obligations and can trade locally. Compliance requirements also differ: the Business Corporation carries more formal annual obligations, including audited accounts in certain cases, while the Nevis LLC operates under a lighter disclosure regime.

The Nevis Business Corporation (NBC), governed by the Nevis Business Corporation Ordinance, does not require public disclosure of shareholder or director identities. Nominee directors and shareholders are permitted, and the registered agent holds the principal information confidentially. Beneficial ownership details are not part of any public registry under current Nevis law.

A single individual can form a Nevis LLC or NBC, as both permit sole membership and sole directorship respectively. General partnerships, however, require at least two partners by definition. Limited partnerships under Nevis law similarly require at least one general partner and one limited partner.

Non-residents may register a Nevis LLC, NBC, or a St. Kitts Business Corporation without restriction on nationality. Foreign individuals and corporate entities are equally eligible as shareholders, members, or directors across most structures. Branch office registration for a foreign company is also available, subject to filing requirements under the Companies Act.

Nevis legislation permits continuation, allowing a foreign entity to re-domicile into a Nevis LLC or NBC. Conversion between a domestic Business Corporation and a Nevis structure is not a straightforward statutory process and typically requires dissolution and re-incorporation. Professional legal guidance is necessary to assess the most appropriate route.

The Nevis LLC carries the lightest ongoing requirements: no mandatory annual general meeting, no public filing of accounts, and a single annual fee payable to the registered agent. By contrast, a St. Kitts Business Corporation must meet more formal annual maintenance requirements under the Companies Act. The NBC sits between the two in terms of formality.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.