Key Takeaways

- Marshall Islands entities governed by the Business Corporations Act operate under a framework with virtually no bilateral tax treaties, forcing structuring advisors to rely on domestic exemptions rather than treaty protections when managing cross-border tax exposure.

- The jurisdiction's historically limited FATF standing increases the due diligence burden on beneficial owners, as correspondent banking relationships become harder to establish and maintain when counterparty banks flag the registration address.

- Without a publicly recognized stock exchange or substantive local banking infrastructure, Marshall Islands companies face material barriers to raising institutional capital or opening operating accounts in jurisdictions with stricter onboarding requirements.

- OECD-driven economic substance pressures mean that passive holding structures incorporated here cannot simply rely on a registered agent address — demonstrable local activity may now be required to avoid reclassification or penalties in the beneficial owner's home jurisdiction.

Marshall Islands operates under a lightly regulated offshore framework, governed primarily by the Business Corporations Act and administered through the Registrar of Corporations. That regulatory posture attracts a specific type of formation activity — but it also produces a defined set of disadvantages of incorporating in Marshall Islands that foreign business owners should assess before committing to the jurisdiction.

Those disadvantages span banking access, international compliance exposure, tax treaty limitations, and market restrictions, each addressed in its own section of this article.

Not every drawback will apply equally to your situation. A holding company with no active trade faces a different compliance profile than a firm conducting transactions with EU counterparties or seeking institutional financing.

This article is most relevant to foreign entrepreneurs, fund managers, and corporate structuring advisors evaluating whether an offshore entity here aligns with their operational and regulatory requirements.

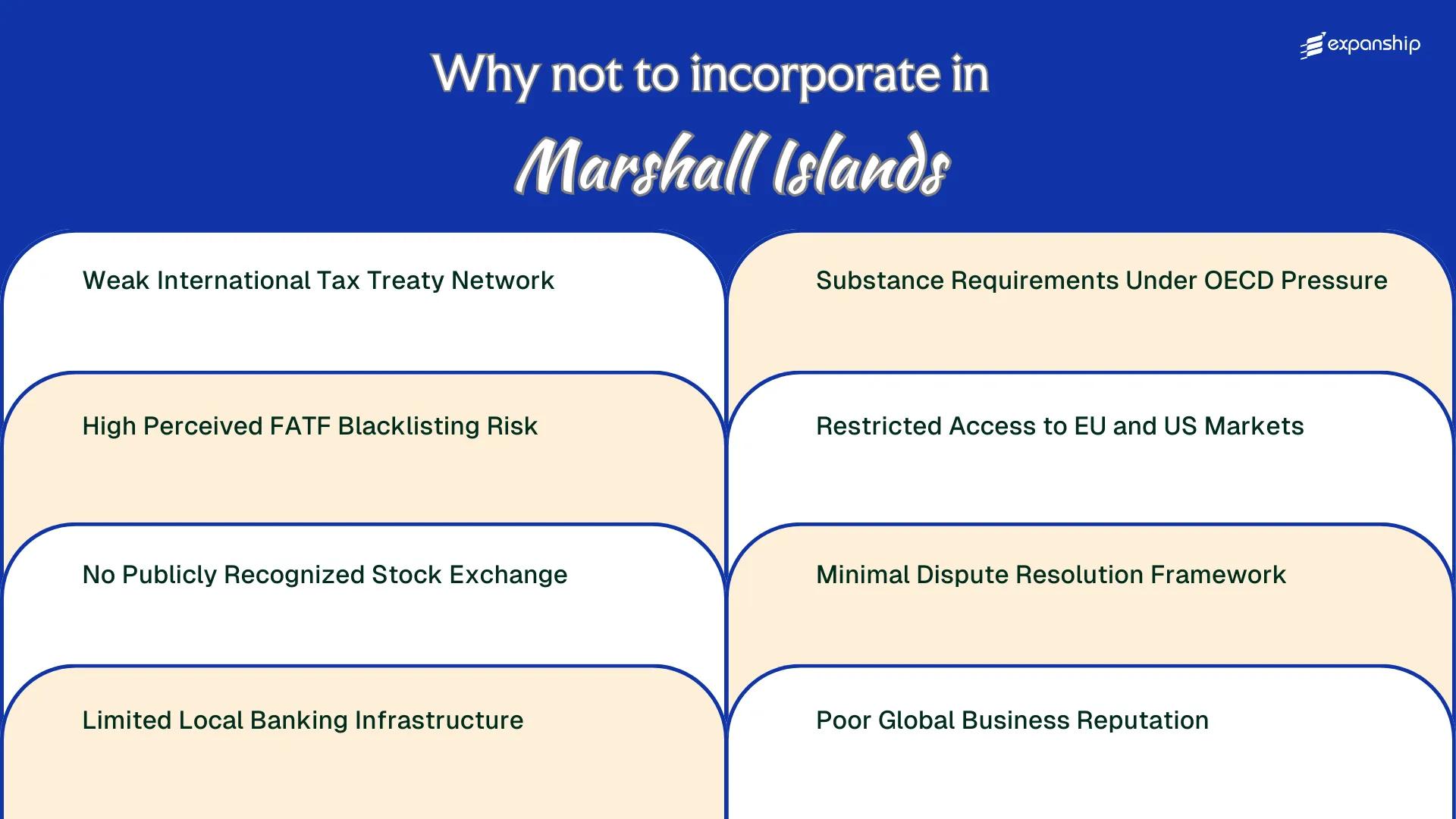

Weak International Tax Treaty Network

Marshall Islands tax treaty limitations create a structural gap that affects how your company's income is treated across borders. The Republic of the Marshall Islands has not signed any comprehensive bilateral double taxation agreements with major economies.

No Treaty Protection for Cross-Border Income

Without a double tax agreement network, income flowing between a Marshall Islands entity and counterparties in the US, EU, or Asia receives no treaty-based withholding tax reductions. Dividend, royalty, and interest payments to or from the company may be subject to full statutory withholding rates in the counterparty country, which can reach 25-30% in jurisdictions such as Germany or Canada.

This absence is not incidental. Operating without treaty coverage means your business cannot claim reduced withholding rates, permanent establishment protections, or tax credit mechanisms that treaty-resident companies routinely access.

Compounding Exposure for Active Businesses

Marshall Islands offshore tax risks intensify when your firm conducts genuine commercial activity, since source-country taxation applies without offset. Foreign tax authorities have no treaty obligation to recognize or defer to the entity's home jurisdiction treatment.

Without any bilateral double taxation treaty, your business bears the full withholding tax burden imposed by each counterparty country with no legal mechanism for relief or credit under international tax law.

High Perceived FATF Blacklisting Risk

Marshall Islands FATF blacklisting risk is not hypothetical. The Financial Action Task Force placed the jurisdiction on its grey list in 2022, citing deficiencies in anti-money laundering controls and the country's framework for combating the financing of terrorism.

Grey-listed status signals to foreign banks and regulators that your entity carries elevated scrutiny by association. Correspondent banks frequently apply enhanced due diligence to transactions involving firms registered there, which translates directly into slower payment processing and higher compliance costs on your end.

The practical friction this creates for a foreign business owner includes:

- Foreign banks may require additional documentation before opening accounts for your firm, extending onboarding timelines by weeks

- Marshall Islands money laundering concerns prompt partner businesses in regulated markets to request costly third-party compliance audits before signing contracts

- Payment processors and fintech platforms often exclude entities from grey-listed jurisdictions under their internal AML policies

- Marshall Islands AML compliance risks can trigger automatic transaction monitoring flags, causing routine wire transfers to be delayed or rejected

The Non-Cooperative Countries and Territories framework operated by the FATF does allow jurisdictions to exit the grey list once remedial measures are verified. Until that status changes, your business carries reputational exposure that has no straightforward workaround at the entity level.

Company Incorporation in Marshall Islands

Understand the full compliance picture before registering your entity in Marshall Islands.

No Publicly Recognized Stock Exchange

Marshall Islands no stock exchange limitations create a direct structural barrier for any company seeking access to public equity markets. No domestic stock exchange operates within the jurisdiction, and no regulatory framework exists under the Business Corporations Act (BCA) to oversee public securities listings or trading activity.

If your firm intends to raise capital from retail or institutional investors through a public offering, incorporation here provides no domestic platform to do so. You would need to cross-list on a foreign exchange, which introduces an entirely separate regulatory regime, additional compliance costs, and listing requirements set by bodies such as the SEC or the FCA.

| Requirement | Position for MH Companies |

|---|---|

| Domestic stock exchange | None |

| Local securities regulator | No dedicated capital markets authority |

| Public listing framework under BCA | Not provided |

| Cross-listing requirement for public fundraising | Mandatory via foreign exchange |

| Estimated cross-listing compliance cost (major exchange) | USD 500,000 or above for initial listing |

Even where a Marshall Islands company successfully lists abroad, the absence of a home capital markets regulator means no domestic oversight body validates or monitors ongoing disclosure obligations. Foreign exchanges treat these entities with additional scrutiny precisely because of this regulatory gap.

The practical consequence for early-stage or growth-focused businesses is that Marshall Islands capital markets restrictions place the full burden of investor access on external jurisdictions, multiplying both cost and administrative complexity.

Limited Local Banking Infrastructure

Marshall Islands banking infrastructure problems are not incidental — they reflect a structural gap that directly affects how your company operates internationally. The Republic has no central bank in the conventional sense; the US dollar circulates as the official currency under a compact arrangement with the United States, but there is no domestic monetary authority issuing policy or backstopping local financial institutions.

Only a small number of commercial banks operate onshore. This thin domestic presence means most Marshall Islands-registered entities cannot open or maintain a local account with any practical ease.

Correspondent banking relationships compound the problem. International banks routinely apply de-risking policies that exclude jurisdictions with limited regulatory oversight, and an entity incorporated here faces routine account refusals from major banking institutions in the EU, the UK, and North America.

Marshall Islands offshore banking restrictions effectively push businesses toward third-country banking arrangements, which introduce foreign exchange costs, reporting obligations, and delays that would not exist with a well-banked jurisdiction.

- No domestic central bank means no lender-of-last-resort protections for locally held funds

- Marshall Islands company bank account difficulties require establishing banking relationships in a third jurisdiction, adding compliance costs

- Correspondent banking risks apply even to accounts held outside the Islands if the incorporation jurisdiction triggers automated screening

- Account applications must typically demonstrate genuine economic activity to satisfy third-party bank due diligence requirements

Despite having no functioning domestic banking sector, Marshall Islands-registered entities are legally permitted to conduct all their banking operations entirely outside the jurisdiction with no statutory obligation to maintain a local account.

Substance Requirements Under OECD Pressure

Marshall Islands substance requirements challenges stem directly from the jurisdiction's offshore architecture, which was built for asset holding rather than genuine operational activity.

What the Pressure Looks Like in Practice

The OECD's Base Erosion and Profit Shifting framework, particularly Actions 5 and 6, targets jurisdictions where entities hold income without corresponding local activity. A Marshall Islands International Business Company that earns passive income or routes profits through the entity without local employees, management decisions, or physical presence may fail substance tests imposed by the tax authorities in your home country, not locally.

This creates a compliance burden that falls entirely on you, since the Republic of the Marshall Islands does not itself enforce economic substance rules of the kind adopted by jurisdictions such as the British Virgin Islands under their Economic Substance (Companies and Limited Partnerships) Act 2018.

Why Foreign Owners Bear the Risk

Your home jurisdiction's tax authority may recharacterize income earned through the entity, triggering additional tax liability, penalties, or disclosure obligations. BEPS compliance problems escalate when your business structure involves related-party transactions or intellectual property licensing routed through a firm with no verifiable local operations.

Assessing Substance Exposure for Your Marshall Islands Entity

Understand how OECD pressure and home-country substance rules may affect your Marshall Islands structure before committing to it.

Restricted Access to EU and US Markets

Marshall Islands EU market access restrictions create direct operational barriers for companies that need to conduct business within the European Union or access US capital markets. These limitations are structural, not incidental.

- The EU has previously listed the Marshall Islands as a non-cooperative jurisdiction for tax purposes under its Annex I list, which triggers automatic restrictions on fund flows, financing arrangements, and certain cross-border transactions for entities registered there.

- European institutional investors and fund managers operating under the Alternative Investment Fund Managers Directive (AIFMD) face heightened due diligence obligations when dealing with Marshall Islands-registered entities, increasing transaction costs and closing timelines.

- US financial institutions applying Bank Secrecy Act compliance standards treat Marshall Islands companies as elevated-risk counterparties, often requiring additional documentation that delays or prevents account opening.

- Correspondent banking restrictions tied to Marshall Islands non-cooperative jurisdiction drawbacks can prevent your firm from settling transactions in USD through US correspondent banks.

- EU public procurement rules effectively exclude entities from jurisdictions on the non-cooperative list, cutting off government contract opportunities across all 27 member states.

Minimal Dispute Resolution Framework

Marshall Islands dispute resolution limitations stem from a structural gap: the jurisdiction lacks a dedicated commercial court, specialist arbitration tribunal, or formal alternative dispute resolution (ADR) institution of its own. For a foreign business owner whose entity faces a contractual breach or investor conflict, this absence means disputes default to a generalist court system that has no established track record in complex cross-border commercial litigation.

The High Court of the Marshall Islands handles civil matters, but its capacity and caseload are not calibrated for sophisticated international commercial disputes. Enforcing a foreign judgment or arbitral award requires navigating a legal system with limited precedent in that area, which introduces uncertainty on timelines and outcomes.

Parties sometimes insert third-country arbitration clauses — specifying Singapore, London, or New York as the seat — precisely because the local legal framework weaknesses make domestic resolution unreliable. That workaround carries its own cost: separate legal representation across jurisdictions and arbitration institution fees that can run into tens of thousands of dollars before a hearing even begins.

A foreign investor pursuing a USD 200,000 contract dispute through a third-country arbitration seat such as the Singapore International Arbitration Centre (SIAC) could face filing fees, arbitrator fees, and legal costs collectively exceeding USD 40,000 to USD 60,000 — a disproportionate burden relative to the claim value, caused directly by the absence of a credible local dispute resolution mechanism.

Poor Global Business Reputation

Marshall Islands offshore reputation problems are not abstract. They stem from documented regulatory history that counterparties, banks, and institutional investors actively reference when assessing risk.

The jurisdiction has appeared on grey lists maintained by the Financial Action Task Force and the EU's list of non-cooperative tax jurisdictions at various points, creating a paper trail that compliance teams at foreign banks and law firms treat as a red flag regardless of current listing status.

Counterparty due diligence is where this disadvantage becomes operational. Many correspondent banks and institutional investors apply enhanced due diligence or outright refusal policies to entities registered in jurisdictions with Marshall Islands tax haven stigma risks, which directly raises your cost of opening accounts or closing commercial agreements.

Marshall Islands company credibility drawbacks surface most acutely in regulated sectors. If your business seeks licensing in finance, insurance, or professional services, regulators in jurisdictions such as the UK, Singapore, or the UAE routinely treat the registered address as a credibility signal, and an address in Majuro can trigger additional scrutiny or disqualification.

The Marshall Islands secrecy jurisdiction concerns attached to the International Business Corporations Act, which permits nominee structures and minimal disclosure, compound the reputational issue by associating the entity with opacity regardless of your actual compliance posture.

Even if your entity is fully compliant today, its registered jurisdiction carries historical listing records that third-party compliance systems may flag automatically, and clearing those flags requires documented evidence of substance and purpose that many straightforward commercial arrangements cannot easily provide.

Overcoming These Incorporation Drawbacks

Overcoming Marshall Islands incorporation drawbacks begins with accepting that no single fix resolves the full range of structural and reputational challenges this jurisdiction presents. Addressing them requires combining entity-level decisions with cross-border compliance planning.

- Establish economic substance in a recognized jurisdiction by maintaining genuine operations, employees, or management activities outside the Marshall Islands to satisfy OECD-aligned substance requirements.

- Register the IBC under a foreign law-governed shareholders' agreement to access dispute resolution mechanisms unavailable under the Business Corporations Act.

- Open corporate banking accounts through correspondent banking networks in jurisdictions with active FATF compliance records, offsetting the local banking infrastructure gap.

- Pair the IBC structure with a tax-resident intermediary entity in a jurisdiction that holds applicable double taxation treaties, addressing the absent treaty network.

- Conduct ongoing FATF grey list monitoring to anticipate compliance posture shifts that affect EU and US market access.

These steps operate within a regulatory environment governed by the Registrar of Corporations under the Marshall Islands Business Corporations Act. None of them eliminates the underlying jurisdictional constraints, which remain structural in nature.

Marshall Islands Still Worth It

Despite the disadvantages covered in this blog, the Marshall Islands remains a functioning incorporation jurisdiction under the Associations Law of 1990, with a well-established non-resident domestic corporation structure that continues to attract international holding companies and shipping entities. The question of whether Marshall Islands incorporation is still worth it depends entirely on how your business is structured and where it operates.

| Pros | Cons |

|---|---|

| No corporate income tax on offshore income for non-resident domestic corporations | No tax treaty network, limiting relief from withholding taxes in counterparty jurisdictions |

| Low incorporation and maintenance costs relative to comparable offshore jurisdictions | Limited local banking infrastructure forces reliance on correspondent banking arrangements abroad |

| Strong privacy provisions under the Associations Law of 1990 | Heightened FATF and OECD scrutiny increases compliance burden and reputational exposure |

| Flexible corporate structures with minimal statutory requirements | EU and US market access restrictions reduce operational utility for client-facing businesses |

| Established use in international shipping and vessel registration | Substance requirements under OECD pressure add cost for entities claiming tax residency benefits |

Suitability is not universal. The Marshall Islands company pros and cons reflect a jurisdiction built for holding structures, asset protection, and vessel ownership, not for businesses requiring active banking relationships, tax treaty access, or EU market entry.

Compliance Services for Companies in the Marshall Islands

Maintain good standing and meet ongoing regulatory obligations for your Marshall Islands non-resident domestic corporation.

Conclusion

A Marshall Islands company formation cons summary reflects a jurisdiction that offers structural simplicity under the Business Corporations Act but carries genuine operational costs. Banking access remains persistently difficult, the absence of tax treaties limits treaty-based planning, and FATF-related reputational exposure affects how counterparties, banks, and regulators in other countries treat your entity. These are not abstract concerns. Structural due diligence and jurisdiction-specific compliance planning determine whether a Marshall Islands IBC functions effectively within your broader corporate structure.

Expanship's Marshall Islands Incorporation Services

Expanship's Marshall Islands incorporation services are structured around the specific compliance pressures this jurisdiction produces. From managing substance documentation under OECD scrutiny to addressing the banking access difficulties that come with a high-risk offshore label, Expanship reduces the operational weight of these obligations without removing the underlying regulatory reality.

Beyond those core challenges, the firm supports your entity across the full incorporation and maintenance cycle:

- Preparing and filing all company registration documents with the Registrar of Corporations.

- Providing a registered agent and office address as required under Marshall Islands law.

- Handling government filings and liaising with relevant regulatory authorities on your behalf.

- Managing ongoing compliance obligations after your company is established.

- Introducing your business to suitable banking contacts to support account opening efforts.

- Assisting with tax registration and coordinating with local authorities where required.

Reach out through Expanship Marshall Islands to discuss what your structure requires.

Frequently Asked Questions (FAQ)

It affects companies differently depending on where their income originates and where their counterparties are based. A business with no operations or revenue streams in treaty-reliant jurisdictions faces fewer direct consequences, but any entity receiving dividends, royalties, or interest from countries that impose withholding taxes will bear the full statutory rate with no treaty reduction available. The Marshall Islands has signed virtually no comprehensive double taxation agreements, so the exposure scales directly with how internationally active your business is.

Non-compliance with the Marshall Islands Business Corporation Act substance provisions, introduced under pressure from the OECD's Base Erosion and Profit Shifting framework, can result in penalties, automatic information exchange with relevant tax authorities, and potential deregistration. The substance requirements apply specifically to entities conducting relevant activities such as holding company functions, intellectual property income, or shipping operations. Regulators in your home jurisdiction may also treat non-compliant structures as tax avoidance arrangements, triggering domestic penalties independently of anything the Marshall Islands authorities impose.

It is comparable to other jurisdictions on the EU's list of non-cooperative tax jurisdictions, but the combination of FATF greylisting history and OECD pressure makes the cumulative compliance burden heavier than jurisdictions that have resolved at least one of those issues. EU entities conducting business with a Marshall Islands company face mandatory disclosure requirements under DAC6 and similar directives. US counterparties applying FBAR and FATCA obligations will subject your entity to additional reporting scrutiny that adds friction to routine commercial transactions.

The cost depends on what activities your entity conducts, but for a holding company to satisfy substance requirements it typically needs local directors with relevant decision-making authority, documented board meetings held in-jurisdiction, and some level of local expenditure on office space or administration. Budget estimates for minimal but defensible substance arrangements in the Marshall Islands generally start in the range of several thousand US dollars annually, and that figure rises sharply if you need qualified resident personnel with genuine management responsibilities rather than nominee arrangements that regulators increasingly reject.

It is increasingly difficult. Major European and US correspondent banks have de-risked by restricting or refusing accounts for entities incorporated in jurisdictions with FATF greylisting history or that appear on the EU's list of non-cooperative jurisdictions for tax purposes. Some private banks and EMIs will still onboard Marshall Islands entities, but they typically impose enhanced due diligence requirements, higher minimum deposits, and ongoing transaction monitoring that smaller businesses may find operationally burdensome. The Marshall Islands' limited local banking infrastructure means you cannot easily substitute domestic banking for the international access that is being restricted.

The Marshall Islands introduced beneficial ownership disclosure obligations through amendments to its corporate legislation, and failure to maintain accurate records can result in administrative penalties and the entity being struck off the register. Penalties are applied by the Registrar of Corporations, and reinstatement after strike-off requires payment of outstanding fees plus compliance with the outstanding reporting obligations. Beyond domestic penalties, the broader risk is that non-compliance becomes discoverable through automatic information exchange under the Common Reporting Standard, exposing the beneficial owner to scrutiny in their home jurisdiction.

It is not adequate for high-value international commercial disputes. The Marshall Islands has no dedicated commercial court and a very limited judiciary, which means complex cross-border disputes cannot be resolved locally with the speed or specialization that sophisticated transactions require. Parties typically need to include arbitration clauses referring disputes to established seats such as Singapore, London, or New York, which adds cost and procedural complexity that would not exist if the entity were incorporated in a jurisdiction with a recognized commercial court system.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.