Key Takeaways

- The Business Corporation (BC) is the most widely registered entity in the Marshall Islands, offering non-residents a tax-neutral status and exemption from local reporting obligations under the Business Corporations Act.

- Corporate oversight in the Marshall Islands falls under the Registrar of Corporations, which has increasingly aligned its regulatory posture with FATF standards and beneficial ownership transparency requirements.

- Distinct structures such as the LLC, Limited Partnership, Non-Resident Domestic Corporation, and Charitable Foundation serve materially different purposes, from pass-through investment arrangements to asset protection and succession planning.

- Non-Resident Domestic Corporations occupy a narrower legal niche than Business Corporations, with specific ownership and operational constraints that distinguish them despite both targeting non-resident use cases.

Introduction to Entity Types in Marshall Islands

Located in the central Pacific Ocean, the Republic of the Marshall Islands is an independent sovereign nation situated between Hawaii and the Philippines, comprising two chains of atolls and islands. Governance over business registration falls under the Registrar of Corporations, which operates within the framework established by the Business Corporations Act and related legislation. Non-resident entities conducting business outside the jurisdiction are generally subject to a zero-tax regime on foreign-sourced income.

Several distinct business structures are available under Marshall Islands law, including the Business Corporation (BC), the Non-Resident Domestic Corporation (NRDC), the Limited Liability Company (LLC), the Limited Partnership (LP), the General Partnership, the Limited Liability Partnership (LLP), and various foreign-registered structures. Non-profit formations and charitable foundations also fall within the available options.

Each of these Marshall Islands entity types carries its own formation requirements, governance rules, liability provisions, and operational constraints. This article examines each structure in turn, covering the legal basis, ownership parameters, and practical considerations relevant to your business.

An Overview of Business Structures in Marshall Islands

The Marshall Islands Companies Act 1990, along with the Limited Liability Company Act 1996 and the Limited Partnership Act, collectively governs the range of legal entities available for formation in the jurisdiction. Seven principal structures are recognised under this framework, each designed to serve a distinct commercial, investment, or operational purpose. The sections that follow examine each in detail.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Business Corporation (BC) | Corporation | Limited | Exempt (non-resident) | No | 1 shareholder | Registrar of Corporations | Companies Act 1990 |

| Non-Resident Domestic Corporation (NRDC) | Corporation | Limited | Exempt (non-resident) | No | 1 shareholder | Registrar of Corporations | Companies Act 1990 |

| Limited Liability Company (LLC) | Hybrid entity | Limited | Pass-through / Exempt | Permitted | 1 member | Registrar of Corporations | LLC Act 1996 |

| Limited Partnership (LP) | Partnership | Mixed | Pass-through | Permitted | 1 GP, 1 LP | Registrar of Corporations | Limited Partnership Act |

| General Partnership (GP) | Partnership | Unlimited | Pass-through | Permitted | 2 partners | Registrar of Corporations | General law |

| Limited Liability Partnership (LLP) | Partnership | Limited | Pass-through | Permitted | 2 partners | Registrar of Corporations | General law |

| Non-Profit Corporation | Corporation | Limited | Exempt | Restricted | 1 director | Registrar of Corporations | Companies Act 1990 |

Each of these structures is examined in full in the sections below.

Marshall Islands Business Corporation (BC)

The Marshall Islands Business Corporation (BC) is governed by the Business Corporations Act (BCA) of 1990, which closely mirrors Delaware corporate law. Marshall Islands BC registration produces a separate legal entity distinct from its shareholders, with liability limited to each member's capital contribution.

Structured for international use, the BC can hold assets, enter contracts, and conduct business in its own name. Shares may be issued in registered or bearer form, though bearer shares are subject to specific custody requirements under current regulations.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Corporation (separate legal personality) | Governed by the Business Corporations Act, 1990 |

| Members | Shareholders (min. 1, no maximum) | Corporate shareholders permitted; nominee shareholders allowed |

| Management | Directors (min. 1, no maximum) | No residency requirement; corporate directors permitted |

| Local Presence | Registered Agent required | No requirement for a local office; agent must be RMI-based |

| Capital | No minimum share capital; USD common | Shares may be par value or no-par value |

| Privacy | Shareholder and director details not filed publicly | Register of directors maintained internally |

Focus Points

- Taxation: BCs conducting business solely outside the RMI pay no corporate income tax, withholding tax, VAT, or stamp duty under the RMI tax framework; domestic activities may attract local obligations.

- Economic Substance: BCs with no income-generating activity in the RMI generally fall outside substance requirements, but holding and IP structures should be reviewed against current OECD guidance.

- Annual Compliance: An annual fee is payable to the Registrar of Corporations; no annual financial statements or audit are required for non-resident BCs.

- Treaty Access: The RMI has a limited tax treaty network, which restricts the BC's utility for treaty-based structuring.

- Conversion: A BC may be converted into an LLC or re-domiciled to or from another jurisdiction under the BCA's continuance provisions.

Closing

The BC suits holding structures, international trading, and asset ownership where limited liability and privacy are priorities. Its main advantage is administrative simplicity with no minimum capital or public disclosure of ownership; the primary limitation is restricted access to tax treaties, which reduces its effectiveness for structures dependent on withholding tax relief.

Best suited for non-resident entrepreneurs and international investors seeking a straightforward, low-maintenance offshore corporate vehicle for holding or trading activities outside the RMI.

Company Incorporation in Marshall Islands

Incorporate a Business Corporation in the Marshall Islands with full registered agent support and compliance setup.

Registered Limited Liability Company (LLC)

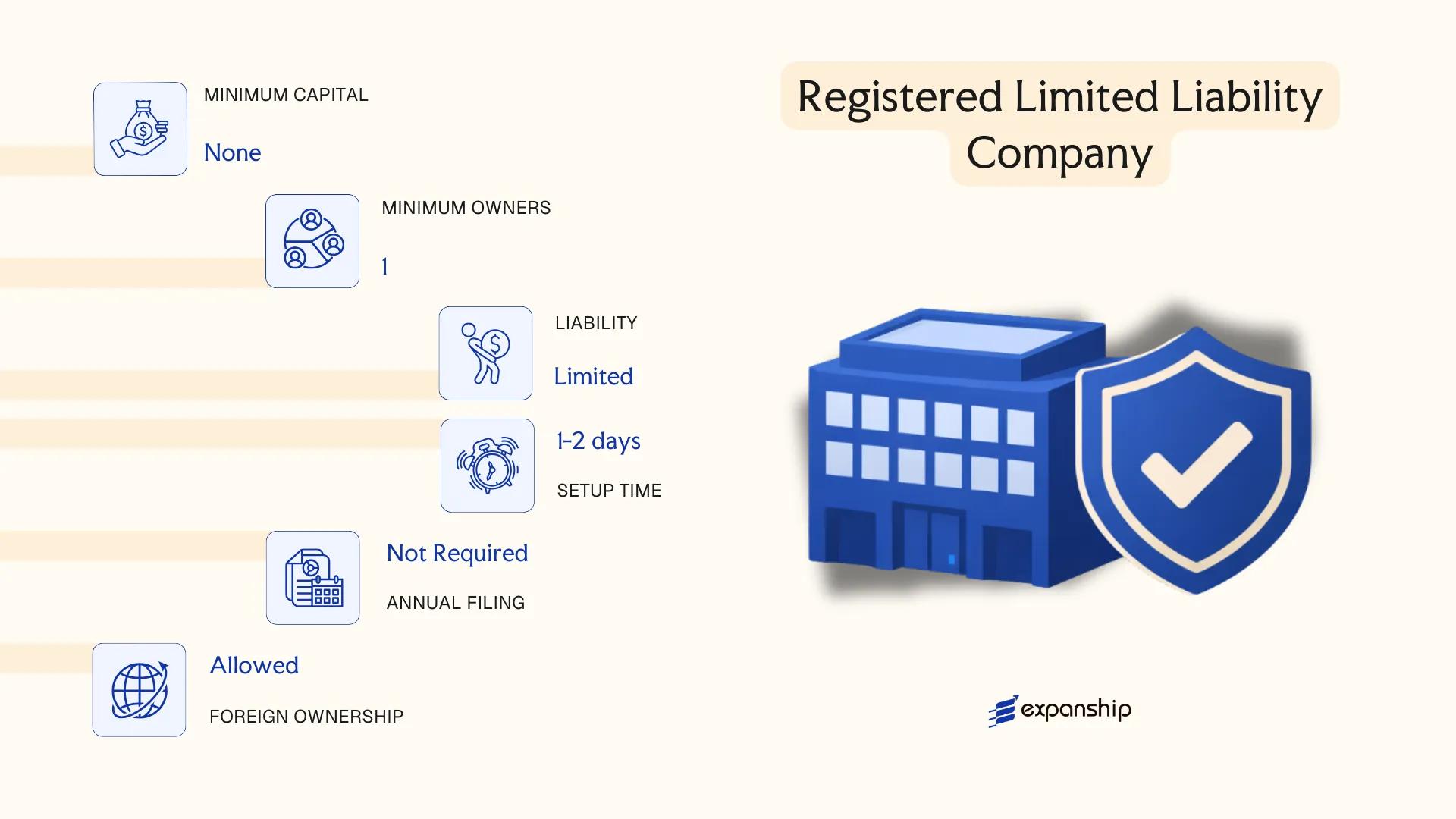

The Marshall Islands LLC is governed by the Limited Liability Company Act of 1996, enacted under the authority of the Republic of the Marshall Islands. This legislation establishes the LLC as a separate legal entity, meaning the company can hold assets, enter contracts, and incur liabilities in its own name, distinct from its members.

Structurally, the RMI LLC registration process produces a hybrid entity that combines the liability protection of a corporation with the operational flexibility typically associated with partnerships. Governance and profit distribution are determined by an operating agreement rather than statutory defaults, giving members considerable freedom to structure internal arrangements.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Limited Liability Company | Separate legal personality; governed by LLC Act 1996 |

| Members | Minimum 1; no maximum | Members may be individuals or corporate entities of any nationality |

| Management | Member-managed or Manager-managed | Determined by the operating agreement; managers need not be members |

| Local Presence | Registered Agent required | Must maintain a registered agent in the RMI; no physical office required |

| Capital | No minimum capital requirement | Contributions may be cash, property, services, or future obligations |

| Privacy | Member and manager names not filed publicly | Operating agreement is a private document |

Focus Points

- Taxation: The RMI imposes no corporate income tax, withholding tax, VAT, or stamp duty on LLCs conducting business exclusively outside the jurisdiction.

- Economic Substance: LLCs engaged in relevant activities as defined under RMI substance regulations may be subject to economic substance requirements.

- Annual Compliance: An annual renewal fee is payable to maintain good standing; no financial statements are required to be filed publicly.

- Treaty Access: The RMI has a limited tax treaty network, which may restrict access to reduced withholding rates in other jurisdictions.

- Conversion: An LLC may be converted to or merged with other entity types permitted under RMI law, including business corporations.

Closing Paragraph

The RMI LLC suits asset holding, investment vehicles, and international trading structures where operational flexibility and privacy are priorities. Its principal limitation is restricted treaty access, which may increase withholding tax exposure on cross-border income flows.

Investors and fund managers seeking a flexible, tax-neutral holding or investment vehicle with minimal administrative obligations and strong privacy protections.

Limited Partnership (LP)

Governed by the Marshall Islands Revised Partnership Act, a Limited Partnership is a formal business arrangement comprising at least one general partner and one limited partner. Marshall Islands Limited Partnership registration produces an entity with separate legal personality, meaning it can hold assets, enter contracts, and incur obligations in its own name.

General partners bear unlimited liability for the LP's obligations, while limited partners' exposure is capped at their capital contribution. This structure suits arrangements where passive investors require liability protection without operational involvement.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Limited Partnership (LP) | Separate legal personality under RMI Revised Partnership Act |

| Partners | Min. 1 General Partner + 1 Limited Partner; no maximum | General partner bears full liability; limited partner is passive investor |

| Local Presence | Registered Agent required; no physical office obligation | Registered Agent must be RMI-based |

| Capital | No minimum capital; no prescribed currency | Contributions may be cash, property, or services |

| Privacy | Partner names not required in public filings | Partnership Agreement remains private |

| Management | Managed by General Partner(s) | Limited partners lose liability protection if they participate in management |

Focus Points

- Taxation: No corporate income tax, capital gains tax, withholding tax, VAT, or stamp duty applies to RMI LPs conducting business outside the jurisdiction.

- Economic Substance: LPs engaged in relevant activities with RMI-sourced income may be subject to substance requirements under domestic regulations.

- Annual Compliance: Annual fees are payable to the Registrar of Corporations; no financial statements are required to be filed publicly.

- Treaty Access: The RMI has a limited tax treaty network, which may restrict treaty-based withholding tax relief for distributions.

- Conversion: An LP may generally be converted to another entity type, such as a BC or LLC, subject to compliance with the applicable statutory procedure.

LPs are used primarily for investment funds, joint ventures, and asset-holding structures where a clear separation between active management and passive capital is required. The absence of capital requirements and public disclosure of partner identities are practical advantages, though the unlimited liability of the general partner remains a structural exposure that requires careful consideration.

Best suited for fund managers, private equity arrangements, and investors seeking a pass-through structure with defined liability separation between operating and capital-contributing parties.

Partnerships [General Partnership, Limited Partnership, Limited Liability Partnership]

Understanding Marshall Islands partnership types explained in full requires reference to the Associations Law of the Republic of the Marshall Islands, which governs the formation and operation of domestic partnerships. Partnerships do not possess separate legal personality under RMI law — obligations and liabilities attach directly to the partners rather than to the firm as a distinct legal entity.

Three structural forms are available: the General Partnership, the Limited Partnership, and the Limited Liability Partnership. The LP structure is addressed separately in this article; the focus here is on the distinctions between general and limited liability arrangements as they apply to partnership registration and liability exposure.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Contractual arrangement among partners | No separate legal personality |

| Members | Partners (general and/or limited) | Minimum 2; no statutory maximum |

| Local Presence | Registered Agent required | Physical RMI office not required for non-resident structures |

| Capital | No minimum prescribed | Contributions defined by partnership agreement |

| Privacy | Partner details not publicly filed | Partnership agreement remains private |

| Liability | Varies by type | GP: unlimited; LLP: limited for qualifying partners |

Focus Points

- Taxation: Partnerships conducting no business within RMI territory are not subject to corporate income tax, withholding tax, VAT, or stamp duty under the non-resident exemption framework.

- Economic Substance: Non-resident partnerships with no RMI-source income are generally outside substance obligation scope.

- Annual Compliance: Annual fees are payable to maintain good standing; no mandatory audit requirement for non-resident structures.

- Treaty Access: RMI has no broad tax treaty network, limiting treaty-based withholding relief.

- Conversion: Partnerships may convert to other entity types permitted under the Associations Law, subject to statutory procedure.

Sub-Types

General Partnership (GP)

All partners carry unlimited personal liability for the obligations of the firm. This structure suits small operating arrangements where partners accept joint and several liability in exchange for simplified governance.

Limited Liability Partnership (LLP)

RMI limited liability partnership registration allows qualifying partners to cap their personal exposure to their capital contribution, provided the LLP is properly registered under the applicable provisions of the Associations Law. It is commonly used for professional service arrangements and cross-border joint ventures where liability segregation is a priority.

Closing Paragraph

Partnerships are suited to joint ventures, fund structures, and arrangements requiring pass-through treatment, with the key advantage of flexible internal governance defined entirely by the partnership agreement. The principal limitation is the absence of separate legal personality, which can complicate contracting, asset ownership, and enforcement in some jurisdictions.

Partnership structures in RMI are best suited to two or more parties seeking contractual flexibility and pass-through treatment, where liability can be managed through an LLP designation or indemnity provisions within the agreement.

Non-Resident Domestic Corporation (NRDC)

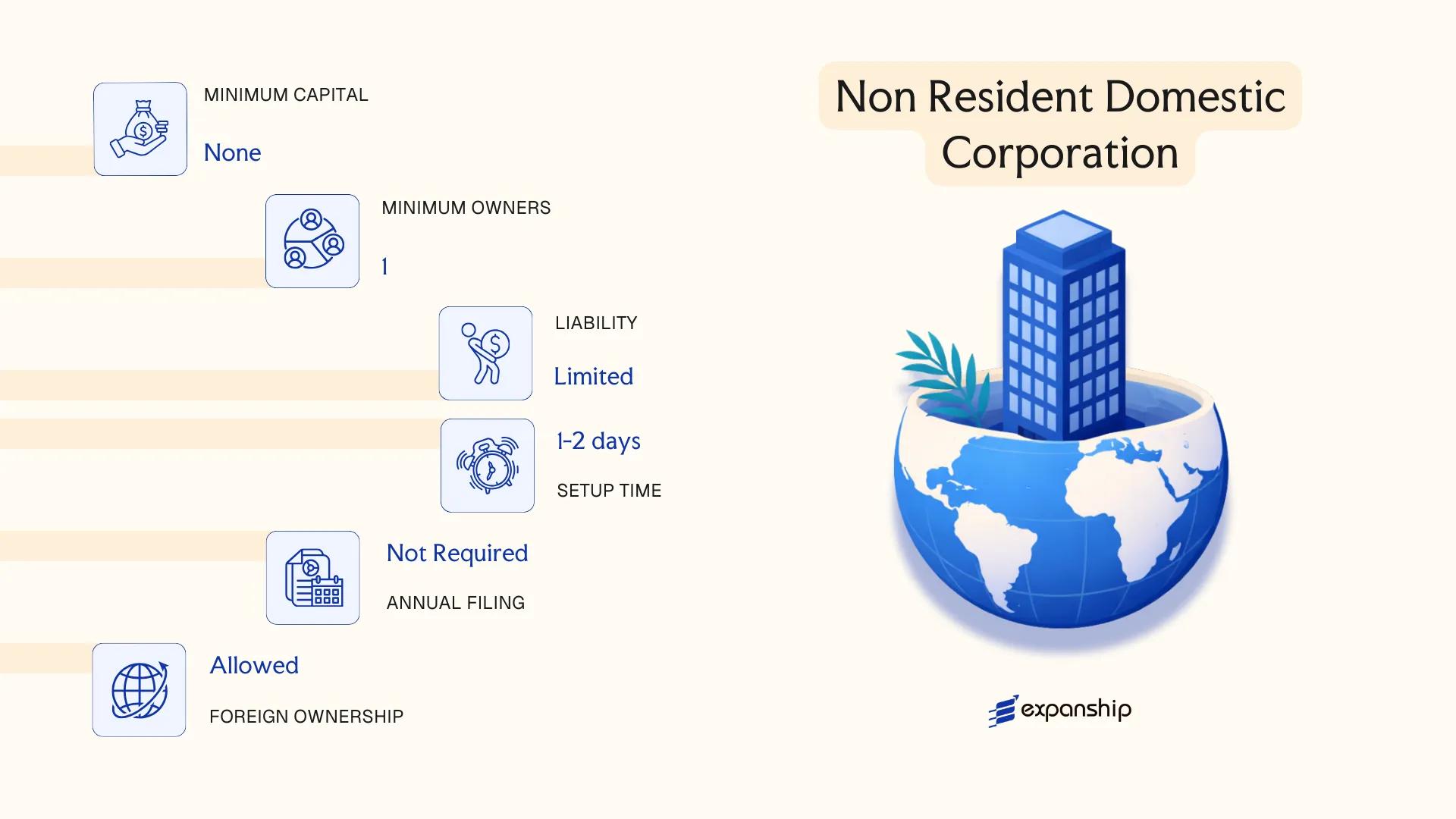

The Marshall Islands Non-Resident Domestic Corporation (NRDC) is established under the Business Corporations Act 1990 and is structurally similar to the Business Corporation (BC), but is specifically designated for entities that conduct no business within the Republic of the Marshall Islands. It carries separate legal personality and confers limited liability on its shareholders.

Registered through the Registrar of Corporations, the NRDC is a domestic entity by formation yet non-resident by operational scope, a distinction that governs its tax treatment and compliance obligations under RMI law.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Corporation | Domestic formation; non-resident operational status |

| Members | Shareholders and Directors | Minimum 1 shareholder; minimum 1 director; no maximum; corporate directors permitted |

| Local Presence | Registered Agent required | Physical office not required; Registered Agent must be RMI-based |

| Capital | No minimum share capital; USD standard | Shares may be par value or no-par value |

| Privacy | Beneficial ownership not publicly filed | Nominee shareholders and directors are permitted |

Focus Points

- Taxation: No corporate income tax, withholding tax, VAT, or stamp duty applies to income derived outside RMI jurisdiction.

- Economic Substance: NRDCs conducting relevant activities may be subject to substance requirements under RMI's economic substance regulations.

- Annual Compliance: Annual renewal fee payable to the Registrar; no audited financial statements required for non-resident entities.

- Treaty Access: RMI has a limited tax treaty network; NRDC structures generally do not benefit from double taxation agreements.

- Restrictions: The entity must not conduct business, earn income, or hold assets within RMI territory to maintain its non-resident status.

Closing

The NRDC suits holding structures, international trading vehicles, and asset-protection arrangements where operational activity remains entirely offshore. Its principal advantage is the absence of local taxation on foreign-sourced income; the main limitation is that any inadvertent business activity within RMI can compromise its non-resident classification.

The NRDC is best suited for international entrepreneurs and holding companies that require a formally incorporated domestic entity with zero local tax exposure and no intention of operating within RMI.

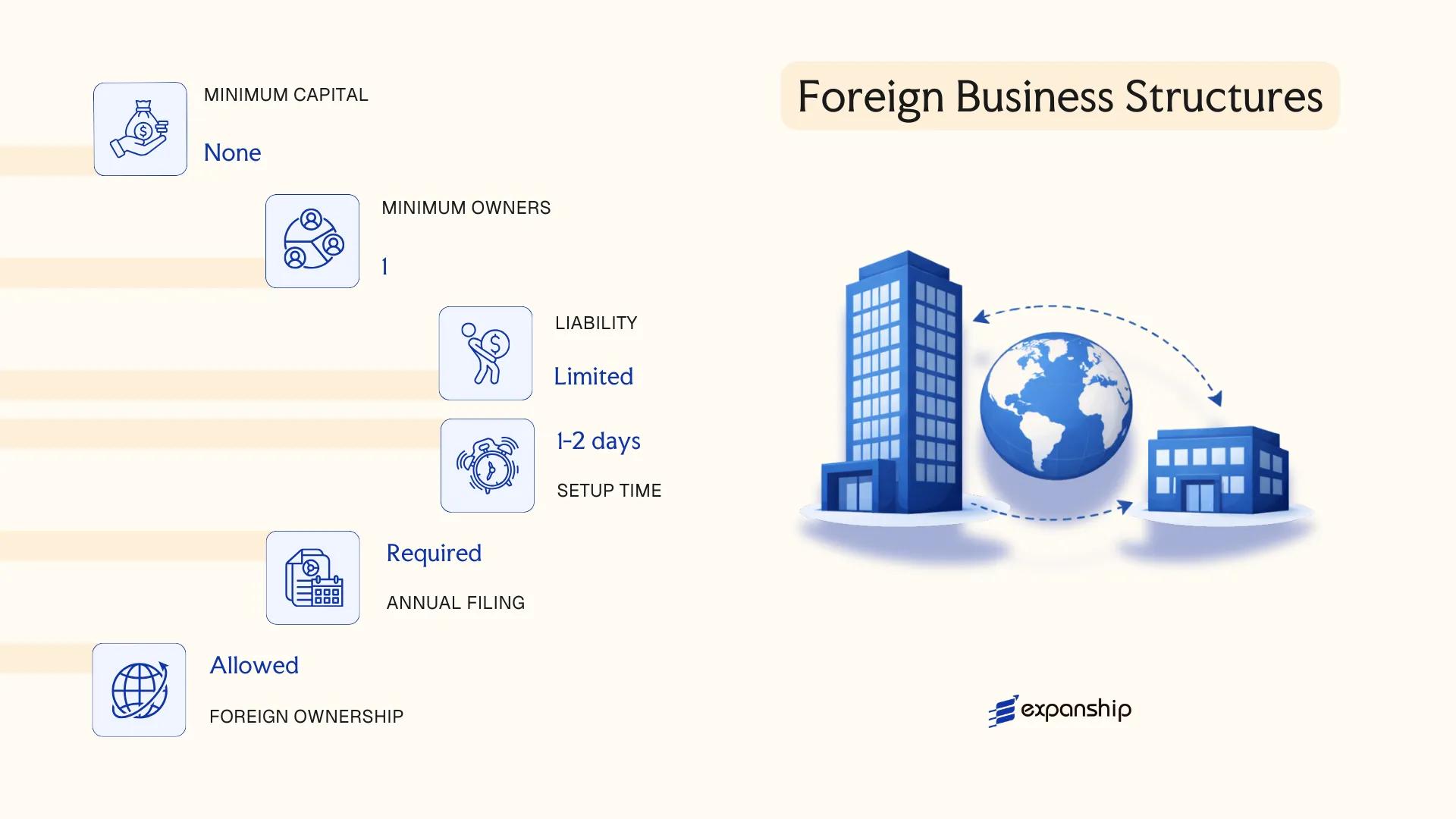

Foreign Business Structures [Foreign Corporation, Foreign LLC, Foreign Partnership]

Foreign corporations, LLCs, and partnerships formed outside the Republic of the Marshall Islands (RMI) can register locally to conduct business or hold assets under the Associations Law of 1990. Registration does not create a new legal entity — the foreign business retains its original legal form, governance structure, and liability characteristics as established in its home jurisdiction.

Foreign corporation registration Marshall Islands follows a formal qualification process administered through a Registered Agent licensed under RMI law. The foreign entity must submit its constituent documents, a certificate of good standing from its home jurisdiction, and appoint a local registered agent. The business does not automatically gain new rights beyond those it holds in its country of formation.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Qualified foreign entity (retains original form) | Not a new RMI entity |

| Governing Members | As defined by home jurisdiction (directors, members, partners) | RMI imposes no separate officer requirements |

| Local Presence | Licensed Registered Agent required | Physical office not mandated |

| Home Jurisdiction Documents | Certificate of good standing + certified constituent documents | Must be current and apostilled where applicable |

| Privacy | Beneficial ownership not publicly disclosed | Subject to RMI's general confidentiality framework |

Focus Points

- Taxation: RMI imposes no corporate income tax, withholding tax, VAT, or stamp duty on foreign-registered entities conducting business outside the RMI.

- Economic Substance: Foreign entities are generally not subject to RMI's domestic economic substance rules unless they generate RMI-sourced income.

- Annual Compliance: Annual renewal fees and maintenance of a licensed registered agent are required to keep the registration in good standing.

- Treaty Access: RMI has a limited tax treaty network; foreign entities registered here do not gain treaty benefits from their RMI registration alone.

- Restrictions: A foreign entity may not conduct activities in RMI beyond those permitted under its registration and home-jurisdiction authorization.

Sub-Types

Foreign Corporation

A foreign corporation qualifying under the Associations Law of 1990 must demonstrate it is validly incorporated and in good standing in its home jurisdiction. This structure is commonly used by multinational firms that need a formal RMI presence for asset-holding or transactional purposes without re-incorporating locally.

Foreign LLC

Marshall Islands foreign LLC registration follows the same qualification pathway as a foreign corporation but preserves the pass-through or hybrid tax treatment the LLC holds under its home jurisdiction's law. It is frequently used by U.S.-based LLCs that operate internationally and require a recognized local registration.

Foreign Partnership

Registering a foreign business entity RMI as a partnership requires submission of the partnership agreement and evidence of valid formation abroad. General and limited partnerships may both qualify, with liability treatment governed entirely by the home jurisdiction instrument.

Foreign business structures suit multinational groups that need a recognized RMI registration without abandoning their existing legal form. The primary advantage is structural continuity — governance, liability, and tax treatment remain anchored to the home jurisdiction. The key limitation is that the entity carries no independent RMI legal identity, which can restrict its ability to enter certain local contracts or access RMI-specific regulatory benefits.

Foreign business structures are best suited for established entities that require a formal RMI foothold for operational or administrative reasons while maintaining their original jurisdiction's legal framework.

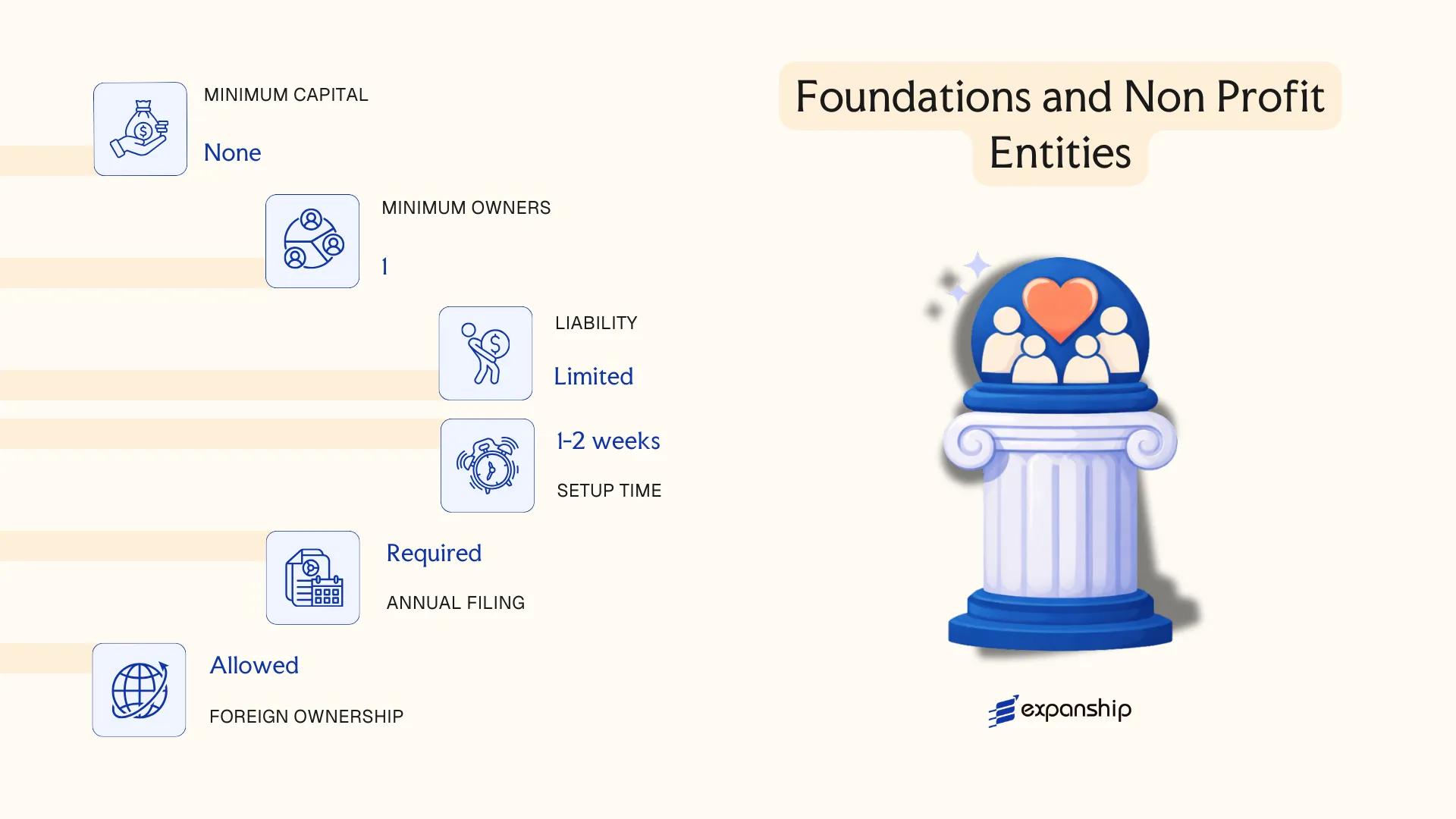

Foundations and Non-Profit Entities [Non-Profit Corporation, Charitable Foundation]

Marshall Islands non-profit corporation formation is governed by the Associations Law of 1990, which provides the statutory framework for both non-profit corporations and charitable foundations operating under RMI jurisdiction. These entities carry separate legal personality, meaning they can enter contracts, hold property, and sue or be sued in their own name.

Non-profit structures in the RMI do not distribute profits to members or directors. Any surplus generated must be applied toward the entity's stated objects, whether humanitarian, religious, educational, or scientific in nature.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Non-Profit Corporation / Charitable Foundation | Separate legal personality under Associations Law 1990 |

| Governance | Directors and Members | Minimum one director; member structure varies by constitution |

| Local Presence | Registered Agent required | Physical office not mandatory; agent must be RMI-based |

| Capital | No share capital | Membership-based; no minimum capital requirement |

| Privacy | Director names may appear in filings | Beneficial ownership disclosure depends on purpose and registration class |

Focus Points

- Taxation: Non-profit entities are generally exempt from RMI corporate income tax provided activities remain within their stated non-commercial purpose; no VAT or withholding tax regime applies domestically.

- Annual Compliance: Annual reporting to the Registrar of Corporations is required to maintain good standing.

- Economic Substance: Charitable foundations engaged solely in qualifying non-profit activities are not subject to economic substance obligations.

- Restrictions: Profit distribution to members, directors, or founders is prohibited; breach can result in dissolution.

- Treaty Access: RMI has limited double tax treaty coverage, which restricts cross-border tax planning through foundation structures.

Sub-Types

Non-Profit Corporation

Formed under the Associations Law, this structure suits membership organisations, NGOs, and religious bodies. Its governance mirrors a standard corporation but replaces shareholder returns with purpose-driven objectives.

Charitable Foundation

Distinct from the non-profit corporation, a charitable foundation is asset-based rather than membership-based. It is typically used for philanthropy, grant-making, or holding assets for defined public benefit purposes, and operates under a foundation charter rather than articles of association.

Closing

Both structures are suited for philanthropic holding, grant distribution, and international NGO operations where profit repatriation is not an objective. The absence of capital requirements lowers the formation threshold, though the prohibition on profit distribution makes these structures unsuitable for any commercially driven activity.

These entities are best suited for founders, international NGOs, or religious organisations seeking a tax-exempt, purpose-driven legal vehicle with no commercial profit mandate.

How to Choose the Right Entity Type in Marshall Islands

Selecting the correct entity structure under the Republic of the Marshall Islands Business Corporations Act has direct legal and financial consequences — not simply administrative ones.

Why Your Entity Choice Matters

Registering the wrong structure can produce concrete, costly outcomes:

- Registering a Business Corporation or LLC for local trading without compliance with domestic licensing requirements constitutes a breach of applicable RMI statutes, which can result in administrative striking off.

- Choosing a tax-exempt offshore entity when treaty-based withholding reductions are needed disqualifies your firm from claiming those reductions, since tax-exempt entities typically fall outside treaty entitlements.

- Forming a corporation when a foundation would better serve asset protection or succession planning locks your structure into annual shareholder meeting obligations and capital maintenance rules that foundations do not carry.

- Selecting an entity with public disclosure requirements when your ownership structure requires confidentiality exposes beneficial owner information unnecessarily.

Key Factors to Consider

Knowing how to choose entity type Marshall Islands involves weighing several operational variables before filing:

- Business Activity: Passive asset-holding, active trading, and regulated activities such as banking or insurance each require a distinct structure under RMI law.

- Local vs. Offshore Operations: Entities intending to transact with RMI residents must satisfy domestic licensing conditions that offshore-designated structures are not designed to meet.

- Ownership and Management: Single-member ownership with informal governance suits an LLC, while multi-party arrangements with defined board authority point toward a corporation.

- Tax Objectives: If tax exemption is sufficient, a non-resident structure applies; if treaty access is required, a different approach is necessary.

- Privacy Requirements: Some structures permit nominee director and shareholder arrangements that limit public disclosure; others do not.

- Exit Strategy: Not all RMI entities support redomiciliation or conversion, so your anticipated exit mechanism should inform the initial structure selection.

Compliance Services for Companies in the Marshall Islands

Conclusion

The Marshall Islands company incorporation summary across available structures reflects a jurisdiction built around offshore utility. The Business Corporation (BC) remains the most commonly registered entity, favored by non-resident entrepreneurs for its tax-neutral status and exemption from local reporting obligations under the Business Corporations Act. LLCs suit those requiring pass-through treatment with contractual flexibility, while Limited Partnerships serve structured investment arrangements. Non-Resident Domestic Corporations occupy a narrower niche, distinct from BCs in their ownership and operational constraints. Foundations address asset protection and succession planning outside the commercial sphere.

Regulatory oversight by the Registrar of Corporations has trended toward greater international compliance alignment, particularly around beneficial ownership transparency and FATF standards. Your choice of structure shapes not only the formation process but the long-term compliance posture of the business. Expanship's team can help match the appropriate entity to your specific operational and jurisdictional requirements.

How Expanship Can Assist You

Expanship Marshall Islands incorporation services cover the full range of entity types registered under the Marshall Islands Business Corporations Act and the Limited Liability Company Act — from offshore Business Corporations and LLCs to Foundations and Non-Profit structures. Your filing goes through the Registrar of Corporations, and our team manages that process directly on your behalf.

From initial document preparation to post-incorporation obligations, Expanship handles every stage of your RMI company formation:

- Registered agent and registered office provision in Majuro

- Government filing and Registrar of Corporations liaison

- Document preparation, notarization, and apostille legalization

- Annual compliance management and good-standing maintenance

- Corporate records maintenance and officer/director updates

- Banking introduction assistance for your new entity

Reach out to our team through the Expanship Marshall Islands contact page to discuss your corporate services needs.

Frequently Asked Questions (FAQ)

The Business Corporation (BC) is the most frequently registered structure under the Business Corporations Act 1990. Its popularity stems from broad operational flexibility, no minimum capital requirement, and no restrictions on foreign ownership or director residency.

A BC is structured primarily for international business and is exempt from local taxation on foreign-sourced income, while a Non-Resident Domestic Corporation (NRDC) is designed for entities that hold assets or conduct specific domestic activities without engaging in general local trade. Compliance obligations for an NRDC tend to be more defined by domestic regulatory requirements. Neither structure permits unrestricted trading with Marshall Islands residents.

The Business Corporation offers the most privacy, as beneficial ownership details and shareholder registers are not publicly disclosed under the Business Corporations Act. Nominee director and shareholder arrangements are permissible, providing an additional layer of confidentiality.

A BC can be formed by one shareholder and one director, who may be the same individual. Partnerships — whether general, limited, or limited liability — require a minimum of two partners by their legal nature. A single-member LLC is permissible under RMI LLC legislation.

Foreign nationals may register a BC, LLC, LP, or NRDC without residency requirements. No local director or shareholder is mandated for most structures, making the jurisdiction broadly accessible to non-resident entrepreneurs and investors.

Conversion and continuation procedures are available under RMI corporate law, allowing a BC to re-register as an LLC or to continue as a foreign entity in another jurisdiction. The process requires filing with the Registrar of Corporations and meeting applicable statutory conditions.

The Business Corporation imposes minimal annual requirements: a registered agent, a registered office address, and payment of the annual renewal fee. No audit, local accounting filing, or financial statement submission is required for BCs conducting purely international business.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.