Key Takeaways

- The Cayman Islands Companies Act (2023 Revision) governs a tiered system of distinct legal entities, with the Exempted Company being the most widely registered structure due to its suitability for investment funds, holding companies, and international businesses that do not trade locally.

- Exempted Limited Partnerships, governed by the Exempted Limited Partnership Act (2021 Revision), serve as the standard vehicle for private fund structures in the jurisdiction.

- The Cayman Islands General Registry administers all company registrations across a jurisdiction that levies no corporate income tax, capital gains tax, or withholding tax on incorporated entities.

- The Cayman Islands Monetary Authority's ongoing alignment with FATF standards continues to shape how entities are structured, maintained, and reported across all available business forms.

Introduction to Entity Types in Cayman Islands

Located in the western Caribbean Sea, the Cayman Islands is a British Overseas Territory comprising three islands — Grand Cayman, Cayman Brac, and Little Cayman — situated south of Cuba and northwest of Jamaica. Companies are registered and regulated by the Cayman Islands General Registry, operating under the oversight of the Registrar of Companies. The jurisdiction imposes no corporate income tax, capital gains tax, or withholding tax on entities incorporated there.

Selecting among the available Cayman Islands business entity types requires a clear understanding of how each structure is defined under local legislation, including the Companies Act (2023 Revision) and the Exempted Limited Partnership Act (2021 Revision).

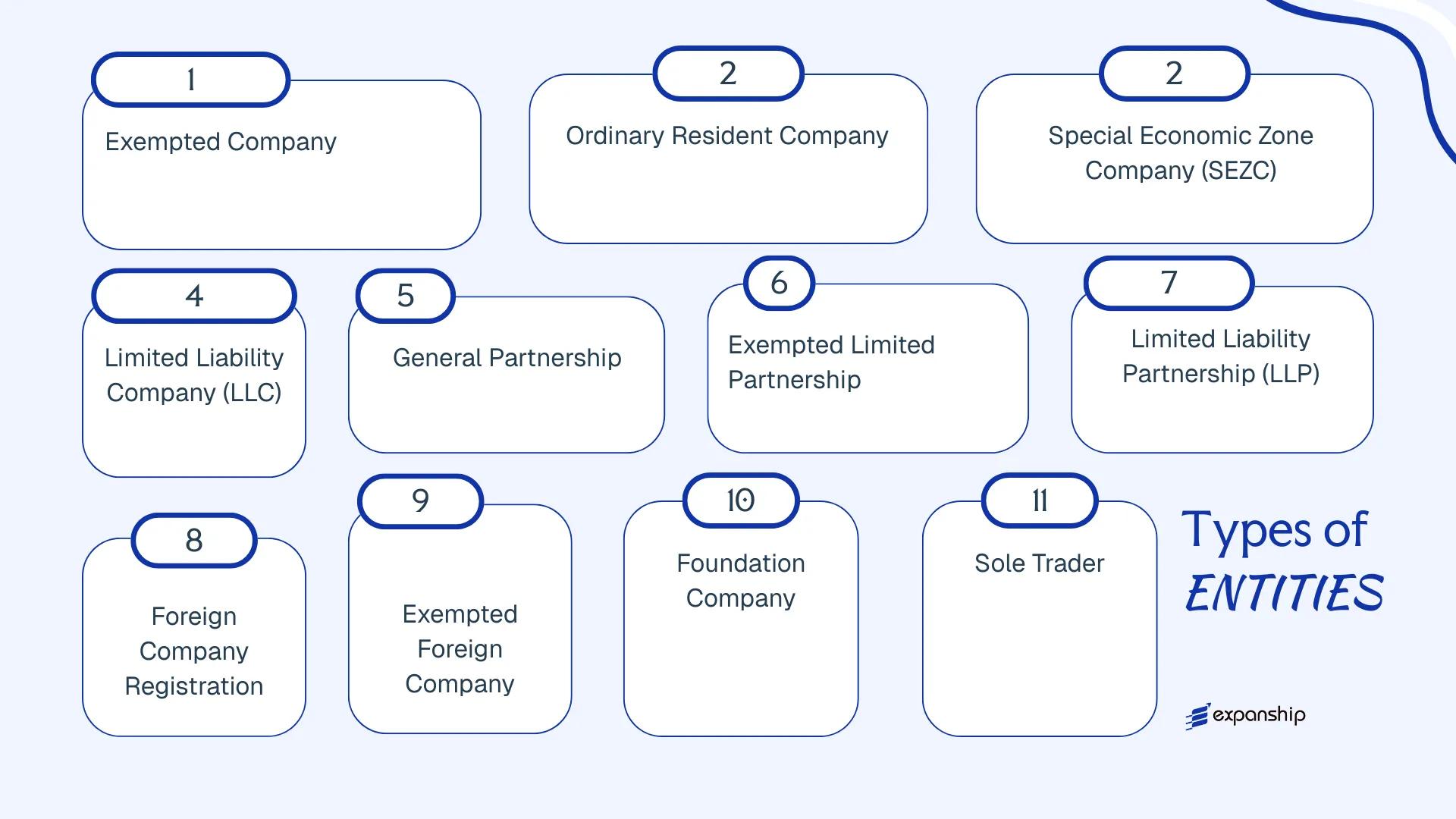

The principal types of companies in Cayman Islands corporate law include the Exempted Company, Ordinary Resident Company, Special Economic Zone Company (SEZC), Limited Liability Company (LLC), General Partnership, Exempted Limited Partnership, Limited Liability Partnership, Foreign Company, Exempted Foreign Company, Foundation Company, and Sole Trader. Each of these Cayman Islands legal entities carries distinct formation requirements, ownership rules, and operational constraints that this article examines in turn.

An Overview of Business Structures in Cayman Islands

The Cayman Islands Companies Act (2023 Revision) and its associated legislation govern the full range of entities available for incorporation and registration across the jurisdiction. Nine distinct structures are recognised under this framework, each designed to meet a different commercial, investment, or operational purpose. The sections that follow examine each in detail.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Exempted Company | Corporate | Limited | Exempt | No | 1 shareholder | CIMA / Registrar | Companies Act (2023 Rev.) |

| Ordinary Resident Company | Corporate | Limited | Exempt | Yes | 1 shareholder | General Registry | Companies Act (2023 Rev.) |

| SEZC | Corporate | Limited | Exempt | SEZ only | 1 shareholder | CIMA / SEZ Authority | SEZ Act (2017 Rev.) |

| LLC | Corporate / Hybrid | Limited | Exempt | Restricted | 1 member | General Registry | LLC Act (2016 Rev.) |

| General Partnership | Partnership | Unlimited | Exempt | Yes | 2 partners | General Registry | Partnership Act |

| Exempted Limited Partnership | Partnership | Mixed | Exempt | No | 2 partners | General Registry | ELP Act (2021 Rev.) |

| Limited Liability Partnership | Partnership | Limited | Exempt | Yes | 2 partners | General Registry | LLP Act |

| Foundation Company | Corporate | Limited | Exempt | Restricted | 1 member | General Registry | Foundation Companies Act |

| Foreign Company Registration | Branch | Parent liability | Exempt | Yes | N/A | General Registry | Companies Act (2023 Rev.) |

| Sole Trader | Sole proprietorship | Unlimited | Exempt | Yes | 1 person | General Registry | Trade and Business Licensing Act |

Each of these structures is examined in full in the sections below.

Exempted Company

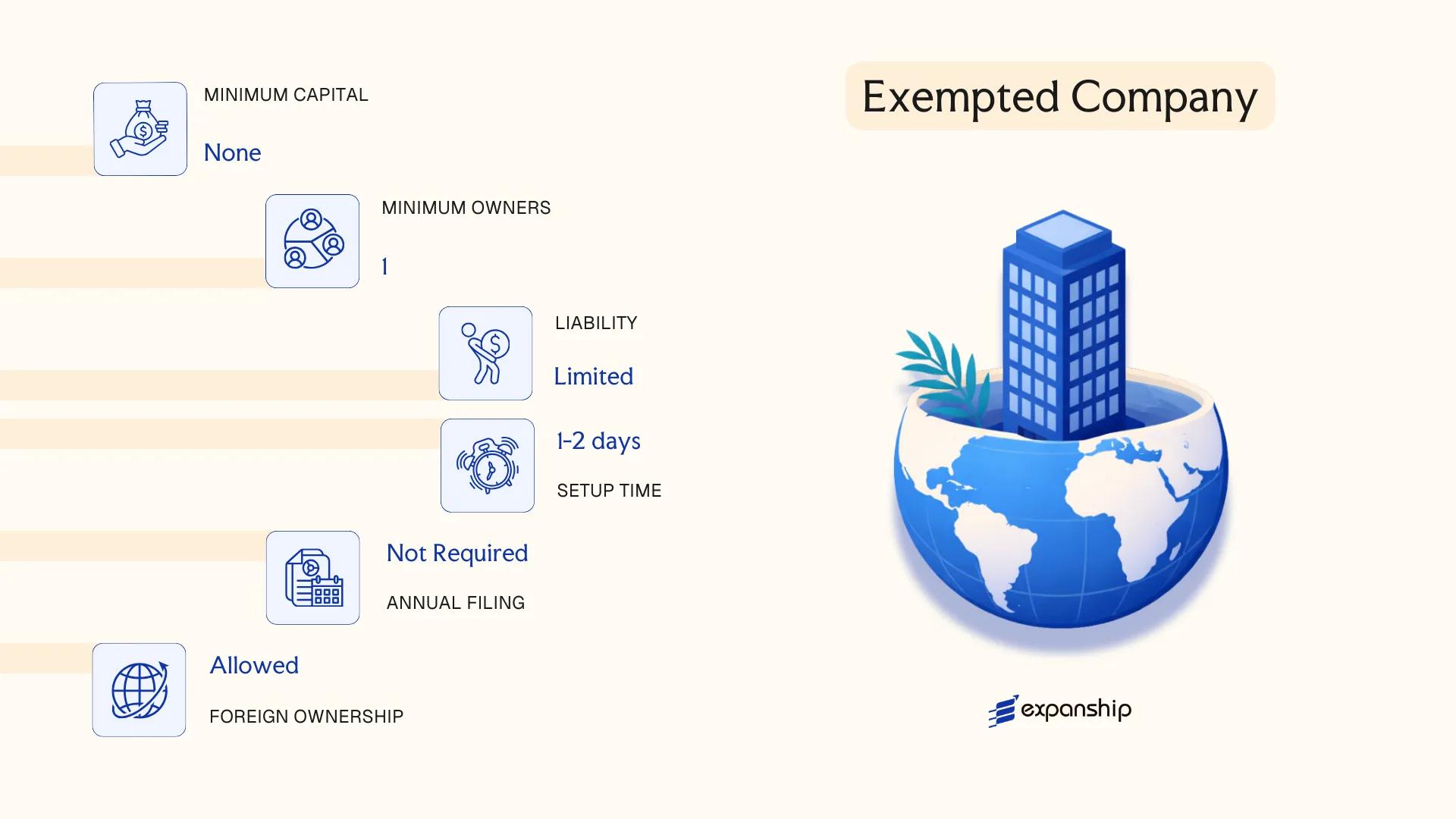

Cayman Islands exempted company formation is governed by the Companies Act (2023 Revision), which consolidates prior legislation and provides the primary legal framework for this structure. An exempted company carries separate legal personality, meaning it can own assets, enter contracts, and incur liabilities in its own name, entirely distinct from its shareholders.

Exempted companies are incorporated with the explicit understanding that their operations will be conducted primarily outside the jurisdiction. This designation is granted at the time of incorporation and is recorded in the name register maintained by the Registrar of Companies.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Limited liability company (shares) | Shareholders' liability capped at unpaid share amount |

| Governed By | Companies Act (2023 Revision) | Registered with the Registrar of Companies |

| Directors | Minimum 1; no maximum; no residency requirement | Corporate directors permitted |

| Shareholders | Minimum 1; maximum 50 for private; no nationality restrictions | Beneficial ownership recorded in the Register of Members |

| Local Presence | Registered office and registered agent required in Cayman Islands | Agent must be licensed under the Companies Act |

| Share Capital | No minimum capital; shares may be denominated in any currency | Par value and no-par-value shares both permitted |

| Privacy | Register of Members not publicly accessible | Beneficial ownership held in a private register |

Focus Points

- Taxation: Exempted companies pay no corporate income tax, capital gains tax, withholding tax, or VAT; a statutory tax exemption undertaking can be obtained for up to 30 years.

- Economic Substance: Entities conducting relevant activities (such as holding, financing, or fund management) must satisfy economic substance requirements under the International Tax Co-operation (Economic Substance) Act (2021 Revision).

- Annual Compliance: Annual return and fees payable to the Registrar of Companies; no requirement to file audited financial statements publicly.

- Treaty Access: The Cayman Islands has no tax treaty network; exempted companies do not benefit from double tax agreements.

- Conversion: An exempted company may be converted into a limited liability company or re-registered as an exempted limited duration company under the Companies Act.

Sub-Types

Exempted Company Limited by Guarantee

Rather than issuing shares, this variant limits member liability to a pre-agreed guarantee amount. It is used primarily for non-profit organisations, industry associations, and certain fund structures where share capital is not appropriate.

Exempted Limited Duration Company (ELDC)

An ELDC has a defined lifespan, not exceeding 30 years, specified in its memorandum of association. This structure suits joint ventures or project-specific vehicles where dissolution on a fixed date is commercially desirable.

Segregated Portfolio Company (SPC)

An SPC allows a single legal entity to create legally separate portfolios, each with ring-fenced assets and liabilities. It is predominantly used in captive insurance and investment fund structures where asset segregation between sub-funds is required.

Common Use Cases and Considerations

Exempted companies are widely used as investment holding vehicles, fund structures, intellectual property holding entities, and regional headquarters for multinational groups. The absence of direct taxation is a clear structural advantage; however, the economic substance obligations introduced in 2019 mean that entities engaged in relevant activities must maintain demonstrable operational substance or risk regulatory penalties.

Best suited for international investors, fund managers, and multinational groups seeking a holding or fund vehicle with no local operational requirements and full foreign ownership.

Company Incorporation in Cayman Islands

Incorporate an exempted company in the Cayman Islands with Expanship's end-to-end support, from name reservation to registered agent appointment.

Ordinary Resident Company

An ordinary resident company in the Cayman Islands is governed by the Companies Act (2023 Revision), the same legislation that underpins most corporate structures registered under Cayman law. Unlike its exempted counterpart, this entity type is specifically designed for businesses that intend to operate locally within the Islands rather than conducting affairs primarily outside the jurisdiction.

The ordinary resident company holds separate legal personality, meaning the entity itself can own assets, enter contracts, and incur liabilities distinct from its shareholders. Liability is limited to each member's shareholding, though the structure carries notable operational restrictions that make it less common among international investors.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Limited liability company with separate legal personality | Incorporated under the Companies Act (2023 Revision) |

| Governance | Directors and shareholders | Minimum one director; no statutory maximum |

| Members | Minimum one shareholder | No maximum; shares may be held by individuals or corporates |

| Local Presence | Registered office required within the Cayman Islands | Must maintain a physical registered address |

| Capital | No minimum share capital; denominated in any currency | Shares may be par value or no-par-value |

| Privacy | Shareholder register is accessible to the public | Less privacy than an exempted company structure |

Focus Points

- Taxation: No corporate income tax, capital gains tax, withholding tax, or VAT applies; stamp duty may apply to certain instruments.

- Economic Substance: Generally not subject to economic substance obligations unless conducting a relevant activity as defined under the Economic Substance Act (2021 Revision).

- Annual Compliance: Annual return and fees payable to the Registrar of Companies; local business licences required under the Trade and Business Licensing Act.

- Restrictions: Prohibited from inviting the public to subscribe for its shares or debentures; cannot conduct business primarily outside the Cayman Islands without converting to an exempted structure.

- Conversion: May apply to re-register as an exempted company if the business purpose changes to predominantly international operations.

Recommendations

An ordinary resident company suits locally operating businesses such as retail traders, service providers, and firms delivering goods or services directly to the Cayman Islands market. The main advantage is straightforward access to local commerce; the principal drawback is the public shareholder register, which reduces confidentiality compared to other structures available under Cayman law.

Local businesses serving the Cayman Islands domestic market, where operating as a recognised resident entity is a regulatory requirement.

Special Economic Zone Company (SEZC)

Established under the Special Economic Zones Act, 2011, the SEZC is a distinct corporate structure available to businesses operating within the Cayman Enterprise City (CEC) special economic zone. Cayman Islands SEZC registration creates a company with separate legal personality and limited liability for its shareholders.

The entity is incorporated under the Companies Act (as revised) but operates subject to the additional regulatory framework of the SEZ Authority, which oversees zone compliance and licensing. Your business must conduct qualifying activities within one of CEC's designated knowledge-based industry clusters to be eligible.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Corporation (company limited by shares) | Incorporated under the Companies Act but licensed by the SEZ Authority |

| Governance | Directors and shareholders | Minimum one director; no maximum. Minimum one shareholder; corporate shareholders permitted |

| Local Presence | Registered office within the SEZ; SEZ licence required | Physical or virtual office provided through CEC |

| Share Capital | No statutory minimum; denominated in any currency | Par value or no-par-value shares permitted |

| Privacy | Shareholder and director details not on public register | Beneficial ownership held in a private register accessible to authorities |

Focus Points

- Taxation: No corporate income tax, no withholding tax, no VAT, and no capital gains tax; the SEZC benefits from a 50-year tax exemption guarantee issued at incorporation.

- Economic Substance: SEZCs conducting relevant activities must satisfy economic substance requirements under the International Tax Co-operation (Economic Substance) Act (as revised).

- Annual Compliance: Annual SEZ licence renewal and filing of beneficial ownership information with the Competent Authority are required.

- Treaty Access: The Cayman Islands has no general tax treaty network; the SEZC does not provide access to double taxation agreements.

- Restrictions: Operations must remain within an approved industry cluster (e.g., technology, media, maritime services); general trading outside the designated categories is not permitted.

Closing

The SEZC suits knowledge-based businesses, tech firms, and financial services companies seeking a physical operational presence within a regulated zone, with the key advantage of a statutory long-term tax exemption. The principal limitation is the restriction to qualifying industry sectors and the mandatory physical or virtual presence within CEC's zone infrastructure.

Technology, media, maritime, and financial services businesses that require an operational base rather than a pure holding structure.

Limited Liability Company (LLC)

Cayman Islands LLC formation is governed by the Limited Liability Companies Act, 2016 (as amended), which introduced a structure modelled closely on Delaware LLC law. The entity carries separate legal personality, meaning it can hold assets, enter contracts, and incur liabilities in its own name. Members' liability is limited to their agreed contributions.

Unlike a company formed under the Companies Act, an LLC is membrane-based and operates through a flexible agreement structure rather than a memorandum and articles of association. This hybrid character — blending corporate limited liability with partnership-style governance — makes it a recognised alternative to the exempted company for fund vehicles and joint ventures where contractual flexibility matters.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Limited Liability Company (LLC) | Separate legal personality; governed by the LLC Act 2016 |

| Governing Members | Members and (optionally) Managers | At least 1 member; no maximum; managers need not be members |

| Local Presence | Registered Office and Registered Agent in Cayman Islands | Agent must be a licensed local firm |

| Capital | No minimum capital; contributions in any agreed form | No par value concept; contributions recorded in LLC agreement |

| Privacy | Member names not on public register | LLC agreement is private; not filed publicly |

| Transferability | Membership interests transferable per LLC agreement | Restrictions or consent requirements set in the agreement |

Focus Points

- Taxation: No corporate income tax, withholding tax, VAT, or capital gains tax; a 20-year tax undertaking is available under the LLC Act.

- Economic Substance: LLCs conducting relevant activities must satisfy economic substance requirements under the Economic Substance Act (2021 Revision).

- Annual Compliance: Annual return and fee payable to the Cayman Islands General Registry; no audited accounts required by default.

- Treaty Access: The Cayman Islands has no tax treaty network; LLC income is not shielded by bilateral agreements.

- Conversion: An LLC may be converted to or from an exempted company or exempted limited partnership under applicable legislation.

Closing

The limited liability company Cayman Islands structure is used predominantly for private equity co-investment vehicles, hedge fund feeders, and joint ventures where parties require granular control over governance and profit allocation through a negotiated agreement. Its primary advantage is the freedom to structure membership economics without the rigid share capital framework of the Companies Act; the corresponding drawback is that the LLC model is less familiar to certain institutional counterparties outside North America.

Cayman LLC structure benefits sophisticated investors, fund managers, and joint venture partners who need contractual flexibility and are accustomed to Delaware-style LLC governance.

Partnerships [General Partnership, Exempted Limited Partnership, Limited Liability Partnership]

Three distinct partnership forms are available under Cayman Islands law. The Cayman Islands exempted limited partnership is governed by the Exempted Limited Partnership Act (2021 Revision), while general partnerships operate under common law principles, and limited liability partnerships are registered under the Limited Liability Partnership Act (2022 Revision).

Each structure differs in how liability is allocated among participants. Exempted limited partnerships have no separate legal personality — the general partner bears unlimited liability — whereas an LLP does carry separate legal personality and offers full limited liability to all partners.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Partnership (contractual or statutory) | ELP has no separate legal personality; LLP does |

| Members Referred To As | General partners / limited partners (ELP); partners (GP, LLP) | ELP requires at least one general partner |

| Member Minimums | Minimum 2 partners across all types; no statutory maximum | ELP: at least 1 GP and 1 LP |

| Local Presence | Registered office and registered agent required for ELP and LLP | General partnerships have no formal registration requirement |

| Capital | No minimum capital; contributions defined in partnership agreement | ELP contributions can be cash, property, or services |

| Privacy | Partnership agreements are private; register of partners not publicly disclosed | ELP must maintain a register of limited partners |

Focus Points

- Taxation: No corporate income tax, capital gains tax, withholding tax, or VAT applies; exempted limited partnerships can obtain a tax undertaking certificate valid for 50 years.

- Economic Substance: ELPs conducting relevant activities must satisfy substance requirements under the International Tax Co-operation (Economic Substance) Act (2021 Revision).

- Annual Compliance: ELPs must file an annual return with the Registrar of Exempted Limited Partnerships and maintain a registered agent.

- Conversion: An ELP may be converted to or registered as a foreign limited partnership under the Act, subject to Registrar approval.

- Restrictions: ELPs may not carry on business with the public in the Cayman Islands except in furtherance of their offshore business.

Sub-Types

General Partnership

Formed by agreement between two or more persons without formal registration. No limited liability protection exists — all partners bear joint and several liability for partnership obligations.

Exempted Limited Partnership

The most widely used structure for private equity and investment funds. Limited partners' liability is capped at their capital contribution, provided they do not participate in management.

Limited Liability Partnership

Carries separate legal personality with full liability protection for all partners. Suited to professional services firms and joint ventures requiring a more corporate-like structure.

Common Use Cases and Considerations

Exempted limited partnerships dominate private equity, hedge fund, and venture capital structures due to their flexible governance and investor-friendly liability framework. The absence of a corporate layer simplifies profit distributions, though the general partner's unlimited liability remains a structural exposure that is typically managed by interposing a limited liability entity as GP.

ELPs are best suited to fund managers, institutional investors, and private equity sponsors structuring pooled investment vehicles with multiple capital contributors.

Foreign Structures [Foreign Company Registration, Exempted Foreign Company]

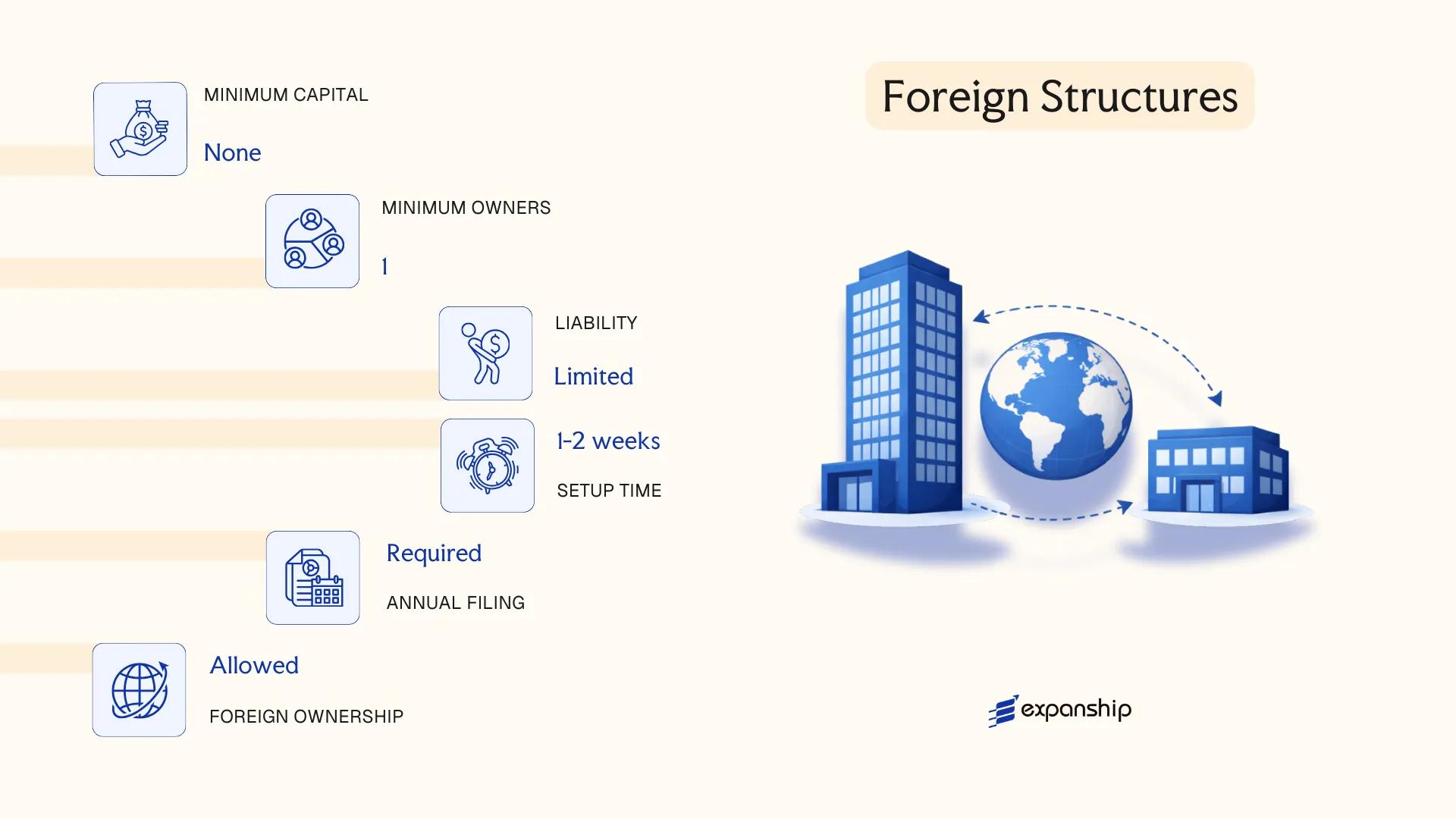

Foreign company registration Cayman Islands is governed by Part IX of the Companies Act (2023 Revision), which sets out the conditions under which overseas entities may operate locally. A foreign company does not create a new legal entity — it is an extension of the parent company, which retains its original legal personality and liability structure under its home jurisdiction's law.

Registration is compulsory for any overseas firm that establishes a place of business or carries out business within the Islands. Once registered, the branch must appoint a local registered agent and maintain a registered office address within the jurisdiction.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Branch of a foreign entity | Not a separate legal entity; parent company bears liability |

| Responsible Persons | Directors of the parent company; local authorized representative | Local rep required for service of process |

| Local Presence | Registered agent and registered office mandatory | Must be a licensed Cayman Islands service provider |

| Capital | No separate capital requirement | Parent company's capital structure applies |

| Filing Requirements | Certified constitutional documents of parent; list of directors; registered agent details | Documents often require notarization and apostille |

| Privacy | Director details filed with Registrar | Not publicly searchable via standard registry access |

Focus Points

- Taxation: No corporate income tax, withholding tax, capital gains tax, or VAT applies to the branch or its parent on Cayman-sourced income; stamp duty may apply on certain instruments.

- Economic Substance: If the branch conducts a relevant activity, economic substance obligations under the International Tax Co-operation (Economic Substance) Act (2021 Revision) apply.

- Annual Compliance: Annual return and renewal fees must be filed with the Registrar of Companies; failure to file triggers penalties and potential deregistration.

- Treaty Access: The Cayman Islands has no double taxation treaties; treaty benefits depend entirely on the parent's home jurisdiction.

- Restrictions: A registered foreign branch cannot conduct business beyond what the parent is authorized to undertake in its home jurisdiction.

Sub-Types

Exempted Foreign Company

A Cayman Islands exempted foreign company is an overseas entity that registers locally but has obtained exempted status, meaning it is prohibited from carrying on business within the Islands with residents. This structure is used by multinational groups seeking a Cayman presence for fund administration, holding activities, or intra-group purposes without conducting domestic trade.

Recommendations

A registered foreign branch suits multinational businesses needing a formal Cayman presence to hold assets, manage regional operations, or satisfy counterparty requirements — the key advantage being speed of establishment without forming a new entity, though the parent company's unlimited liability exposure to branch activities is a material drawback.

Overseas companies already operational in their home jurisdiction that need a recognized legal presence in Cayman Islands for specific operational or contractual purposes.

Foundation Company

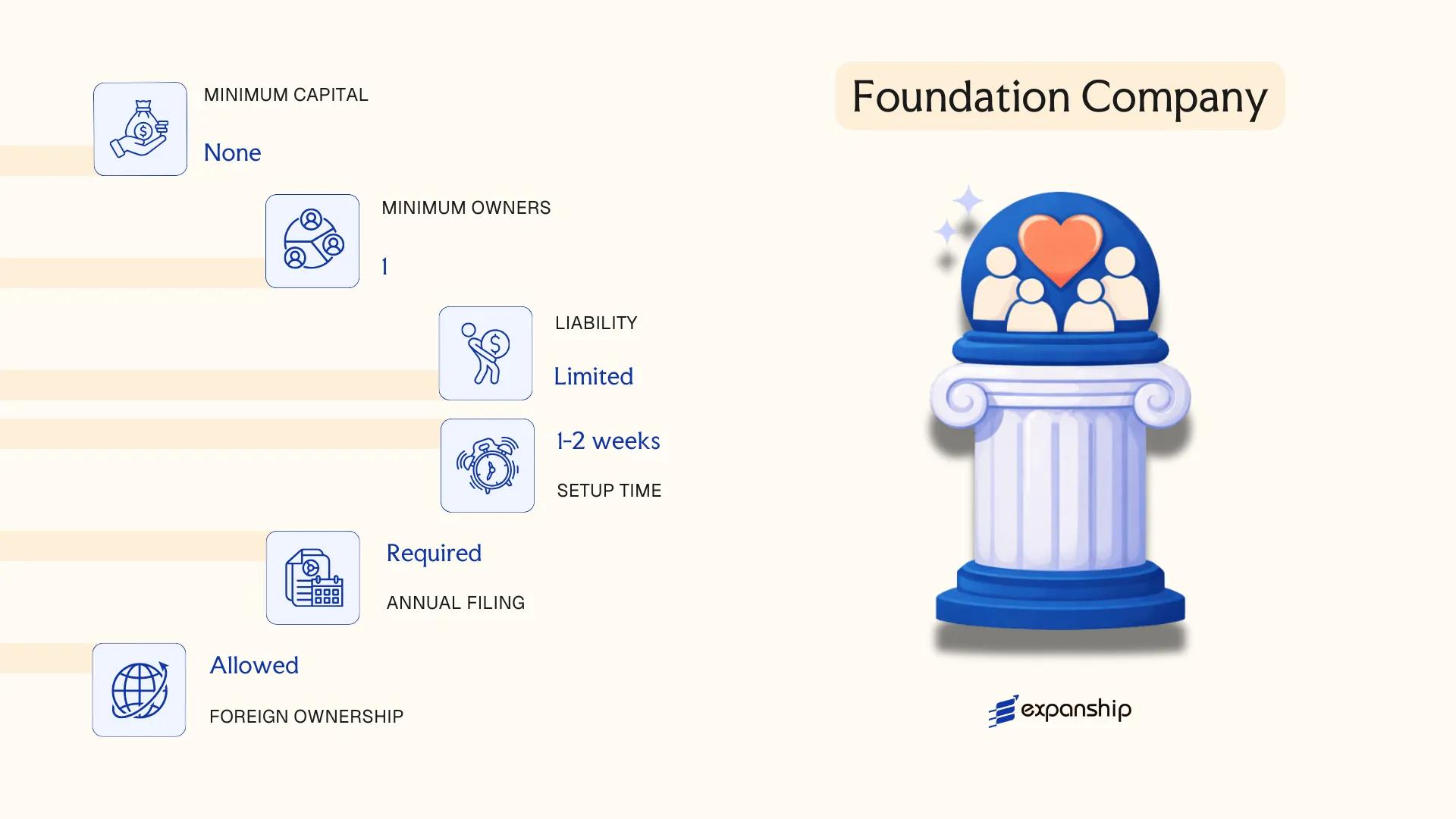

Introduced under the Foundation Companies Act, 2017, the Cayman Islands foundation company is a statutory entity that combines characteristics of a company and a trust within a single structure. It holds separate legal personality and carries limited liability, making a Cayman Islands foundation company setup distinct from both a conventional corporate vehicle and a traditional trust arrangement.

Governed by the Registrar of Companies, the foundation company has no shareholders in the conventional sense. Ownership interests are replaced by beneficiaries and members, and the entity's constitution defines how assets are managed and distributed.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Body corporate with separate legal personality | Hybrid structure; not a trust, not a conventional company |

| Governing Roles | Directors, Secretary, Supervisor (optional), Enforcer | Directors manage; an Enforcer may be appointed to protect beneficiary interests |

| Members | No shareholders; beneficiaries defined in constitutional documents | Beneficiaries may be individuals, entities, or purposes |

| Local Presence | Registered office and registered agent required | Must be maintained with a licensed Cayman Islands service provider |

| Capital | No minimum share capital requirement | Assets held in the foundation; not divided into shares |

| Privacy | Memorandum and articles filed; beneficiary details not publicly disclosed | Constitutional documents are on public record |

Focus Points

- Taxation: No corporate income tax, capital gains tax, withholding tax, or VAT applies; the entity operates in a zero-tax environment.

- Economic Substance: Foundation companies used for holding or investment purposes should assess whether substance obligations apply under the Economic Substance Act.

- Annual Compliance: Annual fees payable to the Registrar of Companies; financial statements not required to be filed publicly.

- Conversion: A foundation company may be converted to or from another Cayman company type subject to statutory requirements under the Act.

- Restrictions: Cannot carry on business with the public in a commercial trading capacity without specific provisions in its constitution.

Closing

Foundation companies are used for wealth structuring, philanthropic purposes, succession planning, and holding family assets where the flexibility of purpose-based governance is preferred over a conventional shareholder model. The absence of mandatory beneficiaries allows for pure purpose structures, though the relative novelty of the legislation means precedent and judicial interpretation remain limited compared to trust law.

Best suited for family offices, private wealth structuring, and philanthropic vehicles where asset segregation and purpose-driven governance are priorities over commercial trading activity.

Sole Trader

Sole trader Cayman Islands registration is not governed by a dedicated sole proprietorship statute in the same way that companies are regulated under the Companies Act (2023 Revision). Operating as a sole trader means the individual and the business are legally the same person — there is no separate legal personality, no limited liability, and no formal incorporation process required to begin trading.

Registration requirements are minimal by comparison to incorporated structures. A sole trader conducting business under a name other than their own legal name must register that trade name under the Registration of Business Names Act, administered through the General Registry. Beyond this, sector-specific licences may apply depending on the nature of the activity.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated | No separate legal personality from the owner |

| Members | Sole proprietor (1 individual) | No shareholders, directors, or members |

| Local Presence | No registered agent required | Trade name registration filed with the General Registry |

| Capital | No minimum | No paid-up capital requirement |

| Liability | Unlimited personal liability | Owner's personal assets are exposed to business debts |

| Privacy | Trade name publicly registered | Owner's identity linked to the trade name on public record |

Focus Points

- Taxation: No corporate income tax, capital gains tax, VAT, or withholding tax; sole traders are subject to the same zero-tax environment as incorporated entities.

- Economic Substance: Economic substance obligations under the International Tax Co-operation (Economic Substance) Act do not apply to sole traders, as these rules target legal entities.

- Annual Compliance: Annual renewal of any registered trade name is required under the Registration of Business Names Act to maintain active status.

- Restrictions: Non-Caymanian individuals must hold a valid work permit or possess the right to work before conducting business as a sole trader.

- Conversion: A sole trader can incorporate into a company at any time, but assets and liabilities must be formally transferred as there is no automatic conversion mechanism.

Closing

A sole trader structure suits individuals providing freelance, consulting, or small-scale services who require minimal administrative overhead and do not need investor participation. The principal limitation is unlimited personal liability, which exposes the owner's personal assets to any business obligations.

Best suited for Caymanian residents or work permit holders operating independently in low-risk service activities where formal incorporation is disproportionate to the scale of the business.

How to Choose the Right Entity Type in Cayman Islands

Selecting how to structure your business in the Cayman Islands has direct legal and financial consequences — the decision shapes your tax position, regulatory obligations, and operational capacity from the date of incorporation.

Why Your Entity Choice Matters

Misjudging the appropriate structure at the outset carries concrete risks:

- Registering an exempted company when your intended activity requires local trading puts you in breach of the Companies Act (2023 Revision), which can result in striking off or regulatory penalties.

- Choosing a tax-exempt structure when your investors or counterparties require treaty access means withholding tax reductions available under bilateral agreements cannot be claimed.

- Forming a standard company when a Foundation Company would serve asset protection or succession planning purposes locks your structure into annual shareholder obligations that foundations are not subject to.

- Selecting an entity that carries audited financial statement requirements for a single-person consulting operation creates recurring compliance costs that serve no functional purpose at that scale.

Key Factors to Consider

- Business Activity: Passive asset-holding, active trading, and regulated activities such as fund management each point toward distinct entity categories under Cayman law.

- Local vs. Offshore Operations: Transacting with Cayman residents requires a structure authorised for local business, whereas purely offshore activity suits an exempted entity.

- Ownership and Management: Multi-party ventures requiring defined governance favour company structures, while single-owner or flexible arrangements may suit an LLC or partnership.

- Tax Objectives: Your need for statutory tax exemption, or absence of one, should be confirmed before selecting a structure that cannot later be reclassified without a formal conversion process.

- Substance Capacity: If you cannot maintain genuine economic presence in the jurisdiction, verify whether your chosen entity type falls within the scope of the International Tax Co-operation (Economic Substance) Act (2021 Revision) and what the applicable thresholds are.

- Exit Strategy: Redomiciliation, conversion, and voluntary winding-up procedures vary across entity types — confirm that your chosen structure accommodates your anticipated exit mechanism before incorporating.

Compliance Services for Companies in the Cayman Islands

Ongoing compliance support for Cayman Islands entities, including annual filings, economic substance reporting, and regulatory correspondence.

Conclusion

The Cayman Islands company formation summary across available structures reflects a jurisdiction with a deliberately tiered regulatory framework. Exempted Companies remain the most registered entity type, favored by investment funds, holding structures, and international businesses with no intent to trade locally. Ordinary Resident Companies serve businesses operating within the islands. The SEZC provides a defined pathway for technology and services firms within the Cayman Enterprise City zone. LLCs offer contractual flexibility suited to joint ventures and private equity arrangements. Exempted Limited Partnerships are the standard vehicle for private funds. Foundation Companies address asset protection and purpose-driven structures. Sole traders and general partnerships carry unlimited liability by design.

Regulatory oversight from the Cayman Islands Monetary Authority continues to align with FATF standards, and the jurisdiction's ongoing engagement with international transparency frameworks shapes how entities are structured and maintained. Your choice of business structure will ultimately determine reporting obligations, governance requirements, and operational scope.

How Expanship Can Assist You

Expanship's Cayman Islands incorporation services cover the full scope of structures discussed in this guide — from Exempted Companies and Foundation Companies to Exempted Limited Partnerships and SEZCs. Our team works directly with the Cayman Islands General Registry and, where applicable, coordinates with the Cayman Islands Special Economic Zone Authority (CSEZA) to ensure your entity is registered correctly from day one.

From initial structure selection through to post-incorporation obligations, Expanship handles the operational details of your Cayman Islands company setup:

- Document preparation and notarization

- Registered agent and registered office provision

- Filing with the General Registry and relevant government authorities

- Annual return submissions and compliance calendar management

- Banking introduction assistance for corporate accounts

- Ongoing corporate secretarial support

Contact Expanship Cayman Islands to discuss which structure fits your objectives.

Frequently Asked Questions (FAQ)

The Exempted Company is by far the most frequently incorporated structure. Its exemption from local income, capital gains, and withholding taxes, combined with the ability to obtain a statutory 20-year tax undertaking, makes it the default choice for international holding, fund, and investment structures.

An Exempted Company cannot trade within the Cayman Islands except in furtherance of its offshore business, whereas an Ordinary Resident Company may conduct local trade and engage with residents directly. The Ordinary Resident Company carries broader domestic compliance obligations, including registration with the General Registry and adherence to local licensing requirements. Tax treatment is broadly similar, as neither entity pays corporate income tax, but the Exempted Company carries the formal tax exemption undertaking.

The Foundation Company provides substantial privacy, as beneficial ownership details are not part of the public register. Shareholder and director information for most entities is filed with the Registrar of Companies but is not publicly searchable in full. Nominee arrangements are permissible, though all structures remain subject to beneficial ownership disclosure requirements under the Beneficial Ownership Transparency Act, 2023.

A sole individual can form an Exempted Company, Ordinary Resident Company, SEZC, LLC, or Foundation Company, as these require only one shareholder and one director or equivalent. Partnerships are the exception — a General Partnership and an Exempted Limited Partnership each require a minimum of two partners. An LLP similarly requires at least two designated members.

Foreigners may incorporate an Exempted Company, LLC, Foundation Company, SEZC, or register as a foreign company without restrictions on nationality. The Exempted Limited Partnership is also available to non-residents acting as limited partners. Ordinary Resident Companies require a local business licence under the Trade and Business Licensing Act if trading domestically, which involves additional scrutiny for foreign-owned entities.

The Companies Act (2023 Revision) allows an Exempted Company to convert into an LLC, and vice versa, through a formal conversion process filed with the Registrar. A foreign company may also continue into the Cayman Islands as an Exempted Company under Part IX of the Act. Not all conversions are available as direct statutory procedures — some restructurings require a new incorporation.

The Exempted Company and the Exempted Limited Partnership are the two structures most widely used for regulated and unregulated fund vehicles. Mutual funds registered under the Mutual Funds Act (2021 Revision) typically adopt the Exempted Company form, while private equity structures frequently use the Exempted Limited Partnership for its pass-through economics and flexible capital account mechanics.

No. A General Partnership does not have separate legal personality under Cayman law, meaning partners bear direct liability for partnership obligations. The Exempted Limited Partnership also lacks separate legal personality, though the LLC, Foundation Company, Exempted Company, and SEZC each hold it. This distinction has material implications for liability exposure and contract enforcement.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.