Key Takeaways

- SVG IBCs operating under the International Business Companies (Amendment and Consolidation) Act are structurally barred from conducting business within the local domestic market, limiting their operational utility to purely cross-border activities.

- St. Vincent and the Grenadines' history on the FATF greylist imposes a measurable compliance burden on counterparties and correspondent banks, which frequently translates into account rejections or enhanced due diligence requirements for IBC clients.

- The jurisdiction's narrow double tax treaty network means SVG IBCs cannot rely on treaty-based withholding tax reductions when repatriating income through higher-treaty jurisdictions, increasing the overall tax cost of international structures.

- Mandatory reliance on a licensed registered agent for all IBC filings and statutory correspondence creates a structural dependency that adds ongoing cost and introduces an intermediary layer outside the direct control of the beneficial owner.

St. Vincent and the Grenadines operates under a lightly regulated offshore framework, governed primarily by the International Business Companies (Amendment and Consolidation) Act, accessible via the SVG laws. The disadvantages of incorporating in St. Vincent and the Grenadines span banking access, international compliance standing, treaty limitations, and operational constraints that affect foreign-owned entities specifically structured as IBCs.

Not every drawback applies equally to all business models. A holding company faces different exposure than a trading firm, and the severity of each limitation depends heavily on your industry, target markets, and banking requirements.

This article is most relevant to foreign entrepreneurs and offshore investors considering an IBC structure for cross-border transactions, asset holding, or international trade.

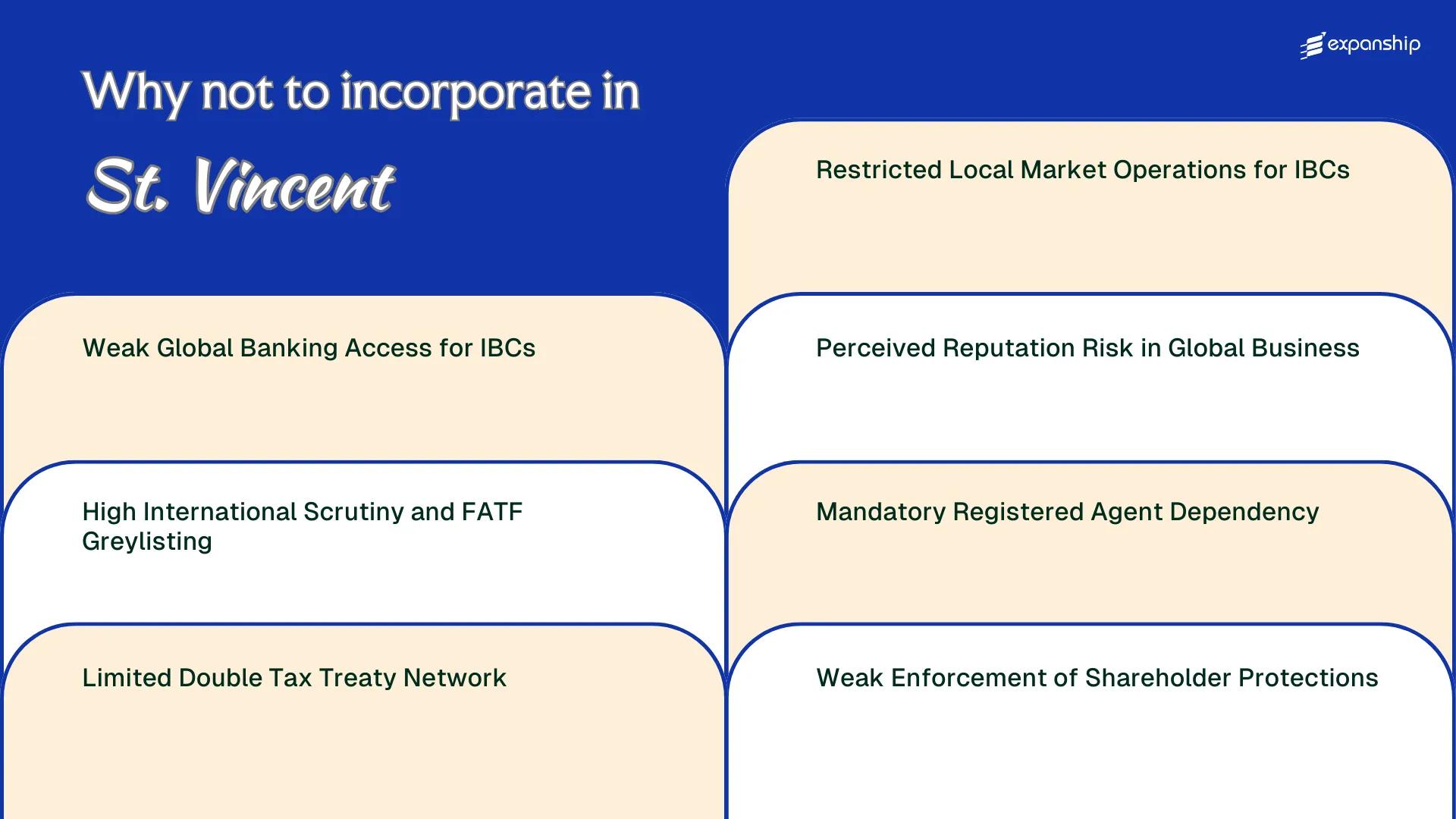

Weak Global Banking Access for IBCs

St. Vincent IBC banking access problems are among the most immediate operational barriers you will face after incorporation. Correspondent banking networks treat SVG-registered entities with heightened suspicion, which translates directly into account rejections and restricted payment rails.

Why Banks Refuse SVG IBCs

International banks apply enhanced due diligence to companies formed under the International Business Companies Act of St. Vincent and the Grenadines, largely because the jurisdiction has faced successive rounds of international scrutiny. Many European and North American correspondent banks have de-risked by refusing to maintain relationships with SVG-domiciled entities altogether, meaning your IBC may be structurally unbankable in major financial markets regardless of its legitimate purpose.

Offshore banking restrictions tied to SVG extend beyond simple account opening refusals. Even where an account is obtained, transaction processing through correspondent networks can be blocked or delayed, making routine operations like supplier payments or payroll in hard currency genuinely difficult.

The Cost of Limited Banking Options

SVG company banking challenges push owners toward smaller, less liquid offshore banks that carry their own counterparty risks. Your business may have no access to trade finance, credit facilities, or multi-currency accounts that operational companies normally require.

Many SVG IBCs are unable to open accounts with Tier 1 banks entirely, forcing reliance on alternative payment providers that may lack regulatory backing in your target markets.

High International Scrutiny and FATF Greylisting

St. Vincent FATF greylisting risks are not theoretical. The jurisdiction was added to the FATF grey list, formally known as the list of jurisdictions under increased monitoring, which signals that international bodies have identified strategic deficiencies in its anti-money laundering and counter-terrorist financing frameworks.

Being greylisted means your SVG-registered entity is automatically subject to enhanced due diligence by foreign banks, correspondent institutions, and counterparties. That translates directly into higher compliance costs and slower account approvals, even for legitimately structured businesses.

The Financial Intelligence Unit of St. Vincent and the Grenadines operates under the Financial Intelligence Unit Act, but the greylisting signals to global regulators that systemic gaps remain. Foreign partners often treat that signal as sufficient reason to decline the relationship.

Practical burdens this creates for your business include:

- Foreign banks may require extensive source-of-funds documentation before processing routine transfers involving your SVG entity

- Compliance officers at EU and US-regulated institutions are required to apply enhanced scrutiny to greylisted jurisdictions, extending onboarding timelines by weeks or months

- Some institutional counterparties maintain internal blacklists that include greylisted jurisdictions regardless of your entity's specific conduct

- SVG AML compliance risks become your reputational exposure even when your own filings are clean

Greylisting status can change if the jurisdiction meets FATF action plan benchmarks, but that process takes time and offers no immediate relief for your current operations.

Company Incorporation in St. Vincent and the Grenadines

Understand the full compliance picture before incorporating in SVG. Expanship manages the entity setup process and registered agent requirements across the jurisdiction.

Limited Double Tax Treaty Network

St. Vincent's limited tax treaty network is one of the more consequential structural gaps for any foreign business owner relying on the jurisdiction for cross-border income flows. The country has signed very few bilateral double taxation agreements, leaving IBCs exposed to full withholding taxes in counterparty countries with no treaty relief available.

| Factor | Detail | Implication for IBC |

|---|---|---|

| Active DTAs | Fewer than 5 confirmed bilateral agreements | No treaty protection across most trading partners |

| Withholding tax relief available | Minimal to none for most jurisdictions | Full source-country tax applies on dividends, royalties, interest |

| OECD treaty partner coverage | Not a signatory to OECD/UN model frameworks | No access to reduced rates standard in OECD networks |

| EU/UK treaty protection | No DTA with EU member states or the UK | High effective tax cost on European-sourced income |

Without a DTA in place, income paid from a foreign counterpart to your SVG entity is taxed at the source country's domestic withholding rate, which can reach 25-30% in jurisdictions such as Germany or Japan. That tax cannot be credited or offset at the SVG level, since IBCs operating under the International Business Companies Act have no domestic tax base against which to apply foreign tax credits.

SVG double taxation agreement limitations mean that structuring royalty flows, intercompany dividends, or service fees through an SVG entity often produces a higher combined tax burden than routing through a jurisdiction with an active treaty network. The exception applies only where the counterparty country's domestic law unilaterally reduces withholding rates regardless of treaty status.

Restricted Local Market Operations for IBCs

Under the International Business Companies Act, an IBC registered in St. Vincent and the Grenadines is explicitly prohibited from conducting business with residents or companies domiciled within the jurisdiction. This restriction means your entity cannot solicit local clients, own domestic real estate for commercial use, or engage in any trade activity directed at the SVG domestic market.

The prohibition is structural, not incidental. If your business model requires any local revenue stream, a standard IBC does not qualify as the appropriate vehicle.

This creates a hard boundary for foreign owners who later identify regional opportunities. Expanding into the local or Eastern Caribbean market requires a separately incorporated domestic entity, which carries different compliance, capitalization, and licensing obligations under SVG law.

- IBCs are legally barred from transacting with SVG residents under the IBC Act

- Domestic commercial real estate ownership is outside the permitted scope of an IBC

- Any local revenue activity triggers the need for a separate domestic incorporation

- Operating in breach of local market restrictions can result in regulatory action by the SVG Financial Services Authority

- The restriction applies regardless of the IBC's ownership structure or nationality of shareholders

An SVG IBC can legally be owned 100% by a local SVG resident, yet that same company is still prohibited from doing business domestically.

Perceived Reputation Risk in Global Business

St. Vincent offshore company reputation risks are a genuine operational concern, not just a perception problem. Counterparties in regulated financial centers often apply heightened due diligence to any entity incorporated under the SVG International Business Companies (Amendment and Consolidation) Act.

How the Jurisdiction's Profile Affects Your Entity's Standing

SVG jurisdiction credibility problems surface most visibly when your IBC attempts to open correspondent banking relationships or onboard institutional clients in the EU, UK, or North America. Compliance teams in those markets routinely apply additional scrutiny to SVG-registered entities, which translates into longer onboarding timelines and, in some cases, outright rejection.

The FSA (Financial Services Authority of SVG) governs IBC registration, but the authority carries less international recognition than regulators in OECD-member jurisdictions. That asymmetry in regulatory prestige directly affects how counterparties assess your firm's governance standards.

Practical Consequences for Foreign Business Owners

St. Vincent and the Grenadines offshore stigma affects contract negotiations as well. Some suppliers, payment processors, and professional service providers apply surcharges or impose stricter contractual terms when the counterpart entity is SVG-incorporated.

St. Vincent IBC perceived legitimacy issues are somewhat less severe for businesses operating purely in emerging markets, where regulatory scrutiny from Western institutions is less pervasive. That exception is narrow, however, and does not apply if your business requires relationships with OECD-regulated banks or investors.

Assessing Reputation Risk Before Incorporating in St. Vincent

Speak with our team about how SVG's regulatory standing may affect your specific counterparty relationships, banking access, and client onboarding requirements before committing to this jurisdiction.

Mandatory Registered Agent Dependency

Under the International Business Companies Act, every IBC registered in SVG must maintain a licensed registered agent at all times. St. Vincent registered agent dependency risks are structural, not incidental, meaning your company's legal standing is directly tied to a third party you may have limited visibility over.

- Your IBC can be struck off the register if the registered agent relationship lapses, regardless of whether your underlying business operations remain active.

- All official government correspondence, compliance notices, and statutory filings are routed through the agent, creating an information bottleneck that delays your awareness of regulatory obligations.

- Annual agent fees are a fixed, non-negotiable operating cost with no option to self-manage your registered office as you might in some other jurisdictions.

- Switching agents requires formal procedural steps under SVG IBC registered agent requirements, introducing transition risk during any period of agent dispute or insolvency.

- Your agent's own licensing status with the Financial Services Authority directly affects your company's compliance standing, a dependency entirely outside your control.

Weak Enforcement of Shareholder Protections

St. Vincent shareholder protection limitations stem partly from structural gaps in how the International Business Companies (Amendment and Consolidation) Act governs minority investor rights. Unlike jurisdictions with dedicated securities regulators or active corporate enforcement bodies, SVG has no equivalent supervisory authority with a mandate to investigate shareholder disputes in IBCs.

Minority shareholders in an SVG IBC have limited statutory remedies if controlling members act against their interests. The court system is the primary recourse, but pursuing litigation through the Eastern Caribbean Supreme Court is expensive and slow for a foreign investor operating across multiple time zones.

Dispute resolution through local courts can cost more than the recoverable value in smaller IBCs. This structural imbalance disproportionately favors controlling shareholders, particularly in closely held entities where governance arrangements are informal.

- Shareholder agreements are not required by statute, leaving minority protections entirely to private contract

- No mandatory audit or financial disclosure requirements exist for IBCs, reducing accountability to co-investors

- Oppression remedies exist in principle but are rarely tested in SVG IBC case law

Hypothetical scenario: A foreign minority shareholder holding 30% of an SVG IBC discovers the majority shareholder has transferred company assets to a related entity without consent. Filing a claim through the Eastern Caribbean Supreme Court circuit, retaining local counsel, and pursuing the matter to judgment could realistically cost USD 25,000 to USD 60,000, often exceeding the value of the disputed transaction in smaller offshore structures.

Overcoming These Incorporation Drawbacks

Overcoming St. Vincent incorporation drawbacks requires structural decisions made before and during the incorporation process, not after problems arise.

- Open a corporate bank account in a jurisdiction with stronger correspondent banking relationships, such as the EU or Singapore, to address SVG IBC banking access limitations.

- Appoint a licensed registered agent in good standing under the International Business Companies (Amendment and Consolidation) Act to satisfy statutory agent requirements.

- Establish substance in a treaty-network jurisdiction by pairing the IBC with an entity that holds double tax agreements relevant to your primary markets.

- Implement a shareholder agreement governed by a foreign law with stronger minority protection provisions, given the limited statutory shareholder protections under SVG IBC law.

- Monitor compliance status through the Financial Intelligence Unit to stay current with SVG's FATF-related obligations and reporting requirements.

Mitigation steps operate within the boundaries set by the International Business Companies Act and local regulatory oversight. Structural solutions reduce exposure but do not eliminate the inherent limitations of this jurisdiction's framework.

St. Vincent and the Grenadines Still Worth It

Despite the disadvantages covered in this blog, St. Vincent and the Grenadines remains a functioning incorporation destination with a clear legal framework under the International Business Companies (Amendment and Consolidation) Act. Asking whether St. Vincent incorporation is worth it depends almost entirely on what your business actually requires from an offshore structure.

| Advantage | Disadvantage |

|---|---|

| Zero corporate tax on foreign-sourced income for IBCs | FATF greylisting increases compliance burdens with banks and counterparties |

| No mandatory public disclosure of beneficial owners under the IBC regime | Correspondent banking access is materially restricted for SVG-registered entities |

| Low annual maintenance costs relative to many comparable offshore jurisdictions | No meaningful double tax treaty network to reduce withholding taxes |

| Incorporation can be completed without physical presence in the jurisdiction | IBCs are legally barred from conducting business with SVG residents or local entities |

| Flexible corporate structuring under the IBC framework | Shareholder protections are weakly enforced in practice |

SVG IBCs continue to serve structures where tax neutrality and administrative simplicity matter more than banking access or treaty protection. The SVG IBC pros versus cons balance shifts unfavorably the moment your business needs active banking relationships or counterparty credibility in regulated markets.

Compliance Services for Companies in St. Vincent and the Grenadines

Maintain your SVG IBC's good standing through annual filings, registered agent requirements, and ongoing regulatory obligations under the IBC framework.

Conclusion

St. Vincent and the Grenadines IBC cons summary points to a jurisdiction that offers low-cost incorporation under the International Business Companies Act but carries structural limitations that affect real-world usability. Banking access remains the most immediate friction point, with many correspondent banks applying heightened due diligence to SVG-registered entities. The FATF greylisting has compounded that difficulty, extending scrutiny beyond banking into broader counterparty relationships. A thin double tax treaty network further limits tax planning utility for businesses with cross-border income flows. Structural guidance from experienced professionals remains relevant when forming and maintaining such an entity.

Expanship's St. Vincent Incorporation Support

Expanship's St. Vincent incorporation support is structured around the specific compliance pressures SVG IBCs face, from satisfying registered agent requirements under the International Business Companies Act to managing reputational exposure tied to the jurisdiction's FATF greylisting history. Expanship's role is to reduce the administrative weight of these obligations, not to remove the underlying requirements.

Beyond formation, the firm handles the full operational scope of getting your entity up and running:

- Company registration and preparation of all incorporation documents are handled from the outset.

- A licensed registered agent and registered office address in St. Vincent are provided to satisfy statutory requirements.

- Government filings and direct liaison with the relevant SVG regulatory authorities are managed on your behalf.

- Post-incorporation compliance, including annual renewals and record-keeping obligations, is tracked and maintained.

- Banking introduction assistance connects your entity with institutions that accept SVG-registered companies.

- Tax registration and coordination with local authorities are arranged where applicable to your structure.

Reach out to Expanship St. Vincent to discuss your incorporation requirements.

Frequently Asked Questions (FAQ)

Under the International Business Companies Act of St. Vincent and the Grenadines, IBCs are structurally prohibited from conducting business with SVG residents or owning local real property as part of their standard operating conditions. This restriction applies to all standard IBCs, not a subset. If you need to operate within the local market, you must register a different entity type, which carries different regulatory requirements.

St. Vincent and the Grenadines has one of the thinner treaty networks among Caribbean offshore centers, with very few active double tax agreements covering major trading economies. Jurisdictions like Mauritius or Cyprus maintain extensive treaty networks that SVG simply does not offer. For businesses with significant cross-border income flows, this gap creates real withholding tax exposure that other jurisdictions would eliminate by treaty.

Your IBC cannot legally continue without a licensed registered agent, as required under the International Business Companies Act. If your agent's license is revoked by the Financial Services Authority, your company risks being struck off the register if a replacement agent is not appointed within the required period. You have no direct standing to file documents or maintain compliance without going through a licensed agent.

Yes, and the exposure is meaningful. SVG IBC legislation does not provide the same statutory minority shareholder remedies found in jurisdictions like the BVI or the Cayman Islands, leaving disputes largely dependent on what the articles of incorporation specify. If your company's constitutional documents are silent or poorly drafted on minority rights, your ability to challenge majority decisions or demand buyouts is severely limited.

Registered agent fees in St. Vincent and the Grenadines typically range from a few hundred to over a thousand US dollars annually, depending on the service provider and scope of services. This is a non-negotiable recurring cost since the International Business Companies Act requires continuous appointment of a local licensed agent. Failure to maintain this appointment puts your entity's good standing at risk directly with the Financial Services Authority.

Banking access for SVG IBCs is genuinely more constrained than for entities from jurisdictions like the BVI, Cayman Islands, or even Seychelles, largely because of the FATF greylisting and the jurisdiction's limited banking relationships. Many European and North American banks now apply automatic enhanced scrutiny or outright refusal policies for SVG-registered entities. The combination of greylisting and reputational caution from compliance officers makes this a structural problem rather than a case-by-case obstacle.

Nominee structures do not remove the reputational risk attached to the jurisdiction of incorporation itself. Banks, counterparties, and regulators conduct beneficial ownership checks under international standards including FATF recommendations, which means the SVG domicile remains visible and subject to scrutiny regardless of who appears on public filings. Using nominees adds a layer of complexity without addressing the underlying concern that compliance officers have about SVG as a jurisdiction.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.