Key Takeaways

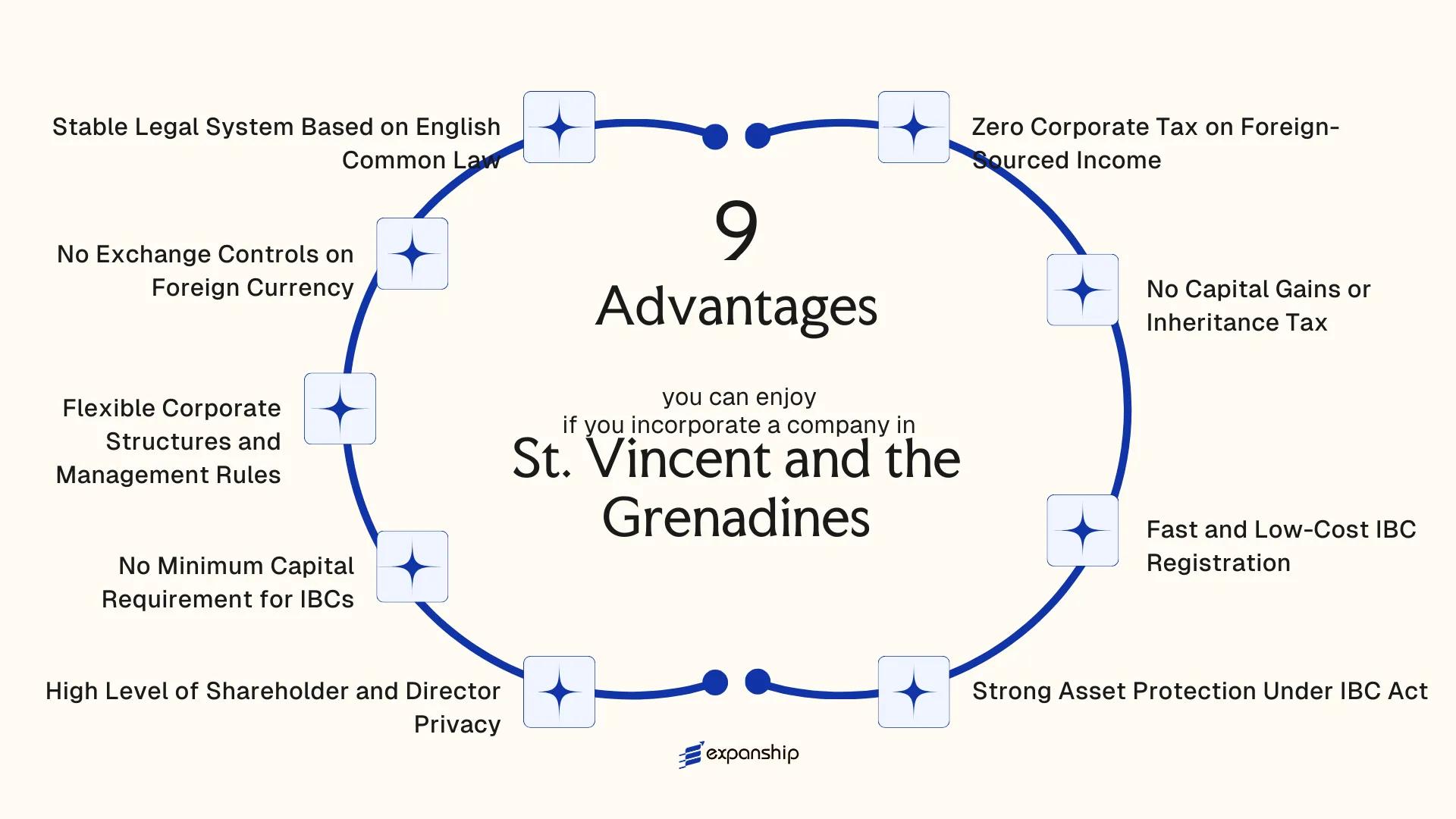

- St. Vincent and the Grenadines IBCs pay zero corporate tax on income sourced outside the jurisdiction, a statutory position established under the International Business Companies Act that directly preserves net returns for internationally operating structures.

- Shareholder and director identities are shielded from public disclosure by law, giving IBC owners a level of privacy that most higher-profile offshore jurisdictions have surrendered under current global transparency frameworks.

- No minimum capital requirement applies to IBC formation, meaning a company can be legally constituted and operational without committing a prescribed amount of funds upfront — a structural flexibility that reduces the financial barrier to entry.

- Oversight by the Financial Services Authority within a legal system grounded in English common law provides a familiar and predictable governance environment for businesses whose principals are accustomed to common law principles of contract and corporate liability.

St. Vincent and the Grenadines is an independent sovereign nation in the southeastern Caribbean, situated within the Windward Islands chain. Company registration falls under the oversight of the Financial Services Authority, the statutory body responsible for regulating and licensing financial and corporate services across the territory.

Foreign businesses incorporating here most commonly do so through an International Business Company. The jurisdiction maintains a zero-tax posture for entities that derive income outside its borders, making it a recognized choice among international entrepreneurs and holding structures. There are no restrictions on foreign ownership, and non-resident individuals or corporate entities can hold full equity in a locally registered firm without requiring a domestic partner or government approval. This article examines the principal advantages that the St. Vincent and the Grenadines company formation framework offers to businesses seeking an offshore corporate base.

Zero Corporate Tax on Foreign-Sourced Income

Under the International Business Companies Act of St. Vincent and the Grenadines, IBCs are fully exempt from corporate income tax on profits generated outside the country. This is the structural foundation of the SVG IBC tax exemption on foreign-sourced income.

What the Exemption Covers

The tax exemption applies to income earned from international operations, meaning that if your business conducts activities exclusively outside SVG, those earnings are not subject to local corporate tax. For a holding company, a trading firm, or an international consultancy structured as an IBC, this means retained earnings remain whole rather than being reduced at the corporate level before any distribution.

How This Differs from Partial Exemption Regimes

Many jurisdictions offer territorial tax systems with carve-outs or conditions that erode the benefit over time. The SVG framework, by contrast, applies the zero-rate exemption at the entity classification level rather than requiring income-by-income sourcing analysis, which reduces administrative overhead for your business.

The exemption requires that the IBC does not conduct business with residents of SVG or hold real property within the jurisdiction.

Foreign-sourced profits retained within your SVG IBC are not reduced by corporate tax, preserving the full capital base for reinvestment or distribution.

No Capital Gains or Inheritance Tax

Under the International Business Companies Act, IBCs registered in St. Vincent and the Grenadines are not subject to capital gains tax on the disposal of assets. No capital gains tax St. Vincent and the Grenadines IBC applies to profits derived from the sale of shares, securities, real property held abroad, or other investment instruments — provided those gains arise outside the jurisdiction.

For foreign investors and holding structures, this has a direct consequence: profits from asset liquidation are not eroded at the entity level, which preserves the full economic return of investment activity structured through an SVG IBC.

Inheritance tax is equally absent. When ownership of an IBC passes between generations or between parties through estate planning mechanisms, no transfer-based levy applies under SVG domestic tax law. This makes the IBC structure particularly functional for multi-generational wealth arrangements, where accumulated assets would otherwise face taxation upon transfer in higher-tax jurisdictions.

Conditions that make this regime straightforward for foreign business owners:

- The exemptions apply by statute, not by discretionary ruling, so no advance tax clearance is required

- There is no minimum holding period before capital gains treatment applies

- The absence of inheritance tax applies to the corporate structure itself, regardless of where the ultimate beneficial owners are resident

Company Incorporation in St. Vincent and the Grenadines

Register an IBC in St. Vincent and the Grenadines and access statutory capital gains and inheritance tax exemptions under the International Business Companies Act.

Fast and Low-Cost IBC Registration

Registered under the International Business Companies (Amendment and Consolidation) Act, Cap. 149, an SVG IBC can typically be incorporated within one to two business days once all required documentation is submitted to the Registrar of Companies. That speed is not incidental — it reflects a registration process deliberately structured to minimize procedural friction for foreign applicants.

The cost structure reinforces this advantage. Government filing fees for IBC registration are modest, and annual renewal costs remain low compared to many regulated offshore centers that have increased compliance-related fees in recent years. For a founder testing a new business structure or a holding entity with limited ongoing activity, lower fixed costs directly reduce the financial risk of establishing a presence.

| Factor | Detail |

|---|---|

| Standard incorporation timeline | 1 to 2 business days |

| Governing legislation | IBC (Amendment and Consolidation) Act, Cap. 149 |

| Registered agent requirement | Yes — a licensed local agent is required |

| Annual renewal obligation | Yes — due on the anniversary of incorporation |

A licensed registered agent based in St. Vincent and the Grenadines must be appointed to process the application, which means the entire procedure is handled locally without requiring the applicant's physical presence. Your business can be incorporated and fully constituted remotely, making the process accessible regardless of where the principals are located. That combination of low entry cost and fast turnaround gives an IBC practical utility from the moment it is formed.

Strong Asset Protection Under IBC Act

The IBC Act of St. Vincent and the Grenadines provides statutory protections that directly shield foreign-owned company assets from third-party claims. St. Vincent and the Grenadines IBC asset protection benefits originate from this legislation, which separates the corporate entity's assets from those of its shareholders, limiting personal exposure to the company's own liabilities.

Under the IBC framework, foreign judgments against your IBC are not automatically enforceable. A creditor must re-litigate their claim before a local court, which can considerably slow or obstruct attempts to seize assets held within the structure. This legal barrier exists by design, not by accident.

Confidentiality reinforces the protection further. Because beneficial ownership records are not part of the public registry, identifying the assets held within a specific entity requires navigating a restricted disclosure process, which narrows the practical avenues available to a creditor pursuing the business.

Keep these points in mind:

- The asset protection applies to foreign-sourced activity; IBCs are prohibited from conducting business with VC residents

- Protection is strongest when corporate formalities are maintained and the entity is not used as an alter ego

- Local courts apply English common law principles when adjudicating creditor claims against IBCs

- A fraudulent conveyance or sham transaction can void statutory protections regardless of the IBC structure

SVG IBC Act asset protection advantage extends to the point that a foreign creditor must initiate entirely new proceedings locally, meaning a judgment already won abroad carries no automatic legal weight against assets held in the IBC.

High Level of Shareholder and Director Privacy

St. Vincent and the Grenadines IBC shareholder privacy benefits are embedded directly into the country's primary corporate legislation, the International Business Companies (Amendment and Consolidation) Act, Cap. 149. Under this Act, IBCs are not required to file shareholder registers or director information with the Companies Registry as part of any publicly accessible record. That structural feature means your ownership details are not available to third parties through a standard registry search.

What the Law Permits

Nominee directors and nominee shareholders are both permitted under Cap. 149, giving you the option to place intermediaries in official roles while retaining beneficial control through private agreements. The actual beneficial owner's identity does not appear in any public-facing document. For business owners operating across multiple markets, this separation between public record and actual control is a concrete legal protection, not a contractual workaround.

Confidentiality in Practice

Registered agents in SVG are subject to AML/CFT obligations and must maintain know-your-customer records internally, but those records are held privately and are not subject to routine disclosure. Information sharing with foreign authorities is governed by treaty obligations and formal legal processes, not automatic exchange. Your identity as a beneficial owner therefore remains protected from casual inquiry, while the firm still meets international compliance standards. This balance makes the jurisdiction meaningfully different from onshore structures where director and shareholder data is routinely published at the point of incorporation.

Understand Your Privacy Options Under SVG's IBC Framework

Speak with our corporate specialists about how Cap. 149 protects your shareholder and director information when incorporating in St. Vincent and the Grenadines.

No Minimum Capital Requirement for IBCs

Under the International Business Companies (Amendment and Consolidation) Act of 2007, SVG IBCs are not required to meet any statutory minimum paid-up capital threshold. A key no minimum capital requirement SVG IBC benefit is that founders can issue a single share at a nominal value, or structure the company with a large authorized share capital at low cost, without the requirement to deposit funds into a local account before commencing operations.

- Your company can be incorporated and fully operational without tying up funds in a paid-in capital account, which directly reduces the upfront financial commitment required to establish a legal presence.

- Authorized share capital can be divided into shares of any par value, or issued as no-par-value shares, giving founders flexibility to structure equity in a way that reflects the actual economics of the business.

- Because capital structure is not dictated by a statutory floor, foreign shareholders can adjust share distribution and ownership percentages at the formation stage without triggering capital adequacy concerns.

- This framework is particularly useful for holding companies, intellectual property vehicles, and trading firms that do not require capitalized balance sheets to fulfill their operational purpose.

The absence of a mandatory capital floor does not remove the general legal obligation to maintain adequate resources to meet the entity's liabilities as they fall due.

Flexible Corporate Structures and Management Rules

St. Vincent and the Grenadines IBC flexible corporate structure benefits stem directly from the International Business Companies (Amendment and Consolidation) Act. Under this legislation, an IBC is not required to hold annual general meetings, and those meetings that do occur can be held in any country. Directors and shareholders can be of any nationality and reside anywhere in the world.

A single individual can simultaneously serve as the sole director and sole shareholder of an IBC. This removes the need to appoint nominee officers or distribute equity among multiple parties simply to satisfy structural minimums, which reduces both administrative overhead and ongoing costs.

Corporate directors are permitted, meaning another company can fulfill the director role rather than a named individual. Your business can also issue shares in multiple classes, with or without par value, giving you discretion over how economic rights and voting rights are allocated across stakeholders.

Decisions can be passed by written resolution rather than formal meetings, provided the Act's procedural conditions are met. For internationally mobile founders managing entities across time zones, this eliminates scheduling constraints that add friction to routine governance.

A founder operating a consulting firm through an SVG IBC from three different countries across a calendar year would not trigger any residency-based meeting requirement or board composition rule under the IBC Act, keeping governance decisions entirely within their own schedule and jurisdiction.

No Exchange Controls on Foreign Currency

St. Vincent and the Grenadines imposes no exchange controls on IBCs, meaning your company can hold, transfer, and convert foreign currency without restriction. This is a direct outcome of the International Business Companies Act, which governs offshore entities and explicitly keeps them outside the domestic monetary control framework administered by the Eastern Caribbean Central Bank.

For a business operating across multiple currencies, the practical consequence is straightforward: funds can move in and out of accounts freely, without requiring central bank approval or triggering mandatory conversion requirements. Operational efficiency depends heavily on this kind of unrestricted capital movement, particularly for firms managing receivables in USD, EUR, GBP, or other major currencies simultaneously.

Under this framework, your IBC can:

- Open and maintain multi-currency bank accounts

- Receive international payments without conversion mandates

- Repatriate profits to any jurisdiction without prior authorization

- Settle intercompany transactions in the currency of your choosing

This absence of currency restrictions directly reduces the administrative overhead that exchange control regimes typically impose on cross-border transactions.

Exchange control exemptions apply specifically to IBCs conducting business outside SVG; any domestic business activity may be subject to different regulatory treatment.

Stable Legal System Based on English Common Law

St. Vincent and the Grenadines English common law business benefits stem from the jurisdiction's position as a member of the Eastern Caribbean Supreme Court (ECSC) system. The ECSC operates across nine member territories and applies principles rooted in English common law, giving your business access to a legal framework that has governed commercial disputes for centuries.

Predictable Judicial Interpretation

Courts in SVG interpret contracts, corporate structures, and commercial agreements using established common law doctrines. This means legal outcomes are more foreseeable, which reduces uncertainty when drafting shareholder agreements, service contracts, or cross-border arrangements involving an SVG-incorporated entity.

Recognized Legal Framework for Offshore Structures

The International Business Companies (Amendment and Consolidation) Act governs IBCs registered in the jurisdiction. Because this legislation is built on common law principles, foreign legal counsel familiar with English law traditions can interpret it without needing to study an entirely different legal system. That compatibility lowers your legal costs and shortens review timelines.

Appeals Through Regional Judicial Structure

Final appeals from SVG courts can be heard by the Caribbean Court of Justice or, in some cases, reach the Privy Council in London. This tiered structure means commercial disputes are not confined to a single national court, and decisions are subject to review by experienced jurists operating within a recognized legal tradition.

- The ECSC shares legal precedents across member states, so rulings from other jurisdictions within the court system can inform SVG commercial cases

- Common law contract enforcement principles apply directly to IBC agreements without requiring separate statutory codification

Why St. Vincent and the Grenadines Stands Apart from Competing Offshore Jurisdictions

Comparing SVG against other offshore jurisdictions reveals a consistent pattern: the combination of statutory tax exemptions under the International Business Companies Act and minimal administrative requirements positions it differently from jurisdictions that have narrowed their offshore offerings in response to international pressure. The competitors most relevant to a foreign investor evaluating SVG are Belize, Seychelles, and Panama — each targeting a similar IBC-oriented client base and operating within comparable cost brackets.

What the table below cannot capture is the structural consistency SVG has maintained. Several competing jurisdictions have introduced beneficial ownership registries or tightened nominee arrangements following FATF reviews, increasing compliance overhead for foreign-held entities. SVG's IBC framework, governed by the International Business Companies Act, has not introduced mandatory public disclosure of beneficial owners for offshore structures, which remains a material distinction for investors who have watched similar privacy protections erode elsewhere.

| Parameter | St. Vincent and the Grenadines | Belize | Seychelles | Panama |

|---|---|---|---|---|

| Corporate Tax on Foreign Income | 0% | 0% | 0% | 0% |

| Annual Government Fee (approx.) | Low, from USD 100 | Low, from USD 100 | Low, from USD 100 | Moderate, from USD 300 |

| Director/Shareholder Privacy | High, no public register for IBCs | High | High | Moderate, some public filing |

| Minimum Share Capital | None | None | None | None |

| English Common Law System | Yes | Yes | Hybrid (civil/common) | Civil law |

| Exchange Controls on Foreign Currency | None | None | None | None |

Compliance Services for Your SVG Company

Maintain your IBC's good standing in St. Vincent and the Grenadines with Expanship's compliance support, covering annual renewals, registered agent requirements, and regulatory filings.

Conclusion

The benefits of incorporating in St. Vincent and the Grenadines rest on a coherent legal and fiscal framework rather than a single standout feature: the International Business Companies Act creates a tax-neutral environment for foreign-sourced income, the IBC structure carries no minimum capital threshold, and shareholder identity is shielded from public disclosure by statute.

Two factors distinguish this case most clearly. Zero corporate tax on foreign-sourced income means profits generated outside the jurisdiction are not subject to local taxation, a structural advantage that directly affects the net returns available to your business. Pair that with the statutory privacy protections available to IBC directors and shareholders, and the entity offers a level of operational discretion that many comparable structures in higher-profile jurisdictions cannot match under current transparency regimes.

Whether this framework aligns with your situation depends on your business model, the jurisdictions where income is generated, and how your home country treats foreign-incorporated entities under its controlled foreign corporation rules. For structures where those conditions are satisfied, the IBC framework in St. Vincent and the Grenadines represents a legally grounded, cost-efficient option. The next practical step is matching that framework to your specific ownership structure, operational requirements, and long-term compliance obligations.

Start Your St. Vincent and the Grenadines Company with Expanship Today

To start a St. Vincent and the Grenadines company with Expanship, you work with a team that handles IBC formation directly under the International Business Companies (Amendment and Consolidation) Act. From confirming name availability with the Registrar of International Business Companies to preparing your Memorandum and Articles of Association, each step is managed in accordance with the requirements of FSA oversight and local corporate registry procedures.

Expanship's service scope covers the full formation and maintenance cycle for your SVG entity:

- Corporate document preparation, notarization, and legalization

- Registered agent and registered office provision in St. Vincent

- Government filing and Registrar of International Business Companies liaison

- Post-incorporation compliance management, including annual renewal obligations

- Banking introduction assistance for offshore account setup

- Ongoing corporate secretarial support

Reach out to Expanship SVG to discuss your incorporation requirements.

Frequently Asked Questions (FAQ)

An IBC incorporated under the International Business Companies Act pays zero corporate tax on income sourced outside St. Vincent and the Grenadines. This exemption applies for the period specified in the Act, provided the entity does not conduct business with residents or engage in activities within the domestic economy. Income generated locally would be subject to standard domestic tax rules.

Registration is generally completed within one to three business days once the required documentation is submitted to the Registrar of Companies. The process does not involve a paid-up capital requirement, which removes a common administrative delay found in other jurisdictions. Exact timelines may vary depending on document preparation and the registered agent used.

A local registered office and a licensed registered agent are required under the International Business Companies Act, but directors do not need to be resident in St. Vincent and the Grenadines. Corporate directors are generally permitted, which allows offshore management structures to remain intact. The registered agent serves as the point of contact with the Registrar of Companies.

Failure to meet annual renewal or compliance requirements can result in the company being struck off the register by the Registrar of Companies. A struck-off entity loses its legal standing and cannot enter into contracts or enforce its rights. Reinstatement may be possible within a prescribed period, though this involves additional fees and procedural steps.

SVG has faced scrutiny from international bodies at various points, and its status on monitoring lists can change following policy reviews. Current listing status directly affects how banks and counterparties in certain jurisdictions treat the entity, including account-opening feasibility and counterparty due diligence requirements. Verifying the jurisdiction's current standing with the Financial Action Task Force and the EU's list of non-cooperative tax jurisdictions before incorporation is a practical step.

Under the International Business Companies Act, assets held within a properly structured IBC are subject to SVG law, which means foreign judgments are not automatically enforceable and must go through local legal proceedings. This creates a procedural barrier that can complicate enforcement actions originating in other jurisdictions. The level of protection depends on how the company is structured and whether assets are genuinely held at the corporate level rather than attributed directly to an individual.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.