Key Takeaways

- Every company incorporated in the Turks and Caicos Islands must appoint a locally licensed registered agent, as mandated under the Companies Ordinance administered by the Financial Services Commission.

- Beneficial ownership information must be disclosed and maintained in compliance with the Beneficial Ownership Secure Search System Act, which applies to all registered entities in the territory.

- Directors and shareholders are subject to KYC documentation requirements at the point of registration, meaning identity and address verification materials must be submitted before a company achieves valid standing.

- The Financial Services Commission serves as the principal regulatory body overseeing entity formation in TCI, and failure to meet its structural or documentary requirements can result in application rejection or post-registration cancellation of company status.

Incorporation requirements in Turks and Caicos are governed primarily by the Companies Ordinance, administered through the Financial Services Commission (FSC), which serves as the principal regulatory body overseeing entity formation and licensing in the territory.

This article addresses the structural, documentary, and regulatory requirements applicable to businesses seeking registration under TCI business incorporation regulations.

Failure to satisfy these requirements results in rejection of the application or, where deficiencies are discovered post-registration, potential administrative penalties or cancellation of the company's standing.

Requirements under Turks and Caicos company registration requirements can differ depending on the entity type selected, the sector in which the business operates, and the residency status of its principals.

Foreign investors and non-resident business owners structuring international holding companies or offshore entities under TCI IBC requirements will find this article most directly applicable to their situation.

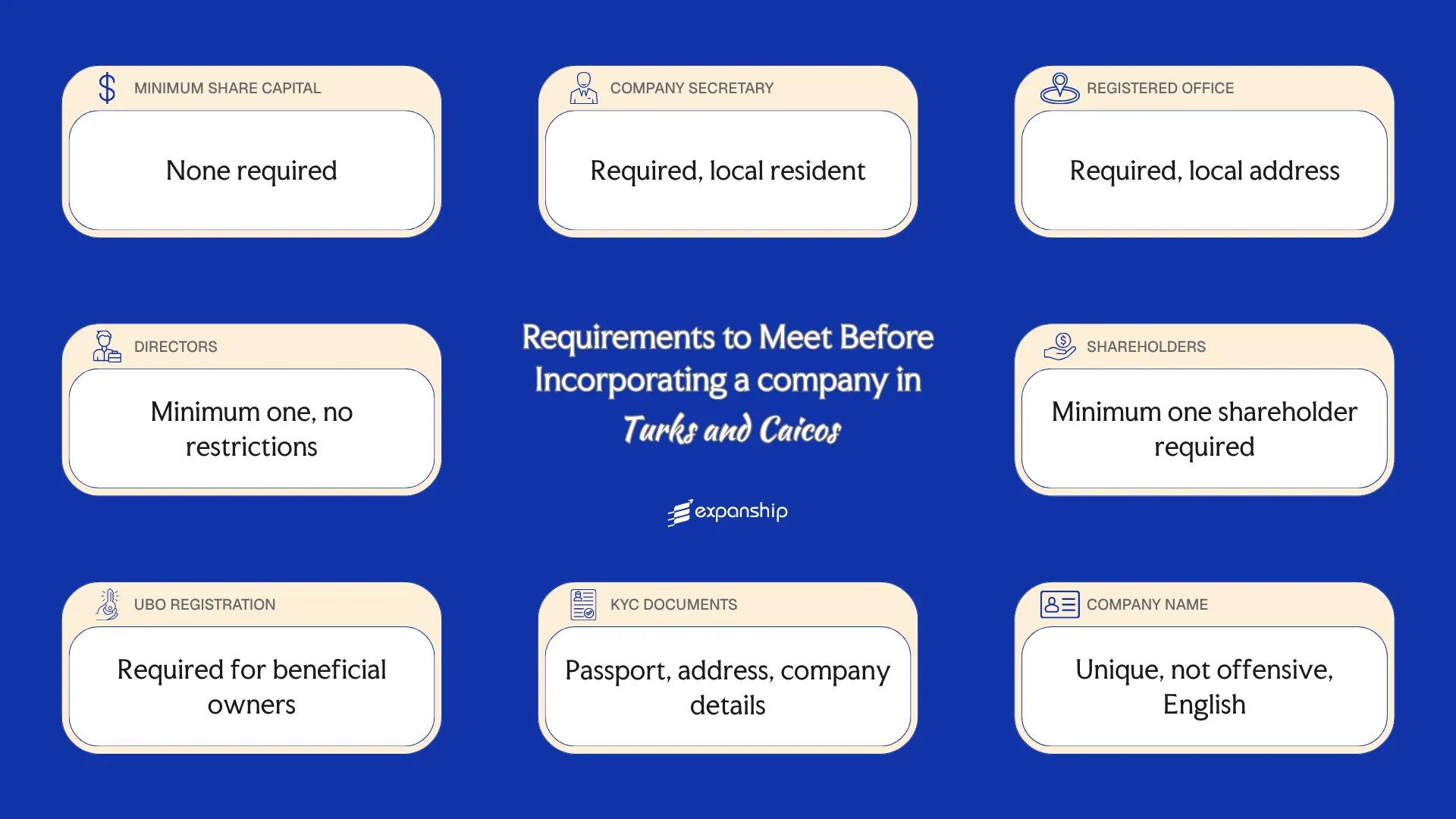

Minimum Share Capital Requirements in Turks and Caicos

Under the Companies Ordinance and the International Business Companies Ordinance governing Turks and Caicos share capital requirements, no minimum authorized share capital is mandated for company formation. Both resident and IBC structures can be incorporated without depositing a set capital amount, though an authorized share capital figure must still be declared in the constitutional documents.

Shares may be issued with or without par value, depending on how the articles of association are drafted. The General Registry of the Turks and Caicos Islands oversees incorporation filings but does not require evidence of capital deposit as a precondition for registration.

| Parameter | Detail |

|---|---|

| Minimum Authorized Share Capital | No statutory requirement |

| Maximum Authorized Share Capital | No statutory cap |

| Minimum Paid-Up Capital | No statutory requirement |

| Paid-Up Requirement at Incorporation | None |

| Accepted Currency | USD and other major currencies |

| Accepted Forms of Contribution | Cash and non-cash assets |

| Timeframe to Deposit Capital | No statutory timeframe |

No minimum capital requirement does not eliminate the need to state an authorized share capital structure in your memorandum and articles. Omitting this detail can cause the General Registry to reject or return the filing.

Registered Agent Requirements in Turks and Caicos

All companies incorporated under the Companies Ordinance in Turks and Caicos are required to appoint a registered agent. Turks and Caicos registered agent requirements apply to both International Business Companies and domestic entities, making this a universal obligation rather than an optional arrangement.

The registered agent acts as the formal point of contact between your company and the Financial Services Commission, the territory's principal regulatory authority. Responsibilities include maintaining statutory records, receiving official correspondence, and ensuring the company remains in good standing with filing obligations.

Qualification criteria for serving as a registered agent:

- Must hold a valid licence issued by the Financial Services Commission of the Turks and Caicos Islands

- Only corporate entities or individuals meeting the FSC's prescribed fit-and-proper standards are eligible

- Physical presence within the territory is required; foreign-based agents cannot fulfil this role

- The agent must operate from a registered office address within the jurisdiction

- Ongoing compliance with FSC conduct and reporting standards is a condition of licence retention

Incorporate a Company in Turks and Caicos Islands

Set up your business entity in TCI with full compliance support, from name reservation through to certificate of incorporation.

Registered Office Requirements in Turks and Caicos

Turks and Caicos registered office requirements are governed by the Companies Ordinance, which mandates that every company incorporated in the territory maintain a registered office address at all times within the Turks and Caicos Islands. Failure to maintain a compliant address can result in the company being struck off the register by the Financial Services Commission.

- A physical street address within the Turks and Caicos Islands is required; a P.O. Box alone does not satisfy this requirement.

- Virtual offices are generally not accepted as a standalone registered office address under local compliance standards.

- The address must be locally based; an overseas address does not fulfil TCI company registered address obligations.

- No ownership of the premises is required, but a valid lease or occupancy arrangement must support the use of the address.

- The registered office address is recorded on the public register maintained by the Financial Services Commission and is accessible to third parties.

- Any change to the registered office address must be formally notified to the Financial Services Commission, and the updated address takes effect only upon registration of that change.

Director Requirements in Turks and Caicos

Under the Companies Ordinance and the International Business Companies Ordinance, directors of a Turks and Caicos company assume fiduciary duties to act in the best interests of the entity and exercise reasonable care and diligence in carrying out their responsibilities. Liability for statutory breaches, including acting outside the company's authorized powers or failing to maintain proper records, attaches personally to the director upon appointment.

| Parameter | Detail |

|---|---|

| Minimum Number of Directors | One director is required. |

| Maximum Number of Directors | No statutory maximum is prescribed. |

| Local/Resident Director Required | No local or resident director is required. |

| Nationality Restrictions | No nationality restrictions apply. |

| Minimum Age Requirement | Directors must be at least 18 years of age. |

| Corporate Directors Permitted | Corporate directors are permitted under the ordinance. |

| Director Must Be a Shareholder | No requirement for a director to hold shares in the company. |

| Publicly Listed on Registry | Director information is not part of the public registry record for IBCs. |

| Disqualification Conditions | A person who has been declared bankrupt or convicted of a relevant criminal offence may be disqualified from serving. |

Despite requiring only one director with no residency obligation, TCI IBC director details are kept off the public register entirely, meaning no director names appear in any publicly searchable filing.

Shareholder Requirements in Turks and Caicos

Under the Companies Ordinance of the Turks and Caicos Islands, an International Business Company (IBC) requires a minimum of one shareholder. No statutory maximum applies, making both sole-shareholder structures and multi-member arrangements permissible.

Nationality and Residency Restrictions

Shareholders face no nationality or residency requirements under TCI company law. Foreign nationals and non-resident individuals may hold 100% of shares without restriction.

Corporate Shareholders

Corporate entities are permitted to act as shareholders in a TCI IBC. No additional conditions specific to corporate shareholding are imposed beyond standard KYC obligations.

Shareholder Liability

Shareholder liability is limited to the amount unpaid on their shares. No general circumstances under the Companies Ordinance extend personal liability beyond that contribution, except in cases of fraud or improper conduct established by a court.

Register of Shareholders

Your company must maintain an internal register of shareholders. This register is not publicly accessible, though it must be kept at the registered office and updated to reflect any changes in share ownership.

Get Guidance on Shareholder Compliance for Your TCI Entity

Speak with our team about structuring shareholding correctly under Turks and Caicos Islands company law before incorporation.

UBO / Beneficial Ownership Disclosure Requirements in Turks and Caicos

Under the beneficial ownership requirements Turks and Caicos framework, a beneficial owner is defined as any individual who ultimately owns or controls 10% or more of the shares or voting rights of a company, as established under the Beneficial Ownership Register of Legal Entities Ordinance 2019.

- Identify all individuals meeting the 10% ownership or control threshold at the time of incorporation.

- Submit beneficial ownership information to the designated competent authority through the licensed registered agent.

- Record the data in the private Beneficial Ownership Register, which is maintained by the registered agent on behalf of the company.

- Notify the competent authority of any changes to beneficial ownership within 30 days of the change occurring.

| Parameter | Detail |

|---|---|

| Ownership Threshold for UBO Status | 10% or more of shares or voting rights |

| Filing Authority | Competent Authority via licensed registered agent |

| Disclosure Deadline at Incorporation | At the time of incorporation |

| Publicly Accessible Register | No; the register is private |

| Penalties for Non-Disclosure | Civil and criminal penalties under the 2019 Ordinance |

| Ongoing Update Obligation | Yes; updates required within 30 days of any change |

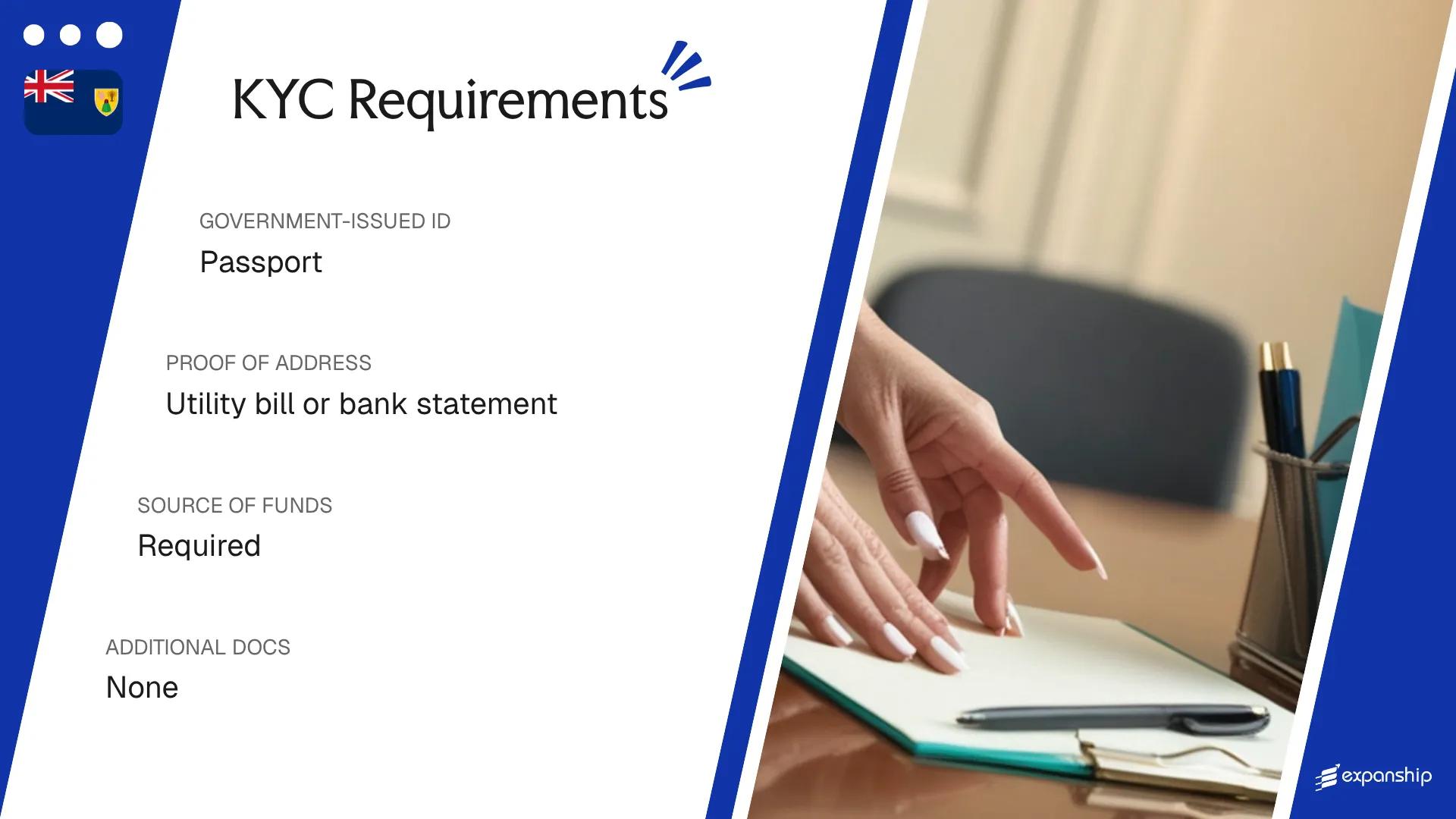

KYC / Document Requirements in Turks and Caicos

KYC requirements Turks and Caicos incorporation are governed by the Financial Intelligence Agency Act and the Anti-Money Laundering and Prevention of Terrorist Financing Regulations, which require registered agents to collect and verify identity documentation before a company can be formed under the FIA.

Individual / Personal Documents

- Certified copy of a valid government-issued passport or national identity card

- Proof of residential address dated within three months, such as a utility bill or bank statement

- Signed and dated KYC declaration or consent form where required by the registered agent

- Recent passport-sized photograph may be requested depending on the agent's internal compliance policy

Corporate Documents

- Certificate of incorporation or equivalent formation document for the corporate shareholder or director

- Constitutional documents, including articles of association or memorandum

- Register of directors and register of shareholders for the corporate entity

- Proof of registered office address for the corporate entity

Source of Funds Documentation

- Recent bank statements covering a minimum of three to six months

- Audited financial statements or accountant-prepared accounts where bank statements are insufficient

- Written explanation of the origin of capital if funds derive from a business sale or inheritance

Notarisation and Apostille Requirements

- Foreign-issued identity documents generally require notarisation by a qualified notary public

- Documents originating outside Commonwealth jurisdictions may require an Apostille under the Hague Convention

- Official translations into English are required for any document not originally in English

Mismatched names across identity documents and corporate records are the most frequent cause of KYC rejection at the incorporation stage.

Company Name Requirements in Turks and Caicos

Company name requirements in Turks and Caicos are assessed by the registry at the point of incorporation, with names evaluated for uniqueness and general suitability. A proposed name that is identical or confusingly similar to an existing registered entity will be rejected.

Structurally, the name must include a legal suffix indicating limited liability, such as "Limited" or "Ltd." English is the standard language of registration, though transliterated or foreign-language names may be considered on a case-by-case basis.

Certain words are restricted and require prior consent from relevant authorities before use — terms implying government affiliation, banking, insurance, or royal connection fall into this category. Words considered offensive or misleading are prohibited outright.

Name reservation is available and can be requested prior to formal incorporation, giving your business time to prepare documentation under a secured name. Reservations are generally valid for a limited period, after which the name returns to the available pool if incorporation has not proceeded.

Compliance Services for Companies in Turks and Caicos

Maintain your company's good standing in Turks and Caicos with ongoing compliance support, including annual filings, registered agent maintenance, and regulatory reporting.

Conclusion

Meeting the incorporation requirements Turks and Caicos sets out under the Companies Ordinance and the Financial Services Commission's regulatory framework involves several distinct obligations. Among the most consequential are the mandatory appointment of a licensed registered agent, adherence to UBO disclosure requirements under the Beneficial Ownership Secure Search System Act, and compliance with KYC documentation standards at the point of registration. Once these requirements are understood, a foreign investor's practical next step is assembling the necessary documentation and identifying a locally licensed agent to begin the formal filing process.

Expanship Services for Turks and Caicos Expansion

Engaging a professional services provider that understands TCI's specific regulatory structure, including the Financial Services Commission's oversight of IBCs and the requirements tied to beneficial ownership registers, reduces the administrative load of getting your entity properly established and maintained.

Expanship's Turks and Caicos company formation services cover the full scope of what incorporation here actually requires, from initial registration through ongoing compliance.

- Your company registration and all supporting document preparation are handled on your behalf, tailored to TCI's statutory requirements.

- A licensed registered agent and a compliant registered office address in the Turks and Caicos Islands are provided as part of your setup.

- All government filings and liaison with the Financial Services Commission are managed directly by our team.

- Post-incorporation compliance management keeps your entity in good standing year over year.

- Banking introduction assistance is available to support your operational setup.

- Tax registration and coordination with relevant local authorities are handled as part of your engagement.

Reach out to Expanship Turks and Caicos to discuss your incorporation requirements.

Frequently Asked Questions (FAQ)

Failure to maintain a registered office can result in the company falling out of good standing with the Turks and Caicos Islands Financial Services Commission, which may lead to administrative dissolution. Reinstatement typically requires settling outstanding fees and penalties before the entity can resume normal legal standing.

Corporate directors are permitted under the TCI IBC framework, meaning another legal entity can be appointed to the board. However, your company must still meet any minimum director count requirements and ensure that the corporate director itself has a defined legal presence and is in good standing in its home jurisdiction.

No minimum paid-up capital is required for an IBC to be incorporated in the Turks and Caicos. The authorized share capital can be set at a nominal level, which is one reason the jurisdiction attracts holding and asset-protection structures.

Foreign nationals are required to submit certified identification, such as a passport, along with proof of residential address dated within a specified recent period. The registered agent is responsible for collecting and verifying these documents in line with the Financial Services Commission's anti-money laundering guidelines before incorporation proceeds.

Beneficial ownership information submitted under the TCI framework is held in a non-public register accessible to competent authorities rather than open to general public inspection. This means your UBO details are disclosed to regulators for oversight purposes without being exposed to commercial third parties.

The Financial Services Commission reviews proposed company names and can reject any name it considers identical or deceptively similar to an existing registered entity, offensive, or otherwise contrary to the public interest. Submitting a name for pre-clearance before filing formal incorporation documents reduces the risk of delays caused by a rejected name.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.