Key Takeaways

- Sint Maarten maintains its own corporate legal framework as a constituent country of the Kingdom of the Netherlands, distinct from Dutch law proper, with the Chamber of Commerce Sint Maarten administering the Commercial Register.

- The Besloten Vennootschap (BV) is the most commonly registered corporate entity in Sint Maarten, making it the default choice for closely held private companies.

- Businesses operating in financial services may face dual regulatory oversight, requiring licensing from the Central Bank of Curaçao and Sint Maarten in addition to Chamber of Commerce registration.

- Available legal forms span from the publicly oriented Naamloze Vennootschap (NV) to informal sole proprietorships (Eenmanszaak), with partnerships, foundations (Stichting), and foreign branch structures filling the range in between.

Introduction to Entity Types in Sint Maarten

Sint Maarten is a constituent country of the Kingdom of the Netherlands, occupying the southern portion of a Caribbean island shared with the French collectivity of Saint-Martin. Situated in the northeastern Caribbean, it lies within the Leeward Islands group, near Anguilla, Saint Barthélemy, and Saint Kitts. As a constituent country, it maintains its own legal and corporate framework, distinct from that of the Netherlands proper.

Company registration and ongoing compliance fall under the oversight of the Chamber of Commerce Sint Maarten, which maintains the Commercial Register. Depending on the nature of the business, certain financial activities also require licensing from the Central Bank of Curaçao and Sint Maarten.

Sint Maarten operates a low-tax regime, with corporate and personal income tax rates that remain materially lower than most OECD jurisdictions.

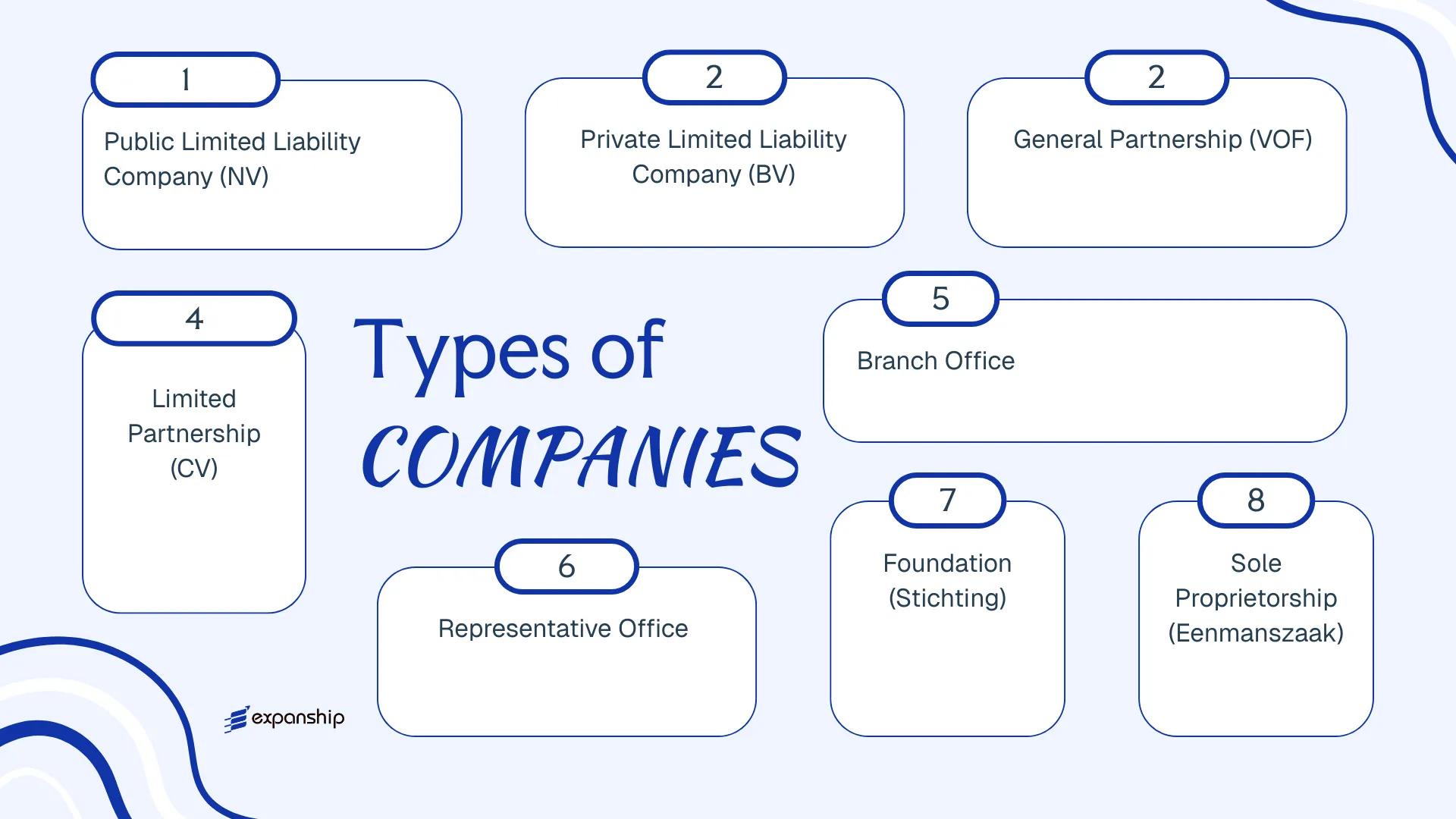

The business entity types Sint Maarten makes available include the Naamloze Vennootschap (NV), the Besloten Vennootschap (BV), the Vennootschap onder Firma, the Commanditaire Vennootschap, the Stichting, the Eenmanszaak, and several forms of foreign business presence. Each of these Sint Maarten company structures carries distinct liability, governance, and tax characteristics that this article examines in turn.

An Overview of Business Structures in Sint Maarten

Sint Maarten's company law framework provides several distinct legal forms for conducting business, governed primarily by the Civil Code of Sint Maarten (Burgerlijk Wetboek) and supplemented by specific national ordinances. Each structure carries different implications for liability, taxation, governance, and permitted activities.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Naamloze Vennootschap (NV) | Public limited company | Limited to share capital | Subject to profit tax | Permitted | 1 shareholder | Chamber of Commerce Sint Maarten | Civil Code of Sint Maarten |

| Besloten Vennootschap (BV) | Private limited company | Limited to share capital | Subject to profit tax | Permitted | 1 shareholder | Chamber of Commerce Sint Maarten | Civil Code of Sint Maarten |

| Vennootschap onder Firma (VOF) | General partnership | Unlimited, joint & several | Partners taxed personally | Permitted | 2 partners | Chamber of Commerce Sint Maarten | Commercial Code |

| Commanditaire Vennootschap (CV) | Limited partnership | Mixed: general/limited | Partners taxed personally | Permitted | 1 general, 1 limited partner | Chamber of Commerce Sint Maarten | Commercial Code |

| Stichting | Foundation | Limited | Generally exempt | Restricted | 1 founder | Chamber of Commerce Sint Maarten | Civil Code of Sint Maarten |

| Eenmanszaak | Sole proprietorship | Unlimited, personal | Owner taxed personally | Permitted | 1 owner | Chamber of Commerce Sint Maarten | Commercial Code |

| Branch Office | Foreign entity extension | Parent company liable | Subject to local profit tax | Permitted | Parent company | Chamber of Commerce Sint Maarten | National Ordinance |

| Representative Office | Non-trading presence | Parent company liable | Generally not taxed | Not permitted | Parent company | Chamber of Commerce Sint Maarten | National Ordinance |

Each of these structures is examined in full in the sections below.

Naamloze Vennootschap (NV)

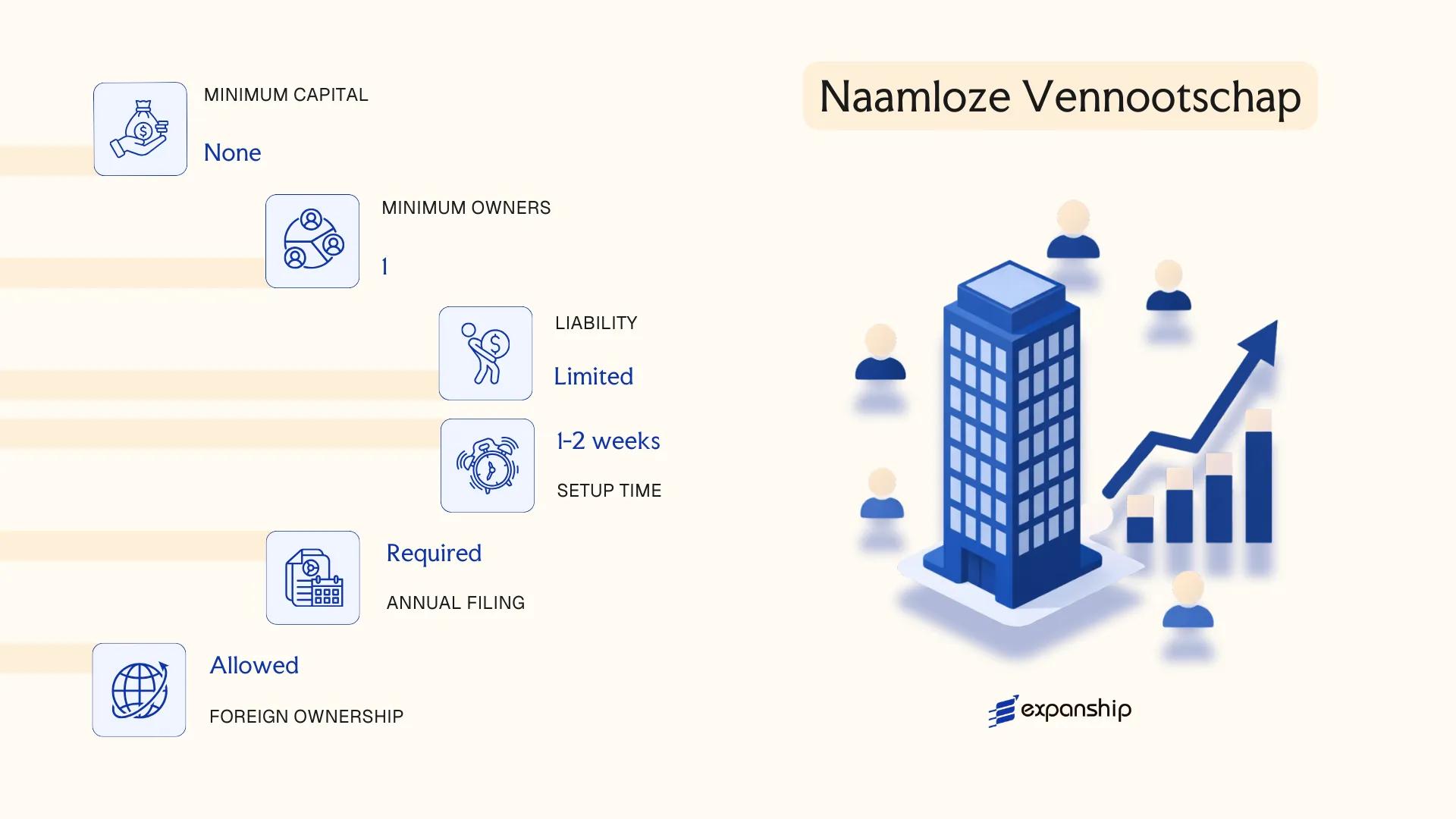

The Naamloze Vennootschap Sint Maarten NV is governed by the National Ordinance on Corporations (Landsverordening op de Naamloze Vennootschappen, PB 1946, no. 46), as amended and applicable under Sint Maarten's autonomous legal framework following the 2010 constitutional reform. It carries separate legal personality, meaning the entity itself holds rights and obligations distinct from its shareholders.

Shares in an NV are freely transferable unless the articles of incorporation impose restrictions, which distinguishes this structure from its BV counterpart. This transferability makes the NV company Sint Maarten framework particularly relevant for businesses seeking capital market access or multi-investor arrangements.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Naamloze Vennootschap (NV) | Public capital company with separate legal personality |

| Members | Shareholders and Directors; minimum 1 shareholder, no maximum | Directors manage the company; shareholders hold equity |

| Local Presence | Registered office in Sint Maarten required | A local registered agent is standard practice |

| Share Capital | No statutory minimum in ANG (Antillean Guilder) or USD | Capital and currency defined in articles of incorporation |

| Share Transferability | Shares freely transferable by default | Restrictions must be explicitly included in the articles |

| Privacy | Shareholder register not publicly disclosed | Director details filed with the Chamber of Commerce |

Focus Points

- Taxation: Sint Maarten imposes a corporate profit tax at a standard rate; no VAT currently applies, though turnover tax (BBO) may be applicable; withholding tax applies to dividend distributions in certain circumstances.

- Economic Substance: Entities engaged in relevant activities must demonstrate genuine economic presence, including local management and operational activity.

- Annual Compliance: Annual financial statements must be prepared; filing obligations with the Chamber of Commerce apply, including directorship updates.

- Conversion: An NV may be converted to a BV under applicable ordinance provisions, subject to notarial deed and regulatory formalities.

- Restrictions: Bearer shares are not permitted; the entity must be incorporated by notarial deed before a Sint Maarten civil law notary.

Closing

The NV suits holding structures, joint ventures, and businesses anticipating multiple investors or eventual share distribution, with freely transferable shares offering structural flexibility. Its primary limitation is the comparatively higher administrative overhead relative to simpler entity forms, particularly for single-owner operations.

The NV is most appropriate for multi-shareholder businesses, investment holding companies, or ventures where share transferability and capital structure flexibility are operational priorities.

Register a Company in Sint Maarten

Expanship assists with NV incorporation, notarial coordination, and ongoing compliance in Sint Maarten.

Besloten Vennootschap (BV)

The Besloten Vennootschap Sint Maarten BV is a private limited liability company governed by the Civil Code of Sint Maarten (Burgerlijk Wetboek), which draws from the Dutch Caribbean legal framework established following the 2010 constitutional reforms. As a distinct legal entity, the BV holds its own rights and obligations separately from its shareholders, meaning personal assets are generally shielded from business liabilities.

Shares in a BV are registered and cannot be freely transferred without shareholder consent or approval mechanisms prescribed in the articles of incorporation, distinguishing this structure from its publicly traded counterpart. This characteristic makes the BV a contained, privately governed structure suited to closely held business operations.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private limited liability company | Separate legal personality; governed by Sint Maarten Civil Code |

| Members | Shareholders and Directors | Minimum 1 shareholder; minimum 1 director; no maximum imposed by statute; director may be corporate |

| Local Presence | Registered office address required in Sint Maarten | No mandatory local director, but registered address must be maintained |

| Share Capital | ANG (Netherlands Antillean Guilder); no statutory minimum capital requirement under current rules | Shares must be registered; bearer shares are not permitted |

| Share Transferability | Restricted transfer; requires shareholder approval or deed of transfer | Transfer restrictions must be reflected in articles of incorporation |

| Privacy | Shareholder details recorded in company register; not fully public | Beneficial ownership disclosure obligations apply under local regulations |

Focus Points

- Taxation: The BV is subject to profit tax (corporate income tax) in Sint Maarten; no VAT currently applies, though turnover tax (BBO) may apply to certain activities; dividend withholding tax may apply on distributions depending on applicable rules and recipient status.

- Economic Substance: BVs engaged in certain activities may be subject to economic substance requirements under Sint Maarten's legislation aligned with international BEPS standards.

- Annual Compliance: Annual financial statements must be prepared; the entity must remain in good standing with the Chamber of Commerce (Kamer van Koophandel) of Sint Maarten.

- Conversion: A BV may be converted into an NV subject to compliance with the procedural requirements under the Civil Code, including notarial deed and amendment of articles.

- Restrictions: BV shares cannot be listed on a public stock exchange; the transfer restriction mechanism must be explicitly addressed in the constitutional documents.

Closing Paragraph

The BV is commonly used for trading operations, holding structures, and family-owned businesses where ownership control and share transfer restrictions are priorities. The built-in transfer restrictions offer a degree of governance certainty, though they can also slow down capital restructuring when investor flexibility is needed.

The BV structure is best suited for closely held businesses, family enterprises, and investors seeking a private corporate vehicle with controlled ownership and limited personal liability.

Partnerships in Sint Maarten [Vennootschap onder Firma, Commanditaire Vennootschap]

Sint Maarten recognises two principal partnership structures under civil law derived from the former Netherlands Antilles legal framework: the Vennootschap onder Firma (VOF), a general partnership, and the Commanditaire Vennootschap (CV), a limited partnership. Both structures are unincorporated and lack separate legal personality, meaning the partners — not a distinct legal entity — bear the rights and obligations arising from business activities.

Partnerships Sint Maarten VOF CV arrangements are registered with the Chamber of Commerce of Sint Maarten (COCI). The VOF binds all partners with unlimited joint and several liability, while the CV introduces a two-tier structure: general partners with unlimited liability and silent (commanditaire) partners whose exposure is capped at their contributed capital.

Key Characteristics

| Requirement | VOF (General Partnership) | CV (Limited Partnership) |

|---|---|---|

| Legal Personality | None | None |

| Members | Partners (minimum 2, no statutory maximum) | At least 1 general partner + 1 limited partner |

| Liability | All partners: unlimited, joint and several | General partner: unlimited; limited partner: capped at capital contribution |

| Local Presence | Registered office address in Sint Maarten; registration with COCI | Same as VOF |

| Capital | No minimum capital requirement; contributions may be cash, labour, or assets | No minimum; limited partner's contribution defines liability ceiling |

| Privacy | Partner names disclosed in COCI registration | General partner disclosed; limited partner identity may have limited disclosure depending on structure |

Focus Points

- Taxation: Partnerships are fiscally transparent; profits are attributed directly to partners and taxed at the individual or corporate level depending on partner type, with no separate entity-level income tax, no withholding tax at partnership level, and no VAT currently applied in Sint Maarten.

- Economic Substance: As pass-through vehicles without separate legal personality, VOF and CV structures are not typically subject to the same economic substance requirements that apply to incorporated entities, though underlying activities may attract scrutiny.

- Annual Compliance: Partners must maintain updated registration details with COCI; there is no statutory requirement to file audited financial statements, though bookkeeping obligations apply.

- Limited Partner Restrictions (CV): A limited partner who participates in management risks losing limited liability status and may be treated as a general partner under applicable law.

- Treaty Access: Because partnerships lack legal personality, access to Sint Maarten's tax treaty network (to the extent applicable) flows through the individual partners rather than the partnership itself.

Sub-Types

Vennootschap onder Firma (VOF)

The VOF is a general partnership where every partner actively manages the business and carries unlimited personal liability for partnership debts. It is commonly used for professional firms and small trading operations where all participants share both operational control and financial exposure.

Commanditaire Vennootschap (CV)

The CV distinguishes itself by permitting passive investors to participate without exposing personal assets beyond their capital contribution, provided they refrain from active management. This structure has historically been used for investment vehicles and family arrangements, though its utility depends on the tax residence of the partners involved.

Both structures suit small-scale commercial operations or investment arrangements where formal incorporation is not required. The absence of minimum capital and lighter compliance obligations offer operational simplicity, though unlimited liability for general partners represents a significant structural risk for higher-exposure activities.

VOF and CV structures are most appropriate for small professional practices, family businesses, or investment arrangements where two or more parties seek a low-cost, flexible operating structure without the formalities of incorporation.

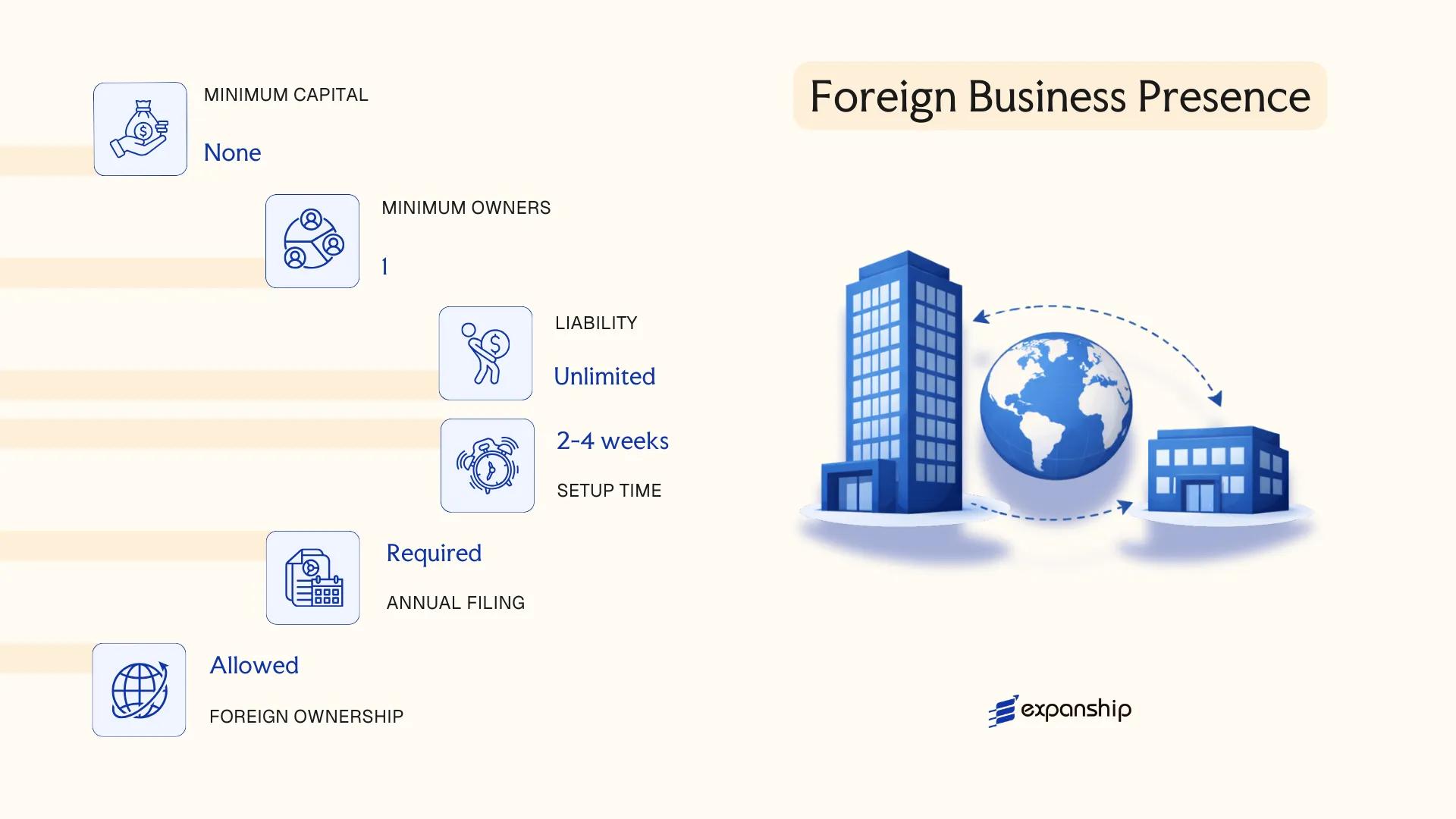

Foreign Business Presence in Sint Maarten [Branch Office, Representative Office]

A foreign company branch office Sint Maarten is not a separate legal entity — it is an extension of the parent company abroad, which retains full liability for the branch's obligations. Registration is governed by the National Ordinance on the Chamber of Commerce and Industry, and the branch must be enrolled with the Sint Maarten Chamber of Commerce before conducting any commercial activity.

Representative offices occupy a narrower position: they may carry out promotional or liaison functions but cannot generate local revenue or enter into contracts on the company's behalf. Both forms require a local point of contact and submission of the parent company's constitutional documents, translated into Dutch or English where applicable.

Key Characteristics

| Requirement | Branch Office | Representative Office |

|---|---|---|

| Legal Personality | None — extension of parent | None — extension of parent |

| Parent Liability | Unlimited | Unlimited |

| Commercial Activity | Permitted | Not permitted |

| Local Contact | Required | Required |

| Registration Body | Chamber of Commerce | Chamber of Commerce |

| Share Capital | None required locally | None required locally |

Focus Points

- Taxation: Branch profits are subject to Sint Maarten's corporate profit tax; no separate withholding tax applies at branch level, though profit remittances may be treated as deemed dividends depending on structuring.

- Economic Substance: Branches engaged in relevant activities must satisfy substance requirements under local economic substance legislation.

- Annual Compliance: Annual renewal of Chamber registration and filing of updated parent company documents is required.

- Treaty Access: Access to tax treaties depends on the parent company's jurisdiction; Sint Maarten's treaty network is limited.

- Restrictions: Representative offices cannot invoice locally or hold inventory for sale.

Closing

A branch suits foreign firms testing the local market or managing regional operations without incorporating a separate entity, though the absence of liability separation is a meaningful structural exposure.

Foreign companies seeking a temporary or exploratory commercial presence without the administrative burden of forming a locally incorporated entity.

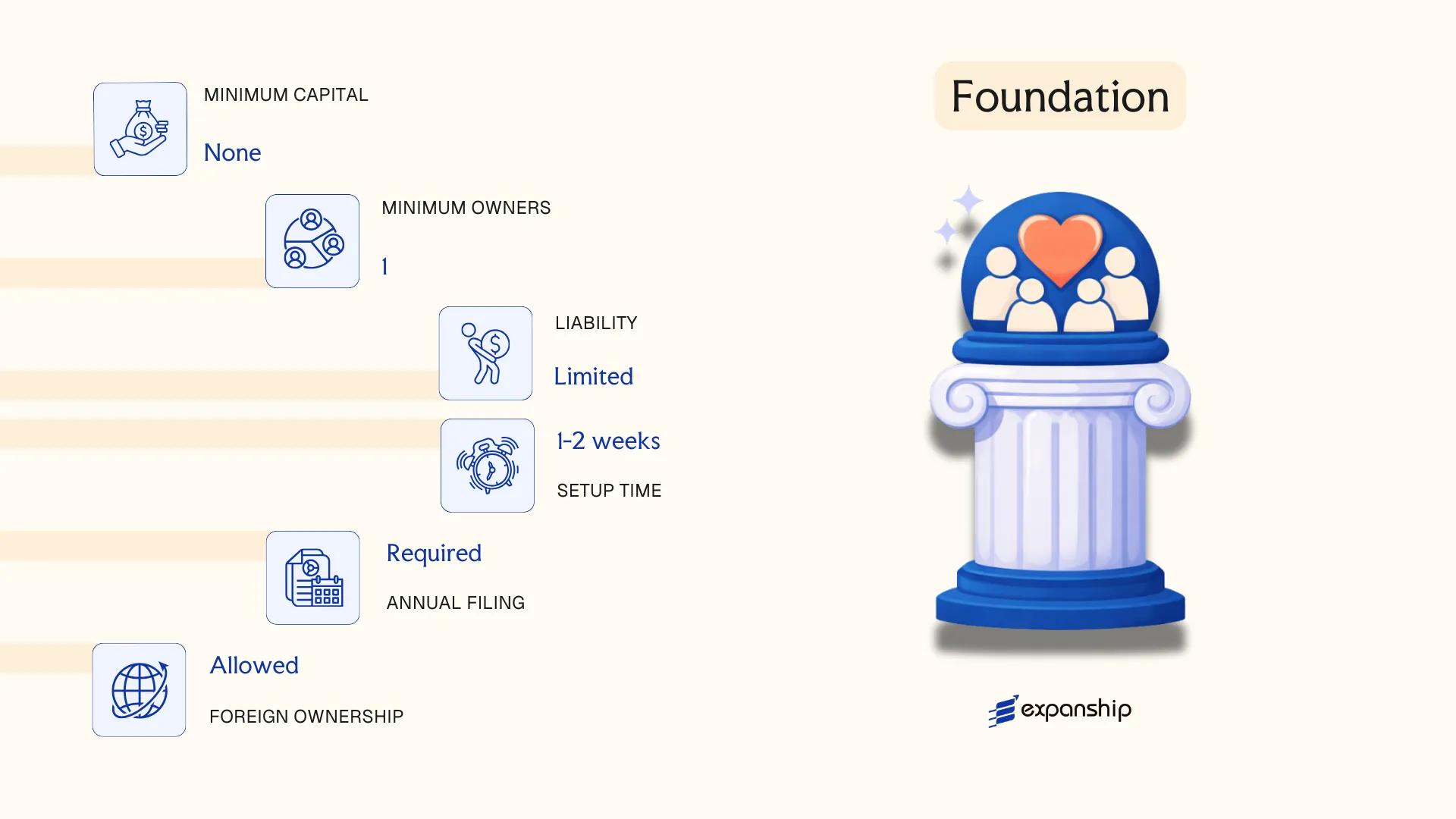

Foundation (Stichting)

A Stichting foundation Sint Maarten is governed by the Civil Code of Sint Maarten, which took effect when Sint Maarten became an autonomous country within the Kingdom of the Netherlands in 2010. The Stichting holds separate legal personality and, by definition, has no members or shareholders — its assets are dedicated to the stated purpose outlined in the notarial deed of incorporation.

Unlike commercial entities, the Stichting cannot distribute profits to founders or directors. It is used for charitable, social, religious, and increasingly, private wealth-structuring purposes under Sint Maarten foundation registration.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Foundation (Stichting) | Separate legal personality; no share capital |

| Governing Body | Board of Directors | Minimum 1 director; no maximum set by law |

| Members | No members or shareholders | Assets dedicated solely to the foundation's purpose |

| Local Presence | Registered office in Sint Maarten | Required; notarial deed must be executed locally |

| Capital | No minimum capital requirement | Contributions made by founders are not returnable |

| Privacy | Deed of incorporation filed with the Chamber of Commerce | Board details generally accessible; beneficial owner rules apply |

Focus Points

- Taxation: Stichtings pursuing genuine non-profit purposes may qualify for exemption from profit tax; commercial activities can attract the standard profit tax rate, currently set at 34.5%. No VAT regime currently applies in Sint Maarten, and withholding tax obligations depend on distributions made.

- Economic Substance: Non-commercial foundations are generally not subject to economic substance requirements, though foundations conducting business activities should seek local legal advice.

- Annual Compliance: Annual financial statements must be prepared; audit requirements depend on the scale of activities.

- Restrictions: The Stichting cannot distribute assets to founders, directors, or third parties except in furtherance of its stated purpose.

- Conversion: Conversion from a Stichting to a commercial entity type is not straightforward and typically requires dissolution and reincorporation.

Closing

Setting up a Stichting Sint Maarten suits non-profit activities, private family foundations, and asset-protection structures where profit distribution is not the objective. Its principal advantage is the clear separation of dedicated assets from personal estates; its primary limitation is the prohibition on profit distribution, which makes it unsuitable for operating businesses seeking returns for owners.

The Stichting is best suited for philanthropic organisations, ecclesiastical bodies, and private wealth-holding structures where asset segregation — rather than commercial return — is the primary objective.

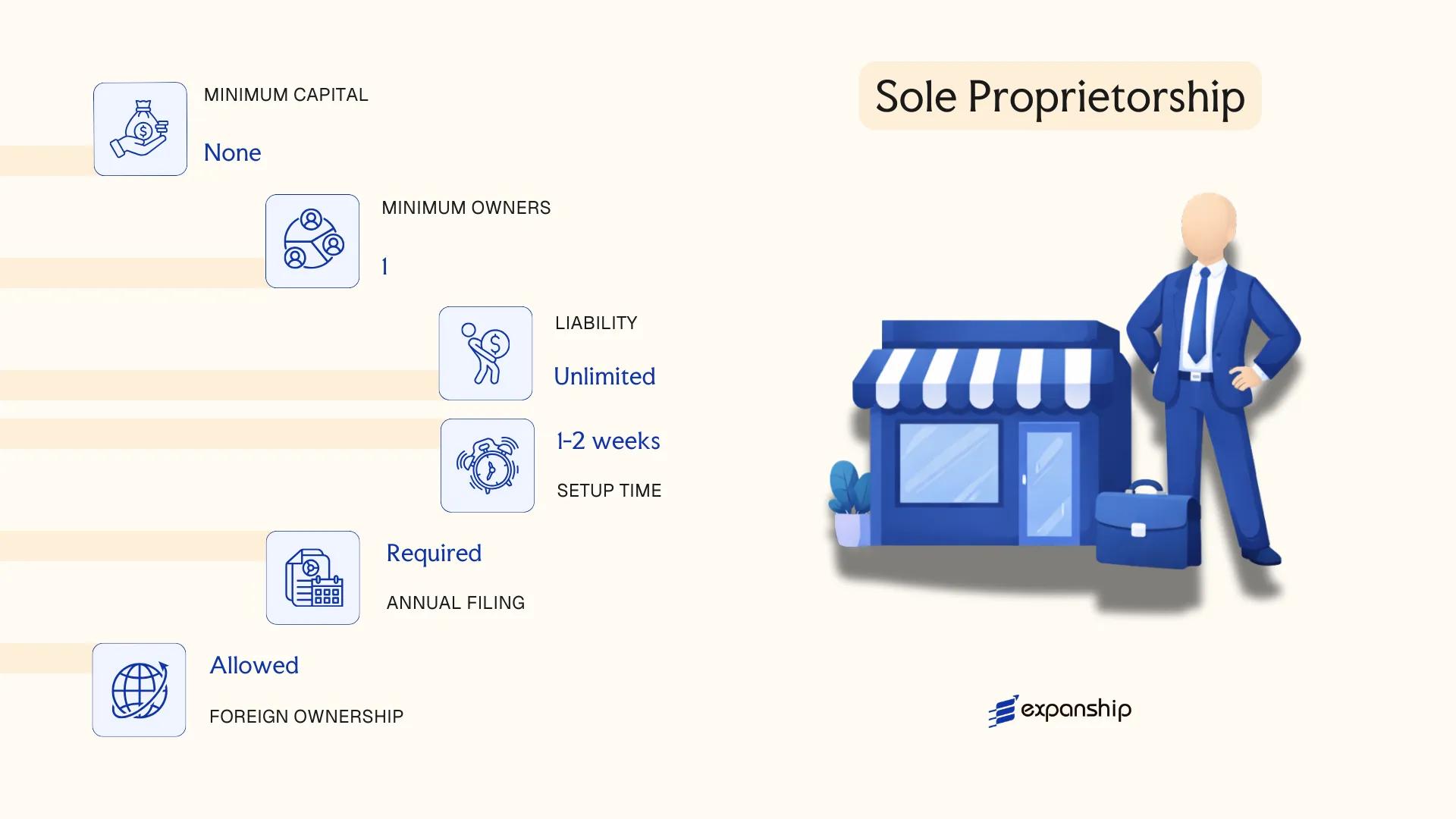

Sole Proprietorship (Eenmanszaak)

A sole proprietorship Sint Maarten Eenmanszaak is the simplest and most direct business form available under Sint Maarten's civil and commercial law framework, derived from the Netherlands Antilles legal tradition and adapted following the 2010 constitutional change. Registration is handled through the Chamber of Commerce of Sint Maarten (COCI), and the business has no legal personality separate from its owner.

Because the proprietor and the business are legally one and the same, personal assets are fully exposed to business liabilities. This structure suits individuals conducting small-scale or local commercial activity under their own name or a trade name.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated sole trader | No separate legal personality from the owner |

| Member Type | Sole Proprietor (1 natural person) | No minimum capital; one owner only — cannot be a legal entity |

| Local Presence | Registered business address in Sint Maarten required | Registration via COCI mandatory |

| Capital | No statutory minimum | Owner funds the business directly |

| Privacy | Proprietor's name on public COCI register | No meaningful privacy protection |

Focus Points

- Taxation: Subject to personal income tax on business profits; no separate corporate income tax applies; turnover tax (equivalent to a local sales levy) may apply depending on activity and thresholds.

- Annual Compliance: Annual renewal of COCI registration required; financial reporting obligations are minimal compared to incorporated entities.

- Economic Substance: No formal substance requirements apply, given the absence of corporate structure.

- Treaty Access: As an unincorporated entity, it does not benefit from tax treaty protections available to corporate entities.

- Conversion: Can be converted into a BV or NV, though this requires full incorporation procedures rather than a simple structural amendment.

Closing Paragraph

The Eenmanszaak suits freelancers, sole traders, and small local service providers seeking a low-cost, low-administration entry into Sint Maarten self-employed business registration. The primary advantage is minimal setup and compliance burden; the significant drawback is unlimited personal liability for all business obligations.

Local freelancers or individual traders operating in Sint Maarten who prioritise simplicity over liability protection.

How to Choose the Right Entity Type in Sint Maarten

Choosing the right company type in Sint Maarten is not a procedural formality — the structure you select has direct legal, tax, and operational consequences that are difficult and costly to reverse.

Why Your Entity Choice Matters

- Registering an offshore-oriented entity while conducting local trade puts your business in breach of the National Ordinance on the Formal Registration of Businesses, exposing it to administrative penalties or deregistration.

- Choosing a tax-exempt entity blocks access to withholding tax reductions under any applicable tax arrangements, since exemption status generally disqualifies a firm from treaty benefits.

- Forming a company when a Stichting would better serve asset protection or succession purposes locks you into annual general meeting obligations and shareholder maintenance requirements that foundations are not subject to.

- Selecting an entity with mandatory audit requirements for a single-person consultancy introduces annual compliance costs that an Eenmanszaak or simple BV structure would not generate.

Key Factors to Consider

- Business Activity: Active trading, passive asset holding, and regulated sectors such as banking or insurance each correspond to distinct permissible structures under Sint Maarten law.

- Local vs. Cross-Border Operations: Entities transacting with local residents face different registration thresholds and licensing requirements than those operating entirely outside the jurisdiction.

- Ownership and Management: A sole director-shareholder arrangement suits a BV, while multi-party ventures with shared liability may point toward a Vennootschap onder Firma.

- Tax Objectives: Your need for full exemption, a standard profit tax rate, or eligibility for a specific fiscal regime will narrow the viable entity options considerably.

- Substance Capacity: If you cannot realistically maintain staff, office space, and local decision-making, the chosen structure must align with applicable substance requirements to avoid reporting failures.

- Exit Strategy: Redomiciliation, conversion, and voluntary dissolution procedures vary by entity type under Sint Maarten's civil and corporate ordinances, so your anticipated exit path should inform your initial formation decision.

The National Ordinance on the Formal Registration of Businesses and the relevant civil code provisions govern these requirements directly.

Corporate Compliance Services in Sint Maarten

Maintain good standing with Sint Maarten's regulatory requirements — from annual filings to substance compliance and directorship obligations.

Conclusion

Sint Maarten company incorporation summary points to a jurisdiction with a well-defined set of legal forms, each serving a distinct purpose. The NV suits publicly oriented or larger commercial ventures, while the BV is the standard choice for closely held private companies and is the most commonly registered corporate entity on the island. Partnerships serve operators who prefer shared liability structures without full corporate formality. A Stichting fits non-profit or asset-holding purposes, and a sole proprietorship remains the entry point for individual traders. Branch offices and representative offices allow foreign firms to establish a local presence without incorporating a separate legal entity.

Regulated by the Kamer van Koophandel Sint Maarten under the civil law framework inherited from the Netherlands Antilles, the registry continues to modernize its procedures. Your choice of structure determines filing obligations, liability exposure, and how your business is treated under local commercial law.

How Expanship Can Assist You

Expanship company formation Sint Maarten services are built around the specific entity types available under the jurisdiction's civil law framework — from the Naamloze Vennootschap and Besloten Vennootschap to foundations and sole proprietorships. Every structure discussed in this blog carries distinct registration requirements with the Chamber of Commerce of Sint Maarten, and our work begins where those requirements do. Your business receives direct support at each stage, not generic advice adapted from another jurisdiction.

From document preparation through to post-incorporation obligations, our service scope covers the full process:

- Document preparation and notarial deed coordination

- Registered agent and registered office provision

- Filing and liaison with the Chamber of Commerce of Sint Maarten

- Post-incorporation compliance management

- Banking introduction assistance

Ready to move forward? Contact [Expanship Sint Maarten](sx/contact-us) to discuss your incorporation.

Frequently Asked Questions (FAQ)

The Naamloze Vennootschap (NV) remains the most frequently registered entity, particularly among international investors. Its ability to issue bearer or registered shares and operate across a broad range of commercial activities makes it the default choice for holding structures and trading companies alike.

The NV can offer shares to the public and has no restriction on share transferability, whereas the BV restricts share transfers and cannot make public share offerings. Both entities are subject to profit tax under the National Ordinance on Profit Tax, though the BV's closed structure generally suits closely held family or partner-owned businesses better than the NV.

The NV, particularly when structured with bearer shares prior to any applicable registration reforms, has historically offered the greatest degree of shareholder confidentiality. Director and shareholder details are not routinely published in a publicly searchable format through the Sint Maarten Chamber of Commerce registration. Nominee arrangements are available under local practice, subject to know-your-customer requirements.

A sole proprietorship (Eenmanszaak) and a foundation (Stichting) can each be established by one individual. Both the Vennootschap onder Firma and the Commanditaire Vennootschap require at least two parties, as their legal character is fundamentally based on a partnership agreement between distinct persons.

Foreign nationals may incorporate an NV or BV, establish a foundation, or register a branch without a requirement for local shareholder participation. Non-residents seeking frequently asked questions Sint Maarten incorporation answers should note that a licensed registered agent or local representative is generally required for the formal registration process at the Chamber of Commerce.

Conversion between entity types is recognized in principle under Sint Maarten corporate law, with the NV-to-BV conversion being the most straightforward given the structural similarities between the two. A formal notarial deed is required, and the entity must satisfy any outstanding compliance obligations before the change is registered.

The NV, BV, and Stichting each carry full separate legal personality, meaning liabilities rest with the entity rather than its founders or members. General partnerships (VOF) do not carry separate legal personality, leaving partners personally exposed to the firm's obligations.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.