Key Takeaways

- Sint Maarten's Civil Code framework, inherited through its constitutional position as a constituent country within the Kingdom of the Netherlands, creates regulatory overlap that can complicate compliance obligations for foreign-owned entities unfamiliar with Dutch Caribbean legal conventions.

- The absence of any double tax treaties means businesses incorporated in Sint Maarten cannot rely on treaty-based withholding tax reductions or dispute resolution mechanisms when dealing with counterparties in major trading jurisdictions.

- Operating costs are structurally elevated by the island's near-total dependence on imported goods and services, which increases input costs across logistics, construction, and professional services relative to larger, self-sufficient markets.

- With a resident population of roughly 40,000, the domestic consumer base is too small to support meaningful revenue scale for most locally focused business models, making market growth contingent on tourism cycles or cross-border trade rather than organic local demand.

Sint Maarten operates under an evolving regulatory framework shaped by its constitutional status as a constituent country within the Kingdom of the Netherlands, with company law governed primarily by the Civil Code. The disadvantages of incorporating in Sint Maarten span operational, financial, and structural categories that affect day-to-day business viability.

The extent to which these drawbacks affect your business depends significantly on your industry, the legal entity you form, and whether your operations are locally focused or internationally oriented.

This article is most relevant to foreign investors and small-to-medium enterprise owners considering Sint Maarten as a base for trading, services, or holding structures who may not yet have full visibility into the cons of registering a business there.

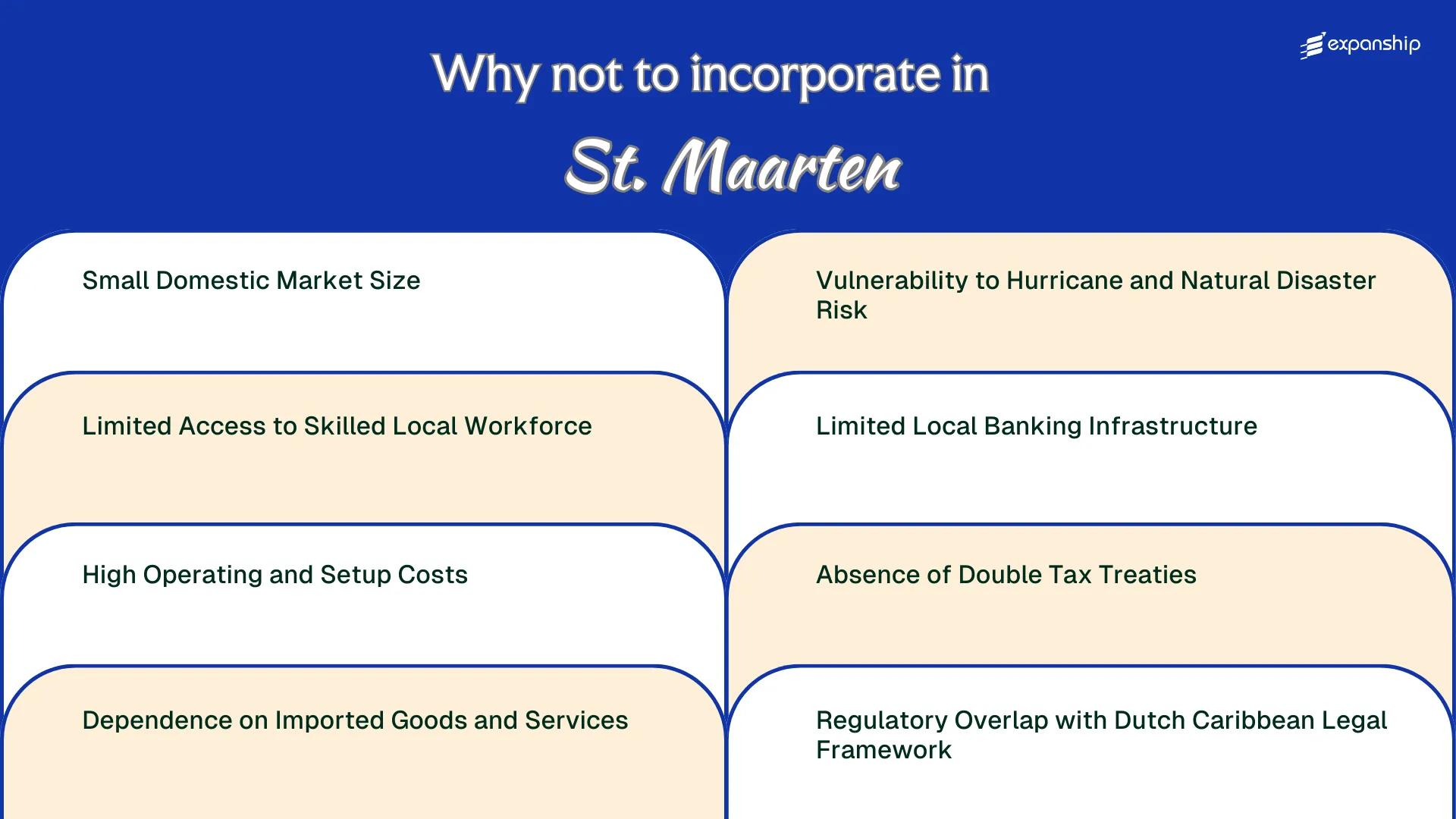

Small Domestic Market Size

Sint Maarten's small market limitations are rooted in a structural reality that cannot be offset by favorable tax conditions alone. With a resident population of approximately 40,000 to 45,000 people, the addressable consumer base is among the smallest of any incorporated jurisdiction in the Caribbean.

Revenue Ceiling for Locally-Focused Business Models

Businesses structured to serve the local market face a hard ceiling on organic revenue growth. Sectors such as retail, food and beverage, and professional services are particularly exposed, as saturation thresholds are reached at relatively modest scale.

Tourism partially supplements domestic demand, but seasonal fluctuations mean consumer spending is uneven across the year. A firm relying on year-round local consumption cannot compensate for this inconsistency through volume alone.

Structural Barriers to Market Expansion

Expanding beyond the island requires operating across separate jurisdictions, each with its own regulatory and compliance requirements. Your business absorbs those costs without the benefit of a regional trade bloc or shared regulatory framework that would otherwise reduce cross-border friction.

Foreign business owners who structure their company around local market revenue will find that Sint Maarten's limited consumer base makes sustainable profitability difficult without a clearly defined export or re-export strategy.

Limited Access to Skilled Local Workforce

Sint Maarten's skilled workforce shortage is a structural constraint that directly affects staffing costs, timelines, and operational continuity for foreign-owned businesses. The island's resident population sits below 45,000, which places a hard ceiling on the local talent pool across most technical and professional disciplines.

Sourcing qualified staff locally is consistently difficult in fields such as finance, IT, engineering, and legal services. When local candidates are unavailable, companies must recruit from abroad, which triggers Sint Maarten's work permit process under the national labor ordinance administered through the Department of Labor Affairs.

That process generates friction at multiple levels:

- Permit processing delays can stall operational launch by several months, creating overhead costs before revenue begins.

- Mandatory labor market tests require demonstrating that no qualified local candidate was available, adding administrative burden and legal fees.

- Foreign hires often demand relocation packages and housing allowances, significantly inflating total compensation costs compared to hiring domestically.

- High staff turnover among expatriate employees compounds recruitment costs over time, as replacement cycles repeat.

Seasonal tourism patterns also distort year-round workforce availability, making consistent staffing harder to maintain for businesses that operate outside the hospitality sector.

Company Incorporation in Sint Maarten

Set up your business in Sint Maarten with guidance on registration requirements, compliance obligations, and entity structuring.

High Operating and Setup Costs

Sint Maarten high business setup costs begin before your company trades a single dollar. Registering a Naamloze Vennootschap (NV) or a Besloten Vennootschap (BV) with the Chamber of Commerce of Sint Maarten requires notarial deed preparation, which carries fees that can exceed USD 1,500 for drafting alone, before registration charges are added.

| Cost Category | Estimated Burden | Why It Restricts |

|---|---|---|

| Notarial deed (NV/BV formation) | USD 1,500+ | Mandatory for incorporation; cannot be bypassed |

| Chamber of Commerce registration | USD 300–600 | Payable upfront before any trading begins |

| Annual audit requirement (NV) | USD 3,000–8,000+ | Statutory obligation regardless of revenue size |

| Office space (commercial, Philipsburg) | USD 30–60 per sq ft/year | Small supply pool drives prices disproportionately high |

Because Sint Maarten operates a consumption-based economy with limited local production, nearly all office supplies, equipment, and professional services carry import premiums on top of already high local rates. A statutory audit obligation imposed on NV structures applies regardless of turnover, meaning early-stage or low-revenue entities absorb the same compliance cost as established businesses.

Professional service fees from local accountants and legal advisors are priced to reflect a limited supply of qualified practitioners on the island. Your operating cost drawbacks compound annually through mandatory renewals, licensing fees, and turnover tax filings under the Landsverordening Omzetbelasting.

Dependence on Imported Goods and Services

Sint Maarten import dependency risks affect virtually every operational cost a foreign business will encounter. The island produces almost no goods domestically, meaning food, construction materials, office equipment, fuel, and consumer products all arrive by sea or air, primarily through Princess Juliana International Airport and the Port of Philipsburg.

Freight consolidation fees, customs duties, and port handling charges accumulate on each shipment. Under the General Customs and Excise Ordinance (Landsverordening in-, uit- en doorvoer), imported goods are subject to turnover tax and applicable import duties, adding a recurring cost layer that businesses in manufacturing-based or continental economies rarely face at this scale.

Supply chains are also thin. A single disruption at the port or airport can delay critical inputs for days, and there are no local alternatives to fall back on.

- Import duties and turnover tax apply to most goods entering under the customs ordinance, affecting your landed cost calculations.

- Your business will depend on international freight schedules outside your control, with no local production fallback.

- Customs procedures and documentation requirements apply to each shipment, creating administrative obligations.

- Price fluctuations in global shipping markets pass directly to your operating costs with no local buffer.

Sint Maarten's import dependency means that even basic office supplies can carry an effective landed cost 30-50% above the supplier's invoice price once duties, freight, and port fees are factored in.

Vulnerability to Hurricane and Natural Disaster Risk

Sint Maarten hurricane risk for businesses is not a peripheral concern — it is a structural exposure that shapes insurance costs, lease terms, and operational continuity planning from the moment you incorporate.

Geographic Exposure and Storm Frequency

Located in the northeastern Caribbean at roughly 18°N latitude, Sint Maarten sits within the Atlantic hurricane belt, where storm activity peaks between June and November each year. Hurricane Irma in 2017 caused catastrophic damage across the island, destroying infrastructure, displacing residents, and suspending commercial activity for an extended period, demonstrating how a single event can eliminate years of business investment.

Operational and Financial Consequences for Foreign-Owned Entities

Your entity faces compounding costs: commercial property insurance premiums in storm-prone Caribbean territories are significantly higher than in continental markets, and coverage gaps for wind and flood damage are common. Business continuity risks in Sint Maarten are further amplified because the island's port, airport, and utility networks are concentrated in a small geographic area, meaning a single storm can simultaneously disrupt supply chains, communications, and power for weeks.

Managing Business Risk When Incorporating in Sint Maarten

Understand the structural and operational challenges of establishing a company in Sint Maarten before committing to incorporation.

Limited Local Banking Infrastructure

Sint Maarten banking infrastructure limitations create tangible friction for foreign-owned entities that require reliable, full-service corporate banking from day one. Only a small number of commercial banks operate on the island, with Windward Islands Bank (WIB) and RBC Royal Bank among the primary institutions serving business clients.

- Opening a corporate account often requires extensive in-person due diligence under the National Ordinance on the Identification of Clients and the Reporting of Unusual Transactions, which adds weeks to your setup timeline.

- Limited banking access in Sint Maarten means correspondent banking relationships with major international financial networks are restricted, complicating cross-border transactions.

- Trade finance products, multi-currency accounts, and sophisticated treasury services that larger financial centres offer are largely unavailable through local institutions.

- Your firm may be required to maintain banking relationships offshore to meet operational needs, creating additional compliance obligations in a second jurisdiction.

- Non-resident directors face heightened scrutiny during account onboarding, which can result in outright refusal from local banks.

Absence of Double Tax Treaties

Sint Maarten has no double tax treaties with any foreign jurisdiction. For businesses with cross-border operations, this means income can be taxed in full by both Sint Maarten and the country where clients, investors, or parent entities are located, with no treaty mechanism to eliminate or reduce that overlap.

Dividend payments, royalties, and service fees remitted abroad are subject to withholding tax under Sint Maarten's domestic rules, without the reduced rates that treaty networks typically provide. A foreign parent company receiving profits from a Sint Maarten subsidiary may face full withholding at source, then taxation again under its home country's rules.

The practical exposure depends on whether your home jurisdiction offers unilateral relief, such as a foreign tax credit or exemption. Where no such relief exists domestically, the total effective tax burden on cross-border income can exceed the combined statutory rates of both countries involved.

A business owner resident in a country with a 25% corporate tax rate and no unilateral foreign tax credit mechanism receives a dividend from their Sint Maarten entity, which has already applied a domestic withholding tax. With no treaty to cap or eliminate that withholding, the same income is taxed twice in full, potentially resulting in an effective combined rate above 40% on distributed profits.

Regulatory Overlap with Dutch Caribbean Legal Framework

Sint Maarten's Sint Maarten Dutch Caribbean regulatory overlap stems from its constitutional position as a constituent country within the Kingdom of the Netherlands. While the island holds autonomous status under the 2010 Charter for the Kingdom of the Netherlands, Kingdom-level legislation still takes precedence in areas including defense, nationality, and certain financial oversight functions. Your business cannot simply treat this as a local compliance environment.

The Financial Intelligence Unit Netherlands Antilles (FIU) and the Central Bank of Curaçao and Sint Maarten (CBCS) both carry supervisory authority over financial institutions operating in the jurisdiction. Reporting to multiple bodies across different levels of governance creates layered compliance obligations that require separate legal counsel familiar with both local ordinances and Kingdom-level statutes.

Dutch Caribbean legal framework challenges also arise because local civil and commercial law descends from the Dutch Antillean Civil Code, which differs from the Netherlands' own civil code. Foreign investors accustomed to EU frameworks may assume harmonization exists where it does not, leading to misapplied contract structures or incorrect assumptions about liability regimes.

Any regulated financial activity, including banking, insurance, or investment services, falls under CBCS supervision, and Kingdom-level intervention powers apply regardless of local incorporation status.

Overcoming Incorporation Challenges in Sint Maarten

Overcoming Sint Maarten incorporation challenges requires a structural approach rather than reactive fixes. The disadvantages covered in this blog stem from identifiable regulatory, geographic, and infrastructural conditions that can be partially addressed through deliberate entity setup and compliance planning.

- Register your entity under the correct legal form via the Centraal Stembureau and confirm ongoing filing obligations with the Tax Administration of Sint Maarten.

- Establish banking relationships with internationally affiliated institutions operating in the jurisdiction to reduce exposure to limited local banking infrastructure.

- Structure contracts and supplier arrangements in advance to account for import dependency and the absence of local procurement alternatives.

- Obtain dedicated hurricane and natural disaster insurance coverage suited to Caribbean operational risk before commencing business activities.

- Consult the Kingdom of the Netherlands tax framework to understand withholding obligations in the absence of bilateral double tax treaties.

- Engage qualified foreign professionals under Sint Maarten's work permit process administered by the Department of Labor to address local workforce gaps.

These steps operate within the jurisdiction's civil law framework, which derives from the Dutch Caribbean legal tradition under the Staatsregeling van Sint Maarten. Addressing each challenge at the formation stage reduces compounding compliance exposure over the operational life of the business.

Sint Maarten's Overall Business Viability

Sint Maarten business viability risks are real and well-documented, but they do not uniformly disqualify the jurisdiction as an incorporation destination. For businesses oriented toward Caribbean trade, tourism-linked services, or regional holding structures, the Dutch Caribbean legal framework and the island's dual-island geographic position still present a credible base of operations.

| Pros | Cons |

|---|---|

| Dutch Caribbean legal framework provides a structured, civil-law foundation for corporate governance | No double tax treaties in force, exposing foreign income to potential dual taxation |

| Geographic position supports access to both Dutch and French Caribbean commercial activity | Small domestic market limits organic revenue growth from local consumer demand |

| Tourism-driven economy creates consistent demand in hospitality and service-adjacent sectors | High import dependence raises operating costs across most business categories |

| Civil law corporate structures are familiar to European and Latin American counterparts | Local banking infrastructure is limited, complicating account opening and financial operations |

| Hurricane exposure creates recurring risk to physical assets and business continuity |

Weighing these factors against your firm's operational model is a practical starting point. A business that relies on physical infrastructure, local staffing, or domestic sales volume will encounter friction that a leaner, regionally focused entity may not.

Corporate Compliance Services in Sint Maarten

Maintain your company's good standing under Sint Maarten's National Ordinance on Corporations and meet all ongoing filing and regulatory obligations.

Conclusion

The Sint Maarten company formation cons summary reflects a jurisdiction with genuine structural constraints rather than isolated regulatory friction. The absence of double tax treaties limits your firm's ability to manage cross-border withholding obligations efficiently. Banking access remains a persistent operational difficulty, with correspondent relationships affecting transaction reliability. Disaster exposure tied to Atlantic hurricane cycles introduces a risk variable that standard business continuity planning must account for. Structural support from professional advisors familiar with the Civil Code of Sint Maarten and the local regulatory environment becomes a practical necessity for most foreign-incorporated entities.

Expanship's Sint Maarten Business Support

Expanship Sint Maarten business support is structured around the specific compliance obligations and structural friction that this blog has outlined — from the absence of double tax treaties and the oversight of the Chamber of Commerce of Sint Maarten to the banking access constraints that affect newly formed entities. Expanship's role is to reduce the operational burden of managing these requirements, not to change the conditions themselves.

Beyond incorporation, the scope of support covers the full formation and maintenance cycle:

- Your company registration and document preparation are handled in accordance with local statutory requirements.

- A registered agent and local office address are provided to satisfy Sint Maarten's physical presence obligations.

- Government filings are submitted on your behalf, including direct liaison with the relevant regulatory authorities.

- Post-incorporation compliance is monitored to keep your entity in good standing with local obligations.

- Banking introductions are facilitated to support your account opening process.

- Tax registration and coordination with local authorities are managed as part of the onboarding process.

Reach out through Expanship Sint Maarten to discuss your incorporation requirements.

Frequently Asked Questions (FAQ)

Yes, Sint Maarten has no double tax treaty network, so all entities incorporated there, regardless of legal form, are exposed to potential double taxation on cross-border income flows. If your business receives dividends, royalties, or service income from a treaty-reliant jurisdiction, those payments may be subject to full withholding tax in the source country with no offsetting relief available in Sint Maarten.

The overlap between Sint Maarten's own national ordinances and the inherited Dutch Caribbean Civil Code adds legal complexity that typically requires dual-qualified legal counsel, which increases advisory fees beyond what you would pay in a single-framework jurisdiction. There is no fixed cost, but businesses frequently report higher-than-expected legal expenses when structuring transactions that touch both layers of the regulatory framework.

Not realistically, given the island's limited local professional services market and the scale of goods that must be imported. Sint Maarten produces very little domestically, so operational inputs ranging from IT infrastructure to specialized business services generally come from outside the island, introducing supply chain exposure and higher per-unit costs compared to larger jurisdictions with developed local markets.

For international business purposes, yes. Sint Maarten has a small number of licensed commercial banks, and correspondent banking relationships have contracted across the Caribbean due to de-risking by major international banks. Opening a corporate account as a foreign-owned entity can involve extended due diligence timelines and, in some cases, outright rejection, which is a more acute problem in Sint Maarten than in jurisdictions like the Cayman Islands or BVI that have larger, more internationally connected banking sectors.

If your business operates in a licensed or regulated sector, relying on expatriate staff requires work permit applications processed through the Sint Maarten Department of Labour, and approvals are not guaranteed. Failure to staff regulated roles with appropriately authorized personnel can result in licensing non-compliance, which may trigger suspension or revocation of the relevant operating permit under Sint Maarten's national ordinances governing business licensing.

Yes, businesses that depend on local consumer demand will find the market too small to sustain operations independently. Sint Maarten's population is approximately 40,000 people, which means any entity requiring meaningful domestic revenue must orient almost entirely toward tourism, regional trade, or international clients, and even those segments are vulnerable to the same natural disaster and infrastructure disruptions that affect the broader economy.

Sint Maarten does offer a relatively low corporate income tax environment, but the setup and operating costs, including import duties on equipment, elevated professional service fees, insurance premiums that reflect hurricane exposure, and the absence of treaty relief on outbound income, can erode the tax advantage quickly. For businesses with significant cross-border income or physical infrastructure requirements, the net financial position may not be favorable compared to jurisdictions that combine competitive tax rates with treaty networks and lower operational overhead.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.