Key Takeaways

- Sint Maarten's territorial tax system, governed by the National Ordinance on Profit Tax, exempts foreign-sourced profits from corporate income tax, allowing internationally structured entities to retain earnings that would be taxed in most onshore jurisdictions.

- Companies incorporated as an NV or BV benefit from a legal framework derived from Dutch civil law, giving foreign investors a degree of structural predictability uncommon among Caribbean jurisdictions of comparable size.

- Operating in a USD-pegged economy removes the exchange rate exposure that frequently complicates financial planning for businesses routing cross-border revenue through Caribbean holding structures.

- Registration is administered through the Chamber of Commerce of Sint Maarten under a relatively defined process, which reduces the procedural uncertainty that can delay market entry in jurisdictions with less standardized formation procedures.

Sint Maarten is a constituent country of the Kingdom of the Netherlands, occupying the southern portion of the island of Saint Martin in the northeastern Caribbean. It operates as a self-governing territory with its own legal and fiscal framework, separate from the Netherlands and from the French collectivity of Saint-Martin to the north. The Chamber of Commerce oversees company registration on the island.

Foreign businesses most commonly establish a Naamloze Vennootschap when structuring operations here. The jurisdiction operates a territorial tax system, meaning income sourced outside its borders is generally not subject to local corporate tax. Foreign ownership is broadly permitted, and the regulatory environment places no significant restrictions on foreign direct investment across most sectors.

Exploring the benefits of incorporating in Sint Maarten requires an understanding of where the jurisdiction sits legally, geographically, and commercially. This article covers the principal advantages your business may encounter when forming a company under Sint Maarten's regulatory framework.

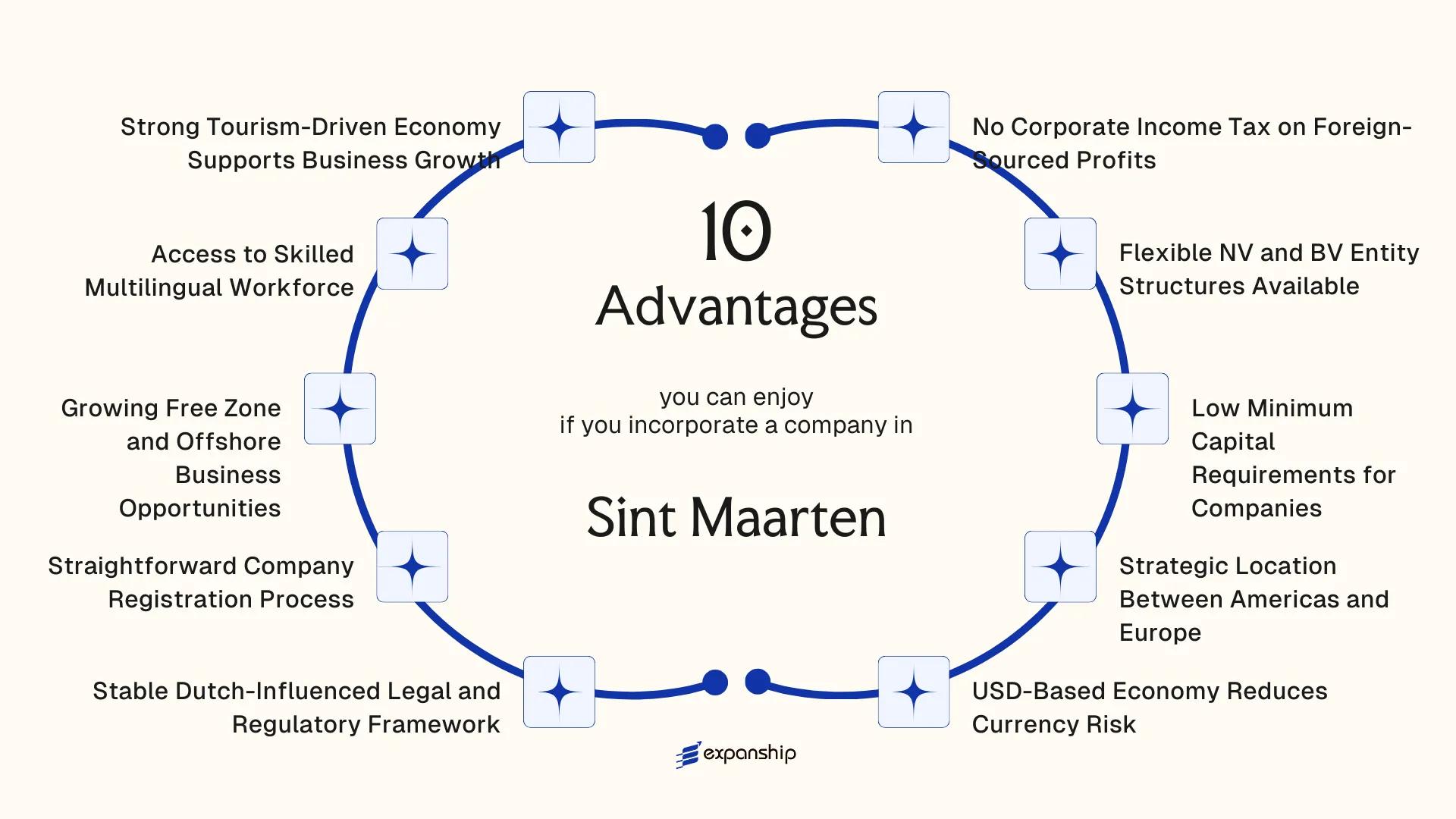

No Corporate Income Tax on Foreign-Sourced Profits

Sint Maarten operates a territorial tax system, meaning profits generated outside the jurisdiction are not subject to local corporate income tax. For businesses structured to earn revenue internationally, this creates a direct and quantifiable cost advantage.

How the Territorial Principle Applies to Corporate Structures

Under Sint Maarten's tax framework, corporate income tax applies only to profits sourced within the territory. A company incorporated here that derives its income from foreign clients, overseas contracts, or cross-border transactions falls outside the scope of local profit taxation on those earnings. This distinction matters because it allows your business to retain a significantly larger share of international revenue than it would in a residence-based tax jurisdiction.

Eligibility and Practical Conditions

The exemption applies to income that is genuinely foreign-sourced, not to profits artificially rerouted through the entity. Your corporate structure must reflect actual economic activity and proper income characterization to support the foreign-source classification under local tax rules.

Foreign-sourced profits earned through your Sint Maarten entity are not subject to local corporate income tax, reducing your effective tax burden on international operations.

Flexible NV and BV Entity Structures Available

Sint Maarten's corporate law recognizes two principal entity forms that are directly relevant to foreign investors: the Naamloze Vennootschap (NV) and the Besloten Vennootschap (BV). Both structures are governed under Sint Maarten's civil code, which draws from the Dutch legal tradition, giving them a well-defined statutory basis rather than a patchwork of case law.

The NV functions as a public limited company, meaning its shares can be freely transferred without restriction. This makes it the preferred structure for businesses that anticipate bringing in multiple shareholders or that require capital mobility. The BV, by contrast, is a private limited company with share transfer restrictions built into its articles of incorporation, which gives founders tighter control over who can hold an equity interest.

For a foreign investor, the practical value of having both options available is significant:

- Share transfer in the NV requires no shareholder approval, reducing friction in future restructurings

- The BV's restricted share transfer rules can be tailored in the articles of incorporation to meet specific ownership governance needs

- Both structures carry limited liability, meaning personal assets remain separate from corporate obligations

- Either entity can be structured to hold assets, operate trading activities, or function as a holding company

This structural flexibility allows your business to match the entity type to its actual ownership and operational model, rather than adapting operations to fit a single rigid corporate form.

Company Incorporation in Sint Maarten

Set up an NV or BV entity in Sint Maarten with full compliance support from registration through to post-incorporation requirements.

Low Minimum Capital Requirements for Companies

Sint Maarten low minimum capital requirements give new businesses a meaningful cost advantage from the moment of formation. Under the civil law framework governing corporate entities on the island, a Besloten Vennootschap (BV) can be incorporated with a nominal share capital requirement that does not demand significant upfront financial commitment. This means capital that would otherwise be tied up in statutory reserves can be deployed directly into operations, staffing, or market entry costs.

The distinction between share capital and paid-up capital also works in your favor. You are not required to fully pay up the subscribed capital at the time of incorporation, which reduces the immediate cash outlay for a foreign founder establishing a new entity.

| Feature | Detail |

|---|---|

| Entity Type | Besloten Vennootschap (BV) |

| Governing Legislation | Civil Code of Sint Maarten |

| Minimum Share Capital | Low nominal threshold |

| Paid-Up Requirement at Formation | Partial payment permitted |

| Currency | US Dollar (USD) |

For early-stage ventures or holding structures where the primary assets are intellectual property or offshore contracts, the low capital threshold for companies means your legal setup cost reflects the actual scale of the business rather than an arbitrary statutory figure. A foreign investor is not required to demonstrate substantial financial reserves simply to establish a corporate presence, making the jurisdiction accessible to a wider range of business structures and sizes.

Strategic Location Between Americas and Europe

Sint Maarten's geographic position is one of the more functionally significant Sint Maarten strategic location advantages for business operating across Atlantic trade corridors. Situated at the northeastern edge of the Caribbean, the island sits roughly equidistant between North America and Western Europe, with direct flight connections to Miami, New York, Amsterdam, and Paris. For a business managing clients or operations across multiple continents, that physical proximity translates into overlapping business hours with both American and European markets within a single working day.

Atlantic Standard Time (UTC-4), observed year-round without daylight saving adjustments, means your firm maintains a predictable schedule relative to New York (one hour ahead) and London (four to five hours behind). Operational consistency across time zones reduces scheduling friction for international teams.

The island's Princess Juliana International Airport serves as a regional transit hub, supporting cargo and passenger traffic that facilitates movement of personnel and goods across the Caribbean basin.

Keep these location-related factors in mind:

- UTC-4 is fixed year-round, eliminating seasonal scheduling adjustments

- Direct routes connect to major financial centers in the US and Netherlands

- Regional proximity supports access to Latin American markets

Sint Maarten shares a land border with the French collectivity of Saint-Martin, meaning your business operates on an island governed by two separate legal systems, which can create structuring options not available on single-jurisdiction Caribbean islands.

USD-Based Economy Reduces Currency Risk

Sint Maarten's official currency is the Netherlands Antillean guilder (ANG), but the U.S. dollar functions as the dominant transactional currency across the island. Most contracts, invoices, and commercial dealings are conducted in USD, which means your business can price services, hold accounts, and settle obligations without converting through a local currency that carries independent exchange risk against the dollar.

Reduced Conversion Costs on Cross-Border Transactions

For companies with revenue streams tied to U.S. markets, North American clients, or dollar-denominated commodities, operating from a USD-functional environment eliminates a layer of forex exposure that companies face in euro- or pound-denominated jurisdictions. The ANG itself is pegged at a fixed rate of 1.79 ANG to 1 USD, a peg maintained by the Centrale Bank van Curaçao en Sint Maarten. That fixed rate means the conversion between ANG obligations and USD holdings remains predictable over time, which simplifies treasury management for entities with mixed-currency reporting requirements.

Practical Advantage for Invoicing and Financial Planning

Tourism operators, professional service firms, and trading companies incorporated as an NV or BV can invoice clients directly in USD without triggering the currency mismatch that complicates financial statements in other Caribbean jurisdictions. Annual forecasting and cost modeling become more straightforward when your functional currency aligns with the currency in which the majority of regional trade and international contracts are denominated. Sint Maarten's USD-centric economy benefits for businesses are particularly relevant for companies sourcing goods, paying suppliers, or distributing profits across the Americas.

Maximize Your Sint Maarten Incorporation Benefits

Speak with an Expanship specialist about structuring your Sint Maarten company to take full advantage of its USD-aligned operating environment and fixed-rate currency framework.

Stable Dutch-Influenced Legal and Regulatory Framework

Sint Maarten's legal system is rooted in Dutch civil law, a foundation that carries meaningful implications for the Sint Maarten Dutch legal framework business advantages available to foreign incorporators. The jurisdiction operates under the legal order established following the 2010 constitutional reform, which gave Sint Maarten autonomous country status within the Kingdom of the Netherlands. That connection to Dutch legal heritage is not nominal — it shapes how courts interpret contracts, how corporate governance is structured, and how disputes are resolved.

- Civil law foundations mean corporate obligations, shareholder rights, and contractual arrangements follow codified statutes rather than case-by-case precedent. For a foreign business owner, this predictability reduces legal uncertainty when structuring agreements.

- The Civil Code of Sint Maarten, derived from the Dutch Civil Code, governs company formation, liability, and commercial transactions. Familiarity with Dutch or continental European legal norms transfers directly to operations here.

- Financial supervision falls under the Central Bank of Curaçao and Sint Maarten (CBCS), a shared institution that applies regulatory standards consistent across both jurisdictions. This institutional oversight provides a level of regulatory credibility that purely offshore, lightly supervised jurisdictions cannot offer.

- Contract enforcement through local courts follows established civil procedure, giving foreign creditors and investors a defined legal pathway that aligns with frameworks familiar across the Kingdom of the Netherlands.

Straightforward Company Registration Process

Sint Maarten's straightforward company registration benefits foreign owners primarily through speed and administrative accessibility. Registration is handled through the Chamber of Commerce of Sint Maarten (COCI), which processes new filings and issues the required commercial registration certificate. The absence of drawn-out pre-approval procedures means a new entity can typically become operational within days of submitting the required documentation.

For a foreign business owner, this matters because time between incorporation and trading is a direct cost. Delays in formation postpone revenue, complicate banking timelines, and extend the period during which your capital is committed without return.

The Sint Maarten business registration advantages also extend to document requirements. Incorporation of a Besloten Vennootschap (BV) or Naamloze Vennootschap (NV) requires submission of a notarially executed deed of incorporation, articles of association, and proof of director identity. No separate foreign investment approval from a government ministry is required at the point of formation.

A foreign-owned BV incorporating with ANG 1 share capital, submitting notarized formation documents to COCI, can receive commercial registration confirmation within approximately 3 to 5 business days, allowing the firm to open a corporate bank account and begin contracting before the end of the same week.

Growing Free Zone and Offshore Business Opportunities

Sint Maarten free zone business opportunities have expanded notably since the establishment of the Princess Juliana International Airport Free Zone and related economic development frameworks. Goods and services processed within designated free zone areas can move with reduced customs friction, which matters directly to trading companies and logistics operators seeking efficient regional distribution.

Offshore entities incorporated under the National Ordinance on Profit Tax are not subject to local profit tax on income generated entirely outside the jurisdiction. For a holding company or international trading firm, this creates a clear fiscal separation between local and foreign-sourced activities.

Free zone operators also benefit from:

- Exemptions from import duties on goods destined for re-export

- Reduced administrative requirements for inventory in transit

- Access to the island's port and air cargo infrastructure without full customs clearance obligations

The combination of Caribbean geographic positioning and Dutch Kingdom affiliation means your business can operate within a legally recognized framework while accessing markets across North America, South America, and Western Europe from a single registered address.

Free zone tax and duty benefits apply specifically to qualifying activities and designated zones; entities conducting business domestically in Sint Maarten do not automatically qualify for these exemptions.

Access to Skilled Multilingual Workforce

Sint Maarten multilingual workforce advantages for business extend well beyond basic communication. The island's population reflects a mix of Dutch, French, English, Spanish, and Papiamentu speakers, a direct product of its geographic position and colonial history. For a foreign-owned firm conducting international operations, this linguistic range reduces reliance on translation services and supports direct client engagement across multiple markets.

English as the Primary Business Language

English functions as the dominant language of commerce and government administration on the Dutch side of the island. Contracts, regulatory filings, and correspondence with bodies such as the Sint Maarten Chamber of Commerce and Industry are conducted in English. This removes a significant operational friction point that companies face when setting up in jurisdictions where Dutch, French, or Spanish is the sole official language of business.

Workforce Profile and Sectoral Depth

The labor pool has been shaped by decades of tourism, hospitality, financial services, and trade activity. As a result, workers with backgrounds in customer service, logistics, and commercial operations are available locally. This sectoral depth means your business is not starting from zero when building an operational team.

- Familiarity with international clients across North America, Europe, and Latin America

- Practical experience in service-oriented industries with cross-cultural customer interaction

- General proficiency across multiple languages in frontline and administrative roles

Implications for Foreign Employers

Hiring locally reduces the cost and administrative burden of relocating staff from abroad. Under Sint Maarten's labor framework, employers engage local talent through contracts governed by the National Ordinance on Labor Contracts, which provides a defined legal structure for employment relationships.

Strong Tourism-Driven Economy Supports Business Growth

Tourism is Sint Maarten's primary economic engine, and for foreign business owners, that concentration creates measurable commercial advantages. The island receives over two million cruise passengers and several hundred thousand stay-over visitors annually, generating consistent demand for retail, hospitality, food and beverage, financial services, and logistics. Sint Maarten tourism economy business growth advantages are most visible in this sustained consumer base, which operates largely independently of the business cycles that affect manufacturing or export-dependent economies.

Visitor spending flows directly into the private sector rather than through state intermediaries. This structure means businesses serving the tourism supply chain, from wholesale distribution to professional services, benefit from predictable seasonal revenue cycles that are easier to plan around than demand-driven markets in other jurisdictions.

The economic activity generated by tourism also supports ancillary sectors that foreign-incorporated firms can position within:

- Marine and yacht services, driven by Sint Maarten's status as a regional sailing and charter hub

- Duty-free retail, which draws high-volume purchasing from cruise visitors

- Short-term property management and hospitality management services

- Event logistics and destination services tied to the conference and wedding tourism segments

Because the economy is oriented toward international visitors, commercial infrastructure, including payment processing, foreign currency handling, and multilingual client services, is already calibrated for cross-border transactions. A firm incorporated here and operating in the tourism supply chain does not need to build that capacity from scratch. The market conditions have shaped it by default.

Why Sint Maarten Stands Out Against Rival Jurisdictions

Positioned in the northeastern Caribbean, Sint Maarten draws comparisons with Curaçao, the British Virgin Islands, and the Cayman Islands — jurisdictions that share a similar investor profile and target broadly the same category of internationally oriented businesses. What the comparison reveals is not simply a difference in tax rates, but a structural divergence in how each territory balances regulatory accessibility with legal credibility. Sint Maarten's Dutch constitutional status, its Civil Code-based legal system, and the absence of corporate tax on foreign-sourced income together create a profile that is difficult to replicate precisely elsewhere in the region.

Curaçao operates under a comparable Dutch legal tradition but carries a more complex offshore licensing regime. The BVI and Cayman Islands offer strong confidentiality frameworks, yet both have faced sustained international pressure on transparency and are subject to UK Overseas Territory oversight. Where Sint Maarten's Sint Maarten advantages over rival jurisdictions become most apparent is in the combination of legal familiarity for European-origin businesses, dollar-denominated operations, and a relatively accessible incorporation process under the same NV and BV structures governed by the Civil Code of Sint Maarten.

| Parameter | Sint Maarten | Curaçao | British Virgin Islands |

|---|---|---|---|

| Legal System | Dutch Civil Code | Dutch Civil Code | English Common Law |

| Corporate Tax on Foreign Income | Not levied | Partial exemptions available | Not levied |

| Primary Entity Types | NV, BV | NV, BV | BC (Business Company) |

| Constitutional Status | Dutch constituent country | Dutch constituent country | UK Overseas Territory |

| Operating Currency | USD | ANG / USD | USD |

| Offshore Licensing Complexity | Moderate | Higher | Low to moderate |

Compliance Services for Companies in Sint Maarten

Sint Maarten-registered entities are subject to ongoing filing, reporting, and regulatory obligations under local law. This service covers the requirements your business needs to remain in good standing.

Conclusion

Sint Maarten's position as a Dutch Caribbean autonomous country gives it a distinct combination of structural and fiscal features that few jurisdictions in the region can replicate at the same scale. The benefits of incorporating in Sint Maarten rest not on any single advantage but on how several elements work together: the exemption of foreign-sourced profits from corporate income tax, the currency peg to the US dollar that eliminates exchange rate exposure, and a legal framework derived from Dutch civil law that gives foreign investors a predictable operating environment.

Your specific industry and corporate structure will determine how much of that framework applies to your situation. A trading company routing international revenue through an NV or BV will encounter a different tax profile than a locally operating firm. The right entity type, the applicable exemptions under the National Ordinance on Profit Tax, and the registration requirements through the Chamber of Commerce of Sint Maarten all depend on factors specific to your business.

For business owners who have assessed those variables, the practical path forward involves engaging qualified local counsel and ensuring ongoing compliance with reporting obligations set by the Tax Administration of Sint Maarten. The formation process is relatively defined in its steps, but the decisions made before and during registration have lasting consequences for how your entity is taxed, governed, and positioned for future expansion.

Let Expanship Handle Your Sint Maarten Incorporation

Expanship Sint Maarten company incorporation services cover the full scope of what foreign business owners encounter when forming an NV or BV under the jurisdiction's civil law framework. From preparing notarial deeds of incorporation to filing with the Centraal Stemregister and maintaining ongoing compliance with the Chamber of Commerce of Sint Maarten, each stage involves documentation and procedural requirements that carry legal consequences if mishandled.

Expanship's service scope for Sint Maarten formations includes:

- Preparation and notarization of founding documents, including articles of incorporation

- Registered agent and registered office provision to satisfy local address requirements

- Liaison with the Chamber of Commerce of Sint Maarten for company registration and extract issuance

- Post-incorporation compliance management, including annual filing obligations and director record maintenance

- Document legalization and apostille processing where required for cross-border use

- Banking introduction assistance to support account opening for the newly formed entity

Each of these services addresses a distinct administrative requirement. Outsourcing them reduces the risk of procedural delays, rejected filings, or compliance gaps that could affect the company's standing with local authorities.

Reach out to Expanship Sint Maarten to discuss your incorporation requirements directly.

Frequently Asked Questions (FAQ)

Incorporation timelines vary depending on entity type and document readiness, but a BV or NV can generally be formed within a few weeks once notarial deed requirements are satisfied and the Chamber of Commerce registration is complete. The process involves notarial execution of the articles of incorporation, which is a mandatory step under local law. Delays most commonly arise from apostille requirements on foreign-sourced documents or incomplete due diligence submissions.

Foreign-sourced profits are generally not subject to corporate income tax under the territorial tax principles applied in Sint Maarten. This treatment is particularly relevant for holding companies and international trading entities that generate income outside the island. The precise scope of what qualifies as foreign-sourced income should be reviewed against the applicable tax ordinances and confirmed with a licensed local tax advisor.

There is no statutory requirement under Sint Maarten corporate law mandating that a director be a local resident for standard NV or BV formation. However, substance requirements may apply if your entity seeks to benefit from specific tax positions or treaty protections. Practical considerations around registered office obligations and notarial deed execution may necessitate engagement with a local service provider regardless of formal director residency rules.

Sint Maarten operates under a Dutch-influenced civil law system, which provides a codified and relatively predictable legal environment compared to common law Caribbean jurisdictions. The framework governing corporate formation and shareholder rights draws from principles embedded in Dutch corporate law traditions, offering familiarity to investors from continental European backgrounds. Comparisons with common law jurisdictions such as the British Virgin Islands or the Cayman Islands depend heavily on the investor's specific structuring objectives and home jurisdiction.

The minimum capital requirements for a BV in Sint Maarten are low relative to many European jurisdictions, though the exact statutory figure should be verified against current local ordinances, as capital rules can be amended by regulation. Unlike the NV, which historically carries higher capital thresholds given its suitability for public or larger commercial structures, the BV is designed for more closely held businesses where flexibility in capitalization is a practical advantage. A local notary overseeing the deed of incorporation will confirm the applicable requirements at the time of formation.

Failure to meet ongoing compliance requirements, including Chamber of Commerce filing obligations, can result in administrative penalties and may affect the company's good standing status. A company that loses its good standing may face restrictions on its ability to conduct certain transactions or access banking services locally. Reinstatement procedures exist but typically involve settling outstanding fees and filings, and prolonged non-compliance can lead to administrative dissolution under local corporate regulations.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.