Key Takeaways

- The Conservatória do Registo Comercial serves as the governing body for company incorporation and registration in São Tomé and Príncipe, operating under a civil law framework inherited from Portuguese legal traditions.

- Among available structures, the Sociedade por Quotas (LDA) is the most commonly used entity for small to mid-sized foreign investors due to its lower capital requirements and flexible quota management.

- The Sociedade Anónima (SA) is better suited to larger ventures that require share transferability and the ability to raise external capital, distinguishing it structurally from the LDA.

- Regulatory development in São Tomé and Príncipe is ongoing, with efforts directed toward aligning its commercial framework with OHADA principles and improving investment registration processes.

Introduction to Entity Types in São Tomé and Príncipe

São Tomé and Príncipe is a small island nation in the Gulf of Guinea, off the west coast of Central Africa, comprising two main islands and several smaller islets. It is an independent republic and a former Portuguese colony, which means its legal and corporate framework draws heavily from Portuguese civil law traditions.

Company registration falls under the jurisdiction of the Conservatória do Registo Comercial (Commercial Registry), which oversees the incorporation and ongoing registration of business entities in the country. The tax system is not a zero-tax or classic offshore regime — the country applies a standard territorial-based corporate tax framework, with rates and incentives that vary by sector and investment type.

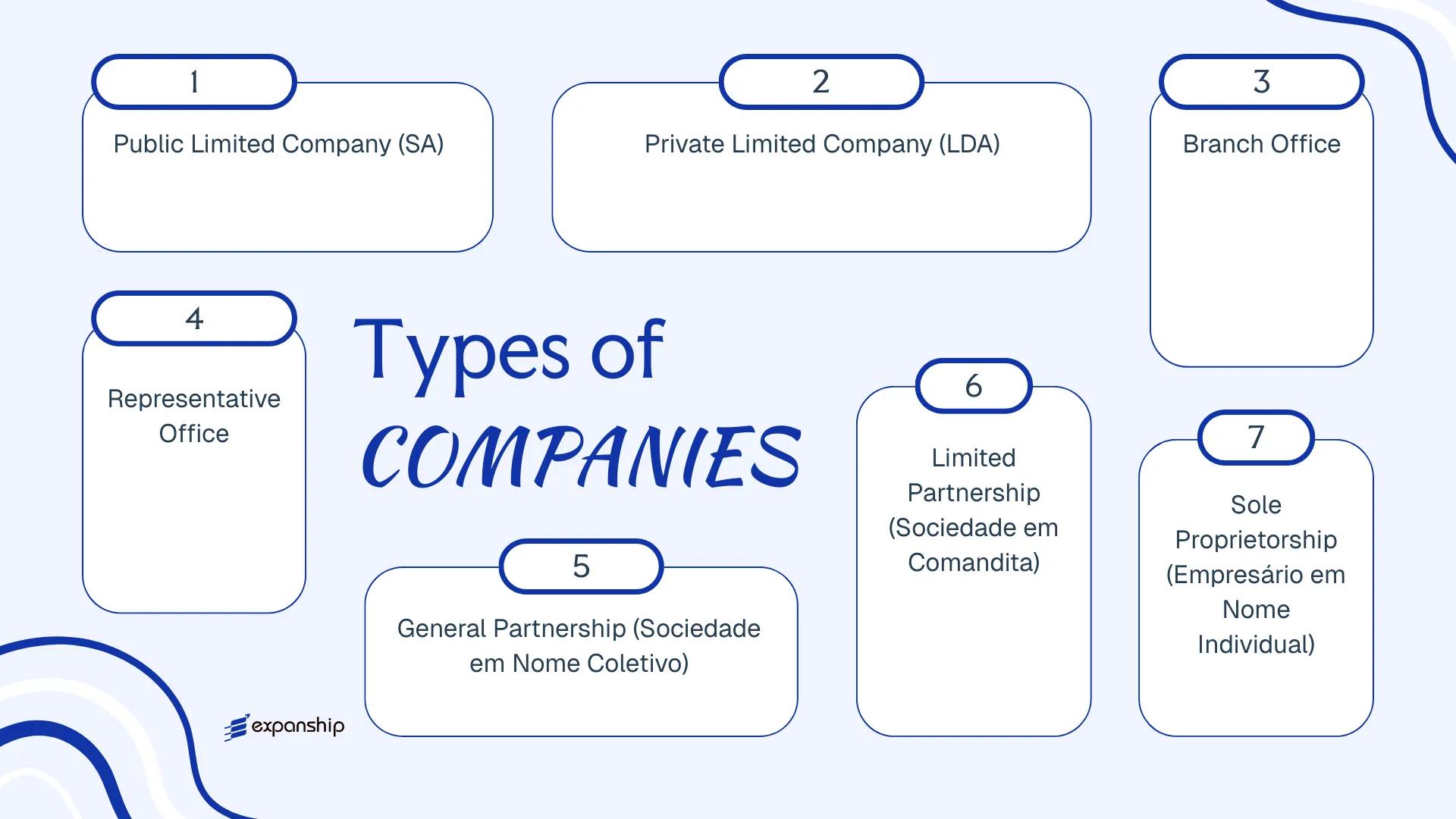

Several distinct business entity types São Tomé and Príncipe recognizes under its commercial code include:

- Sociedade Anónima (SA)

- Sociedade por Quotas (LDA)

- Sociedade em Nome Coletivo

- Sociedade em Comandita

- Empresário em Nome Individual

- Branch Office

- Representative Office

Each of these São Tomé and Príncipe corporate structures carries different requirements around capital, liability, governance, and registration procedure. This article examines each legal entity in turn, covering formation requirements, ownership rules, and practical considerations for foreign investors and local operators alike.

An Overview of Business Structures in São Tomé and Príncipe

São Tomé and Príncipe's company law framework, grounded primarily in the Código das Empresas Comerciais, provides several distinct legal structures for conducting business. Each form carries different implications for liability, governance, and capital requirements. The sections that follow examine each structure in detail.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Sociedade Anónima (SA) | Public Limited Company | Limited to share capital | Taxed | Yes | 5 shareholders | COSSIL / Commercial Registry | Código das Empresas Comerciais |

| Sociedade por Quotas (LDA) | Private Limited Company | Limited to quota value | Taxed | Yes | 2 members | Commercial Registry | Código das Empresas Comerciais |

| Branch Office | Foreign branch | Parent fully liable | Taxed on local income | Yes | N/A (parent entity) | Commercial Registry | Código das Empresas Comerciais |

| Representative Office | Non-trading presence | Parent fully liable | Generally exempt | No | N/A (parent entity) | Commercial Registry | Código das Empresas Comerciais |

| Sociedade em Nome Coletivo | General Partnership | Unlimited, joint | Taxed | Yes | 2 partners | Commercial Registry | Código das Empresas Comerciais |

| Sociedade em Comandita | Limited Partnership | Mixed (general/limited) | Taxed | Yes | 2 partners | Commercial Registry | Código das Empresas Comerciais |

| Empresário em Nome Individual | Sole Proprietorship | Unlimited, personal | Taxed | Yes | 1 individual | Commercial Registry | Código das Empresas Comerciais |

Each of these structures is examined in full in the sections below.

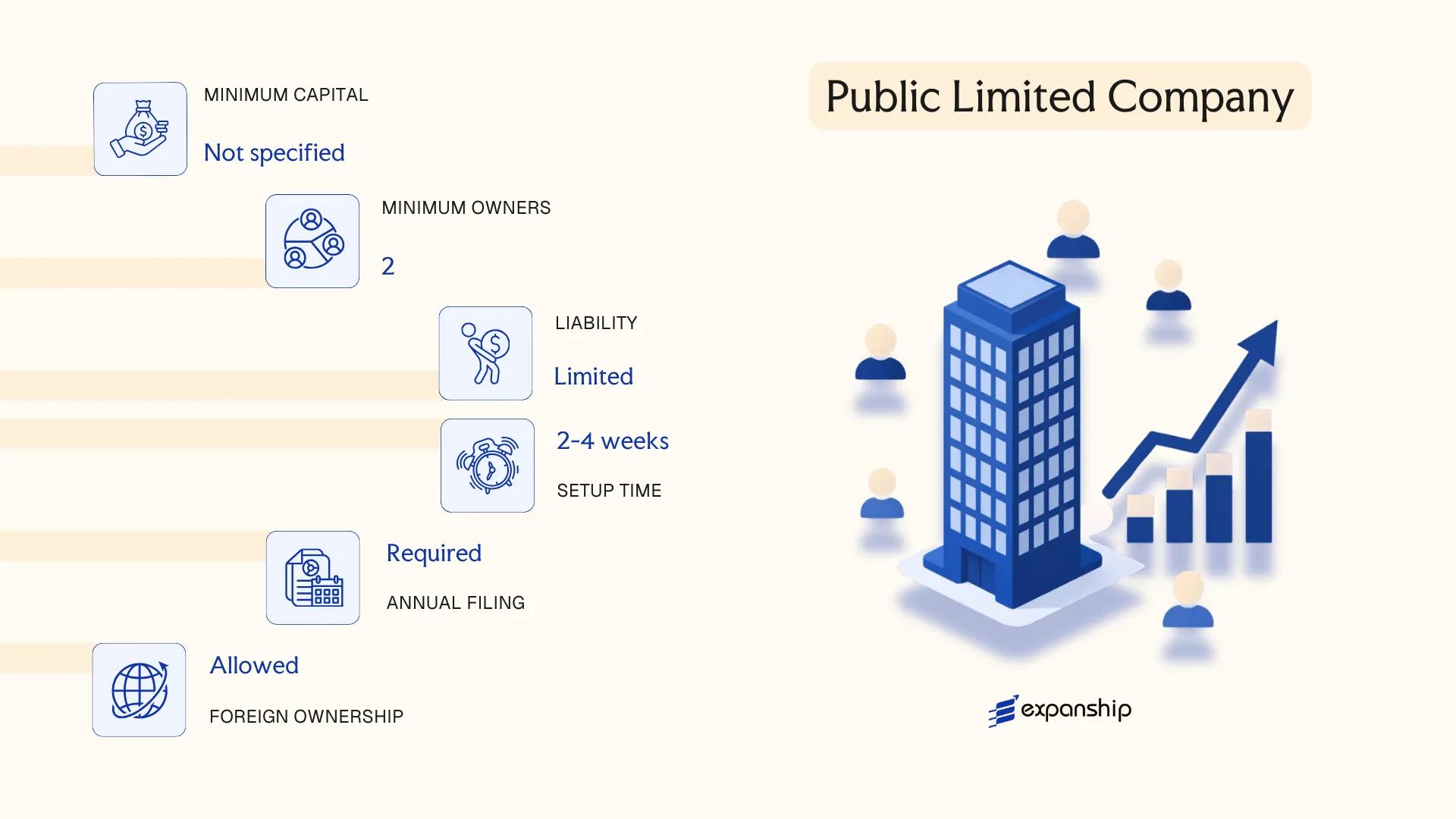

Sociedade Anónima (SA) — Public Limited Company

The Sociedade Anónima São Tomé and Príncipe framework is governed by the Commercial Companies Code (Código das Sociedades Comerciais), enacted in 2004 under Law No. 11/2004. The SA holds a distinct legal personality, fully separate from its shareholders, with liability confined to each shareholder's subscribed capital.

Structured around freely transferable shares, the SA suits businesses seeking external investment or eventual public listing. Shares may be registered or bearer form, subject to applicable regulatory conditions.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sociedade Anónima (SA) | Separate legal personality; limited liability |

| Members | Shareholders (minimum 2) | No statutory maximum on shareholders |

| Governance | Board of Directors + Supervisory Board (Conselho Fiscal) | Companies above certain thresholds must appoint a statutory auditor (Revisor Oficial de Contas) |

| Local Presence | Registered office in São Tomé and Príncipe | No mandatory local director requirement under general rules |

| Share Capital | Minimum STD 20,000,000 (approx. USD 900) | Must be fully subscribed at incorporation; at least 30% paid up |

| Privacy | Shareholder register maintained at company; public filing required with Conservatória do Registo Comercial | Beneficial ownership disclosure obligations apply |

Focus Points

- Taxation: Corporate income tax (Imposto sobre o Rendimento das Pessoas Colectivas, IRPC) applies at the standard rate; VAT (Imposto sobre o Valor Acrescentado, IVA) applies to taxable supplies; withholding taxes apply to dividends, interest, and royalties paid to non-residents. See the Direcção dos Impostos e das Alfândegas for current rates.

- Annual Compliance: Annual accounts must be filed with the Conservatória do Registo Comercial; general shareholder meetings are required at least once per year.

- Economic Substance: No OECD-style substance regime currently legislated, though commercial activity requirements under the Companies Code apply.

- Treaty Access: São Tomé and Príncipe has a limited double tax treaty network; treaty benefits should not be assumed without verification.

- Conversion: An SA may be converted to a Sociedade por Quotas (LDA) by shareholder resolution, subject to compliance with capital and procedural requirements under the Companies Code.

Closing

The SA structure suits trading companies, investment holding vehicles, and businesses anticipating equity participation from multiple investors. Its freely transferable share structure offers a clear advantage for capital-raising, though the mandatory supervisory board and statutory audit requirements above prescribed thresholds impose a higher administrative burden than a private limited form.

Best suited for larger commercial enterprises, joint ventures, or businesses planning to bring in institutional investors or external shareholders.

Company Incorporation in São Tomé and Príncipe

Expanship assists with end-to-end SA registration, from name reservation through to commercial registry filing.

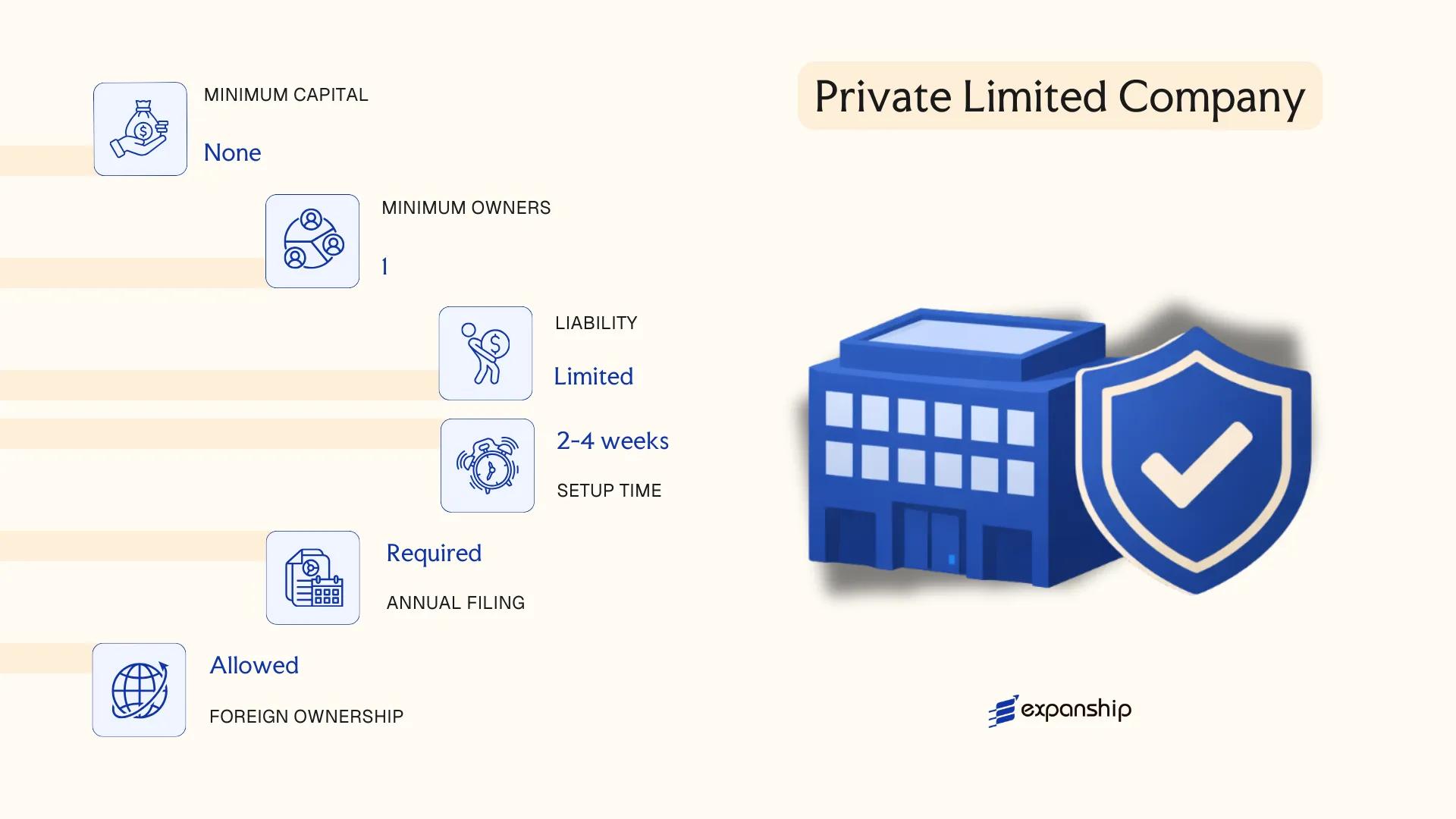

Sociedade por Quotas (LDA) — Private Limited Company

The Sociedade por Quotas São Tomé and Príncipe structure is governed by the Commercial Companies Code (Código das Sociedades Comerciais), which draws substantially from Portuguese corporate law tradition. As a distinct legal entity, the LDA carries its own rights and obligations, separate from those of its members.

Capital is divided into quotas rather than shares, and liability is limited to each member's subscribed quota. This hybrid character makes the LDA suitable for both closely held family businesses and foreign-invested trading or holding structures.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sociedade por Quotas (LDA) | Separate legal personality; governed by the Commercial Companies Code |

| Members | Minimum 2 quotaholders; no statutory maximum | Members hold quotas, not shares; single-member variant (Unipessoal LDA) also recognised |

| Management | One or more managers (gerentes) | Managers need not be members; no board requirement for standard LDA |

| Local Presence | Registered office address required in São Tomé and Príncipe | No statutory requirement for a resident registered agent, but a local address is mandatory |

| Capital | Minimum capital of 5,000,000 Dobras (STD); no paid-up instalment requirement specified | Denominated in São Tomé Dobra (STD); quotas must be fully described in the articles |

| Privacy | Member names appear in public registration records | No bearer quota mechanism; beneficial ownership is identifiable through registry |

Focus Points

- Taxation: Corporate income tax applies at the standard rate; VAT obligations arise on taxable supplies; withholding tax applies to dividends, interest, and royalties paid to non-residents; stamp duty may apply to certain instruments.

- Annual Compliance: Annual accounts must be filed with the Registo Comercial; financial statements are required regardless of activity level.

- Economic Substance: No OECD-style substance legislation currently enacted, though general tax residency rules apply.

- Restrictions: Foreign ownership is permitted across most sectors; certain regulated industries require prior ministerial approval.

- Conversion: An LDA may be converted to an SA by amending the articles and meeting the SA's higher capital threshold.

Closing

The LDA is the predominant vehicle for small to mid-scale trading, services, and foreign direct investment projects where a full SA structure is disproportionate. Its quota-based capital model simplifies member transfers, though unanimous or supermajority consent requirements for quota assignments can restrict exit flexibility.

Best suited for foreign investors and small-to-medium enterprises seeking a straightforward private structure with limited liability and without the governance burden of a public company.

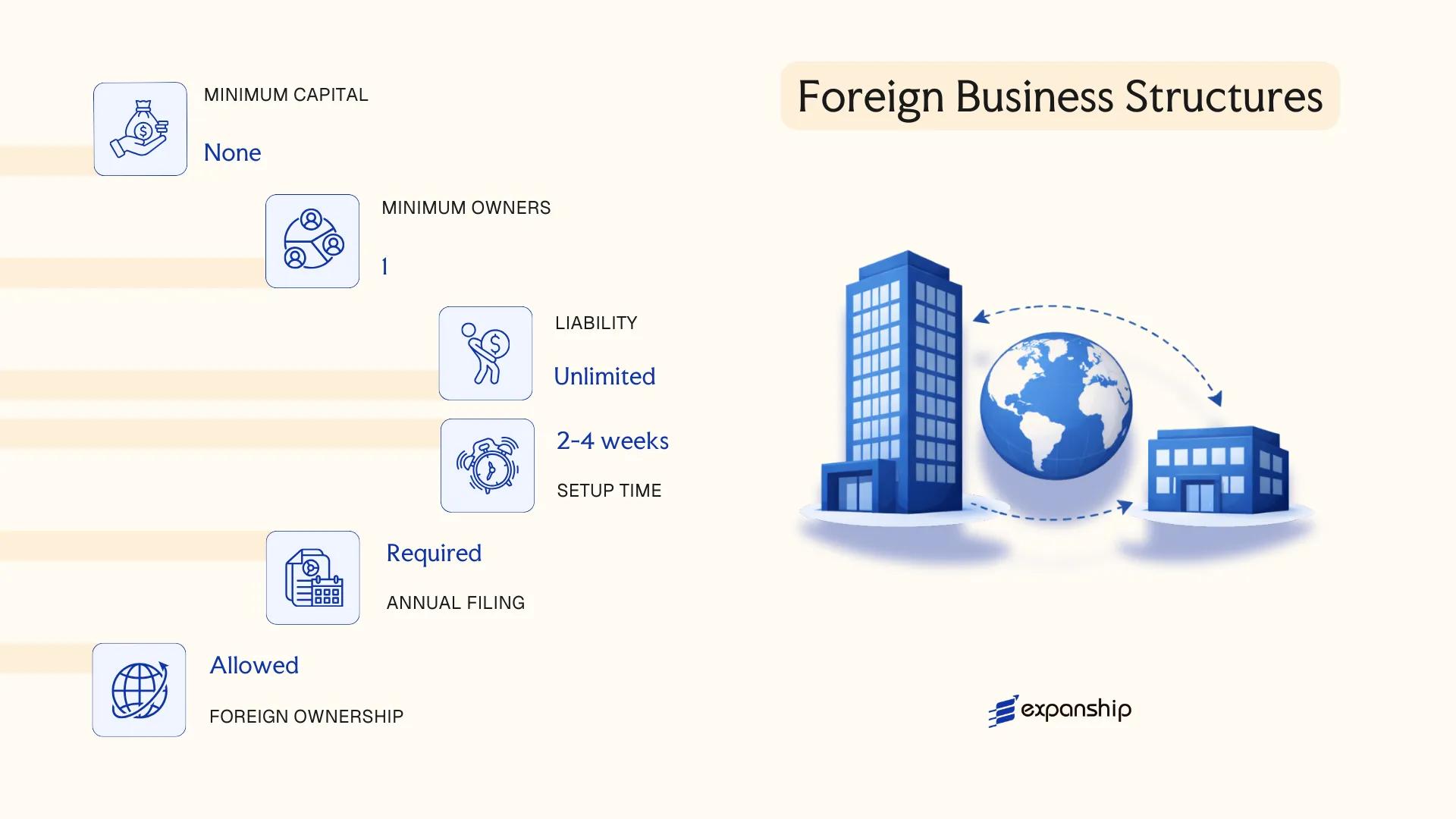

Foreign Business Structures in São Tomé and Príncipe [Branch Office, Representative Office]

Foreign companies seeking a presence in the country without forming a new local entity have two principal options: establishing a branch office or registering a representative office. Under the Commercial Companies Code (Código das Sociedades Comerciais), a foreign branch office in São Tomé and Príncipe is treated as an extension of the parent company rather than a distinct legal entity, meaning the parent retains full liability for all obligations the branch incurs.

Registration of either structure is administered through the Conservatória do Registo Comercial, which requires submission of authenticated and apostilled parent company documents, including constitutional documents and evidence of good standing in the home jurisdiction.

Key Characteristics

| Requirement | Branch Office | Representative Office |

|---|---|---|

| Legal Form | Extension of foreign parent; no separate legal personality | Extension of foreign parent; no separate legal personality |

| Liability | Parent company bears full liability | Parent company bears full liability |

| Designated Representative | Locally appointed legal representative required | Locally appointed representative required |

| Local Presence | Registered address in-country required | Registered address in-country required |

| Capital | No statutory minimum capital requirement | No statutory minimum capital requirement |

| Permitted Activities | Commercial and operational activities allowed | Limited to liaison, market research, and promotion — no revenue-generating activity |

Focus Points

- Taxation: Branch profits are subject to corporate income tax (Imposto sobre o Rendimento das Pessoas Colectivas) at the standard rate; VAT and withholding tax obligations apply to taxable transactions conducted through the branch.

- Economic Substance: The branch must maintain genuine operational activity in-country; a representative office, by contrast, is restricted from conducting direct commercial operations.

- Annual Compliance: Both structures are required to file periodic reports and maintain updated registration records with the Conservatória do Registo Comercial.

- Treaty Access: Access to double tax treaties depends on the parent company's home jurisdiction; São Tomé and Príncipe has a limited treaty network, which may affect withholding tax exposure.

- Conversion: A branch may be converted into a locally incorporated entity, though this requires a separate incorporation process under the Commercial Companies Code.

Sub-Types

Branch Office (Sucursal)

A sucursal conducts active commercial operations and enters into contracts directly, making it suitable for foreign firms with ongoing trading or service delivery activity in the country.

Representative Office (Escritório de Representação)

This structure is confined to non-commercial functions such as promotion, liaison, and market intelligence. It cannot generate local revenue, sign commercial contracts, or invoice clients independently.

Closing Paragraph and Recommendations

Both structures suit foreign businesses testing market entry or maintaining an operational footprint without full local incorporation, though the branch's unlimited parental liability is a material exposure that should be assessed against the volume and nature of intended activities.

A branch office is best suited to established foreign companies with confirmed commercial activity in-country; a representative office fits those conducting preliminary market research or maintaining client liaison functions only.

Partnerships in São Tomé and Príncipe [Sociedade em Nome Coletivo, Sociedade em Comandita]

Partnerships in São Tomé and Príncipe are governed by the Commercial Code (Código Comercial), which provides for two distinct partnership structures: the Sociedade em Nome Coletivo São Tomé Príncipe (general partnership) and the Sociedade em Comandita (limited partnership). Both forms carry full legal personality upon registration with the Conservatória do Registo Comercial.

The general partnership (Sociedade em Nome Coletivo) holds all partners jointly and unlimitedly liable for the firm's obligations. The Sociedade em Comandita introduces a hybrid liability model, separating partners into two classes with differing exposure to the entity's debts.

Key Characteristics

| Requirement | Sociedade em Nome Coletivo | Sociedade em Comandita |

|---|---|---|

| Legal Form | General Partnership | Limited Partnership (Simple or by Shares) |

| Members | Partners (minimum 2, no statutory maximum) | General partners (min. 1) + Limited partners (min. 1) |

| Liability | Unlimited, joint and several for all partners | General partners: unlimited; Limited partners: capped at capital contribution |

| Local Presence | Registered office in São Tomé and Príncipe required | Registered office required |

| Capital | No statutory minimum; denominated in Dobra (STN) | No statutory minimum for simple form |

| Privacy | Partner names publicly registered | General and limited partner names disclosed in registration |

Focus Points

- Taxation: Profits are generally taxed at the entity level under the Imposto sobre o Rendimento das Pessoas Colectivas (IRPC); VAT (Imposto sobre o Valor Acrescentado) applies to applicable commercial activities; withholding tax applies to distributions to non-resident partners.

- Annual Compliance: Firms must file annual accounts and maintain updated partner records with the Conservatória do Registo Comercial.

- Treaty Access: Access to double tax treaties is limited given the jurisdiction's narrow treaty network; professional advice is warranted before structuring cross-border arrangements through a partnership.

- Conversion: Conversion from a partnership to a Sociedade por Quotas or Sociedade Anónima is permissible under the Commercial Code, subject to regulatory procedures.

- Restrictions: Foreign nationals may face additional requirements when registering as general partners with unlimited liability exposure.

Sub-Types

Sociedade em Comandita Simples (Simple Limited Partnership)

Partners contribute capital directly, with limited partners' liability confined to their respective contributions. This structure is typically used for family-owned ventures or professional collaborations where some participants require liability protection.

Sociedade em Comandita por Ações (Limited Partnership by Shares)

Limited partners hold transferable shares rather than fixed quota interests, allowing for broader capital participation. This variation is less common and generally suited to larger commercial operations requiring more flexible ownership arrangements.

Partnership structures are most commonly used for professional services firms, family businesses, and certain trading activities where partners accept direct operational involvement. The principal advantage of the Sociedade em Comandita is its ability to accommodate passive investors alongside active managers within a single entity. However, unlimited personal liability for general partners represents a material drawback that limits appeal for higher-risk commercial activities.

Partnership structures in São Tomé and Príncipe are best suited for closely held businesses, professional practices, or family enterprises where partners have an established level of mutual trust and direct operational control.

Sole Proprietorship in São Tomé and Príncipe [Empresário em Nome Individual]

The Empresário em Nome Individual São Tomé Príncipe is the simplest form of business registration available under the country's commercial framework, governed by the Código Comercial (Commercial Code). Unlike capital companies, this structure carries no separate legal personality — the business and its owner are legally the same person.

Because no distinction exists between personal and business assets, the proprietor bears unlimited liability for all obligations incurred. Registration is handled through the Instituto de Inovação Empresarial (IPEX) and the relevant civil registry authorities, making self-employed registration São Tomé Príncipe relatively straightforward in procedural terms.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sole Proprietorship (Empresário em Nome Individual) | No separate legal personality from owner |

| Members | Single proprietor | No minimum capital partners; one individual only |

| Liability | Unlimited personal liability | Personal assets fully exposed to business debts |

| Local Presence | Registered business address required | Physical presence in the country expected |

| Capital | No statutory minimum | Declared capital is informally recorded at registration |

| Privacy | Owner's name is publicly associated with the business | No anonymity available |

Focus Points

- Taxation: Subject to personal income tax (IRS) on business profits; VAT registration required once turnover thresholds are met; no corporate income tax applies.

- Annual Compliance: Required to maintain basic accounting records and submit annual income declarations to the Direcção dos Impostos.

- Treaty Access: As an unincorporated individual trader, access to double tax treaty benefits is limited compared to corporate entities.

- Conversion: Can be converted into a Sociedade por Quotas or other capital company as business activity grows, though the process requires a new registration rather than a structural transformation.

- Restrictions: Foreign nationals face additional requirements around residency permits before operating as an individual business owner in São Tomé and Príncipe.

Closing

This structure suits freelancers, artisans, and small-scale local traders who operate independently without plans for external investment. The primary advantage is minimal setup cost and administrative simplicity; the significant drawback is full personal exposure to business liabilities with no protective corporate veil.

Local residents or established residents operating low-risk, low-turnover businesses who do not require external financing or liability protection.

How to Choose the Right Entity Type in São Tomé and Príncipe

Choosing the right company structure in São Tomé and Príncipe has direct legal and financial consequences — the wrong choice creates compliance exposure, not just inconvenience.

Why Your Entity Choice Matters

- Selecting an entity without the capacity to conduct local commercial activity when you intend to trade with residents puts your business in breach of the Commercial Companies Code (Código das Sociedades Comerciais), which can result in administrative penalties or forced dissolution.

- Choosing a structure that carries a tax exemption may disqualify your entity from claiming reduced withholding tax rates under any applicable double taxation agreements, since treaty benefits typically require the claimant to be subject to tax.

- Picking a corporate structure when your purpose is asset protection or succession planning subjects you to ongoing shareholder meeting requirements and annual reporting obligations that would not apply under a trust or foundation arrangement.

Key Factors to Consider

- Business Activity: Active trading, passive asset-holding, and regulated sectors each point to a distinct structure under the Commercial Companies Code.

- Local vs. Cross-Border Operations: Transacting with São Tomé and Príncipe residents generally requires a locally registered entity rather than a foreign branch or representative office.

- Ownership and Management: A single-owner consultancy may find the Empresário em Nome Individual sufficient, while multi-party ventures require the governance framework of an LDA or SA.

- Tax Objectives: Your need for full exemption, a standard corporate rate, or treaty eligibility determines which entity fits your fiscal position.

- Substance Capacity: If you cannot maintain a physical presence and local decision-making, confirm whether your chosen structure carries minimum substance thresholds before registering.

- Exit Strategy: Confirm in advance whether your structure permits redomiciliation, conversion, or voluntary winding-up under applicable procedural rules.

The primary legislation governing company formation is the Commercial Companies Code of São Tomé and Príncipe, administered through the Conservatória do Registo Comercial.

Compliance Services for Companies in São Tomé and Príncipe

Ongoing compliance support for registered entities, including annual filings, registered agent maintenance, and regulatory reporting obligations.

Conclusion

Incorporating a company in São Tomé and Príncipe requires selecting from a defined set of structures, each suited to distinct operational and ownership profiles. The Sociedade por Quotas remains the most commonly registered entity among small to mid-sized foreign investors, given its lower capital threshold and flexible quota management. The Sociedade Anónima suits larger ventures requiring share transferability and access to external capital. Branch offices serve foreign firms with existing legal personality that need a direct operational presence, while representative offices are confined to non-commercial functions. Partnerships and sole proprietorships address locally oriented, smaller-scale activity.

Regulatory reform in São Tomé and Príncipe has been gradual, with ongoing efforts to align commercial frameworks more closely with OHADA principles and improve investment registration processes. Your choice of structure will increasingly carry implications as the jurisdiction continues refining its business environment and bilateral engagement.

How Expanship Can Assist You

Expanship provides company incorporation services São Tomé Príncipe businesses and foreign investors rely on when registering a Sociedade por Quotas, Sociedade Anónima, or branch structure with the Registo Comercial. From initial structuring decisions to filing with the relevant public registry, your setup process is managed with direct knowledge of local procedures.

Expanship's São Tomé and Príncipe business setup support covers the full formation and post-registration cycle:

- Document preparation, notarization, and legalization for submission

- Registered agent and registered office provision in São Tomé

- Government filing and Registo Comercial liaison on your behalf

- Ongoing compliance management, including annual obligations

- Corporate secretarial support for statutory record-keeping

- Banking introduction assistance for local and international accounts

Reach out to Expanship São Tomé and Príncipe to discuss your entity structure and next steps.

Frequently Asked Questions (FAQ)

The Sociedade por Quotas (LDA) is the most frequently incorporated structure. Its lower minimum capital threshold and simplified governance requirements make it the default choice for small and medium-sized businesses.

An SA requires higher share capital and must maintain a more formal governance structure, including a supervisory board in certain configurations. An LDA restricts the transfer of quotas, which offers tighter ownership control but limits capital-raising options. Both structures are subject to domestic corporate tax obligations and can conduct local trading activities.

Under São Tomé and Príncipe commercial law, neither the SA nor the LDA provides absolute beneficial ownership confidentiality, as registration details are filed with the Registo Comercial. Nominee arrangements may be used in practice, but their legal effect depends on underlying contractual documentation and applicable local regulations.

An LDA can be formed by a single quota-holder. A Sociedade em Nome Coletivo and Sociedade em Comandita each require a minimum of two partners by their legal nature. An SA requires at least one shareholder but broader governance structures may require multiple appointees.

Foreign nationals may incorporate an LDA or SA without restrictions on nationality. A branch office requires the foreign parent entity to be duly constituted abroad and registered with the competent Santomean commercial registry. Representative offices are available for non-trading purposes and carry fewer compliance obligations.

Conversion between an LDA and an SA is generally recognised under Santomean commercial law, subject to satisfying the capital and governance requirements of the target structure. The process requires updated articles of association and re-registration with the Registo Comercial. Conversion into a partnership form from a limited liability structure is less commonly pursued and subject to creditor notification requirements.

An SA, LDA, and both forms of Sociedade em Comandita hold separate legal personality distinct from their members. A Sociedade em Nome Coletivo does not fully insulate partners from liability, as general partners remain jointly and severally liable for the firm's obligations. Sole proprietorships under the Empresário em Nome Individual carry no legal separation between the individual and the business.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.