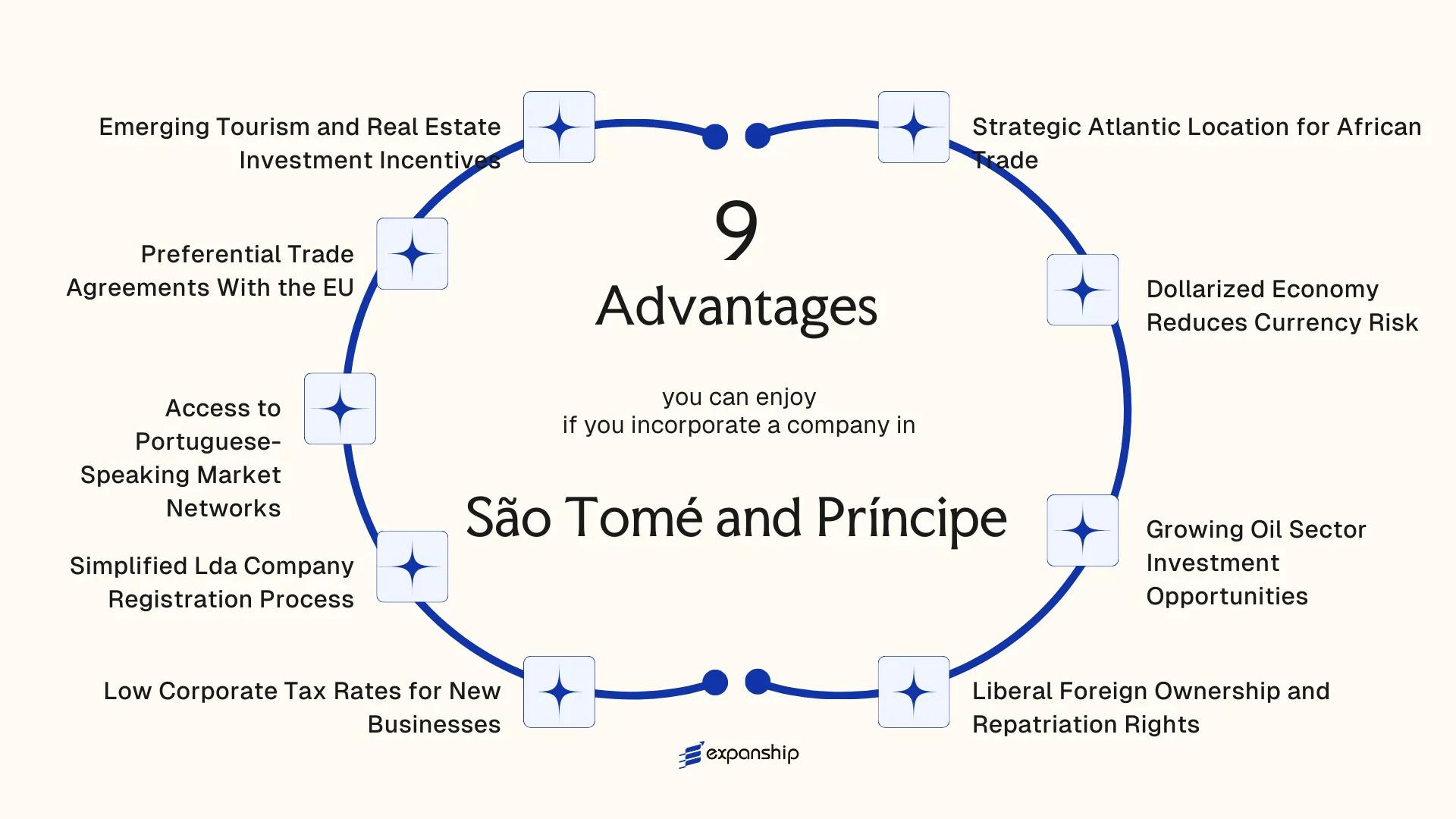

Key Takeaways

- Foreign investors benefit from oversight under the IGAE (Inspecção-Geral das Actividades Económicas), which provides a defined regulatory pathway for commercial registration and business licensing through the Sociedade por Quotas (Lda) structure.

- Conducting business in a dollarized economy eliminates exchange rate exposure that would otherwise affect cross-border profit calculations and financial planning for foreign-owned entities.

- Priority sectors including energy, tourism, and trade intermediation carry access to targeted tax incentive structures that reduce the effective corporate burden beyond the standard low-tax baseline São Tomé and Príncipe already maintains.

- Statutory protections permitting full repatriation of profits mean foreign shareholders can extract returns without the capital controls that complicate operations in many competing Gulf of Guinea jurisdictions.

São Tomé and Príncipe is an independent island nation located in the Gulf of Guinea, positioned along the central Atlantic coast of West Africa. Understanding the benefits of incorporating in São Tomé and Príncipe begins with recognizing the country's regulatory framework, which falls under the oversight of the IGAE (Inspecção-Geral das Actividades Económicas), the body responsible for commercial registration and business licensing. Foreign businesses most commonly establish a presence through the Sociedade por Quotas, known locally as the Lda.

The country maintains a generally low-tax posture, with incentive structures designed to attract foreign direct investment across priority sectors. Ownership restrictions on foreign entities are limited, and the legal framework broadly permits international investors to hold equity in locally registered firms.

This article outlines the principal advantages that a registered business entity in this jurisdiction can offer to foreign investors and multinational operators.

Strategic Atlantic Location for African Trade

São Tomé and Príncipe's position in the Gulf of Guinea places it roughly equidistant between the west coast of Central Africa and the major Atlantic shipping corridors. For businesses targeting sub-Saharan markets, this geographic positioning translates into direct proximity to Nigeria, Gabon, Cameroon, and the Democratic Republic of Congo without requiring a regional headquarters in any of those jurisdictions.

Proximity to West and Central African Markets

The archipelago sits within the Gulf of Guinea business hub, approximately 300 kilometers off the coast of Gabon. This puts your firm within short haul distance of some of Africa's largest oil-producing and resource-extraction economies, reducing transit times and logistical costs for goods and personnel moving across the region.

A Practical Gateway for Atlantic-Facing Trade

The country's two deepwater ports serve vessels operating on transatlantic routes connecting Africa to Europe and the Americas. Businesses registered here can position operations to service both inbound investment flows and outbound commodity trade, without requiring a physical presence in higher-cost neighboring jurisdictions.

Your registered entity gains a geographically central base for coordinating Gulf of Guinea trade activity without the regulatory overhead of larger regional markets.

Dollarized Economy Reduces Currency Risk

São Tomé and Príncipe's currency, the dobra (STN), has been pegged to the euro since 1999 under a formal agreement with Portugal and the European Central Bank. This fixed exchange rate arrangement eliminates the unpredictable fluctuation that affects many other sub-Saharan African currencies, giving foreign businesses a stable pricing environment for contracts, invoicing, and financial planning.

For companies that trade in euros or operate across the eurozone, this peg functions as a built-in hedge. Your costs denominated in dobra remain predictable when converted, reducing the need for expensive currency hedging instruments that firms operating in free-floating African markets routinely require.

The São Tomé and Príncipe dollarized economy benefits for investors extend into operational practicality:

- Profit repatriation calculations are straightforward because the dobra-euro conversion rate does not shift with local monetary policy decisions

- Foreign suppliers and contractors invoicing in euros face no conversion uncertainty when dealing with locally incorporated entities

- Multi-year investment models hold their assumptions without building in a currency depreciation buffer

- Banking relationships with Portuguese and European correspondent banks are simplified by the shared currency framework

The peg is maintained through the Banco Central de São Tomé e Príncipe under terms of the monetary cooperation agreement, meaning exchange rate policy is structurally constrained rather than subject to discretionary central bank intervention.

Company Incorporation in São Tomé and Príncipe

Incorporate your business in São Tomé and Príncipe with full support from entity selection through registration and compliance setup.

Growing Oil Sector Investment Opportunities

São Tomé and Príncipe oil sector investment opportunities have drawn growing attention since the archipelago's waters were confirmed to sit within the hydrocarbon-rich Gulf of Guinea. Seismic surveys conducted across the country's Exclusive Economic Zone and within the Joint Development Zone (JDZ) shared with Nigeria have identified significant offshore oil and gas potential, placing this small island nation in a category that few Atlantic jurisdictions of comparable size can claim.

The JDZ, governed by the Nigeria-São Tomé and Príncipe Joint Development Authority (JDA), operates under a formal treaty framework that structures block licensing, revenue sharing, and dispute resolution. Foreign firms entering through JDA-administered concessions gain a defined legal basis for operations rather than relying on administrative discretion.

| Feature | Detail |

|---|---|

| Joint Zone Regulator | Nigeria-STP Joint Development Authority (JDA) |

| STP Revenue Share (JDZ) | 40% of JDZ petroleum revenues |

| STP Exclusive Economic Zone | Governed by domestic petroleum legislation |

| Block Licensing Model | Production sharing agreements (PSAs) |

São Tomé and Príncipe retains 40% of JDZ revenues under the treaty terms, and that income stream flows through a National Oil Account structure designed to maintain fiscal transparency. For energy sector investors, this institutional architecture reduces the counterparty risk that frequently accompanies petroleum ventures in smaller emerging economies. Production sharing agreements used in block licensing also allow your firm to negotiate cost recovery terms before profit oil is divided, which directly affects project-level returns from the earliest phases of development.

Liberal Foreign Ownership and Repatriation Rights

Foreign ownership rights in São Tomé and Príncipe are governed under the country's investment framework, which permits non-nationals to hold 100% equity in locally incorporated companies. No mandatory joint-venture requirement exists with a local partner, meaning your firm retains full structural control from the point of registration. This directly removes one of the most common barriers foreign investors face in other sub-Saharan jurisdictions.

Under the Investment Law, foreign capital invested in qualifying sectors is protected against arbitrary expropriation, and approved investors may repatriate profits, dividends, and capital abroad without government-imposed restrictions tied to minimum holding periods. The practical effect is that your business can distribute returns to shareholders in any currency without waiting years for regulatory clearance.

Keep the following in mind:

- 100% foreign ownership São Tomé and Príncipe companies is permitted without mandatory local partnership

- São Tomé and Príncipe profit repatriation advantages apply to approved foreign investments under the formal investment registration process

- Registration with the relevant investment authority is required before repatriation protections formally apply

- Currency exchange transactions must pass through licensed domestic banking institutions

The São Tomé and Príncipe liberal investment laws for foreign investors also extend to property rights associated with business operations, which reinforces the ownership protections already available at the equity level.

São Tomé and Príncipe's investment protections apply equally to diaspora investors and non-resident foreigners, with no nationality-based distinction in ownership entitlements.

Low Corporate Tax Rates for New Businesses

São Tomé and Príncipe low corporate tax rate advantages are most visible in how the country's fiscal code treats newly established entities during their early operating years. Under the Investment Code, qualifying businesses can benefit from tax exemptions or reductions during an initial period, with the standard corporate income tax (IRC) rate set at 25%. While that headline rate is not unusually low on its own, the incentive structure changes the effective burden substantially for eligible firms.

Tax Holidays and Reduced Rates Under the Investment Code

New businesses registered under the national Investment Code can access graduated tax reductions that lower the effective IRC rate during the startup phase. Your company's tax position in the first years of operation can differ significantly from what the statutory rate alone would suggest, particularly if the entity is classified within a priority investment sector.

These reductions are tied to declared investment amounts and sectoral classification, so the benefit scales with the scale of commitment. A firm investing in tourism, agriculture, or export-oriented activities may qualify for an extended reduction period, meaning lower tax drag precisely when capital is being deployed and returns have not yet stabilized.

Implications for Foreign Investor Cash Flow

For a foreign investor, reduced corporate tax during the establishment phase directly improves early-stage cash flow. Lower tax exposure in years one through five can make the difference between reinvesting profits locally and drawing on external capital to fund expansion.

The fiscal incentives for companies are administered through the Investment Promotion Agency (API-STP), which evaluates applications and certifies eligibility.

Maximize Your Tax Position Before You Incorporate in São Tomé and Príncipe

Expanship's specialists can assess which fiscal incentives your business qualifies for under the Investment Code and guide you through the API-STP certification process.

Simplified Lda Company Registration Process

Forming a Sociedade por Quotas (Lda) in São Tomé and Príncipe carries procedural advantages that directly reduce the time and cost of establishing a legal presence. The registration framework is administered through the Conservatória do Registo Comercial, and the documentary requirements for an Lda are comparatively limited, which matters when your business needs to operate quickly rather than wait months on bureaucratic processing.

- A single shareholder can form an Lda, removing the requirement to identify and onboard multiple founding partners before incorporation can proceed.

- Minimum capital requirements for an Lda are low by regional standards, meaning capital is not tied up in statutory deposits before the entity can trade.

- Shareholder liability is capped at each party's subscribed quota, so personal assets remain separated from company obligations from the moment of registration.

- The Lda structure does not require a local resident director in all circumstances, which reduces the operational overhead for foreign-owned entities during setup.

- Once registered, the Lda can open a corporate bank account and enter contracts in its own name, giving your firm legal standing without requiring a physical office to be established first.

The combination of a low formation threshold and defined liability separation means foreign investors can test commercial activity in the market without committing to the full infrastructure of a branch or subsidiary.

Access to Portuguese-Speaking Market Networks

São Tomé and Príncipe's membership in the Comunidade dos Países de Língua Portuguesa (CPLP) gives companies registered there a culturally and linguistically direct entry point into a bloc that spans nine member states across four continents, with a combined population exceeding 260 million people. That shared language framework reduces friction in contract negotiation, regulatory communication, and partnership formation across Angola, Mozambique, Brazil, Portugal, and Cape Verde, among others.

For businesses targeting Sub-Saharan Africa specifically, the CPLP business network advantages extend beyond language. Angola and Mozambique are among Africa's larger resource economies, and a company established under São Tomé and Príncipe's legal framework can position itself as a Lusophone-registered entity when engaging procurement, distribution, or joint venture discussions in those markets.

Portuguese is also an official working language of the African Union, which adds institutional relevance when your business participates in regional trade forums or bids on multilateral development contracts across the continent.

A firm registered in a CPLP member state engaging with Angola's oil services sector or Mozambique's LNG corridor faces fewer interpretive and procedural barriers than a non-Lusophone entity operating under translated documentation and third-party legal intermediaries, directly reducing transaction costs.

Preferential Trade Agreements With the EU

São Tomé and Príncipe EU trade agreement benefits for businesses stem from the country's status as an ACP (African, Caribbean and Pacific) state under the Cotonou Agreement framework and its subsequent engagement with the EU's Economic Partnership Agreement (EPA) process. As a Least Developed Country (LDC), the archipelago also qualifies for Everything But Arms (EBA) preferential access, meaning goods originating here can enter the EU market duty-free and quota-free across virtually all product categories.

For a trading entity registered on the islands, this translates into a structurally lower cost of accessing European consumers compared to firms based in non-LDC jurisdictions that face standard Most Favoured Nation (MFN) tariff schedules.

ACP EU trade benefits for São Tomé and Príncipe companies extend beyond tariff savings:

- Preferential rules of origin under EPA frameworks allow qualifying products to enter EU markets without full domestic content requirements

- Agricultural and processed food exports can access EU markets under reduced tariff conditions unavailable to most developing economies

- Bilateral trade facilitation commitments reduce documentary friction at EU customs entry points

EBA and EPA preferences apply to goods with verified origin status; your products must meet the specific rules of origin defined under the relevant agreement to qualify for preferential rates.

Emerging Tourism and Real Estate Investment Incentives

São Tomé and Príncipe tourism investment incentives for businesses are anchored in the country's Investment Law (Law No. 13/2019), which establishes a legal framework for qualifying projects in priority sectors, including tourism and hospitality. Projects that meet defined thresholds in job creation and capital expenditure can access tax exemptions on corporate income for a specified period, along with customs duty waivers on imported equipment. For a foreign operator developing a hotel or resort, this directly reduces the capital cost of entering the market.

Designated Tourism Zones

The government has identified specific geographic areas, particularly along coastal zones on both the main island and Príncipe, as priority development corridors. Investment projects located within these designated zones may qualify for accelerated depreciation allowances and reduced land use fees under applicable licensing frameworks administered by the Agência de Promoção de Investimentos (API-STP). This zone-based structure means your project's location carries direct fiscal consequences.

Property Access for Foreign Entities

Foreign-registered companies can hold real estate in their own name under the local legal framework, provided the entity is formally incorporated and compliant with registration requirements. This matters because it removes the structural need for a local nominee or joint-venture arrangement solely for land-holding purposes.

Early-Market Positioning

The hospitality sector remains underdeveloped relative to the archipelago's ecological profile as a UNESCO-recognized biosphere reserve. With limited branded hotel inventory currently in place, incoming operators face reduced direct competition, which affects both pricing power and occupancy projections in feasibility modeling.

Why São Tomé and Príncipe Beats Rival African Jurisdictions

Compared against other small-island or coastal African jurisdictions that also target foreign incorporation, São Tomé and Príncipe holds measurable structural advantages in several parameters. The most realistic competitor set for a foreign investor evaluating this archipelago includes Mauritius, Seychelles, and Cape Verde, each of which markets itself to international businesses on broadly similar grounds: political stability, Atlantic or Indian Ocean positioning, and investment-friendly legislation.

What the comparison reveals is less about headline tax rates and more about access and friction. Mauritius and Seychelles have matured into well-regulated financial centres, but that maturity has produced heavier compliance requirements, including FATF-aligned beneficial ownership registers and increasingly scrutinised substance requirements. Cape Verde, geographically the closest Atlantic African comparator, operates within a narrower trade network. The São Tomé and Príncipe advantages over other African jurisdictions become tangible when you examine currency stability, EU preferential access under the Cotonou framework successors, and the relatively open foreign ownership framework under the national investment code.

| Parameter | São Tomé and Príncipe | Mauritius | Seychelles | Cape Verde |

|---|---|---|---|---|

| Currency risk | Low (USD-pegged dobra) | Moderate (floating rupee) | Moderate (floating rupee) | Moderate (EUR-pegged escudo) |

| EU preferential trade access | Yes (EPA framework) | Partial (IEPA) | Limited | Yes (EPA framework) |

| Foreign ownership cap | None (100% permitted) | None | None | Sector restrictions apply |

| Corporate tax for new investments | Reduced rates under investment incentives | 15% standard GBC rate | 0–1.5% (offshore structures) | 25% standard rate |

| Substance requirements | Minimal at present | Enforced rigorously | Increasing post-FATF review | Moderate |

| Portuguese-language market access | Direct | None | None | Direct |

Compliance Services for Companies in São Tomé and Príncipe

Maintain your company's good standing with ongoing compliance support, including annual filings, registered agent services, and regulatory reporting under São Tomé and Príncipe law.

Conclusion

São Tomé and Príncipe presents a coherent case for foreign incorporation when its individual advantages are considered together. The combination of a dollarized economy that removes exchange rate exposure, statutory protections for full profit repatriation, and tax incentives directed at priority sectors creates a structurally sound environment for foreign capital.

The benefits of incorporating in São Tomé and Príncipe carry the most weight for businesses aligned with its core economic drivers, particularly energy, tourism, and trade intermediation across the Gulf of Guinea. A firm that operates outside those sectors may find the incentive framework less directly applicable, though the general corporate environment remains open to foreign ownership across most industries.

Getting the most from this jurisdiction requires that your business structure, tax residency position, and operational model align with what the local framework actually offers. The next step is translating that alignment into a properly registered, compliant entity under São Tomean law.

Let Expanship Handle Your São Tomé and Príncipe Incorporation

Expanship provides corporate services for foreign investors forming a Sociedade por Quotas (Lda) or other permitted entity structures in this jurisdiction. From initial documentation to post-incorporation compliance, the firm works directly with the Conservatória do Registo Comercial and coordinates with the Centro de Formalidades das Empresas where applicable to keep filings on schedule and in proper form.

Engagements cover the full formation and maintenance cycle:

- Preparation and legalization of constitutional documents, including the Pacto Social

- Registered agent and registered office provision within the jurisdiction

- Filing liaison with the Conservatória do Registo Comercial and relevant fiscal authorities

- Post-incorporation compliance management, including annual obligations under the commercial registry framework

- Notarial coordination for document authentication requirements

- Banking introduction assistance for corporate account opening with locally operating institutions

Reach Expanship São Tomé and Príncipe to discuss your formation requirements.

Frequently Asked Questions (FAQ)

Registration timelines vary depending on document completeness and the processing capacity of the relevant commercial registry, but the process generally takes several weeks from submission of the required incorporation documents. Delays most commonly arise from notarisation requirements or incomplete statutory filings rather than from the registration procedure itself.

New businesses operating under approved investment status may benefit from reduced corporate income tax rates during an initial period, as provided under the country's investment incentive regime. The specific rate and duration of the benefit are subject to the nature of the activity and the approval granted by the relevant authority overseeing investment promotion.

The country benefits from preferential trade arrangements with the EU as part of its status as an African, Caribbean and Pacific (ACP) state, which can affect the trading terms available to businesses operating through a locally registered entity. These arrangements govern goods trade rather than direct corporate tax relief, so the advantage is commercial rather than fiscal in nature.

A local director is not universally required for an Lda, but at least one manager must be formally appointed and their details registered with the commercial registry. Where the appointed manager is non-resident, practical compliance obligations around document execution and regulatory correspondence may necessitate appointing a local representative on a functional basis.

Failure to meet filing or renewal obligations can result in administrative penalties and, in more serious cases, the involuntary dissolution of the entity by the registry authority. Keeping the registered office active and filing any required annual returns or tax declarations with the Direcção dos Impostos is necessary to maintain the company in good standing.

The dobra (STN) is the official currency, but the economy operates with a high degree of dollarisation in practice, and the dobra maintains a peg to the euro through an agreement with Portugal. Repatriation of profits by foreign investors is generally permitted under the investment framework, though transactions are subject to applicable foreign exchange procedures administered through the banking system.

Upstream oil and gas activities are governed by separate sectoral legislation and require specific concession agreements with the national authority responsible for petroleum resources, meaning a standard Lda registration alone is insufficient to operate in that sector. Investors targeting oil-related activities must satisfy the licensing conditions set out under the applicable hydrocarbon laws before commencing operations.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.