Key Takeaways

- Suriname's corporate legal framework is rooted in Dutch civil law tradition, resulting in entity structures such as the Naamloze Vennootschap (NV) and Besloten Vennootschap (BV) that closely mirror their Dutch counterparts.

- All company registrations in Suriname are processed through the Chamber of Commerce and Industry (KKF), which maintains the commercial register and serves as the primary authority for new business filings.

- The NV is historically the most registered structure for substantive commercial activity in Suriname, making it the default choice for larger enterprises or those requiring external investment through share issuance.

- Foreign entities can establish a presence in Suriname without incorporating a separate legal entity by operating through a branch or representative office, each carrying different operational and compliance implications.

Introduction to Entity Types in Suriname

Suriname sits on the northeastern coast of South America, bordered by Guyana, Brazil, and French Guiana. It is an independent republic and a former Dutch colony, which explains why its corporate legal framework draws heavily from Dutch civil law traditions — a distinction that shapes the types of business entities in Suriname available to both residents and foreign investors.

Company registration falls under the authority of the Suriname Chamber of Commerce and Industry (KKF), which maintains the commercial register and processes new business filings. The tax system operates on a territorial basis, meaning income sourced outside the country may be treated differently from domestic earnings.

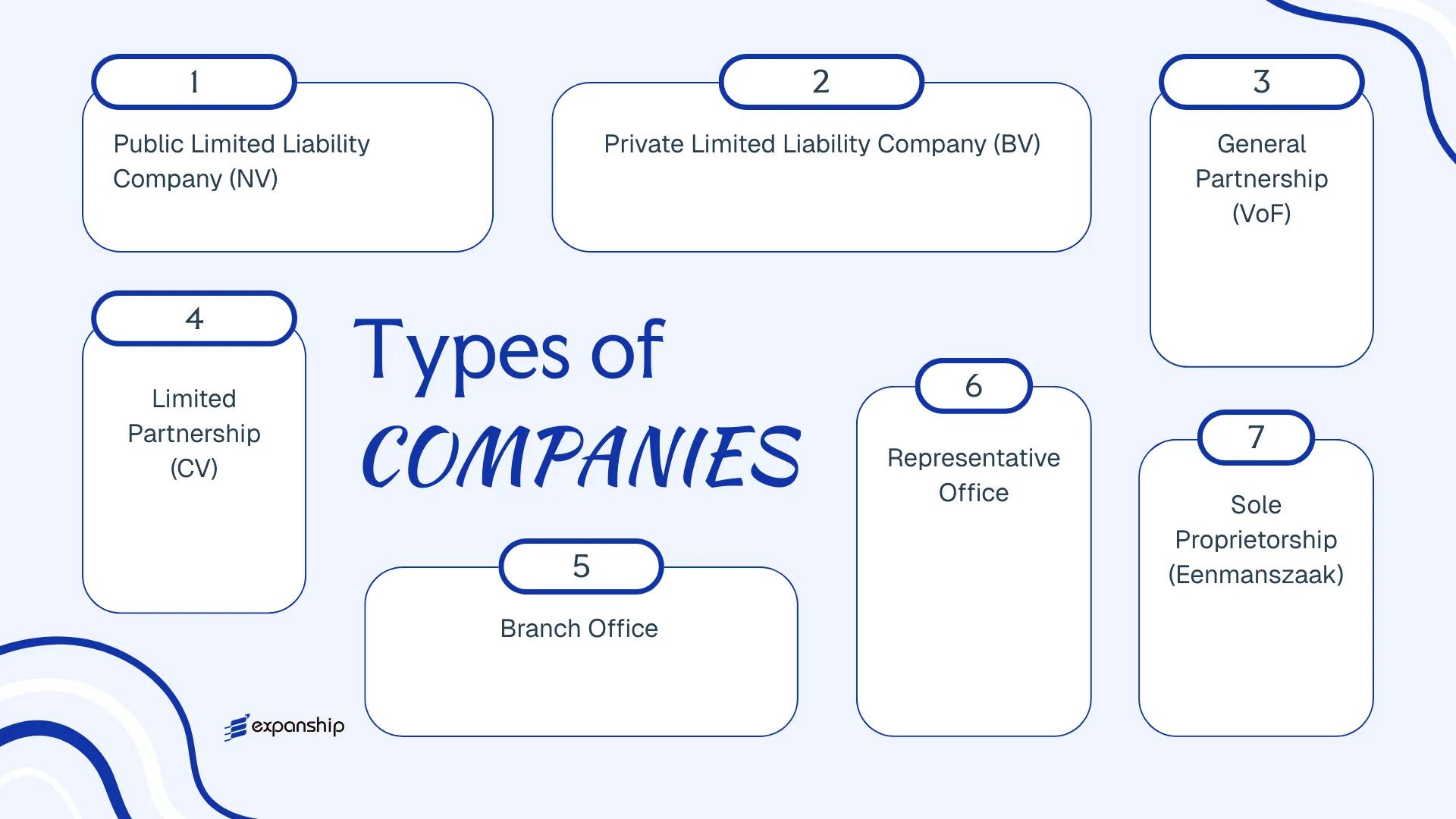

Several legal entity forms are recognized under Surinamese law. These include:

- Naamloze Vennootschap (NV)

- Besloten Vennootschap (BV)

- Vennootschap onder Firma (VoF)

- Commanditaire Vennootschap (CV)

- Branch Office

- Representative Office

- Eenmanszaak (Sole Proprietorship)

Each structure carries distinct implications for liability, governance, and tax treatment. This article examines each form in detail to help your business identify the most appropriate corporate structure for operating in or through Suriname.

An Overview of Business Structures in Suriname

Suriname's company law framework accommodates several distinct entity types, each governed primarily by the Wetboek van Koophandel (Commercial Code) and supplementary civil legislation. Depending on the scale, ownership structure, and commercial objectives of your business, the applicable legal form will differ significantly in terms of liability exposure, governance requirements, and tax treatment.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Tax Status | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Naamloze Vennootschap (NV) | Public limited company | Limited to share capital | Corporate tax applies | Permitted | 1 shareholder | Chamber of Commerce | Wetboek van Koophandel |

| Besloten Vennootschap (BV) | Private limited company | Limited to share capital | Corporate tax applies | Permitted | 1 shareholder | Chamber of Commerce | Wetboek van Koophandel |

| Vennootschap onder Firma (VoF) | General partnership | Unlimited, joint & several | Pass-through to partners | Permitted | 2 partners | Chamber of Commerce | Wetboek van Koophandel |

| Commanditaire Vennootschap (CV) | Limited partnership | Mixed: general/limited | Pass-through to partners | Permitted | 2 partners | Chamber of Commerce | Wetboek van Koophandel |

| Branch Office | Foreign establishment | Parent company liable | Corporate tax on local income | Permitted | N/A | Chamber of Commerce | Wetboek van Koophandel |

| Representative Office | Foreign establishment | Parent company liable | Generally non-trading | Restricted | N/A | Chamber of Commerce | Wetboek van Koophandel |

| Eenmanszaak | Sole proprietorship | Unlimited, personal | Personal income tax | Permitted | 1 owner | Chamber of Commerce | Wetboek van Koophandel |

Each of these structures is examined in full in the sections below.

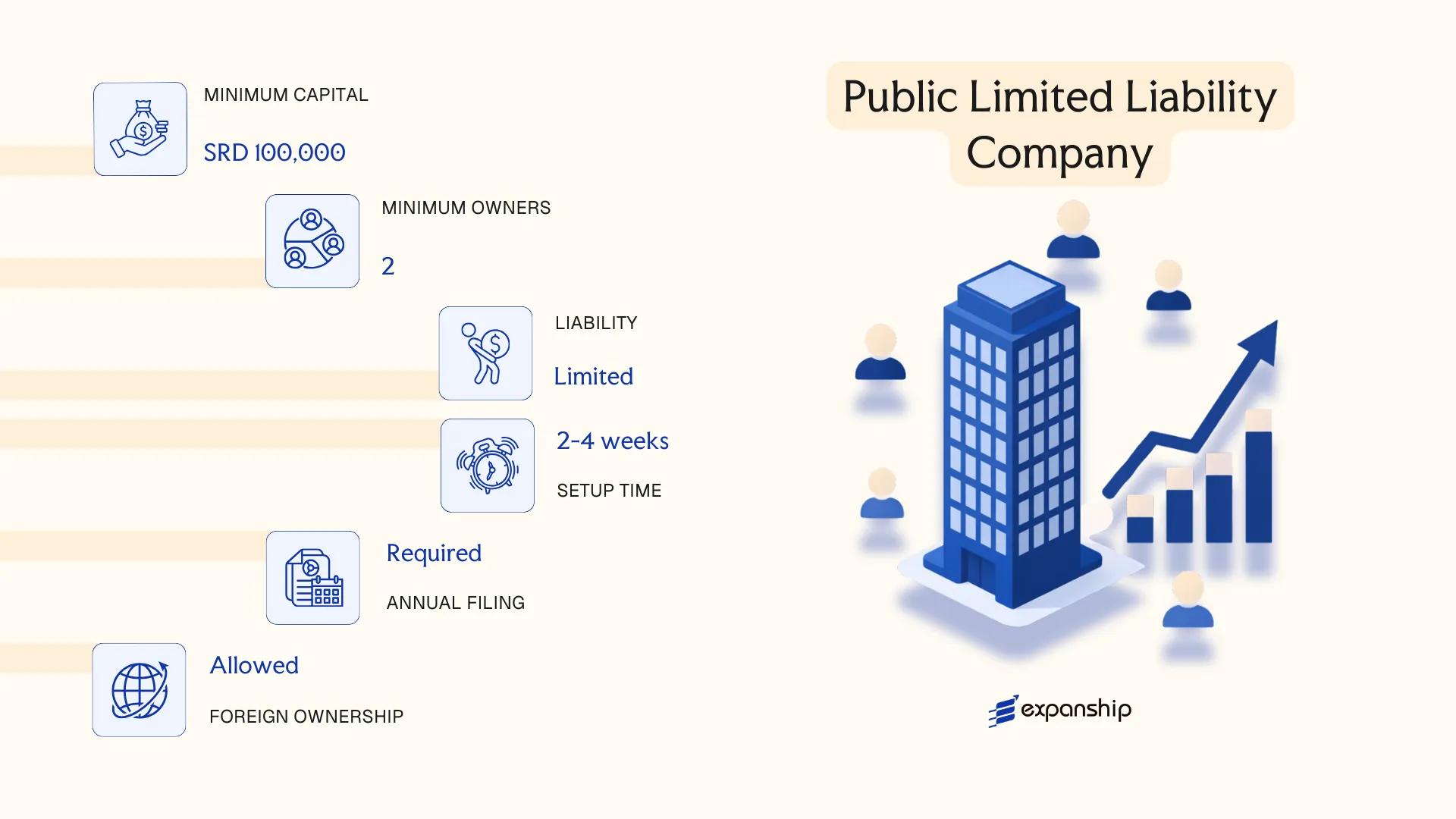

Naamloze Vennootschap (NV) — Public Limited Liability Company

The Naamloze Vennootschap Suriname NV is governed by the Wetboek van Koophandel (Commercial Code) of Suriname and represents the most structurally formal corporate entity available under local law. It carries separate legal personality, meaning the company itself holds rights and obligations distinct from those of its shareholders.

Liability is limited to each shareholder's capital contribution. The NV can issue shares to the public, which distinguishes it structurally from its private counterpart and makes it the preferred vehicle for larger commercial operations, joint ventures, and foreign investment structures.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Naamloze Vennootschap (NV) | Separate legal personality; limited liability |

| Governing Members | Shareholders (aandeelhouders); Board of Directors (Raad van Bestuur) | No statutory maximum on shareholders; minimum 1 director required |

| Minimum Members | 1 shareholder (natural or legal person) | No maximum shareholder cap |

| Local Presence | Registered office in Suriname required | A local registered address must be maintained; no mandatory resident director under general rules |

| Share Capital | Surinamese Dollar (SRD); no universally codified statutory minimum under current general practice | Capital must be stated in the deed of incorporation; shares may be in bearer or registered form |

| Privacy | Shareholder details filed with the Suriname Chamber of Commerce (KKF) | Beneficial ownership disclosure requirements apply under AML legislation |

Focus Points

- Taxation: Corporate income tax applies at a rate of 36% on net profits; VAT (OB) applies at 10%; dividend withholding tax is levied on distributions; stamp duties apply to certain instruments — consult the Suriname Tax Authority (Belastingdienst) for current rates.

- Annual Compliance: Annual financial statements must be filed; general meetings of shareholders are required by statute.

- Treaty Access: Suriname has a limited tax treaty network; NV entities may have restricted access to double tax agreement benefits depending on structure.

- Economic Substance: No formal OECD-style economic substance regime currently mandated, though AML and commercial presence requirements apply.

- Conversion: An NV may generally be converted to a BV through a formal notarial process, subject to shareholder approval and re-registration with the KKF.

Closing

The NV suits holding structures, large trading companies, and businesses anticipating external investment or eventual public participation. Its primary advantage is unrestricted share issuance; its principal drawback is the administrative burden of ongoing statutory compliance relative to simpler entity forms.

The NV is best suited for medium-to-large enterprises, joint ventures, and foreign investors seeking a formally recognised corporate structure with the capacity to raise capital through share issuance.

Company Incorporation in Suriname

Incorporate a Naamloze Vennootschap (NV) or other business entity in Suriname with end-to-end support from Expanship.

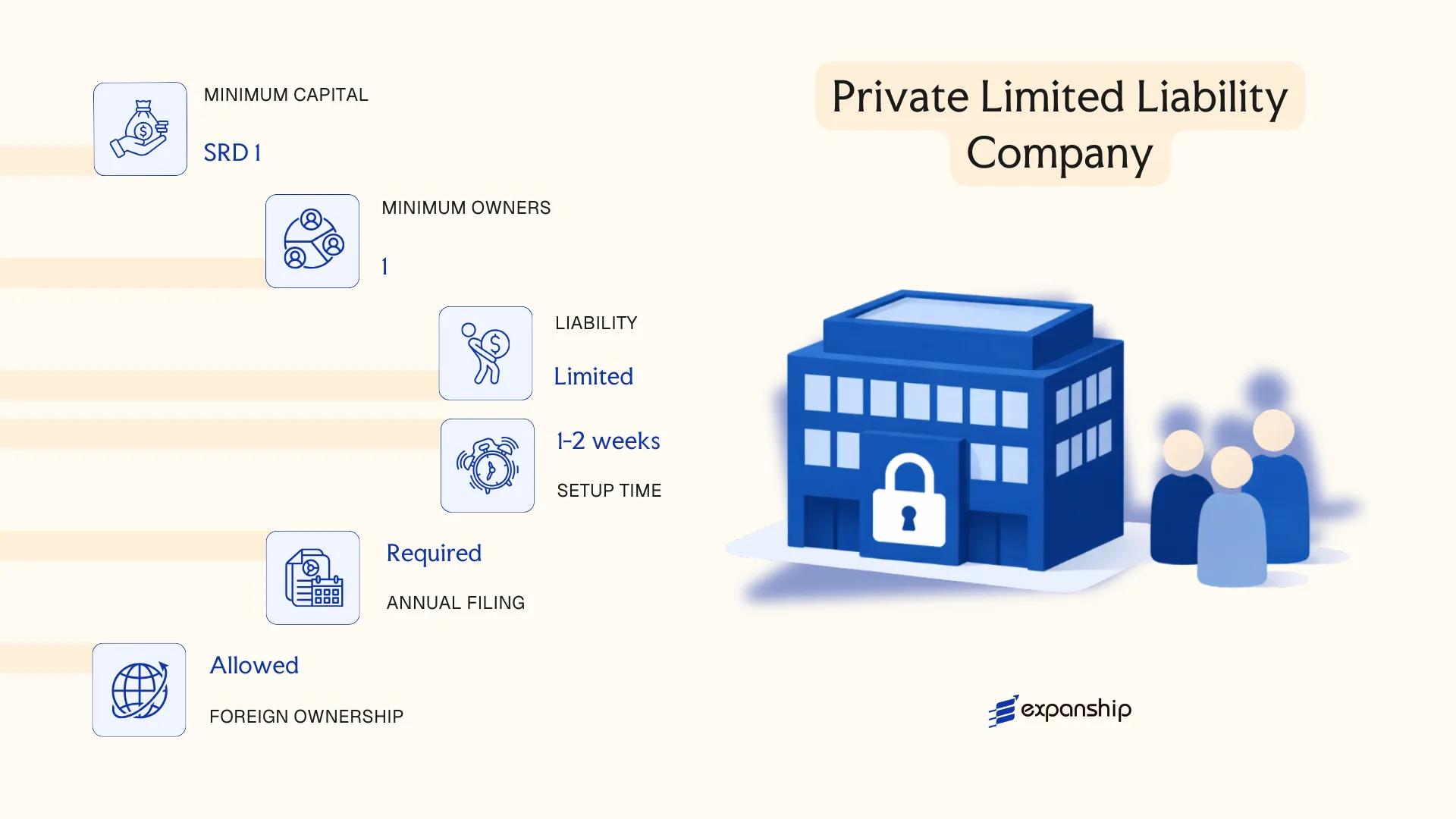

Besloten Vennootschap (BV) — Private Limited Liability Company

The Besloten Vennootschap Suriname BV is governed by the Surinamese Civil Code and related corporate legislation derived from the Dutch legal tradition. It carries separate legal personality, meaning the entity's obligations are distinct from those of its shareholders.

Shares in a BV are not freely transferable without restriction — transfer requires approval under the company's articles of association, distinguishing this structure from its publicly listed counterpart. This closed-share characteristic makes it a practical vehicle for closely held businesses and family-owned enterprises.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private limited liability company | Separate legal personality; shareholders not personally liable for company debts |

| Members | Shareholders (minimum 1, no maximum) | Directors (minimum 1); no distinction between local and foreign shareholders required |

| Local Presence | Registered office in Suriname required | A local registered address must be maintained |

| Capital | SRD (Surinamese Dollar); no statutory minimum prescribed under general practice | Capital is divided into shares; amount stated in articles of association |

| Share Transferability | Restricted; subject to approval clauses in articles | Shares cannot be offered to the general public |

| Privacy | Shareholder details filed with the Chamber of Commerce | Beneficial ownership disclosure obligations apply |

Focus Points

- Taxation: Subject to corporate income tax; standard rate applies to net profits; VAT obligations apply to taxable supplies; withholding tax may apply to dividend distributions to non-residents.

- Annual Compliance: Annual financial statements must be filed; failure to maintain records or meet filing deadlines can result in penalties from the Suriname Chamber of Commerce.

- Economic Substance: No formal substance regime equivalent to some offshore jurisdictions, but physical presence via registered office is required.

- Treaty Access: Suriname's limited tax treaty network may affect withholding tax positions for foreign shareholders.

- Conversion: A BV can generally be converted to an NV through a formal notarial process, subject to amended articles and regulatory notification.

Closing

A BV suits trading operations, holding structures, and family-owned businesses where shareholder control and share transfer restrictions are operationally desirable. The closed-share structure provides ownership stability, though it limits the entity's ability to raise capital from external investors.

Best suited for foreign investors and local entrepreneurs seeking a privately held operating or holding entity with defined ownership control and limited personal liability.

Partnerships in Suriname [Vennootschap onder Firma (VoF), Commanditaire Vennootschap (CV)]

Suriname VoF CV partnership registration is governed primarily by the Wetboek van Koophandel (Commercial Code), which draws heavily from Dutch colonial-era commercial legislation. Neither the Vennootschap onder Firma nor the Commanditaire Vennootschap carries separate legal personality under Surinamese law, meaning partners remain personally exposed to the firm's obligations.

Registration takes place through the Kamer van Koophandel en Fabrieken (Chamber of Commerce and Industry). Both structures require a partnership deed, typically executed before a notary, and must be registered in the commercial register to be operative against third parties.

Key Characteristics

| Requirement | VoF | CV |

|---|---|---|

| Legal Form | General partnership; no separate legal personality | Limited partnership; no separate legal personality |

| Partners | General partners (vennoten); minimum 2, no maximum | At least 1 general partner (beherende vennoot) + 1 limited partner (commanditaire vennoot); no maximum |

| Liability | All partners bear unlimited, joint and several liability | General partners: unlimited liability; limited partners: liable only up to capital contribution |

| Local Presence | Registered office address in Suriname required | Registered office address in Suriname required |

| Capital | No statutory minimum; contributions defined in partnership deed; SRD or foreign currency permissible | No statutory minimum; limited partner's contribution documented in deed |

| Privacy | Partnership deed is registered and publicly accessible via the commercial register | Same as VoF; limited partner identity disclosed in registration |

Focus Points

- Taxation: Partnerships are generally treated as fiscally transparent; partners are taxed individually on their share of profits under personal income tax rules, though professional advice should be sought on withholding obligations for non-resident partners.

- Annual Compliance: No statutory audit requirement for either structure; however, annual financial records must be maintained and any material changes to the partnership deed require notarial amendment and re-registration.

- Treaty Access: As fiscally transparent entities, VoF and CV structures may face limitations in accessing Suriname's tax treaty network, since treaty benefits typically accrue to the individual partners rather than the partnership itself.

- Conversion: Conversion from a VoF or CV into a capital company such as a BV is possible but requires a formal legal process involving notarial deed and new registration.

- Restrictions: Limited partners in a CV must not engage in management acts; doing so triggers unlimited personal liability equivalent to that of a general partner.

Sub-Types

Vennootschap onder Firma (VoF)

The VoF is the standard general partnership form in which all partners actively manage the business and each bears unlimited joint liability for the firm's debts. It is commonly used for small professional practices and family-owned trading businesses.

Commanditaire Vennootschap (CV)

The CV introduces a two-tier partner structure, separating active management from passive investment. Limited partners contribute capital and share in profits but are prohibited from management participation, making this form suitable for arrangements where investors seek profit participation without operational responsibility.

Recommendations

Both structures are suited to smaller domestic operations, joint ventures between known parties, or arrangements where one partner contributes capital while another manages. The primary advantage is structural simplicity with minimal formation cost; the significant limitation is the unlimited personal liability carried by general partners in both forms.

VoF and CV structures are most appropriate for small-to-medium domestic businesses or investor-operator arrangements where parties accept personal liability exposure and do not require the liability shield of a capital company.

Foreign Business Establishments in Suriname [Branch Office, Representative Office]

A foreign branch office Suriname setup operates under the Commercial Code of Suriname (Wetboek van Koophandel), which requires foreign entities to formally register before conducting business activities locally. Unlike an independently incorporated subsidiary, a branch has no separate legal personality — the parent company retains full liability for all obligations the branch incurs.

Registration is handled through the Chamber of Commerce and Industry (Kamer van Koophandel en Fabrieken), which maintains the Commercial Register. Your foreign entity must submit certified constitutional documents, proof of the parent company's legal existence, and details of the appointed local representative.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Branch Office or Representative Office | Branch may trade; Representative Office is restricted to non-commercial activities |

| Legal Personality | None | Parent company bears full liability |

| Local Representative | Required | Must be resident in Suriname with authority to act on behalf of the parent |

| Registered Office | Required | Physical address in Suriname mandatory for registration |

| Capital Requirement | None prescribed | Parent company's capital structure governs |

| Privacy | Parent company details disclosed | Constitutional documents filed in public Commercial Register |

Focus Points

- Taxation: Branch profits are subject to corporate income tax at the standard rate; VAT obligations apply to taxable supplies; withholding tax may apply on profit remittances to the parent.

- Economic Substance: No formal substance regime is codified for branches, but the local representative requirement provides a baseline operational presence.

- Annual Compliance: Annual filing with the Chamber of Commerce required; financial statements of the branch must be maintained locally.

- Treaty Access: Access to Suriname's limited tax treaty network depends on the parent entity's jurisdiction of incorporation, not the branch itself.

- Restrictions: A representative office cannot generate revenue or enter commercial contracts on its own account.

Sub-Types

Branch Office

A branch office is an extension of the foreign parent and may engage in full commercial and trading activities, entering contracts and generating revenue directly.

Representative Office

A representative office is limited to promotional, liaison, and market research activities. It cannot sign commercial contracts or invoice clients, making it suitable for market entry assessment rather than active operations.

Closing Remarks

Foreign firms already operating in multiple markets often use a branch for trading activity, given lower setup complexity compared to incorporating a new local entity, though the absence of liability separation is a meaningful commercial exposure. A representative office suits pre-commercial phases where your firm is assessing market conditions before committing to full establishment.

Foreign companies testing the Surinamese market or maintaining a controlled operational presence without incorporating a standalone local entity.

Sole Proprietorship (Eenmanszaak)

The Eenmanszaak is the simplest business form available in Suriname, governed by the general civil and commercial code provisions applicable to sole traders rather than a dedicated corporations statute. Registration is handled through the Kamer van Koophandel en Fabrieken (Chamber of Commerce and Industry).

Unlike capital companies, the Eenmanszaak carries no separate legal personality. The proprietor and the business are legally indistinguishable, meaning personal assets are fully exposed to business liabilities.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sole Proprietorship (Eenmanszaak) | No separate legal personality |

| Member Type | Sole Proprietor | One individual only; no co-owners permitted |

| Local Presence | Registered business address in Suriname | Required for Chamber of Commerce registration |

| Capital | No minimum capital requirement | Capital is entirely the proprietor's personal funds |

| Liability | Unlimited personal liability | Personal assets fully at risk |

| Privacy | Proprietor's name on public record | No nominee arrangements available |

Focus Points

- Taxation: Subject to personal income tax under the Surinaamse belastingwetgeving; no separate corporate income tax applies, though turnover-based obligations and VAT registration may be required above threshold.

- Annual Compliance: Annual renewal of Chamber of Commerce registration required; bookkeeping obligations apply.

- Treaty Access: No access to corporate tax treaty benefits, as income flows directly to the individual.

- Conversion: Can be converted into a BV, though the process requires a formal incorporation procedure.

- Restrictions: Foreign nationals face limitations on sole trader registration tied to residency and work permit requirements.

Closing

The Eenmanszaak suits local freelancers, consultants, and small-scale traders operating without partners who want minimal administrative overhead. The primary advantage is simplicity of setup; the defining drawback is unlimited personal liability with no structural protection.

Local Surinamese residents or eligible individuals running low-risk, owner-operated businesses who do not require liability separation.

How to Choose the Right Entity Type in Suriname

Choosing the right company type in Suriname is not a procedural formality — the structure you register determines your tax exposure, liability, reporting obligations, and operational capacity from day one.

Why Your Entity Choice Matters

Selecting the wrong structure produces concrete, often costly outcomes:

- A foreign firm that registers a representative office but conducts active local sales is operating outside the scope permitted under Surinamese commercial law, which can result in forced dissolution or administrative penalties.

- Opting for a structure that falls outside Suriname's tax treaty coverage means your foreign counterparts cannot apply reduced withholding rates on dividends or royalties paid to you.

- Forming an NV or BV when your purpose is asset protection or succession planning locks your structure into annual shareholder meeting requirements and capital maintenance rules that a foundation arrangement would not impose.

- Choosing an entity that mandates audited financial statements for a single-director consultancy creates recurring compliance costs that have no operational benefit.

Key Factors to Consider

- Business Activity: Active trading, passive asset holding, and regulated sectors such as banking or insurance each require a distinct legal structure under Surinamese law.

- Ownership Configuration: A sole operator has little reason to maintain a full NV board structure; multi-party arrangements may need the formal governance an NV provides.

- Tax Position: Your need for treaty access, full exemption, or a standard corporate rate directly narrows which entity qualifies.

- Substance Capacity: If you cannot maintain a physical presence or local decision-making, select a structure with lower or no substance thresholds.

- Disclosure Tolerance: The public commercial register administered by the Surinamese Chamber of Commerce (KKF) records director and shareholder details for most entities; nominee arrangements may be required if confidentiality is a priority.

- Exit Flexibility: Not all Surinamese entities permit conversion or redomiciliation — confirm whether your chosen structure supports your anticipated exit route before registration.

For the governing text on company formation, refer to the Wetboek van Koophandel as published through the official Surinamese government gazette.

Corporate Compliance Services in Suriname

Ongoing compliance support for companies registered in Suriname, including annual filings, registered agent services, and regulatory reporting.

Conclusion

Suriname's legal framework offers five principal structures for business registration, each suited to a different operational profile. The NV accommodates larger enterprises or those seeking external investment through share issuance. A BV suits closely held businesses where ownership control is a priority. Partnerships — the VoF and CV — fit smaller ventures or professional arrangements where formal incorporation is not required. Branch and representative offices serve foreign entities testing or maintaining a market presence without establishing a separate legal entity. The Eenmanszaak remains the simplest form, used exclusively by individual operators.

Among these, the NV is historically the most registered structure for substantive commercial activity in Suriname. For those incorporating a company in Suriname guide considerations matter: the Chamber of Commerce and the relevant civil law notary requirements shape timelines and costs significantly. Ongoing treaty negotiations and gradual regulatory modernization suggest the jurisdiction's compliance standards will continue to align more closely with international norms over the coming years. Expanship's team works directly within this framework.

How Expanship Can Assist You

Expanship's Suriname company formation services cover the full registration process for each entity type discussed in this guide — from the Naamloze Vennootschap and Besloten Vennootschap through to branch offices and sole proprietorships. Every structure requires engagement with the Suriname Chamber of Commerce and Industry (KKF), and our team manages that liaison directly on your behalf.

From initial document preparation through to post-incorporation obligations, your business has a single point of contact throughout:

- Document preparation, notarization, and legalization

- Registered agent and registered office provision

- KKF filing and government authority coordination

- Post-incorporation compliance management

- Banking introduction assistance

Reach out to Expanship Suriname to discuss which structure fits your operational goals.

Suriname Company Formation

Register your business entity in Suriname with full KKF liaison and compliance support.

Frequently Asked Questions (FAQ)

The Naamloze Vennootschap (NV) has historically been the most widely registered entity, largely because it accommodates both private and publicly oriented structures under the Commercial Code. Its flexible share transfer rules and established legal framework make it the default choice for medium-to-large enterprises.

The NV issues shares that can, in principle, be transferred freely, while the BV restricts share transferability to pre-approved parties, giving shareholders greater control over ownership composition. Both entities are subject to corporate income tax under Surinamese tax law, and both may trade locally. The BV generally carries lighter administrative requirements than the NV.

The BV offers comparatively greater ownership privacy, as shareholder details are not routinely exposed through public filings in the same manner as an NV with publicly listed shares. Nominee arrangements are legally permissible, though ultimate beneficial ownership remains subject to regulatory disclosure requirements. Bearer shares are not a feature of either structure.

A sole proprietorship (Eenmanszaak) is by definition a one-person structure. Both the NV and BV can technically be formed with a single shareholder, though director minimums apply. Partnerships, whether a Vennootschap onder Firma (VoF) or a Commanditaire Vennootschap (CV), require at least two parties by their legal nature.

Foreign nationals may establish an NV or BV without a residency requirement, though certain regulated sectors impose local participation conditions. A branch office of a foreign firm is also available, registered through the Trade Register at the Suriname Chamber of Commerce and Industry. Foreign investors should verify whether their intended business activity falls under any sector-specific licensing regime.

Surinamese corporate law permits restructuring between entity forms, most commonly from a sole proprietorship or partnership into an NV or BV as a business scales. The process involves notarial deed execution and re-registration with the Chamber of Commerce. Conversion between an NV and BV is generally achievable through a formal amendment to the articles of association.

The NV, BV, and branch office (as an extension of its parent) each carry distinct legal standing, but in different ways. A VoF does not have full separate legal personality under Surinamese law, meaning partners retain personal liability for firm obligations. The CV provides limited liability only to silent partners, not to managing general partners.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.