Key Takeaways

- Slovakia's Commercial Code (Obchodný zákonník) governs the full range of business entities, with the Slovak Business Register (Obchodný register) administered by district courts serving as the central public record for all legal entities.

- The s.r.o. (Spoločnosť s ručením obmedzeným) is the most frequently registered entity in Slovakia, accounting for the majority of new business formations each year.

- Founders requiring equity flexibility without the capital requirements of a full joint stock company (a.s.) can use the Jednoduchá spoločnosť na akcie (j.s.a.) as an intermediate structure.

- Foreign companies can establish a branch or representative office to test the Slovak market before committing to local incorporation under the Commercial Code.

Introduction to Entity Types in Slovakia

Slovakia is a landlocked Central European country bordered by Austria, the Czech Republic, Hungary, Poland, and Ukraine. It is an independent republic and a member of the European Union, which means its corporate law operates within an EU regulatory framework while retaining its own national legislation — primarily the Commercial Code (Obchodný zákonník).

Company registration falls under the jurisdiction of the Slovak Business Register (*Obchodný register*), administered by the district courts. The register maintains public records for all legal entities operating in the country.

From a tax standpoint, Slovakia applies a standard territorial-based corporate tax system with applicable EU directives governing cross-border transactions.

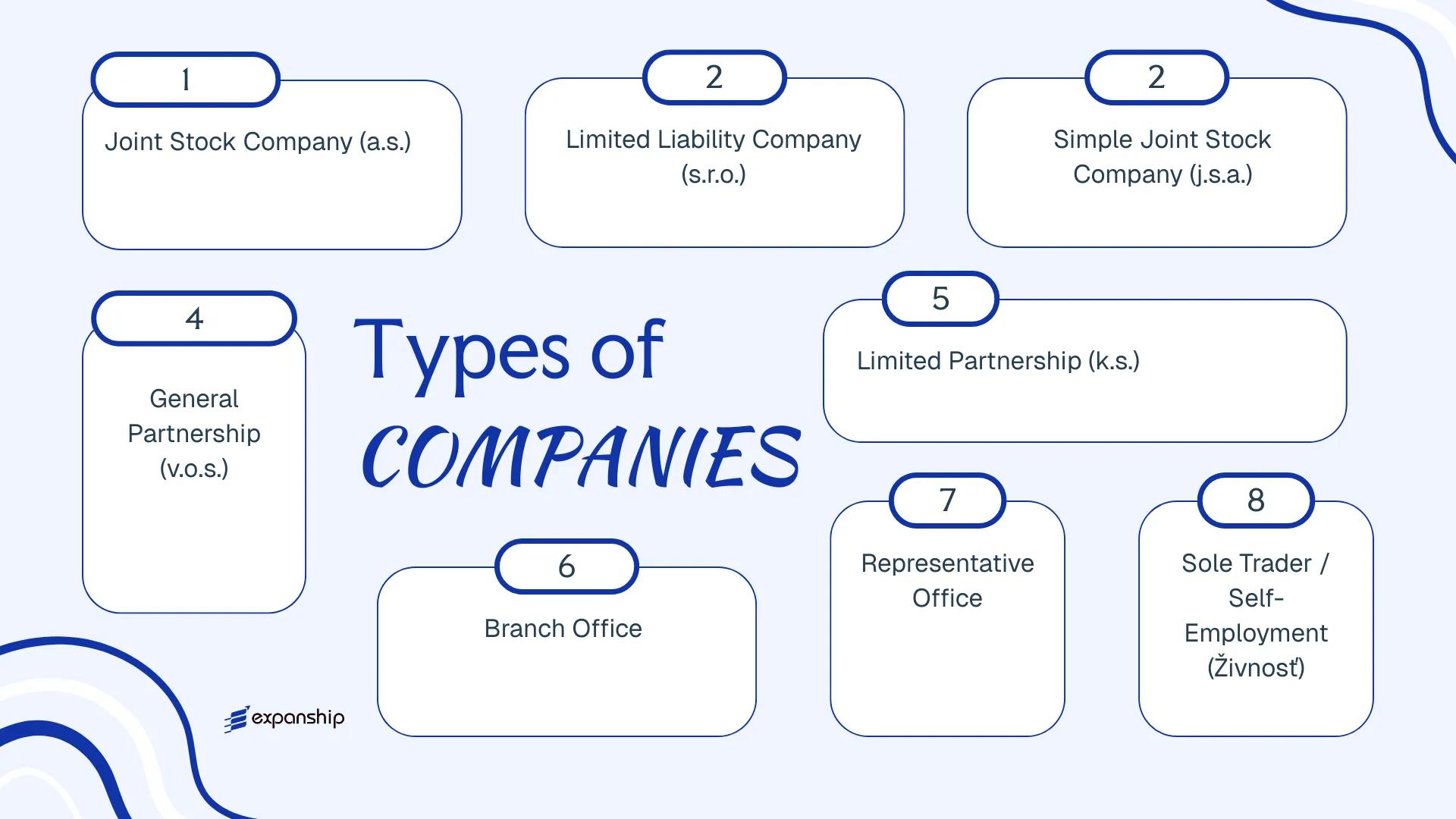

Businesses establishing a presence here can choose from several legal entity forms:

- Spoločnosť s ručením obmedzeným (s.r.o.)

- Akciová spoločnosť (a.s.)

- Jednoduchá spoločnosť na akcie (j.s.a.)

- Verejná obchodná spoločnosť (v.o.s.)

- Komanditná spoločnosť (k.s.)

- Branch Office

- Representative Office

- Živnosť (sole trader)

Each of these types of business entities in Slovakia carries distinct liability structures, capital requirements, and compliance obligations, all of which this article examines in detail.

An Overview of Business Structures in Slovakia

Slovak company law recognises six principal corporate forms, each governed primarily by the Obchodný zákonník (Commercial Code, Act No. 513/1991 Coll.) and its amendments. The overview of business structures in Slovakia reflects a framework designed to accommodate domestic traders, private investors, capital-market participants, and foreign operators under distinct legal arrangements. Each form carries different rules on liability, capital, and governance, which the sections below address individually.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Akciová spoločnosť (a.s.) | Joint Stock Company | Limited to share capital | Taxed | Yes | 1 founder | Slovak Trade Register | Commercial Code |

| Spoločnosť s ručením obmedzeným (s.r.o.) | Limited Liability Company | Limited to contribution | Taxed | Yes | 1 member | Slovak Trade Register | Commercial Code |

| Jednoduchá spoločnosť na akcie (j.s.a.) | Simple Joint Stock Company | Limited to share capital | Taxed | Yes | 1 founder | Slovak Trade Register | Commercial Code |

| Verejná obchodná spoločnosť (v.o.s.) | General Partnership | Unlimited, joint | Taxed | Yes | 2 partners | Slovak Trade Register | Commercial Code |

| Komanditná spoločnosť (k.s.) | Limited Partnership | Mixed liability | Taxed | Yes | 2 partners | Slovak Trade Register | Commercial Code |

| Organizačná zložka (Branch) | Branch Office | Parent bears liability | Taxed on local income | Yes | 1 parent entity | Slovak Trade Register | Commercial Code |

| Representative Office | Non-trading presence | Parent bears liability | Generally exempt | No | 1 parent entity | Slovak Trade Register | Commercial Code |

| Živnosť | Sole Trader | Unlimited personal | Taxed | Yes | 1 individual | Trade Licensing Office | Trade Licensing Act |

Each of these structures is examined in full in the sections below.

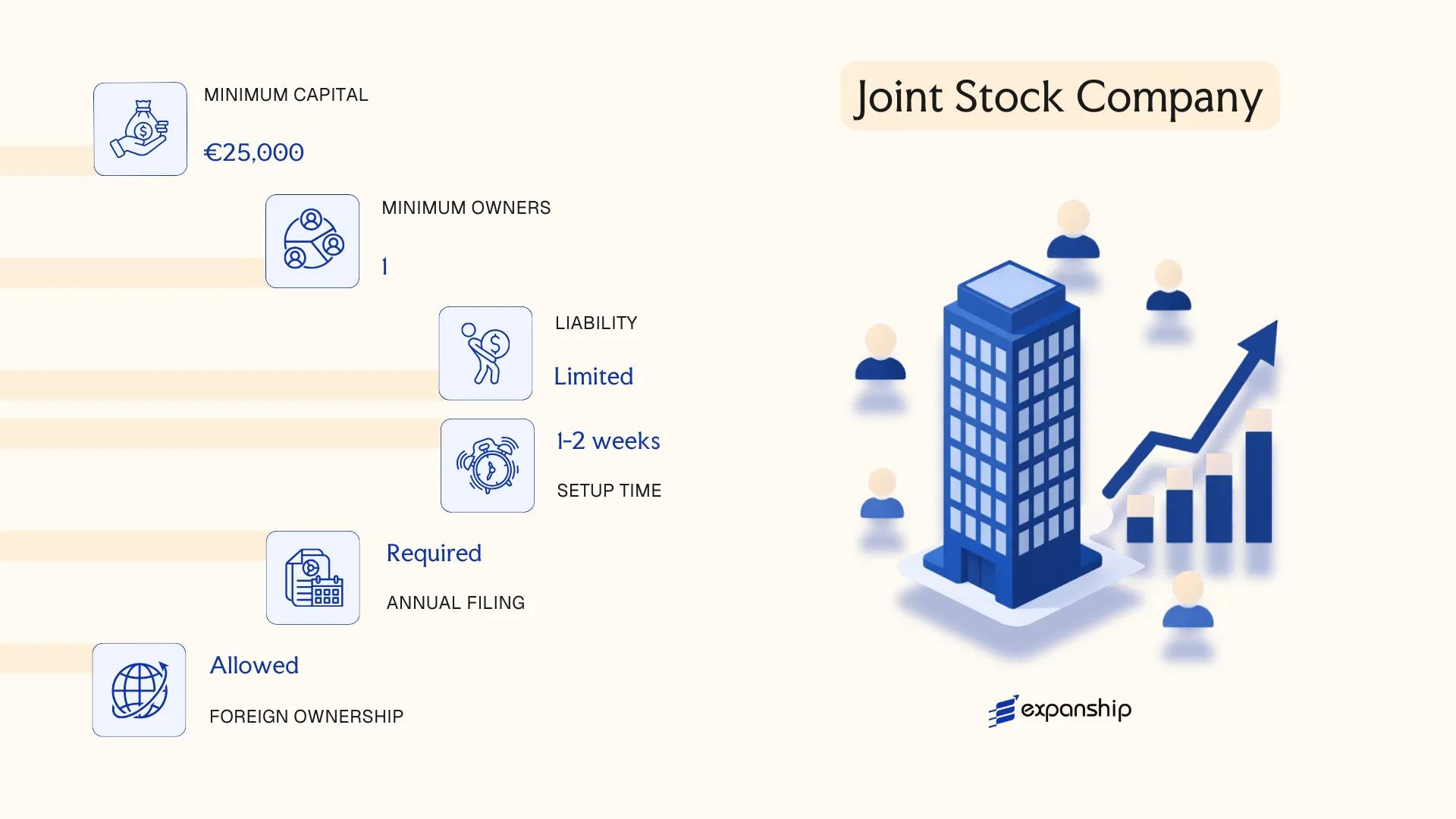

Akciová Spoločnosť (a.s.) – Joint Stock Company

Governed by the Slovak Commercial Code (Act No. 513/1991 Coll.), the akciová spoločnosť a.s. formation Slovakia follows a well-established statutory framework that has remained the primary vehicle for large-scale corporate activity. The entity carries full separate legal personality, meaning its obligations are entirely distinct from those of its shareholders.

Liability is capped at the value of subscribed shares. This structure suits firms seeking to raise capital from a broad investor base or planning a future public listing, given its capacity to issue transferable shares across multiple classes.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Joint Stock Company (a.s.) | Governed by Act No. 513/1991 Coll. |

| Members | Shareholders: min. 1 (legal entity) or min. 2 (natural persons); no maximum | Board of Directors (min. 3 members) and Supervisory Board (min. 3 members) required under two-tier governance |

| Share Capital | Min. EUR 25,000; must be fully subscribed at incorporation | Shares may be registered or bearer (bearer shares now significantly restricted) |

| Local Presence | Registered office address in Slovakia required | No mandatory local director requirement under current law |

| Privacy | Shareholders disclosed in the Commercial Register | Register is publicly accessible |

| Governance Model | Two-tier: Board of Directors + Supervisory Board | Single-tier model permitted if adopted in articles of association |

Focus Points

- Taxation: Corporate income tax applies at 15% (micro-entities) or 21% on profits; standard VAT rate is 23%; dividends paid to non-residents may attract 7% withholding tax, subject to applicable double tax treaties.

- Annual Compliance: Mandatory annual financial statements filed with the Commercial Register; statutory audit required if the entity meets two of three size thresholds (turnover, assets, employees).

- Treaty Access: Slovakia's tax treaty network (70+ agreements) is accessible to resident a.s. entities, subject to beneficial ownership conditions.

- Conversion: An a.s. may be converted into an s.r.o. or j.s.a. through a formal transformation procedure under the Commercial Code.

- Share Transferability: Share transfers in a non-listed a.s. may be restricted by the articles of association but cannot be prohibited outright.

Closing

The a.s. suits holding structures, capital-intensive operations, and businesses with multiple institutional investors. Its primary advantage is unrestricted share transferability and the capacity for public offerings; its principal drawback is the administrative burden of dual-board governance and mandatory audit obligations.

Best suited for large enterprises, institutional joint ventures, or businesses planning a public listing on the Bratislava Stock Exchange or a foreign exchange.

Company Incorporation in Slovakia

Incorporate an Akciová Spoločnosť or any other business entity in Slovakia with end-to-end support from Expanship.

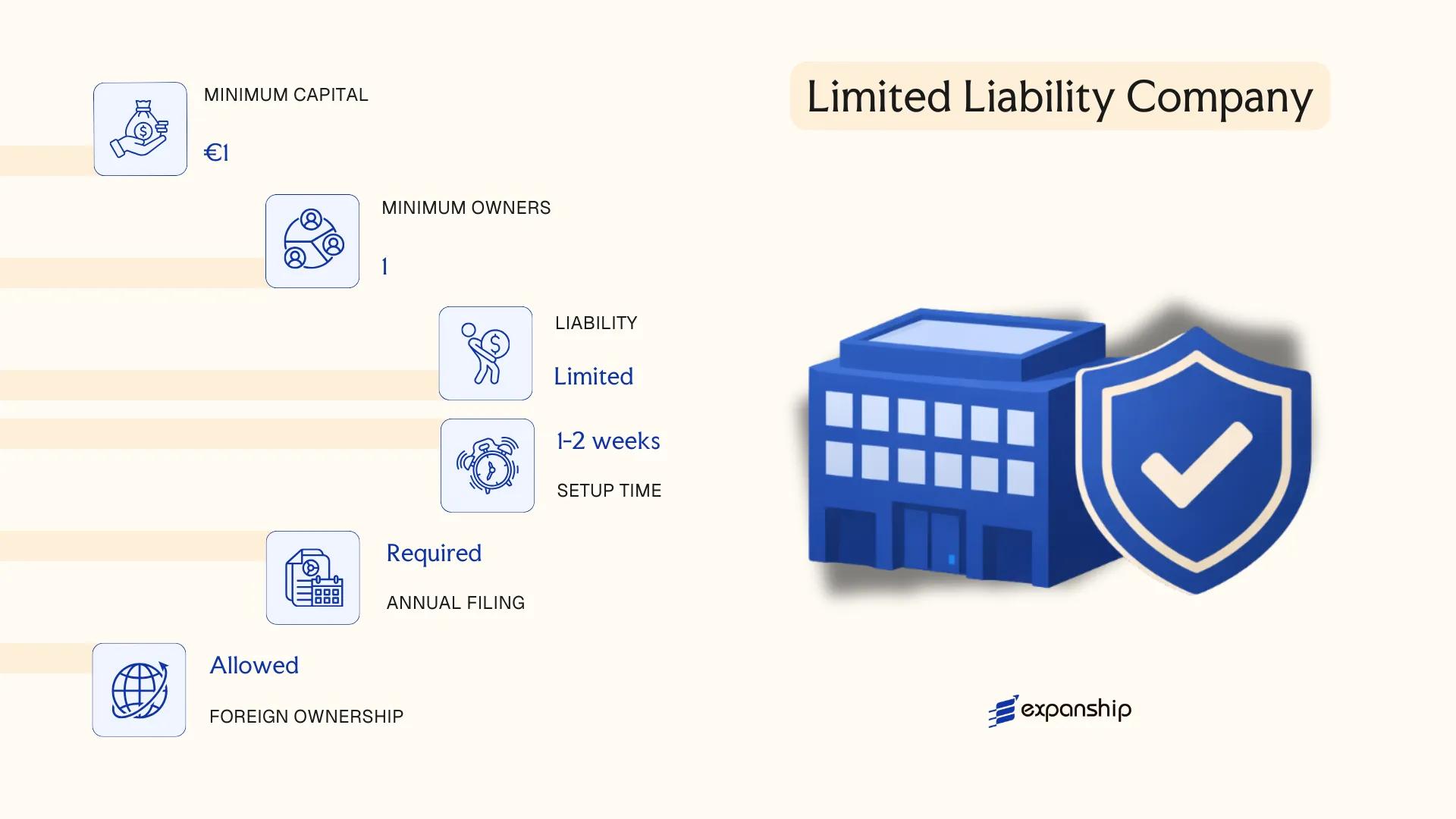

Spoločnosť s Ručením Obmedzeným (s.r.o.) – Limited Liability Company

The spoločnosť s ručením obmedzeným s.r.o. Slovakia is governed primarily by the Commercial Code (Act No. 513/1991 Coll.), which establishes it as a separate legal entity distinct from its members. Liability is capped at each member's unpaid contribution to the registered capital.

Structurally, the s.r.o. sits between a sole trader and a joint stock company — it carries corporate legal personality while retaining a relatively simple internal governance framework. This makes it the most widely registered business form in the country.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Limited Liability Company (s.r.o.) | Separate legal personality; governed by Act No. 513/1991 Coll. |

| Members | 1–50 shareholders | Shareholders hold business shares (obchodný podiel); a single-member s.r.o. is permitted |

| Management | Minimum 1 konatelia (executive director) | Directors need not be Slovak residents; no supervisory board required unless stipulated in the articles |

| Local Presence | Registered address in Slovakia required | A physical or virtual registered office address must be maintained |

| Share Capital | Minimum EUR 5,000; minimum per-member contribution EUR 750 | Contributions may be monetary or in-kind; must be recorded in the Commercial Register |

| Privacy | Shareholder and director details are publicly available | Filed with the Obchodný register (Commercial Register) administered by the Ministry of Justice |

Focus Points

- Taxation: Subject to 21% corporate income tax; standard VAT rate of 20% applies upon registration threshold; dividends paid to non-residents attract a 7% withholding tax; no stamp duty on share transfers.

- Annual Compliance: Financial statements must be filed with the Financial Administration of the Slovak Republic; annual tax returns are required; larger entities may trigger statutory audit obligations.

- Economic Substance: No statutory economic substance regime, though genuine business activity is expected for treaty access and transfer pricing purposes.

- Treaty Access: Slovakia's tax treaty network covers 70+ jurisdictions, and an s.r.o. qualifies as a resident entity for treaty benefits under standard conditions.

- Conversion: An s.r.o. may be converted into an a.s. or j.s.a. under the Commercial Code transformation procedures.

Closing Paragraph

The s.r.o. suits trading operations, holding structures, and professional services businesses where limited liability is required without the administrative burden of a joint stock company. Its principal limitation is the 50-shareholder cap, which restricts equity raises at scale.

Small to mid-sized businesses, foreign investors establishing a local operating subsidiary, and entrepreneurs seeking a straightforward liability shield with minimal governance requirements.

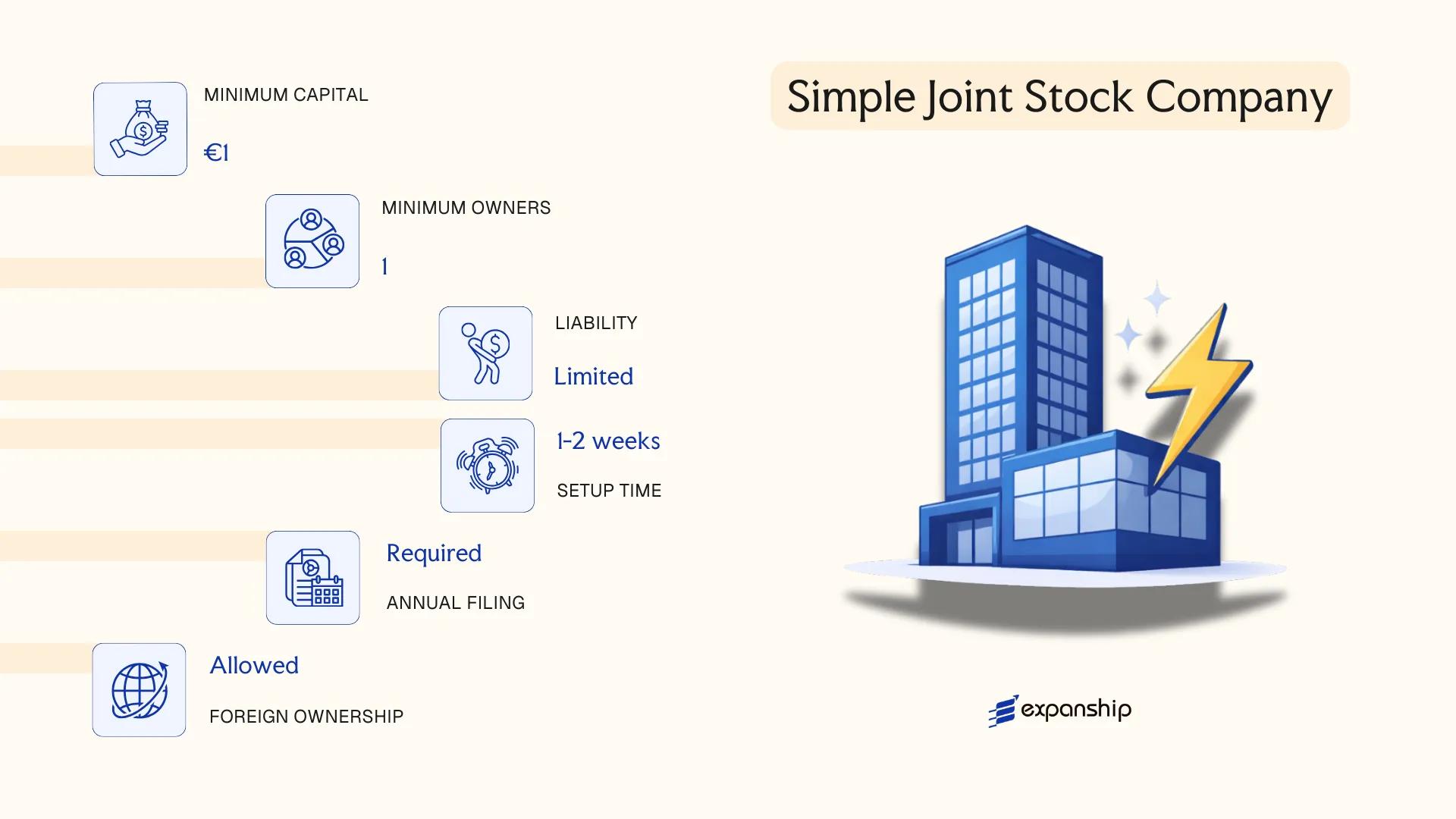

Jednoduchá Spoločnosť na Akcie (j.s.a.) – Simple Joint Stock Company

Introduced under Act No. 513/1991 Coll. (the Commercial Code) through an amendment effective 1 January 2017, the jednoduchá spoločnosť na akcie j.s.a. Slovakia was created specifically to address the structural needs of early-stage and venture-backed businesses. It carries separate legal personality and offers shareholders limited liability capped at their share of unpaid capital.

The j.s.a. is a hybrid form sitting between the s.r.o. and the a.s. It borrows equity flexibility from the joint stock model while retaining governance features suited to smaller, growth-oriented firms. Shares can be issued at a nominal value of as little as €0.01, enabling employee equity schemes and investor participation structures that the s.r.o. cannot accommodate.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Slovak simple joint stock company j.s.a. | Governed by the Commercial Code, as amended in 2017 |

| Members | Shareholders (min. 1, max. unlimited) | Single-shareholder structure is permitted |

| Management | Board of Directors (min. 1 member) + optional Supervisory Board | Supervisory Board is not mandatory, unlike in the a.s. |

| Local Presence | Registered office address in Slovakia required | No statutory requirement for a resident director |

| Share Capital | Min. €1; shares from €0.01 nominal value | Enables flexible equity distribution for founders and investors |

| Privacy | Shareholder register is not fully public | Beneficial ownership data filed with the Register of Public Sector Partners where applicable |

Focus Points

- Taxation: Subject to standard Slovak corporate income tax at 21% (15% for entities with taxable income up to €100,000); VAT registration required once turnover exceeds €49,790; dividends distributed to non-residents may attract withholding tax subject to applicable double tax treaties.

- Annual compliance: Mandatory filing of financial statements with the Commercial Register; obligation to convene a General Meeting at least once per financial year.

- Conversion: The j.s.a. may be converted into an a.s. or s.r.o. under the Commercial Code transformation provisions, subject to creditor protection requirements.

- Restrictions: Cannot be used as a banking, insurance, or investment fund vehicle without sector-specific licensing.

- Economic substance: No statutory minimum substance requirements beyond a registered office, though tax residency rules under Slovak law and relevant tax treaties may impose additional conditions.

Closing Paragraph

The startup company structure Slovakia j.s.a. suits venture-backed companies, technology firms, and businesses requiring employee share option plans, given its low minimum capital and flexible share structure. Its principal limitation is administrative: compliance obligations are more involved than those of the s.r.o., which may be disproportionate for very small operations.

The j.s.a. is best suited for growth-stage startups and investor-backed businesses that require a scalable equity structure without the full administrative weight of a joint stock company.

Partnerships in Slovakia [Verejná Obchodná Spoločnosť (v.o.s.) – General Partnership, Komanditná Spoločnosť (k.s.) – Limited Partnership]

Both partnership forms available under Slovak law are governed by the Commercial Code (Zákon č. 513/1991 Zb., Obchodný zákonník). A verejná obchodná spoločnosť v.o.s. Slovakia practitioners recognise as a general partnership carries separate legal personality but imposes unlimited joint and several liability on all partners. The komanditná spoločnosť (k.s.) is a hybrid structure, combining at least one general partner bearing unlimited liability with at least one limited partner whose exposure is capped at their agreed contribution.

Registration of both forms is administered through the Commercial Register maintained by the district courts, with the filing submitted electronically via the Business Register portal.

Key Characteristics

| Requirement | v.o.s. (General Partnership) | k.s. (Limited Partnership) |

|---|---|---|

| Legal Form | Commercial partnership with full legal personality | Hybrid partnership with full legal personality |

| Partners | Minimum 2 general partners; no statutory maximum | Minimum 1 general partner + 1 limited partner |

| Liability | All partners: unlimited and joint | General partner: unlimited; limited partner: capped at contribution |

| Minimum Capital | No statutory minimum | No statutory minimum for general partner; limited partner's contribution set in founding deed |

| Local Presence | Registered seat in Slovakia required | Registered seat in Slovakia required |

| Management | All general partners, unless deed restricts | General partners manage; limited partners excluded from management |

Focus Points

- Taxation: Both partnerships are fiscally transparent at entity level; profits are allocated to partners and taxed at their applicable personal or corporate income tax rates, with VAT registration required once turnover exceeds the statutory threshold.

- Annual Compliance: Both entities must file annual financial statements with the Commercial Register and maintain proper accounting records under Act No. 431/2002 Coll. on Accounting.

- Treaty Access: As Slovak-registered entities with legal personality, both forms can in principle access Slovakia's tax treaty network, though treaty benefits depend on each partner's residency status.

- Conversion: A v.o.s. may be converted into a k.s. or a capital company (s.r.o. or a.s.) through a statutory transformation procedure under the Commercial Code.

- Restrictions: Neither form is permitted to issue transferable securities; ownership transfer requires amendment of the founding deed and partner consent.

General and limited partnerships are used primarily by professional service providers, family businesses, and joint venture arrangements where operational control and pass-through taxation are priorities. The absence of a minimum capital requirement lowers the formation barrier, but unlimited liability exposure for general partners is a material structural risk that limits broader commercial adoption.

These structures suit small professional partnerships or closely held family ventures where partners accept personal liability in exchange for simplified governance and pass-through tax treatment.

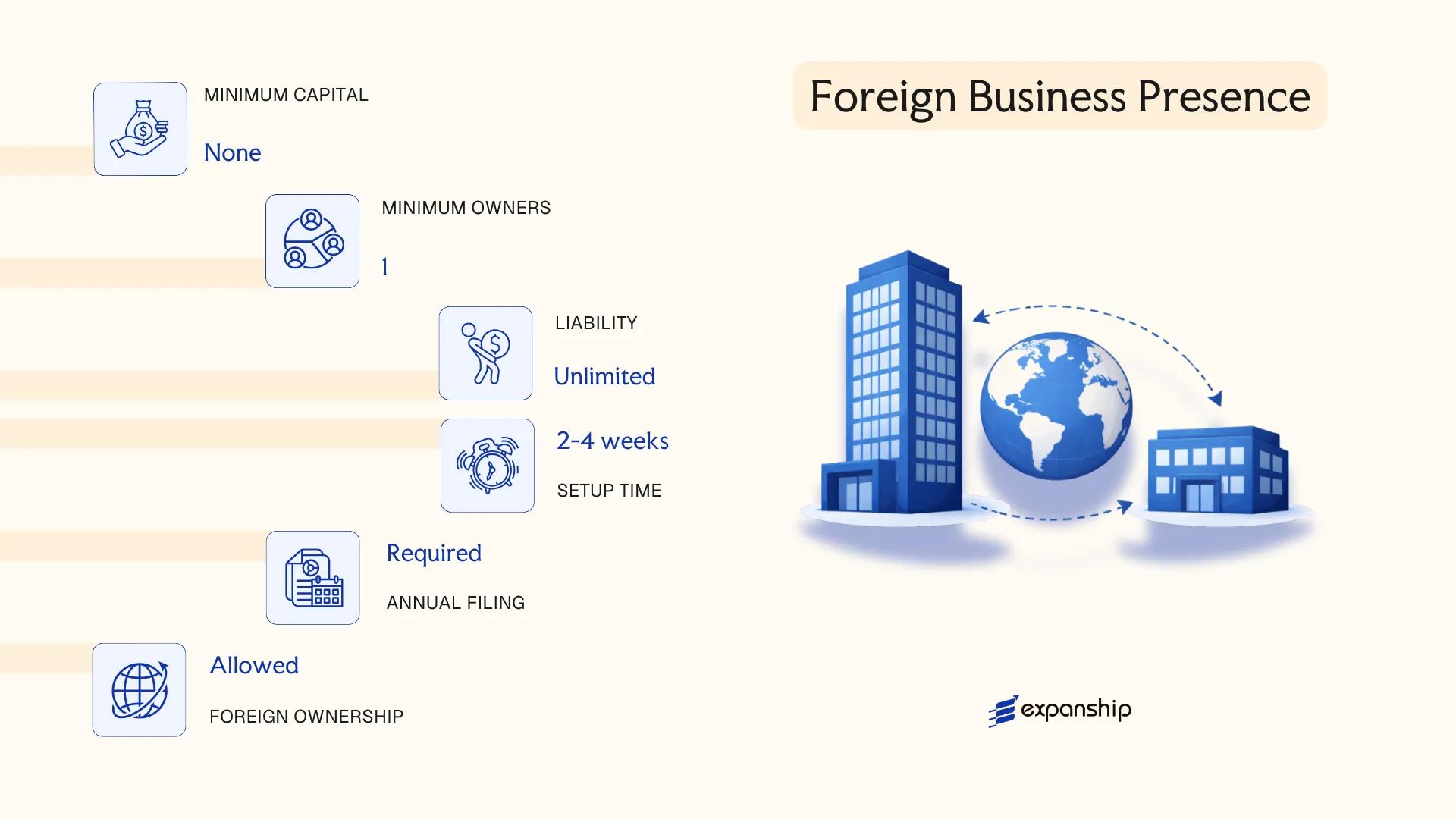

Foreign Business Presence in Slovakia [Branch Office, Representative Office]

Registering a foreign company branch office Slovakia is governed primarily by the Commercial Code (Act No. 513/1991 Coll.), which requires foreign entities to register their branch or representative office in the Slovak Commercial Register before commencing operations. Neither structure constitutes a separate legal entity — both remain an extension of the parent company, which retains full legal and financial liability for their activities.

The distinction between the two structures is operational. A branch office may conduct commercial activities on behalf of the parent. A representative office is restricted to non-commercial functions such as market research, promotion, or liaison activities, and may not generate revenue directly.

Key Characteristics

| Requirement | Branch Office | Representative Office |

|---|---|---|

| Legal Personality | None — extension of parent company | None — extension of parent company |

| Commercial Activity | Permitted | Not permitted |

| Registration Body | Slovak Commercial Register (Obchodný register) | Slovak Commercial Register |

| Local Representative | Mandatory — an appointed head of branch (vedúci pobočky) | Mandatory — appointed representative |

| Registered Address | Required in Slovakia | Required in Slovakia |

| Capital Requirement | None specified | None |

| Privacy | Parent company details publicly disclosed in Commercial Register | Same |

Focus Points

- Taxation: Branch profits are subject to 21% corporate income tax; VAT registration is required if turnover exceeds the statutory threshold; withholding tax may apply to profit remittances depending on the applicable double tax treaty.

- Economic Substance: The appointed branch head must be verifiably resident or present; the registered address must be a genuine operational address.

- Annual Compliance: Annual financial statements must be filed with the Commercial Register; the branch consolidates into the parent's accounts.

- Treaty Access: Access to Slovakia's tax treaty network depends on the parent entity's tax residency and treaty eligibility — the branch itself is not a treaty resident.

- Restrictions: A representative office cannot invoice clients, hold inventory for sale, or enter into commercial contracts in its own operational capacity.

Closing

A branch office suits foreign firms testing the Slovak market or managing local contracts without incorporating a separate subsidiary, though the parent's unlimited exposure to branch liabilities is a significant structural drawback.

Foreign companies seeking a temporary or exploratory presence in Slovakia without committing to a standalone subsidiary structure.

Živnosť – Sole Trader / Self-Employment

Živnosť sole trader registration Slovakia is governed by Act No. 455/1991 Coll. (the Trade Licensing Act), which defines a živnosť as a systematic, independent, profit-oriented activity carried out under one's own name and on one's own account. Unlike capital companies, this form carries no separate legal personality — the proprietor and the business are legally the same person.

Registration is handled through the District Trade Licensing Office (Okresný úrad, odbor živnostenského podnikania), which issues the živnostenský list (trade licence) upon approval. Foreign nationals from outside the EU may face additional conditions, including a valid residence permit, before obtaining a licence.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sole trader (natural person) | No separate legal personality; proprietor bears full personal liability |

| Proprietor | Single individual (proprietor) | Cannot have co-owners; not suitable for multi-party ventures |

| Local Presence | Registered business address in Slovakia | Place of business must be stated on the licence |

| Capital | No minimum required | No share capital or registered capital obligation |

| Liability | Unlimited personal liability | Personal assets are exposed to business debts |

| Privacy | Proprietor's name and address appear in public registers | Minimal privacy; data published in the Trade Register |

Focus Points

- Taxation: Proprietors are subject to personal income tax (19%/25% progressive rates) on net business income; VAT registration is mandatory once turnover exceeds €49,790 annually; no corporate tax applies.

- Social and health contributions: Mandatory contributions to the Social Insurance Agency (Sociálna poisťovňa) and health insurance funds apply from the first year of active trading.

- Annual compliance: No statutory audit requirement; annual income tax return filed with the Slovak Tax Authority (Finančná správa); simplified or flat-rate expense accounting available.

- Conversion: A živnosť can be converted into an s.r.o., though the process requires establishing a new legal entity and transferring assets separately.

- Treaty access: As a natural person, the proprietor may access Slovakia's double tax treaty network, subject to individual residency status.

Sub-Types

Voľná Živnosť (Free Trade)

Covers activities that require no specific professional qualification — such as general retail or administrative services. Registration is straightforward, with no examination or credential verification required by the licensing office.

Remeselná Živnosť (Craft Trade)

Applies to regulated crafts listed in Annex 1 of the Trade Licensing Act, where proof of vocational qualification or apprenticeship is a prerequisite for obtaining the licence.

Viazaná Živnosť (Bound Trade)

Requires documented professional qualifications or specific certifications, as prescribed for each activity in Annex 2 of the Act — typically covering technical or specialised service sectors.

A živnosť suits individuals providing services or goods on a small-to-medium scale without the administrative overhead of a capital company. The absence of a minimum capital requirement is a practical entry point, but unlimited personal liability remains a significant structural drawback for any activity carrying financial or legal risk.

Freelancers, consultants, and sole practitioners seeking a low-cost, straightforward operating structure for individual professional or trade activity in Slovakia.

How to Choose the Right Entity Type in Slovakia

Selecting how to structure your business presence in Slovakia shapes your tax position, liability exposure, administrative burden, and ability to raise capital — often from the day of registration.

Why Your Entity Choice Matters

Concrete consequences follow from mismatched structures:

- Selecting an s.r.o. or a.s. when your actual activity requires a licensed structure — such as a bank, insurer, or investment fund — means operating without the authorisation required under Act No. 566/2001 Coll. on Securities, exposing the entity to regulatory sanction or forced dissolution.

- Choosing a structure that is not a Slovak tax resident means forfeiting access to Slovakia's double tax treaty network, preventing your business from claiming withholding tax reductions in counterpart countries.

- Forming a capital company when asset protection is the primary goal locks you into annual shareholder meeting obligations and mandatory share register disclosures that do not apply to alternative structures.

- Picking an a.s., which requires statutory audit under Act No. 431/2002 Coll. on Accounting when threshold criteria are met, adds recurring audit costs that are disproportionate for a single-person consultancy.

Key Factors to Consider

- Business Activity: Active trading, passive asset-holding, and regulated sectors each correspond to distinct permissible structures under Slovak commercial law.

- Ownership and Management: A single founder suits an s.r.o.; multi-investor arrangements with transferable securities point toward an a.s. or j.s.a.

- Tax Objectives: Your need for full treaty access, participation exemption eligibility, or a specific withholding rate determines whether full Slovak tax residency is required.

- Public Disclosure Tolerance: Directors and shareholders of Slovak entities are recorded in the Obchodný register, which is publicly searchable; nominee structures can address disclosure sensitivity within legal bounds.

- Substance Capacity: If your business cannot maintain genuine management and operations locally, choose a structure with lower substance thresholds to avoid transfer pricing or permanent establishment exposure.

- Exit Strategy: Only certain Slovak entities permit cross-border conversion or redomiciliation under EU Directive 2019/2121; verify this before registering.

The full text of the Commercial Code (Act No. 513/1991 Coll.) governing entity formation and operation in Slovakia is available on the official Slov-Lex legal database.

Compliance Services for Companies in Slovakia

Ongoing compliance support for Slovak entities, including statutory filings, register maintenance, and regulatory reporting.

Conclusion

Slovakia offers a defined set of legal structures, each suited to distinct ownership profiles and operational scales. This setting up a company in Slovakia guide has covered the full spectrum — from sole trader registrations under the Trade Licensing Act to capital-intensive joint stock companies governed by the Commercial Code. The s.r.o. remains the most commonly registered entity, accounting for the majority of new business formations each year. The j.s.a. serves founders who require equity flexibility without the capital burden of a full a.s. Partnerships suit smaller, relationship-based operations where personal liability is an accepted condition. Branch and representative offices address foreign firms testing the market before committing to local incorporation. Slovakia's expanding tax treaty network and its EU membership continue to shape its attractiveness for cross-border structures. Determining the right fit depends on your ownership structure, liability tolerance, and long-term operational intent — factors that Expanship's advisory team works through with each client individually.

How Expanship Can Assist You

Expanship Slovakia company formation services cover the full process of establishing and maintaining a legal entity under Slovak law. From registering an s.r.o. at the District Court Commercial Register to meeting the capital requirements of an a.s. or j.s.a., we handle the specifics — not just the paperwork.

Our team works directly with the Obchodný register and relevant Slovak authorities on your behalf. Here is what that looks like in practice:

- Document preparation, notarisation, and apostille where required

- Registered agent and registered office provision in Slovakia

- Filing and liaison with the Commercial Register (Obchodný register)

- Post-incorporation compliance: annual returns, statutory updates, and director obligations

- Corporate bank account introduction assistance with Slovak and international banks

Ready to incorporate in Slovakia with professional help? Reach out to the Expanship Slovakia team to discuss your specific situation.

Frequently Asked Questions (FAQ)

The s.r.o. (spoločnosť s ručením obmedzeným) is the most frequently incorporated business form in Slovakia. Its combination of limited liability, a low minimum share capital of EUR 5,000, and a single-member formation option makes it the default choice for both domestic entrepreneurs and foreign investors.

Both carry limited liability, but the a.s. requires a minimum share capital of EUR 25,000 and is subject to more extensive disclosure and governance obligations, including a supervisory board in certain configurations. The s.r.o. imposes lighter compliance requirements and suits closely-held businesses, while the a.s. is structured for firms seeking external capital or institutional investment.

Not all structures permit sole formation. A v.o.s. and a k.s. each require a minimum of two partners by statute. By contrast, an s.r.o., a.s., and j.s.a. can each be founded by one person or one legal entity.

All principal Slovak entity types — including the s.r.o., a.s., and j.s.a. — are open to foreign founders and directors without residency requirements. A foreign firm preferring not to incorporate locally can instead register a branch office (organizačná zložka) through the Commercial Register.

The s.r.o., a.s., and j.s.a. each hold full legal personality distinct from their members. A v.o.s. and k.s. also possess legal personality under Slovak law, though partners in a v.o.s. retain unlimited personal liability for the firm's obligations.

The Commercial Code permits the transformation (premena) of companies, including conversion from an s.r.o. to an a.s. Conversions require a notarial deed, shareholder approval, and re-registration in the Commercial Register maintained by the district court.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.