Key Takeaways

- Slovakia's flat 21% corporate income tax rate establishes a predictable, defined tax position from the moment of incorporation, removing ambiguity for international businesses structuring cross-border operations.

- Foreign founders can register a fully operational EU-resident S.R.O. without meeting a minimum share capital threshold, reducing the upfront financial commitment required to establish a legal presence in the single market.

- The Obchodný zákonník (Slovak Commercial Code) governs company formation under a consistent legal framework that applies equally to domestic and foreign founders, providing regulatory certainty rather than discretionary treatment.

- Slovakia's active network of double taxation agreements reduces withholding tax exposure on cross-border income flows, making the jurisdiction structurally advantageous for businesses managing royalties, dividends, or intercompany payments across borders.

Situated in Central Europe and bordered by Austria, the Czech Republic, Hungary, Poland, and Ukraine, Slovakia is a sovereign republic and a full member of the European Union. Company registration is administered by the Slovak Business Register, which operates under the Ministry of Justice. Foreign businesses incorporating here most commonly do so through an S.R.O. The country maintains a treaty-based tax posture, with an active network of double taxation agreements that shapes how cross-border income is treated. Foreign ownership of Slovak companies faces no general statutory restrictions, and the government has maintained an open stance toward foreign direct investment across most sectors.

Regulated under the Obchodný zákonník — the Slovak Commercial Code — business formation follows a defined legal process that applies equally to domestic and foreign founders. Your entity, once registered, operates within an EU-regulated environment with access to the single market. This article sets out the principal advantages that incorporation in Slovakia offers to international businesses and investors.

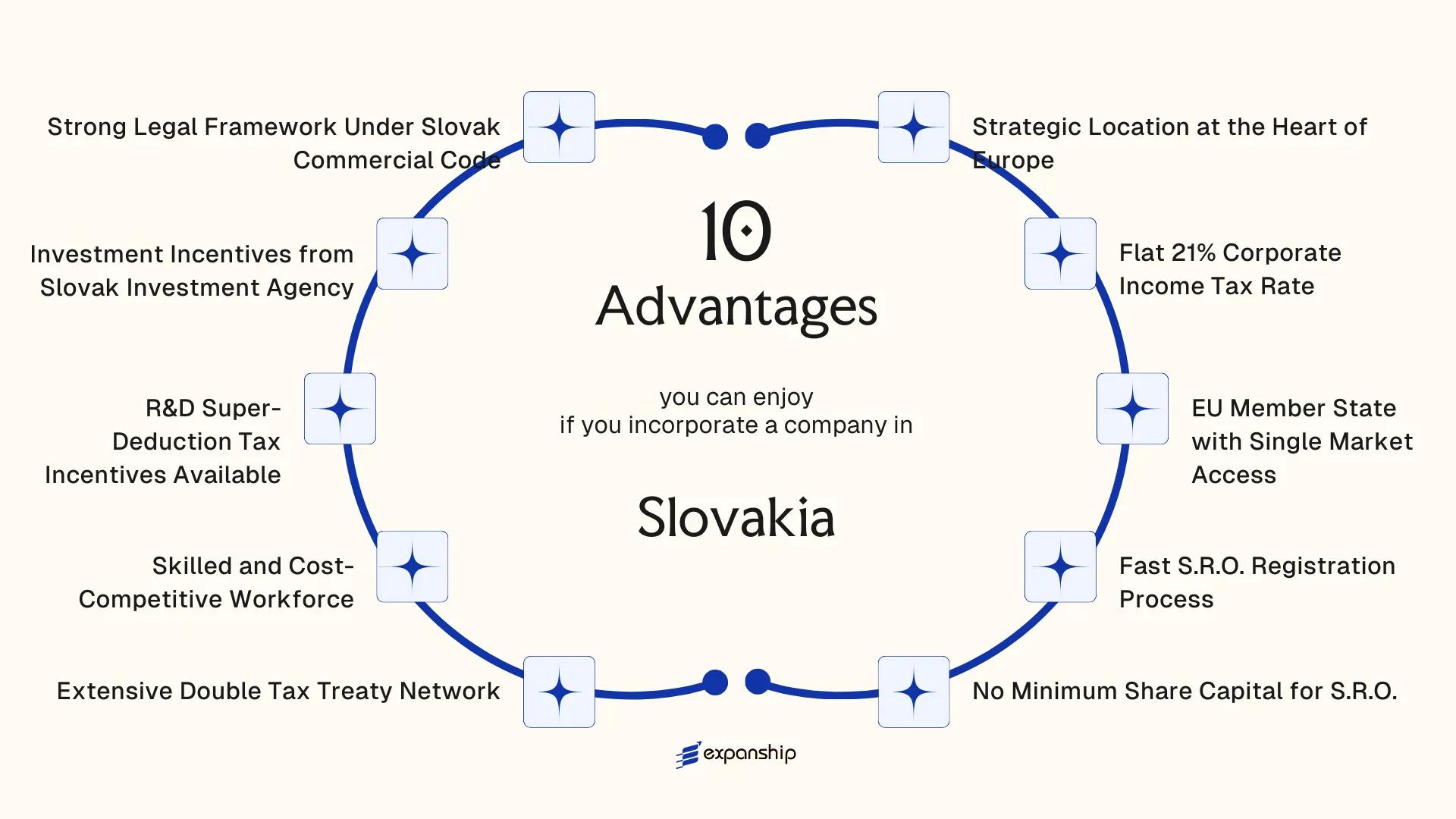

Strategic Location at the Heart of Europe

Slovakia's strategic location in Central Europe places your business within a four-hour drive of Vienna, Prague, Budapest, and Warsaw. That proximity is not incidental — it reflects a geographic position that sits at the intersection of Western, Central, and Eastern European trade corridors.

Access to Major EU Markets Without Logistical Overhead

Slovakia's membership in the Schengen Area removes border controls with eight neighboring or near-neighboring states, meaning goods and personnel move without customs stops across much of the continent. For a distribution-oriented entity, this translates directly into lower transit costs and faster delivery cycles across markets that collectively represent hundreds of millions of consumers.

Infrastructure That Supports Cross-Border Operations

The country sits along the Pan-European Transport Corridors IV and V, two designated EU freight routes connecting Western Europe to Ukraine and the Adriatic. Bratislava's position on the Danube also provides inland waterway access that few Central European capitals can match. A firm operating from here can realistically serve both German and Romanian clients from a single operational base.

A company registered in Slovakia can serve EU and non-EU markets from a single base without the logistical costs typically associated with multi-country distribution setups.

Flat 21% Corporate Income Tax Rate

Slovakia applies a flat 21% corporate income tax rate to the net taxable profits of resident companies and Slovak-registered branches of foreign entities. This rate has remained consistent, giving your business a predictable tax position from the outset. The Slovakia flat 21% corporate tax rate advantage becomes particularly clear when set against the EU average corporate tax rate, which sits closer to 21.3% according to Tax Foundation data, placing the Slovak rate in a competitive position while offering the full benefits of EU membership.

Under the Income Tax Act (Act No. 595/2003 Coll.), taxable income is calculated after allowable deductions, meaning your actual effective rate is often lower than the statutory figure. That gap matters for businesses with significant operating costs or depreciable assets.

The flat structure itself carries practical value for foreign investors:

- A single rate applies regardless of profit volume, so scaling your business does not trigger a higher tax band

- Profit repatriation planning is more straightforward because the tax outcome on distributed earnings is calculable in advance

- There is no distinction between retained and distributed profits at the corporate level, which supports reinvestment decisions

Tax obligations for a Slovak entity are administered through the Financial Administration of the Slovak Republic, and corporate tax returns are filed annually, with the option to extend the filing deadline to 18 months in certain cases involving foreign-source income.

Company Incorporation in Slovakia

Register your Slovak s.r.o. or a.s. and establish a compliant, tax-efficient presence in the EU.

EU Member State with Single Market Access

As a Slovakia EU member state single market access benefit, EU accession in 2004 gave Slovak-registered entities full access to a market of over 440 million consumers across 27 member states, without customs duties, tariffs, or import licensing requirements that would otherwise apply to third-country businesses.

A company incorporated under the Slovak Commercial Code (Act No. 513/1991 Coll.) is treated as an EU entity by default. This means your firm can supply goods and services across the EU without establishing separate legal presence in each target country. For businesses selling into Germany, Austria, or France, a single Slovak entity is legally sufficient.

| Entitlement | Basis | Practical Scope |

|---|---|---|

| Free movement of goods | EU Treaty on the Functioning of the EU (TFEU) | No intra-EU tariffs or customs declarations |

| Freedom to provide services | TFEU Article 56 | Cross-border service delivery without local entity |

| EU VAT regime participation | EU VAT Directive 2006/112/EC | Access to OSS scheme for EU-wide VAT reporting |

| EU regulatory passporting | Sector-specific EU directives | Applicable in financial services, pharmaceuticals, and others |

Participation in the EU's One Stop Shop (OSS) VAT scheme is available to Slovak entities, allowing consolidated VAT filings for cross-border B2C sales across all member states through a single registration with the Slovak Tax Authority (Finančná správa). This removes the administrative burden of registering for VAT separately in every country where you sell.

Fast S.R.O. Registration Process

Registering an S.R.O. (Spoločnosť s ručením obmedzeným) in Slovakia has become noticeably faster following procedural reforms that reduced bureaucratic friction at the Commercial Register. For foreign founders, the Slovakia S.R.O. fast registration advantages are direct: less time waiting for legal status means faster access to contracts, banking, and EU market operations.

Under current rules, registration through the Slovak Commercial Register can be completed within a few business days when documentation is in order. That speed matters because your entity cannot legally invoice, hire staff under a Slovak employment contract, or open a corporate bank account until registration is confirmed.

Notarisation requirements apply to the founding deed (zakladateľská listina) for a sole founder, or the memorandum of association (spoločenská zmluva) for multiple founders. Both must be authenticated before submission, which is a fixed procedural step regardless of how quickly other stages move.

- Founding deed or memorandum of association must be notarised before filing

- Registration application submitted to the relevant district court's Commercial Register

- A registered seat address in Slovakia is required at the time of filing

- All directors must be identified with valid identification documents

A single-founder S.R.O. can be established entirely by one individual acting as both the sole shareholder and the sole director, with no requirement for a local Slovak resident in either role.

No Minimum Share Capital for S.R.O.

One of the more operationally significant Slovakia S.R.O. no minimum share capital benefit is that the spoločnosť s ručením obmedzeným technically requires only a €5,000 total registered capital, with a minimum contribution per founder set at €750. While that nominal threshold exists on paper, it represents one of the lowest effective entry points in the EU, and it does not need to be fully paid up before registration in all cases.

What the Capital Structure Actually Means for Your Business

Under the Slovak Commercial Code (Obchodný zákonník), founders are not required to deploy significant funds simply to satisfy a registration formality. For a foreign investor testing the Slovak market, this means capital can be directed toward operations, staffing, or infrastructure rather than held in a statutory account as a compliance condition.

A single-member S.R.O. remains fully permissible under this structure, which removes the need to recruit co-founders purely to distribute capital obligations.

How This Compares Structurally

Across several EU jurisdictions, minimum share capital requirements for private limited companies range into tens of thousands of euros, creating a front-loaded cost before the entity generates any revenue. The Slovak low share capital requirement for an S.R.O. eliminates this barrier, allowing your firm to become legally operational with minimal upfront statutory commitment.

Liability remains capped at the value of each member's contribution, so the capital advantage does not come at the cost of personal exposure beyond that defined limit.

Structure Your Slovak S.R.O. Capital the Right Way

Speak with our team about how the S.R.O. capital rules apply to your specific ownership structure and business objectives in Slovakia.

Extensive Double Tax Treaty Network

Slovakia's double tax treaty network advantages are among the more practical structural benefits available to foreign investors operating through a Slovak entity. The country has concluded over 70 bilateral double taxation agreements, covering major trading partners across Europe, Asia, North America, and the Middle East. These treaties generally follow the OECD Model Tax Convention, providing predictable rules on the allocation of taxing rights between contracting states.

- Reduced withholding tax rates on dividends, interest, and royalties paid across borders, often significantly below domestic statutory rates, directly reduce the cost of repatriating profits or servicing intercompany financing arrangements.

- Treaty-based permanent establishment definitions give your business clearer thresholds for determining when a taxable presence is triggered in a partner country, reducing unintended tax exposure during cross-border operations.

- The mutual agreement procedure available under these treaties provides a formal mechanism to resolve double taxation disputes between tax authorities, giving foreign investors a defined process rather than unilateral exposure.

- Treaties with key jurisdictions including Germany, the United States, China, and the United Arab Emirates mean that businesses structuring regional operations through a Slovak company can access treaty protection across a wide range of commercial corridors.

Eligibility for treaty benefits generally requires that the Slovak entity has sufficient substance and is not treated as a conduit arrangement under anti-avoidance provisions applicable in the relevant partner jurisdiction.

Skilled and Cost-Competitive Workforce

Slovakia's skilled cost-competitive workforce advantage is one of the more concrete operational benefits available to foreign businesses establishing a presence here. Average gross monthly wages remain well below the EU-27 average, while tertiary education enrollment and STEM graduate output are comparatively high, particularly in engineering, IT, and economics disciplines.

Bratislava and Košice both host universities producing graduates who enter the labour market with technical qualifications that align with the needs of manufacturing, software development, and shared service operations. Your firm can hire mid-level engineers or software developers at total employment costs that are structurally lower than in Austria, Germany, or the Netherlands, with no compromise on formal qualification levels.

Labour relations in Slovakia are governed by Act No. 311/2001 Coll. (the Labour Code), which sets out employment contract terms, working time limits, and termination procedures within a predictable legal framework. This gives your business a clear basis for workforce planning from the first hire.

A software developer with five years of experience in Bratislava earns approximately €2,000–€2,500 gross per month. An equivalent profile in Vienna or Munich typically commands €4,500–€5,500 gross. For a team of ten, that differential translates to annual savings exceeding €300,000 in payroll costs alone, before accounting for employer social contributions.

R&D Super-Deduction Tax Incentives Available

Slovakia's R&D super-deduction tax incentive benefits companies that conduct qualifying research and development activities within the country. Under the Income Tax Act (Act No. 595/2003 Coll.), eligible entities can deduct R&D expenditure twice: once as a standard operating cost and again as a super-deduction of 100% of qualifying costs. This means a single euro of R&D spending reduces taxable income by two euros.

Qualifying expenditure covers personnel costs, depreciation on R&D assets, and direct material costs tied to eligible projects. The deduction applies in the tax year costs are incurred, which improves cash flow rather than deferring the benefit.

For a foreign-owned entity operating through a Slovak s.r.o., this structure meaningfully reduces the effective corporate tax rate below the standard 21% on income generated through innovation activities. Technology firms, pharmaceutical companies, and engineering businesses operating in the country stand to benefit most.

- Qualifying projects must constitute systematic research or experimental development as defined under the Act

- The super-deduction cannot exceed the tax base; unused amounts can be carried forward for up to four consecutive tax periods

- Costs must be separately tracked and documented to satisfy the tax authority (Finančná správa SR)

The super-deduction applies only to costs directly attributable to qualifying R&D projects, so mixed-use expenditure must be apportioned before the deduction is claimed.

Investment Incentives from Slovak Investment Agency

SARIO, the Slovak Investment and Trade Development Agency, administers a structured programme of state-backed incentives designed to attract foreign direct investment into the country. For qualifying businesses, these incentives directly reduce the capital burden of establishing or expanding operations.

The available instruments include:

- Cash grants for initial investment in manufacturing, technology centres, and shared services

- Tax relief on corporate income tax for a defined period following the investment

- Contributions toward job creation costs, particularly in regions with higher unemployment

- Support for vocational training and employee upskilling linked to the investment project

Eligibility under the Slovak Investment Aid Act depends on factors including the sector of activity, the volume of investment committed, the number of jobs created, and the location of the project within Slovakia. Investments directed at less-developed regions typically qualify for higher support intensity under EU state aid rules, which cap the maximum allowable grant as a percentage of eligible costs.

From a practical standpoint, the cash grant mechanism means that a foreign company can offset a measurable portion of its capital expenditure directly from state funds, rather than relying solely on tax-based recovery over time. This shortens the effective payback period on the initial investment.

SARIO investment incentives advantages for Slovakia-based projects are assessed on a project-by-project basis. Your business submits a formal application, and the Ministry of Economy of the Slovak Republic issues the final decision on whether investment aid is granted.

Strong Legal Framework Under Slovak Commercial Code

The Slovak Commercial Code legal framework benefits foreign businesses because the primary statute governing companies, Act No. 513/1991 Coll. (the Obchodný zákonník), has been in continuous force since 1991 and provides codified rules on company formation, shareholder rights, director obligations, and contractual relationships. That legislative continuity means the rules your entity operates under are well-tested and predictably interpreted by Slovak courts.

Predictability extends to dispute resolution. Commercial cases are heard by specialised divisions within the Slovak district and regional court system, which apply the Obchodný zákonník directly. Foreign investors are not subject to ad hoc regulatory interpretation; the statutory framework defines obligations precisely.

Key structural protections under the Obchodný zákonník include:

- Codified rules on transferability of business shares (obchodný podiel) in an s.r.o., with defined procedures for consent and registration at the Obchodný register

- Statutory minimum content requirements for the memorandum of association (spoločenská zmluva), reducing ambiguity in foundational documents

- Defined liability separation between the company and its shareholders, enforceable under Slovak civil and commercial law

- Mandatory disclosure obligations via the Obchodný register, which is publicly accessible and maintained by the Ministry of Justice

Slovakia's membership in the EU further reinforces the domestic framework. EU directives on company law, including those on single-member companies and cross-border mergers, have been transposed into Slovak law, aligning the Obchodný zákonník advantages for companies with EU-wide standards. A foreign-owned s.r.o. therefore operates within a legal architecture that is both locally codified and externally validated by supranational legislation.

Why Slovakia Stands Out Among EU Jurisdictions

Compared against other Central European EU members, Slovakia sits in a cluster of jurisdictions, including Czechia, Hungary, and Poland, that frequently attract the same profile of foreign investor: manufacturers, regional holding structures, and service exporters seeking EU market access without the overhead costs of Western Europe. These three were selected as comparison anchors because a business evaluating incorporation in Bratislava would realistically be weighing the same decision against Prague, Budapest, or Warsaw.

What the comparison reveals is not a single decisive advantage but a consistent pattern. Slovakia's 21% flat corporate rate sits below Poland's standard 19% on paper, though Poland applies that rate only to smaller firms, with larger entities taxed at 19% while Slovakia applies one uniform rate regardless of size. Hungary's 9% rate draws attention, but its compliance environment and banking access conditions differ substantially. Czechia matches Slovakia closely on several parameters, making the S.R.O. structure and treaty network the differentiating factors for entity selection between the two.

| Parameter | Slovakia | Czechia | Hungary | Poland |

|---|---|---|---|---|

| Standard CIT Rate | 21% (flat) | 21% | 9% | 19% (9% for small taxpayers) |

| Minimum Share Capital (Private LLC) | €1 (S.R.O.) | CZK 1 (approx. €0.04) | HUF 3,000,000 (approx. €7,500) | PLN 5,000 (approx. €1,150) |

| Double Tax Treaties (approx.) | 70+ | 90+ | 80+ | 90+ |

| EU VAT Registration | Required at threshold | Required at threshold | Required at threshold | Required at threshold |

| R&D Super-Deduction | Yes (up to 200%) | Yes | Yes | Yes |

| Investment Incentive Agency | SARIO | CzechInvest | HIPA | PAIiH |

Compliance Services for Companies in Slovakia

Ongoing compliance for Slovak S.R.O. entities, covering annual filings, statutory reporting, and Commercial Register obligations under Slovak law.

Conclusion

Slovakia presents a coherent case for foreign business incorporation when its structural features are considered together rather than in isolation. The flat 21% corporate income tax rate, combined with access to the EU single market and the absence of a minimum share capital requirement for the s.r.o., means that an international entrepreneur can establish a fully operational EU-resident entity with limited upfront capital and a defined, predictable tax position from day one.

The benefits of incorporating in Slovakia are most pronounced for businesses that value regulatory consistency alongside cost efficiency. The Slovak Commercial Code provides a well-defined legal framework, and the country's network of double tax treaties reduces withholding tax exposure on cross-border income flows. These are structural advantages rather than discretionary incentives, which means they apply broadly rather than depending on a specific approval process.

Whether these advantages translate into the right outcome for your business depends on your industry, existing group structure, and the nature of your cross-border activity. A holding company with significant royalty flows will evaluate the jurisdiction differently than an operational subsidiary targeting Central European markets. The specific fit matters. For businesses where the structural profile aligns, the next step involves engaging with the formal registration process under Slovak law and confirming compliance requirements with qualified local advisers.

Start Your Slovak Company with Expanship Today

Expanship assists foreign entrepreneurs with the formation of Slovak spoločnosť s ručením obmedzeným (s.r.o.) entities, covering the full registration cycle through the Obchodný register (Commercial Register) administered by the relevant district court. The benefits examined throughout this blog, from the flat 21% corporate tax rate to the R&D super-deduction and the Slovak Investment and Trade Development Agency incentives, reflect a jurisdiction where the regulatory structure consistently works in favor of foreign-owned businesses.

Expanship's service scope for Slovakia covers the following:

- Preparation and legalization of incorporation documents, including the memorandum of association and notarial deeds

- Registered agent and registered office provision at a Slovak address, as required under the Commercial Code

- Filing with the Obchodný register and liaison with the relevant district court registry

- Post-incorporation compliance management, including statutory reporting and annual obligations

- Tax registration with the Finančná správa (Financial Administration of the Slovak Republic)

- Banking introduction assistance to support corporate account opening with Slovak financial institutions

Each service is handled by professionals familiar with Slovak commercial law and the procedural requirements of local authorities, reducing the administrative burden on you as a foreign founder.

Contact Expanship Slovakia to discuss your company formation requirements.

Frequently Asked Questions (FAQ)

The standard corporate income tax rate is 21% on taxable profits. Smaller entities with taxable income not exceeding EUR 100,000 are subject to a reduced rate of 15%. These rates apply to profits generated within Slovakia, though a firm with cross-border structures should also consider the application of relevant double tax treaties.

Slovak tax legislation permits companies to deduct qualifying research and development expenditure at a rate exceeding 100% of the actual costs incurred, effectively reducing the taxable base beyond the nominal expense. Eligible costs generally include personnel expenses and direct R&D project costs, subject to conditions set out in the Income Tax Act (Act No. 595/2003 Coll.). Expenditure must relate to activities that meet the statutory definition of research or development under Slovak law.

EU membership means a Slovak-registered entity can operate within the single market under EU passporting principles applicable to relevant regulated activities, and benefit from the free movement of goods, services, and capital across member states. For unregulated commercial activities, the firm can trade across the EU without establishing separate legal entities in each country. This is governed by EU treaty provisions rather than Slovak domestic law alone.

The Slovak Investment and Trade Development Agency (SARIO) administers incentive schemes that may include cash grants, tax relief, and contributions toward job creation costs, primarily targeting manufacturing, technology centres, and shared service operations. Eligibility depends on factors including the sector, investment volume, and regional location, with less-developed regions generally qualifying for higher incentive ceilings. Applications are assessed under Act No. 57/2018 Coll. on Regional Investment Aid.

Effective from amendments introduced under Slovak commercial law reforms, the minimum share capital requirement for an S.R.O. was reduced to EUR 1. Each founder's individual contribution must be at least EUR 1 as well. This removes a practical financial barrier for early-stage businesses or holding structures that do not require substantial initial capitalisation.

Failure to comply with statutory obligations, such as filing financial statements with the Slovak Business Register or holding required general meetings, can result in administrative penalties and, in serious cases, court-ordered dissolution of the entity. The Commercial Register Court monitors filing compliance, and persistent non-filing can trigger ex officio proceedings. Directors bear personal responsibility for ensuring the company meets its statutory deadlines under the Slovak Commercial Code.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.