Key Takeaways

- Singapore's territorial tax system taxes only locally sourced income, making the Private Limited Company (Pte. Ltd.) the dominant structure for both resident founders and foreign investors seeking access to incentives under the Income Tax Act 1947.

- The Variable Capital Company (VCC) is a structure unique to Singapore designed specifically for fund managers, offering sub-fund segregation not available under a standard private limited company.

- ACRA administers company registration and ongoing compliance across all recognised business structures — including the Companies Act, the Limited Liability Partnerships Act, and related statutes — from a single regulatory authority.

- Foreign companies entering Singapore can operate through a Branch Office or Representative Office without establishing a separate legal entity, though neither structure carries the liability protection of an incorporated subsidiary.

Introduction to Entity Types in Singapore

Singapore sits at the southern tip of the Malay Peninsula, bordered by Malaysia to the north and Indonesia to the south, and functions as an independent city-state and sovereign republic. As a global financial and trade hub in Southeast Asia, it attracts significant foreign investment — partly due to its territorial tax system, under which only income sourced within the jurisdiction is subject to corporate tax.

Company registration and ongoing compliance fall under the authority of the Accounting and Corporate Regulatory Authority (ACRA), which administers the Companies Act, the Limited Liability Partnerships Act, and several other statutes governing business formation.

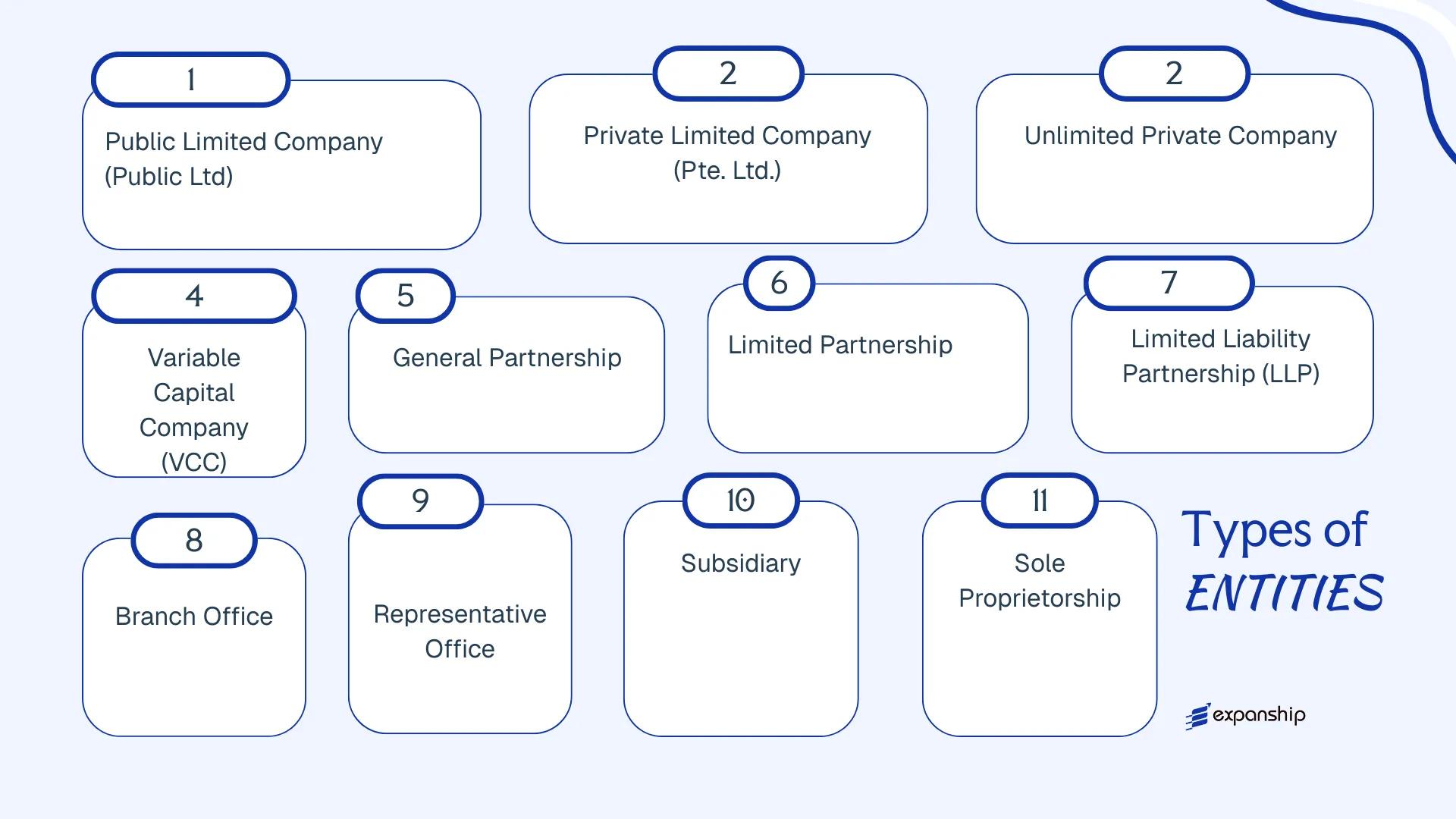

Across these types of business entities in Singapore, the law recognizes several distinct legal structures: the Private Limited Company (Pte. Ltd.), Public Limited Company, Unlimited Private Company, Variable Capital Company (VCC), General Partnership, Limited Partnership, Limited Liability Partnership, Branch Office, Representative Office, and Sole Proprietorship. Each structure carries its own liability treatment, ownership rules, regulatory obligations, and suitability for different business profiles. This article examines each option in detail to help you determine which structure fits your operational and legal requirements.

An Overview of Business Structures in Singapore

Singapore's company law framework provides nine distinct entity types for businesses operating within or from the jurisdiction. The primary legislation governing these structures is the Companies Act (Cap. 50), with certain specialised vehicles regulated under separate statutes — for instance, Variable Capital Companies fall under the Variable Capital Companies Act 2018, and Limited Liability Partnerships are governed by the Limited Liability Partnerships Act 2005. Each structure carries different implications for liability, ownership, taxation, and permitted activities.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Public Limited Company | Incorporated company | Limited | Taxed | Yes | 1 shareholder | ACRA | Companies Act |

| Private Limited Company | Incorporated company | Limited | Taxed | Yes | 1 shareholder | ACRA | Companies Act |

| Unlimited Private Company | Incorporated company | Unlimited | Taxed | Yes | 1 shareholder | ACRA | Companies Act |

| Variable Capital Company | Incorporated company | Limited | Exempt / Taxed | Restricted | 1 shareholder | MAS / ACRA | VCC Act 2018 |

| General Partnership | Unincorporated | Unlimited | Partners taxed | Yes | 2 partners | ACRA | Partnership Act |

| Limited Partnership | Unincorporated | Mixed | Partners taxed | Yes | 2 partners | ACRA | Limited Partnerships Act |

| Limited Liability Partnership | Incorporated body | Limited | Partners taxed | Yes | 2 partners | ACRA | LLP Act 2005 |

| Branch Office | Foreign extension | Unlimited | Taxed | Yes | Parent company | ACRA | Companies Act |

| Representative Office | Non-legal entity | N/A | Exempt | No | Parent company | EnterpriseSG | N/A |

| Sole Proprietorship | Unincorporated | Unlimited | Owner taxed | Yes | 1 owner | ACRA | Business Names Registration Act |

Each of these structures is examined in full in the sections below.

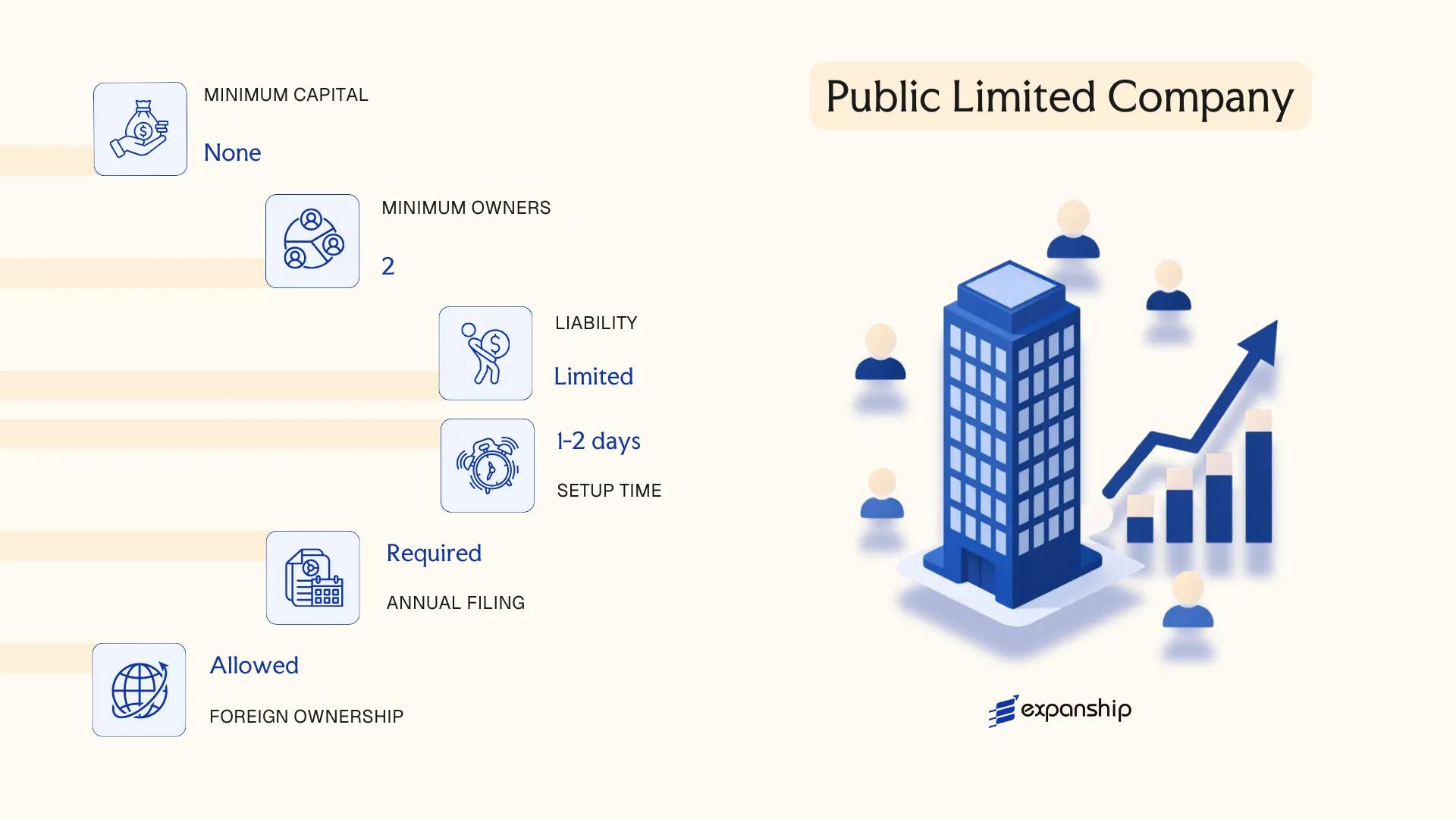

Public Limited Company (Public Ltd)

Governed by the Companies Act (Cap. 50), a public limited company in Singapore is a separate legal entity with limited liability for its shareholders. Meeting Singapore public limited company requirements involves a higher compliance threshold than private structures, given the entity's capacity to offer shares and debentures to the public.

Incorporation with the Accounting and Corporate Regulatory Authority (ACRA) is mandatory. The company must have "Limited" or "Ltd" in its name, and before any public offering, it must lodge a prospectus with the Monetary Authority of Singapore (MAS) under the Securities and Futures Act 2001.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Public Limited Company | Separate legal personality; shareholders not personally liable for company debts |

| Members | Min. 1 shareholder; no maximum cap | Directors: min. 1 (must be ordinarily resident in Singapore); Company Secretary required within 6 months |

| Local Presence | Registered office address in Singapore | Must be a physical address; P.O. boxes not permitted |

| Capital | SGD; no statutory minimum paid-up capital | Must have a share capital structure; capital requirements apply if listing on SGX |

| Privacy | Shareholder register is publicly accessible via ACRA BizFile+ | Financial statements filed with ACRA are publicly available |

Focus Points

- Taxation: Corporate tax rate is 17% on chargeable income (IRAS); GST applies at 9% if turnover exceeds SGD 1 million; dividends paid under the one-tier system are tax-exempt in shareholders' hands; withholding tax applies to certain payments to non-residents; stamp duty applies on share transfers.

- Annual Compliance: Must hold an AGM, file annual returns with ACRA, and submit audited financial statements; audit is mandatory regardless of size.

- SGX Listing: To list on the Singapore Exchange (SGX), the company must meet SGX Mainboard or Catalist board admission criteria, including minimum profit, market capitalisation, or revenue thresholds.

- Conversion: Can be converted to a private company if the shareholder count falls and public offering activity ceases, subject to ACRA approval.

- Treaty Access: Singapore's extensive double tax agreement network is accessible, subject to substance and beneficial ownership conditions.

Suitable Uses and Limitations

A public limited company is appropriate for businesses seeking to raise capital from public markets or institutional investors, particularly those pursuing an SGX listed company structure. The main advantage is unrestricted share transferability and access to public capital. The compliance burden is considerably heavier than private structures, including mandatory audits, prospectus obligations, and continuous disclosure requirements.

Large enterprises or growth-stage companies planning an IPO or seeking broad-based capital raising in regulated public markets.

Company Incorporation in Singapore

Incorporate your Singapore entity with full regulatory compliance support from ACRA registration to post-incorporation obligations.

Private Limited Company (Pte. Ltd.)

The private limited company is the most widely used business structure for Singapore Pte Ltd company registration, governed by the Companies Act (Cap. 50). It holds a distinct legal identity separate from its shareholders, meaning the entity can own assets, enter contracts, and incur liabilities in its own name.

Liability exposure for shareholders is capped at the amount unpaid on their shares. This separation between personal and corporate liability makes the structure suitable for both operational businesses and holding arrangements.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private company limited by shares | Incorporated under the Companies Act (Cap. 50) |

| Members | Shareholders (min. 1, max. 50) | Corporate shareholders permitted; single-member company allowed |

| Management | Directors (min. 1 must be ordinarily resident in Singapore) | Resident director can be a Singapore citizen, PR, or valid pass holder |

| Local Presence | Registered office address in Singapore | Must be a physical address; P.O. boxes not accepted |

| Capital | SGD; no minimum paid-up capital required | Typical practice is SGD 1; share capital can be increased post-incorporation |

| Privacy | Shareholder and director details filed with ACRA | Beneficial ownership registered in the Register of Registrable Controllers |

Focus Points

- Taxation: Corporate tax rate is 17% on chargeable income; partial tax exemptions apply for the first SGD 200,000 of income for qualifying new start-ups; GST registration is mandatory once taxable turnover exceeds SGD 1 million; withholding tax applies to certain payments to non-residents.

- Treaty Access: Qualifies for Singapore's extensive tax treaty network, subject to meeting beneficial ownership and substance requirements.

- Annual Compliance: Annual general meeting requirements, filing of annual returns with ACRA, and financial statement preparation (audit obligatory once thresholds for revenue, assets, or employee count are met).

- Conversion: A Pte. Ltd. can be converted to a public limited company or re-registered as an unlimited company under the Companies Act.

- Restrictions: Share transfer requires compliance with any shareholders' agreement and company constitution; public share offerings are prohibited.

Closing

The private limited company suits trading operations, regional holding structures, and IP ownership vehicles, with the perpetual succession and contractual capacity of a separate legal entity being a clear structural advantage. The 50-shareholder cap and the restriction on public fundraising, however, limit scalability for businesses seeking broad capital market access.

Entrepreneurs, SMEs, and foreign investors seeking a locally incorporated entity with full operational capacity and access to Singapore's treaty network.

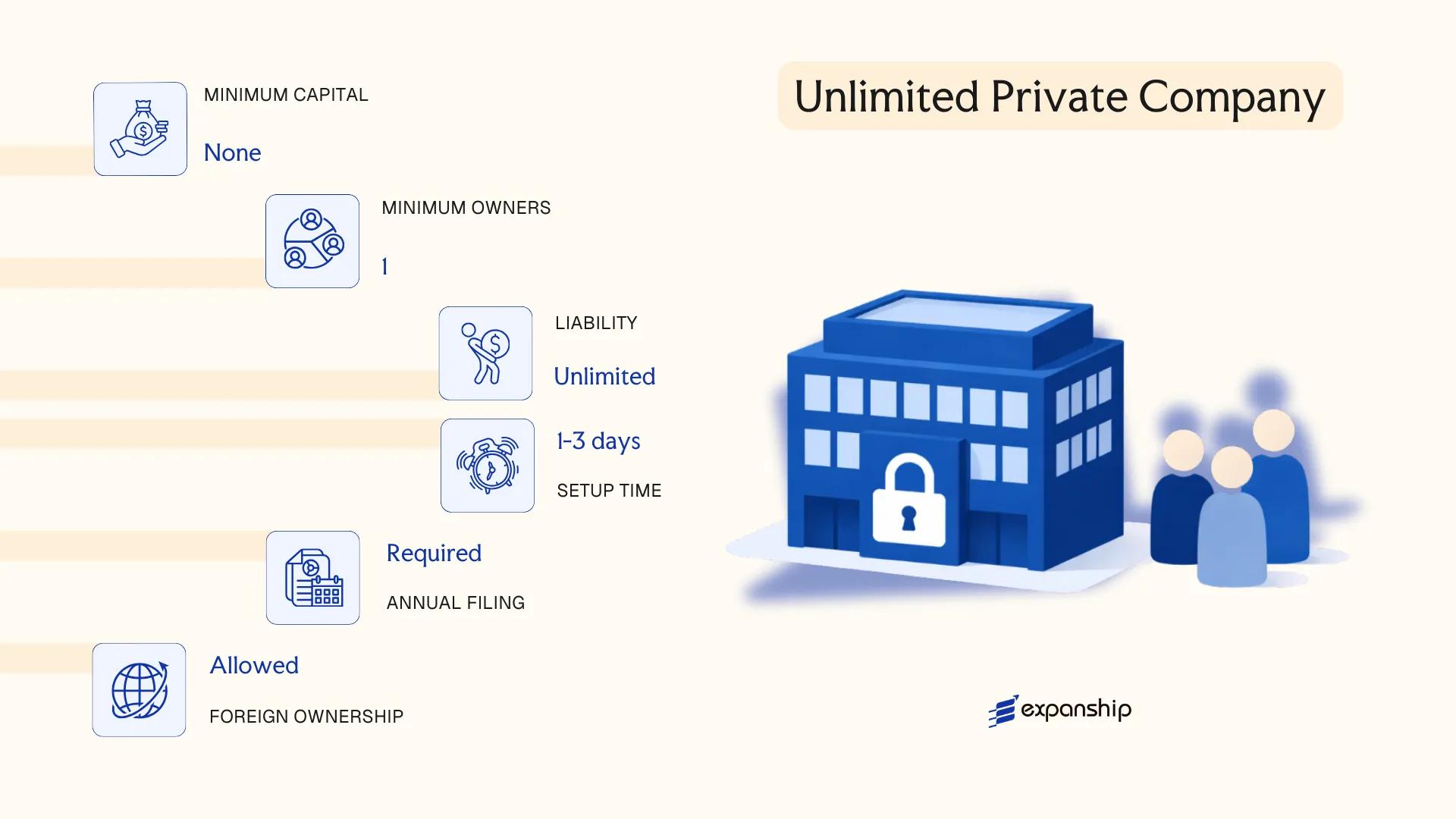

Unlimited Private Company

Registered under the Companies Act (Cap. 50), an unlimited private company in Singapore is a corporate entity with separate legal personality but without any cap on the liability of its members. Unlike a Pte. Ltd., members are personally liable for the company's debts in full if the entity is wound up with insufficient assets.

This structure is rarely used in practice. Its primary application arises in specific regulatory or structural contexts where the absence of a liability cap is either acceptable or required by a parent entity's home jurisdiction.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unlimited Private Company | Separate legal entity; no liability cap on members |

| Members | Shareholders; minimum 1, maximum 50 | Excludes employees who hold shares |

| Officers | Minimum 1 director; must be ordinarily resident in Singapore | A company secretary is also required |

| Local Presence | Registered office address in Singapore | Must be a physical address; P.O. Box not permitted |

| Capital | SGD; no minimum paid-up capital required | Shares may be issued in any currency |

| Privacy | Financial statements need not be filed publicly | This is a notable distinction from a standard Pte. Ltd. |

Focus Points

- Taxation: Subject to the standard corporate income tax rate of 17% on chargeable income; GST registration required if taxable turnover exceeds SGD 1 million; withholding tax applies to certain payments to non-residents.

- Annual Compliance: Must file annual returns with ACRA; exempt from lodging financial statements with ACRA, though accounts must still be prepared and audited.

- Conversion: Can be re-registered as a limited liability company under the Companies Act without dissolving and re-incorporating.

- Treaty Access: Qualifies as a Singapore tax resident entity for purposes of accessing the country's tax treaty network, subject to meeting substance requirements.

- Restrictions: Cannot offer shares to the public; shareholder count capped at 50.

Closing

An unlimited private company suits situations where a foreign parent requires a subsidiary structure without public disclosure of financials, and where the parent is prepared to absorb unlimited liability exposure. The exemption from public financial statement filing is the structure's primary functional advantage; the uncapped member liability remains a significant deterrent for most use cases.

Best suited for wholly-owned subsidiaries of foreign firms that require financial privacy and whose parent entity is willing to accept unlimited liability obligations.

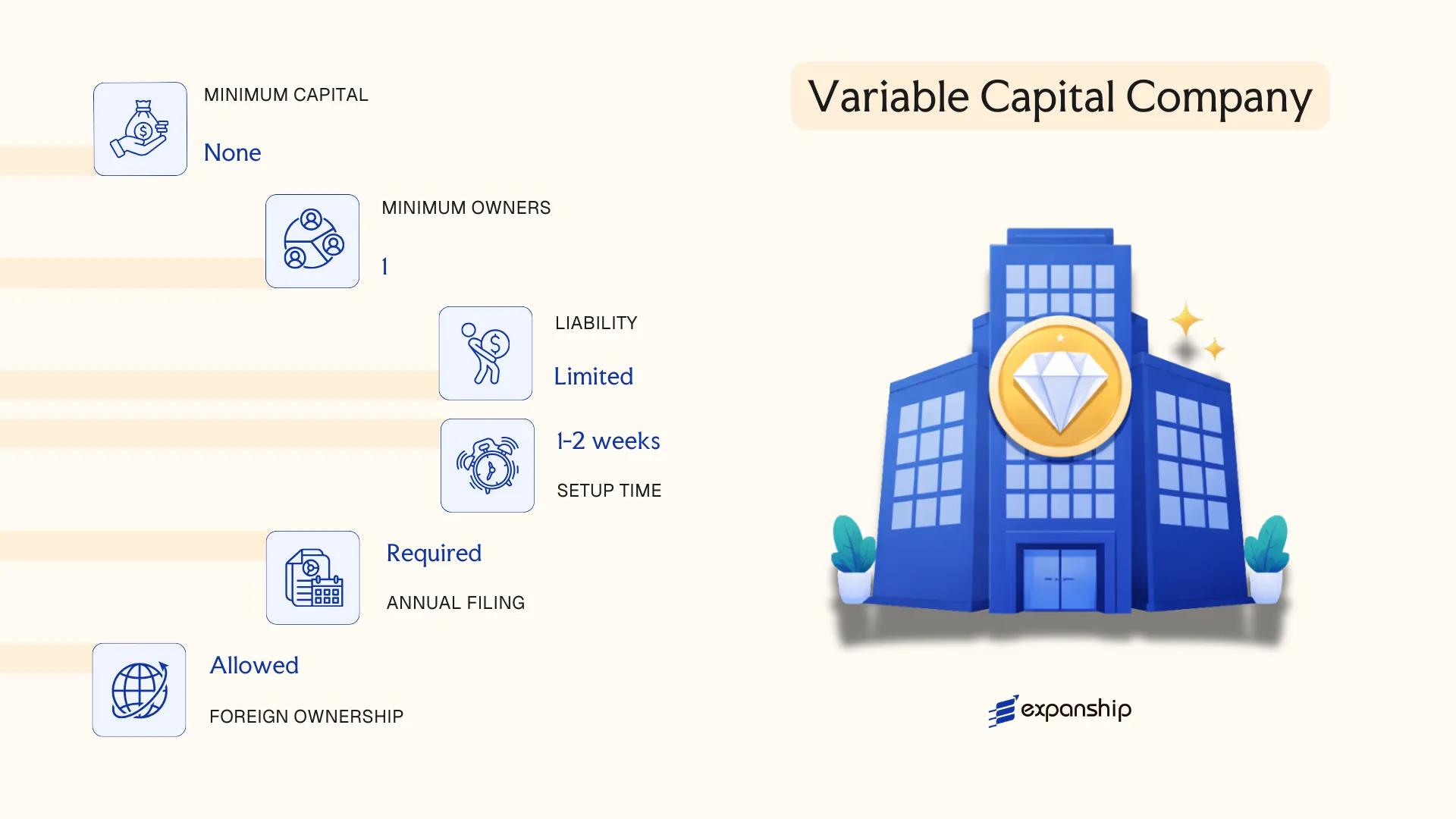

Variable Capital Company (VCC)

The Variable Capital Company is a corporate structure introduced under the Variable Capital Companies Act 2018, designed specifically for investment funds. As a Variable Capital Company Singapore VCC offers a distinct legal framework: the entity carries separate legal personality and limited liability, while allowing its capital to fluctuate without the procedural constraints that apply to conventional corporate structures.

Registered with and regulated by the Accounting and Corporate Regulatory Authority (ACRA) in conjunction with the Monetary Authority of Singapore (MAS), a VCC must appoint a licensed fund manager. This hybrid nature makes it suitable for both open-ended and closed-ended fund strategies.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Corporate entity with variable capital | Separate legal personality; capital can be increased or reduced without court approval |

| Members | Referred to as shareholders; no minimum or maximum prescribed | Shareholder register may be kept private |

| Local Presence | Registered office in Singapore; licensed fund manager required | Fund manager must hold a CMS licence or be an exempt financial adviser |

| Capital | No minimum paid-up capital; denominated in any currency | Capital equals net assets; reflects fund's NAV |

| Privacy | Shareholder register not publicly accessible | Registers filed with ACRA but withheld from public inspection |

Focus Points

- Taxation: Subject to corporate tax at 17%, with access to the Singapore Variable Capital Companies Tax Incentive schemes (13R/13X equivalents under Section 13O and 13U of the Income Tax Act); GST and withholding tax obligations depend on fund activities and investor residency.

- Economic Substance: Must maintain a licensed fund manager in Singapore; investment management activities must be genuinely conducted locally.

- Annual Compliance: Annual general meeting, annual return filing with ACRA, and audited financial statements required for each sub-fund.

- Treaty Access: May access Singapore's tax treaty network, subject to meeting conditions under the relevant tax treaty and MAS licensing requirements.

- Conversion: Existing foreign fund structures, including variable capital companies incorporated in certain recognised jurisdictions, may re-domicile into a VCC under the VCC Act.

Sub-Types

Standalone VCC

A single-fund structure with one pool of assets and one class or multiple classes of shares, all held within a single legal entity.

Umbrella VCC

Contains two or more sub-funds, each with segregated assets and liabilities. Investors in one sub-fund have no recourse against the assets of another, making this structure suitable for managers running multiple strategies under one corporate vehicle.

Closing

The VCC structure is used primarily by fund managers operating collective investment schemes, hedge funds, and private equity vehicles seeking a tax-efficient, MAS-regulated framework with portfolio segregation capability. The umbrella structure's sub-fund segregation is a material structural advantage, though the mandatory requirement for a licensed fund manager makes the VCC unsuitable for operating businesses or holding companies.

The VCC is suited for licensed fund managers seeking a regulated, tax-incentive-eligible fund vehicle with the ability to house multiple strategies under a single corporate umbrella.

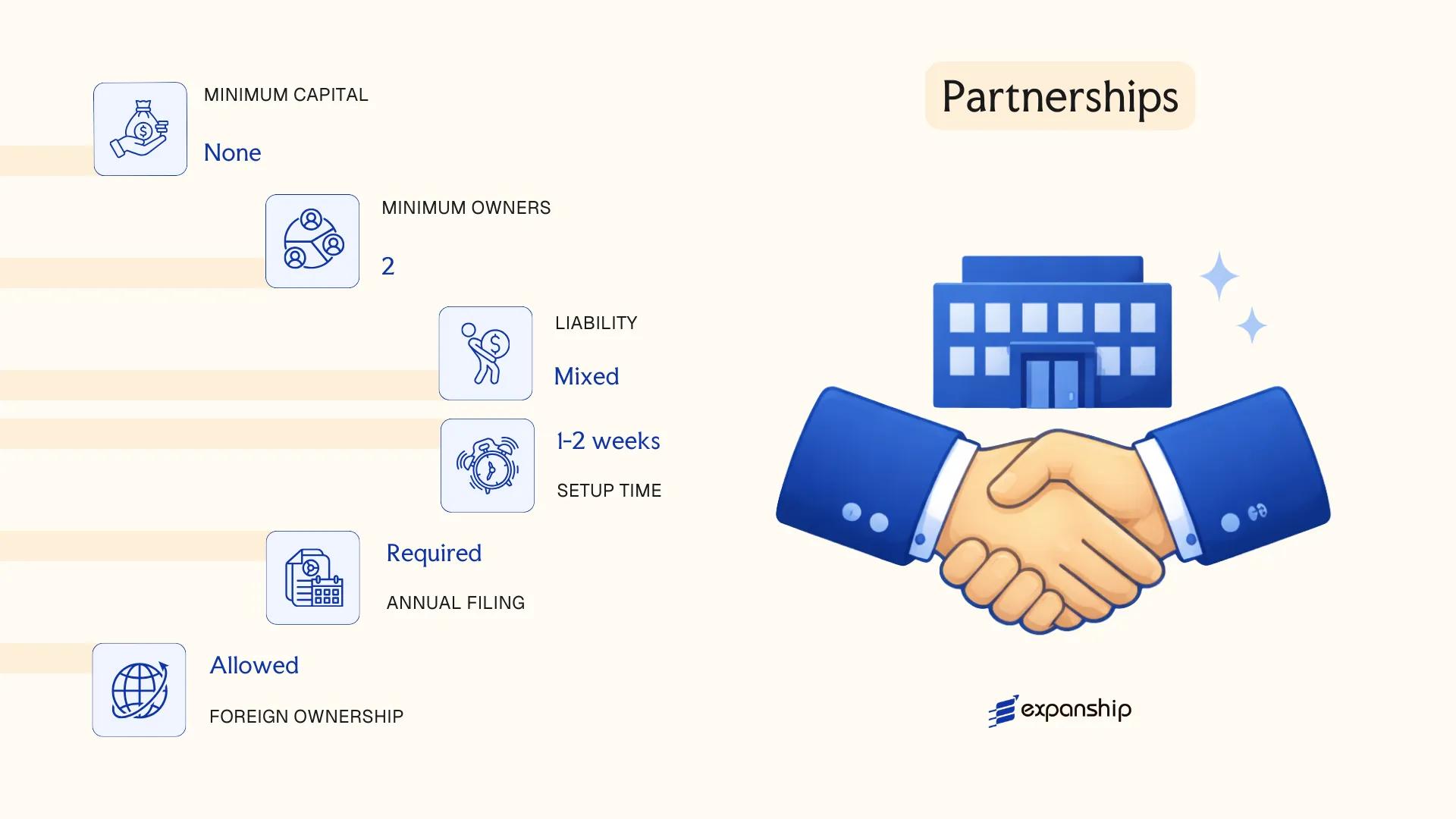

Partnerships [General Partnership, Limited Partnership, Limited Liability Partnership]

Registered under the Limited Liability Partnerships Act 2005 or the Partnership Act 1890 (as applied in Singapore), partnership structures occupy a distinct space from incorporated companies. Singapore limited liability partnership registration, governed by the Accounting and Corporate Regulatory Authority (ACRA), produces an entity with separate legal personality, unlike a general partnership, which does not confer that status on its members.

Liability exposure varies significantly across the three forms. An LLP shields individual partners from debts incurred by other partners' wrongful acts, while a general partnership holds each partner jointly and severally liable for the firm's obligations.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | GP: Unincorporated; LP: Unincorporated; LLP: Incorporated body | Only LLP has separate legal personality |

| Members | Partners (GP: min. 2, no max; LP: min. 1 general + 1 limited; LLP: min. 2, no max) | LLP partners may be individuals or corporate bodies |

| Local Presence | Registered office address in Singapore; LLP requires a local manager | Local manager must be ordinarily resident in Singapore |

| Capital | No statutory minimum for any form; contributions are contractual | No share capital structure applies |

| Privacy | Partnership agreements are not publicly filed; partner details on ACRA register | ACRA register is publicly searchable |

Focus Points

- Taxation: Partnerships are tax-transparent; profits taxed at partner level under personal or corporate income tax rates; GST registration required if turnover exceeds SGD 1 million; no separate entity-level corporate tax for GP or LP; LLP may elect for tax transparency.

- Annual Compliance: LLPs must file an Annual Declaration of Solvency or Insolvency with ACRA; GPs and LPs have lighter filing obligations but must renew registration annually.

- Conversion: An LLP may convert to a private limited company under the Limited Liability Partnerships Act without dissolving the entity.

- Treaty Access: Partnerships generally do not access Singapore's tax treaties directly; treaty benefits depend on the partner's own tax residency.

- Restrictions: LLP partners cannot be employed by the LLP in a capacity separate from their partner role without specific structuring.

Sub-Types

General Partnership (GP)

A GP offers no liability protection and no separate legal identity; each partner is personally liable for the firm's debts. Typically used by small professional practices where partners prefer minimal administrative structure.

Limited Partnership (LP)

Registered under the Limited Partnerships Act 2009, an LP distinguishes between at least one general partner bearing unlimited liability and one or more limited partners whose liability is capped at their agreed contribution. This structure is commonly used for private equity and fund vehicles.

Limited Liability Partnership (LLP)

The LLP provides separate legal personality combined with pass-through taxation, making it a preferred form for professional services firms such as law and accounting practices. When comparing LLP vs LP Singapore structures, the LLP offers broader liability protection to all partners without requiring a general partner to bear unlimited exposure.

Choosing a Partnership Structure

Partnerships suit professional services, joint ventures, and fund structures where pass-through taxation and flexible governance are priorities. The LLP's combination of legal personality and tax transparency is a practical advantage, though the absence of a share capital framework limits its utility for businesses seeking external equity investment.

Partnership structures are most appropriate for licensed professionals, fund managers, and joint venture arrangements where partners prefer contractual governance over a corporate constitution.

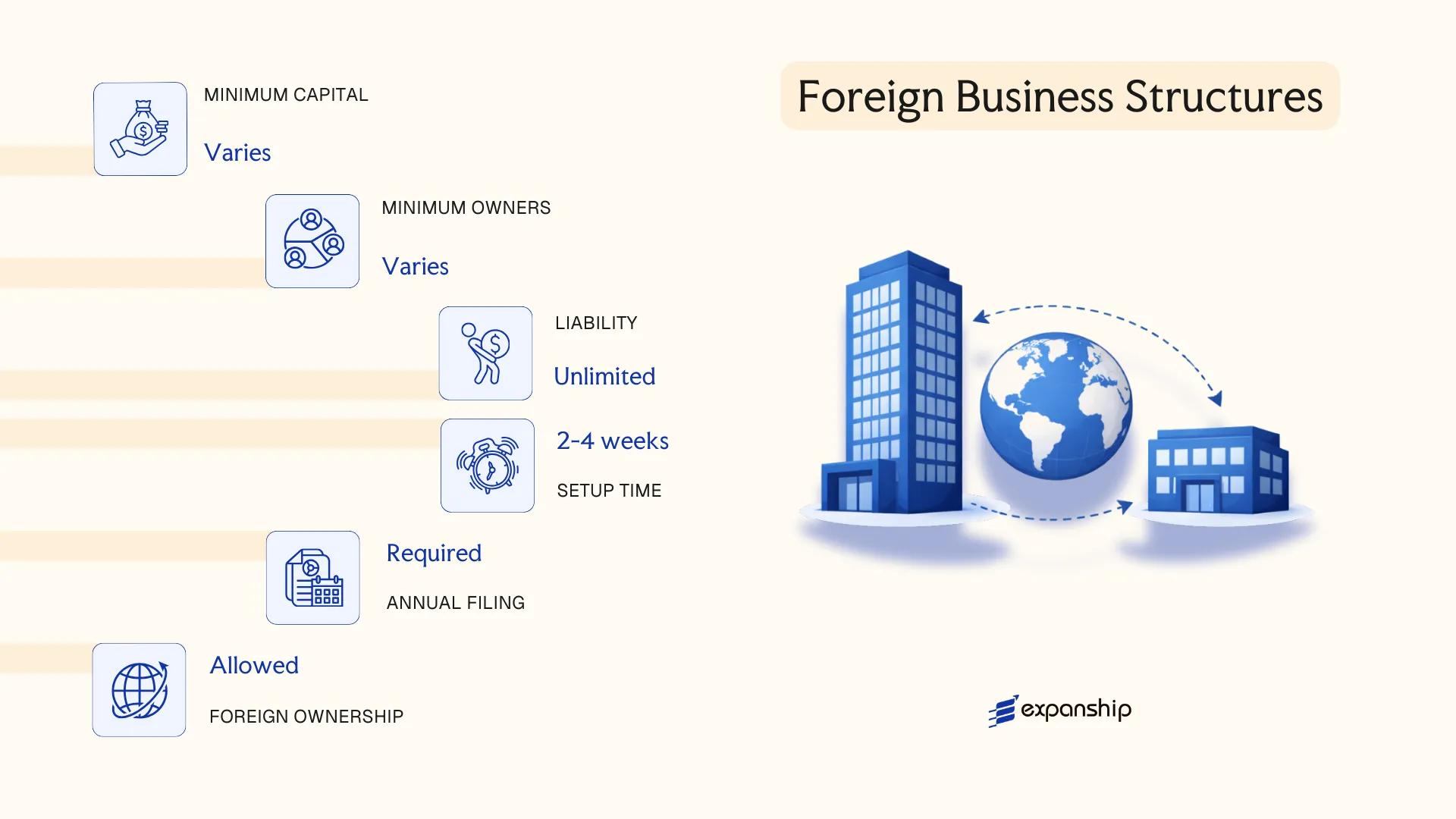

Foreign Business Structures [Branch Office, Representative Office, Subsidiary]

Registering a foreign company branch office in Singapore is governed by the Companies Act (Cap. 50), specifically Division 2 of Part 11, which outlines the requirements for foreign companies operating within the jurisdiction. Unlike a locally incorporated entity, these structures extend an overseas parent's presence into Singapore rather than creating a fully independent legal body.

Each structure carries distinct legal implications. A branch office is not a separate legal entity — it is an extension of the parent company, which remains liable for its obligations. A representative office holds no legal standing at all and cannot conduct revenue-generating activities. A subsidiary, by contrast, is incorporated as a private limited company under the Companies Act and carries its own separate legal personality.

Key Characteristics

| Requirement | Branch Office | Representative Office | Subsidiary |

|---|---|---|---|

| Legal Form | Extension of foreign parent; no separate legal personality | Temporary, non-legal administrative presence | Separate legal entity (Pte. Ltd.) |

| Registered With | ACRA | Singapore Economic Development Board (EDB) or relevant trade body | ACRA |

| Members / Officers | Minimum 1 locally resident authorised representative | Chief representative (often seconded from parent) | Min. 1 director (resident); min. 1 shareholder |

| Local Presence | Registered address in Singapore required | Registered address required | Registered office address required |

| Capital | No minimum paid-up capital requirement | No capital requirement | No statutory minimum (S$1 common) |

| Liability | Parent company bears full liability | Parent company bears full liability | Limited to the subsidiary's own assets |

Focus Points

- Taxation: Branch profits are taxed at the standard corporate rate of 17%; branches do not benefit from startup tax exemptions available to locally incorporated firms. Subsidiaries qualify for the partial tax exemption and startup exemption schemes. GST registration is required at the S$1 million taxable turnover threshold for both branches and subsidiaries.

- Duration: Representative offices are approved for an initial one-year period, renewable up to three years; they must transition to a registered business structure thereafter.

- Treaty Access: Branches and representative offices may face limitations accessing Singapore's tax treaty network, as treaty benefits typically require tax residency, which branches do not independently hold.

- Compliance: Branches must file the parent company's audited foreign financial statements with ACRA annually; subsidiaries file their own independently audited accounts.

- Conversion: A branch office can be converted to a subsidiary, but the process requires fresh incorporation rather than a direct structural conversion.

Sub-Types

Branch Office

A branch is the direct operational extension of a foreign parent and can conduct the same business activities as the parent, subject to licensing. Because the parent bears unlimited liability for the branch's obligations, this structure is less common among firms seeking liability segregation.

Representative Office

A representative office is restricted to non-transactional activities such as market research, liaison, and promotional work on behalf of the parent. It cannot sign contracts, earn income, or invoice clients — making it a purely exploratory structure.

Subsidiary

Incorporated as a private limited company, a subsidiary operates independently from its foreign parent for legal and tax purposes. This is the most widely used structure for foreign businesses seeking full operational capacity in Singapore.

A foreign subsidiary is suited to businesses seeking full operational scope and liability protection, while a branch fits firms with shorter-term commitments or those required by their parent to maintain a unified legal identity. The principal constraint of a branch or representative office is the absence of separate legal personality, which concentrates risk at the parent level.

A subsidiary is the structure of choice for foreign businesses seeking tax treaty access, liability separation, and long-term operational presence; a representative office suits early-stage market exploration with no intent to transact.

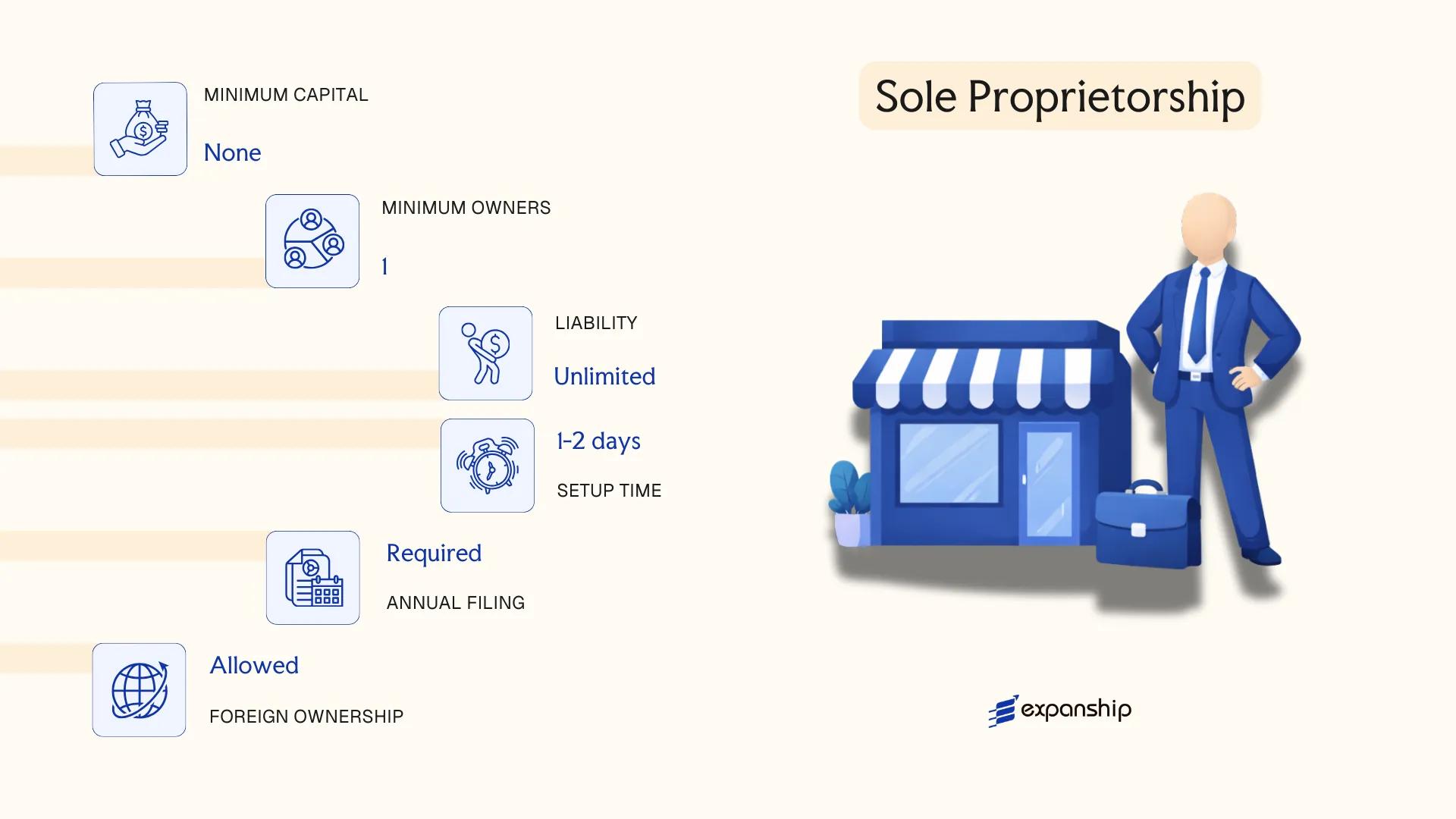

Sole Proprietorship

Sole proprietorship registration Singapore is governed by the Business Names Registration Act 2014, administered by the Accounting and Corporate Regulatory Authority (ACRA). Unlike a private limited company, a sole proprietorship carries no separate legal personality — the business and its owner are legally the same entity, meaning personal assets are fully exposed to business liabilities.

Registration is straightforward and completed through ACRA's BizFile+ portal. The business name must comply with ACRA's naming guidelines, and registration is renewable annually or every three years.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated business | No separate legal personality from the owner |

| Owner Title | Sole Proprietor | One individual only; no partners or shareholders |

| Membership | 1 proprietor (min and max) | Must be an individual, not a corporate entity |

| Local Presence | Singapore citizen, PR, or EntrePass/Employment Pass holder; local registered address required | Foreigners must appoint a locally resident authorised representative |

| Capital | No minimum capital requirement | No share structure |

| Privacy | Business name and owner details publicly accessible via BizFile+ | Limited privacy |

Focus Points

- Taxation: Income taxed as personal income at progressive rates up to 24%; not eligible for corporate tax rate or the partial tax exemption scheme available to companies. GST registration is required if annual turnover exceeds SGD 1 million.

- Annual Compliance: Registration must be renewed with ACRA; no audit requirement, but accurate business records must be maintained.

- Conversion: Can be converted to a Pte. Ltd. via ACRA's conversion process, retaining the business name subject to availability.

- Restrictions: Foreign individuals cannot register directly without an eligible pass; corporate bodies are ineligible as proprietors.

- Treaty Access: No access to Singapore's tax treaty network, as sole proprietorships are not corporate taxpayers.

Closing

A sole proprietorship suits low-risk, owner-operated businesses where administrative simplicity outweighs the need for liability protection. The primary limitation is unlimited personal liability, which creates significant financial exposure as the business scales.

Freelancers, consultants, and small traders testing a business concept before committing to formal incorporation.

How to Choose the Right Entity Type in Singapore

Knowing how to choose the right business entity in Singapore requires more than comparing registration fees — the structure you select has direct legal, tax, and operational consequences that can be difficult or costly to reverse.

Why Your Entity Choice Matters

Registering the wrong entity type creates concrete, foreseeable problems:

- A branch office conducting activities beyond its approved scope may be struck off or penalised under the Companies Act (Cap. 50).

- Selecting a Variable Capital Company for active trading rather than fund management removes access to the standard corporate tax exemption framework applicable to ordinary resident companies.

- Forming a private limited company when a trust structure would serve asset protection or estate planning locks you into mandatory annual AGM obligations, statutory filings, and shareholder requirements that do not apply to trust arrangements.

- Registering a structure without genuine local substance, where IRAS or a foreign tax authority applies economic substance tests, can trigger transfer pricing adjustments or treaty benefit denial.

Key Factors to Consider

- Business Activity: Active trading, passive asset holding, and regulated activities such as fund management each require a different licensed or registered structure under the relevant sectoral legislation.

- Tax Objectives: Your eligibility for the partial tax exemption under Section 43 of the Income Tax Act 1947, or access to Singapore's treaty network, depends on the entity type and its tax residency status.

- Ownership Structure: Single-owner operations, joint ventures, and multi-party arrangements push toward different structures — a sole proprietorship offers no liability separation, while an LLP provides it without a full corporate framework.

- Substance Capacity: If you cannot maintain a physical presence, local directors, or board meetings in the jurisdiction, certain structures will expose you to residency challenges from IRAS.

- Exit Strategy: Redomiciliation is permitted for VCCs under the Variable Capital Companies Act 2018, but not available for all entity types — confirm exit options before registering.

- Privacy Requirements: Directors and shareholders of private limited companies are disclosed on the ACRA public register; nominee arrangements are permitted but must comply with the Accounting and Corporate Regulatory Authority's beneficial ownership disclosure rules.

The full text of the Companies Act (Cap. 50) is available on the Singapore Statutes Online database.

Corporate Compliance Services in Singapore

Ongoing statutory compliance for Singapore-registered entities, including annual filings, AGM requirements, and ACRA obligations.

Conclusion

Singapore company incorporation summary points to a single consistent pattern: the Private Limited Company (Pte. Ltd.) is by far the most registered structure, favoured by resident founders and foreign investors alike for its liability protection and access to local tax incentives under the Income Tax Act 1947.

Each remaining structure serves a distinct profile. The Variable Capital Company suits fund managers requiring sub-fund segregation. Unlimited private companies fit intra-group transfers where disclosure flexibility matters. Partnerships serve professional firms or small operators with shared ownership. Branch and representative offices address foreign companies testing or extending their presence without separate legal personality. The sole proprietorship remains the simplest entry point for individual traders.

Administered by ACRA and IRAS, Singapore's regulatory framework continues to evolve through expanded tax treaty coverage and growing alignment with OECD transparency standards. Your choice of structure will determine not only your tax position but your compliance obligations from day one.

How Expanship Can Assist You

As a corporate services firm, Expanship supports Singapore incorporation from entity selection through to post-registration compliance. Whether your focus is a Private Limited Company (Pte. Ltd.) under the Companies Act, a Variable Capital Company governed by the VCC Act, or a Limited Liability Partnership registered with ACRA, the processes and obligations differ meaningfully between structures. Expanship's Singapore company formation services are built around those differences, not a generic checklist.

From document preparation to ongoing statutory filings, the scope of support includes:

- Memorandum and Articles of Association drafting and notarization

- ACRA registration and government filings

- Registered office and local resident director provision

- Post-incorporation compliance management, including annual returns

- Corporate secretarial services

- Banking introduction assistance

Reach out to Expanship Singapore to discuss your specific structure and timeline.

Frequently Asked Questions (FAQ)

The Private Limited Company (Pte. Ltd.) is the most frequently incorporated structure, registered under the Companies Act (Cap. 50) and administered by ACRA. Its combination of limited liability, separate legal personality, and eligibility for tax incentives under the Income Tax Act makes it the default choice for both resident and foreign entrepreneurs.

A Branch Office is a legal extension of its foreign parent, meaning the parent bears full liability for the branch's obligations in Singapore. A Pte. Ltd., by contrast, is a distinct legal entity; its liabilities are ring-fenced from any parent company. From a tax perspective, both are subject to the prevailing corporate tax rate, but a Pte. Ltd. may access startup exemptions unavailable to branches.

Among structures registered with ACRA, the Variable Capital Company (VCC) permits sub-fund information to be kept out of the public register, making it the most privacy-accommodating option for fund managers. Nominee director and shareholder arrangements are legally permissible across most entity types under the Companies Act, provided ultimate beneficial ownership is disclosed to ACRA per the Beneficial Ownership framework.

A sole proprietorship and a Pte. Ltd. can each be formed by one individual. Partnerships, by definition, require a minimum of two partners, whether under the Partnership Act or the Limited Liability Partnerships Act (Cap. 163A). A VCC requires a licensed fund manager rather than an individual acting alone.

Foreigners may incorporate a Pte. Ltd., establish a Branch Office, or register a VCC, provided at least one locally resident director is appointed as required under Section 145 of the Companies Act. A Representative Office does not require a local director but is restricted to non-commercial activities and must be renewed annually through the relevant lead agency. Sole proprietorships and general partnerships generally require the owner or partners to be Singapore residents.

ACRA permits conversion between certain structures; the most common path is converting a sole proprietorship or partnership into a Pte. Ltd. under the Companies Act. Direct conversion from a Branch Office to a Pte. Ltd. is not a single-step statutory process; it typically requires incorporating a new entity and transferring assets separately. A VCC cannot be converted into a standard company under the current Variable Capital Companies Act (VCA).

Not all registered structures are legally distinct from their owners. A Pte. Ltd., Public Ltd., VCC, and Limited Liability Partnership each carry separate legal personality. A sole proprietorship, general partnership, and Representative Office do not; in those cases, the owner or parent entity retains direct legal exposure for obligations incurred.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.