Key Takeaways

- Every Singapore private limited company must appoint at least one ordinarily resident director under the Companies Act, creating a structural dependency for non-resident founders who cannot satisfy this requirement personally.

- Foreign-owned entities are subject to strict beneficial ownership disclosure obligations, which add an administrative layer that companies in less transparent jurisdictions do not face.

- Sector-specific activities regulated by the Monetary Authority of Singapore require separate licensing beyond standard ACRA incorporation, meaning certain business models carry a materially higher compliance burden before they can operate lawfully.

- Corporate tax exemptions available to Singapore-resident companies are subject to eligibility thresholds and ownership conditions, so not all incorporated entities can access the headline benefits commonly associated with the jurisdiction.

Singapore operates under one of the more heavily regulated corporate frameworks in the Asia-Pacific region, with statutory obligations governed primarily by the Companies Act. Understanding the disadvantages of incorporating in Singapore requires looking beyond registration formalities into the ongoing compliance structure that governs every private limited company.

The disadvantages covered in this article span director residency rules, secretary requirements, disclosure obligations, sectoral licensing, and cost structures.

Not every business will encounter these constraints equally. A sole foreign founder operating a service firm faces a materially different compliance burden than a multi-shareholder entity seeking regulated financial activity under the Monetary Authority of Singapore.

This article is most relevant to foreign entrepreneurs, non-resident investors, and overseas holding structures considering a Singapore private limited company as their primary operating or holding entity.

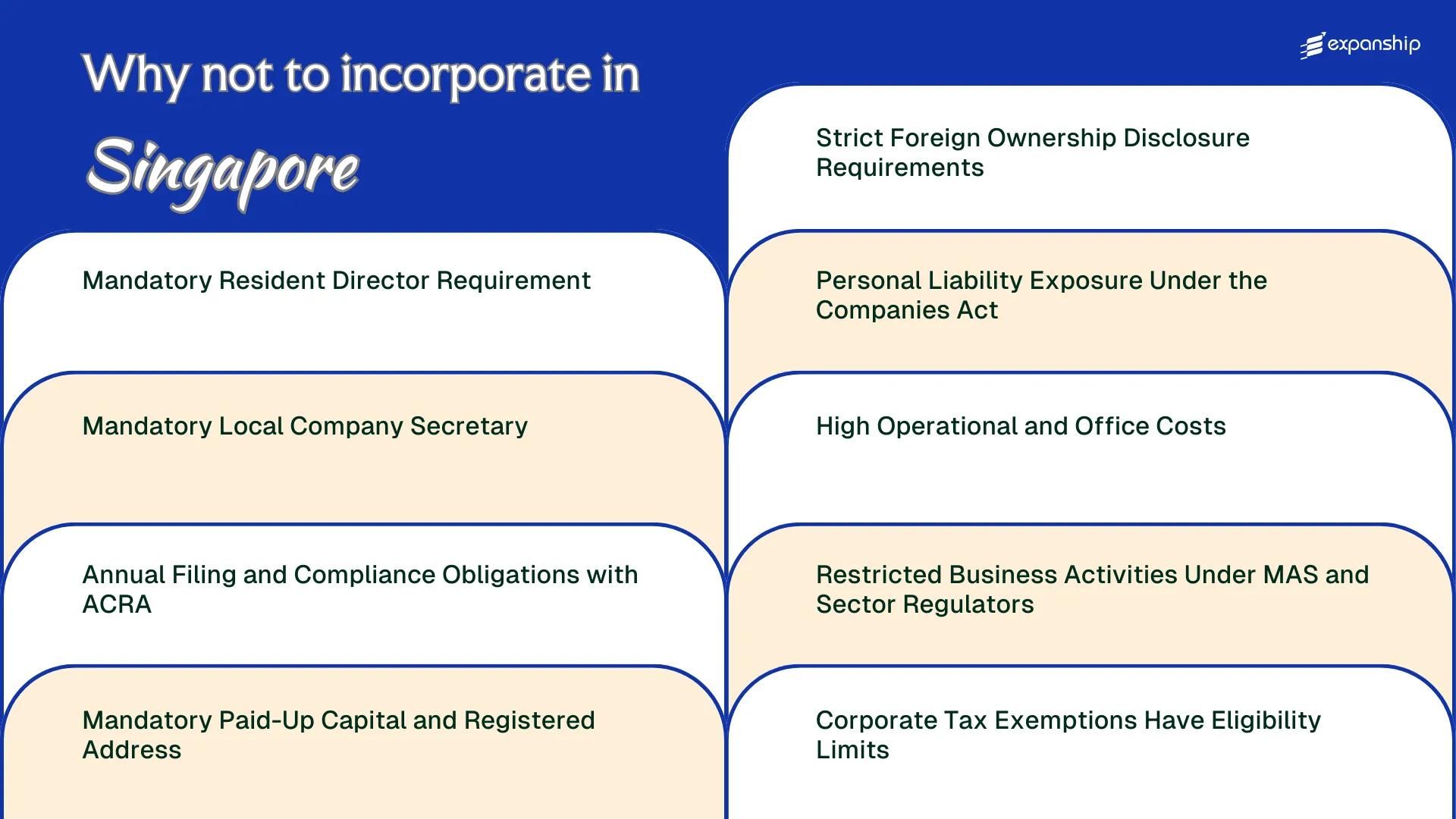

Mandatory Resident Director Requirement

Under Section 4 of the Companies Act 1967, every company incorporated in Singapore must appoint at least one director who is ordinarily resident in the country. For foreign founders who have no local ties, this Singapore resident director requirement problem surfaces immediately at the point of incorporation.

What the Obligation Actually Costs You

Satisfying this requirement typically means engaging a nominee director service, which carries an annual fee that varies by provider. This is not a one-time administrative step; it creates a recurring financial and contractual dependency on a third party whose name appears on official records filed with the Accounting and Corporate Regulatory Authority (ACRA).

That dependency introduces governance risk. If the relationship with your nominee director breaks down, your company may fall out of compliance with the mandatory local director Singapore restriction under the Companies Act until a replacement is formally appointed.

Why Foreign Owners Bear the Burden Disproportionately

Resident founders absorb this requirement at no additional cost. A foreign business owner, by contrast, must pay for a compliance function that provides no operational value to the business itself.

If your nominee director resigns without a qualified replacement already in place, ACRA records a directorial vacancy that places your company in breach of the Companies Act, exposing it to regulatory action.

Mandatory Local Company Secretary

Under Section 171 of the Companies Act, every Singapore-incorporated company must appoint a company secretary within six months of incorporation. That secretary must be a natural person ordinarily resident in the country, meaning a nominee or remote appointment from abroad does not satisfy the requirement.

For a foreign founder operating from outside Singapore, this creates a direct and recurring cost. You cannot self-appoint unless you are personally resident there, so engaging a local corporate secretarial firm becomes a fixed operational expense regardless of your company's revenue or activity level.

The practical friction this creates extends across several areas:

- You become dependent on a third party to file annual returns with ACRA, making your compliance timeline subject to another firm's workload and responsiveness.

- Any delay or error by the appointed secretary can result in penalties against your company, even though the failure is not yours.

- Switching secretaries mid-year requires a formal ACRA notification, adding administrative steps that disrupt routine compliance cycles.

- Costs for corporate secretarial services vary significantly across providers, making consistent budgeting difficult for early-stage businesses.

The ACRA company secretary obligation applies to all private limited companies without exception, including dormant entities.

Company Incorporation in Singapore

Set up your Singapore private limited company with full compliance support, including company secretary appointment and ACRA registration.

Annual Filing and Compliance Obligations with ACRA

Singapore ACRA compliance obligations create a recurring administrative burden that many foreign business owners underestimate before incorporation. Under the Companies Act (Cap. 50), every private limited company must file an annual return with the Accounting and Corporate Regulatory Authority within a prescribed period after its financial year end.

The annual return must be accompanied by financial statements prepared in accordance with the Singapore Financial Reporting Standards. For companies that are not small companies under the Act's three-criterion test, an independent audit is also mandatory, adding professional fees on top of filing costs.

| Obligation | Requirement | Implication for Foreign Owner |

|---|---|---|

| Annual Return Filing | Within 7 months of financial year end | Missed deadline triggers penalties from S$300 upward |

| Financial Statements | SFRS-compliant accounts required | Requires qualified accountant; not a DIY process |

| Statutory Audit | Mandatory if company fails small company test | Additional audit fees typically S$3,000–S$10,000+ annually |

| AGM Requirement | Private companies may dispense with AGM but must circulate financials | Directors abroad must still coordinate and sign off |

Even firms that qualify as small companies and avoid the audit requirement must still prepare full financial statements and maintain proper accounting records throughout the year. The exemption reduces one cost but does not remove the structural reporting obligation.

Coordinating these filings from overseas adds a layer of difficulty. Your appointed company secretary bears some responsibility, but ultimate legal accountability under the Companies Act remains with the directors, who may face personal penalties for non-compliance.

Mandatory Paid-Up Capital and Registered Address

Singapore paid-up capital requirements impose no statutory minimum for private limited companies under the Companies Act (Cap. 50). Most incorporations proceed with SGD 1 in paid-up capital. That flexibility sounds straightforward, but it creates a practical trap: certain business licences, government tenders, and sector regulators require proof of adequate capitalisation before granting approvals, meaning your SGD 1 company may face immediate disqualification from regulated activities.

Financial institutions, MAS-licensed entities, and specific trade bodies each set their own internal capital thresholds. A foreign owner who incorporates without accounting for downstream licensing requirements will encounter delays and additional costs when those thresholds cannot be met quickly.

Every Singapore-incorporated company must also maintain a registered office accessible during business hours under Section 142 of the Companies Act. Using a virtual address is common, but the registered office must be capable of receiving statutory correspondence and ACRA notices. If your address provider fails that obligation, your company bears the compliance risk directly.

- Paid-up capital of SGD 1 is legally sufficient but may disqualify your firm from licences requiring minimum capitalisation

- MAS and sector regulators set their own capital adequacy thresholds independently of ACRA

- The registered office must be operational and accessible during standard business hours

- ACRA must be notified within 14 days of any change to the registered office address

- A P.O. box address does not satisfy the registered office requirement under the Companies Act

Despite having no minimum paid-up capital requirement, Singapore banks routinely decline to open corporate accounts for entities capitalised below SGD 50,000, creating an informal threshold that the law itself does not impose.

Strict Foreign Ownership Disclosure Requirements

Singapore foreign ownership disclosure restrictions are among the more demanding in Southeast Asia, governed primarily by the Companies Act 1967 and reinforced through ACRA's registry framework. Any foreign investor holding shares in a Singapore-incorporated entity must understand that transparency obligations extend well beyond simple shareholding records.

Scope of the Disclosure Obligation

Under the Register of Registrable Controllers (RORC) requirements introduced in 2017, companies must identify and record individuals who ultimately own or control more than 25% of shares or voting rights. This register must be maintained and, in most cases, filed with ACRA, meaning beneficial ownership information becomes accessible to public authorities rather than remaining a private internal record.

Practical Burden on Foreign Shareholders

For foreign investors accustomed to jurisdictions with lighter disclosure thresholds or nominee arrangements that obscure ultimate ownership, the Singapore company shareholder disclosure obligations create meaningful structural constraints. Multi-layered holding structures that span several jurisdictions may require disclosure at each ownership tier, multiplying the compliance effort and legal cost for the foreign shareholder.

Foreign shareholder transparency rules in Singapore also apply to changes in controller status, requiring updates within prescribed timeframes. Failure to maintain an accurate RORC carries penalties under the Companies Act, placing the compliance burden directly on the entity and its officers.

Managing Ownership Disclosure Requirements in Singapore

Understand how Singapore's beneficial ownership framework applies to your shareholding structure and what it means for your compliance obligations.

Personal Liability Exposure Under the Companies Act

Personal liability risks under the Singapore Companies Act extend well beyond what many foreign founders anticipate before incorporating. Directors cannot treat the corporate structure as an automatic shield against personal exposure.

- Under Sections 157 and 199 of the Companies Act, directors who breach their duty of care or fail to maintain proper accounting records can be held personally liable, exposing your personal assets to civil claims.

- Insolvent trading provisions hold directors personally accountable for debts incurred when the company was unable to pay them, removing the protection of limited liability at the moment it is most needed.

- ACRA can disqualify directors who fail to meet statutory obligations, barring them from acting in any directorial capacity across all Singapore-registered entities.

- Nominee directors bear the same legal duties as executive directors under the Act, meaning liability does not diminish simply because a director holds the role in name only.

High Operational and Office Costs

High operational costs Singapore incorporation presents are not incidental — they reflect the city-state's position as one of the most expensive commercial real estate markets in Asia-Pacific. For a foreign-owned private limited company, the overhead of maintaining a physical or registered office presence can strain early-stage cash flow significantly.

Grade A office space in the Central Business District consistently ranks among the highest-priced in the region. Even co-working memberships or serviced office arrangements used to satisfy the registered address requirement under the Companies Act 1967 carry recurring monthly fees that accumulate across a financial year.

Beyond rent, employment costs compound the burden. The CPF (Central Provident Fund) contribution framework requires employers to contribute up to 17% of an eligible employee's monthly wages, which raises the effective cost of each local hire above the nominal salary figure.

- Utility and facilities costs in commercial districts are priced at market rates with no regulatory cap for businesses.

- Professional employer organisation (PEO) arrangements, sometimes used to avoid direct hiring, carry their own management fees.

- Foreign staff relocation and Employment Pass application fees add further setup expenditure from day one.

A hypothetical scenario: A foreign-incorporated startup leasing a modest serviced office in Tanjong Pagar at SGD 1,200/month, hiring two local employees at SGD 4,000 each, and engaging a corporate secretary and registered agent would face fixed monthly overhead exceeding SGD 10,000 before any operational activity begins. This figure excludes MAS-regulated licensing costs if the business falls under a controlled sector.

Restricted Business Activities Under MAS and Sector Regulators

MAS restricted business activities in Singapore cover a wide range of financial and quasi-financial functions. Under the Securities and Futures Act 2001 (SFA) and the Financial Advisers Act 2001 (FAA), any entity dealing in capital markets products, providing financial advisory services, or operating a payment system must obtain the relevant MAS licence before commencing operations. For a foreign-founded company, this licensing process adds cost, time, and a compliance infrastructure that many early-stage businesses are not equipped to support.

Sector-specific restrictions extend beyond MAS. Activities in banking, insurance, telecommunications, and broadcasting are governed by separate regulators — the Monetary Authority, the Info-communications Media Development Authority (IMDA), and others — each with their own fit-and-proper assessments and capital adequacy conditions.

Regulated activities that commonly require prior approval include:

- Payment services under the Payment Services Act 2019

- Fund management and capital markets services under the SFA

- Insurance broking under the Insurance Act 1966

- Broadcasting and media operations under the Broadcasting Act 1994

Obtaining even a single licence can take several months, and MAS routinely requires applicants to demonstrate local operational substance, not just a registered address.

If your business model involves any payment, lending, or investment activity, operating without the applicable MAS or sector regulator licence exposes your company to criminal penalties under Singapore law, regardless of where the ultimate customers or transactions are located.

Corporate Tax Exemptions Have Eligibility Limits

Singapore corporate tax exemption eligibility limits are a structural constraint that can catch foreign founders off guard. The Start-Up Tax Exemption (SUTE) scheme exempts 75% of the first S$100,000 of chargeable income and 50% of the next S$100,000, but only for the first three consecutive years of assessment.

Beyond that window, the firm transitions to the Partial Tax Exemption (PTE) scheme, which offers lower relief thresholds. This means early-stage businesses that take longer to generate profit may exhaust the scheme before fully benefiting from it.

SUTE scheme eligibility drawbacks extend further. Companies where corporate shareholders hold 10% or more of the ordinary shares are excluded from qualifying, a restriction that directly affects foreign-owned entities structured with a parent company as the shareholder.

Investment holding companies are also ineligible, regardless of their incorporation date. For foreign investors using Singapore as a holding structure, this exclusion removes the exemption entirely.

Ways to Overcome These Challenges

Overcoming Singapore incorporation challenges requires structural planning before the entity is registered, not after problems arise.

- Appoint a locally resident director who meets the criteria under Section 145 of the Companies Act before submitting your incorporation application to ACRA.

- Engage a qualified company secretary within six months of incorporation, as required under Section 171 of the Companies Act.

- Register a physical or virtual office address in Singapore that satisfies ACRA's registered address requirements under the Companies Act.

- Identify whether your intended business activity falls under MAS licensing requirements or any sector-specific regulatory regime prior to incorporation.

- Confirm your company's eligibility for the Start-Up Tax Exemption scheme against the qualifying conditions set by the Inland Revenue Authority of Singapore.

- Submit your beneficial ownership information accurately to ACRA's Bizfile portal to satisfy foreign ownership disclosure obligations.

Each of these steps corresponds directly to obligations imposed under Singapore's Companies Act or sector-specific regulations. Addressing them at the formation stage reduces the risk of non-compliance penalties or structural restructuring later.

Singapore Still a Strong Business Destination

Singapore's compliance requirements, disclosure obligations, and cost base are real constraints that affect foreign-owned companies. Weighed against them, the jurisdiction offers a stable legal system under the Companies Act (Cap. 50), a territorial tax regime administered by IRAS, and a well-functioning regulatory environment overseen by ACRA and MAS. For businesses whose structure and activities align with these conditions, Singapore business destination despite drawbacks remains a credible assessment.

| Pros | Cons |

|---|---|

| Corporate tax rate of 17% with partial exemptions available to qualifying new and existing companies | Tax exemption schemes carry eligibility limits that exclude many foreign-owned or revenue-generating entities |

| ACRA's online filing system supports efficient annual return and financial statement submission | Ongoing ACRA filing obligations create recurring administrative and cost burdens |

| A private limited company (Pte. Ltd.) limits shareholder liability under the Companies Act | Directors can face personal liability for insolvent trading and statutory breaches |

| Singapore's open foreign ownership policy allows 100% foreign shareholding | Full beneficial ownership disclosure is mandatory under the Register of Registrable Controllers |

| Established financial and professional services sector supports business operations | Office space and operational costs rank among the highest in the Asia-Pacific region |

Satisfying the resident director requirement and maintaining a registered local address adds a layer of structural obligation that purely offshore jurisdictions do not impose. Whether that trade-off suits your business depends on what the Singapore framework actually delivers in return.

Compliance Services for Companies in Singapore

Understand your ongoing obligations under the Companies Act, ACRA filing requirements, and Singapore's regulatory framework.

Conclusion

Singapore's overall position as a business destination remains well-established, yet the Singapore incorporation disadvantages summary presented across this blog reflects real structural obligations that affect incorporated entities. The resident director requirement under the Companies Act, the disclosure obligations tied to beneficial ownership, and the sector-specific licensing conditions imposed by the Monetary Authority of Singapore each carry compliance weight that demands ongoing attention. For some business models, these aren't minor friction points. Knowing where your structure may fall short is the first step toward building one that holds.

Expanship's Singapore Incorporation Services

Expanship's Singapore incorporation services are designed to reduce the operational weight of the compliance requirements covered throughout this blog — from satisfying ACRA's annual filing obligations to meeting the resident director and company secretary mandates under the Companies Act 1967. Your business still carries those obligations; Expanship helps you manage them without building an internal compliance function from scratch.

Beyond initial registration, the firm supports the full lifecycle of a Singapore entity:

- Preparing incorporation documents and filing your company registration with ACRA

- Providing a registered office address and acting as your local registered agent

- Handling government filings and liaising directly with ACRA and relevant sector regulators

- Managing ongoing post-incorporation compliance, including annual returns and statutory updates

- Facilitating introductions to banking institutions for corporate account opening

- Registering your entity for tax purposes and coordinating with IRAS on applicable filings

Reach out to Expanship Singapore to discuss your incorporation requirements.

Frequently Asked Questions (FAQ)

Yes, every company incorporated in Singapore, regardless of revenue or headcount, must appoint a qualified company secretary within six months of incorporation under the Companies Act. The secretary must be a natural person ordinarily resident in Singapore, so a foreign individual based abroad cannot fill this role remotely. Failing to maintain this appointment is a breach of the Act and can result in penalties for both the company and its directors.

ACRA imposes financial penalties for late or missed filings, and persistent non-compliance can result in the company being struck off the register. Directors who repeatedly fail to meet filing obligations under the Companies Act may face personal fines and, in serious cases, disqualification from holding directorships. The penalties escalate with the duration of the default, so a missed deadline does not remain a flat-fee issue.

At a minimum, you will pay for a registered office address, a nominee director, and a company secretary, which collectively can cost several thousand Singapore dollars annually before accounting for accounting, audit, or tax filing fees. If your business falls outside the audit exemption threshold, statutory audit costs add a further significant layer of expense. For a lean foreign-owned entity with minimal Singapore operations, these fixed compliance costs can be disproportionate relative to early-stage revenue.

Singapore requires full disclosure of beneficial owners through the Register of Registrable Controllers, which must be maintained by the company and, in most cases, filed with ACRA. This goes beyond what several offshore jurisdictions require and means there is no meaningful layer of ownership privacy available to foreign investors. For businesses where confidentiality of shareholding is a commercial priority, this transparency obligation is a material constraint.

A company that loses its registered address, for example because a service provider relationship lapses, is immediately in breach of the Companies Act and must rectify the situation without delay. While the minimum paid-up capital of SGD 1 is nominal, the registered address obligation is ongoing and non-negotiable; ACRA can initiate action against a company that cannot demonstrate a valid local address. Directors bear responsibility for ensuring these requirements are continuously met, not just at the point of incorporation.

Only if the business activity falls entirely outside a regulated sector. If your company conducts any activity that MAS classifies as a financial service, or operates in areas overseen by bodies such as the Ministry of Health or the Info-communications Media Development Authority, a separate licence or approval is required before commencing operations. Incorporating the entity with ACRA does not grant any permission to operate in a regulated sector, and operating without the relevant licence carries criminal liability under the applicable sectoral legislation.

No. The scheme excludes companies where 50% or more of shares are held by corporate shareholders, which immediately disqualifies many foreign holding-company structures. A qualifying company must also be a tax resident of Singapore and must not be engaged in property development or investment holding as its principal activity. This means a significant portion of foreign-owned entities established for holding or property purposes will not benefit from the exemptions that are often cited as a reason to incorporate in Singapore.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.