Key Takeaways

- Singapore's 17% headline corporate tax rate, combined with the partial tax exemption framework available to qualifying companies, allows foreign-owned entities to operate at an effective tax burden materially below that headline figure during early years of operation.

- With over 90 double tax agreements in force and no capital gains tax chargeable under the Income Tax Act 1947, the combined tax position available to a Singapore-incorporated entity is stronger than in most comparable regional jurisdictions.

- ACRA's fully digital registration system reduces the time required to incorporate a private limited company to as little as one to three business days, removing a practical barrier that slows market entry in many other jurisdictions.

- Entities incorporated in Singapore gain access to MAS-regulated financial infrastructure and government support mechanisms such as the Enterprise Development Grant administered by EnterpriseSG, broadening both operational capability and funding options depending on entity type and industry.

Singapore is an independent city-state in Southeast Asia, governed under a Westminster-style parliamentary system with a legal framework derived from English common law. Foreign businesses incorporating here most commonly do so through a private limited company. Company registration is administered by the Accounting and Corporate Regulatory Authority, which also oversees ongoing compliance obligations for all locally registered entities.

The country operates a territorial tax system, meaning tax is generally levied on income sourced within its borders rather than on worldwide earnings. Foreign ownership is broadly permitted across most sectors, with few restrictions on foreigners holding full equity in a locally incorporated firm — making it accessible to international investors without requiring local partnership arrangements.

This article covers the key advantages of incorporating a business here, drawing on the specific regulatory, financial, and operational conditions that define the environment for foreign companies setting up in the jurisdiction.

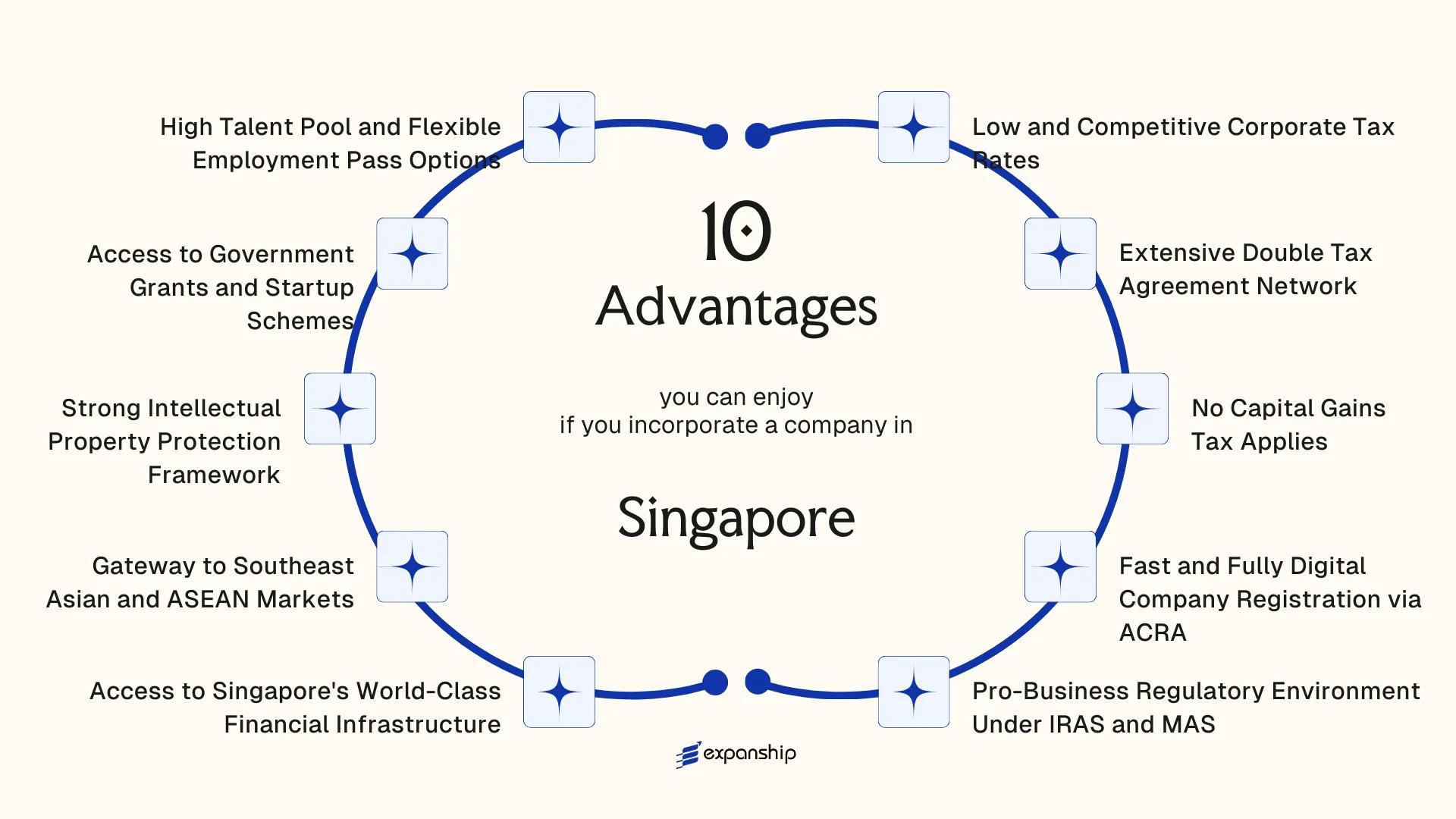

Low and Competitive Corporate Tax Rates

Singapore's low corporate tax rate benefits foreign businesses through a flat headline rate of 17%, applied to chargeable income under the Income Tax Act 1947. This rate sits well below the OECD average of approximately 23%, producing a measurable cost advantage for incorporated entities.

Partial Tax Exemptions for New Companies

Under the Inland Revenue Authority of Singapore's startup tax exemption scheme, newly incorporated companies that meet qualifying conditions pay 0% on the first SGD 100,000 of chargeable income and 8.5% on the next SGD 100,000 in their first three years of assessment. This structure means an early-stage business retains significantly more capital during the period when cash flow matters most.

Effective Tax Rates Below the Headline Figure

The partial exemption framework means your firm's effective tax rate can fall considerably below 17% during those initial years. Beyond the startup window, a partial tax exemption for companies continues to apply, keeping the effective burden lower than the statutory rate suggests for qualifying resident entities.

Your company's effective tax rate in the first three years can be substantially lower than the 17% headline rate under IRAS's startup exemption framework.

Extensive Double Tax Agreement Network

Singapore's double tax agreement network benefits businesses by eliminating one of the most persistent costs in cross-border operations: being taxed twice on the same income. With over 90 comprehensive DTAs in force, income earned by a Singapore-resident company from treaty partners is either exempt from withholding tax at source or taxed at a reduced rate. This directly increases the after-tax return on international transactions.

Under the Income Tax Act 1947, IRAS administers double taxation relief through either full exemption or a tax credit mechanism. For a foreign investor structuring regional operations through a Singapore entity, this means dividend remittances, royalty payments, and service fees flowing from treaty countries carry significantly lower withholding costs than they would through a non-treaty jurisdiction.

The treaty network spans key trading partners including China, India, the United States, the United Kingdom, Germany, Japan, and most ASEAN economies. This geographic coverage matters because it reduces friction in the most commercially active corridors your business is likely to use.

Treaty access is conditional on your entity meeting the residency requirements under the relevant agreement, which typically requires demonstrable substance in Singapore rather than a shell arrangement.

Several practical features make this network particularly accessible:

- Treaty benefits apply automatically through IRAS's existing tax credit framework, without requiring separate approval processes for each transaction

- Most agreements include provisions on permanent establishment, which gives your business clarity on when overseas activity creates a taxable presence

- The network includes emerging markets where withholding tax rates can otherwise reach 20% or higher, making treaty access financially material

- Treaty provisions are backed by IRAS's published guidance, reducing interpretive uncertainty when applying reduced rates

Incorporate Your Company in Singapore

Set up a Singapore-resident company and access one of the world's most extensive double tax agreement networks through a straightforward incorporation process.

No Capital Gains Tax Applies

No capital gains tax in Singapore advantage sits at the center of why many foreign investors structure exits, asset disposals, and investment holdings through a Singapore-incorporated entity. Under the Income Tax Act 1947, there is no statutory provision that taxes capital gains, meaning profits derived from the sale of shares, securities, or capital assets are not subject to tax at the corporate level.

The practical implication is significant. When your company disposes of a subsidiary, exits a shareholding, or sells an asset classified as capital in nature, the proceeds are not included in taxable income under the Inland Revenue Authority of Singapore (IRAS) framework.

| Asset Type | Tax Treatment | Governing Framework |

|---|---|---|

| Sale of shares in subsidiary | Not taxable if capital in nature | Income Tax Act 1947 |

| Disposal of investment property | Determined by capital vs. income intent | IRAS income/capital distinction |

| Intellectual property sale | May be taxable if part of trade | Case-by-case IRAS assessment |

| Securities held for investment | Not taxable if not held as trading stock | IRAS administrative guidance |

The distinction between capital and income receipts is determined by IRAS based on factors including holding period, frequency of transactions, and the original intent behind acquiring the asset. A firm that holds shares as a long-term investment rather than as trading stock will generally see disposal proceeds treated as non-taxable capital receipts. This classification-based approach gives your business a degree of planning certainty that purely rate-based systems do not always provide.

Fast and Fully Digital Company Registration via ACRA

Singapore ACRA digital company registration benefits are visible from the moment you begin the incorporation process. Registration is handled through BizFile+, the Accounting and Corporate Regulatory Authority's online portal, which allows you to incorporate a private limited company without visiting any office or submitting paper documents.

Most incorporations are approved within 1 to 3 working days. Where the application requires no referral to an external agency for name approval, same-day approval is common. For a foreign business owner, this means your entity can be legally operational within days of deciding to enter the market.

The entire process is conducted digitally under the Companies Act (Cap. 50), which governs the formation and administration of business entities registered in the jurisdiction. Directors and shareholders are not required to be physically present; a registered filing agent can submit the incorporation application on your behalf.

Keep these points in mind:

- A local registered address is required at incorporation

- At least one director must be ordinarily resident in Singapore

- A company secretary must be appointed within 6 months of incorporation

- Foreign nationals cannot file directly through BizFile+ without using an ACRA-registered filing agent

Singapore does not require a minimum paid-up capital above S$1 to incorporate a private limited company, meaning your entity can be legally formed with a nominal share value on day one.

Pro-Business Regulatory Environment Under IRAS and MAS

Singapore's pro-business regulatory environment advantages are most visible in how its two principal regulators, the Inland Revenue Authority of Singapore (IRAS) and the Monetary Authority of Singapore (MAS), operate with a mandate to facilitate business rather than obstruct it. Both bodies publish detailed guidance, binding rulings, and advance determination processes that give your entity predictability before it commits to a structure or transaction.

IRAS and Tax Certainty for Foreign-Owned Entities

IRAS offers an advance ruling system under Section 108 of the Income Tax Act 1947, allowing a company to obtain a binding written ruling on how a specific provision of tax law applies to a contemplated transaction. For a foreign business owner structuring an entry into the region, this removes ambiguity at the planning stage rather than at the audit stage. Rulings are legally binding on IRAS for the period specified, which gives your business a concrete planning baseline.

MAS and Financial Regulatory Accessibility

MAS operates a licensing framework that includes a regulatory sandbox under the FinTech Regulatory Sandbox Guidelines, permitting firms to test financial products in a live environment under relaxed legal requirements for a defined period. This is codified under MAS's supervisory framework and is available to both locally incorporated and foreign-founded entities that meet eligibility criteria. Beyond fintech, MAS's published licensing timelines and accessible pre-application consultation process reduce uncertainty for firms entering regulated financial activities.

Understand the Full Regulatory Advantages Before You Incorporate in Singapore

Speak with an Expanship specialist to map out how IRAS rulings and MAS frameworks apply to your specific business structure.

Access to Singapore's World-Class Financial Infrastructure

Singapore's financial infrastructure benefits for businesses stem from a combination of institutional depth, regulatory clarity, and direct access to capital that few jurisdictions outside major financial centres can match.

- The Monetary Authority of Singapore (MAS) functions as both the central bank and integrated financial regulator, meaning firms deal with a single supervisory body rather than a fragmented multi-agency system. For a foreign business, this reduces administrative friction when opening accounts, seeking licenses, or accessing financial services.

- Singapore hosts over 200 banks, including the regional headquarters of major global institutions. Your company gains access to multi-currency accounts, trade finance facilities, and sophisticated treasury services that are essential for cross-border operations.

- MAS has issued frameworks for digital payment tokens and electronic money under the Payment Services Act 2019, making Singapore one of the few jurisdictions with a clear legal basis for fintech and digital asset businesses to operate.

- The city-state's position as a foreign exchange trading hub, consistently ranked among the top five globally by the Bank for International Settlements, means your treasury operations benefit from high liquidity and tight spreads.

- Corporate entities incorporated under the Companies Act can open multi-currency business accounts locally, which is particularly valuable for firms managing revenue streams across multiple ASEAN markets.

Gateway to Southeast Asian and ASEAN Markets

Singapore's position as a gateway to ASEAN markets is structural, not incidental. The city-state sits at the geographic center of a trade bloc comprising ten member states with a combined GDP exceeding USD 3.6 trillion and a population of over 680 million. For a foreign business incorporating here, that proximity translates into logistical and commercial reach that would otherwise require multiple regional entities.

Under the ASEAN Free Trade Area (AFTA) framework and the ASEAN Trade in Goods Agreement (ATIGA), goods traded between member states benefit from significantly reduced or zero tariff rates. A firm registered here can use its Singapore entity as the operational anchor for regional distribution, without establishing separate legal presences across every target market.

Beyond goods, the ASEAN Framework Agreement on Services (AFAS) and bilateral agreements with major economies including the United States, EU, China, and India extend preferential market access to Singaporean-registered entities.

A company incorporated in Singapore and exporting to ASEAN markets under ATIGA preferential tariff rates can access duty reductions on thousands of product lines across member states, compared to the standard MFN tariff rates that a non-ASEAN-based entity would face.

Strong Intellectual Property Protection Framework

Singapore intellectual property protection benefits are grounded in a statutory regime that aligns with the major international conventions, including the Paris Convention, the Berne Convention, and the Patent Cooperation Treaty. Your IP rights are enforceable from the moment of registration, and the legal framework covering patents, trademarks, and copyrights is administered by the Intellectual Property Office of Singapore (IPOS).

Patents registered through IPOS grant exclusive rights for up to 20 years. Trademarks can be renewed indefinitely in ten-year intervals, giving your brand long-term territorial protection within a jurisdiction that actively enforces IP rights through its civil courts.

For businesses holding significant intangible assets, the IP Development Incentive scheme allows qualifying income derived from patents and copyrighted software to be taxed at a concessionary rate, subject to IPOS approval and nexus requirements under the modified nexus approach.

- Foreign-owned entities can register IP directly under Singapore law without a local partner requirement.

- IPOS offers a Fast Track examination route for patents, reducing examination timelines significantly.

- Singapore is a signatory to the Madrid Protocol, allowing trademark protection to be extended internationally from a single application filed locally.

The concessionary IP tax rate under the IP Development Incentive applies only to qualifying IP income and requires pre-approval from IPOS; it does not apply automatically upon registration.

Access to Government Grants and Startup Schemes

Singapore government grants benefits for startups are administered through Enterprise Singapore (EnterpriseSG), a statutory board under the Ministry of Trade and Industry. These programs are structured to reduce early-stage capital risk, which means a foreign founder can offset a meaningful portion of qualifying expenditure through public funding rather than equity dilution or debt.

Startup SG Founder Grant

Administered by EnterpriseSG, Startup SG Founder provides first-time entrepreneurs with a capital grant of SGD 50,000, subject to a SGD 10,000 co-investment requirement from the applicant. Your business must be incorporated in Singapore and mentored by an Accredited Mentor Partner (AMP) to qualify. That mentorship condition is not merely administrative; it connects your company to local networks, distribution channels, and institutional knowledge that foreign founders would otherwise spend years building.

Enterprise Development Grant

The Enterprise Development Grant (EDG) supports projects across three pillars: core capabilities, innovation and productivity, and market access. Qualifying firms can receive funding support covering up to 50% of eligible project costs, with higher support levels available for smaller enterprises. For a foreign-owned company pursuing regional expansion or process automation, this grant directly subsidises activity that would otherwise sit entirely on the company's balance sheet.

Additional Schemes Worth Noting

- Startup SG Tech funds proof-of-concept and proof-of-value projects in proprietary technology

- Startup SG Equity co-invests with institutional investors in deep-tech companies

- Market Readiness Assistance (MRA) Grant offsets costs related to overseas market entry, including market assessments and business development

High Talent Pool and Flexible Employment Pass Options

Singapore Employment Pass benefits for businesses extend directly into your ability to hire and retain qualified foreign professionals without the structural barriers common in other developed economies.

The Employment Pass (EP) is issued by the Ministry of Manpower (MOM) and targets foreign professionals, managers, and executives earning above a qualifying salary threshold, which MOM adjusts periodically based on market benchmarks. Because the EP is employer-sponsored rather than tied to a quota system, your firm can hire based on role requirements rather than nationality caps. This makes workforce planning more predictable for foreign-owned entities expanding into Asia.

Entrepreneurs who intend to found and operate a business personally can apply for the EntrePass, a separate scheme administered by MOM designed for foreign startup founders. EntrePass eligibility is linked to business innovation criteria and funding or incubation status, meaning the scheme filters for commercially viable ventures rather than functioning as a general work authorization route.

For businesses that need to bring in senior specialists for fixed periods, the Personalised Employment Pass (PEP) offers additional flexibility. Unlike the standard EP, the PEP is not tied to a specific employer, allowing high-earning professionals to switch roles without reapplying for a new pass.

Key structural features relevant to employers:

- EP holders can be sponsored across multiple industries without sector-specific licensing under MOM's general framework

- MOM's Fair Consideration Framework requires firms to advertise roles on MyCareersFuture before filing EP applications, applying only to companies with 25 or more employees

- EntrePass holders can bring in additional foreign employees under a dependency ratio tied to local headcount

Why Singapore Stands Out Against Other Business Hubs

Comparing Singapore's incorporation profile against its closest regional competitors, Hong Kong and the British Virgin Islands (BVI), reflects what many founders and CFOs actually face when shortlisting jurisdictions. Hong Kong targets a similar international investor base and shares a common-law legal foundation, while BVI attracts offshore holding structures. Where the comparison becomes meaningful is in tax treaty access, regulatory transparency, and the ability to conduct substantive operations without triggering redomiciliation concerns.

Singapore's 80-plus tax treaties give incorporated entities treaty-resident status that BVI structures cannot access, since BVI does not operate as a treaty jurisdiction. Against Hong Kong, the distinction is less binary but still material: while both jurisdictions offer competitive profits tax rates, Singapore's 17% headline corporate tax rate applies alongside a territorial system, a 9% effective rate for the first SGD 300,000 in chargeable income, and no dividend withholding tax on outbound distributions. For businesses running regional operations from a single incorporated entity, these parameters affect structuring decisions directly.

| Parameter | Singapore | Hong Kong | BVI |

|---|---|---|---|

| Corporate Tax Rate | 17% (headline) | 16.5% (headline) | 0% (no local tax) |

| Tax Treaty Network | 80+ DTAs | 45+ CDTAs | None |

| Capital Gains Tax | None | None | None |

| Dividend Withholding Tax | None | None | None |

| Regulatory Oversight Body | ACRA / MAS / IRAS | CR / IRD / SFC | BVI FSC |

| Substance Requirements | Required for treaty benefits | Required for treaty benefits | Applies under BOSS Act |

| FATF Status | Member (compliant) | Member (compliant) | Non-member (monitored) |

| Regional Market Access (ASEAN) | Direct member | Observer status | No access |

Compliance Services for Companies in Singapore

Stay aligned with ACRA, IRAS, and MAS requirements. Expanship manages your ongoing statutory obligations so your Singapore entity remains in good standing.

Conclusion

Singapore's position as a corporate domicile rests on a combination of structural features that are difficult to replicate elsewhere in the region. A 17% headline corporate tax rate, reinforced by the partial tax exemption framework for qualifying companies, means your effective tax burden can fall well below that headline figure in the early years of operation. Pair that with over 90 double tax agreements and the absence of capital gains tax under the Income Tax Act 1947, and the overall tax position for a foreign-owned entity becomes materially stronger than in most comparable jurisdictions.

Beyond tax, the benefits of incorporating in Singapore extend to operational fundamentals. ACRA's fully digital incorporation system allows a private limited company to be registered within one to three business days, and MAS-regulated financial infrastructure gives incorporated entities direct access to one of Asia's most developed banking and payments ecosystems.

Your specific industry, ownership structure, and target markets will determine how much weight each of these factors carries for your business. A holding company with passive income has a different calculus than a regional sales entity or a startup seeking Enterprise Development Grant support through EnterpriseSG. The framework accommodates a wide range of structures, but the fit is not automatic.

Understanding which incentives apply to your entity type, and which conditions must be met to access them, is the practical work that follows the decision to incorporate.

Start Your Singapore Company with Expanship Today

Incorporating in Singapore with Expanship means your business receives structured support across every stage of the process governed by the Accounting and Corporate Regulatory Authority (ACRA). From selecting the appropriate entity type, whether a Private Limited Company, Variable Capital Company, or Branch Office, to managing the annual filing obligations these structures carry, Expanship coordinates each requirement directly with the relevant authorities.

Working with Expanship as your Singapore company formation services partner, you receive assistance across the following:

- Company name reservation and ACRA BizFile+ incorporation filing

- Preparation and legalization of constitutional documents, including the company constitution

- Registered office address and resident company secretary provision, as required under the Companies Act

- Ongoing compliance management covering annual returns, AGM requirements, and IRAS tax filings

- Government liaison and corporate secretarial support throughout the entity's operational life

- Introduction to banking partners for corporate account establishment

For foreign investors setting up a Singapore company with a corporate services firm, having a single point of coordination for ACRA registration, IRAS correspondence, and post-incorporation obligations reduces administrative exposure and keeps your entity in good standing from day one.

Reach out to Expanship Singapore to discuss your incorporation requirements.

Frequently Asked Questions (FAQ)

For most applications, ACRA processes incorporation within one to three business days once all documents are submitted through the BizFile+ portal. Applications flagged for additional review by a referring agency, such as MAS or the Ministry of Education, take longer and timelines vary by case. Name reservation is a separate step and is valid for 120 days.

The headline corporate tax rate is 17%, applied to chargeable income under the Income Tax Act 1947. Qualifying new companies may pay substantially less in their first three years due to the Start-Up Tax Exemption scheme administered by IRAS, which exempts a portion of the first S$200,000 of chargeable income. After the exemption period, the Partial Tax Exemption continues to reduce effective rates for most SMEs.

Foreign-sourced income remitted into Singapore is generally exempt from tax under Section 13(8) of the Income Tax Act 1947, provided three conditions are met: the income was subject to tax in the source jurisdiction, the foreign headline tax rate is at least 15%, and the exemption is beneficial to the company. Dividends, branch profits, and service income are the three categories explicitly covered under this provision.

Yes, foreign-owned companies incorporated and operating in Singapore can apply for the Enterprise Development Grant administered by Enterprise Singapore, provided the entity is registered as a business in Singapore and meets the qualifying criteria, which include a minimum 30% local shareholding for certain grant categories. Eligibility conditions vary by grant type and activity, so the specific shareholding threshold should be verified against the relevant grant guidelines at the time of application.

Singapore does not impose withholding tax on dividends paid to shareholders, regardless of their tax residency, because the corporate tax system operates on a one-tier basis under Section 43 of the Income Tax Act 1947. Once tax has been paid at the corporate level, dividends distributed are not subject to further taxation. Singapore's network of over 90 DTAs becomes more relevant for other payment types such as royalties, interest, and service fees where withholding tax may otherwise apply.

A private limited company can be incorporated with a minimum paid-up capital of S$1. There is no statutory minimum beyond this amount for most business activities under the Companies Act. Regulated activities supervised by MAS, such as holding a capital markets services licence or a payment service licence, carry separate minimum capital requirements set by MAS under the relevant licensing frameworks.

A company incorporated in Singapore but managed and controlled from another jurisdiction may lose its tax residency status in Singapore under IRAS guidelines. Tax residency is determined by where the board of directors exercises its decision-making authority, not solely by the place of incorporation. A non-resident company may still be subject to Singapore tax on income sourced from Singapore, but would not qualify for treaty benefits or the various tax exemptions available exclusively to tax-resident entities.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.