Key Takeaways

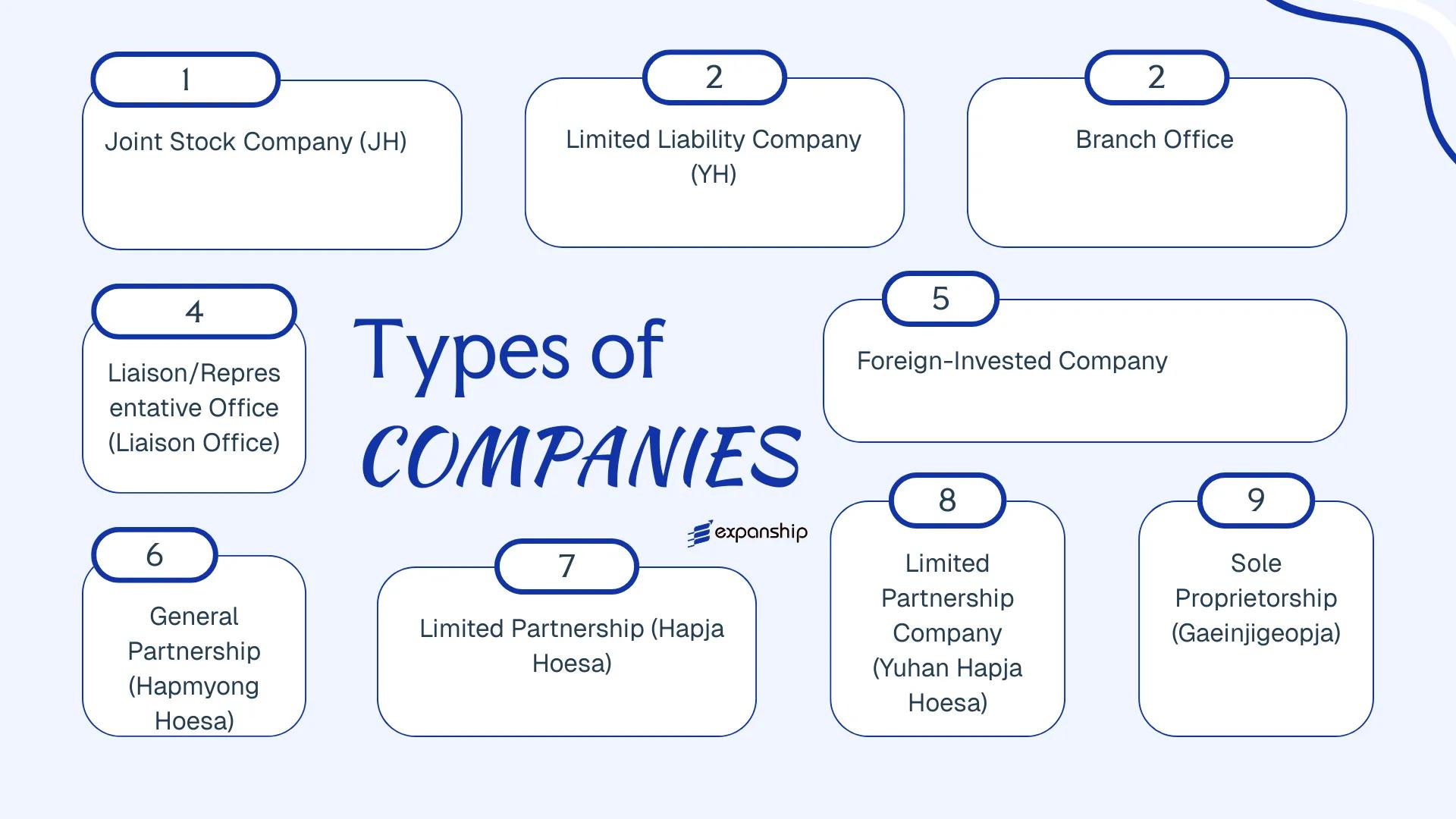

- South Korea offers eight distinct business entity types, ranging from the Jusik Hoesa (Joint Stock Company) to the Sole Proprietorship (Gaeinjigeopja), each carrying different implications for liability, governance, and tax treatment.

- Company registration in South Korea falls under the jurisdiction of the Supreme Court's Registry Office, with the Korea Fair Trade Commission and the Financial Supervisory Service overseeing corporate conduct and financial compliance respectively.

- Branch offices expose the parent entity to full liability, while liaison offices are restricted to non-commercial activities, making the choice between the two consequential for foreign businesses entering the Korean market.

- Foreign investment in South Korea is regulated under the Foreign Investment Promotion Act and overseen by the Ministry of Justice, within a framework that has become progressively more accessible to foreign capital through successive reform cycles.

Introduction to Entity Types in South Korea

South Korea occupies the southern portion of the Korean Peninsula in East Asia, bordered by North Korea to the north and flanked by Japan to the east and China to the west across the Yellow Sea. It is an independent republic governed under a presidential system, with Seoul serving as its commercial and administrative capital.

Company registration falls under the jurisdiction of the Supreme Court's Registry Office, with the Korea Fair Trade Commission and the Financial Supervisory Service overseeing aspects of corporate conduct and financial compliance respectively. Businesses operating in South Korea are subject to a residence-based corporate tax system, with rates and treaty obligations applying depending on the nature of the entity and its income sources.

Several distinct business entity types in South Korea are available to both domestic and foreign investors:

- Jusik Hoesa (Joint Stock Company)

- Yuhan Hoesa (Limited Liability Company)

- Hapmyong Hoesa (General Partnership)

- Hapja Hoesa (Limited Partnership)

- Yuhan Hapja Hoesa (Limited Partnership Company)

- Branch Office

- Liaison Office

- Sole Proprietorship (Gaeinjigeopja)

Each structure carries different implications for liability, ownership, governance, and tax treatment — this article examines each one in detail.

An Overview of Business Structures in South Korea

South Korea's commercial legislation recognises six primary business structures, each governed principally by the Commercial Act (Sangbeop, Act No. 1000) and, for foreign-invested entities, by the Foreign Investment Promotion Act (FIPA). Each structure carries distinct implications for liability, governance, taxation, and the scope of permitted activities.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Tax Treatment | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Jusik Hoesa (JH) | Joint Stock Company | Limited to shares | Corporate tax applies | Permitted | 1 shareholder | FSS / MOCI | Commercial Act |

| Yuhan Hoesa (YH) | Limited Liability Company | Limited to contribution | Corporate tax applies | Permitted | 1 member | MOCI | Commercial Act |

| Branch Office | Foreign branch | Parent liable | Corporate tax on Korean income | Permitted | Parent company | MOCI / tax office | FIPA / Commercial Act |

| Liaison Office | Representative office | Parent liable | Generally exempt | Not permitted | Parent company | MOCI | FIPA |

| Hapmyong Hoesa | General Partnership | Unlimited, joint | Pass-through | Permitted | 2 partners | MOCI | Commercial Act |

| Hapja Hoesa | Limited Partnership | Mixed | Pass-through | Permitted | 2 partners | MOCI | Commercial Act |

| Yuhan Hapja Hoesa | LP Company | Mixed | Corporate tax applies | Permitted | 2 members | MOCI | Commercial Act |

| Gaeinjigeopja | Sole Proprietorship | Unlimited | Individual income tax | Permitted | 1 individual | NTS / district office | Small Business Act |

Each of these structures is examined in full in the sections below.

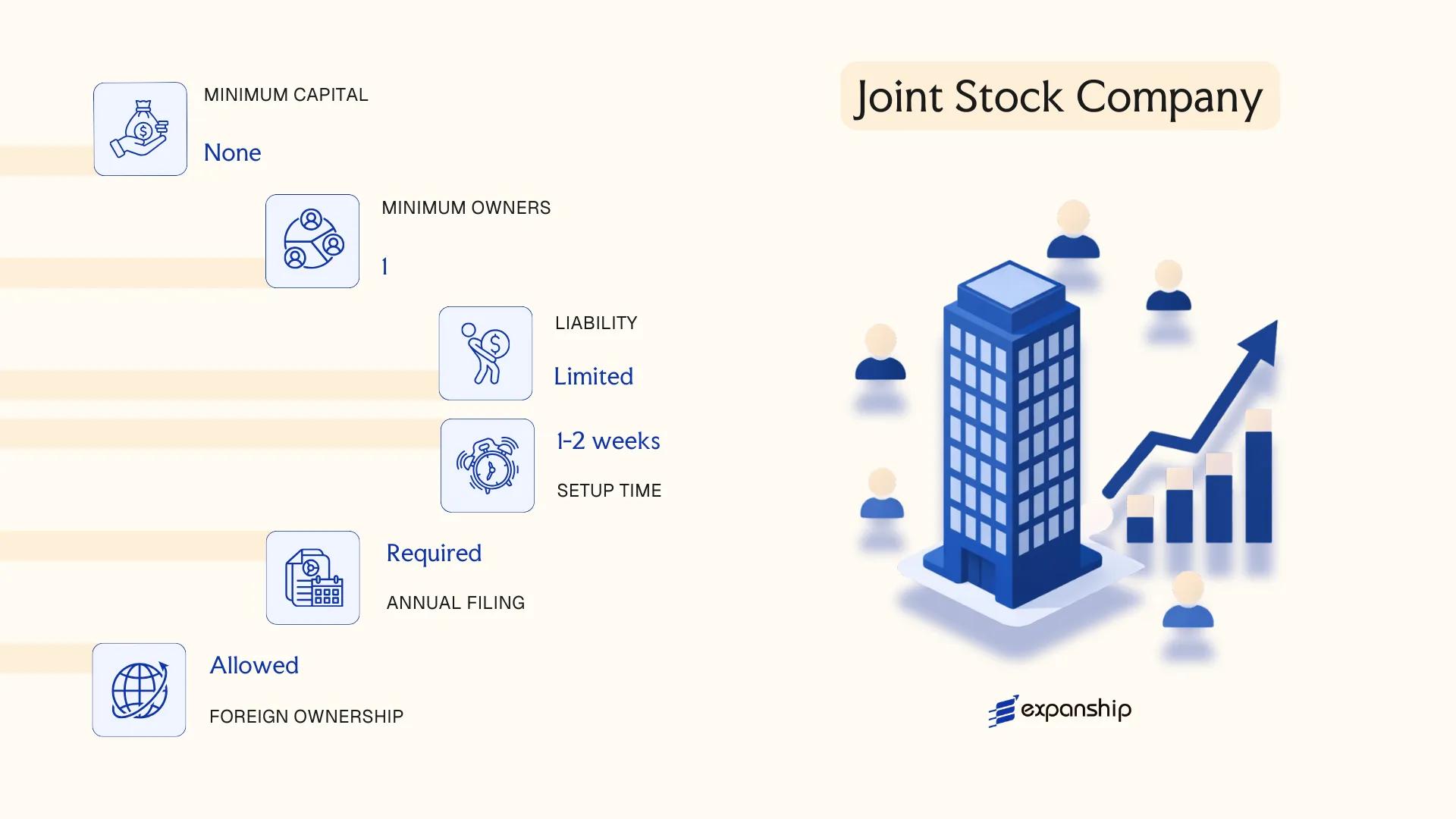

Jusik Hoesa (JH) — Joint Stock Company

The Jusik Hoesa (주식회사) is the most widely used corporate form in South Korea and the structure most foreign investors default to when entering the market. Governed by the Commercial Act (Sangbeop), which was originally enacted in 1962 and has been amended substantially since, the entity carries full separate legal personality distinct from its shareholders.

Liability is limited to each shareholder's capital contribution. The structure accommodates both private and publicly listed configurations, making it suitable for businesses at different stages of growth.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Incorporated company (separate legal entity) | Governed by the Commercial Act (Sangbeop) |

| Members | Shareholders (주주, Juju); minimum 1 shareholder | No maximum shareholder limit; one person can hold all shares |

| Management | Minimum 1 director; Board of Directors required if capital ≥ KRW 1 billion or 3+ directors appointed | Companies with capital below KRW 1 billion may operate with a sole director |

| Local Presence | Registered office address in South Korea required | A resident representative is required for foreign-invested companies under the Foreign Investment Promotion Act (FIPA) |

| Capital | Minimum paid-in capital: KRW 100 million for foreign-invested companies under FIPA; no statutory minimum for domestic JH | Shares must have a par value of at least KRW 100 per share |

| Privacy | Shareholder and director information is filed with the court registry and publicly accessible via the Supreme Court Registry Office (SCRO) | Beneficial ownership disclosure requirements apply under anti-money laundering regulations |

Focus Points

- Taxation: Subject to corporate income tax at progressive rates (10% on the first KRW 200 million, 20% up to KRW 20 billion, 22% up to KRW 300 billion, 25% above); VAT applies at a standard rate of 10%; withholding tax on dividends, interest, and royalties paid to non-residents ranges from 10–22% depending on treaty status; securities transaction tax may apply on share transfers.

- Annual Compliance: Financial statements must be submitted to shareholders and filed with the relevant court registry; external audit requirements apply to companies meeting certain size thresholds under the Act on External Audit of Stock Companies.

- Treaty Access: South Korea maintains an extensive tax treaty network; a JH incorporated locally is generally eligible for reduced withholding tax rates under applicable bilateral treaties.

- Conversion: A JH may be converted to other commercial entity types under the Commercial Act, subject to shareholder approval and court registry re-registration.

- Foreign Ownership: 100% foreign ownership is permitted in most sectors; restricted or prohibited sectors are defined under the Foreign Investment Promotion Act and the relevant negative list.

Closing

The Jusik Hoesa is the standard vehicle for trading operations, manufacturing subsidiaries, and holding structures requiring access to Korea's treaty network or future public listing. Its principal limitation is the comparatively higher administrative burden relative to simpler entity forms, particularly for small-scale operations.

The JH structure suits mid-to-large foreign enterprises, joint venture partners, and any business anticipating significant revenue, external investment, or eventual listing on the Korea Exchange (KRX).

Company Incorporation in South Korea

Establish a Jusik Hoesa or other corporate entity in South Korea with end-to-end registration support across legal, tax, and compliance requirements.

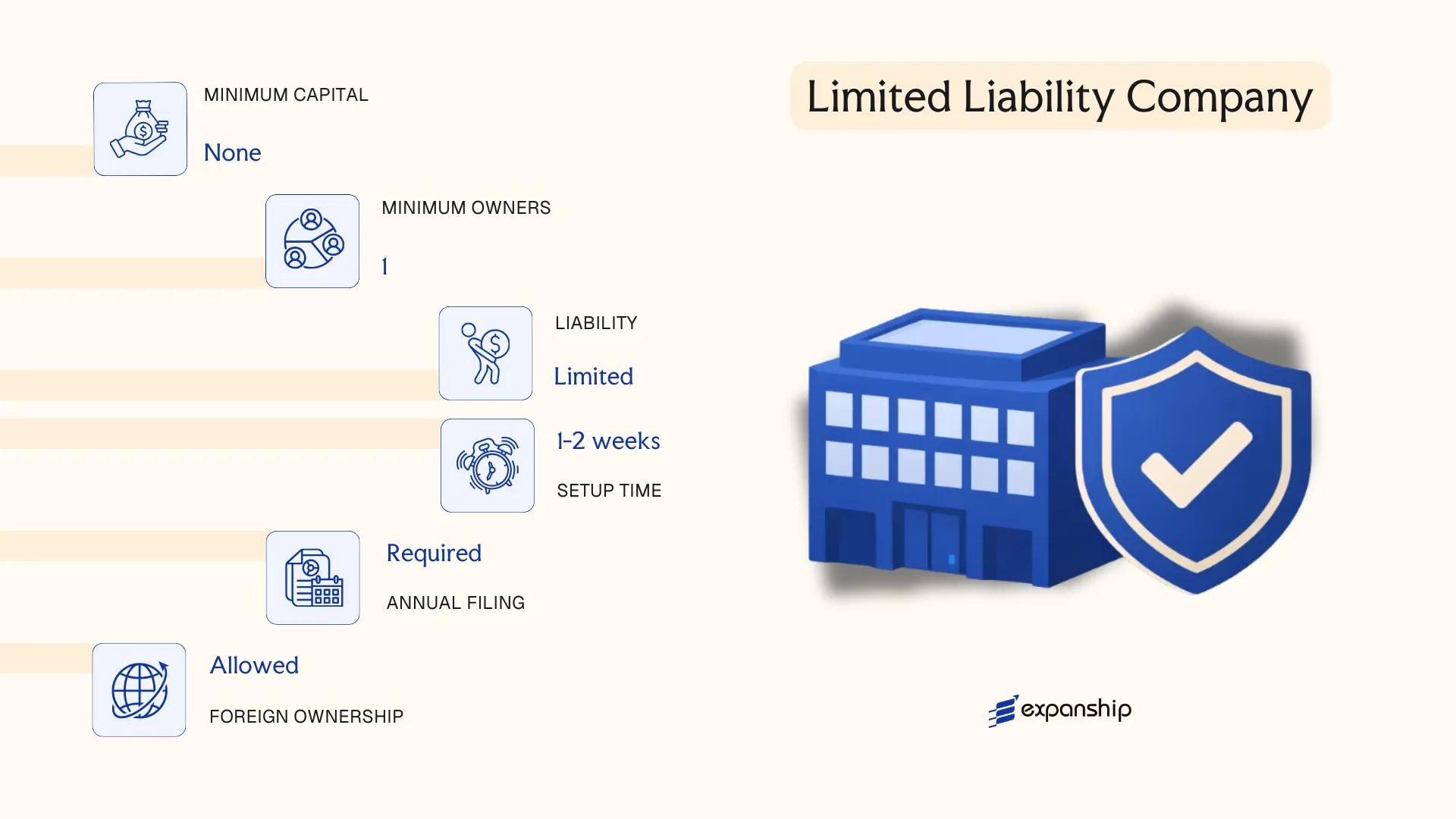

Yuhan Hoesa (YH) — Limited Liability Company

The Yuhan Hoesa limited liability company Korea structure is governed by the Commercial Act (Sangbeop), originally enacted in 1962 and subsequently amended, which codifies its status as a separate legal entity distinct from its members.

Structurally, the YH sits between a joint stock company and a partnership: members hold limited liability capped at their capital contributions, yet the firm retains a more flexible, privately held character than a Jusik Hoesa.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Limited Liability Company (Yuhan Hoesa) | Separate legal personality; governed by the Commercial Act |

| Members | 1–50 members (called sawon) | No distinction between managing and non-managing members by default |

| Management | One or more directors (isa) appointed by members | Directors need not be members; foreign nationals permitted |

| Registered Office | Must maintain a registered address in South Korea | Required for official correspondence and regulatory filings |

| Capital | No statutory minimum; contributions recorded in the articles | Contributions can be cash or in-kind assets |

| Privacy | Member details filed with the court registry | Not publicly listed on a stock exchange; ownership remains relatively private |

Focus Points

- Taxation: Subject to Corporate Income Tax at progressive rates (9%–24%), VAT at 10% on taxable supplies, and withholding tax on dividends, interest, and royalties paid to non-residents; no separate stamp duty on share transfers.

- Annual Compliance: Financial statements must be prepared and approved by members; audit requirements generally lighter than those applying to larger Jusik Hoesa entities.

- Treaty Access: Qualifies as a resident entity for South Korea's tax treaty network, subject to applicable treaty conditions and beneficial ownership tests.

- Conversion: A YH may be converted into a Jusik Hoesa under the Commercial Act, which is a common path when the business seeks external investment or plans a public listing.

- Transfer Restrictions: Member equity interests (jibun) cannot be freely transferred without the consent of other members, limiting liquidity compared to publicly traded shares.

Closing

The YH suits small-to-medium foreign-invested businesses, holding structures, and domestic ventures where close ownership control and lighter governance obligations are priorities; its primary limitation is the 50-member cap, which constrains equity fundraising at scale.

The Yuhan Hoesa is best suited for foreign investors and small-to-medium enterprises seeking a privately held, operationally active presence in South Korea with controlled ownership and manageable compliance obligations.

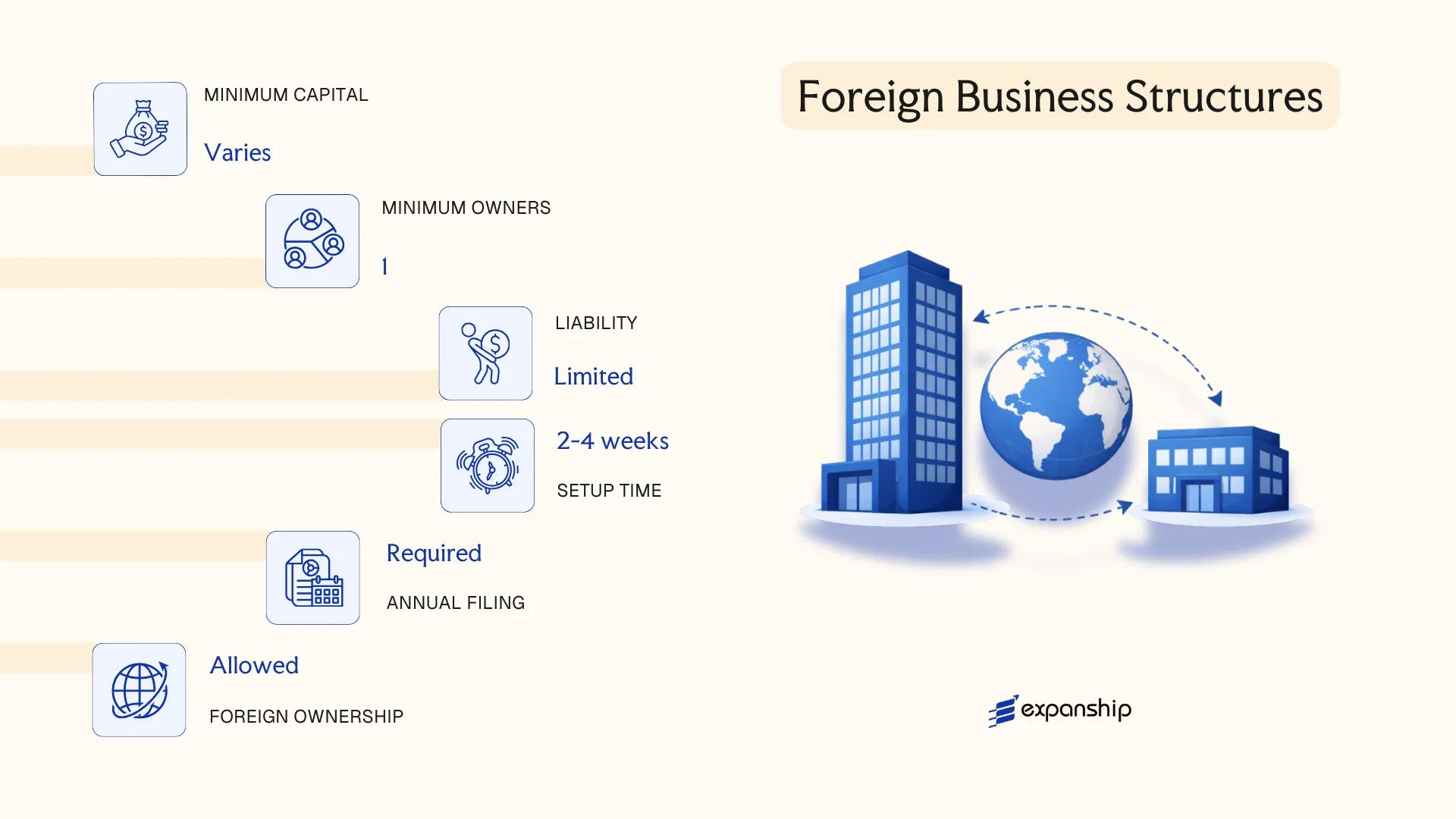

Foreign Business Structures in South Korea [Branch Office, Liaison/Representative Office, Foreign-Invested Company]

Foreign businesses entering the Korean market without establishing a fully localised entity operate under the Foreign Investment Promotion Act (FIPA) of 1998 and the Commercial Act. The three primary foreign business structures in South Korea are the branch office, the liaison office, and the foreign-invested company, each carrying distinct legal standing and operational scope.

A branch office holds no separate legal personality — it is an extension of the parent company, which remains directly liable for its obligations. A liaison office is more restricted still, prohibited from engaging in revenue-generating activity. The foreign-invested company, by contrast, constitutes a fully independent Korean legal entity incorporated under local law.

Key Characteristics

| Requirement | Branch Office | Liaison Office | Foreign-Invested Company |

|---|---|---|---|

| Legal Form | Extension of parent; no separate legal personality | Extension of parent; no separate legal personality | Independent Korean legal entity (typically JH or YH) |

| Representative | Appointed local representative required | Appointed local representative required | Directors appointed per entity type rules |

| Local Presence | Registered business address in Korea | Registered address in Korea | Registered office in Korea |

| Minimum Capital | No statutory minimum | No statutory minimum | KRW 100 million under FIPA for foreign-invested status |

| Revenue Activity | Permitted | Not permitted | Permitted |

| Privacy | Parent company details disclosed on registration | Parent company details disclosed | Shareholder and director details in public registry |

Focus Points

- Taxation: Branch offices are subject to Korean corporate income tax (11–24% on taxable income) on Korea-sourced income, plus a 2% branch profits tax in lieu of dividend withholding tax; liaison offices have no tax liability given the absence of taxable activity; foreign-invested companies are taxed as domestic entities, with VAT at 10% and dividend withholding tax at 20% (reducible under applicable tax treaties).

- Treaty Access: Foreign-invested companies and branch offices may access Korea's tax treaty network; liaison offices generally cannot, as they produce no taxable income.

- Annual Compliance: Branch offices must file corporate tax returns and submit financial statements; foreign-invested companies follow full Korean corporate compliance cycles including audit requirements above certain thresholds.

- Restrictions: Liaison offices are explicitly barred from sales, contract execution, and invoicing under Korean regulatory interpretation; operating beyond this scope triggers reclassification risk.

- Foreign Investment Registration: Foreign-invested companies must register with the Korea Trade-Investment Promotion Agency (KOTRA) or an authorised foreign exchange bank under FIPA to obtain foreign-invested enterprise status and access associated incentives.

Sub-Types

Branch Office

Registered under the Commercial Act, a branch office must be reported to the local court registry and obtain a business registration number from the National Tax Service. It is the standard structure for foreign firms that need full operational capability without incorporating a separate Korean entity.

Liaison/Representative Office

This structure requires registration with the foreign exchange bank designated by the Bank of Korea. Its use is strictly limited to market research, business promotion, and liaison functions — activities that support the parent without generating local revenue.

Foreign-Invested Company (FIC)

Established under FIPA, this entity qualifies for the foreign-invested enterprise designation when a foreign investor holds at least KRW 100 million (approximately USD 75,000) in equity. The designation unlocks potential tax incentives in designated free economic zones and industrial complexes, subject to sector eligibility.

Closing

Branch offices suit foreign firms testing Korean operations or executing contracts on behalf of the parent, while foreign-invested companies are the appropriate vehicle for long-term market presence requiring full contractual and employment capacity. The primary limitation across all three structures is that none eliminates the need for local compliance infrastructure, including tax filing and regulatory reporting.

Foreign-invested companies are best suited for businesses committing to sustained commercial operations in Korea that require full legal autonomy from the parent entity.

Partnerships in South Korea [Hapmyong Hoesa (General Partnership), Hapja Hoesa (Limited Partnership), Yuhan Hapja Hoesa (Limited Partnership Company)]

Partnership structures in South Korea are governed by the Commercial Act (Sangbeop), which was first enacted in 1962 and has been amended periodically since. Unlike a Jusik Hoesa or Yuhan Hoesa, partnerships do not always carry a separate legal personality distinct from their members, and liability exposure varies significantly depending on the chosen structure.

Three distinct forms exist under Korean commercial law: the Hapmyong Hoesa (general partnership), the Hapja Hoesa (limited partnership), and the Yuhan Hapja Hoesa (limited partnership company). Each differs in how liability is allocated between partners and in the degree of management control each partner class may exercise.

Key Characteristics

| Requirement | Hapmyong Hoesa | Hapja Hoesa | Yuhan Hapja Hoesa |

|---|---|---|---|

| Legal Form | General Partnership – no separate legal personality | Limited Partnership – no separate legal personality | Limited Partnership Company – separate legal personality |

| Members | Partners (min. 2 general partners; no statutory maximum) | General partners (min. 1) + limited partners (min. 1); no statutory maximum | General partners (min. 1) + limited partners (min. 1); no statutory maximum |

| Liability | All partners: unlimited, joint and several | General partners: unlimited; limited partners: liability capped at capital contribution | General partners: unlimited; limited partners: liability capped at capital contribution |

| Minimum Capital | No statutory minimum | No statutory minimum | No statutory minimum |

| Local Presence | Registered office in Korea required | Registered office in Korea required | Registered office in Korea required |

| Registration | Filed with the district court registry | Filed with the district court registry | Filed with the district court registry |

Focus Points

- Taxation: Partnerships are generally treated as pass-through entities for Korean tax purposes; income is attributed to and taxed at the partner level under the individual or corporate income tax rates applicable to each partner, though the Yuhan Hapja Hoesa may be subject to corporate income tax depending on its classification.

- VAT: Partners conducting taxable business activities must register for VAT under the Value-Added Tax Act if annual supplies exceed the registration threshold.

- Annual Compliance: All three forms must maintain accounting records and file annual reports; the Yuhan Hapja Hoesa faces additional corporate disclosure obligations given its separate legal personality.

- Treaty Access: Access to Korea's tax treaty network depends on how each partner's home jurisdiction classifies the entity; hybrid mismatches can arise and should be assessed before structuring.

- Restrictions: Foreign nationals may face additional scrutiny under the Foreign Investment Promotion Act when establishing or joining a Korean partnership.

Sub-Types

Hapmyong Hoesa (General Partnership)

All members bear unlimited joint and several liability for the firm's obligations, and each partner has the right to participate in management. This structure is rarely used in commercial practice due to its unrestricted liability exposure.

Hapja Hoesa (Limited Partnership)

Two classes of partner exist: general partners with unlimited liability who manage the business, and limited partners whose liability is capped at their capital contribution and who are restricted from participating in management. This separation makes the form more attractive than the Hapmyong Hoesa for passive investors.

Yuhan Hapja Hoesa (Limited Partnership Company)

Introduced through amendments to the Commercial Act, this form carries a separate legal personality, which distinguishes it from the other two partnership types. Its structure closely resembles a limited partnership but with the added benefit of corporate-level legal standing, making it a more viable option for fund structures and joint ventures.

Partnership forms are infrequently used by foreign investors in Korea, though the Yuhan Hapja Hoesa has gained traction in private equity and fund management contexts. The pass-through tax treatment is a notable structural benefit, but the unlimited liability carried by general partners in all three forms represents a material operational risk.

Partnership structures in Korea are best suited to domestic joint ventures, investment funds, or professional service arrangements where the partners have an established relationship and clearly defined roles.

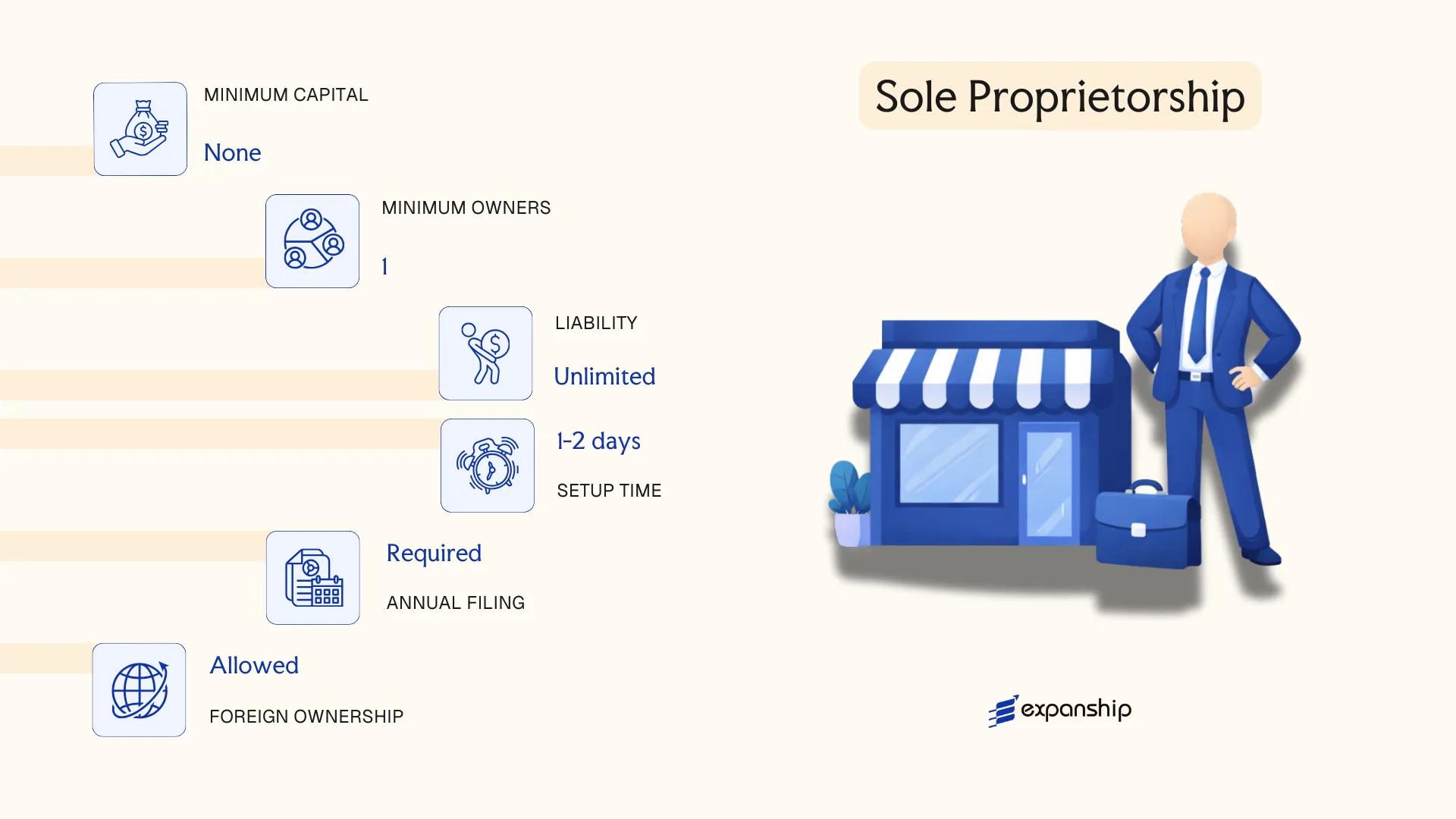

Sole Proprietorship (Gaeinjigeopja)

A sole proprietorship South Korea Gaeinjigeopja is the simplest form of business registration available to individuals operating commercially. Governed primarily by the Commercial Act and administered through the National Tax Service (NTS), this structure carries no separate legal personality — the proprietor and the business are legally the same person.

Liability is therefore unlimited. All business debts and obligations fall directly on the individual owner, with no statutory protection separating personal assets from business exposure.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated sole trader | No separate legal entity; owner and business are one |

| Members | Single proprietor | No minimum capital contributor; no shareholders or directors |

| Local Presence | Business address required | Must register with the local district tax office (세무서) under the NTS |

| Capital | No statutory minimum | No prescribed currency requirement or paid-in capital threshold |

| Privacy | Owner's name publicly associated | Registration details filed with NTS; limited public disclosure compared to incorporated entities |

Focus Points

- Taxation: Subject to global income tax (6%–45% progressive rates) on business income; VAT registration required once annual turnover exceeds KRW 80 million; no separate corporate tax applies.

- Annual Compliance: Annual income tax return due by May 31; VAT returns filed biannually or quarterly depending on turnover classification.

- Treaty Access: No access to South Korea's tax treaty network for reduced withholding rates, as treaties apply to corporate entities, not individuals acting as sole traders.

- Conversion: Can be converted into a Yuhan Hoesa or Jusik Hoesa; assets and liabilities transfer through a business transfer agreement rather than a statutory conversion mechanism.

- Foreign National Restrictions: Non-Korean nationals must hold an appropriate visa category permitting self-employed activity before proceeding with the Gaeinjigeopja registration process.

Closing

A Gaeinjigeopja suits low-volume domestic trading, freelance services, or early-stage self-employed business Korea setup where administrative simplicity outweighs the need for liability protection. The primary advantage is minimal compliance overhead; the clear limitation is unlimited personal liability with no statutory cap.

Best suited for Korean nationals or eligible foreign residents operating as individual service providers or small-scale traders with no immediate need for external investment or liability separation.

How to Choose the Right Entity Type in South Korea

Knowing how to choose a company type in South Korea requires more than a general preference for simplicity or cost. The structure you register has binding legal, tax, and operational consequences from day one.

Why Your Entity Choice Matters

- Registering a foreign liaison office while conducting revenue-generating transactions violates its permitted scope under the Foreign Exchange Transactions Act, which can result in forced closure and administrative penalties.

- Selecting a structure ineligible under a bilateral tax treaty means your business cannot claim reduced withholding tax rates on dividends, royalties, or interest paid to non-resident counterparties.

- Forming a Jusik Hoesa when your operation is a single-person consultancy subjects you to mandatory external audit thresholds and shareholder meeting requirements that add recurring compliance costs with no operational benefit.

- Choosing a branch office, which lacks separate legal personality under Korean law, exposes the foreign parent entity to direct liability for all Korean-based obligations.

Key Factors to Consider

- Business Activity: Active trading, regulated sectors such as banking or insurance, and passive asset-holding each point toward different permitted structures under the Commercial Act.

- Ownership Structure: A single-investor operation may function adequately as a Yuhan Hoesa, while multi-party ventures requiring formal governance boards will need a Jusik Hoesa.

- Tax Objectives: Your need for treaty access, eligibility for the flat 20% corporate tax rate on foreign-invested companies, or exemption status should directly inform your entity selection.

- Liability Exposure: Whether your parent company can absorb unlimited liability through a branch, or requires the legal separation that an incorporated entity provides, is a threshold question.

- Substance Capacity: If you cannot realistically maintain staff, a registered office, and management decision-making in Korea, certain structures will fail to meet operational legitimacy requirements under National Tax Service guidelines.

- Exit Strategy: Conversion between entity types in Korea is procedurally restricted, so your ability to redomicile or wind up cleanly should be assessed before registration, not after.

Corporate Compliance Services in South Korea

Maintain good standing with Korean regulatory requirements, including annual filings, audit obligations, and statutory reporting.

Conclusion

Selecting the right structure is one of the most consequential decisions in this South Korea company formation process. The Jusik Hoesa suits companies expecting external investment or public capital markets, while the Yuhan Hoesa serves closely held businesses that prioritize simplified governance. Branch offices retain full liability exposure for the parent entity; liaison offices are limited to non-commercial activities. Among partnerships, each tier reflects a distinct balance between operational control and personal liability.

The Jusik Hoesa is by far the most commonly registered entity type, favored across industries from manufacturing to fintech.

Registered under the Foreign Investment Promotion Act and overseen by the Ministry of Justice, South Korea's regulatory framework has grown more accessible to foreign capital over successive reform cycles. Treaty networks continue to expand, reinforcing the jurisdiction's position as a structured and transparent destination for international business. Expanship's formation and compliance services cover each entity type discussed throughout this guide.

How Expanship Can Assist You

Expanship's corporate services South Korea team works directly with businesses forming a Jusik Hoesa, Yuhan Hoesa, or any foreign-invested structure under the Foreign Investment Promotion Act. From initial structuring decisions to filings with the Korea Customs Service and the Ministry of Justice's immigration-linked corporate registers, your setup is handled by people who know the local process.

Expanship's company incorporation assistance in South Korea covers each stage of the formation and maintenance cycle:

- Document preparation, notarization, and apostille legalization

- Registered agent and local office address provision

- Government filing and liaison with the Supreme Court Registry (the authority overseeing commercial registration)

- Post-incorporation compliance management, including annual reporting obligations

- Corporate bank account introduction assistance

Your business deserves accurate, jurisdiction-specific guidance rather than generic advice recycled from another market.

To discuss your South Korea entity formation, contact Expanship Korea.

Frequently Asked Questions (FAQ)

The Jusik Hoesa (JH) is the most frequently registered entity, primarily because it can issue shares, attract institutional investment, and list on the Korea Exchange. Its governance framework under the Commercial Act also makes it the default choice for ventures expecting external capital.

A Branch Office is not a separate legal entity; it is an extension of the foreign parent and carries no independent liability shield. A Jusik Hoesa is locally incorporated, subject to Korean corporate income tax on its worldwide income, and must meet full disclosure and audit obligations under the Act on External Audit of Stock Companies. The compliance burden is higher for a JH, but local trading rights are broader.

The Yuhan Hoesa (YH) offers comparatively limited public disclosure requirements, as it is not subject to mandatory external audit unless it meets specific thresholds under the External Audit Act. Shareholder information is not routinely published in public registries the way it is for listed JH companies. Nominee arrangements are legally permissible but must still comply with beneficial ownership reporting under the Financial Intelligence Unit regulations.

A Jusik Hoesa and Yuhan Hoesa can each be formed by a single incorporator. Partnerships are structurally different: a Hapmyong Hoesa requires at least two general partners, a Hapja Hoesa requires at least one general and one limited partner, and a Yuhan Hapja Hoesa follows similar dual-partner logic. Sole proprietorships are by definition single-person structures registered with the local tax office.

Foreigners may establish a JH, YH, Branch Office, or Liaison Office under the Foreign Investment Promotion Act (FIPA), provided registration is completed with the Korea Trade-Investment Promotion Agency (KOTRA) or an authorised foreign exchange bank. Certain regulated sectors require prior approval regardless of entity type. Partnership structures are not explicitly restricted, but foreign participation in them is uncommon due to unlimited liability exposure in some forms.

The Korean Commercial Act permits conversion between certain entity types, most commonly from a YH to a JH, through a formal reorganisation procedure involving shareholder resolution and re-registration with the court registry. Conversion from a partnership to a share-issuing entity is procedurally more complex and may trigger tax consequences. Not all conversions are available in both directions.

The JH, YH, and Yuhan Hapja Hoesa all possess separate legal personality under Korean law. A Hapmyong Hoesa and Hapja Hoesa also have legal personality, though general partners in both structures bear unlimited personal liability for company obligations. Liaison Offices and Branch Offices do not constitute independent legal persons.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.