Key Takeaways

- Foreign investors incorporating in Tanzania must navigate a multi-agency compliance environment governed by the Companies Act (Cap. 212), which creates layered procedural obligations that extend well beyond initial registration.

- Business registration through BRELA introduces delays that can disrupt operational timelines, particularly for foreign entities unfamiliar with Tanzania's administrative processes.

- Currency exposure is a structural risk for foreign-owned Tanzanian entities, as the Shilling's volatility and applicable foreign exchange controls can complicate cross-border profit repatriation and financial planning.

- Accessing capital through local Tanzanian financial institutions presents a material constraint for incorporated businesses, as the depth and accessibility of the domestic lending market remains limited relative to more established jurisdictions.

Tanzania operates under an evolving but heavily regulated corporate framework, and the disadvantages of incorporating in Tanzania span procedural, financial, and operational categories that foreign investors must account for before committing to a structure.

The drawbacks covered in this article range from registration bottlenecks and capital requirements to financing constraints and currency risk. Not all of these will apply equally — the relevance of each depends significantly on your business model, sector, and intended ownership structure.

The governing legislation is the Companies Act (Cap. 212), which establishes the foundational rules for company formation and ongoing compliance. Regulatory obligations under this framework are administered by multiple bodies, creating layered requirements that affect how your entity operates day to day.

This article is most relevant to foreign entrepreneurs and multinational firms considering a direct incorporation rather than a representative or branch arrangement.

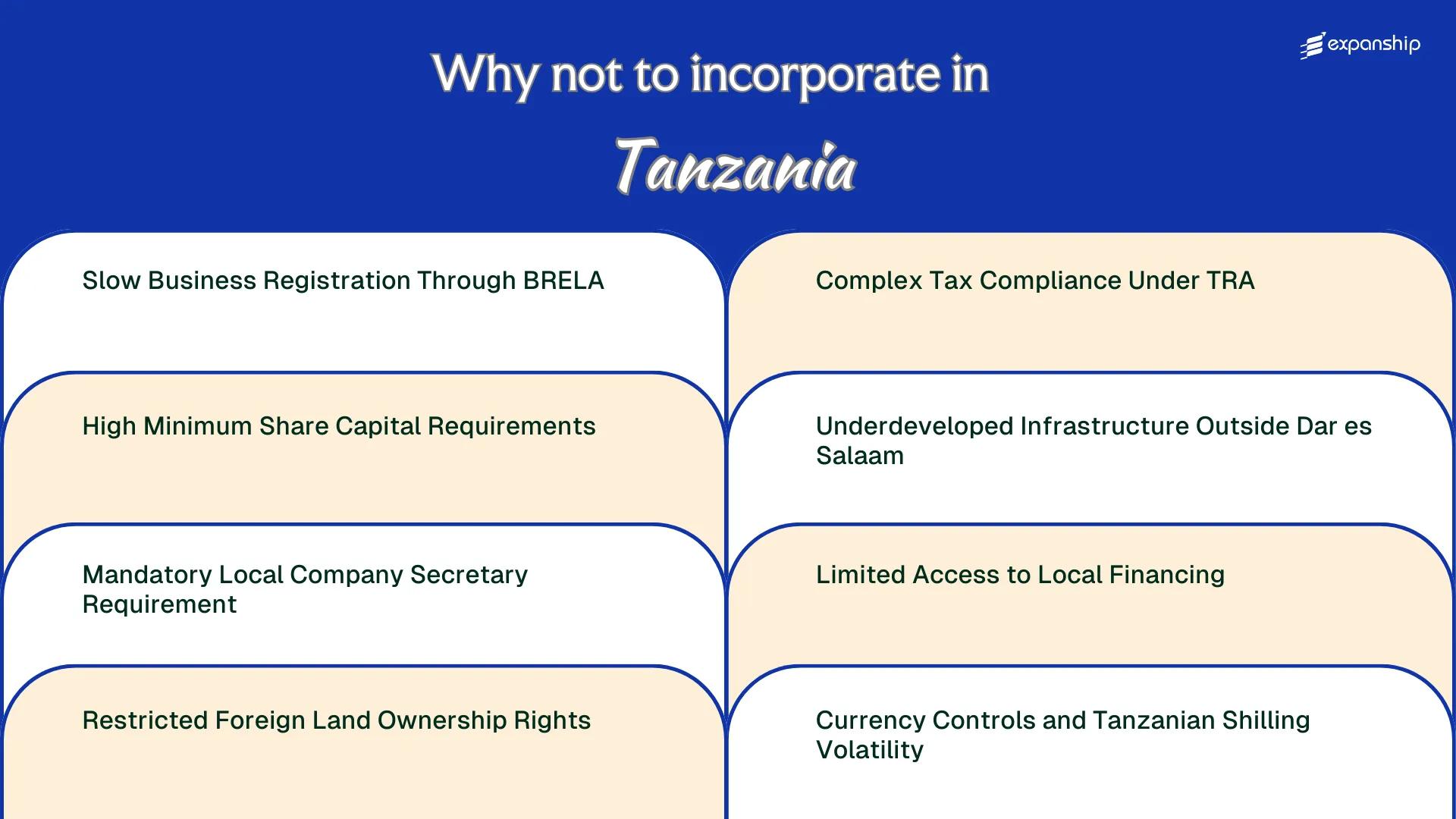

Slow Business Registration Through BRELA

BRELA registration delays Tanzania are a documented friction point for foreign investors attempting to establish a local entity. Processing times frequently exceed official timelines, creating operational uncertainty before your business has formally begun.

Systemic Delays at the Registration Authority

The Business Registrations and Licensing Agency, known as BRELA, handles all company incorporations under the Companies Act, Cap 212. Despite an online portal introduced to reduce processing times, manual verification steps and internal backlogs routinely extend registration beyond the stated five to seven business day window. For a foreign investor with lease agreements, staff contracts, or client commitments tied to an incorporation date, each additional week carries direct financial cost.

Downstream Consequences of Late Registration

Your company cannot legally open a corporate bank account, apply for a Tax Identification Number with the Tanzania Revenue Authority, or obtain sector-specific licenses until BRELA issues the certificate of incorporation. This sequential dependency means a single administrative delay at BRELA stalls your entire operational setup. The slow business registration process in Tanzania disproportionately affects foreign-owned entities, which often require additional document authentication steps not required of locally owned firms.

A delayed BRELA certificate directly postpones TRA registration and banking access, meaning your business may be unable to transact or receive payments for weeks after your intended launch date.

High Minimum Share Capital Requirements

Tanzania minimum share capital requirements vary by company type, but for foreign-owned private limited companies, the thresholds set by the Tanzania Investment Centre and enforced under the Companies Act create a tangible barrier to entry. Foreign investors are generally required to demonstrate a minimum capital of USD 100,000 for a locally incorporated entity, a figure that excludes many small and mid-sized businesses from establishing a formal presence.

This threshold is not a guarantee of operational approval. It is a precondition that ties up capital before your business generates a single dollar of revenue.

For a foreign business owner, this structure creates several compounding pressures:

- Your working capital is partially immobilised at incorporation, reducing liquidity during the setup phase when operational costs are highest.

- The USD 100,000 floor makes Tanzania structurally inaccessible for early-stage or bootstrapped foreign firms that could otherwise register legally.

- Meeting the requirement through foreign currency transfers triggers additional scrutiny under the Bank of Tanzania's foreign exchange regulations, adding procedural delay.

- Local subsidiaries of foreign groups must still satisfy this threshold independently, creating duplicated capital commitments across a corporate structure.

Private companies incorporated solely by Tanzanian nationals face no equivalent minimum under the Companies Act Cap. 212, which underscores the unequal burden placed specifically on foreign-owned entities.

Company Incorporation in Tanzania

Understand the capital requirements, regulatory steps, and structural options for incorporating a foreign-owned company in Tanzania.

Mandatory Local Company Secretary Requirement

Under the Tanzania Companies Act (Cap. 212), every registered company must appoint a company secretary. For foreign-incorporated entities establishing a local presence, satisfying the Tanzania local company secretary requirement means sourcing a qualified individual resident within the country, which adds a recurring operational cost that has no equivalent in many other jurisdictions.

The secretary must hold qualifications recognized under Tanzanian law, typically a legal, accounting, or chartered secretary credential. This restriction on who qualifies effectively limits your options to a narrow pool of local professionals, and that scarcity drives up service fees considerably.

| Requirement | Detail | Implication for Foreign Owners |

|---|---|---|

| Residency condition | Secretary must be locally based | Remote appointment from home country is not permissible |

| Qualification standard | Legal, accounting, or ICSA-equivalent credential required | Narrows eligible candidate pool significantly |

| Appointment obligation | Mandatory from date of incorporation | No grace period; immediate cost from day one |

| Annual retention cost | Market rates for qualified professionals in Dar es Salaam | Ongoing fixed overhead regardless of business activity |

Sourcing a compliant secretary through BRELA's registration process is not a one-time task. The appointment must be maintained continuously, meaning even a dormant entity carries this mandatory compliance burden indefinitely.

Foreign firms with no substantive local operations still cannot waive this obligation. There is no statutory exemption based on company size or turnover level.

Restricted Foreign Land Ownership Rights

Foreign land ownership restrictions in Tanzania are codified directly into law. Under the Land Act, Cap. 113, all land in the country is public land held in trust by the President. Foreign nationals and foreign-owned companies cannot hold a right of occupancy under this framework.

What foreign investors can access is a derivative right, granted through the Tanzania Investment Centre. This is a lesser, time-bound interest in land, not outright ownership, and it is conditional on the investment being registered and approved.

For a foreign-incorporated entity, this creates a structural ceiling on property rights. You cannot hold land on equal footing with a domestic company, which directly affects your ability to use land as collateral for financing or to provide security in commercial arrangements.

- Foreign companies cannot hold a right of occupancy under the Land Act, Cap. 113

- Derivative rights must be obtained through the Tanzania Investment Centre approval process

- The land interest is time-limited and tied to the approved investment purpose

- Land cannot be freely used as collateral without clear title, limiting financing options

Even a majority foreign-owned company registered locally in Tanzania is still treated as a foreign entity under land law, meaning local incorporation alone does not unlock standard land ownership rights.

Complex Tax Compliance Under TRA

Tanzania tax compliance challenges under the Tanzania Revenue Authority (TRA) go well beyond filing annual returns, and for foreign-owned companies, the administrative burden translates directly into recurring professional costs.

Multiple Tax Heads Filed Separately

Your firm must comply with distinct obligations across corporate income tax, VAT, payroll taxes, withholding tax, and skills and development levy, each administered under separate filing schedules and governed primarily by the Income Tax Act Cap. 332 and the Value Added Tax Act Cap. 148. Missing a single filing window triggers penalties and interest charges that accrue automatically, creating financial exposure even when the underlying tax liability is negligible.

Audit Risk and Enforcement Pressure on Foreign Entities

The TRA holds broad authority to conduct transfer pricing audits on related-party transactions, requiring documentation that meets standards most small-to-mid-size foreign investors are not structured to produce without specialist advisors. Complex tax obligations in Tanzania companies therefore carry an indirect cost: retaining local tax counsel is effectively non-optional, not a discretionary expense.

Support for Tax Compliance Challenges in Tanzania

Get structured guidance on managing TRA obligations, filing schedules, and corporate tax risks for your Tanzania-registered entity.

Underdeveloped Infrastructure Outside Dar es Salaam

Outside Dar es Salaam, Tanzania infrastructure limitations create direct operational costs that businesses absorb without any corresponding regulatory offset. Road quality, power supply, and digital connectivity deteriorate significantly once you move beyond the commercial capital.

- Unreliable electricity supply in upcountry regions forces businesses to invest in independent generation capacity, adding capital and maintenance costs that urban competitors in Dar es Salaam do not face at the same scale.

- Poor road conditions across large parts of the country increase freight transit times and vehicle operating costs, compressing margins on any supply chain that extends beyond the port corridor.

- Limited mobile and fixed-line internet penetration in rural and secondary urban areas restricts your ability to run cloud-dependent systems or maintain consistent communication with overseas principals.

- Underdeveloped regions present business challenges around talent retention, as skilled employees frequently decline postings outside Dar es Salaam, raising recruitment costs for upcountry operations.

- Tanzania logistics and connectivity problems are most acute in regions served only by seasonal or unpaved roads, where supply disruptions during heavy rains can halt operations entirely.

Limited Access to Local Financing

Limited financing access Tanzania companies face is a structural constraint, not an administrative inconvenience. The domestic credit market is shallow by regional standards, and commercial banks tend to concentrate lending toward established local enterprises with documented collateral, typically land titles or fixed assets that foreign-incorporated entities cannot easily hold given the restrictions on non-citizen land ownership.

Foreign businesses are generally perceived as higher-risk borrowers by Tanzanian banks, which means credit terms, when available, carry elevated interest rates. The Bank of Tanzania's benchmark lending rates have historically contributed to commercial rates well above those in comparable East African markets, making local debt financing an expensive option.

Microfinance institutions and development finance channels exist but are oriented toward small domestic enterprises. For a foreign firm seeking working capital or growth financing, these channels are functionally inaccessible.

A foreign-owned limited company incorporated in Tanzania requiring TZS 500 million (approximately USD 190,000) in working capital could face commercial lending rates exceeding 20% per annum from local banks, compared to rates of 7-10% the same firm might access from its home-country lenders, effectively doubling the cost of debt financing for local operations.

Currency Controls and Tanzanian Shilling Volatility

Tanzania shilling volatility currency risks are a consistent operational concern for foreign-owned entities receiving or repatriating funds across borders. The shilling has experienced periods of significant depreciation against major currencies, which directly erodes the real value of locally held capital and profit distributions.

Under the Foreign Exchange Act (Cap. 271) and regulations administered by the Bank of Tanzania, foreign companies must conduct certain transactions through licensed commercial banks and comply with documentation requirements when transferring funds abroad. This creates delays and administrative friction that affect cash flow planning for your business.

Repatriating dividends or loan repayments requires documented proof of the underlying transaction, and failure to produce the correct paperwork can result in funds being held. For businesses with lean treasury operations, this is a material operational constraint.

The shilling's limited convertibility in international markets also means your firm cannot easily hedge exposure through standard forward contracts or currency derivatives available in more liquid markets. Exchange rate losses become a direct cost rather than a manageable risk.

- Foreign currency accounts are permitted but subject to Bank of Tanzania oversight

- Export proceeds must generally be repatriated within a specified period

- Undeclared foreign currency holdings can attract regulatory penalties

Any foreign currency transferred out of Tanzania must be supported by documentation acceptable to a Bank of Tanzania-licensed bank, and non-compliant transfers may be blocked regardless of the underlying transaction's legitimacy.

Overcoming These Incorporation Challenges

Overcoming these incorporation challenges in Tanzania requires structural preparation before any registration steps begin, not adjustments made after obstacles arise.

- Pre-register with the Business Registrations and Licensing Agency (BRELA) online portal to reduce processing delays associated with in-person submissions.

- Structure your entity's share capital at or above the minimum threshold required for your chosen company class before filing constitutional documents.

- Appoint a Tanzania-resident company secretary prior to incorporation to satisfy the mandatory residency requirement under the Companies Act, Cap. 212.

- Obtain a Tax Identification Number (TIN) and register for applicable taxes with the Tanzania Revenue Authority (TRA) immediately upon incorporation to avoid compliance arrears.

- Establish a foreign currency account under Bank of Tanzania regulations to manage Tanzanian shilling exposure within the permitted controls framework.

- Conduct land access arrangements through long-term lease structures via the Tanzania Investment Centre (TIC) rather than direct ownership attempts.

These mitigation steps operate within a multi-agency regulatory environment spanning BRELA, TRA, and the TIC, each with distinct filing requirements and timelines. Coordination across these bodies is a structural feature of doing business in this jurisdiction, not an anomaly.

Tanzania's Overall Investment Viability

Tanzania investment viability for foreign companies is shaped by a combination of genuine structural barriers and real economic opportunity. The disadvantages covered in this blog are not incidental friction — they reflect systemic conditions that affect how foreign businesses operate, plan, and remain compliant. That said, the country's population size, regional trade position within the East African Community, and ongoing infrastructure investment mean it retains credibility as a mid-to-long-term market entry destination for businesses prepared to absorb the operational complexity.

| Pros | Cons |

|---|---|

| Large domestic market with a growing consumer base | BRELA's manual registration processes create delays that extend incorporation timelines |

| East African Community membership enables regional trade access | Minimum share capital thresholds can restrict entry for smaller foreign firms |

| Strategic coastal position supports import and export logistics | Foreign entities cannot directly own land, requiring leasehold arrangements |

| Active sectors including mining, agriculture, and energy draw sustained foreign interest | TRA's tax compliance framework carries high administrative burden and audit exposure |

| Infrastructure gaps outside Dar es Salaam raise operational costs significantly | |

| Tanzanian shilling volatility and foreign exchange controls complicate profit repatriation |

Corporate Compliance Services for Companies in Tanzania

Stay current with Tanzania's regulatory requirements, including TRA obligations, annual filings with BRELA, and company secretary compliance under the Companies Act.

Conclusion

The cons of Tanzania company incorporation extend across regulatory, financial, and operational dimensions. BRELA's registration delays, the mandatory resident company secretary requirement, and the TRA's multi-layered compliance obligations each present measurable friction for foreign investors. Currency exposure through Tanzanian shilling volatility adds further financial risk that affects long-term planning.

Structural barriers are real, and the risks of registering a company in Tanzania warrant careful assessment before committing capital. Firms that enter with accurate expectations and qualified local support are better positioned to manage the process without costly missteps.

Expanship's Tanzania Expansion Support

Working with BRELA's registration procedures, TRA's tax compliance requirements, and Tanzania's foreign ownership restrictions creates a genuine administrative load for incoming businesses. Tanzania expansion support corporate services from Expanship are designed to reduce that burden by managing the specific filing, liaison, and compliance obligations that slow most foreign incorporations down.

Beyond registration, Expanship covers a practical range of services for businesses entering Tanzania:

- Your company documents are prepared and submitted to BRELA accurately and on time.

- A registered agent and local office address are provided to satisfy statutory requirements.

- Filings and correspondence with government bodies, including TRA and BRELA, are handled on your behalf.

- Ongoing post-incorporation compliance obligations are tracked and managed throughout the year.

- Banking introduction assistance is provided to help your entity establish a local account.

- Tax registration and liaison with the Tanzania Revenue Authority are coordinated from the outset.

To discuss your incorporation requirements, contact Expanship Tanzania.

Frequently Asked Questions (FAQ)

The requirement applies to companies incorporated under the Companies Act, Cap. 212, which covers the most common structures foreign investors use, including private limited companies. Your appointed company secretary must be resident in Tanzania and hold recognized qualifications, meaning you cannot simply assign the role to an offshore administrator. Failure to maintain a qualified, in-country secretary leaves your company in breach of statutory obligations, which can result in penalties from the Registrar of Companies at BRELA.

The Tanzania Revenue Authority can impose interest charges, administrative penalties, and in serious cases, initiate prosecution under the Tax Administration Act, Cap. 438. Penalties for late filing or underpayment are calculated as a percentage of the outstanding tax liability, and interest accrues from the due date. TRA also has the authority to freeze business accounts and place restrictions on your company's operations pending settlement of outstanding obligations.

The Land Act, Cap. 113, prohibits non-citizens from owning land in Tanzania outright, which affects foreign-owned companies across virtually all sectors that require physical premises or operational land. Foreign investors can access land only through granted rights of occupancy or derivative rights, typically through the Tanzania Investment Centre, and these are time-limited rather than permanent. This applies whether your business is in manufacturing, hospitality, agriculture, or retail, making it a broad structural constraint rather than a sector-specific one.

The minimum capital threshold for foreign-owned companies is set significantly higher than for locally owned entities, and under the Tanzania Investment Act, foreign investors are generally required to demonstrate a minimum capital investment of USD 500,000 for a foreign-owned company or USD 100,000 for a joint venture with Tanzanian partners. These figures are separate from registration fees and do not account for working capital, infrastructure costs, or compliance expenditure. Locking up that level of capital before your business generates revenue creates a substantial financial barrier, particularly for small and mid-sized foreign firms.

To a degree, yes, but at significant cost. Businesses operating outside Dar es Salaam frequently invest in their own power generation, water supply, and logistics capacity because public infrastructure is unreliable. Those private solutions add considerable overhead that would not apply in a more developed market, and they must be factored into your financial modelling before committing to an upcountry location.

Commercial lending rates in Tanzania frequently exceed 20% per annum, which is high even by regional standards, making local debt financing an impractical option for most foreign-owned companies. In Kenya, for comparison, commercial rates have historically been lower and the capital market is more developed, offering additional financing instruments that are not readily available in Tanzania. For foreign businesses, this gap means you will almost certainly need to self-fund or secure financing outside Tanzania, which requires careful structuring to comply with TRA's transfer pricing and thin capitalisation rules.

A delayed certificate of incorporation from BRELA directly delays your ability to register for a Taxpayer Identification Number with TRA, which in turn blocks you from opening a corporate bank account or entering formal contracts. Since TRA registration cannot proceed without a confirmed BRELA registration number, any backlog in the BRELA process creates a cascading delay across your entire pre-operational setup. There is no parallel-processing option that allows you to begin TRA registration before BRELA formalities are complete.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.