Key Takeaways

- Tanzania's business registration framework is administered by BRELA under the Ministry of Industry and Trade, with company formation governed specifically by the Companies Act 2002.

- The Private Limited Company is the most widely used entity type in Tanzania, offering liability protection for both resident and foreign investors under a relatively straightforward BRELA registration process.

- Foreign businesses entering Tanzania can operate through a Branch Office without creating a separate legal person, making it a lower-commitment market entry option.

- Structures such as Sole Proprietorships and General Partnerships carry unlimited personal liability, limiting their practical suitability to small, low-risk operations under Tanzanian law.

Introduction to Entity Types in Tanzania

Tanzania sits in East Africa, bordered by Kenya, Uganda, Rwanda, Burundi, the Democratic Republic of Congo, Zambia, Malawi, and Mozambique, with the Indian Ocean coastline to the east and the semi-autonomous islands of Zanzibar forming part of its territory. It is an independent sovereign republic, and the types of business entities in Tanzania are governed primarily through the Business Registrations and Licensing Agency (BRELA), which operates under the Ministry of Industry and Trade.

Registration of companies falls under the Companies Act 2002, while other structures are governed by separate legislation including the Partnership Act and the Cooperative Societies Act. Tanzania operates a residence-based tax system administered by the Tanzania Revenue Authority.

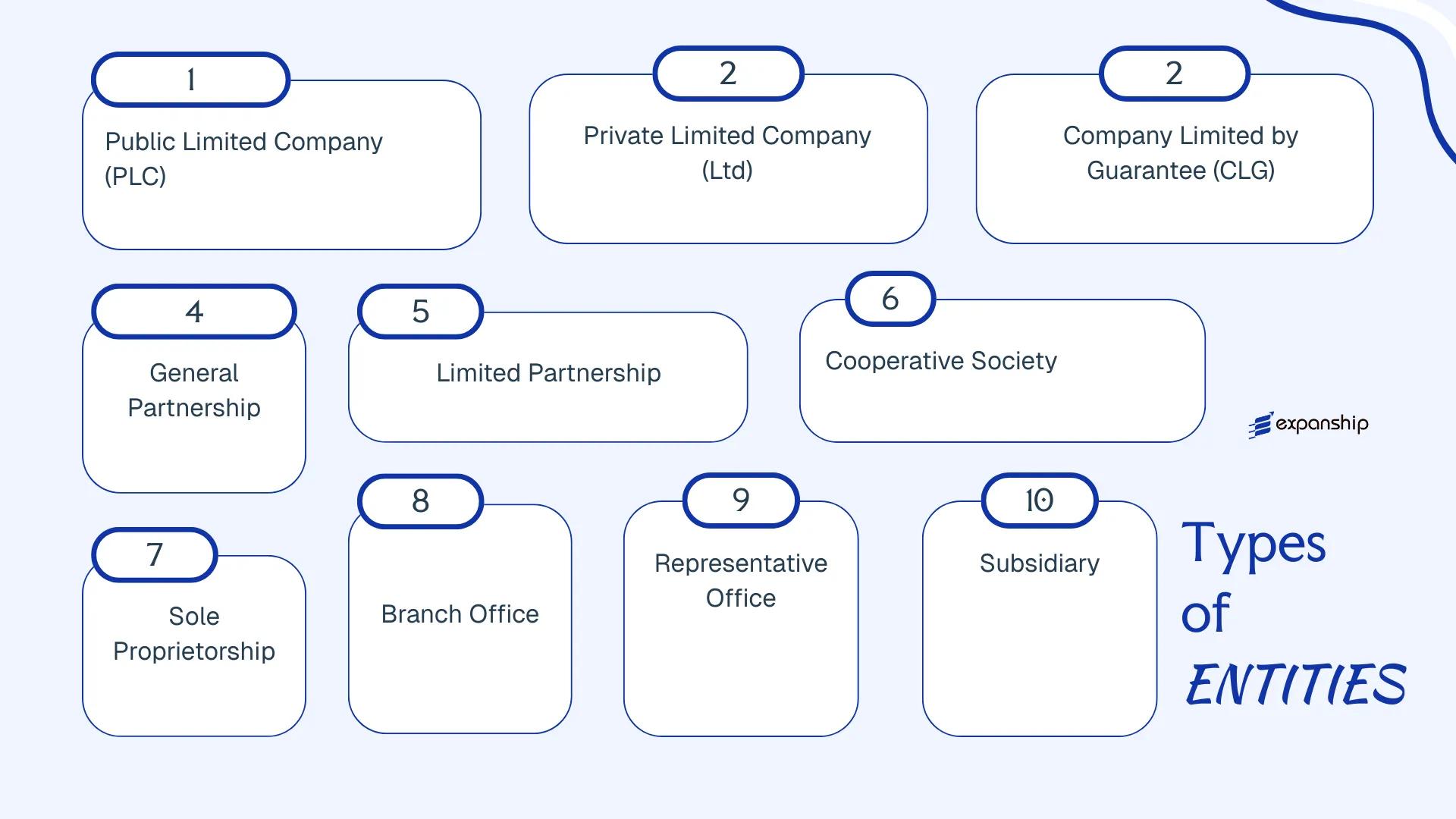

Businesses registering in the country can choose from several distinct legal forms: Public Limited Company, Private Limited Company, Company Limited by Guarantee, General Partnership, Limited Partnership, Cooperative Society, Sole Proprietorship, Branch Office, Representative Office, and Subsidiary. Each structure carries different implications for liability, ownership, taxation, and regulatory obligations. This article examines each of these forms in detail.

An Overview of Business Structures in Tanzania

Several entity types are available to businesses operating under the corporate law framework of Tanzania, with the primary legislation being the Companies Act 2002 (Cap. 212 R.E. 2002), administered by the Business Registrations and Licensing Agency (BRELA). Additional structures fall under separate statutes, including the Partnership Act and the Cooperative Societies Act. Each form carries distinct implications for liability, ownership, taxation, and permitted activities.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Public Limited Company (PLC) | Incorporated company | Limited to shares | Taxed | Yes | 2 shareholders | BRELA | Companies Act 2002 |

| Private Limited Company (Ltd) | Incorporated company | Limited to shares | Taxed | Yes | 1 shareholder | BRELA | Companies Act 2002 |

| Company Limited by Guarantee | Incorporated company | Limited to guarantee | Taxed / Exempt | Restricted | 1 member | BRELA | Companies Act 2002 |

| General Partnership | Unincorporated firm | Unlimited | Taxed | Yes | 2 partners | BRELA | Partnership Act |

| Limited Partnership | Unincorporated firm | Mixed | Taxed | Yes | 2 partners | BRELA | Partnership Act |

| Cooperative Society | Incorporated body | Limited | Taxed / Exempt | Yes | Varies | MUCCOBS | Cooperative Societies Act |

| Sole Proprietorship | Unincorporated business | Unlimited | Taxed | Yes | 1 owner | BRELA | Business Names Act |

| Branch Office | Foreign entity extension | Parent liable | Taxed | Yes | N/A | BRELA / TIC | Companies Act 2002 |

| Representative Office | Foreign entity extension | Parent liable | Generally exempt | No | N/A | TIC | Investment Act 1997 |

| Subsidiary | Incorporated company | Limited to shares | Taxed | Yes | 1 shareholder | BRELA | Companies Act 2002 |

Each of these structures is examined in full in the sections below.

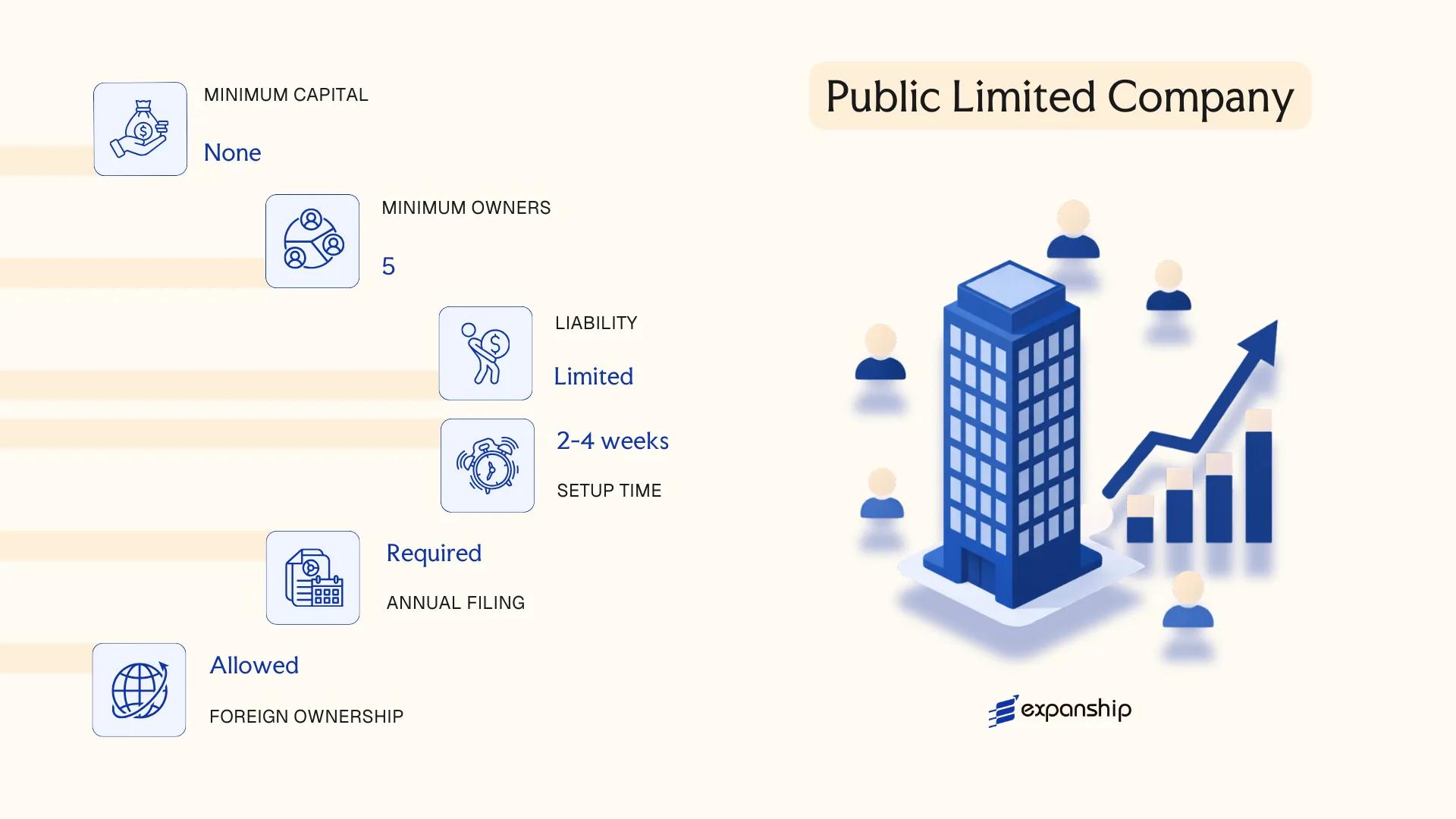

Public Limited Company (PLC) under the Companies Act 2002

A public limited company in Tanzania is governed by the Companies Act 2002 (Cap. 212), which consolidates the rules on formation, governance, and dissolution of companies registered in the country. As a primary keyword, the public limited company Tanzania Companies Act 2002 framework grants the entity separate legal personality, meaning it can own property, enter contracts, and incur liabilities independently of its shareholders.

Shares in a PLC are transferable and may be offered to the general public, including through listing on the Dar es Salaam Stock Exchange (DSE). This distinguishes the structure from a private company, where share transfers are restricted. Shareholders bear liability only to the extent of unpaid amounts on their shares.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Public Limited Company (PLC) | Incorporated under the Companies Act 2002 (Cap. 212) |

| Members | Shareholders; minimum 7, no maximum | Directors: minimum 2; a company secretary is required |

| Local Presence | Registered office in Tanzania; company secretary required | Registered office address must be maintained at all times |

| Capital | TZS-denominated; no statutory minimum share capital prescribed | Authorised and issued capital stated in the memorandum |

| Share Transferability | Shares freely transferable; may be offered to the public | DSE listing is optional but permitted |

| Privacy | Register of members and directors is publicly accessible | Annual filings with BRELA are publicly available |

Focus Points

- Taxation: Corporate income tax applies at 30% on net profits; VAT at 18% on taxable supplies; withholding tax rates vary by payment type; stamp duty applies on certain instruments.

- Annual Compliance: Annual returns, audited financial statements, and filing with the Business Registrations and Licensing Agency (BRELA) are mandatory.

- Economic Substance: No formal economic substance regime comparable to offshore jurisdictions; standard operational presence expected.

- Treaty Access: Tanzania has a limited network of double taxation agreements; PLC residents may access applicable treaties.

- Conversion: A PLC may be re-registered as a private limited company subject to shareholder approval and BRELA confirmation.

Closing

A PLC suits large-scale trading, infrastructure, or financial services businesses intending to raise capital from the public or pursue a DSE listing. The structure offers broad capital-raising capacity, but the compliance burden — including mandatory audits, public disclosure, and regulatory oversight — is significantly heavier than that of a private company.

Best suited for large enterprises or ventures planning to raise public capital or list on the Dar es Salaam Stock Exchange.

Company Incorporation in Tanzania

Incorporate your business entity in Tanzania with expert guidance on BRELA registration, compliance, and post-incorporation requirements.

Private Limited Company (Ltd) under the Companies Act 2002

Private limited company Tanzania Ltd registration is governed by the Companies Act 2002 (Cap. 212), which replaced the earlier colonial-era legislation and brought the framework broadly in line with modern commonwealth company law. The Act is administered by the Business Registrations and Licensing Agency (BRELA), operating under the Ministry of Industry and Trade.

A private limited company holds separate legal personality from its shareholders, meaning it can own property, enter contracts, and incur liabilities in its own name. Shareholder liability is capped at the amount unpaid on their shares, insulating personal assets from business debts.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private Company Limited by Shares | Incorporated under Companies Act 2002 (Cap. 212) |

| Members | Shareholders: min. 1, max. 50 | Shares cannot be offered to the general public |

| Directors | Min. 1 director required | At least one director must be a natural person |

| Local Presence | Registered office address in Tanzania; Company Secretary required | Registered office must be a physical address, not a P.O. Box |

| Capital | Minimum share capital: TZS 200,000 (general requirement); no statutory paid-up minimum for most private companies | Foreign-owned entities may face higher thresholds under TIRA or TIC licensing |

| Privacy | Shareholder register is filed with BRELA but not publicly searchable online | Beneficial ownership disclosure required under AML regulations |

Focus Points

- Taxation: Subject to corporate income tax at 30% on net profits; VAT registration required once turnover exceeds the statutory threshold; withholding tax applies to dividends, interest, and service fees paid to non-residents at rates generally ranging from 5% to 15% under domestic law or applicable tax treaties.

- Annual Compliance: Annual returns must be filed with BRELA; audited financial statements required; companies must maintain statutory books and registers.

- Treaty Access: Tanzania has double taxation agreements with several countries, including the UK, India, Canada, and Scandinavian nations, potentially reducing withholding tax burdens.

- Foreign Ownership: 100% foreign ownership is permitted in most sectors; however, certain strategic sectors require local equity participation under the Tanzania Investment Act.

- Conversion: A private limited company may be re-registered as a public limited company under the Companies Act 2002, subject to meeting the applicable share capital and governance thresholds.

A private limited company suits trading operations, holding structures, and joint ventures where liability protection and operational flexibility are both required. The separate legal personality is a significant structural benefit, though the 50-shareholder cap restricts equity fundraising beyond a closed investor group.

Small to medium-sized enterprises, wholly owned foreign subsidiaries, and joint ventures seeking limited liability without public disclosure obligations.

Company Limited by Guarantee

A company limited by guarantee Tanzania operates under the Companies Act 2002, the same legislation governing share-based companies, but carries a structurally distinct character. Instead of issuing shares, it draws its liability ceiling from the amount each member agrees to contribute in the event of winding up. This makes it a separate legal entity capable of entering contracts, holding property, and suing or being sued in its own name.

Registered with the Business Registrations and Licensing Agency (BRELA), this structure is used almost exclusively for non-commercial purposes. Charities, professional associations, sports clubs, and educational institutions commonly adopt it because surplus income is retained within the entity rather than distributed to members.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Incorporated entity with separate legal personality | Governed by the Companies Act 2002; registered through BRELA |

| Members | Minimum 2; no statutory maximum | Referred to as "members"; no shareholders or shares issued |

| Liability | Limited to the guaranteed amount per member | Guarantee amount is stated in the Memorandum of Association |

| Local Presence | Registered office within Tanzania required | Physical address; a P.O. Box alone does not suffice |

| Capital | No share capital; members provide a nominal guarantee | Guarantee amount is often set at TZS 10,000–50,000 per member |

| Privacy | Directors and members appear in public BRELA records | No share register, but membership lists may be disclosed |

Focus Points

- Taxation: Exempt from corporate income tax if registered as a non-profit and income is applied solely to stated objectives; VAT registration may still be required if taxable supplies exceed the threshold; donations received are generally not subject to withholding tax, though commercial income earned alongside charitable activity is taxable.

- Annual Compliance: Annual returns and audited financial statements must be filed with BRELA; larger entities receiving foreign funding may face additional reporting under the Non-Governmental Organisations Act.

- Restrictions: Distribution of profits or surpluses to members is prohibited; any commercial activity must remain incidental to the stated non-profit purpose.

- Conversion: Conversion from a guarantee company to a share-based company is not a standard procedure under the Act and would generally require dissolution and re-incorporation.

- Treaty Access: As a non-profit entity, access to Tanzania's double tax agreements is limited; treaty benefits apply primarily to income-generating entities.

Closing

This structure suits organisations whose purpose is civic, educational, or associational rather than commercial, with the primary advantage being the combination of legal personality and member liability protection without the need for share capital. The key limitation is the prohibition on profit distribution, which makes it unsuitable for any venture where financial returns to participants are expected.

Non-governmental organisations, trade associations, and membership bodies that require a formal legal structure without share capital or profit distribution.

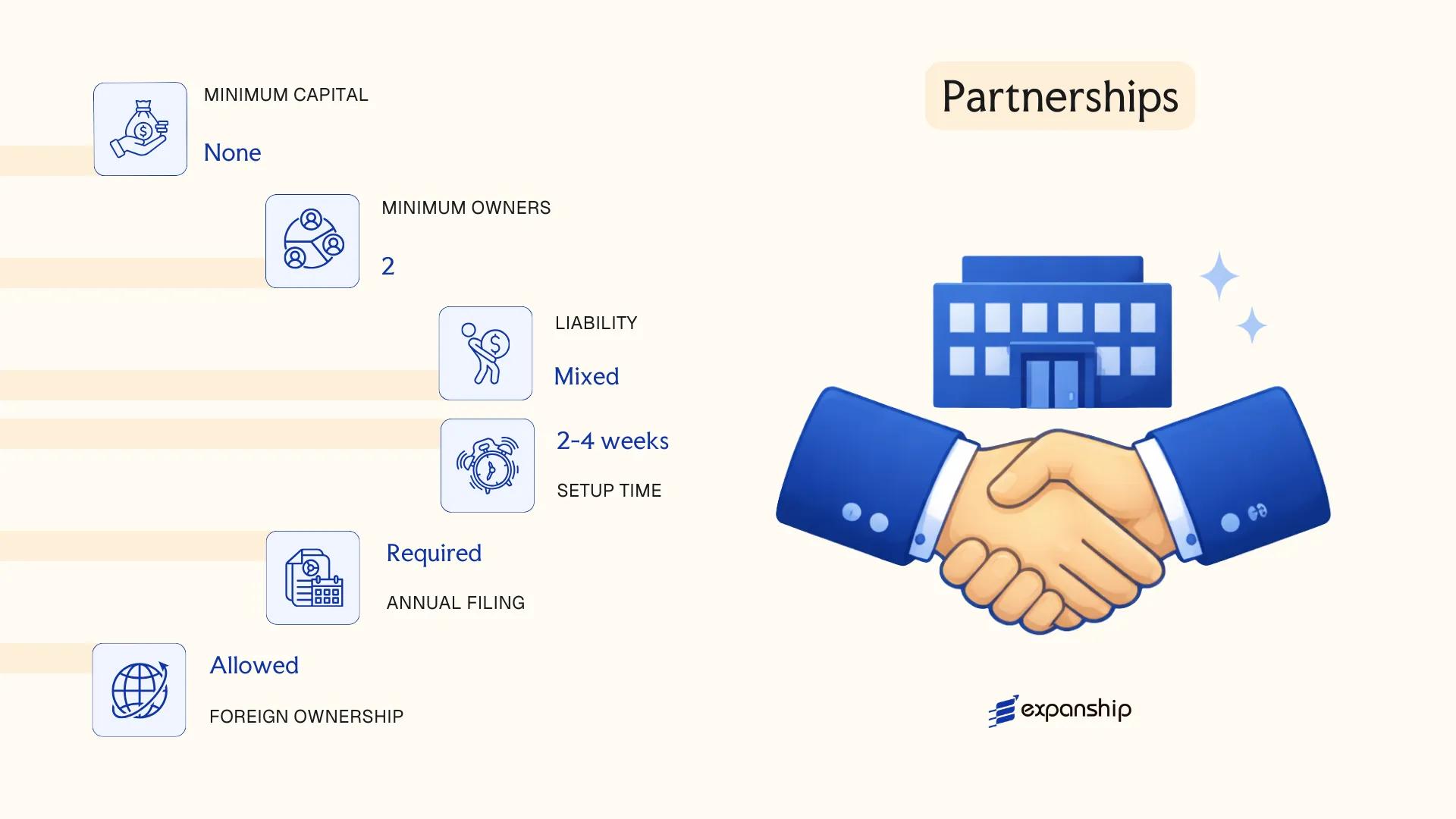

Partnerships in Tanzania [General Partnership, Limited Partnership]

Partnership registration in Tanzania for general and limited structures is governed by the Partnership Act, Cap. 375 of the Laws of Tanzania. A general partnership does not possess separate legal personality — partners bear unlimited joint and several liability for the firm's obligations. A limited partnership, by contrast, permits designated limited partners to cap their liability at the value of their capital contribution.

Registration is administered through the Business Registrations and Licensing Agency (BRELA). Both structures require filing with BRELA, and a limited partnership must clearly distinguish between general partners (who manage the firm and carry unlimited liability) and limited partners (who cannot participate in management without forfeiting their liability protection).

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated association | No separate legal personality in either structure |

| Members | Partners (general or limited) | Minimum 2; no statutory maximum specified |

| Liability | General: unlimited; Limited: capped at contribution | Limited partners lose protection if they participate in management |

| Local Presence | Registered office in Tanzania required | BRELA registration mandatory for both types |

| Capital | No statutory minimum; denominated in TZS | Contributions defined in the partnership agreement |

| Privacy | Partnership agreement not publicly filed in full | Basic registration details held by BRELA |

Focus Points

- Taxation: Partnerships are fiscally transparent; profits are taxed in the hands of individual partners under the Income Tax Act 2004, at applicable individual or corporate rates depending on partner type; VAT registration required if turnover exceeds the threshold.

- Annual Compliance: Partners must file annual returns with BRELA and maintain proper accounting records.

- Treaty Access: Fiscal transparency means the partnership itself does not directly access Tanzania's double tax agreements; treaty eligibility depends on each partner's residence.

- Restrictions: Foreign nationals may face ownership restrictions in certain regulated sectors regardless of partnership structure.

- Conversion: A partnership can be converted to a limited company under the Companies Act 2002, subject to BRELA procedures.

Sub-Types

General Partnership

All partners hold equal management rights and carry unlimited personal liability for the firm's debts. This structure is common among professional service providers such as law firms and accounting practices.

Limited Partnership

At least one general partner manages the business and bears unlimited liability, while one or more limited partners contribute capital without taking part in day-to-day operations. This structure is used where passive investors require liability capped at their contributed capital.

Closing

Partnerships suit professional service firms and joint ventures where participants prefer a flexible, agreement-driven governance structure over a formal corporate framework. The absence of a minimum capital requirement lowers the entry barrier, though unlimited liability for general partners represents a significant exposure that should be assessed against the nature of the business activities.

Partnerships in Tanzania are best suited for professional practices or small joint ventures where the partners have an established level of mutual trust and wish to avoid the full compliance burden of a limited company.

Cooperative Society under the Cooperative Societies Act

Cooperative society registration Tanzania is governed by the Cooperative Societies Act, Cap. 211, which provides the legal basis for forming member-owned enterprises across agricultural, financial, housing, and consumer sectors. A registered cooperative acquires separate legal personality upon registration, meaning it can own property, enter contracts, and sue or be sued in its own name. Liability of members is generally limited to their share contributions, making this a hybrid structure that combines collective ownership with formal legal protection.

Registration is handled by the Registrar of Cooperative Societies, operating under the Ministry responsible for cooperatives. The entity must adopt bylaws conforming to the Act and submit them as part of the registration process.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Separate legal entity | Registered under the Cooperative Societies Act, Cap. 211 |

| Members | Referred to as members; minimum 10 individuals | No statutory maximum; membership is open and voluntary |

| Governance | Managed by an elected Board of Directors | Officers include Chairperson, Secretary, and Treasurer |

| Registered Office | Physical address required within Tanzania | Must be maintained throughout the cooperative's existence |

| Share Capital | Denominated in TZS; no prescribed statutory minimum | Capital raised through member share subscriptions |

| Privacy | Bylaws and member registers accessible to members | Not fully private; regulatory filings are subject to inspection |

Focus Points

- Taxation: Cooperatives are subject to corporate income tax at the standard 30% rate; VAT applies to taxable supplies; withholding tax obligations apply on dividends and service payments; agricultural cooperatives may qualify for certain exemptions under the Income Tax Act.

- Annual Compliance: Annual general meetings are mandatory; audited financial statements must be submitted to the Registrar of Cooperative Societies each year.

- Economic Substance: No formal economic substance regime applies, but cooperatives must demonstrate active operations and member participation to maintain registration.

- Conversion: A cooperative society cannot be directly converted into a company under the Companies Act 2002; dissolution and re-incorporation as a separate entity would be required.

- Restrictions: Cooperatives must operate for the mutual benefit of members; profit distribution to non-members is not permitted.

Sub-Types

Primary Cooperative Society

Formed directly by individual members, this is the base-level cooperative. It serves members within a defined locality or sector and is the most common formation used for agricultural marketing, savings and credit, and consumer goods.

Secondary Cooperative Society (Union)

A union is formed by two or more primary cooperative societies rather than by individual members. It exists to coordinate activities and provide shared services to its constituent primaries, such as bulk purchasing or collective marketing.

Apex Cooperative Society

Formed by unions or secondary societies at the national level, an apex body represents the interests of cooperatives across an entire sector or the country. Membership is restricted to registered secondary societies.

When to Use This Structure

A cooperative society suits member-based enterprises where profits are shared according to participation rather than capital investment, particularly in agriculture, microfinance through SACCOs, and consumer trade. Its main advantage is the collective bargaining power it extends to members who would otherwise operate individually. The principal limitation is restricted access to external equity investment, as ownership cannot be extended to outside investors in the way a company structure permits.

This structure is most appropriate for groups of individuals or organisations seeking a legally recognised, member-governed entity for collective economic activity, particularly in agricultural or financial cooperative sectors.

Sole Proprietorship

Sole proprietorship registration in Tanzania falls under the Business Licensing Act and is administered at the local government level, with the Business Registrations and Licensing Agency (BRELA) handling business name registration under the Business Names (Registration) Act, Cap. 213. Unlike a limited company, a sole proprietorship carries no separate legal personality — the owner and the business are legally the same person, meaning personal assets are exposed to business liabilities without restriction.

Registration is straightforward. The proprietor registers a business name with BRELA if trading under a name other than their own, then obtains the relevant business licence from the local authority in the area of operation.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated sole proprietorship | No separate legal personality from the owner |

| Members | Single proprietor | No minimum capital; no co-owners permitted |

| Local Presence | Physical place of business; local authority licence | Business must operate within a licensed premises |

| Capital | TZS; no statutory minimum | Owner funds the business directly |

| Registration Body | BRELA (business name) + Local Government Authority (licence) | Both registrations are required to operate legally |

| Privacy | Business name and owner details are publicly registered | No share register or director filings |

Focus Points

- Taxation: Subject to personal income tax under the Income Tax Act, Cap. 332; VAT registration is required once annual turnover exceeds the prescribed threshold (currently TZS 200 million); no corporate income tax applies.

- Annual Compliance: Business licence renewal is required annually through the relevant local authority; no statutory audit obligation.

- Treaty Access: No access to double tax treaties, which apply only to corporate entities.

- Conversion: Can be converted into a private limited company by incorporating a new entity and transferring business assets; no automatic conversion mechanism exists under Tanzanian law.

- Restrictions: Foreign nationals face significant restrictions on operating as sole traders; the Business Activities (Prohibition) Act reserves several business categories exclusively for Tanzanian citizens.

Closing

A sole proprietorship suits small-scale trading, artisan services, and early-stage local businesses where simplicity of operation outweighs the need for liability protection. The absence of incorporation formalities reduces setup costs, but unlimited personal liability remains a substantial structural risk for any business with meaningful contractual or financial exposure.

Tanzanian citizens running small, owner-operated businesses with low liability exposure and no immediate plans for external investment or expansion.

Foreign Business Structures in Tanzania [Branch Office, Representative Office, Subsidiary]

Registering a foreign company branch office Tanzania requires compliance with the Companies Act 2002, which governs the establishment of overseas entities operating within the country. Under Part XII of the Act, a foreign company must register with the Business Registrations and Licensing Agency (BRELA) within one month of establishing a place of business locally.

A branch office does not constitute a separate legal entity — it remains an extension of the parent company, which retains full liability for its operations. A subsidiary, by contrast, is incorporated as a local private limited company and carries separate legal personality, with liability confined to its own assets.

Key Characteristics

| Requirement | Branch Office | Representative Office | Subsidiary |

|---|---|---|---|

| Legal Form | Extension of parent; no separate legal personality | Extension of parent; no separate legal personality | Locally incorporated private limited company |

| Members / Officers | Local authorised agent; parent directors govern | Local authorised agent appointed | Directors and shareholders per Companies Act 2002 |

| Local Presence | Registered physical address; authorised local agent mandatory | Registered address; authorised agent required | Registered office; resident director generally required |

| Capital | No minimum prescribed; parent's capital structure applies | No minimum prescribed | No statutory minimum share capital |

| Permitted Activities | Trading and commercial operations | Non-trading only (liaison, market research, promotion) | Full range of commercial activities |

| Privacy | Parent financials may require disclosure to BRELA | Limited disclosure obligations | Statutory filing requirements apply |

Focus Points

- Taxation: Branch profits are subject to corporate income tax at 30%; VAT registration is required once taxable turnover thresholds are met; withholding tax applies to remittances and service payments; a representative office with no taxable income may have reduced obligations, but tax residency rules still apply.

- Economic Substance: No formal economic substance regime analogous to some offshore jurisdictions, but genuine local operations are expected to support tax positions.

- Annual Compliance: Branch and subsidiary entities must file annual returns with BRELA; audited financial statements are required for companies meeting prescribed thresholds under the Companies Act 2002.

- Treaty Access: Tanzania maintains a limited network of double taxation agreements; subsidiaries incorporated locally generally have stronger treaty standing than branches.

- Restrictions: Representative offices are prohibited from generating revenue or entering commercial contracts directly; foreign ownership in certain sectors may require partnership with local entities under sector-specific legislation.

Sub-Types

Branch Office

A branch is registered under Part XII of the Companies Act 2002 and carries no legal separation from its parent. It suits foreign firms that require direct operational presence without incorporating a new entity.

Representative Office

A representative office is confined strictly to non-commercial functions such as liaison, market research, and promotion. It cannot invoice clients or generate revenue, making it appropriate only for market entry reconnaissance or coordination activities.

Foreign Subsidiary

Incorporated as a local private limited company, the subsidiary is the only structure that provides full legal separation from the parent. Foreign ownership is permissible in most sectors, subject to the Tanzania Investment Act 1997 and relevant sector regulations.

A branch or representative office suits firms testing the market or coordinating regional operations, while a subsidiary is the standard structure for sustained commercial activity given its separate legal standing and cleaner tax position. One key limitation of operating through a branch is that the parent company bears unlimited liability for all local obligations.

Foreign companies intending to conduct active trading operations in Tanzania are best served by incorporating a local subsidiary under the Companies Act 2002.

How to Choose the Right Entity Type in Tanzania

Choosing the right business entity in Tanzania determines your tax exposure, compliance burden, and legal capacity to operate — and errors at the formation stage are rarely simple to reverse.

Why Your Entity Choice Matters

The structure you register has direct legal and financial consequences:

- Registering a foreign branch when BRELA requires a locally incorporated company for your activity type can result in regulatory penalties or forced dissolution.

- Selecting a tax-exempt structure disqualifies your business from claiming reduced withholding tax rates under Tanzania's double taxation agreements, since treaty access generally requires resident taxpayer status.

- Forming a private limited company for a single-person consultancy subjects you to annual audit requirements and filing obligations that add costs disproportionate to your operating scale.

- Choosing a structure without the legal capacity to hold property or enter contracts in Tanzania exposes transactions to enforceability risk under the Companies Act 2002.

Key Factors to Consider

- Business Activity: Active trading, passive asset holding, and regulated sectors such as banking or insurance each require distinct entity types under Tanzanian law.

- Ownership Structure: A sole director-shareholder arrangement suits a private limited company, while multi-party ventures with profit-sharing arrangements may fit a partnership registered under the Partnership Act.

- Tax Objectives: Your need for treaty access, sector-specific incentives, or Tanzania Revenue Authority exemptions should guide structure selection before incorporation.

- Substance Capacity: If you cannot maintain a physical office, resident staff, or local decision-making, confirm whether your chosen entity type carries substance obligations under applicable regulations.

- Public Disclosure Tolerance: Directors and shareholders of companies registered with BRELA appear on a public register; partnerships offer different disclosure profiles.

- Exit Flexibility: Not all Tanzanian entity types permit conversion, redomiciliation, or straightforward winding-up — verify the exit mechanism before committing to a structure.

Compliance Services for Companies in Tanzania

Maintain your legal standing with BRELA and the Tanzania Revenue Authority through structured compliance support.

Conclusion

Selecting the right structure is the first binding decision your business makes under Tanzanian law, and this Tanzania company incorporation summary guide reflects how varied those choices are. The Private Limited Company remains the most commonly registered entity, favored by resident and foreign investors alike for its liability protection and relatively straightforward registration through BRELA under the Companies Act 2002. A Branch Office suits foreign firms testing the market without establishing a separate legal person. Cooperative Societies serve member-based commercial activity, while a Company Limited by Guarantee fits non-profit purposes. Sole Proprietorships and General Partnerships carry unlimited liability, making them more appropriate for small, low-risk operations.

Tanzania continues to refine its investment framework, with the Tanzania Investment Centre actively updating procedures and the country's tax treaty network gradually expanding. Professional legal and corporate advisory support becomes relevant at the point where entity selection intersects with sector-specific licensing requirements.

How Expanship Can Assist You

Expanship company registration Tanzania services cover the full incorporation process, from entity selection through to certificate issuance by the Business Registrations and Licensing Agency (BRELA). Whether your preference is a private limited company under the Companies Act 2002, a branch office, or any other structure discussed in this guide, our team handles the procedural groundwork so your business is properly constituted from day one.

From document preparation to ongoing compliance, our service scope includes:

- Memorandum and Articles of Association drafting and notarization

- BRELA filing and company name reservation

- Registered office and local agent provision

- Tanzania Revenue Authority (TRA) tax registration

- Post-incorporation compliance management, including annual returns

- Banking introduction assistance

Reach out to Expanship Tanzania to discuss your specific requirements with our corporate services team.

Frequently Asked Questions (FAQ)

Among the options available under the Companies Act 2002, the private limited company (Ltd) is the most frequently incorporated structure. Its combination of limited liability, a single-shareholder minimum, and suitability for both resident and foreign ownership makes it the default choice for most business incorporation FAQ searches related to Tanzania.

A private limited company restricts share transfers and cannot solicit public investment, whereas a public limited company (PLC) may list on the Dar es Salaam Stock Exchange and offer shares to the public. The PLC carries significantly heavier disclosure and governance obligations under the Companies Act 2002, including mandatory audited financial reporting filed with BRELA.

A company limited by guarantee does not issue shares, so there is no public shareholder register reflecting ownership stakes. Nominee arrangements are available for directors in Tanzania, though beneficial ownership disclosure requirements have tightened under anti-money laundering regulations administered by the Financial Intelligence Unit.

A sole proprietorship and a private limited company can each be established by a single individual. Partnerships, by definition under Tanzanian law, require a minimum of two partners, and cooperative societies require a substantially larger founding membership under the Cooperative Societies Act.

Foreign nationals may register a private limited company, a public limited company, or establish a branch office or subsidiary through the Business Registrations and Licensing Agency (BRELA) and the Tanzania Investment Centre (TIC). Foreign investors in designated sectors must comply with minimum capital thresholds and local partnership requirements set by the Tanzania Investment Act 1997.

Conversion between certain entity types is permissible under the Companies Act 2002; a private limited company may re-register as a public limited company upon meeting the prescribed conditions. Conversion from a corporate structure to a partnership, however, is not a direct statutory process and would generally require dissolution and fresh registration.

Private limited companies, public limited companies, and companies limited by guarantee each possess separate legal personality distinct from their members. Sole proprietorships and general partnerships do not, meaning the owner or partners bear personal liability for business obligations without a corporate shield.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.