Key Takeaways

- Foreign investors benefit from Tanzania's 30% corporate tax rate under the Income Tax Act, which is paired with depreciation allowances and capital expenditure deductions that reduce effective tax burden during the critical early years of operation.

- Companies registered through BRELA gain access to the East African Community's integrated market under the Treaty for the Establishment of the East African Community, eliminating the need to incorporate separately across member states to reach regional customers.

- Entities that register with the Tanzania Investment Centre can unlock sector-specific incentive packages that materially lower the cost of capital-intensive or export-oriented operations from the outset.

- Agriculture, extractive, and manufacturing businesses stand to benefit from a distinct combination of TIC incentive structures and licensing frameworks that are calibrated specifically to Tanzania's natural resource base and economic development priorities.

Situated in East Africa along the Indian Ocean coast, Tanzania is an independent sovereign republic and one of the continent's larger economies by landmass and population. Foreign businesses typically incorporate here as a Private Limited Company, registered through the Business Registrations and Licensing Agency (BRELA), which serves as the principal authority overseeing company formation and commercial licensing. The country operates a residence-based tax system administered by the Tanzania Revenue Authority, with corporate tax obligations applying to locally sourced and, in certain circumstances, foreign-sourced income.

Openness to foreign direct investment is reflected in the legal framework governing business entry, with most sectors permitting overseas participation subject to minimum capital thresholds and sector-specific regulations. Understanding the benefits of incorporating in Tanzania requires examining several distinct areas — from ownership rules and investment incentives to trade access and workforce economics.

This article outlines the key advantages your business stands to gain by registering a corporate entity here.

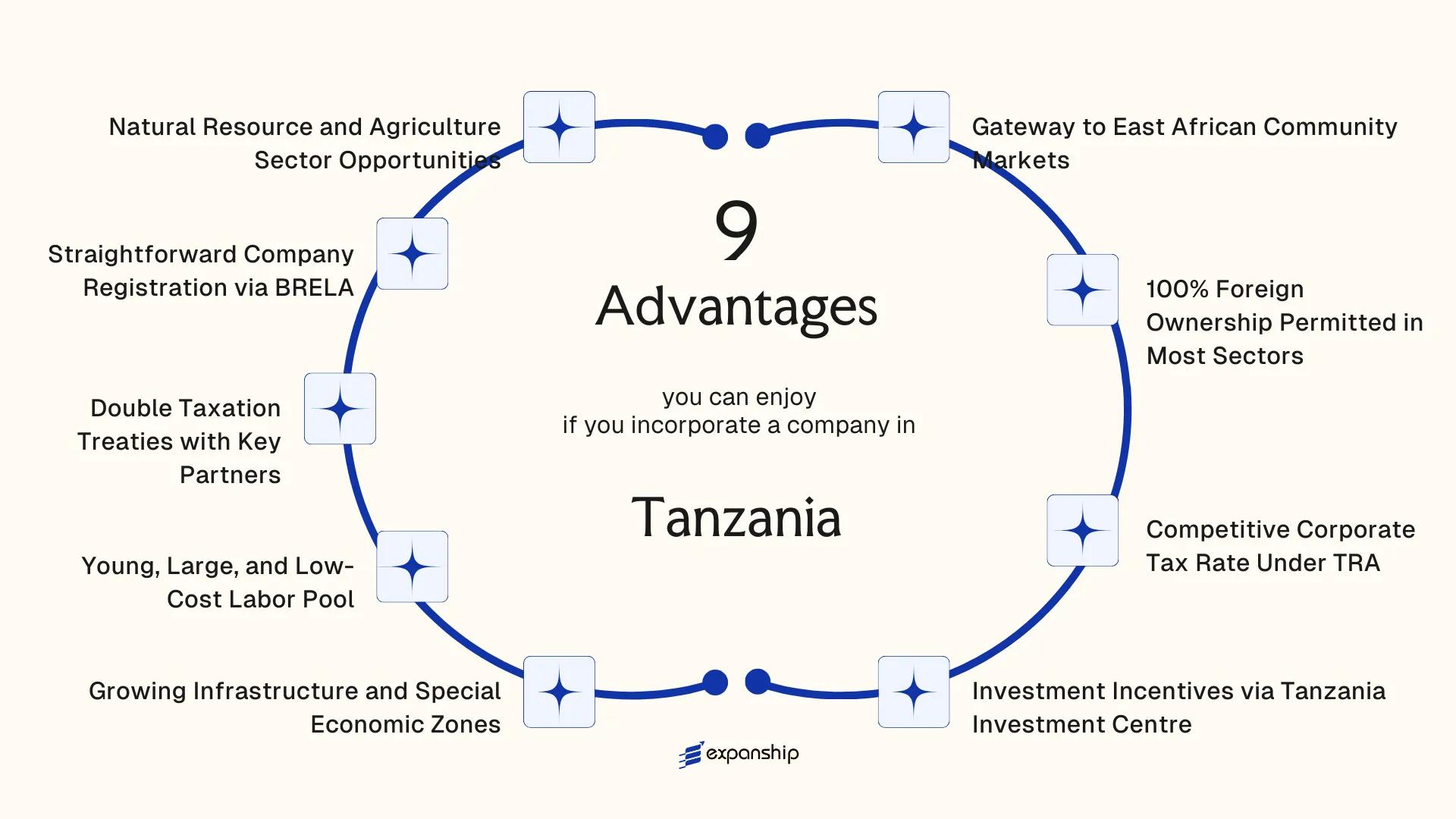

Gateway to East African Community Markets

Tanzania's position as a Tanzania gateway to East African Community markets gives incorporated businesses direct access to a trading bloc of over 300 million consumers across seven member states, governed by the EAC Treaty and its subsequent protocols on the customs union and common market.

Preferential Trade Access Within the Bloc

Under the EAC Customs Union Protocol, goods produced by a registered entity in Tanzania move across partner state borders at zero or reduced tariff rates. This means your business avoids the import duties that non-member competitors face when supplying the same markets from outside the bloc.

Strategic Geographic Position

Dar es Salaam and the port of Tanga serve as primary entry points for landlocked EAC members including Uganda, Rwanda, and Burundi. A company incorporated here gains proximity to those supply chains, reducing logistics costs that would otherwise affect pricing competitiveness in those markets.

A Tanzania-incorporated entity operates inside the EAC's preferential trade framework from day one, giving your goods and services a structural cost advantage over suppliers based outside the bloc.

100% Foreign Ownership Permitted in Most Sectors

Under the Tanzania Investment Act of 1997, foreign nationals are permitted to hold 100% foreign ownership Tanzania companies across the majority of commercial sectors. This means your business does not require a local partner or co-investor to satisfy ownership thresholds, a requirement that remains common in several other African markets. Full equity control allows you to make decisions on profit distribution, operational direction, and exit strategy without negotiating with a mandatory local shareholder.

The Tanzania Investment Centre (TIC) registers and facilitates wholly foreign-owned entities, and its Certificate of Incentives formalizes your ownership rights within the statutory framework. Once registered, your entity has the same legal standing as a domestically owned firm under Tanzanian law.

Sectors open to complete foreign ownership include:

- Manufacturing and processing, where no minimum local equity is prescribed

- Tourism and hospitality, a sector with active TIC facilitation

- ICT and financial services, which have attracted significant foreign direct investment

- Agriculture-linked commercial ventures outside smallholder-reserved categories

Reserved sectors do exist. Certain activities, including small-scale mining and specific retail trade thresholds, are restricted to Tanzanian citizens under the Business Activities (Prohibition) Act. Outside these categories, however, a wholly foreign-owned company structure is legally uncomplicated to establish and maintain.

Company Incorporation in Tanzania

Register a wholly foreign-owned company in Tanzania with guidance from Expanship's corporate services team.

Competitive Corporate Tax Rate Under TRA

Tanzania's standard corporate income tax rate sits at 30% for resident companies, administered by the Tanzania Revenue Authority (TRA) under the Income Tax Act, Cap. 332. For newly listed companies on the Dar es Salaam Stock Exchange, a reduced rate of 25% applies for three consecutive years following listing, provided that at least 30% of shares are floated to the public.

| Entity Type | Applicable Rate | Condition |

|---|---|---|

| Resident company (general) | 30% | Standard rate |

| Newly listed DSE company | 25% | Min. 30% public float; first 3 years |

| Non-resident company | 30% | On Tanzania-sourced income only |

| Newly incorporated startup (priority sectors) | Variable | Subject to TIC approval |

For foreign investors, the 30% rate is applied only to Tanzania-sourced income for non-resident entities, which limits the tax base to locally generated profits rather than global earnings. This territoriality principle reduces your firm's exposure compared to jurisdictions that tax worldwide income at the corporate level.

The TRA also permits deductions on qualifying business expenses, depreciation allowances, and certain capital expenditures under Part IV of the Income Tax Act, which can meaningfully reduce a company's effective tax rate below the statutory 30%. The gap between statutory and effective rates is often where the real fiscal advantage materialises for well-structured foreign-owned businesses operating in the country.

Investment Incentives via Tanzania Investment Centre

The Tanzania Investment Centre (TIC) operates as the primary government body administering investment incentives under the Tanzania Investment Act, Cap. 38. Registering with the TIC and obtaining a Certificate of Incentives unlocks a defined package of fiscal and non-fiscal benefits that a standard business registration through BRELA does not automatically provide.

Holding a Certificate of Incentives entitles your business to import capital goods, including machinery and equipment, free of customs duty and VAT. For capital-intensive projects, this alone can represent a significant reduction in initial setup costs before operations generate revenue.

Beyond import relief, TIC-registered entities benefit from guaranteed repatriation of profits and capital. This protection is grounded in the Investment Act itself, reducing exposure to arbitrary capital controls. Foreign investors committing to qualifying sectors such as manufacturing, tourism, or agribusiness may also access land through TIC-facilitated processes, which is otherwise restricted under general land tenure rules.

The minimum capital threshold for foreign investors seeking TIC registration is USD 500,000, while for joint ventures with Tanzanian nationals it is USD 100,000.

Keep the following in mind:

- Certificate of Incentives must be maintained through compliance with TIC reporting requirements

- Incentives apply to approved projects, not to all activities a company may later undertake

- Capital goods imported duty-free must be used within the approved project scope

- Misuse of incentives can result in revocation of the Certificate and recovery of waived duties

A TIC Certificate of Incentives does not require the company to be newly incorporated; an existing Tanzanian-registered firm can apply retroactively if its project meets the qualifying criteria.

Growing Infrastructure and Special Economic Zones

Tanzania Special Economic Zones business benefits are most clearly visible through the Export Processing Zones Authority (EPZA), the regulatory body that administers both Export Processing Zones (EPZs) and Special Economic Zones (SEZs) under the Export Processing Zones Act and the Special Economic Zones Act. These two frameworks offer distinct but overlapping incentive packages that directly reduce operating costs for foreign-owned entities.

Tax and Duty Structures Inside the Zones

Companies operating within designated EPZs receive a ten-year corporate tax holiday, followed by a reduced rate thereafter, along with exemptions from withholding tax on dividends and import duties on capital goods and raw materials. For a manufacturing or logistics firm, this means the cost baseline during the critical early years of operations is structurally lower than it would be outside the zones. EPZ status requires that at least 80% of production be destined for export, which determines eligibility from the outset.

SEZs carry a broader mandate. Unlike EPZs, they accommodate firms selling to both export and domestic markets, making them accessible to businesses with mixed revenue models.

Physical Infrastructure Supporting Zone Operations

Dedicated zones such as the Benjamin William Mkapa SEZ in Morogoro and the Bagamoyo Economic Zone project are designed around industrial-grade utilities, road access, and port connectivity. For an investor in manufacturing or distribution, co-location within a serviced zone removes the need to independently secure and fund infrastructure that many greenfield sites in the region require. This distinction has a direct effect on capital allocation from day one.

Structure Your Tanzania Setup to Access SEZ Benefits

Our team can assess whether EPZ or SEZ registration aligns with your business model and walk you through the EPZA qualification process.

Young, Large, and Low-Cost Labor Pool

Tanzania's low-cost labor pool advantages are among the most quantifiable for manufacturing, agriculture, and services firms looking to keep operational costs contained. The country's population exceeded 63 million as of recent census estimates, with a median age below 18 years. That demographic profile means a growing working-age cohort entering the labor market each year, giving employers consistent access to entry-level and trainable workers without the supply constraints common in older economies.

- Minimum wage rates in Tanzania are set by sector through the Employment and Labour Relations Act, Cap. 366, and the National Minimum Wages Order. Rates vary by industry but remain materially lower than regional peers in comparable sectors, which directly reduces your firm's base payroll cost.

- A young workforce is disproportionately available for skills-based training programs, allowing businesses to shape competencies around their operational model rather than inheriting entrenched practices.

- The workforce size reduces dependence on any single labor pool region. Urban centers like Dar es Salaam and Mwanza, alongside secondary towns, give your entity geographic flexibility when siting operations.

- For investors in export-oriented sectors operating through Special Economic Zones, labor cost advantages compound against the backdrop of reduced duty exposure, improving unit economics on exports.

Double Taxation Treaties with Key Partners

Tanzania double taxation treaty benefits apply to a defined network of bilateral agreements that directly reduce withholding tax exposure on dividends, interest, and royalties paid across borders. For a foreign company operating here, these treaties can mean the difference between a tax-efficient structure and being taxed twice on the same income stream.

Concluded treaties include agreements with Canada, Denmark, Finland, India, Italy, Norway, Sweden, and Zambia, among others. Each treaty sets reduced withholding rates on specific income types, overriding the domestic rates that would otherwise apply under the Income Tax Act, Cap. 332.

India, for instance, is a significant trade and investment partner in the region. Under the Tanzania-India treaty, withholding tax on dividends and technical fees is capped below standard domestic rates, reducing the cost of repatriating profits to an Indian parent company.

Hypothetical scenario: A Swedish firm receiving TZS 500 million in dividends from its Tanzanian subsidiary would pay withholding tax at the treaty-reduced rate rather than the standard 10% domestic rate under the Income Tax Act. On that sum, even a 5-percentage-point reduction saves approximately TZS 25 million per distribution cycle.

Treaty eligibility generally requires the recipient entity to meet the residency conditions specified in each individual agreement.

Straightforward Company Registration via BRELA

Tanzania BRELA company registration advantages begin with the agency itself. The Business Registrations and Licensing Agency (BRELA) operates as the single point of registration for companies incorporated under the Companies Act (Cap. 212). Foreign investors do not need to work through multiple ministries to establish a legal entity, which reduces administrative friction and shortens the timeline from decision to operational status.

BRELA's online registration portal allows applicants to submit incorporation documents electronically. For a private limited company, the core requirements include a memorandum and articles of association, details of directors and shareholders, and a registered local address. This defined documentation structure means your legal advisors can prepare filings without ambiguity about what the regulator expects.

Registered entities receive a Certificate of Incorporation, which then supports downstream processes such as TIN registration with the Tanzania Revenue Authority and sector-specific licensing. Each step follows a sequential but predictable path, reducing the risk of delays caused by unclear procedural requirements.

Foreign-owned companies in certain regulated sectors may require additional approvals from sector-specific authorities before the Certificate of Incorporation can be used to commence operations.

Natural Resource and Agriculture Sector Opportunities

Tanzania natural resources investment opportunities span mining, hydrocarbons, forestry, and agriculture — each governed by a distinct regulatory framework that defines the terms under which foreign capital can participate.

Mining and Extractives

The Mining Act (Cap. 123) and the Natural Wealth and Resources Acts of 2017 govern mineral rights and revenue-sharing arrangements. Foreign firms may hold prospecting licences and mining licences, though the government retains a minimum 16% free-carried interest in mining projects under the 2017 legislation. This statutory structure means your entity enters with a defined ownership ceiling, which allows for accurate financial modeling at the pre-incorporation stage.

Gold, tanzanite, nickel, coal, and natural gas are among the commercially significant resources. The Tanzania Petroleum Development Corporation (TPDC) oversees upstream oil and gas activities, and foreign firms participate through production-sharing agreements.

Agriculture and Agribusiness

Arable land availability combined with varied climate zones across the country supports production of:

- Coffee, tea, and tobacco as established export crops

- Cashew nuts, a commodity with strong Asian market demand

- Sisal, of which the country has historically been among the top global producers

- Horticulture and floriculture with export access via EAC trade corridors

The Agriculture (Amendment) Act and the Tanzania Investment Centre both provide frameworks under which agribusiness ventures can access designated land and qualify for sector-specific incentives. Foreign firms investing through TIC registration may access land facilitation support, which is otherwise a more complex process under general land law.

How Tanzania Stacks Up Against Regional Rivals

Kenya and Uganda are the natural comparison points for any investor evaluating East Africa. Both share EAC membership with Tanzania, target overlapping categories of foreign investment, and compete directly for manufacturing, logistics, and services-sector capital. Comparing these three on parameters relevant to corporate structure reveals that Tanzania holds a measurable position on several dimensions that affect operating costs and regulatory exposure.

Where Kenya's corporate tax rate sits at 30% for resident companies and Uganda applies the same standard rate, Tanzania's 30% rate is equivalent — but the availability of TIC-administered incentives, including reduced rates and tax holidays in qualifying sectors, shifts the effective burden meaningfully. Registration timelines and minimum capital thresholds also vary across the three, with practical consequences for how quickly a foreign entity can begin operating and how much capital it must commit at the outset.

| Parameter | Tanzania | Kenya | Uganda |

|---|---|---|---|

| Standard Corporate Tax Rate | 30% (reduced rates available via TIC incentives) | 30% | 30% |

| Minimum Share Capital (General) | No statutory minimum for most private companies | No statutory minimum | No statutory minimum |

| Foreign Ownership (General Sectors) | Up to 100% permitted | Up to 100% permitted | Up to 100% permitted |

| EAC Member | Yes | Yes | Yes |

| SEZ/EPZ Framework | Yes (EPZA-administered) | Yes | Yes |

| Company Registration Body | BRELA | Business Registration Service (BRS) | URSB |

| Investment Promotion Body | Tanzania Investment Centre (TIC) | Kenya Investment Authority (KenInvest) | Uganda Investment Authority (UIA) |

Compliance Services for Companies in Tanzania

Maintain good standing with TRA, BRELA, and sector regulators through structured compliance support tailored to Tanzania's statutory requirements.

Conclusion

Tanzania positions itself as a viable incorporation destination through a combination of structural advantages that are difficult to replicate collectively within the East African region. EAC market access under the Treaty for the Establishment of the East African Community, combined with the Tanzania Investment Centre's sector-specific incentive packages, gives foreign-owned entities a measurable operational and cost advantage from the outset.

The benefits of incorporating in Tanzania are most pronounced for businesses operating in capital-intensive or export-oriented sectors. A 30% corporate tax rate administered by the Tanzania Revenue Authority, alongside depreciation allowances and capital expenditure deductions available under the Income Tax Act, directly affects the bottom line in ways that matter during the early years of establishment.

Your specific industry classification, ownership structure, and intended markets will determine how fully these advantages apply to your entity. A firm oriented toward agriculture or extractive industries, for example, will interact with a different set of TIC incentives and licensing requirements than one focused on services or manufacturing. The decision to register through the Business Registrations and Licensing Agency reflects a broader commitment to operating within a defined legal and regulatory framework, one that carries both obligations and protections. Clarifying how that framework applies to your particular business model is the step that converts general jurisdictional advantages into concrete operational outcomes.

Let Expanship Handle Your Tanzania Company Formation

Expanship Tanzania company formation services cover the full sequence of steps that this blog has outlined, from selecting the right entity structure under the Companies Act (Cap. 212) to meeting post-registration obligations administered by BRELA and the Tanzania Revenue Authority. Rather than managing those requirements across multiple local agents, you can consolidate the engagement with a single professional services provider.

Expanship's scope of work for Tanzanian incorporations includes:

- Preparation and legalization of incorporation documents, including Memoranda and Articles of Association

- Registered agent and registered office provision to satisfy BRELA's local presence requirements

- Government filing and direct liaison with BRELA throughout the registration process

- Post-incorporation compliance management, covering annual returns and TRA registration obligations

- Coordination with the Tanzania Investment Centre for TIC Certificate applications where applicable

- Banking introduction assistance to support account opening with local and regional financial institutions

Each of these services addresses a specific procedural requirement that a foreign business owner would otherwise need to source independently, often without existing relationships with local authorities or familiarity with current filing protocols.

Reach out to Expanship Tanzania to discuss your incorporation requirements.

Frequently Asked Questions (FAQ)

Yes, full foreign ownership is permitted in most sectors under the Tanzania Investment Act. Certain industries, including mining and broadcasting, carry ownership restrictions or require local equity participation, so sector-specific rules under the relevant licensing authority apply. Confirming your intended activity against the Tanzania Investment Centre's sector guidelines before incorporation will clarify whether any exceptions apply to your business.

Registration with the Business Registrations and Licensing Agency (BRELA) typically takes between three and ten working days once all required documents are submitted in proper order. Delays most commonly arise from incomplete documentation or discrepancies in director identification records. Processing times can differ between online submissions through the BRELA e-registry portal and in-person filings.

The Tanzania Revenue Authority (TRA) applies a standard corporate income tax rate of 30% to resident companies. Newly listed companies on the Dar es Salaam Stock Exchange may qualify for a reduced rate for a specified period, subject to conditions under the Income Tax Act. Businesses operating within designated Special Economic Zones or under Tanzania Investment Centre certificates may access further reductions.

The Tanzania Investment Centre (TIC) issues a Certificate of Incentives to qualifying investors, which provides access to benefits including import duty relief on capital goods and VAT exemptions, subject to minimum investment thresholds. The thresholds differ for foreign and local investors, with foreign applicants generally required to meet a higher minimum capital requirement. Incentives are tied to the approved project scope, so amendments to business activities may require a revised certificate.

Tanzania has concluded double taxation agreements with several countries, including Canada, Denmark, India, Italy, Norway, Sweden, and Zambia, among others. These treaties generally govern the allocation of taxing rights over dividends, interest, royalties, and business profits between the contracting states. The specific relief available depends on the provisions of the applicable treaty and the residency status of the entity or individual claiming benefits.

Tanzania is a member of the East African Community (EAC), which provides access to a regional market operating under a common external tariff and a customs union framework. The country is also a member of the Southern African Development Community (SADC), extending additional trade relationships. A company incorporated locally can export goods within the EAC under preferential tariff terms, subject to meeting applicable rules of origin requirements.

Failure to file annual returns with BRELA can result in penalties and, in persistent cases, administrative strike-off of the company from the register. Directors of a struck-off entity may face restrictions on incorporating or holding directorships in new entities until the matter is resolved. Reinstatement is possible under the Companies Act, but the process involves additional fees and a formal application.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.