Key Takeaways

- The D.O.O. is Slovenia's most widely registered entity, offering limited liability without the capital requirements imposed on a Delniška Družba (D.D.).

- All company registrations and ongoing compliance obligations in Slovenia fall under the jurisdiction of AJPES, which maintains the country's Business Register.

- Partnerships such as the Družba z Neomejeno Odgovornostjo (D.N.O.) and Komanditna Družba (K.D.) expose principals to personal liability, distinguishing them from capital-based structures.

- Slovenia's EU membership and expanding network of double taxation treaties make it a viable base for regional operations across Central Europe.

Introduction to Entity Types in Slovenia

Situated in Central Europe, Slovenia shares borders with Austria, Italy, Hungary, and Croatia. An independent republic and European Union member state since 2004, the country operates under a civil law system. Company registration and ongoing compliance fall under the jurisdiction of the Agency of the Republic of Slovenia for Public Legal Records and Related Services (AJPES), which maintains the Business Register of Slovenia.

Corporate taxation follows a standard EU-aligned model, with a general corporate income tax rate applicable to resident entities on their worldwide income.

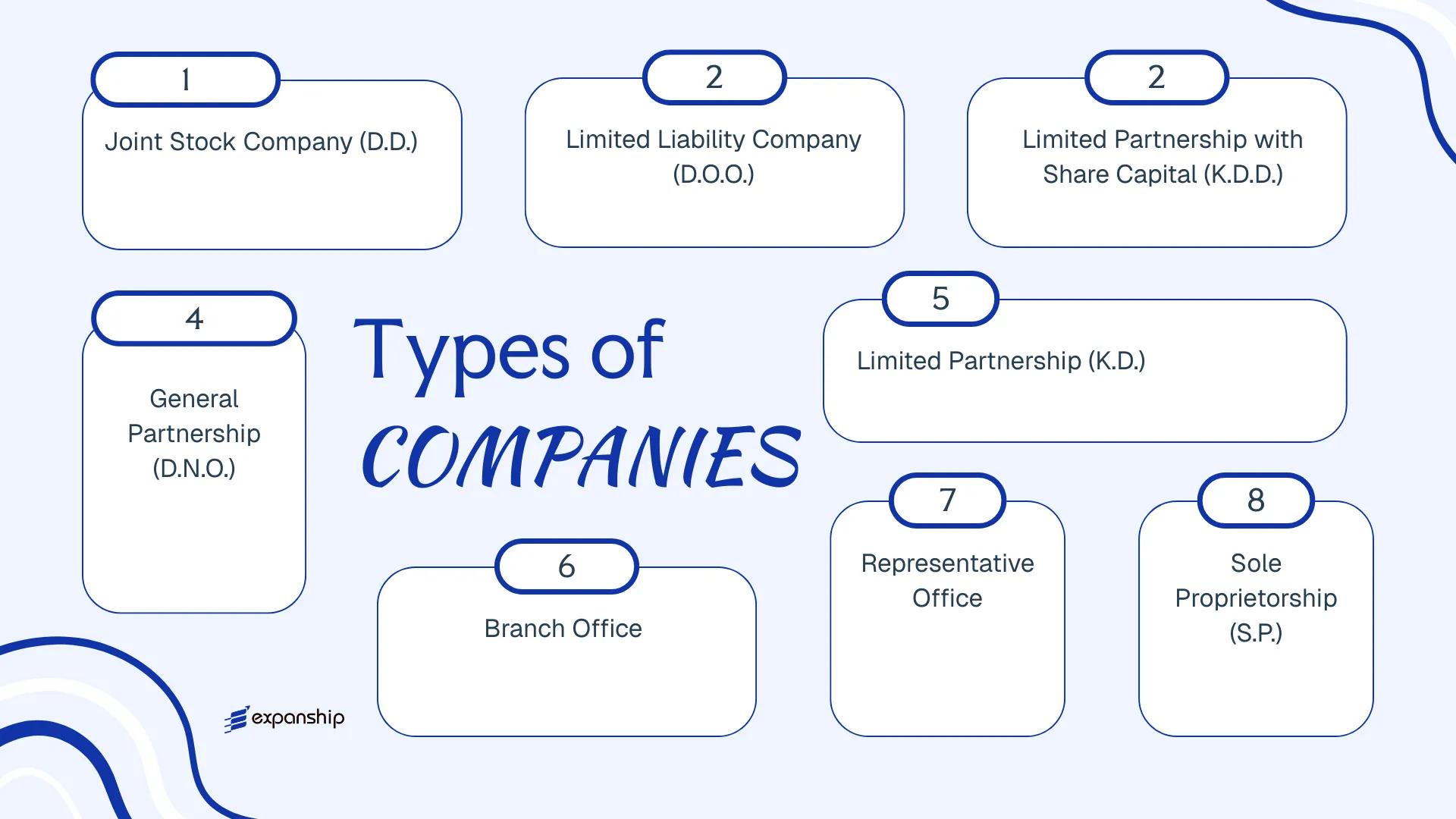

Several legal forms are available to those structuring a business here. The principal types of business entities in Slovenia include:

- Družba z Omejeno Odgovornostjo (D.O.O.)

- Delniška Družba (D.D.)

- Komanditna Delniška Družba (K.D.D.)

- Družba z Neomejeno Odgovornostjo (D.N.O.)

- Komanditna Družba (K.D.)

- Samostojni Podjetnik (S.P.)

- Branch Office

- Representative Office

Each form carries distinct requirements around capital, liability, governance, and regulatory obligations. The sections that follow examine each structure in detail to help you determine which fits your specific operational and ownership needs.

An Overview of Business Structures in Slovenia

Slovenian company law recognises seven principal entity types, each governed primarily by the Zakon o gospodarskih družbah (ZGD-1), or Companies Act, which has been in force since 2006 and amended periodically to align with EU directives. Additional structures, including the sole proprietorship, fall under the same legislative framework but operate under distinct registration rules. Each form carries a different liability profile, capital requirement, and operational scope.

| Entity Type | Legal Form | Liability | Corporate Tax | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Delniška Družba (D.D.) | Joint Stock Company | Limited | Taxed | Yes | 1 shareholder | AJPES / SPIRIT | ZGD-1 |

| Družba z Omejeno Odgovornostjo (D.O.O.) | Limited Liability Company | Limited | Taxed | Yes | 1 member | AJPES | ZGD-1 |

| Komanditna Delniška Družba (K.D.D.) | Limited Partnership with Share Capital | Mixed | Taxed | Yes | 2 partners | AJPES | ZGD-1 |

| Družba z Neomejeno Odgovornostjo (D.N.O.) | General Partnership | Unlimited | Taxed | Yes | 2 partners | AJPES | ZGD-1 |

| Komanditna Družba (K.D.) | Limited Partnership | Mixed | Taxed | Yes | 2 partners | AJPES | ZGD-1 |

| Branch Office | Non-resident branch | Parent liability | Taxed on local income | Yes | N/A | AJPES | ZGD-1 |

| Representative Office | Non-trading presence | Parent liability | Exempt from CIT | No | N/A | AJPES | ZGD-1 |

| Samostojni Podjetnik (S.P.) | Sole Proprietorship | Unlimited | Personal income tax | Yes | 1 individual | AJPES | ZGD-1 / ZDoh-2 |

Each of these structures is examined in full in the sections below.

Delniška Družba (D.D.) — Joint Stock Company

The Delniška Družba (D.D.) is Slovenia's joint stock company structure, governed by the Companies Act (Zakon o gospodarskih družbah, ZGD-1), first enacted in 2006 and since amended. It carries separate legal personality, meaning the entity bears its own rights and obligations independently of its shareholders.

Liability is limited to each shareholder's subscribed capital contribution. The D.D. is the primary vehicle for larger enterprises, institutional investors, and businesses seeking access to public capital markets under the supervision of the Slovenian Securities Market Agency (Agencija za trg vrednostnih papirjev, ATVP).

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Joint Stock Company (Delniška Družba) | Separate legal personality; governed by ZGD-1 |

| Members | Shareholders (minimum 1; no maximum) | Single-shareholder D.D. permitted; shares may be publicly listed |

| Governance | Management Board + Supervisory Board (two-tier) or single-tier Board of Directors | Two-tier structure is the default; single-tier requires statutory opt-in |

| Local Presence | Registered seat in Slovenia required | Physical registered address mandatory; no mandatory resident director under ZGD-1 |

| Share Capital | Minimum EUR 25,000; must be fully subscribed at incorporation | At least 25% of cash contributions paid up at registration; non-cash contributions valued by a court-appointed auditor |

| Share Transferability | Shares freely transferable unless restricted by articles | Bearer shares are not permitted; shares are registered (imenski) |

| Privacy | Shareholders and directors appear in the Business Register (AJPES) | Register is publicly accessible |

Focus Points

- Taxation: Subject to 19% corporate income tax; standard VAT rate of 22% applies to taxable supplies; withholding tax of 15% on dividends, interest, and royalties paid to non-residents, reducible under applicable tax treaties or EU Directives.

- Treaty Access: Slovenia has an extensive double tax treaty network; D.D. entities qualify as tax residents when incorporated or effectively managed in Slovenia.

- Annual Compliance: Mandatory annual financial statements filed with AJPES; audit required if the entity meets two of three statutory size thresholds under ZGD-1.

- Economic Substance: No specific substance scoring regime, but effective management must be demonstrably located in Slovenia to maintain tax residency.

- Conversion: A D.D. may be converted into a D.O.O. or other recognised form through a statutory transformation procedure under ZGD-1, subject to creditor protection requirements.

Sub-Types

Javna Delniška Družba — Public Joint Stock Company

A D.D. whose shares are admitted to trading on a regulated market qualifies as a javna delniška družba. This sub-type is subject to additional obligations under the Market in Financial Instruments Act (ZTFI-1) and continuous disclosure requirements enforced by ATVP, including prospectus rules and ongoing transparency reporting.

Established enterprises, investment holding structures, and businesses pursuing a public listing are the primary users of the D.D. form. Its capacity to issue transferable shares across an unrestricted shareholder base is a structural advantage, but the EUR 25,000 minimum capital requirement and mandatory two-tier governance make it administratively heavier than simpler Slovenian structures.

The D.D. is best suited for larger businesses, institutional ventures, or companies planning to raise capital through a regulated market listing.

Company Incorporation in Slovenia

Expanship assists with D.D. and D.O.O. formation, registered address provision, and ongoing compliance in Slovenia.

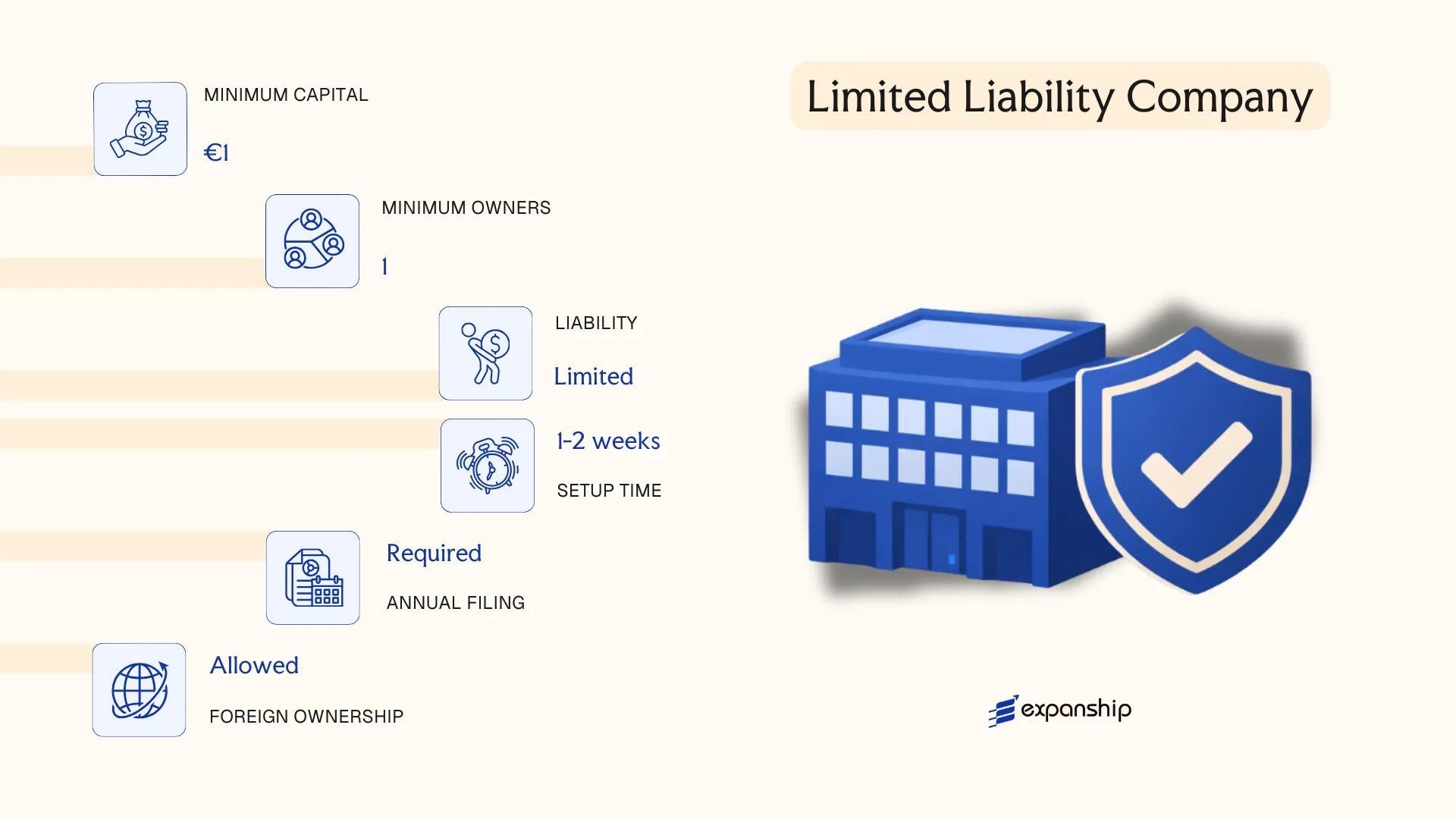

Družba z Omejeno Odgovornostjo (D.O.O.) — Limited Liability Company

The Družba z Omejeno Odgovornostjo D.O.O. Slovenia is governed by the Companies Act (Zakon o gospodarskih družbah, ZGD-1), first enacted in 2006 and subsequently amended. It carries separate legal personality, meaning the entity bears its own rights and obligations distinct from those of its members.

Liability is capped at each member's capital contribution. This hybrid structure sits between a partnership and a joint stock company, making it the most frequently registered business form in the country.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private limited liability company | Governed under ZGD-1 |

| Members | 1–50 members | Members hold business stakes (poslovni delež); no public share issuance permitted |

| Management | Minimum one director (poslovodja) | Director may be a non-resident; supervisory board optional below certain thresholds |

| Local Presence | Registered office address in Slovenia required | No mandatory resident director, but a registered address must be maintained |

| Capital | Minimum EUR 7,500 | At least EUR 50 per member contribution; paid-up in full before registration |

| Privacy | Members listed in the court register (sodni register) | Beneficial ownership disclosed to AJPES under anti-money laundering rules |

Focus Points

- Taxation: Subject to 19% corporate income tax; standard VAT rate of 22% applies once threshold is met; withholding tax on dividends is 15% (treaty reductions available); no stamp duty on capital contributions.

- Annual Compliance: Annual financial statements must be filed with AJPES; audit required only above statutory size thresholds.

- Treaty Access: Slovenia's tax treaty network covers 60+ jurisdictions, making a D.O.O. eligible for reduced withholding rates on dividends, interest, and royalties.

- Conversion: A D.O.O. may convert into a D.D. through a formal transformation procedure under ZGD-1 without dissolving the legal entity.

- Transfer Restrictions: Transfer of a business stake to third parties requires compliance with pre-emption rights held by existing members unless the articles of association provide otherwise.

Closing

D.O.O. company registration in Slovenia suits trading operations, holding structures, and IP ownership vehicles where limited liability and operational flexibility are both required. The EUR 7,500 minimum capital threshold is low relative to a joint stock company, though the 50-member cap restricts this form for businesses anticipating broad equity participation.

Small to mid-sized businesses, foreign investors establishing a subsidiary, and entrepreneurs seeking a straightforward corporate structure with capped personal liability.

Komanditna Delniška Družba (K.D.D.) — Limited Partnership with Share Capital

The Komanditna Delniška Družba K.D.D. Slovenia is governed by the Companies Act (Zakon o gospodarskih družbah, ZGD-1), the same legislation that regulates all commercial entities in the country. It carries separate legal personality, meaning the firm itself holds rights and obligations distinct from its members.

Structurally, the K.D.D. is a hybrid: it combines the share capital mechanics of a joint stock company with the partnership dynamic of a limited partnership. At least one general partner (komplementar) bears unlimited personal liability, while limited partners (komanditisti) hold transferable shares and are liable only to the extent of their contribution.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Komanditna Delniška Družba (K.D.D.) | Separate legal personality; hybrid partnership-share capital structure |

| Members | Min. 1 general partner (komplementar) + min. 1 limited partner (komanditist); no statutory maximum | General partner has unlimited liability; limited partner liability capped at share contribution |

| Capital | EUR 25,000 minimum share capital | Shares issued to limited partners only; general partners do not hold shares |

| Local Presence | Registered office in Slovenia required | No statutory requirement for a local resident director, but general partner may be natural or legal person |

| Governance | General partners manage the entity; limited partners have no management rights by default | Supervisory board may be required depending on size thresholds under ZGD-1 |

| Privacy | Ownership and partnership details filed in the Business Register of Slovenia (AJPES) | Register is publicly accessible |

Focus Points

- Taxation: Subject to 19% corporate income tax on profits; standard VAT rate of 22% applies if registered; dividend withholding tax of 15% applies, reducible under applicable double tax treaties; transfer of shares may attract capital gains tax at the entity level.

- Annual Compliance: Financial statements must be filed with AJPES annually; audit obligations depend on size classification under ZGD-1.

- Treaty Access: As a resident legal entity, the K.D.D. can access Slovenia's network of double tax treaties, subject to beneficial ownership requirements.

- Restrictions: General partners cannot limit their personal liability through the articles of association; this structural constraint limits the entity's appeal for risk-averse investors.

- Conversion: ZGD-1 permits conversion into other corporate forms, including a D.D. or D.O.O., through a formal transformation procedure.

Closing

The K.D.D. suits structures where one party assumes management control and personal liability while external investors participate through transferable shares with capped exposure — common in family-controlled businesses or closed investment vehicles. Its principal limitation is the unavoidable unlimited liability carried by every general partner.

This entity suits experienced business principals willing to accept personal liability in exchange for full management control, paired with passive investors who require transferable, liability-capped share participation.

Partnerships in Slovenia [Družba z Neomejeno Odgovornostjo (D.N.O.) — General Partnership, Komanditna Družba (K.D.) — Limited Partnership]

Both general and limited partnerships in Slovenia are governed by the Companies Act (Zakon o gospodarskih družbah, ZGD-1), first enacted in 2006 and amended several times since. Unlike capital companies, partnerships are founded on the personal involvement of their members, and liability exposure varies significantly depending on the structural form chosen.

A D.N.O. (Družba z Neomejeno Odgovornostjo) holds separate legal personality under Slovenian law, yet all partners bear unlimited, joint, and several liability for the firm's obligations. The K.D. (Komanditna Družba) introduces a hybrid arrangement: at least one general partner carries unlimited liability, while one or more limited partners are liable only up to their agreed capital contribution.

Key Characteristics

| Requirement | D.N.O. (General Partnership) | K.D. (Limited Partnership) |

|---|---|---|

| Legal Form | Separate legal personality; unlimited liability for all partners | Separate legal personality; mixed liability structure |

| Members | Partners — minimum 2, no statutory maximum | Minimum 1 general partner + 1 limited partner; no maximum |

| Local Presence | Registered office in Slovenia required | Registered office in Slovenia required |

| Capital | No minimum capital requirement; contributions may be monetary or in-kind | No minimum capital requirement; limited partner's liability capped at contribution |

| Privacy | Partner names disclosed in the court register (AJPES) | General and limited partner names publicly registered via AJPES |

Focus Points

- Taxation: Both entity types are fiscally transparent by default — profits pass through to partners and are taxed at the individual income tax rate (up to 50%) or corporate rate (19%) depending on the partner's legal status; VAT registration applies when turnover exceeds the statutory threshold.

- Annual Compliance: Both forms must file annual accounts with AJPES; a D.N.O. with no employees and below certain thresholds may qualify for simplified reporting.

- Treaty Access: Tax treaty benefits depend on the tax residency and legal status of each individual partner, not the partnership itself.

- Conversion: A D.N.O. can be converted into a K.D. or a capital company (D.O.O. or D.D.) under ZGD-1 conversion procedures without dissolving the entity.

- Restrictions: Neither form is permitted to operate in regulated sectors (banking, insurance, investment services) as the primary licensed entity.

Sub-Types

Družba z Neomejeno Odgovornostjo (D.N.O.) — General Partnership

All partners manage the business and hold equal authority unless the founding agreement specifies otherwise. This structure is used primarily by small professional firms or family-run businesses where all participants take active management responsibility.

Komanditna Družba (K.D.) — Limited Partnership

The K.D. separates active management (general partners) from passive investors (limited partners), who may not participate in management without forfeiting their liability protection. This form suits arrangements where capital investors seek limited exposure without operational involvement.

Closing

Partnerships suit small-scale, domestically focused operations where the founders maintain direct control and operational involvement outweighs the need for liability protection. The absence of minimum capital requirements lowers the entry barrier, though unlimited liability for general partners represents a material legal risk for businesses with significant obligations.

D.N.O. and K.D. structures are best suited for small professional practices, family businesses, or investor-operator arrangements where personal liability is manageable and simplified governance is a priority.

Foreign Business Presence in Slovenia [Branch Office, Representative Office]

A foreign company branch office Slovenia registration falls under the Companies Act (Zakon o gospodarskih družbah, ZGD-1), which governs both branch offices and representative offices as forms of foreign business presence. Neither structure constitutes a separate legal entity — each remains an extension of the parent company, which retains full legal and financial liability for its activities.

Registration is handled through the Agency of the Republic of Slovenia for Public Legal Records and Related Services (AJPES) via the court register. A branch office may conduct full commercial operations, while a representative office is restricted to non-revenue-generating activities such as market research and liaison work.

Key Characteristics

| Requirement | Branch Office | Representative Office |

|---|---|---|

| Legal Personality | None — extension of parent | None — extension of parent |

| Commercial Activity | Permitted | Not permitted |

| Registration Body | AJPES / Court Register | AJPES / Court Register |

| Local Representative | Required (authorised agent) | Required (authorised agent) |

| Registered Address | Required in Slovenia | Required in Slovenia |

| Share Capital | None required | None required |

Focus Points

- Taxation: Branch profits are subject to the standard 19% corporate income tax; VAT registration is required if taxable supplies exceed the threshold; withholding tax may apply to profit remittances depending on the applicable double tax treaty.

- Economic Substance: The branch must maintain genuine operational activity locally; a purely nominal presence may be challenged by the tax authority (FURS).

- Annual Compliance: Branches must file annual financial statements with AJPES; accounting records must comply with Slovenian standards.

- Treaty Access: Access to Slovenia's tax treaty network depends on the parent company's residence and treaty eligibility — the branch itself does not independently qualify.

- Restrictions: Representative offices cannot invoice, sign commercial contracts, or generate revenue in any form.

Closing

A branch office suits foreign firms testing the Slovenian market or managing regional operations without full incorporation, though the parent company's unlimited exposure to local liabilities is a material drawback. A representative office offers a lower-commitment entry point but is structurally unsuitable for any revenue-generating activity.

A branch office is most appropriate for established foreign companies seeking an operational presence without incorporating a separate subsidiary.

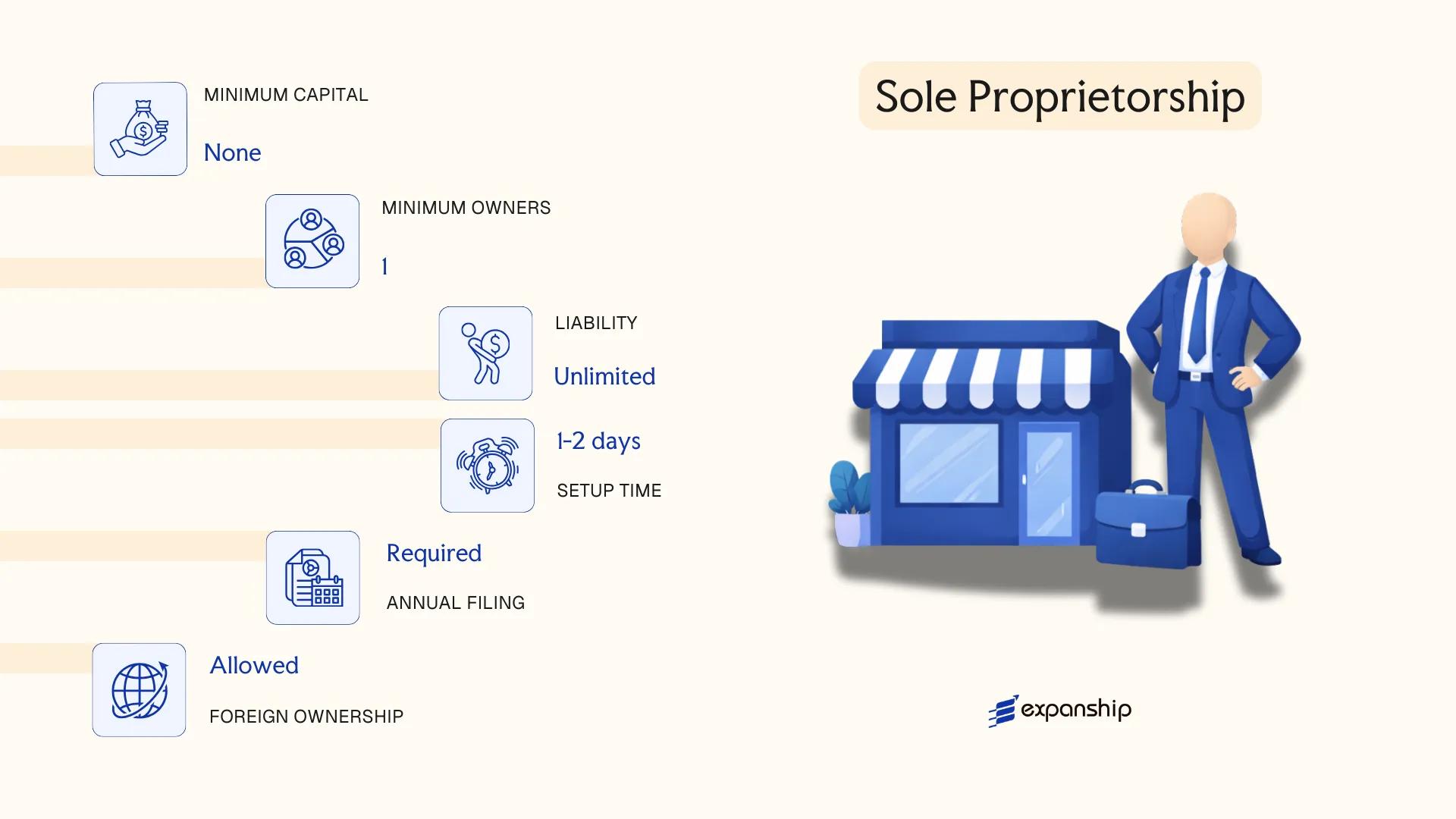

Samostojni Podjetnik (S.P.) — Sole Proprietorship

The Samostojni Podjetnik (S.P.) is the simplest registered business form available under Slovenian law, governed primarily by the Zakon o gospodarskih družbah (Companies Act, ZGD-1) alongside the Zakon o samostojnih podjetnikih posameznikih. Unlike a D.O.O. or D.D., the S.P. does not constitute a separate legal entity — the proprietor and the business are legally identical.

Registration is handled through the AJPES (Agency of the Republic of Slovenia for Public Legal Records and Related Services) portal, and the process can typically be completed within one business day. Because no minimum capital is required, the structure carries a low entry threshold, though personal asset exposure is unlimited.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sole Proprietorship | No separate legal personality; proprietor bears full personal liability |

| Member Designation | Proprietor (Podjetnik) | One natural person only; legal entities cannot register as S.P. |

| Membership | 1 proprietor (maximum 1) | Cannot have partners, shareholders, or co-owners |

| Local Presence | Registered address in Slovenia required | Must be a physical address; registered through AJPES |

| Minimum Capital | None | No paid-in capital requirement at registration |

| Privacy | Name and address publicly listed in the AJPES register | No meaningful privacy protection |

Focus Points

- Taxation: Subject to personal income tax (dohodnina) on business profit at progressive rates up to 50%; VAT registration mandatory once turnover exceeds the statutory threshold (currently EUR 50,000); no corporate income tax applies; social security contributions are compulsory.

- Annual Compliance: Annual financial statements must be submitted to AJPES; bookkeeping obligations apply based on turnover level (cash-basis or full accrual).

- Treaty Access: As a non-corporate structure, access to double tax treaty benefits is limited and fact-dependent; professional advice is warranted before relying on treaty relief.

- Conversion: An S.P. can be converted into a D.O.O. under ZGD-1 provisions, allowing migration to limited liability without full dissolution.

- Restrictions: Foreign nationals outside the EU/EEA may face additional permit requirements before registering as a sole trader.

Closing

The S.P. suits freelancers, individual consultants, and micro-scale traders who prioritise low administrative overhead over liability protection. The primary advantage is minimal setup cost and rapid registration; the central drawback is unlimited personal liability, which extends to the proprietor's private assets.

The S.P. is best suited for individual professionals and sole traders operating at a small scale who do not require a separate legal personality or intend to bring in co-owners.

How to Choose the Right Entity Type in Slovenia

Selecting how to choose the right company type in Slovenia is not a formality — the structure you register determines your liability exposure, tax treatment, reporting obligations, and ability to scale or exit.

Why Your Entity Choice Matters

Choosing the wrong legal form produces concrete, correctable-but-costly outcomes:

- Forming a D.O.O. when your activity requires a licensed financial intermediary structure can result in the Agency for Public Legal Records and Related Services (AJPES) flagging registration inconsistencies, and the competent supervisory authority may prohibit operations.

- Selecting a D.N.O. or K.D. when you need access to Slovenia's tax treaty network may disqualify your firm from withholding tax reductions, since partnerships are fiscally transparent and treaties generally apply at partner level.

- Registering an S.P. when your business generates substantial liability exposure leaves personal assets fully at risk, with no statutory separation between business and personal patrimony.

- Choosing a structure that mandates a statutory audit when your business operates below the thresholds set under the Companies Act (ZGD-1) adds recurring professional costs without regulatory benefit.

Key Factors to Consider

- Business Activity: Active trading, passive asset holding, and regulated sectors each require a different structure under ZGD-1.

- Ownership and Management: Single-owner ventures suit the D.O.O. or S.P., while multi-party arrangements with capital contributions may warrant a D.D. or K.D.D.

- Tax Objectives: Your need for treaty access, participation exemption eligibility, or pass-through taxation should drive the entity decision before registration.

- Liability Exposure: If personal asset protection is a priority, only limited liability structures under ZGD-1 provide statutory separation.

- Substance Capacity: If you cannot maintain a registered office, employees, or local decision-making, certain structures will attract scrutiny from the Financial Administration of the Republic of Slovenia (FURS).

- Exit Strategy: Not all Slovenian entity types support conversion or redomiciliation equally — confirm procedural compatibility before committing to a structure.

Compliance Services for Companies in Slovenia

Ongoing compliance support for Slovenian entities, including statutory filings, AJPES reporting, and regulatory monitoring.

Conclusion

Incorporating a company in Slovenia requires matching your operational profile to the correct legal form before approaching the Agency of the Republic of Slovenia for Public Legal Records and Related Services (AJPES) for registration. The D.O.O. remains the most widely registered entity, suited to small and mid-sized businesses that require limited liability without the capital thresholds of a joint stock company. The D.D. serves larger enterprises planning public capital raises. Partnerships such as the D.N.O. and K.D. are reserved for principals willing to accept personal liability. The S.P. fits individual traders operating with minimal structural overhead.

Slovenia's growing network of double taxation treaties and its EU membership continue to strengthen its position as a credible base for regional operations. For businesses requiring professional guidance through AJPES procedures and corporate structuring, Expanship provides jurisdiction-specific assistance.

How Expanship Can Assist You

Expanship's company formation services in Slovenia cover the full registration process, from selecting the right legal structure to filing with the Agency of the Republic of Slovenia for Public Legal Records and Related Services (AJPES). Whether your focus is a D.O.O., a D.D., or establishing a branch, each path carries distinct registration requirements and ongoing compliance obligations that our team handles directly.

Expanship Slovenia incorporation assistance spans every practical step of getting your entity operational and maintaining it correctly over time.

- Document preparation, notarization, and legalization

- Registered agent and registered office provision

- AJPES filing and government authority liaison

- Post-incorporation compliance management

- Corporate account opening introductions

Ready to move forward? Reach out to Expanship Slovenia to discuss your specific requirements.

Frequently Asked Questions (FAQ)

The Družba z Omejeno Odgovornostjo (D.O.O.) is the most frequently incorporated entity in the country. Its EUR 7,500 minimum share capital requirement and single-member eligibility make it accessible for small and medium enterprises, while its limited liability structure suits founders who want personal asset protection without the administrative burden of a joint stock company.

The D.D. is subject to heavier governance obligations, including a supervisory board requirement once certain thresholds are met under the Companies Act (ZGD-1), while a D.O.O. operates under a simplified management structure. Public securities issuance is only available to the D.D., which also carries a higher minimum share capital of EUR 25,000. For most domestically focused businesses, the D.O.O. offers a proportionate compliance load relative to its operational scope.

Among registered structures, the D.O.O. allows for nominee arrangements, though beneficial ownership must still be disclosed to the Agency of the Republic of Slovenia for Public Legal Records and Related Services (AJPES) under anti-money laundering obligations. Shareholder details are held in the court register, which is publicly accessible. Full anonymity is not achievable under current Slovenian corporate law.

A sole individual can register a D.O.O., D.D., or Samostojni Podjetnik (S.P.) without additional co-founders. Partnerships are structurally different: a Družba z Neomejeno Odgovornostjo (D.N.O.) requires at least two general partners, and a Komanditna Družba (K.D.) requires at least one general and one limited partner. The Komanditna Delniška Družba (K.D.D.) similarly requires both a general partner and shareholders.

Foreign individuals and legal entities may register a D.O.O. or D.D. without restrictions on nationality or residency, provided they comply with ZGD-1 requirements. A foreign company may also establish a branch office (podružnica), which operates under the parent entity's legal personality and does not constitute a separate legal entity. Non-residents should account for the need for a Slovenian registered address and, in some cases, a local contact person for tax correspondence.

ZGD-1 permits the transformation of one company form into another through a formal conversion procedure, including the change from a D.O.O. to a D.D. or vice versa. The process requires a notarised conversion plan, shareholder approval, and registration with AJPES. Not all conversions follow the same procedural path, and transformations involving partnerships carry additional requirements regarding partner liability continuity.

The D.O.O., D.D., and K.D.D. each hold separate legal personality, meaning the entity can contract, own assets, and incur liabilities independently of its members. General partnerships (D.N.O.) and limited partnerships (K.D.) also have legal personality under ZGD-1, but general partners retain unlimited personal liability for the entity's obligations. The Samostojni Podjetnik (S.P.) does not constitute a separate legal entity; the individual and the business are legally the same person.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.