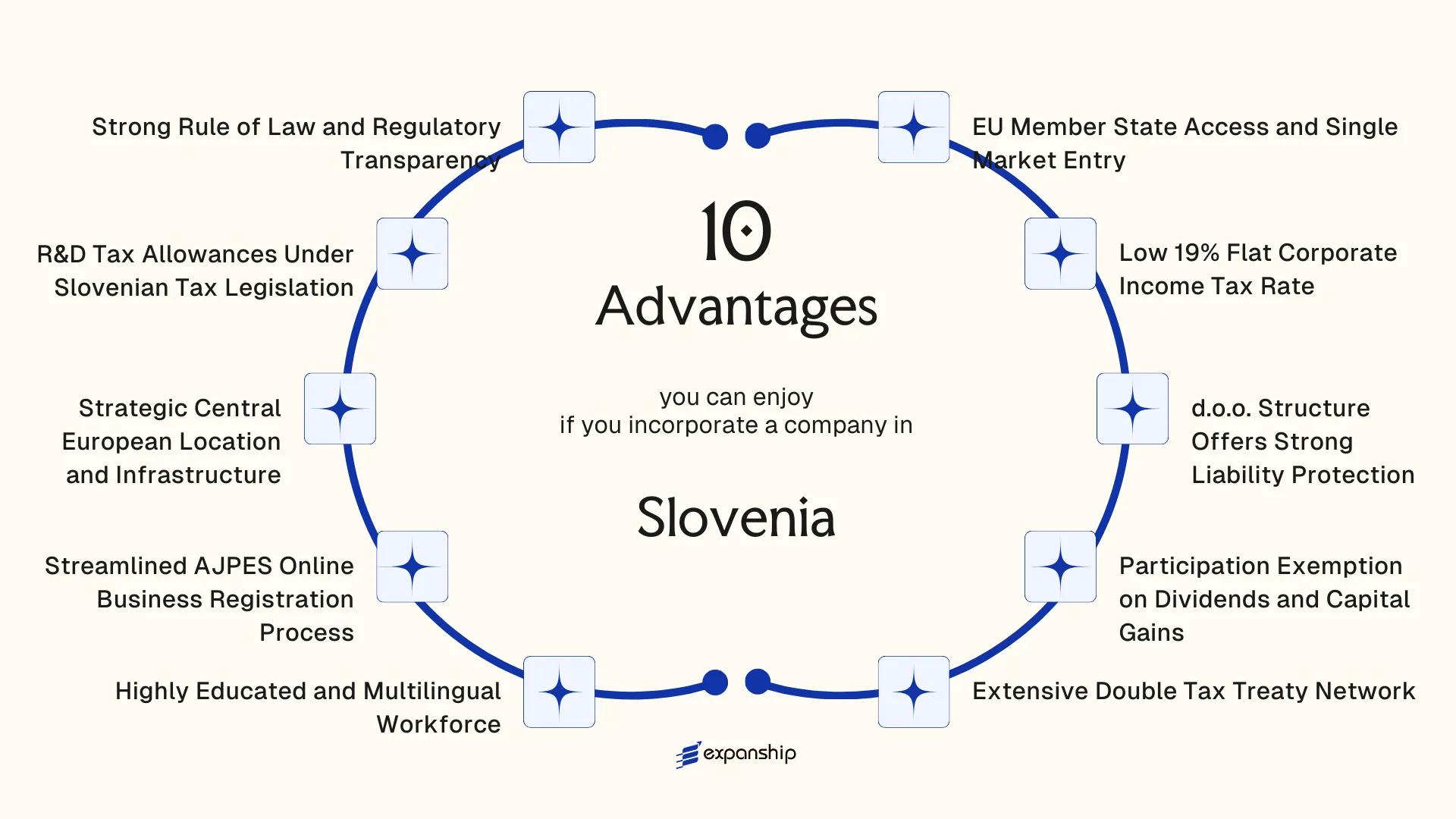

Key Takeaways

- Slovenia's 19% flat corporate income tax rate, governed by the Corporate Income Tax Act (ZDDPO-2), provides a predictable and competitive fiscal baseline that does not shift with discretionary government policy.

- Foreign investors structuring operations through a d.o.o. gain liability protection while facing no general restrictions on foreign ownership under Slovenian law, keeping equity and control arrangements straightforward.

- The participation exemption under the Corporate Income Tax Act shields qualifying dividends and capital gains from domestic tax, which materially reduces the tax cost of extracting profits from EU subsidiaries held through a Slovenian structure.

- Because registration is administered directly through AJPES and Slovenia operates within the EU single market, a company formed here gains both a streamlined incorporation pathway and immediate access to passporting rights across member states.

Situated in Central Europe, Slovenia is an independent EU member state that has maintained a stable, treaty-based tax framework since adopting its corporate tax legislation. The benefits of incorporating in Slovenia draw attention from businesses across multiple sectors, and this article examines the specific structural and fiscal advantages that company formation here offers. Registration of legal entities falls under the authority of the AJPES, the Agency of the Republic of Slovenia for Public Legal Records and Related Services, which administers the court register through which businesses are formally established.

Foreign investors most commonly structure their operations through a d.o.o. Tax obligations are governed by the Corporate Income Tax Act (ZDDPO-2), which applies a flat rate within a system that also incorporates an extensive network of bilateral double tax treaties. Slovenian law places no general restrictions on foreign ownership of domestic companies, and the country has maintained an open posture toward foreign direct investment across most sectors. Each of the core advantages is addressed in the sections that follow.

EU Member State Access and Single Market Entry

As an EU member state, Slovenia gives foreign businesses direct access to the EU single market -- a trading bloc of over 440 million consumers -- without the need for subsidiary structures in separate member states.

Passporting Rights and Cross-Border Operations

A company incorporated in Slovenia can provide goods and services across all 27 EU member states under the EU's foundational freedom of movement principles. This eliminates the cost and administrative burden of establishing distinct legal entities in each country you intend to operate in.

Customs Union and Regulatory Harmonisation

Operating within the EU customs union means your business moves goods across member state borders without internal tariffs or customs declarations. EU regulatory harmonisation also means that product standards, procurement rules, and conformity assessments accepted in Slovenia are recognised across the bloc -- a significant reduction in compliance overhead for firms selling into multiple European markets.

One Slovenian entity can serve the entire EU market without requiring separate registrations in each member state.

Low 19% Flat Corporate Income Tax Rate

Slovenia's standard corporate income tax rate sits at 19%, which falls below the EU average of approximately 21.3%. Under the Corporate Income Tax Act (Zakon o davku od dohodkov pravnih oseb, ZDDPO-2), this rate applies uniformly to resident companies on their worldwide income, while non-resident entities are taxed only on income sourced within the country.

For foreign investors, a flat rate removes the uncertainty of graduated tax schedules. Your projected tax liability is calculable from the outset, which simplifies financial modelling and cross-border profit planning.

The Slovenia 19% flat corporate tax rate advantage becomes particularly tangible when you consider what that rate covers:

- The rate applies without a minimum income threshold, so early-stage entities are not penalised during low-revenue periods

- No surtax or local corporate tax is levied on top of the national rate, keeping the effective burden predictable

- The same rate applies regardless of the legal form, whether a d.o.o. or a delniška družba (d.d.)

- Foreign-owned firms face no discriminatory rate adjustments compared to domestically owned businesses

The Slovenia low corporate income tax benefit is codified at the national level, meaning regional or municipal authorities have no power to alter it, giving your business consistent treatment across all operating locations.

Company Incorporation in Slovenia

Set up your Slovenian company with full compliance support across registration, tax, and legal structuring.

d.o.o. Structure Offers Strong Liability Protection

A družba z omejeno odgovornostjo, or d.o.o., is Slovenia's primary private limited liability company structure. Under the Companies Act (Zakon o gospodarskih družbah, ZGD-1), shareholders are liable only up to the value of their capital contributions. Personal assets remain outside the reach of business creditors, which is a structural protection that holds regardless of your residency or nationality.

The minimum share capital requirement is EUR 7,500, and it does not need to be fully paid up at incorporation. This relatively low threshold means you can establish a legally separated entity without committing substantial capital, while still benefiting from the full liability shield the structure provides.

| Parameter | Detail |

|---|---|

| Governing legislation | ZGD-1 (Companies Act) |

| Minimum share capital | EUR 7,500 |

| Shareholder liability | Limited to capital contribution |

| Maximum number of shareholders | 50 |

| Legal personality | Separate from shareholders |

Foreign investors operating through a d.o.o. gain a clear legal boundary between personal and corporate exposure. If the business incurs debt or faces litigation, your personal financial position is not automatically at risk. This separation also simplifies cross-border investment structuring, since the entity itself holds assets, enters contracts, and bears obligations independently. The company's separate legal personality under ZGD-1 is what makes that boundary enforceable and predictable.

Participation Exemption on Dividends and Capital Gains

Under the Corporate Income Tax Act (ZDDPO-2), Slovenia participation exemption on dividends and capital gains allows a Slovenian holding entity to exclude qualifying income from its taxable base. Dividends received from subsidiaries are 95% exempt, meaning only 5% is included in the tax calculation. The same 95% exemption applies to capital gains on the disposal of qualifying shareholdings.

For a foreign business structuring a European holding operation, this directly reduces the tax cost of repatriating profits or exiting investments through a Slovenian intermediate entity.

Eligibility is not automatic. The receiving company must hold at least an 8% stake in the subsidiary, and the participation must be held for an uninterrupted period of at least six months.

Keep these conditions in mind before structuring around this exemption:

- Minimum 8% shareholding in the distributing entity is required

- Holding period must be at least six months, held continuously

- The subsidiary must be subject to corporate income tax in its home jurisdiction

- The 95% exemption applies to both dividends received and qualifying capital gains

- Anti-avoidance provisions under ZDDPO-2 may disqualify arrangements lacking genuine commercial substance

The capital gains exemption under ZDDPO-2 applies equally to gains from share disposals as it does to dividends, which is not universally the case across EU holding regimes.

Extensive Double Tax Treaty Network

Slovenia's double tax treaty network benefits foreign businesses by eliminating one of the most common friction points in cross-border operations: being taxed twice on the same income. The country has concluded over 60 bilateral tax treaties, covering major trading partners across Europe, Asia, and North America, which directly reduces withholding tax rates on dividends, interest, and royalties paid between your entity and counterparties abroad.

Treaty Coverage and What It Means for Withholding Costs

Under Slovenia's domestic tax law, standard withholding tax rates apply to outbound payments, but treaty provisions frequently reduce these substantially. A treaty with a jurisdiction like Germany or the United States, for example, can lower dividend withholding to rates well below the statutory default, which affects your actual after-tax returns when repatriating profits or servicing intercompany financing.

These reductions are not automatic. Your business must demonstrate tax residency and satisfy the beneficial ownership conditions written into each specific treaty to qualify for the reduced rates.

Practical Value for Holding and IP Structures

For firms using a Slovenian entity within a regional holding or intellectual property structure, treaty access determines the net cost of royalty flows and dividend distributions across borders. Slovenia's treaties with countries including Austria, the Netherlands, and Switzerland give your structure predictable tax outcomes on these flows, reducing reliance on unilateral domestic relief.

The treaties are grounded in the OECD Model Tax Convention framework, meaning interpretation and anti-avoidance provisions follow internationally recognized standards.

Make the Most of Slovenia's Tax Treaty Network

Speak with our corporate services team about structuring your Slovenian entity to access applicable treaty benefits from day one.

Highly Educated and Multilingual Workforce

Slovenia's highly educated multilingual workforce advantage is one of the more concrete, measurable benefits your business gains at the point of hiring. According to Eurostat data, Slovenia consistently ranks among the higher-performing EU member states for tertiary education attainment, with a significant share of its working-age population holding university-level qualifications.

- English proficiency is widespread among university graduates and professionals, particularly in technical, legal, and financial fields. For foreign-owned entities operating across EU markets, this reduces onboarding friction and removes the need for extensive language infrastructure.

- German and Italian are also commonly spoken in the workforce, reflecting the country's geographic position between Austria, Germany, and Italy. Businesses targeting Central European or DACH-region clients gain a practical communication advantage without incurring translation overhead.

- The University of Ljubljana and the University of Maribor, both public institutions, produce graduates across engineering, computer science, economics, and law. This creates a local talent pipeline relevant to firms in technology, professional services, and manufacturing.

- Slovenian labor law, governed primarily by the Employment Relationships Act (ZDR-1), provides a structured framework for employment contracts, including fixed-term and part-time arrangements, giving foreign employers defined parameters within which to hire locally.

Streamlined AJPES Online Business Registration Process

Slovenia AJPES online business registration benefits begin at a practical level: the Agency of the Republic of Slovenia for Public Legal Records and Related Services (AJPES) operates an electronic registration portal through which a d.o.o. can be registered without requiring your physical presence in the country. For foreign entrepreneurs, this removes a logistical barrier that remains common across several EU member states.

Registration through the AJPES e-VEM portal connects directly to the Companies Register, meaning your entity receives its registration number and tax identification from a single, integrated process. The entire procedure is typically completed within a few business days. That speed has direct commercial value: your business can open a bank account and begin operations without an extended pre-launch period.

No notarized deed is required for a standard d.o.o. formation when using the electronic route, which reduces both cost and document preparation time for non-resident founders. This positions Slovenia's formation process as materially faster than jurisdictions where notarial authentication remains mandatory.

A hypothetical scenario: A foreign founder registering a d.o.o. electronically through AJPES with the minimum share capital of EUR 7,500 can complete registration without traveling to Slovenia, saving approximately EUR 800 to EUR 1,500 in notary, apostille, and travel costs typically incurred in comparable Central European jurisdictions.

Strategic Central European Location and Infrastructure

Slovenia's central European location business advantage is geographic and logistical. The country shares borders with Italy, Austria, Hungary, and Croatia, placing your business within direct reach of four distinct EU and regional markets. The Port of Koper, on Slovenia's short Adriatic coastline, is one of the fastest-growing cargo ports in the Mediterranean basin and serves as a primary entry point for goods moving toward Central and Eastern Europe.

Road and rail connectivity reinforce this position. The TEN-T (Trans-European Transport Network) corridors passing through the country link your operations to major distribution hubs across the continent without requiring transhipment through Western European ports.

For foreign companies moving goods, managing regional distribution, or coordinating European operations, the practical benefit is reduced transit times and lower logistics costs compared to hub-based operations in more peripheral EU member states.

- Access to the Adriatic via Koper without routing through North Sea ports

- Direct road links to Vienna, Milan, Zagreb, and Budapest

- Rail freight connections integrated into the broader European rail freight network

Physical presence or operational activity in the country may be required to justify using a Slovenian entity as a regional distribution or logistics hub for tax and substance purposes.

R&D Tax Allowances Under Slovenian Tax Legislation

Slovenia R&D tax allowances benefits for businesses are grounded in Article 55 of the Corporate Income Tax Act (Zakon o davku od dohodkov pravnih oseb, ZDDPO-2). Under this provision, companies can deduct 100% of qualifying research and development expenditure from their tax base, in addition to recognising the same costs as a regular business expense. That double deduction mechanism directly reduces taxable income beyond what standard expense treatment permits.

Qualifying expenditure covers internal R&D activities as well as contracted research, provided the work meets the definition of basic research, applied research, or experimental development under the applicable legislation. For a foreign-owned entity operating through a Slovenian subsidiary, this means that product development, process innovation, and technical feasibility work carried out locally can generate a material reduction in the corporate tax base each year.

The deduction applies to:

- Costs of researchers' salaries and related contributions

- Depreciation of equipment used exclusively for R&D purposes

- Costs of materials and supplies consumed in qualifying projects

- Contracted research costs paid to external institutions or companies

Unused allowances that cannot be absorbed in the year they arise may be carried forward for up to five tax periods. This carry-forward provision means that early-stage businesses, which often incur R&D costs before generating significant revenue, are not permanently excluded from the benefit simply due to timing. The combination of a 19% corporate rate and the 100% additional deduction creates a compounding tax efficiency that is difficult to replicate in higher-rate jurisdictions.

Strong Rule of Law and Regulatory Transparency

Slovenia's rule of law and regulatory transparency benefits foreign businesses in a concrete, measurable way: legal outcomes are predictable, enforcement is consistent, and the rules that govern your company today are unlikely to shift arbitrarily.

As an EU member state, the country operates under a dual layer of legal oversight. Domestic corporate law, primarily governed by the Companies Act (Zakon o gospodarskih družbah, ZGD-1), aligns with EU directives, which means the standards your firm is held to are compatible with the broader European regulatory framework. This alignment reduces the gap between what you expect and what you encounter.

The Agency of the Republic of Slovenia for Public Legal Records and Related Services (AJPES) maintains public registers of companies, financial statements, and beneficial ownership data. Transparency in these records means counterparties, investors, and regulators can verify your entity's standing without relying on informal channels.

Judicial independence in Slovenia ranks among the higher tiers in the EU, according to the European Commission's Rule of Law Report. For a foreign business owner, this matters because contract enforcement and dispute resolution follow established legal processes rather than discretionary authority.

Key structural features that support regulatory transparency include:

- Public access to the court register and annual financial filings through AJPES

- Mandatory beneficial ownership disclosure under the Financial Administration of the Republic of Slovenia (FURS) and anti-money laundering frameworks

- ZGD-1 codifies director duties, shareholder rights, and capital requirements in a single, publicly accessible statute

- EU-derived accounting standards (SRS or IFRS) apply to Slovenian entities, providing internationally recognized financial reporting consistency

Why Slovenia Stands Out Among EU Incorporation Destinations

Assessed against comparable Central European EU members, Slovenia presents a consistent regulatory and fiscal profile that holds up well under direct scrutiny. The jurisdictions most likely to appear on the same shortlist — Austria, Hungary, and Croatia — share the regional geography and EU membership, yet differ materially on tax rates, treaty depth, and ownership cost. Those differences, rather than any single headline figure, are what make the comparison instructive for a foreign business owner evaluating where to establish a foothold in the EU.

What the comparison below reflects is not simply a lower headline rate but a convergence of factors: the corporate tax framework under the Corporate Income Tax Act (ZDDPO-2), the participation exemption treatment, and the low minimum share capital requirement for a d.o.o. — all of which reduce both the tax burden and the administrative cost of maintaining an active entity. Austria, for instance, carries a higher standard corporate rate and a substantially higher minimum share capital threshold. Hungary's 9% rate is lower, but its regulatory environment and treaty network profile differ from what a firm seeking EU Single Market credibility typically requires.

| Parameter | Slovenia | Austria | Hungary | Croatia |

|---|---|---|---|---|

| Standard Corporate Tax Rate | 19% | 23% | 9% | 18% |

| Minimum Share Capital (standard LLC) | EUR 7,500 | EUR 35,000 | ~EUR 9,000 | EUR 2,650 |

| Participation Exemption on Dividends | Yes (95%) | Yes | Yes (with conditions) | Yes |

| Double Tax Treaties (approx.) | 60+ | 90+ | 80+ | 60+ |

| EU VAT Registration Available | Yes | Yes | Yes | Yes |

| Online Company Registration | Yes (AJPES) | Partial | Yes | Yes |

| Rule of Law Index (EU context) | High | High | Moderate | Moderate |

Compliance Services for Companies in Slovenia

Maintain your Slovenian d.o.o. in good standing with AJPES, FURS, and other statutory obligations through Expanship's ongoing compliance support.

Conclusion

Incorporating through Slovenia's d.o.o. structure gives foreign business owners a combination of advantages that are structurally embedded in local law rather than dependent on discretionary incentives. The 19% flat corporate income tax rate, participation exemption on qualifying dividends and capital gains, and full EU single market access create a tax and regulatory position that holds up under normal commercial conditions, not just favourable ones.

Those benefits carry weight because they are grounded in binding frameworks: the Corporate Income Tax Act governs the exemption rules, and EU membership underpins passporting rights across member states. For a business targeting Central European operations or cross-border EU trade, the combination of these two factors is functionally difficult to replicate outside the bloc at a comparable cost structure.

Whether this structure suits your business depends on its specific profile. A holding company extracting dividends from EU subsidiaries will benefit differently than a technology firm claiming R&D allowances under Article 55 of the Corporate Income Tax Act. The applicable advantages shift based on your revenue model, ownership structure, and operating geography. For businesses where the fit is clear, the legal and fiscal framework here is stable, well-documented, and enforceable through a court system that meets EU standards. Formalising that position starts with understanding exactly which elements of Slovenian company formation apply to your situation.

Start Your Slovenian Company Formation With Expanship Today

Expanship assists foreign founders and investors in establishing a d.o.o. under the Companies Act (ZGD-1), managing obligations with AJPES, the Agency of the Republic of Slovenia for Public Legal Records and Related Services, and maintaining ongoing compliance with FURS, the Financial Administration of the Republic of Slovenia. The services cover the full lifecycle discussed throughout this blog, from initial registration through to tax and statutory reporting requirements.

Our service scope for your Slovenian entity includes:

- Document preparation, apostille, and notarisation coordination

- Registered address and resident agent provision in Slovenia

- AJPES filing and company registration liaison

- Post-incorporation compliance management, including annual reporting and tax registration

- Corporate bank account introduction assistance

- Ongoing registered office maintenance and statutory correspondence handling

Expanship Slovenia is available to discuss your incorporation requirements directly.

Frequently Asked Questions (FAQ)

The minimum share capital for a d.o.o. is EUR 7,500, of which at least EUR 7,500 must be paid in before or at the time of registration. Each founder's minimum contribution is EUR 50. This figure is set under the ZGD-1 and has remained unchanged, making the entry threshold relatively low compared to some other EU jurisdictions with higher paid-in requirements.

Under the Corporate Income Tax Act (Zakon o davku od dohodkov pravnih oseb, ZDDPO-2), dividends received from qualifying subsidiaries are 95% exempt from corporate income tax, with the remaining 5% treated as a non-deductible expense. The exemption applies when the Slovenian parent holds at least 10% of the shares in the distributing company for a minimum holding period. The same 95% exemption framework extends to qualifying capital gains on the disposal of shareholdings.

Slovenia taxes resident companies on their worldwide income at the flat 19% rate under ZDDPO-2. Foreign-sourced income is included in the taxable base, but double tax treaty relief or a foreign tax credit can reduce or eliminate double taxation on income already taxed abroad. The applicable treatment depends on whether a treaty exists with the source country and the specific provisions of that treaty.

Under ZDDPO-2, companies can deduct 100% of qualifying R&D expenditure as an additional allowance against their taxable base, on top of the ordinary expense deduction. Qualifying activities must meet the OECD Frascati Manual criteria, covering basic research, applied research, and experimental development. Expenditure on routine product testing, market research, or quality control generally does not qualify.

Registration through the AJPES (Agencija Republike Slovenije za javnopravne evidence in storitve) online portal can be completed within one business day for straightforward cases where all documentation is in order. The e-registration process covers the entry into the Business Register of Slovenia, tax registration, and assignment of a VAT identification number if applicable. Delays typically arise from apostilled foreign documents or notarisation requirements for certain foreign-national directors.

The liability protection of a d.o.o. under the ZGD-1 limits shareholder exposure to the amount of their unpaid capital contribution, but this protection does not extend to directors who have provided personal guarantees to creditors. A director can also face personal liability under the ZGD-1 for acts of wrongful trading or breach of fiduciary duty. Personal guarantees are contractual obligations that sit outside the statutory liability shield entirely.

Slovenia has concluded over 60 double tax treaties, covering major trading and investment partners across Europe, Asia, and North America. These agreements generally reduce or eliminate withholding taxes on dividends, interest, and royalties paid to treaty-country residents, though the exact rates vary by treaty. Where no treaty applies, domestic withholding tax rates under ZDDPO-2 govern the transaction.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.