Key Takeaways

- Sweden's corporate framework under the Aktiebolagslagen imposes governance obligations on foreign directors that extend well beyond simple registration, covering shareholder agreements, board composition, and ongoing statutory compliance.

- Employer payroll tax contributions in Sweden rank among the highest in the EU, adding substantial overhead to workforce costs that directly reduces the cost-efficiency argument for establishing operations there.

- The Bokföringslagen (Accounting Act) sets strict bookkeeping and financial reporting standards that require dedicated compliance infrastructure, creating an ongoing administrative burden for foreign-owned subsidiaries unfamiliar with Swedish regulatory norms.

- Foreign investors forming a private limited company (Aktiebolag) must meet a mandatory share capital threshold, tying up capital at the point of incorporation before any operational revenue is generated.

Sweden operates under one of the more heavily regulated corporate frameworks in the EU, with obligations touching tax administration, employment, accounting, and company governance. The disadvantages of incorporating in Sweden span several of these categories, and this article addresses the specific friction points that foreign investors most commonly encounter during and after the formation process.

Not every drawback applies equally. Your exposure to particular compliance burdens will depend on your entity type, the size of your workforce, and the industry sector your business falls under.

Formed under the Aktiebolagslagen (the Swedish Companies Act), a Swedish entity carries obligations that can catch foreign directors and shareholders off guard. This article is most relevant to non-EU investors and foreign entrepreneurs establishing a subsidiary or wholly owned company in Sweden for the first time.

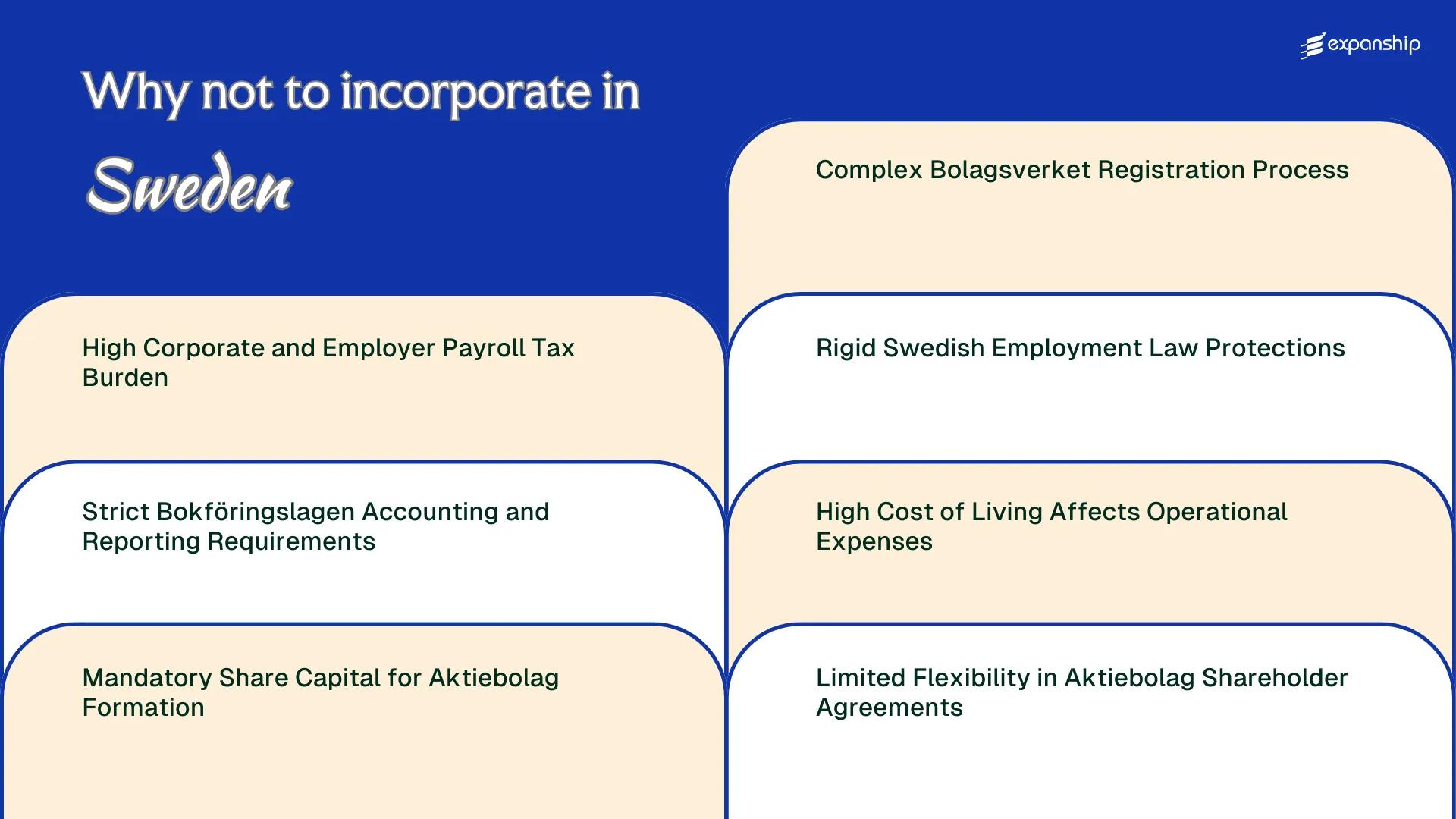

High Corporate and Employer Payroll Tax Burden

Sweden's high employer payroll tax burden ranks among the most significant cost pressures for foreign-owned businesses operating through a Swedish aktiebolag or branch structure.

Arbetsgivaravgifter: The Statutory Employer Contribution Rate

Arbetsgivaravgifter, the statutory employer social contributions, are levied at approximately 31.42% on top of each employee's gross salary. For a foreign business hiring locally, this means that every 100 SEK in gross wages costs the employer an additional 31.42 SEK before any other overhead is factored in, compressing margins substantially.

This rate applies across most employee categories and is collected by Skatteverket, Sweden's tax authority, through mandatory monthly PAYE filings. Reduced rates exist for younger and older workers under specific age thresholds, but the standard rate governs the majority of hires.

Corporate Tax in Context

The corporate income tax rate sits at 20.6%, which is broadly aligned with EU norms. However, combined with the arbetsgivaravgifter obligations, the total employer tax exposure on a staffed Swedish operation significantly exceeds what many mid-sized foreign firms anticipate when projecting entry costs.

Foreign businesses that underestimate arbetsgivaravgifter obligations when building initial payroll budgets risk structurally underpricing their Swedish operations from the outset.

Strict Bokföringslagen Accounting and Reporting Requirements

Sweden's Bokföringslagen (Accounting Act, SFS 1999:1078) sets out detailed obligations for how businesses record, store, and present financial information. For foreign-owned entities, meeting these Sweden Bokföringslagen accounting requirements demands local expertise that most international operators do not already have on staff.

All accounting records must be kept in Swedish kronor and, in practice, in Swedish. Source documents must be retained for seven years. The obligation applies from the first transaction, meaning your compliance clock starts before you generate any revenue.

Swedish accounting compliance burdens become concrete quickly for foreign owners:

- Hiring a locally qualified bookkeeper or accountant adds a fixed monthly cost that cannot be deferred until the business scales.

- Annual reports (årsredovisning) must follow the Swedish Annual Accounts Act (Årsredovisningslagen) and be filed with Bolagsverket within seven months of the financial year end, creating hard deadlines your home-country finance team is unlikely to manage unaided.

- Financial statements prepared under IFRS or US GAAP require conversion to Swedish standards before submission, duplicating reporting work.

- Digital archiving of accounting records must meet specific technical standards, adding infrastructure requirements beyond standard bookkeeping software.

Smaller entities classified as K1 or K2 companies face simplified rules, but most foreign-owned subsidiaries fall under K3, which carries significantly more detailed disclosure requirements.

Company Incorporation in Sweden

Understand the full compliance framework before you register. Expanship supports foreign businesses with entity setup and ongoing statutory obligations in Sweden.

Mandatory Share Capital for Aktiebolag Formation

Sweden Aktiebolag share capital requirements impose a minimum of SEK 25,000 (approximately EUR 2,200) before registration can proceed through Bolagsverket. That threshold must be fully paid up at the time of formation, not pledged or deferred.

For a foreign founder, this is liquid capital that must be committed upfront before the entity generates a single Swedish krona in revenue.

| Requirement | Detail | Implication |

|---|---|---|

| Minimum share capital | SEK 25,000 | Must be fully paid before registration |

| Capital availability | Required at incorporation | No deferred payment permitted |

| Governing law | Aktiebolagslagen (ABL) Ch. 1 | Statutory obligation, not discretionary |

| Private vs. public AB | SEK 25,000 vs. SEK 500,000 | Public AB threshold is significantly higher |

Under Aktiebolagslagen (ABL), the capital must be deposited and verifiable before Bolagsverket processes the registration. This creates a structural cash-flow burden that precedes any operational activity.

A foreign business testing the Swedish market cannot structure entry as a low-cost pilot; the mandatory share capital drawback in Swedish AB formation means capital is locked into the entity's equity from day one. Sole-trader alternatives exist under Swedish law, but they do not provide the limited liability protection that most foreign investors require.

Complex Bolagsverket Registration Process

The Bolagsverket registration process problems begin before your company is even formed. Bolagsverket, Sweden's Companies Registration Office, requires foreign incorporators to submit documentation in Swedish, which immediately creates a translation burden for non-Swedish-speaking founders.

Registration processing times can extend to several weeks when applications are submitted by post, which remains common for foreign applicants who cannot use the Swedish e-identification system (BankID). BankID access is typically restricted to Swedish residents, meaning most foreign founders are excluded from the faster digital registration pathway.

Your application must include a certified memorandum of association and articles of association that meet specific formal requirements. Any deviation in document structure or missing information results in rejection, restarting the clock on your registration timeline.

- All registration documents must be submitted in Swedish

- Foreign nationals without BankID cannot access the online registration portal

- The articles of association must conform to the Swedish Companies Act (Aktiebolagslagen) formatting standards

- Rejected applications do not carry forward; a new submission is required

- A registered address in Sweden must be provided before registration is approved

Sweden has no notarisation requirement for company formation documents, yet foreign applicants still face longer processing delays than domestic ones due to the BankID access restriction alone.

Rigid Swedish Employment Law Protections

Swedish employment law restrictions for businesses represent one of the more consequential structural constraints foreign employers encounter when operating through a Swedish entity.

The Scope of Protections Under LAS

Lagen om anställningsskydd (LAS), the Employment Protection Act, governs termination rights, notice periods, and redundancy procedures in ways that significantly limit employer discretion. Dismissals must be based on either personal reasons or shortage of work (arbetsbrist), and employers must follow strict seniority-based rules when selecting which employees to let go, known as "turordningsregler."

For smaller foreign-owned firms without a dedicated HR or legal function in Sweden, these obligations create real exposure. An incorrectly handled redundancy process can result in reinstatement orders or substantial financial liability, regardless of the commercial rationale behind the decision.

Operational Constraints for Foreign Employers

Collective bargaining agreements (kollektivavtal) extend these protections further, often imposing conditions beyond LAS minimums on notice periods and consultation requirements with unions. Firms that operate across multiple jurisdictions frequently find that the rigid Sweden labor law challenges here are incompatible with the flexible workforce restructuring models they apply elsewhere. Companies with fewer than 10 employees face a partial exemption from certain seniority rules, but this threshold offers limited relief for mid-sized or growing operations.

Managing Employment Compliance Challenges in Sweden

Get guidance on employer obligations, LAS requirements, and workforce structuring when operating a Swedish entity.

High Cost of Living Affects Operational Expenses

Sweden's high cost of living creates direct pressure on operational expense challenges in Sweden that foreign businesses often underestimate before establishing a local presence.

- Office rents in central Stockholm rank among the highest in the EU, meaning physical premises absorb a disproportionate share of your firm's fixed costs from day one.

- Average gross salaries for skilled professionals in Sweden are substantially higher than in most Central and Eastern European EU member states, raising your baseline payroll commitments before employer contributions are even factored in.

- Utility and facility management costs follow the same upward curve as residential prices, pushing Sweden business operating costs well above the European median for comparable square footage.

- Statutory meal allowances and transport reimbursements for employees, governed by Skatteverket guidelines, add recurring expenses that sit outside basic salary negotiations.

- These cost pressures apply regardless of company size, so a newly registered Aktiebolag carries the same high-cost environment as an established multinational entity operating locally.

Limited Flexibility in Aktiebolag Shareholder Agreements

Sweden Aktiebolag shareholder agreement limitations stem primarily from the Aktiebolagslagen (ABL), the Companies Act that governs all Swedish limited liability companies. Any shareholder agreement provision that conflicts with ABL is unenforceable against the company itself, even if all shareholders have signed it.

This distinction matters significantly for foreign investors. An agreement might be binding between the shareholders personally under contract law, yet the company's board and management can still act contrary to it without triggering corporate-level remedies.

Provisions common in other jurisdictions, such as veto rights, drag-along enforcement through the company, or board composition obligations, cannot override ABL's mandatory rules. Your only recourse for breaches is typically contractual damages between parties, not injunctive relief against corporate decisions.

- Deadlock resolution mechanisms have no statutory backing under ABL

- Transfer restrictions must be structured through the articles of association to bind the company

- Pre-emption rights are only enforceable at the corporate level if incorporated into the bolagsordningen (articles)

A foreign investor holding 30% in a Swedish AB under a shareholder agreement containing a veto on major acquisitions may find that if the provision is absent from the bolagsordningen, the board can approve the acquisition regardless, leaving the investor with a damages claim but no ability to reverse the transaction.

Navigating Challenges for Mitigating These Drawbacks

Mitigating Sweden incorporation drawbacks requires a structural approach rather than reactive fixes. The disadvantages outlined in this blog — from payroll tax exposure to Bolagsverket registration complexity — can each be addressed through deliberate planning before the entity is formed.

- Register your aktiebolag through the Bolagsverket e-tjänster portal to reduce processing delays in the formation workflow.

- Deposit the minimum SEK 25,000 share capital requirement into a blocked account prior to submitting your registration application.

- Engage a licensed Swedish auditor early to establish Bokföringslagen-compliant accounting systems before the first financial year closes.

- Consult Skatteverket's employer registration process to calculate total payroll cost, including social contributions, before hiring staff.

- Draft shareholder agreements with explicit provisions that account for the limited default flexibility under the Aktiebolagslagen.

- Benchmark salary structures against Swedish cost-of-living indices to set realistic operational budgets from the outset.

Each of these steps operates within a tightly regulated framework where Skatteverket, Bolagsverket, and Swedish labour law collectively define the boundaries of compliant operations. Overcoming Sweden company formation risks depends largely on how thoroughly your business accounts for these interdependencies before incorporation, not after.

Sweden's Business Landscape Still Worth It

Sweden's corporate tax rate sits at 20.6%, employer payroll contributions add roughly 31.42% on top of salaries, and the administrative obligations under Bokföringslagen are non-trivial. These are real structural costs. Against that, the country offers a stable legal system, reliable institutional infrastructure, and consistent enforcement of commercial contracts — conditions that matter to foreign-owned entities operating at a distance.

| Pros | Cons |

|---|---|

| Sweden's legal and regulatory framework is predictable, with consistent enforcement through established institutions. | The 20.6% corporate tax rate, combined with employer contributions of approximately 31.42%, creates a high total labour cost. |

| Bolagsverket operates as a structured registry with clear procedures, providing legal certainty once registration is complete. | The Aktiebolag requires a minimum share capital of SEK 25,000, which must be paid up before registration is finalised. |

| Membership in the EU single market gives Swedish-registered companies direct access to European trade and financial systems. | Bokföringslagen imposes strict bookkeeping and annual reporting obligations that require ongoing professional oversight. |

| Swedish employment law provides a stable, well-defined framework that reduces ambiguous contractual disputes. | Lagen om anställningsskydd (LAS) limits dismissal flexibility, making workforce adjustments procedurally complex and costly. |

| High labour productivity and education levels can offset some of the cost burden over the longer term. | High operating costs driven by the cost of living affect office rental, salaries, and general overhead in ways that compound incorporation costs. |

Shareholder agreement flexibility within an Aktiebolag is also constrained relative to other jurisdictions, limiting how founders can structure governance and exit provisions. For a business that requires lean operational costs or a flexible equity structure at the outset, those constraints carry weight.

Compliance Services for Companies in Sweden

Managing ongoing obligations under Bokföringslagen, Bolagsverket reporting requirements, and Swedish corporate law involves recurring deadlines and procedural precision. Review what compliance support for a Swedish entity covers.

Conclusion

The cons of Sweden business incorporation are real and measurable. Employer social contributions running above 31% of gross salary, combined with the Aktiebolag's SEK 25,000 minimum share capital requirement and the administrative weight of Bokföringslagen compliance, create a cost structure that demands careful financial modelling before entry. Bolagsverket's registration process adds procedural layers that extend timelines. These are structural features of the Swedish system, not temporary conditions. How you prepare for them determines whether your entity operates efficiently or absorbs avoidable costs from the outset.

Expanship's Support for Your Sweden Expansion

Expanship works with businesses managing Sweden expansion compliance support across the specific obligations this structure demands, from coordinating with Bolagsverket during registration to maintaining ongoing adherence under Bokföringslagen's accounting requirements and the Swedish Tax Agency's reporting cycles. Our role is to reduce the administrative burden these processes place on your team, not to change how Swedish regulation works.

Beyond formation, Expanship supports the full scope of establishing your entity in Sweden.

- We prepare and file company registration documents on your behalf.

- Registered agent and office services are provided to satisfy Swedish address requirements.

- Our team liaises directly with Bolagsverket and other relevant authorities on government filings.

- Post-incorporation compliance management keeps your firm aligned with ongoing Swedish obligations.

- Banking introduction assistance connects your business with suitable financial institutions.

- We handle tax registration and coordinate with the Swedish Tax Agency on your behalf.

Reach out to Expanship Sweden to discuss how we can support your incorporation process.

Frequently Asked Questions (FAQ)

Sweden's corporate income tax rate sits at 20.6%, which is broadly competitive within the EU. The more significant burden comes from employer social contributions, which add approximately 31.42% on top of gross salaries. When you combine payroll taxes with Sweden's high statutory minimum compensation expectations, total employment costs can be substantially higher than in jurisdictions like Ireland or Estonia.

The SEK 25,000 minimum share capital requirement applies specifically to the private Aktiebolag (AB), which is the most commonly used structure for foreign entrants. A public Aktiebolag (publ) carries a significantly higher threshold of SEK 500,000. Other Swedish business forms, such as the handelsbolag or enskild firma, do not carry a share capital requirement, though they come with their own structural limitations for foreign owners.

Violations of the Bokföringslagen, Sweden's Accounting Act, can result in criminal liability, including fines or imprisonment in serious cases involving intentional misrepresentation or failure to maintain records. Bolagsverket can also initiate compulsory liquidation proceedings if a company fails to submit annual reports to the agency within prescribed deadlines. The standard deadline for filing annual accounts is seven months after the end of the financial year.

Under the Aktiebolagslagen, Sweden's Companies Act, if a board of directors identifies that equity has fallen below half of the registered share capital, they are legally required to prepare a balance sheet for liquidation purposes and convene an extraordinary general meeting. Failure to follow this procedure exposes individual board members to personal liability for company debts incurred during the period of inaction. This obligation applies regardless of whether the shortfall is temporary.

Foreign nationals without a Swedish personal identity number (personnummer) face additional steps during registration, including submitting certified identification documents and, in some cases, appointing a local authorized representative. Bolagsverket does not accept unsigned or uncertified foreign documents, which can extend the registration timeline considerably. EU and non-EU nationals are subject to broadly the same documentation requirements, though notarization standards vary by country of origin.

Swedish authorities, including the Swedish Tax Agency (Skatteverket), apply a substance-over-form analysis when assessing whether a working relationship constitutes employment. If a contractor works exclusively or predominantly for one company, follows its direction, and lacks genuine entrepreneurial independence, the relationship may be reclassified as employment under the Lag om anställningsskydd (LAS). Reclassification triggers retroactive obligations including social contributions, vacation pay under the Semesterlagen, and potential unfair dismissal exposure.

LAS requires employers to follow a strict "last in, first out" seniority principle when conducting redundancies, unless a separate collective bargaining agreement modifies the order. Employees with longer tenure must be retained over newer hires, even when the newer hire holds more relevant skills for a restructured operation. Deviating from this order without a valid collective agreement or individual written exception exposes the company to reinstatement claims and significant damages.

The cost burden is proportionally heavier for foreign entrants because they lack established local supplier relationships, often need to offer relocation packages or premium salaries to attract talent, and face currency conversion costs if their treasury operates outside the Swedish krona. Domestic firms have typically absorbed cost structures over time and benefit from existing contracts. Office rental costs in Stockholm in particular rank among the highest in Northern Europe, compounding the impact on early-stage foreign operations.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.