Key Takeaways

- The Privat Aktiebolag (AB) is Sweden's most commonly registered entity, offering limited liability to both resident and non-resident founders through a defined share capital requirement.

- All legal entities in Sweden are registered and maintained through the Bolagsverket (Swedish Companies Registration Office), with ongoing tax compliance administered by Skatteverket.

- Handelsbolag and Kommanditbolag expose partners to personal liability, making them suitable only for closely-held ventures where that risk is acceptable.

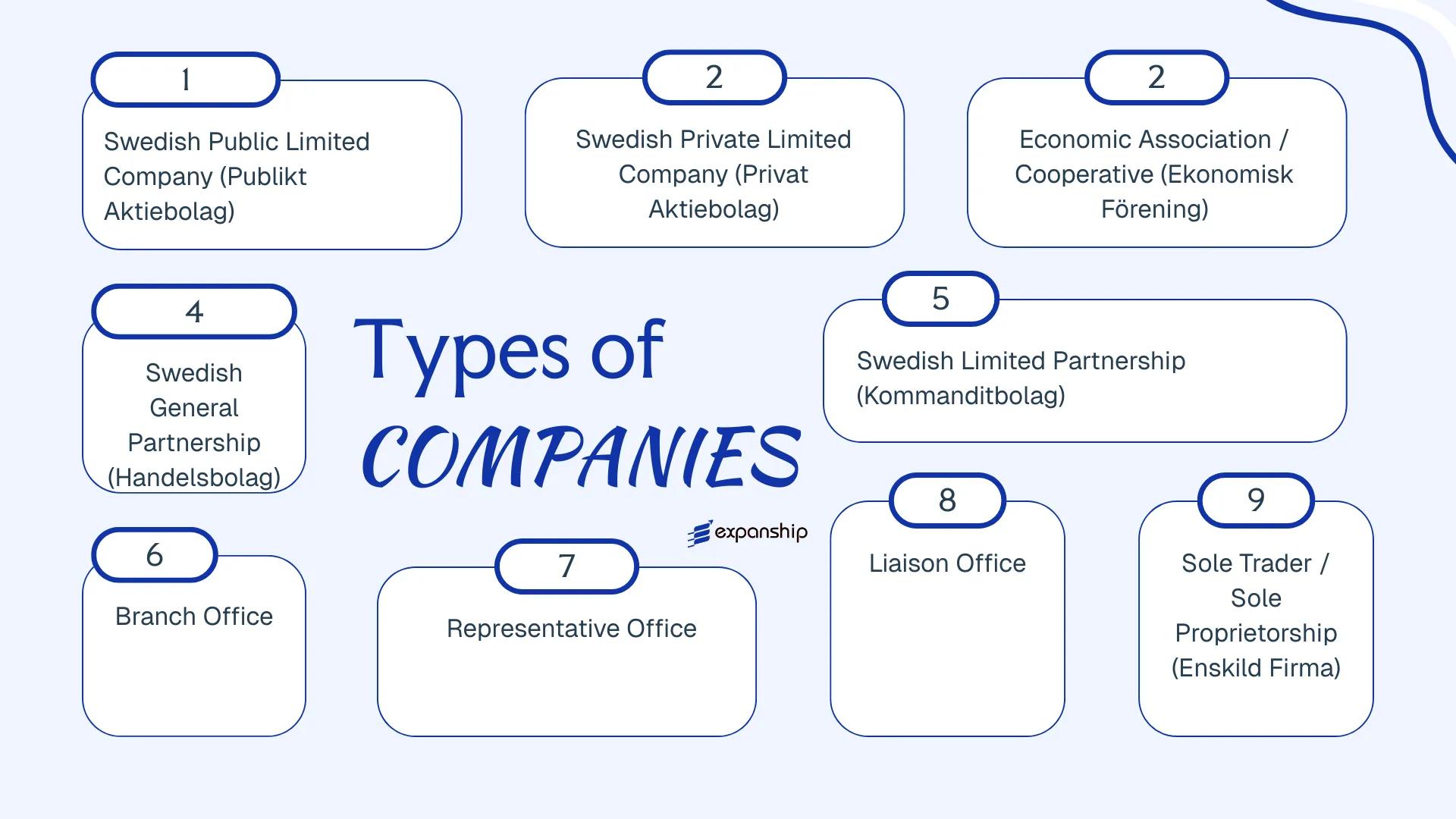

- Sweden's corporate framework spans seven distinct legal forms — from the Publikt Aktiebolag for capital-market-facing enterprises to the Enskild Firma for individual sole traders — each carrying different obligations for liability, governance, and taxation.

Introduction to Entity Types in Sweden

Situated in northern Europe, Sweden shares land borders with Norway and Finland and sits across the water from Denmark. As a sovereign state and member of the European Union, the country operates a mature, well-regulated corporate environment governed by the Bolagsverket (Swedish Companies Registration Office), which administers the registration and maintenance of legal entities in Sweden.

Sweden applies a residence-based tax system with a standard corporate income tax rate, participation in the EU VAT framework, and an extensive network of double tax treaties.

The types of business entities in Sweden span a range of structures suited to different operational needs and investor profiles. Available forms include the Privat Aktiebolag, Publikt Aktiebolag, Handelsbolag, Kommanditbolag, Ekonomisk Förening, Enskild Firma, and foreign business presence vehicles such as branch offices and representative offices.

Each structure carries distinct implications for liability, taxation, governance, and registration requirements — this article examines all of them in detail.

An Overview of Business Structures in Sweden

Sweden's company law framework accommodates several distinct entity types, each governed primarily by the Aktiebolagslagen (Companies Act 2005:551) and, for other structures, by dedicated legislation such as the Lag om handelsbolag och enkla bolag (1980:1102) and the Lag om ekonomiska föreningar (2018:672). Each structure carries different implications for liability, ownership, taxation, and operational scope. The sections that follow examine each in detail.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Privat Aktiebolag (AB) | Private limited company | Limited | Taxed | Yes | 1 shareholder | Bolagsverket | Aktiebolagslagen (2005:551) |

| Publikt Aktiebolag (publ AB) | Public limited company | Limited | Taxed | Yes | 1 shareholder | Bolagsverket / Finansinspektionen | Aktiebolagslagen (2005:551) |

| Handelsbolag (HB) | General partnership | Unlimited | Partners taxed | Yes | 2 partners | Bolagsverket | Lag (1980:1102) |

| Kommanditbolag (KB) | Limited partnership | Mixed | Partners taxed | Yes | 2 partners (1 general) | Bolagsverket | Lag (1980:1102) |

| Ekonomisk Förening | Cooperative / association | Limited | Taxed | Yes | 3 members | Bolagsverket | Lag om ekonomiska föreningar (2018:672) |

| Filial (Branch Office) | Branch of foreign entity | Parent liable | Taxed on Swedish income | Yes | N/A | Bolagsverket | Lag om utländska filialer (1992:160) |

| Representationskontor | Representative office | Parent liable | Generally exempt | Restricted | N/A | Bolagsverket | No dedicated statute |

| Enskild Firma | Sole proprietorship | Unlimited | Owner taxed | Yes | 1 individual | Bolagsverket / Skatteverket | Lag (1985:286) |

Each of these structures is examined in full in the sections below.

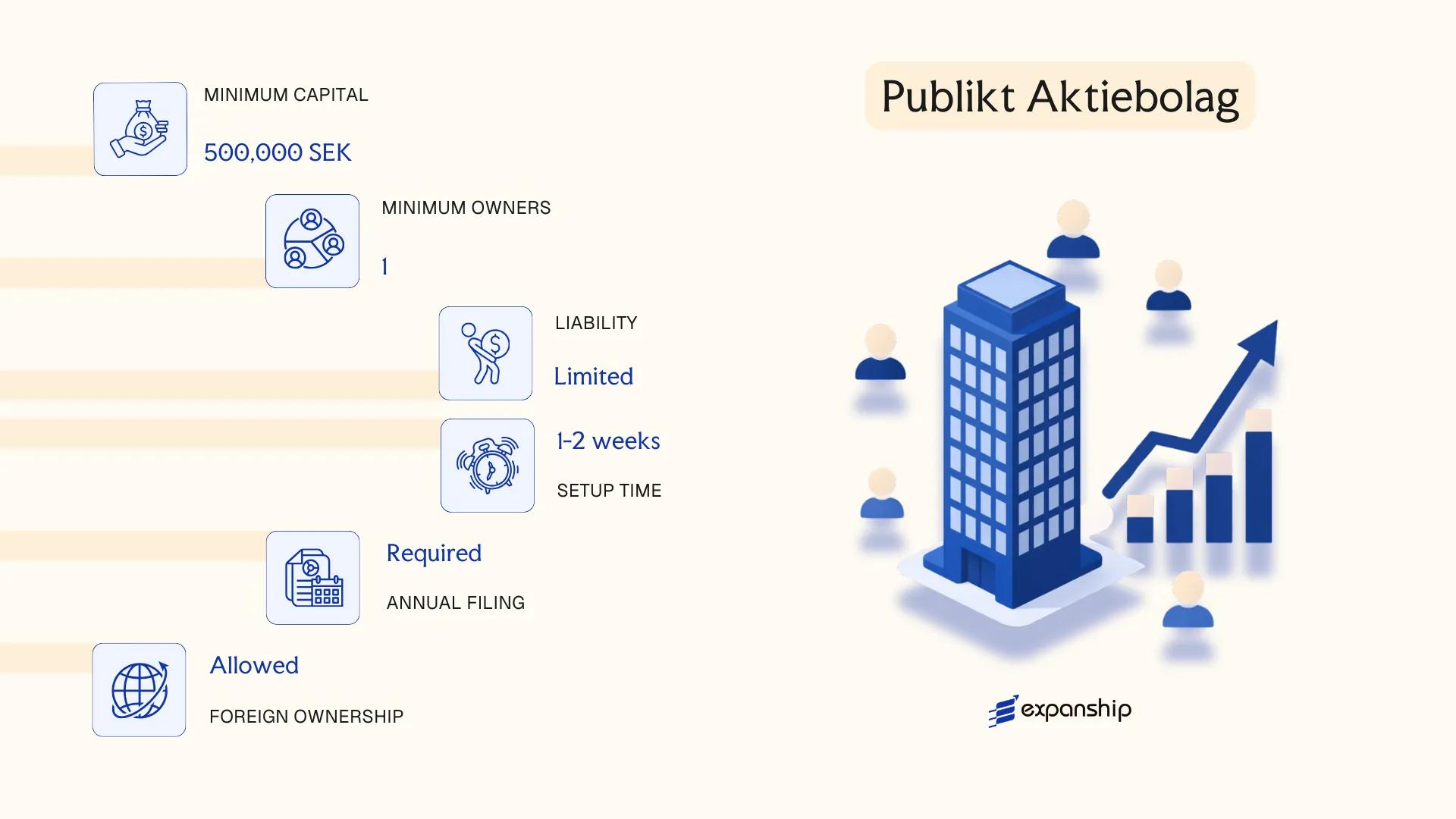

Publikt Aktiebolag (Swedish Public Limited Company)

A Publikt Aktiebolag (publ AB) is the public limited company structure under Swedish law, governed by the Aktiebolagslag (2005:551). As with all aktiebolag, the entity holds separate legal personality distinct from its shareholders, meaning liabilities remain confined to the company's assets rather than extending to individual owners.

Publ AB formation in Sweden is the required route for any business seeking a listing on a regulated stock exchange, such as Nasdaq Stockholm or NGM Equity. The designation "publ" must appear in the firm's registered name, and shares may be offered to the public under applicable securities regulations.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Publikt Aktiebolag (publ AB) | Separate legal entity; limited liability |

| Members | Shareholders (no minimum number); Board of Directors: min. 3 members | A Managing Director is required; at least one board member and the MD must be EEA-resident unless exemption granted by Bolagsverket |

| Local Presence | Registered office in Sweden required | Registered with Bolagsverket (Companies Registration Office) |

| Share Capital | Minimum SEK 500,000 | Must be fully subscribed at formation; shares can be publicly traded |

| Privacy | Shareholder register is public | Annual reports filed with Bolagsverket are publicly accessible |

| Auditor | Certified auditor (revisor) mandatory | Must be approved by Revisorsinspektionen |

Focus Points

- Taxation: Subject to corporate income tax at 20.6%; VAT registration obligations apply; withholding tax of 30% on dividends to non-residents, reducible under applicable tax treaties; no stamp duty on share transfers.

- Annual Compliance: Mandatory annual general meeting; audited financial statements filed with Bolagsverket within seven months of the financial year-end.

- Treaty Access: Qualifies as a Swedish tax resident entity, giving access to Sweden's extensive double tax treaty network.

- Securities Regulation: Public share offerings fall under Finansinspektionen's oversight; a prospectus is required for listings.

- Conversion: Can be converted to a privat aktiebolag (private limited company) provided the share capital is reduced to meet private thresholds and public offerings cease.

Closing

A publ AB suits large enterprises, publicly listed corporations, and businesses requiring access to capital markets through public equity issuance. The ability to freely offer shares to the public is a defining structural advantage, though the elevated minimum share capital of SEK 500,000 and mandatory audit requirements make it a disproportionate structure for smaller or closely held operations.

Businesses planning a public listing or requiring broad shareholder participation through regulated Swedish or EU capital markets.

Company Incorporation in Sweden

Incorporate a Swedish Aktiebolag or explore the right entity structure for your business in Sweden.

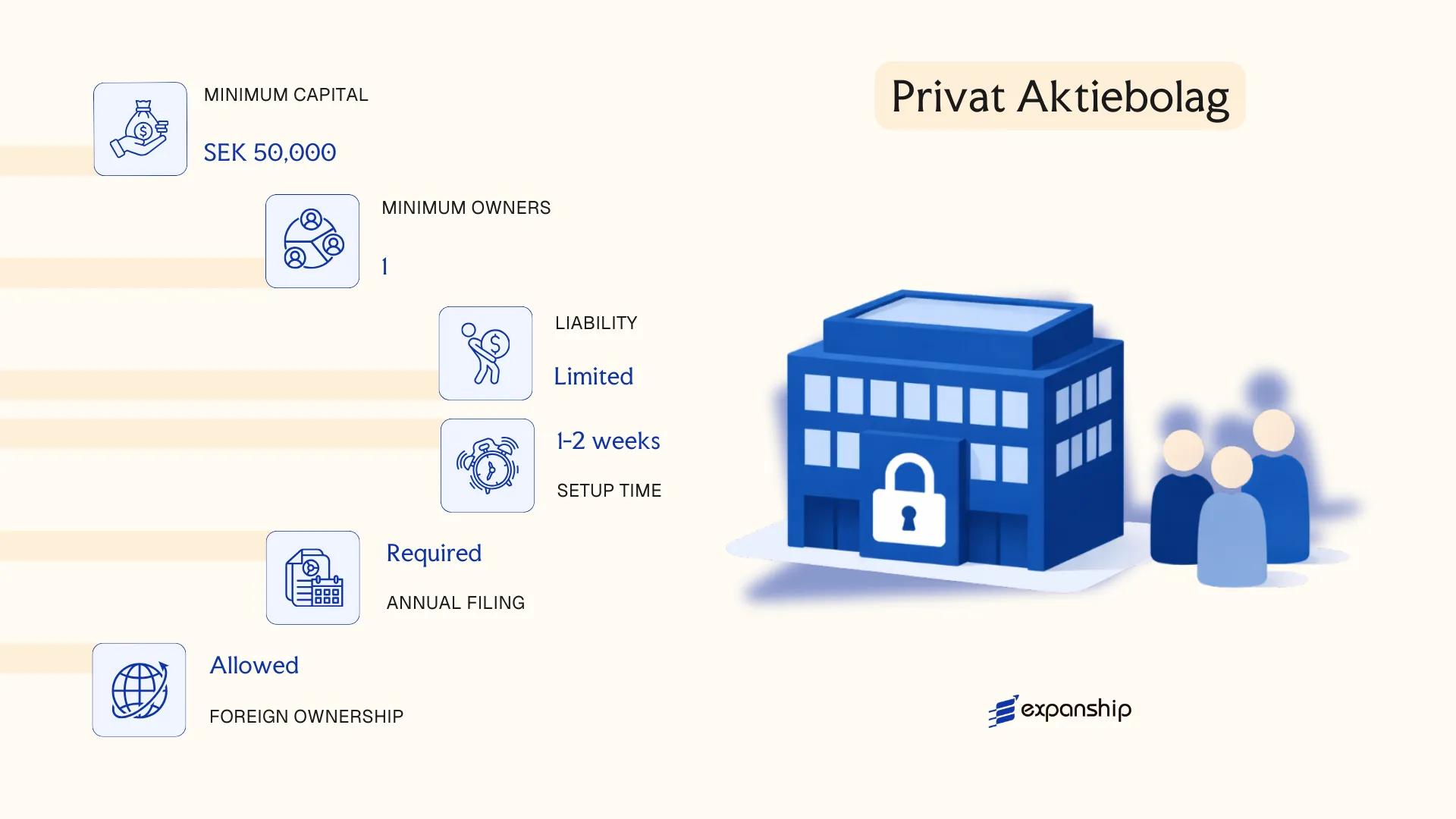

Privat Aktiebolag (Swedish Private Limited Company)

The privat aktiebolag (private limited company Sweden) is governed by the Aktiebolagslagen (Companies Act, SFS 2005:551). It is the most commonly registered corporate form for small and medium-sized enterprises operating in Sweden, offering shareholders full limited liability separate from the company's obligations.

Registration is handled through the Bolagsverket (Swedish Companies Registration Office), which maintains the central business register. The entity holds a distinct legal personality, meaning it can enter contracts, own assets, and incur liabilities in its own name.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Privat Aktiebolag (AB) | Private, non-publicly traded company |

| Members | Shareholders: minimum 1, no maximum; Board of Directors: minimum 1 director | A sole shareholder may also serve as the sole board member |

| Local Presence | Registered office address in Sweden required; at least one board member must be resident in the EEA | Non-EEA residents require a special dispensation from Bolagsverket |

| Share Capital | SEK 25,000 minimum | Must be fully paid up before registration |

| Privacy | Shareholder register is not publicly searchable by default; annual reports filed with Bolagsverket are public record | Beneficial ownership must be reported to Bolagsverket under anti-money laundering rules |

Focus Points

- Taxation: Subject to corporate income tax at 20.6%; VAT registration required if turnover exceeds SEK 80,000; withholding tax of 30% applies to dividends paid to non-resident shareholders, reducible under applicable tax treaties; no stamp duty on share transfers.

- Annual Compliance: Annual accounts must be filed with Bolagsverket; an auditor is mandatory once the entity meets two of three thresholds (50+ employees, SEK 40M+ net turnover, SEK 20M+ balance sheet total).

- Treaty Access: Sweden's extensive tax treaty network is accessible, making the AB a viable structure for international holding arrangements.

- Conversion: An AB can be converted to a publikt aktiebolag (public limited company) provided it meets the higher share capital and governance requirements under the same Aktiebolagslagen.

Closing

The AB company registration Sweden structure suits trading operations, holding arrangements, and IP ownership vehicles where liability protection and access to Sweden's treaty network are priorities. Its main limitation is the ongoing compliance burden, particularly the mandatory audit requirement once the entity scales beyond statutory thresholds.

The privat aktiebolag is best suited for entrepreneurs and foreign investors establishing an active trading presence or holding structure in Sweden with one or more shareholders.

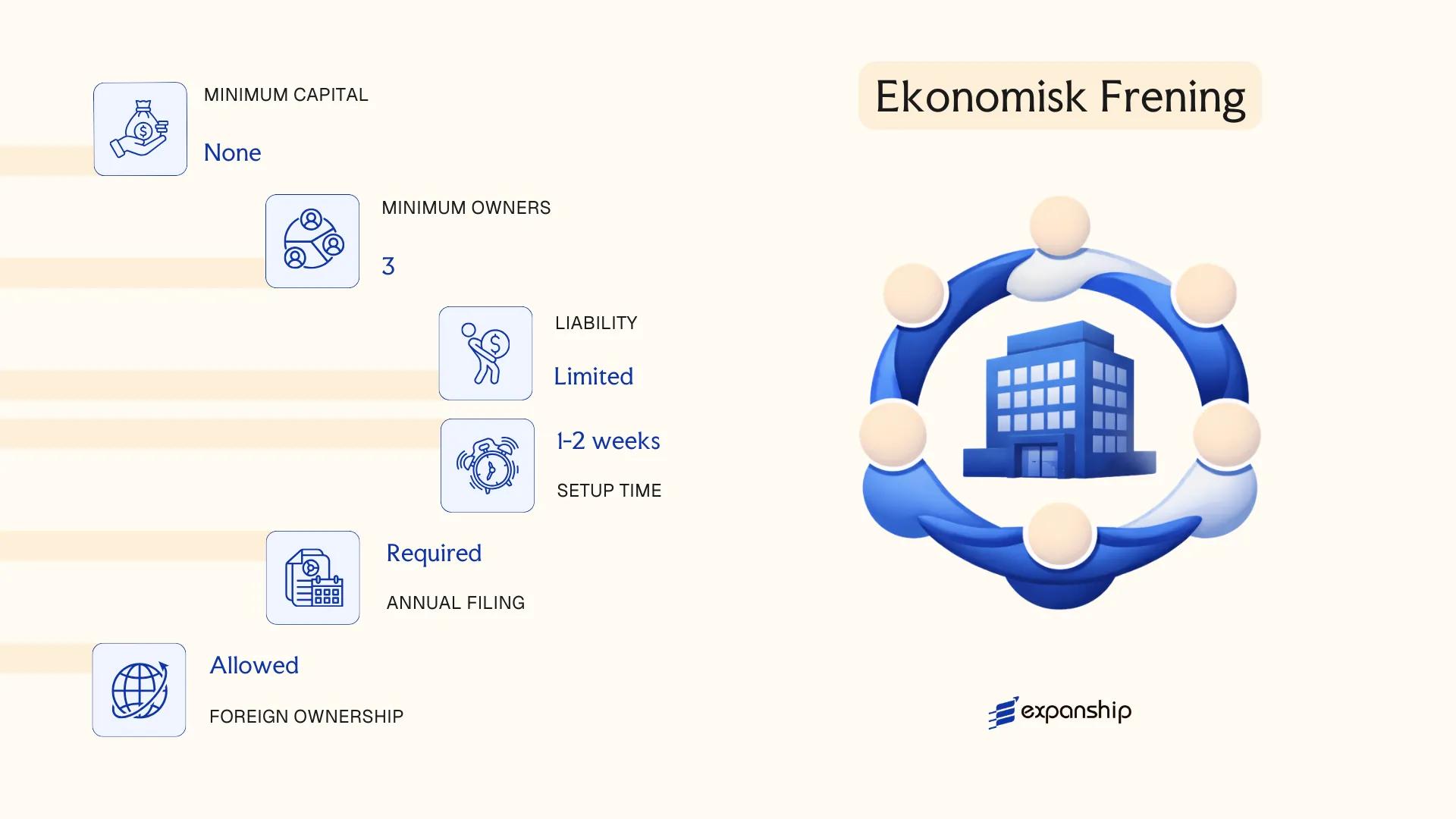

Ekonomisk Förening (Economic Association / Cooperative)

An ekonomisk förening cooperative in Sweden is governed by the Lag om ekonomiska föreningar (Swedish Cooperative Societies Act, 2018:672). The entity holds a separate legal personality distinct from its members, and members are generally protected by limited liability for the association's obligations.

Unlike capital-driven structures, this form is built around member benefit rather than investor return. Surplus generated by the entity is distributed based on each member's participation or transaction volume with the cooperative, not on capital contribution.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Economic Association (Cooperative) | Separate legal personality; registered with Bolagsverket |

| Members | Minimum 3 members (natural or legal persons) | No statutory maximum; membership is open by default unless the bylaws restrict it |

| Governing Body | Board of Directors (styrelse) | Minimum 3 board members; one must be a Swedish resident unless exempted |

| Registered Office | Must maintain a registered address in Sweden | Required for Bolagsverket registration |

| Share Capital | No minimum share capital requirement | Members pay an insatsskyldighet (contribution) as set in the bylaws |

| Privacy | Member register is not publicly disclosed | Board details are publicly available via Bolagsverket |

Focus Points

- Taxation: Subject to 20.6% corporate tax on net income; VAT registration required above SEK 80,000 threshold; member distributions may attract income tax depending on recipient type; no specific withholding tax exemptions unique to this form.

- Annual Compliance: Annual accounts must be filed with Bolagsverket; larger cooperatives require a certified auditor (revisor).

- Economic Substance: The entity must actively serve member interests to retain its cooperative classification; purely passive structures risk reclassification.

- Conversion: Conversion to an aktiebolag is possible under Swedish law, subject to member approval and regulatory filing requirements.

- Restrictions: Cannot list shares publicly; profit distribution logic is member-participation-based, which limits use as a standard investment vehicle.

Closing

An ekonomisk förening suits member-driven operations such as agricultural cooperatives, housing associations, and worker-owned service businesses, where the commercial purpose is to serve members rather than generate investor returns. The absence of minimum capital is an accessible feature, though the mandatory member-benefit structure makes this form unsuitable for conventional equity investment or shareholder profit distribution models.

This entity is best suited for groups of three or more individuals or organisations seeking to operate a shared commercial activity where economic benefit flows back to participants based on use rather than ownership stake.

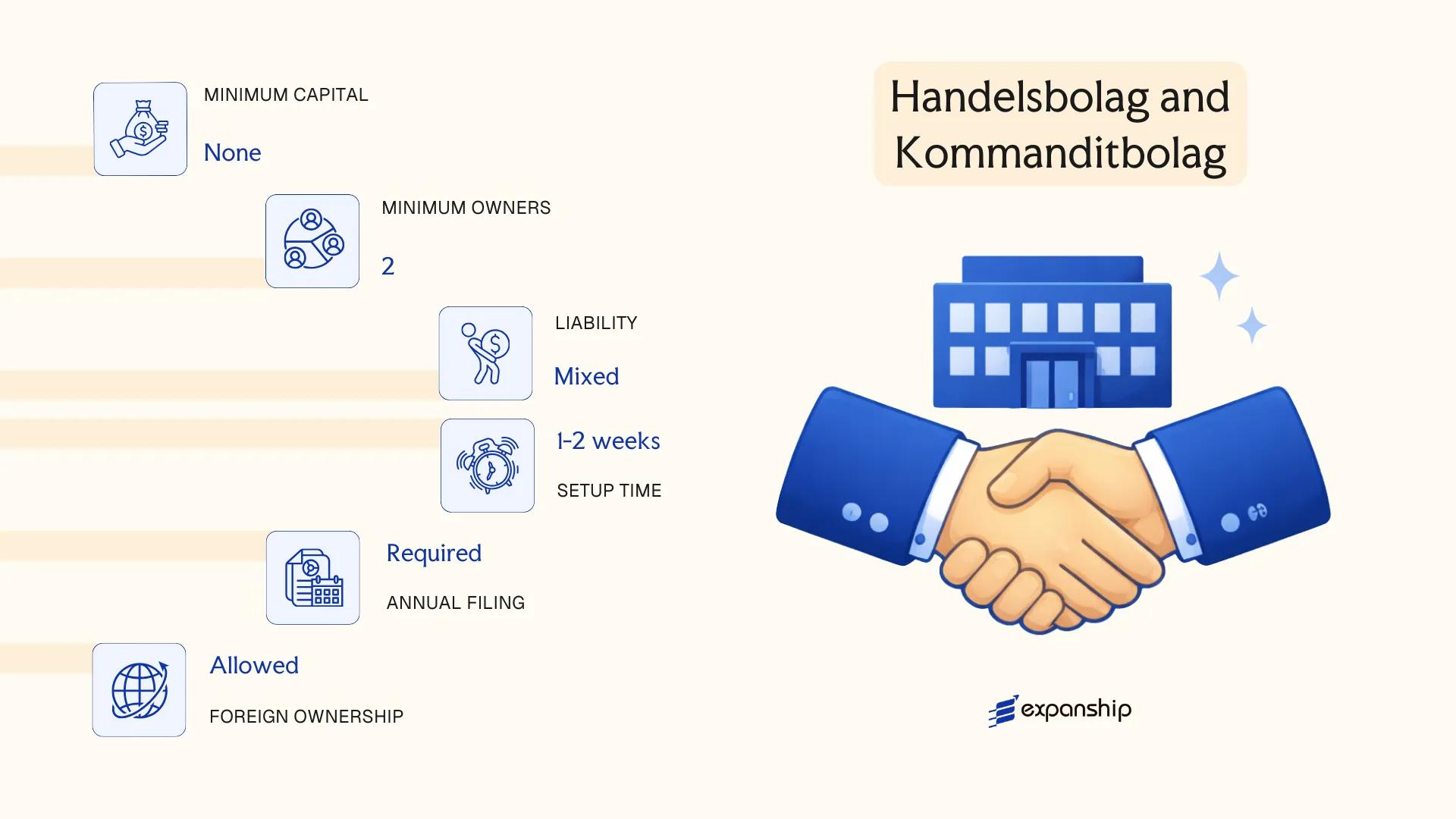

Handelsbolag and Kommanditbolag (Swedish Partnerships) [General Partnership, Limited Partnership]

Both the Handelsbolag (HB) and Kommanditbolag (KB) are governed by the Partnership and Simple Partnership Act (Lag om handelsbolag och enkla bolag, 1980:1102). Each form carries separate legal personality — the firm can own assets, enter contracts, and incur liabilities in its own name — yet neither structure offers limited liability to all its partners by default.

The core structural difference lies in liability exposure. In a Handelsbolag, every partner bears joint and several personal liability for the firm's obligations. A Kommanditbolag splits that liability: at least one general partner retains unlimited liability, while one or more limited partners are liable only up to their registered capital contribution. Both must be registered with Bolagsverket, the Swedish Companies Registration Office.

Key Characteristics

| Requirement | Handelsbolag (HB) | Kommanditbolag (KB) |

|---|---|---|

| Legal Form | Partnership with separate legal personality | Limited partnership with separate legal personality |

| Partners | Referred to as partners (bolagsmän); minimum 2, no maximum | Minimum 1 general partner (komplementär) + 1 limited partner (kommanditdelägare); no maximum |

| Liability | All partners: unlimited, joint and several | General partner: unlimited; limited partner: capped at registered contribution |

| Registered Capital | No minimum capital requirement | No minimum; limited partner's contribution must be registered |

| Local Presence | Registered address in Sweden required; no mandatory local director | Registered address in Sweden required; general partner may be a legal entity |

| Privacy | Partner names and roles disclosed in public register | General and limited partner details publicly registered with Bolagsverket |

Focus Points

- Taxation: Partnerships are fiscally transparent — profits are allocated to and taxed at the partner level, not the entity level; partners subject to Swedish income tax or corporate tax depending on their legal status; VAT registration required if turnover exceeds the applicable threshold.

- Annual Compliance: Annual accounts must be filed with Bolagsverket; Kommanditbolag above certain size thresholds are subject to statutory audit requirements.

- Economic Substance: No formal substance regime, but partners conducting business through the entity may trigger permanent establishment considerations for foreign partners.

- Conversion: A Handelsbolag may be converted into a Kommanditbolag or an Aktiebolag through a statutory process without dissolving the firm.

- Restrictions: Foreign nationals may act as partners, though non-EEA residents should verify residence and permit requirements before registration.

Sub-Types

Handelsbolag (General Partnership)

All partners hold equal management rights by default unless the partnership agreement specifies otherwise. This structure suits small professional practices or family-run trading operations where all participants accept unlimited exposure.

Kommanditbolag (Limited Partnership)

Only the general partner manages the business; limited partners are prohibited from actively managing the firm without risking the loss of their liability protection. This form is frequently used for private equity fund structures and real estate investment vehicles in Sweden.

Closing

Partnerships suit small domestic ventures, professional collaborations, and certain fund structures where pass-through taxation is preferred over corporate-level tax. The fiscal transparency is a clear structural advantage, though unlimited personal liability for at least one partner remains a substantive operational risk.

Handelsbolag and Kommanditbolag are best suited for small domestic businesses or structured investment vehicles where partners are comfortable with pass-through taxation and have assessed their personal liability exposure.

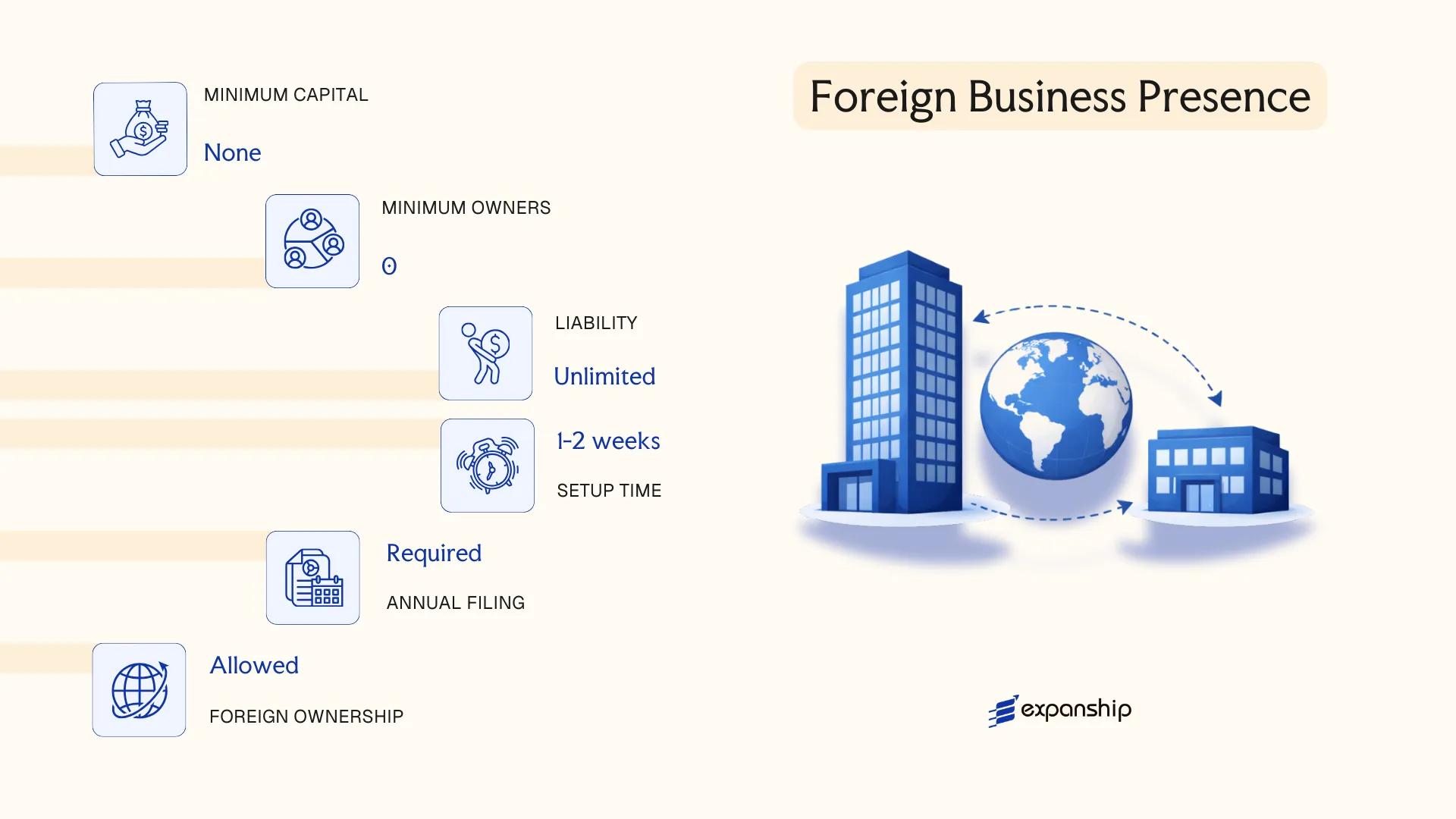

Foreign Business Presence in Sweden [Branch Office, Representative Office, Liaison Office]

A foreign company branch office Sweden registration is governed by the Foreign Branches Act (Lag om utländska filialer m.m., 1992:160), which sets out the conditions under which non-Swedish entities may conduct business activity within the country. A branch (filial) is not a separate legal entity — it remains an extension of the parent company, which bears full liability for the branch's obligations.

Registration is handled through the Swedish Companies Registration Office (Bolagsverket). The branch must appoint a managing director (verkställande direktör) who is resident in the European Economic Area, unless an exemption is granted.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Branch (Filial) — not a separate legal entity | Parent company retains full liability |

| Managing Director | One EEA-resident individual required | Exemption possible via Bolagsverket |

| Registered Address | Physical address in Sweden required | Cannot use a P.O. box |

| Capital | No minimum capital requirement | Parent company's capital structure applies |

| Accounting | Separate Swedish accounts required | Must follow Swedish accounting standards |

| Privacy | Managing director's details publicly registered | Parent company documents filed with Bolagsverket |

Focus Points

- Taxation: Branch profits are subject to Swedish corporate income tax (20.6%); VAT registration required if taxable turnover thresholds are met; withholding tax may apply to certain cross-border payments depending on applicable tax treaties.

- Economic Substance: The branch must genuinely operate in Sweden — Bolagsverket and the Swedish Tax Agency (Skatteverket) may scrutinise dormant or minimal-activity registrations.

- Annual Compliance: Annual reports must be filed with Bolagsverket within seven months of the parent's financial year-end.

- Treaty Access: Branches may access Sweden's tax treaty network, though treaty benefits depend on the parent company's residence and the specific treaty provisions.

Sub-Types

Representative Office / Liaison Office

Sweden does not maintain a formally separate "representative office" or "liaison office" registration category under Swedish law. A foreign business wishing to conduct only preparatory or auxiliary activities — such as market research or promotional work — without commercial transactions may do so without registering a branch, provided the activities fall outside the definition of conducting business (bedriva näringsverksamhet) under the Foreign Branches Act. No formal registration with Bolagsverket is required in such cases, but tax residency implications should be assessed with Skatteverket.

Closing

A branch is suited to foreign companies that want direct operational presence without incorporating a local subsidiary, though the parent's unlimited exposure to branch liabilities is a material drawback for risk management purposes.

Foreign companies testing the Swedish market or executing specific project-based work before committing to a full subsidiary structure.

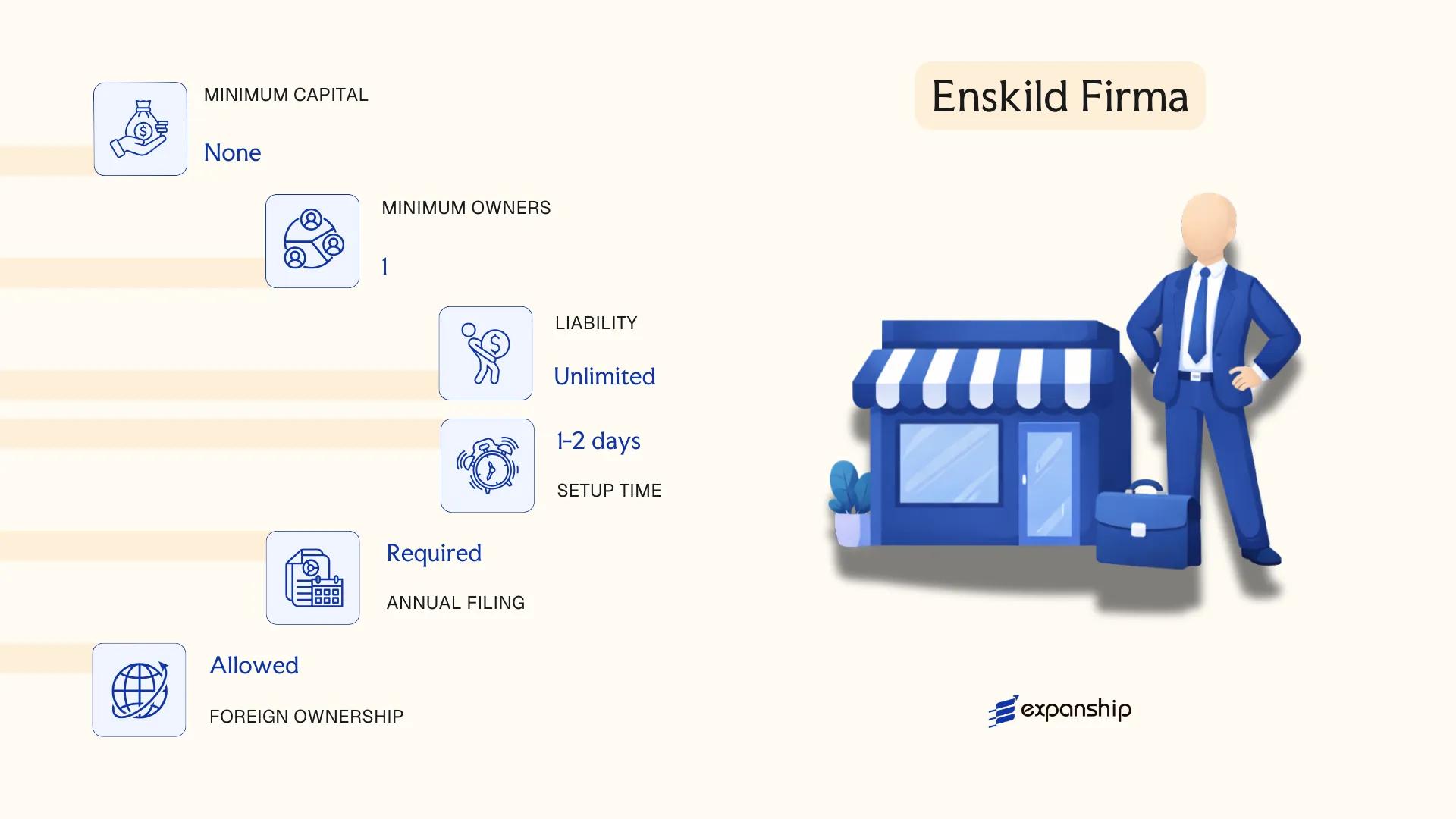

Enskild Firma (Sole Trader / Sole Proprietorship)

An enskild firma sole trader Sweden structure is governed by the Business Names Act (Lag om företagsnamn, 2018:1653) and related provisions under Swedish commercial law. Unlike an aktiebolag, this form carries no separate legal personality — the proprietor and the business are legally the same entity, meaning personal assets are fully exposed to business liabilities.

Registration is handled through the Swedish Companies Registration Office (Bolagsverket), and the process is straightforward for Swedish residents. Non-EU nationals face significant restrictions, as this structure is generally unavailable to those without residency or a Swedish personal identity number (personnummer).

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated sole proprietorship | No separate legal personality from the owner |

| Members | One proprietor | Must be a natural person; no co-ownership permitted |

| Local Presence | Registered Swedish address required | Must be a physical address; no P.O. boxes |

| Capital | No minimum capital requirement | No share capital; proprietor funds operations directly |

| Liability | Unlimited personal liability | All personal assets at risk for business debts |

| Privacy | Owner name publicly linked to the firm | Bolagsverket records are publicly accessible |

Focus Points

- Taxation: Business income is taxed as personal income under Swedish progressive tax rates (up to approximately 57%); VAT registration is required once turnover exceeds SEK 80,000 annually; no corporate tax applies.

- Social Contributions: The proprietor pays egenavgifter (self-employed social security contributions) at approximately 28.97% on net profit.

- Annual Compliance: No statutory audit requirement; annual income must be declared via the proprietor's personal tax return (inkomstdeklaration).

- Conversion: The firm can be converted into a privat aktiebolag, though assets and liabilities must be formally transferred as the enskild firma itself cannot be merged or acquired.

- Restrictions: Only Swedish residents with a personnummer may register; foreign nationals without residency cannot use this structure.

Closing

This structure suits freelancers, consultants, and sole operators running low-risk, low-turnover activities where administrative simplicity outweighs the absence of liability protection. The primary advantage is minimal setup cost and compliance burden; the clear limitation is unlimited personal liability, which makes it unsuitable for businesses carrying financial or legal risk.

Best suited for Swedish residents operating as self-employed individuals with limited commercial risk and no intention to raise external capital or take on partners.

How to Choose the Right Entity Type in Sweden

Selecting how to choose the right company type in Sweden requires examining your operational profile against the legal characteristics of each available structure before any registration takes place.

Why Your Entity Choice Matters

The structure you register has binding legal and financial consequences that are difficult to reverse after formation.

- Registering a branch (filial) when your activity constitutes a permanent establishment under Swedish domestic law may not shield the parent company from Swedish corporate tax obligations, exposing it to unexpected tax liability.

- Choosing an Enskild Firma when your business incurs significant third-party liability leaves you personally responsible for all debts, since no legal separation exists between you and the firm.

- Selecting a Handelsbolag for multi-party operations without a carefully drafted partnership agreement exposes each general partner to unlimited joint and several liability under the Act on Trading Companies and Simple Partnerships (lag om handelsbolag och enkla bolag, 1980:1102).

- Forming a Privat Aktiebolag when your capital-raising needs require public issuance locks you into a structure that prohibits offering shares to the general public under the Swedish Companies Act (aktiebolagslagen, 2005:551).

Key Factors to Consider

- Business Activity: Active trading, regulated financial services, and passive asset-holding each point toward different structures, from AB to Ekonomisk Förening.

- Ownership and Management: A sole operator may find the Enskild Firma or single-shareholder Privat Aktiebolag sufficient, while multi-party ventures typically require a partnership deed or shareholder agreement.

- Tax Objectives: Your need to access Sweden's tax treaty network, or eligibility for the participation exemption on dividends, depends on operating through a Swedish tax-resident entity such as an aktiebolag.

- Liability Exposure: If personal asset protection is a priority, only structures with separate legal personality — the aktiebolag forms and the Ekonomisk Förening — provide a liability shield.

- Substance Capacity: If you cannot maintain genuine management and decision-making within Sweden, structures that trigger permanent establishment rules under Swedish tax law will create compliance obligations you may be unable to meet.

- Exit Strategy: The Swedish Companies Act (aktiebolagslagen 2005:551) governs conversion, merger, and voluntary liquidation procedures for aktiebolag, while partnerships dissolve under entirely different statutory rules.

Corporate Compliance Services in Sweden

Ongoing compliance obligations in Sweden vary by entity type and include annual reporting, audit thresholds, and Bolagsverket filing deadlines. Expanship assists companies in meeting these requirements across all Swedish business structures.

Conclusion

Sweden offers a structured range of legal forms, each suited to a distinct business profile. The Privat Aktiebolag (AB) remains the most commonly registered entity, favored by resident and non-resident founders alike for its limited liability and defined capital requirement. The Publikt Aktiebolag suits larger firms with external capital needs; the Ekonomisk Förening serves member-driven enterprises; Handelsbolag and Kommanditbolag carry personal liability exposure that limits their appeal to closely-held ventures; and the Enskild Firma fits individual traders operating at small scale.

Setting up a company in Sweden guide resources consistently point to Bolagsverket as the central registration authority, with the Swedish Tax Agency (Skatteverket) governing ongoing compliance obligations. Regulatory expectations around beneficial ownership disclosure and economic substance have tightened in recent years, aligning Swedish corporate law with broader EU directives. Your choice of structure will determine which obligations your business assumes from the date of registration onward.

How Expanship Can Assist You

Registering a business in Sweden involves more than submitting paperwork to the Swedish Companies Registration Office (Bolagsverket). As a corporate services company formation Sweden specialist, Expanship handles the full process — from selecting the right entity type among the aktiebolag structures, partnerships, and cooperative forms covered in this guide, to meeting Skatteverket's tax registration requirements.

From initial filing through to ongoing compliance, our Sweden business setup service covers:

- Document preparation and notarisation

- Registered agent and office address provision

- Government filings and Bolagsverket liaison

- Post-incorporation compliance management

- Corporate bank account introduction support

- Ongoing annual report and maintenance support

Get in touch with Expanship Sweden to discuss your specific setup requirements.

Frequently Asked Questions (FAQ)

The Privat Aktiebolag (AB) is the most frequently formed business entity, largely because it limits shareholder liability to contributed capital and requires a relatively modest share capital of SEK 25,000. Its governance framework under the Swedish Companies Act (Aktiebolagslagen 2005:551) is well understood by banks, counterparties, and public authorities alike.

A Privat Aktiebolag cannot offer shares to the public and has a minimum share capital of SEK 25,000, while a Publikt Aktiebolag must maintain at least SEK 500,000 and may list shares on a regulated market. Both structures are subject to Swedish corporate income tax at the same rate and carry equivalent compliance obligations, though the public variant faces additional disclosure and auditor requirements under Aktiebolagslagen.

Sweden maintains a public register through Bolagsverket, so director and shareholder information for most entities is accessible. An Enskild Firma discloses the owner's personal identity number publicly, whereas an AB separates personal identity from the trading entity to a degree. Nominee arrangements are not a standard feature of Swedish corporate practice.

A single individual can register an Enskild Firma or a Privat Aktiebolag. A Handelsbolag requires at least two partners, and a Kommanditbolag needs at least one general partner and one limited partner. An Ekonomisk Förening requires a minimum of three members under the Swedish Economic Associations Act (lag 2018:672).

Foreign nationals may form a Privat Aktiebolag or Publikt Aktiebolag without residency requirements, provided at least one board member is resident within the European Economic Area unless Bolagsverket grants an exemption. Non-residents may also register a branch (filial) under the Foreign Branch Offices Act. Operating as an Enskild Firma requires a Swedish personal identity number, which limits that structure to residents.

Conversion between entity types is permitted in limited circumstances. An Handelsbolag may be converted into an Aktiebolag through a regulated process under Aktiebolagslagen, transferring assets and liabilities to the new entity. Direct conversion between a sole proprietorship and a limited company is not available; a new entity must be formed and assets transferred separately.

Not all structures do. A Privat Aktiebolag, Publikt Aktiebolag, and Ekonomisk Förening each hold legal personality distinct from their members. A Handelsbolag and Kommanditbolag do not grant partners liability protection, as partners remain personally liable for the firm's obligations under the Partnership and Simple Partnership Act (lag 1980:1102).

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.