Key Takeaways

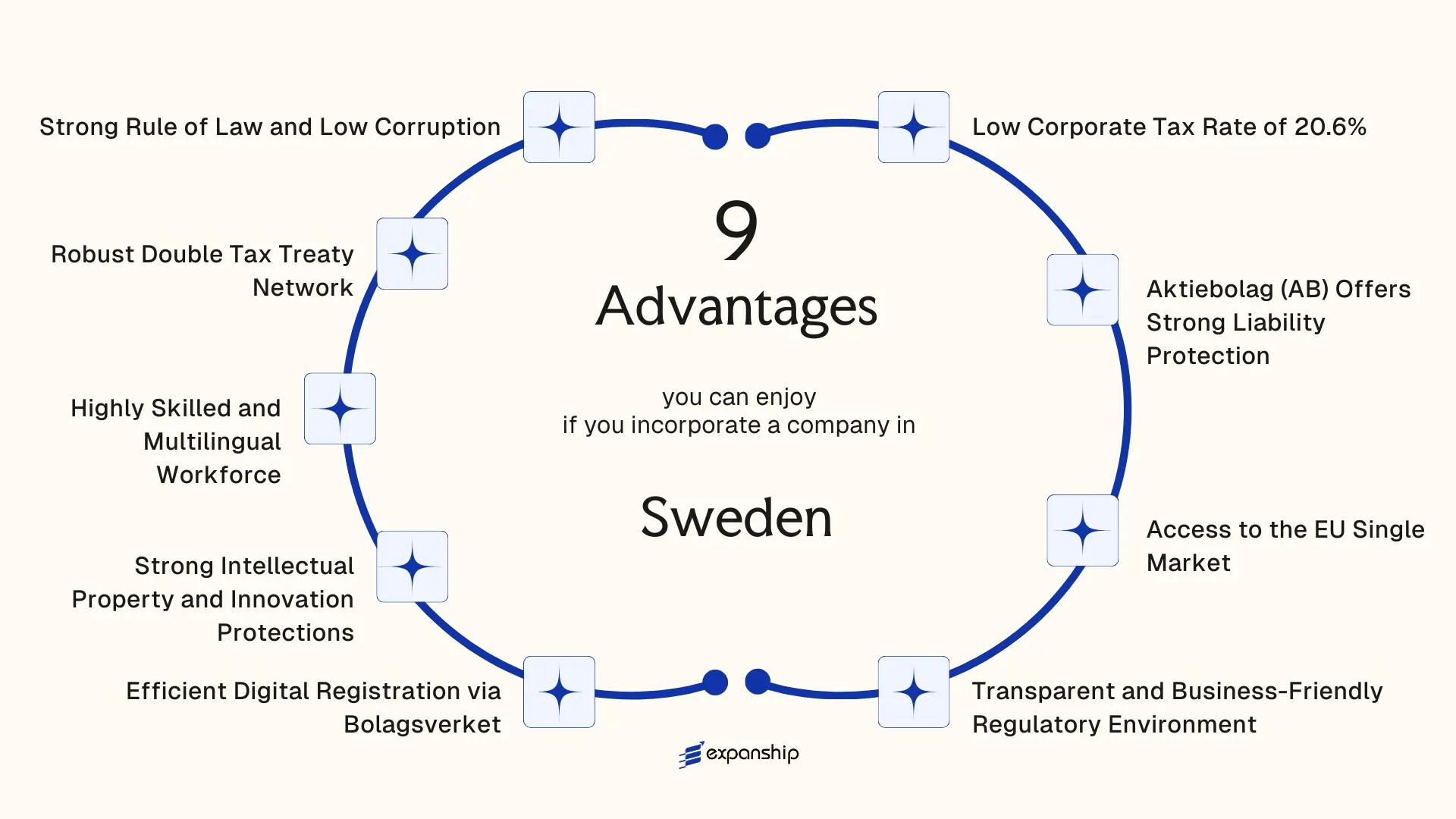

- Sweden's corporate income tax rate of 20.6% places it in the low-to-mid range among EU member states, giving foreign-owned entities a predictable and internationally competitive tax position without relying on zero-tax structures.

- The Aktiebolag (AB) structure establishes a clear legal separation between shareholder and company liability, which directly limits personal financial exposure for foreign founders operating in Swedish-registered businesses.

- Foreign investors benefit from Sweden's extensive double tax treaty network, which reduces withholding tax friction on cross-border income flows and strengthens the jurisdiction's utility within multinational corporate structures.

- Company registration through Bolagsverket, Sweden's statutory Companies Registration Office, is conducted digitally and imposes no general requirement for a local shareholder or resident director under standard formation rules, lowering the administrative threshold for foreign entrants.

Situated in northern Europe, Sweden is an independent sovereign nation and a full member of the European Union. Company registration is administered by Bolagsverket, the Swedish Companies Registration Office, and the most common legal vehicle used by foreign businesses is the Aktiebolag. The country operates a territorial-leaning tax system with a moderate corporate rate and an extensive treaty network, positioning it as a low-to-mid tax jurisdiction rather than a zero-tax one.

Foreign ownership of Swedish companies faces no general statutory restrictions, and the country maintains an open posture toward foreign direct investment across most sectors. Regulatory requirements apply equally to domestic and foreign-owned entities, with no mandatory local shareholder or director under standard formation rules.

The benefits of incorporating in Sweden are wide-ranging, spanning tax efficiency, market access, and institutional reliability. This article examines the key advantages of Swedish business registration to help you assess whether this jurisdiction fits your corporate structure.

Low Corporate Tax Rate of 20.6%

Sweden's corporate income tax rate sits at 20.6%, a figure that directly shapes the after-tax return on any profit your business generates within the country.

What the Rate Means in Practice

At 20.6%, the Swedish corporate tax rate falls below the OECD average of approximately 23%, meaning a greater share of operating profit stays within the company. This rate applies to the worldwide income of Swedish-resident entities, including an Aktiebolag (AB), calculated on taxable profit after permitted deductions under the Swedish Income Tax Act (Inkomstskattelagen).

Swedish tax law also allows deductions for interest expenses, depreciation, and certain group contributions between affiliated entities, which can reduce the effective tax burden below the statutory rate. The result is a tax base that, with proper structuring, can be meaningfully narrower than the headline figure suggests.

Conditions That Apply

Resident companies are taxed on net profit after deductions; branch offices of foreign firms are taxed only on Swedish-source income. Tax filings are administered through Skatteverket, the Swedish Tax Agency, which operates a digital self-assessment system that reduces administrative overhead.

A 20.6% rate combined with deductible group contributions means retained earnings in a Swedish AB compound faster than in many comparable EU jurisdictions.

Aktiebolag (AB) Offers Strong Liability Protection

The Aktiebolag structure provides aktiebolag liability protection benefits that are clearly defined under Swedish law, specifically the Aktiebolagslag (2005:551). Under this statute, shareholders are not personally liable for the company's debts or obligations. Your exposure as an investor is limited strictly to the capital you contribute.

This separation between personal assets and corporate liabilities is particularly significant for foreign investors operating from outside Sweden. If the business incurs debt or faces a legal claim, your personal finances remain insulated from the proceedings.

The minimum share capital requirement for a private AB is SEK 25,000. This threshold is not high by European standards, and the conditions attached to it are structured in a way that keeps entry accessible:

- Paid-in capital can be contributed in cash or qualifying assets, giving you flexibility in how you meet the requirement

- No ongoing capital maintenance rules require you to top up equity after incorporation

- The threshold applies per entity, not per shareholder, so co-founders are not each required to contribute the full amount independently

Swedish private limited company protection under the AB form is not contingent on local residency. Foreign nationals and foreign-owned entities can hold shares and directorship positions, subject to meeting standard registration requirements with Bolagsverket, the Swedish Companies Registration Office.

Incorporate a Company in Sweden

Set up your Swedish Aktiebolag with Expanship and benefit from clearly defined liability protections under Swedish corporate law.

Access to the EU Single Market

Membership in the European Union gives your Swedish-registered company direct access to a single market covering over 440 million consumers and 27 member states. That access is not incidental — it is structural. An Aktiebolag or filial registered in Sweden operates under EU law, meaning goods, services, capital, and personnel can move across member state borders without the customs duties, import quotas, or regulatory duplication that non-EU entities routinely face.

| Access Dimension | What It Covers | Governing Framework |

|---|---|---|

| Free Movement of Goods | Tariff-free trade across all EU member states | TFEU Articles 28-37 |

| Freedom to Provide Services | Cross-border service provision without local re-registration | TFEU Articles 56-62 |

| Free Movement of Capital | Unrestricted transfer of funds between member states | TFEU Articles 63-66 |

| Passporting Rights | Financial services authorization recognized EU-wide | Relevant EU Directives (e.g., MiFID II, AIFMD) |

Incorporating in Sweden for EU market access also means your business benefits from mutual recognition of product standards and CE marking compliance, which eliminates the need to certify products separately for each national market. For companies in regulated sectors such as financial services, the passporting mechanism under directives including MiFID II allows an authorized Swedish entity to serve clients across member states under a single license.

EU procurement rules additionally open public contracts across all member states to Swedish-registered entities, a channel that would otherwise require separate local presence in each country. This is not available to third-country firms on equivalent terms.

Transparent and Business-Friendly Regulatory Environment

Sweden's business-friendly regulatory environment advantages are rooted in a legal system that enforces predictability. Rules are applied consistently, published in accessible formats, and enforced by agencies with clearly defined mandates. For a foreign business owner, this means the obligations governing your company are knowable in advance, not subject to informal interpretation.

The Swedish Companies Act (Aktiebolagslagen, 2005:551) governs corporate conduct with a level of statutory clarity that reduces legal exposure. Regulatory decisions from bodies such as Finansinspektionen (the financial supervisory authority) and Skatteverket (the Swedish Tax Agency) are subject to formal appeal processes, giving your entity defined recourse if a ruling is disputed.

Transparency extends to financial reporting. Swedish firms must file annual accounts with Bolagsverket, which are then publicly available. This disclosure obligation creates a level commercial environment where your counterparties, suppliers, and clients can verify the standing of any business they engage with.

Keep these points in mind:

- Corporate filings and ownership records are publicly searchable through Bolagsverket

- Regulatory decisions by public authorities can be appealed through the administrative courts (förvaltningsdomstolarna)

- Annual reports must comply with the Annual Accounts Act (Årsredovisningslagen, 1995:1554)

- Certain regulated sectors, including financial services and insurance, require additional licensing from Finansinspektionen before commencing operations

Sweden publishes the full text of all government bills and regulatory proposals in a searchable online archive, meaning you can trace the legislative intent behind any commercial law before your legal counsel even files an opinion.

Efficient Digital Registration via Bolagsverket

Bolagsverket digital registration advantages are most visible in the speed and accessibility of the process. Foreign founders can submit incorporation documents entirely online through Bolagsverket's e-services portal, without requiring physical presence in the country. That single structural feature removes one of the most common friction points for international business owners.

Processing Times That Reduce Operational Delay

Standard digital applications for an Aktiebolag are typically processed within one to two weeks, compared to several weeks or months in many other European jurisdictions. For a foreign business owner, a shorter registration window means earlier access to a Swedish corporate bank account, VAT registration with Skatteverket, and the ability to begin contracting under a locally incorporated entity.

System Integration That Supports Ongoing Compliance

Once registered, your company's records are held centrally within Bolagsverket's public registry, which links directly with Skatteverket for tax registration and other Swedish public agencies. This interconnected structure means that updates to company details, such as changes to the board of directors or share capital, propagate across government systems without redundant filings to multiple bodies. The practical result is a lower administrative burden over the life of the firm, not just at formation.

Applications must meet specific documentation requirements under the Swedish Companies Act (Aktiebolagslagen), and submissions that are incomplete will extend processing timelines.

Plan Your Sweden Incorporation With Confidence

Speak with an Expanship adviser about structuring your Swedish company registration and meeting Bolagsverket requirements from day one.

Strong Intellectual Property and Innovation Protections

Sweden intellectual property protection benefits are grounded in a mature legal framework that gives foreign businesses genuine ownership security from the moment they begin operating.

- Patent protection is administered through the Swedish Intellectual Property Office (PRV), which handles national applications under the Patents Act (Patentlagen 1967:837). Registration through PRV also connects your business to the European Patent Convention system, extending protection across member states without requiring separate national filings in each.

- Sweden is a signatory to the TRIPS Agreement and the Berne Convention, meaning copyright in original works arises automatically upon creation. No registration is required for copyright to be enforceable, which reduces administrative overhead for companies holding software, creative, or technical assets.

- EU trademark and design rights apply directly to Swedish-registered entities. A single EU Intellectual Property Office (EUIPO) filing gives your firm protection across all 27 member states, making Sweden an efficient base for managing EU-wide IP portfolios.

- Sweden participates in the PCT (Patent Cooperation Treaty), allowing a single international patent application to preserve priority rights in over 150 countries. For technology and life sciences companies expanding globally, this substantially reduces the cost and complexity of multi-jurisdiction patent strategy.

Highly Skilled and Multilingual Workforce

Sweden's skilled multilingual workforce advantage is measurable: approximately 90% of the Swedish population speaks English, according to the EF English Proficiency Index, which has consistently ranked Sweden among the top three non-native English-speaking countries globally. For a foreign business owner, this eliminates the translation overhead and miscommunication costs that affect operations in many other EU jurisdictions.

Swedish higher education institutions, including KTH Royal Institute of Technology and Chalmers University of Technology, produce significant numbers of graduates in engineering, computer science, and life sciences annually. The country's strong tradition in these fields means your firm can recruit technical talent without relying solely on costly international transfers.

Proficiency extends beyond English. A substantial portion of the working population holds functional or professional command of German, French, and Nordic languages, which can reduce the cost of serving clients across multiple European markets from a single operating base.

Sweden ranks 2nd globally in the EF English Proficiency Index 2023, with an EF EPI score of 631 out of 800, placing it above the Western European average.

— EF Education First, EF EPI 2023

Robust Double Tax Treaty Network

Sweden's double tax treaty network benefits foreign businesses through one of Europe's most extensive bilateral frameworks. The country has concluded tax treaties with over 80 jurisdictions, covering major economies across North America, Asia, Europe, and the Middle East.

Under these agreements, withholding tax rates on dividends, interest, and royalties paid across borders are reduced or eliminated entirely. For a foreign investor, this directly lowers the tax cost of repatriating profits or receiving payments from a Swedish entity. The specific rates vary by treaty, but many agreements reduce dividend withholding to 0-15%, depending on ownership thresholds.

Sweden is also a party to the EU Parent-Subsidiary Directive and the Interest and Royalties Directive, which further reduce intra-EU withholding obligations. This means businesses structured within the EU group framework often face minimal or zero withholding on qualifying payments, independent of bilateral treaty terms.

Treaty benefits generally apply when a company meets residency and beneficial ownership conditions set out in the relevant agreement. Swedish treaties increasingly incorporate OECD Base Erosion and Profit Shifting (BEPS) minimum standards, including principal purpose tests that assess whether a structure has genuine commercial substance.

Treaty benefits are subject to anti-avoidance provisions under BEPS-aligned principal purpose tests; structures lacking genuine commercial substance in Sweden may be denied treaty protection.

Strong Rule of Law and Low Corruption

Sweden rule of law business advantages are grounded in institutional architecture, not reputation alone. The country consistently ranks among the top three globally on Transparency International's Corruption Perceptions Index, scoring 82 out of 100 in 2023. For a foreign business owner, this means contracts are enforced as written, public procurement decisions are auditable, and regulatory outcomes are not subject to informal influence.

Predictable Legal Enforcement

Swedish courts operate under a codified framework that includes the Code of Judicial Procedure (Rättegångsbalken), and commercial disputes are handled through an independent judiciary with no political appointment process for sitting judges. Arbitration is also well-established, with the Stockholm Chamber of Commerce (SCC) Arbitration Institute recognized as a neutral forum for international commercial disputes. Your business can structure agreements knowing that enforcement mechanisms are accessible and consistent.

Regulatory Transparency

Government agencies in Sweden are subject to the principle of public access to official documents, established under the Freedom of the Press Act (Tryckfrihetsförordningen) of 1766, one of the oldest such laws in the world. Regulatory decisions affecting your company can be reviewed, appealed, and scrutinized through formal administrative processes under the Administrative Procedure Act (Förvaltningslagen).

What This Means for Foreign Investors

Low corruption benefits for investors extend beyond ethics into operational certainty:

- Licensing decisions follow published criteria, reducing unpredictability in market entry

- Public contracts are subject to the Public Procurement Act (Lagen om offentlig upphandling)

- Financial reporting standards are enforced consistently across domestic and foreign-owned entities

Why Sweden Stands Out Among European Business Destinations

Foreign businesses evaluating European incorporation options typically consider jurisdictions with comparable market access, governance standards, and tax positioning. The most relevant comparators for Sweden are the Netherlands, Denmark, and Ireland — each targets a similar profile of internationally oriented companies and competes on overlapping parameters such as treaty networks, regulatory transparency, and EU market access.

Where Sweden distinguishes itself is in the combination of factors that individually exist elsewhere but rarely converge. Ireland's corporate tax rate is lower at 12.5%, and the Netherlands offers its own holding structures, yet neither scores as consistently across governance indicators, IP protection frameworks, and digital public administration as Sweden does. Corruption Perceptions Index data from Transparency International consistently places Sweden among the top five globally, a standing that directly affects contract enforceability and counterparty confidence for foreign investors.

| Parameter | Sweden | Netherlands | Denmark | Ireland |

|---|---|---|---|---|

| Corporate Tax Rate | 20.6% | 19–25.8% (tiered) | 22% | 12.5% (trading) |

| EU Single Market Access | Yes | Yes | Yes | Yes |

| Corruption Perceptions Rank (2023) | Top 5 globally | Top 10 | Top 2 | Top 15 |

| Digital Company Registration | Yes (Bolagsverket) | Yes (KVK) | Yes (Erhvervsstyrelsen) | Yes (CRO) |

| Double Tax Treaties | 80+ | 100+ | 75+ | 75+ |

| IP Box Regime | No formal box; R&D deductions available | Innovation Box (9%) | No IP box | 6.25% Knowledge Development Box |

| Minimum Share Capital (main private entity) | SEK 25,000 (AB) | EUR 0.01 (BV) | DKK 40,000 (ApS) | EUR 1 (LTD) |

Compliance Services for Companies in Sweden

Maintain good standing with Swedish regulatory requirements, including annual filings with Bolagsverket, tax registrations, and ongoing statutory obligations.

Conclusion

Sweden combines a predictable tax environment, direct access to EU markets, and a legal framework that has consistently ranked among the most transparent in the world. The benefits of incorporating in Sweden are grounded in structural features that serve foreign business owners directly: a corporate income tax rate of 20.6%, an Aktiebolag structure that draws a firm line between personal and company liability, and a digital registration process through Bolagsverket that reduces the administrative burden of entry.

Not every jurisdiction suits every business model. An entity dependent on physical distribution may weigh EU market access most heavily, while a firm built around proprietary technology may find the intellectual property protections and innovation incentive schemes more relevant. The advantages of Swedish business registration apply differently depending on your industry, ownership structure, and long-term operating plans.

What remains consistent is the underlying reliability of the system. Sweden's double tax treaty network, its standing under EU law, and the low-corruption regulatory environment mean that a business registered here operates with a degree of legal certainty that is difficult to replicate in many other markets. For foreign investors assessing where to establish a European presence, that certainty has measurable operational value. The next step is matching these structural features to your specific corporate objectives.

Start Your Swedish Company Formation With Expanship Today

Expanship assists foreign founders with Sweden company formation, from Aktiebolag registration with Bolagsverket through to ongoing compliance under the Swedish Companies Act (Aktiebolagslagen). The firm's scope covers the full formation lifecycle, including the specific processes this blog has outlined: share capital structuring, VAT and employer registration with Skatteverket, and maintaining the records requirements that Swedish law imposes on all registered entities.

For each engagement, Expanship coordinates the practical tasks that foreign principals typically find time-consuming or procedurally unfamiliar:

- Preparation and legalization of formation documents, including articles of association and shareholder resolutions

- Registered agent and registered office provision to satisfy Swedish domicile requirements

- Filing and liaison with Bolagsverket for company registration and Skatteverket for tax enrollment

- Post-incorporation compliance management, including annual report filing obligations under the Swedish Annual Accounts Act (Årsredovisningslagen)

- Banking introduction assistance for corporate account establishment with Swedish financial institutions

Your business can direct specific questions about entity formation, applicable timelines, or compliance obligations to the team directly. Contact Expanship Sweden to discuss your requirements.

Frequently Asked Questions (FAQ)

The minimum share capital for a private Aktiebolag is SEK 25,000, a figure established under the Swedish Companies Act (Aktiebolagslagen). This amount must be fully paid before the company is formally registered with Bolagsverket. Public limited companies (Publikt Aktiebolag) carry a higher threshold of SEK 500,000.

A foreign-owned Aktiebolag is taxed as a Swedish resident entity, meaning the 20.6% corporate income tax rate applies to profits generated by that subsidiary in the same way it applies to domestically owned firms. The rate is flat with no graduated tiers based on profit size. Applicable deductions, including interest expenses subject to the limitation rules introduced in the 2019 tax reform, can affect the effective rate.

Sweden's tax treaties frequently reduce or eliminate withholding tax on dividends paid to qualifying foreign parent companies, though the exact rate depends on the specific bilateral treaty in force. Within the EU, the Parent-Subsidiary Directive may eliminate withholding tax entirely where the parent holds at least 10% of the subsidiary's share capital. Outside the EU, treaty rates typically range between 0% and 15%.

Under the Aktiebolagslagen, directors who knowingly continue trading after the company's equity falls below half of the registered share capital without following the mandatory capital deficiency procedure can become personally liable for debts incurred during that period. The procedure requires the board to draw up a special balance sheet and, if the deficit is not rectified, initiate liquidation. Failure to follow these steps removes the liability shield that the Aktiebolag structure would otherwise provide.

Intellectual property registered through Swedish bodies, such as the Swedish Intellectual Property Office (PRV), can work in conjunction with EU-wide frameworks including the European Union Trade Mark (EUTM) system and the European Patent Convention. A patent or trademark granted at the EU level automatically covers Sweden as a member state without requiring a separate national filing. This means a company incorporated in Sweden can use a single EU registration to protect its assets across all member states simultaneously.

Sweden's Financial Supervisory Authority, Finansinspektionen, supervises financial services firms including fintech entities operating under EU regulatory frameworks such as PSD2 and MiFID II. The authority has established dedicated licensing tracks for payment institutions and e-money issuers. Sweden's alignment with EU digital regulations, combined with PRV's IP protections, makes the regulatory structure applicable to technology-focused businesses, though sector-specific licensing requirements must be assessed individually.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.