Key Takeaways

- All companies incorporated in Réunion must register through the Centre de Formalités des Entreprises and be recorded in the Registre du Commerce et des Sociétés at the local Greffe du Tribunal de Commerce, as the jurisdiction operates under the French Code de commerce rather than a separate territorial framework.

- Foreign investors are required to disclose beneficial ownership information in compliance with French anti-money laundering legislation, making UBO registration a mandatory step rather than an optional disclosure.

- A physical registered office address within Réunion is an obligatory condition of incorporation, not a procedural formality, and failure to maintain one creates ongoing compliance exposure under French commercial law.

- KYC documentation submitted during entity formation must meet the same standards applied across metropolitan France, meaning foreign directors and shareholders cannot expect a reduced or simplified verification process based on the overseas department status of the jurisdiction.

Réunion operates as an overseas department of France, which means entity formation is governed by French commercial law rather than a separate territorial code. The primary legislative framework is the Code de commerce, and company registration is administered through the Centre de Formalités des Entreprises (CFE) and recorded in the Registre du Commerce et des Sociétés (RCS) held at the local Greffe du Tribunal de Commerce.

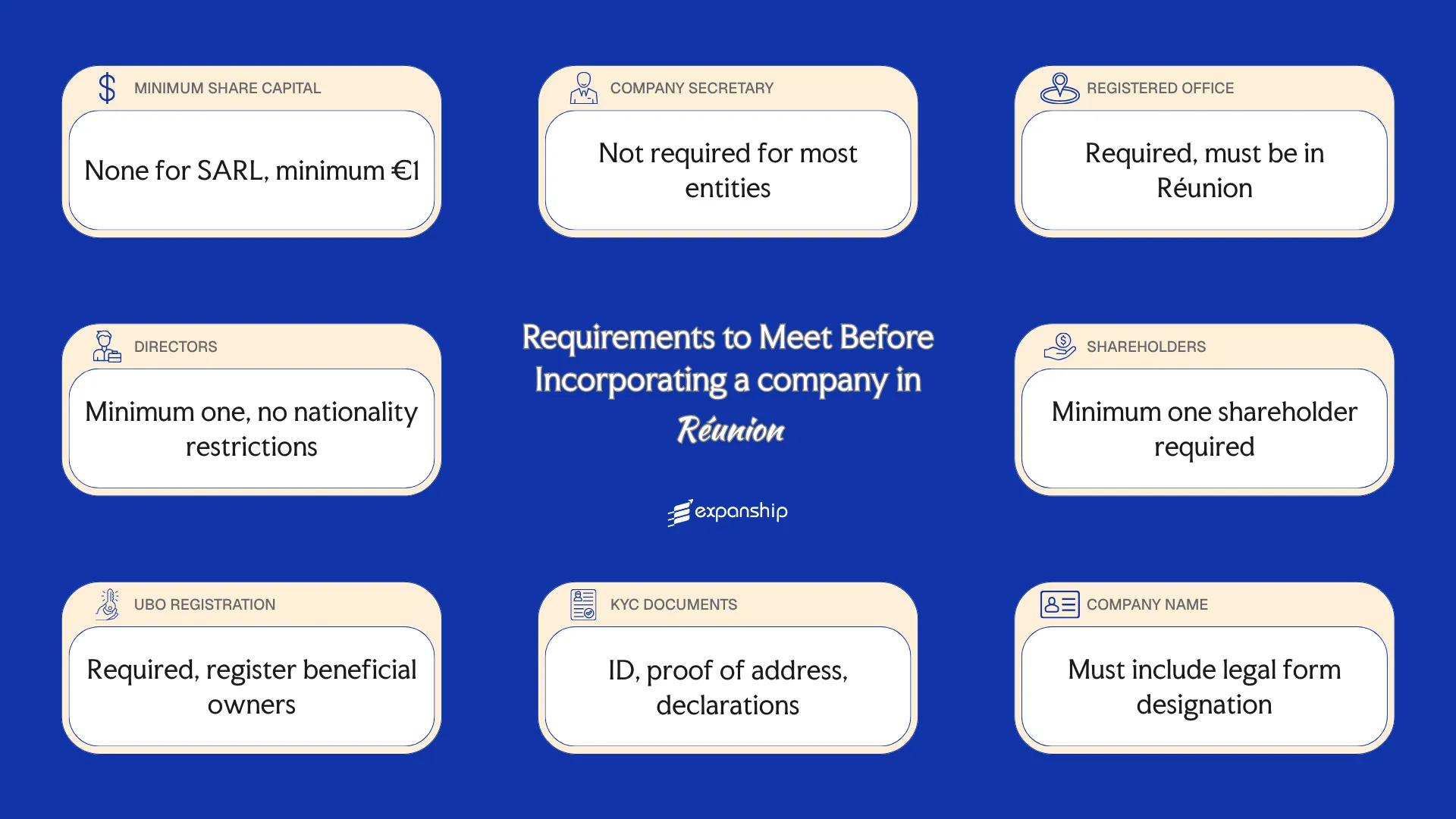

Incorporation requirements in Réunion span multiple categories, from capital thresholds and directorship rules to disclosure obligations and documentation standards.

Failure to satisfy these requirements results in rejection of the registration application or, where a business begins operating without proper registration, exposure to civil and criminal liability under French law. Requirements differ depending on the legal form you choose, your sector of activity, and whether your business involves foreign capital.

This article is most relevant to foreign investors and non-resident business owners seeking to establish a legal presence under French corporate law through a Réunion-registered entity.

Minimum Share Capital Requirements in Réunion

As an overseas department of France, Réunion minimum share capital requirements follow metropolitan French company law, specifically the rules under the Code de commerce. The Greffe du Tribunal de Commerce handles registration and verifies capital declarations at the point of incorporation.

For a SARL, there is no statutory minimum share capital under current French law, though a nominal amount of at least €1 is required in practice to constitute a valid share structure. An SAS likewise carries no minimum capital threshold, giving founders flexibility in setting their authorized capital amount.

| Parameter | Detail |

|---|---|

| Minimum Authorized Share Capital | No statutory minimum (€1 in practice) |

| Maximum Authorized Share Capital | No statutory maximum |

| Minimum Paid-Up Capital | No statutory minimum |

| Paid-Up Requirement at Incorporation | At least 20% of cash contributions must be deposited at incorporation for a SARL; remainder within 5 years |

| Accepted Currency | Euro (EUR) |

| Accepted Forms of Contribution | Cash, tangible assets, intangible assets |

| Timeframe to Deposit Capital | Minimum 20% deposited prior to registration with the Greffe |

Share capital funds must be deposited into a blocked bank account before the entity is registered. The Greffe requires proof of this deposit as part of the incorporation dossier; registration cannot proceed without it.

Company Secretary Requirements in Réunion

As an overseas département of France, Réunion follows French commercial law, which does not impose a mandatory company secretary requirement equivalent to those found in common law jurisdictions. Under the French corporate framework, the company secretary requirements in Réunion are governed by the same statutes that apply across metropolitan France, with no separate local corporate secretary regime.

Certain legal forms do assign administrative and compliance functions to specific officers. For a Société à Responsabilité Limitée (SARL), a gérant handles statutory obligations, while a Société Anonyme (SA) may designate a directeur général délégué to support governance functions.

Qualification criteria for those serving in an administrative officer capacity generally reflect the following conditions:

- No prior criminal convictions relating to business fraud or financial misconduct under French law

- Individuals must have full legal capacity under French civil law

- Corporate entities may serve in officer roles for certain legal forms, subject to French company law

- No mandatory residency requirement exists under French law for most officer positions

- No licensing or professional certification is required to serve in a general administrative officer capacity

Company Incorporation in Réunion

Set up your business entity in Réunion under the applicable French commercial framework, with guidance on legal form selection and statutory filings.

Registered Office Requirements in Réunion

Registered office requirements in Réunion follow French corporate law, as the territory is an overseas department (département d'outre-mer) of France, meaning the siège social must be established at a real, locatable address within the territory before registration with the Greffe du Tribunal de Commerce.

- A physical address is required; a PO box alone does not satisfy the siège social obligation.

- The address must be located within Réunion; a metropolitan France address does not fulfil local registration requirements.

- Virtual office addresses are generally permissible provided the provider can demonstrate a genuine physical premises and mail-handling capacity at that location.

- Proof of occupancy is required at incorporation, typically a lease agreement, property title, or a domiciliation contract with a certified domiciliation company.

- The registered address is publicly listed in the Registre du Commerce et des Sociétés (RCS) and is accessible through official directories.

- Any change of registered address must be formally declared to the Greffe and recorded in the RCS; operating with an outdated address can expose the entity to administrative penalties and affect the validity of legal notices served on the company.

- Failure to maintain a compliant address may result in the company being struck from the RCS or render official correspondence legally undeliverable.

Director Requirements in Réunion

As an overseas department of France, director requirements in Réunion follow French corporate law, principally the Code de commerce. Upon appointment, directors assume statutory duties including acting in the company's corporate interest (intérêt social), exercising loyalty toward shareholders, and bearing personal civil or criminal liability for management faults (faute de gestion).

| Parameter | Detail |

|---|---|

| Minimum Number of Directors | One gérant is required for a SARL; an SAS requires at least one président. |

| Maximum Number of Directors | No statutory maximum applies for a SARL gérant structure; SAS articles govern this internally. |

| Local/Resident Director Required | No statutory residency requirement exists under French law. |

| Nationality Restrictions | Non-EU nationals must hold a valid autorisation de travail or titre de séjour permitting self-employed commercial activity. |

| Minimum Age Requirement | Directors must be at least 18 years of age and legally capable (capacité juridique). |

| Corporate Directors Permitted | A legal entity may serve as gérant of a SARL, provided a permanent representative (représentant permanent) is designated. |

| Director Must Be a Shareholder | No statutory requirement obliges a gérant or président to hold shares. |

| Publicly Listed on Registry | Director identity is filed with the Greffe du Tribunal de Commerce and publicly visible via the Registre du Commerce et des Sociétés (RCS). |

| Disqualification Conditions | A director may be disqualified under Articles L. 653-1 to L. 653-11 of the Code de commerce following insolvency proceedings, fraud, or judicial prohibition. |

Despite Réunion being an overseas French department, a foreign national with no connection to France or the EU can legally serve as sole gérant of a Réunion-registered SARL, provided they obtain the appropriate commercial residence authorisation before taking up the role.

Shareholder Requirements in Réunion

Shareholder requirements in Réunion follow French commercial law, as the territory operates under the same legal framework as metropolitan France. A Société à Responsabilité Limitée (SARL) requires between one and one hundred shareholders, with a single-shareholder variant known as the EURL permitted for sole operators.

Nationality and Residency Restrictions

No nationality or residency requirements apply to shareholders. Foreign individuals and entities may hold full ownership without a local partner, subject to standard French regulatory compliance.

Corporate Shareholders

Corporate entities are permitted to act as shareholders in both SARLs and Sociétés par Actions Simplifiées (SAS). No specific conditions restrict the nationality of the corporate shareholder, provided the entity can furnish the required identification documentation.

Shareholder Liability

In a SARL or SAS, your liability is limited to your capital contribution. Extended liability may arise in cases of fraud, undercapitalisation, or a court piercing the corporate veil under French insolvency proceedings.

Register of Shareholders

A register of shareholders, known as the registre des associés, must be maintained at the company's registered office. It is not publicly accessible, but must be updated following any transfer of shares or change in ownership structure.

Shareholder Structuring Support for Your Réunion Entity

Get guidance on structuring shareholder arrangements that meet French commercial law requirements applicable in Réunion, from initial setup through ongoing compliance.

UBO / Beneficial Ownership Disclosure Requirements in Réunion

Beneficial ownership disclosure in Réunion follows French metropolitan law, as the territory is an integral part of France and subject to the same legal framework, including the obligations established under the Code de commerce and transposing the EU's Anti-Money Laundering Directives. A beneficial owner (bénéficiaire effectif) is generally defined as any natural person holding, directly or indirectly, more than 25% of the capital or voting rights of a legal entity.

- Identify all natural persons meeting the ownership or control threshold at the time of incorporation.

- File a declaration of beneficial owners (déclaration des bénéficiaires effectifs) with the greffe du tribunal de commerce as part of the registration process.

- Submit updates to the register within 30 days of any change in beneficial ownership.

- Retain supporting documentation to substantiate the declared information.

| Parameter | Detail |

|---|---|

| Ownership Threshold for UBO Status | More than 25% of capital or voting rights |

| Filing Authority | Greffe du tribunal de commerce |

| Disclosure Deadline at Incorporation | At the time of registration |

| Publicly Accessible Register | Accessible to competent authorities and persons with a legitimate interest |

| Penalties for Non-Disclosure | Criminal and civil penalties under French law, including fines |

| Ongoing Update Obligation | Within 30 days of any change |

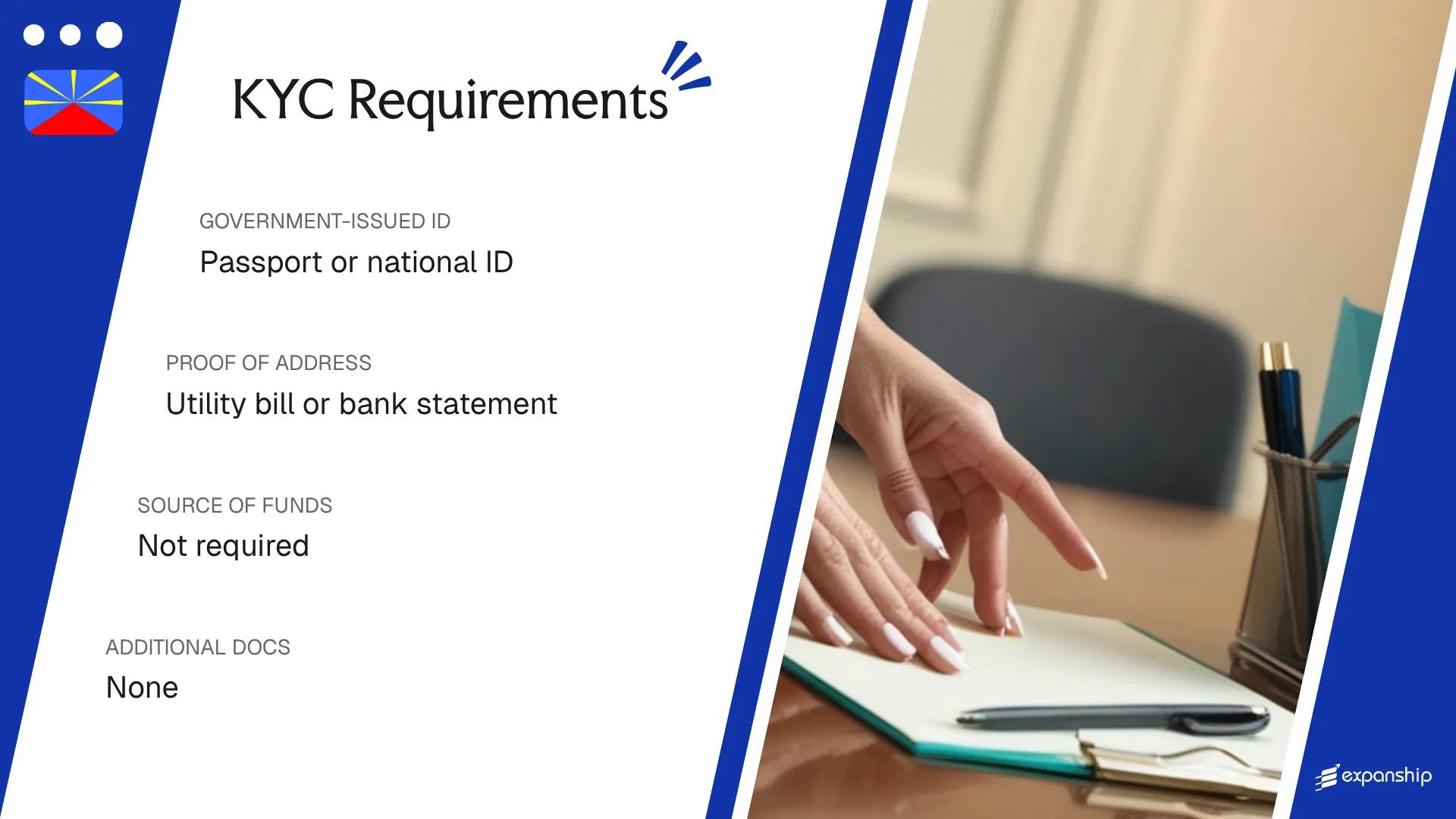

KYC / Document Requirements in Réunion

As an overseas department of France, Réunion applies French AML legislation directly, meaning KYC requirements Réunion company registration processes must satisfy the obligations set out under France's transposition of the EU's Anti-Money Laundering Directives, overseen by Tracfin, the national financial intelligence unit.

Individual / Personal Documents

- Valid government-issued photo identity document (passport or national identity card) for each individual director, shareholder, or beneficial owner

- Proof of residential address dated within three months, such as a utility bill or official bank statement

- Signed and dated specimen signature

- Tax identification number where the individual holds one in their country of residence

Corporate Documents

- Certified copy of the certificate of incorporation or equivalent constitutional document for the corporate entity

- Extract from the relevant commercial register, dated within three months

- Register of directors and, where applicable, register of shareholders

- Proof of the corporate entity's registered office address

Source of Funds Documentation

- Recent bank statements covering a minimum of three months prior to incorporation

- Audited financial accounts or equivalent where the entity has been trading

- Written declaration explaining the origin of capital being introduced

Notarisation and Apostille Requirements

- Foreign documents must be apostilled under the 1961 Hague Convention if issued outside France

- Official translations into French are required for all documents not originally issued in French

- Notarisation by a French notaire may be required for certain constitutional documents

Incomplete or untranslated foreign corporate documents are the most frequent cause of registration delays at the Greffe du Tribunal de Commerce.

Company Name Requirements in Réunion

Proposed company name requirements in Réunion are assessed during the incorporation process through the Centre de Formalités des Entreprises (CFE), which verifies that the chosen name does not conflict with an existing registered business. Availability is checked against the Registre du Commerce et des Sociétés (RCS).

Your chosen dénomination sociale must be written in French and accompanied by the appropriate legal suffix reflecting the entity type, such as SARL or SAS. No statutory minimum or maximum character length is prescribed under general French commercial law as applied in Réunion.

Certain words are prohibited or require prior authorisation. Terms implying a connection to public authorities, regulated professions, or financial institutions fall into the restricted category and cannot be used without approval from the relevant supervisory body.

Name reservation is available through the RCS prior to formal incorporation. The reserved name is held for a limited period, typically a few months, and the reservation is submitted alongside or in advance of the full registration dossier.

Compliance Services for Companies in Réunion

Expanship supports businesses registered in Réunion with ongoing compliance obligations, including RCS filings, statutory record maintenance, and regulatory reporting requirements.

Conclusion

Réunion operates under French commercial law, meaning incorporation requirements in Réunion mirror the metropolitan French framework administered through the Centre de Formalités des Entreprises. Among the requirements covered, beneficial ownership disclosure under French anti-money laundering legislation and the physical registered office obligation carry particular weight for foreign investors. KYC documentation standards are also applied consistently with French regulatory norms. Once these requirements are understood, a foreign investor's practical next step is identifying a local service provider capable of managing filings with the relevant registries.

Expanship's Corporate Services for Réunion Expansion

Réunion company formation services sit within a French legal framework, meaning your registration process runs through the Centre de Formalités des Entreprises and follows metropolitan French corporate law applied locally. Expanship works with you to manage the documentation, filing sequences, and administrative coordination that this system demands, reducing the operational burden of working across a jurisdiction where procedures mirror mainland France but local context still matters.

Beyond registration, Expanship supports the full scope of your incorporation and maintenance needs:

- We prepare your company documentation and handle registration through the relevant formation authorities.

- Your entity receives a compliant registered office address and appointed registered agent in Réunion.

- We liaise directly with government bodies and regulatory offices on your behalf throughout the filing process.

- Post-incorporation obligations, from annual filings to statutory updates, are managed on an ongoing basis.

- Where required, we facilitate introductions to local banking institutions to support your account opening process.

- Tax registration and coordination with local fiscal authorities are handled as part of your setup.

Reach out to Expanship Réunion to discuss your incorporation requirements.

Frequently Asked Questions (FAQ)

A SASU can be incorporated with a minimum share capital of €1, though only half of any cash contributions above €1 must be deposited at the time of registration, with the remainder payable within five years. The funds must be held in a blocked bank account until the Kbis extract is issued by the Greffe du Tribunal de Commerce confirming registration. Choosing a nominal capital figure well below operational needs can affect creditor confidence and access to financing.

Foreign nationals from outside the European Union who wish to act as a director in Réunion must hold a valid titre de séjour autorisant l'exercice d'une activité commerciale before taking up the role. EU citizens face no such restriction, as Réunion operates under French law and EU freedom of establishment applies. Failure to hold the correct residency authorisation before assuming directorship is a criminal offence under French commercial law.

Any legal entity registered in Réunion must declare its ultimate beneficial owners to the Registre des Bénéficiaires Effectifs, which is maintained by the Greffe du Tribunal de Commerce. The declaration must identify any individual holding more than 25% of shares or voting rights, or who otherwise exercises effective control over the entity. This obligation is imposed by French Ordinance No. 2016-1635, which transposed the EU's Fourth Anti-Money Laundering Directive into domestic law.

Failure to file or maintain accurate beneficial ownership information with the Registre des Bénéficiaires Effectifs exposes both the legal entity and its directors to criminal sanctions under French law, including fines of up to €7,500 for individuals and €37,500 for legal persons. Directors may also face a prohibition from managing a company. The obligation to update the register arises within 30 days of any change in beneficial ownership.

French company law does not impose a mandatory company secretary requirement for a SARL or SAS incorporated in Réunion. Statutory filings, minute-keeping, and compliance obligations are typically managed by the gérant in a SARL or by a designated officer in an SAS, as defined in the company's statuts. Larger entities or those with complex shareholding structures often engage an external service provider to manage these obligations, though this is a commercial decision rather than a legal requirement.

Yes, this structure is specifically accommodated by the SASU, the single-shareholder simplified joint-stock company form available under French law as applied in Réunion. The sole shareholder assumes the functions of président and holds all shares, with decisions recorded in the register of sole shareholder decisions rather than through formal general meetings. The same individual must still comply with all registration, KYC, and beneficial ownership disclosure obligations.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.