Key Takeaways

- Businesses incorporated in Réunion operate under the LODEOM regime and Loi Girardin provisions of the Code général des impôts, which provide tax incentives specifically calibrated for overseas economic development rather than standard metropolitan French rates.

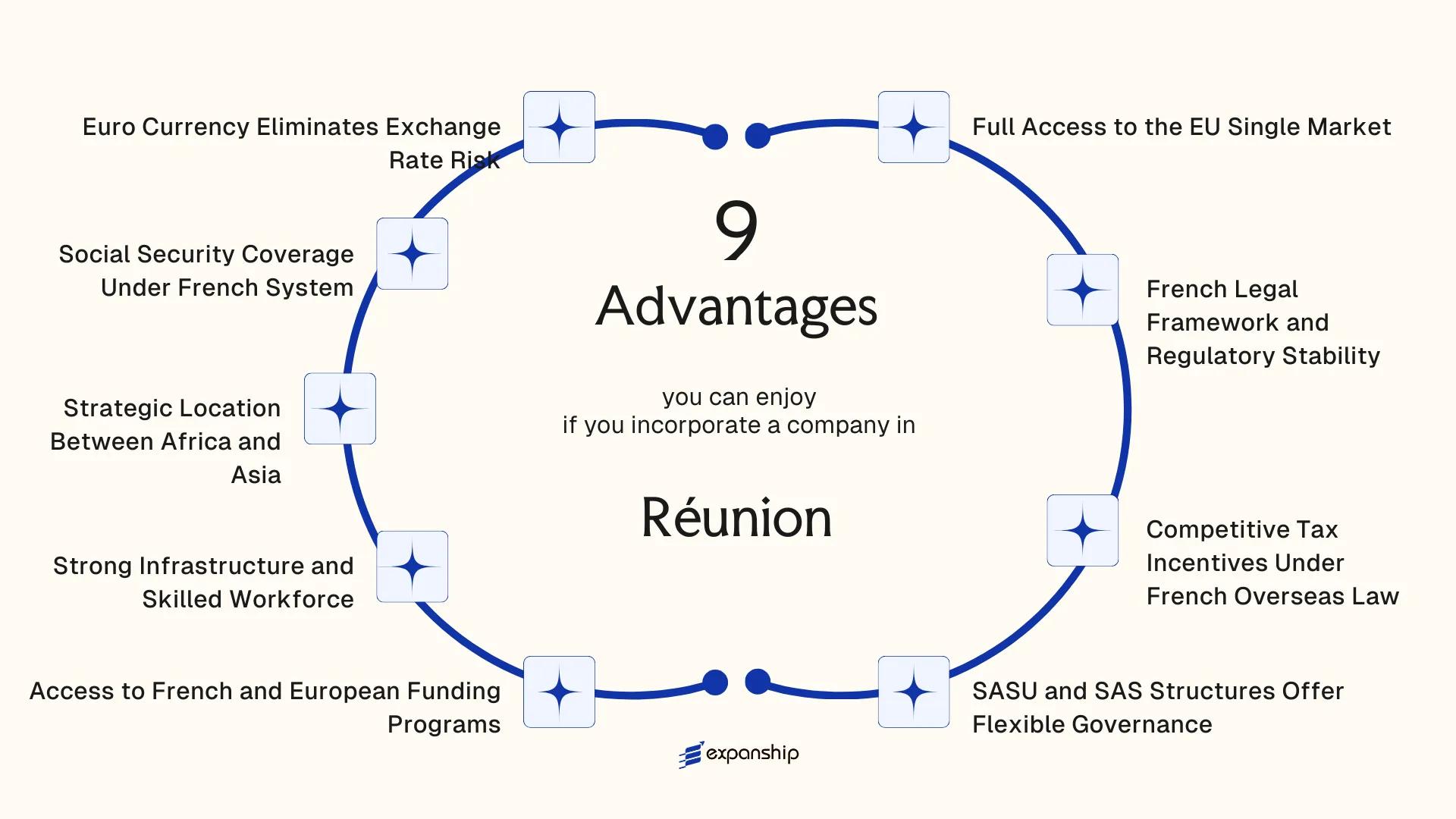

- Because Réunion holds outermost region status within the European Union, companies registered there gain full access to the EU single market under French constitutional law — an advantage unavailable through offshore or autonomous territory registrations in the same geographic zone.

- The SAS and SASU corporate structures available through the Greffe du Tribunal de Commerce de Saint-Denis allow foreign investors to establish governance arrangements with meaningful flexibility while remaining within a stable, enforceable French legal framework.

- Réunion's position approximately 800 kilometres east of Madagascar places incorporated entities within practical distribution range of both African and Asian markets, offering a geographic advantage that a purely European registration cannot replicate.

Réunion is a French overseas department (département d'outre-mer) and an outermost region of the European Union, situated in the Indian Ocean roughly 800 kilometres east of Madagascar. That political status places it under French constitutional law and full EU legal frameworks, distinguishing it from offshore or autonomous territories with separate regulatory regimes.

Company registration is administered by the Greffe du Tribunal de Commerce de Saint-Denis, which processes filings and maintains the official commercial register. Foreign investors most commonly establish a SAS for operations in the territory. From a tax standpoint, businesses here fall under the French general tax code as modified by specific overseas provisions under the LODEOM regime, creating a territorial posture that differs from standard metropolitan French rates.

Foreign ownership faces no sector-wide restrictions at the ownership level, and the French regulatory environment treats non-resident investors on comparable terms to domestic ones in most commercial activities. This article examines the principal advantages that the benefits of incorporating in Réunion present to internationally operating businesses and investors.

Full Access to the EU Single Market

As an outermost region (OMR) of the European Union under Article 349 of the Treaty on the Functioning of the European Union (TFEU), a company registered here carries the same EU market standing as one incorporated in Paris or Berlin. Réunion EU single market access benefits are therefore substantive, not symbolic.

Passport Rights Across 27 Member States

A business entity incorporated in Réunion operates under French commercial law and holds full legal standing within the EU's single market framework. This means your goods, services, capital, and personnel can move freely across all 27 member states without the customs friction, tariff barriers, or regulatory duplication that non-EU entities face when exporting into Europe.

Treaty-Backed Trade Agreements

The EU's network of free trade agreements, including CETA with Canada and EPA arrangements with various African and Pacific states, extends automatically to firms established in French overseas departments. Your company gains access to preferential trade terms negotiated at the EU level, without requiring separate bilateral arrangements.

EU market access through a Réunion company is legally equivalent to incorporation in metropolitan France, without additional licensing, re-registration, or regulatory approval at the EU border.

French Legal Framework and Regulatory Stability

Businesses incorporated in Réunion operate under French law, which means the entire body of the Code de commerce applies directly. This is not an adapted or simplified version of French commercial law — it is the same framework governing mainland France. For foreign investors, that distinction matters: your entity has the same legal standing and protections as any company registered in Paris or Lyon.

French commercial law advantages in Réunion extend to contract enforcement, creditor rights, and corporate governance standards. France ranked consistently among OECD countries for judicial efficiency in commercial disputes, and because Réunion falls under the jurisdiction of French courts, rulings are enforceable within the full French and EU legal order.

Regulatory stability for foreign investors comes from a source that cannot shift with local politics. Since Réunion is a French overseas department (département d'outre-mer), no separate regional legislature can alter the core legal framework.

This structural arrangement produces several concrete advantages for your business:

- French commercial courts (tribunaux de commerce) handle disputes under codified, well-documented procedures

- Intellectual property registered in France covers Réunion automatically under the same registration

- Contract law under the Code civil provides predictable, tested standards for commercial agreements

- Regulatory oversight bodies such as the AMF and ACPR operate with the same authority as on the mainland

Company Incorporation in Réunion

Incorporate your company in Réunion under the French legal framework with full access to EU regulatory standards.

Competitive Tax Incentives Under French Overseas Law

Réunion overseas tax incentives for businesses are grounded in two major legislative frameworks: the Loi Girardin (Law No. 2003-660) and the LODEOM (Law No. 2009-594 for the economic development of overseas territories). Together, these laws create a fiscal environment that differs substantially from metropolitan France.

Under Loi Girardin, businesses investing in productive equipment in qualifying sectors can benefit from tax reductions applied against French income tax, with rates that have historically exceeded the value of the investment itself. For corporate entities operating locally, LODEOM introduced targeted social contribution exemptions on wages, which directly reduces payroll costs, a material advantage when hiring local staff at competitive salary levels.

| Instrument | Type of Benefit | Applies To |

|---|---|---|

| Loi Girardin (productive) | Tax reduction on qualifying investment | Equipment, productive assets |

| LODEOM social exemptions | Reduced employer social contributions | Local payroll costs |

| Zone Franche d'Activité (ZFA) | Corporate tax reduction up to 50% | SMEs in eligible sectors |

The Zone Franche d'Activité scheme, established under LODEOM, allows qualifying small and medium enterprises to reduce their taxable profits by up to 50%, provided the entity operates in sectors such as agri-food, tourism, or technology. This reduction applies at the local level without forfeiting access to the broader French tax treaty network, which currently covers over 120 countries. Eligibility conditions apply, including thresholds on headcount and sector classification.

SASU and SAS Structures Offer Flexible Governance

Both the SAS (Société par Actions Simplifiée) and its single-shareholder variant, the SASU (Société par Actions Simplifiée Unipersonnelle), are governed under French company law — specifically the Code de commerce — which applies in full to Réunion as an integral part of France. The SASU SAS governance advantages in Réunion are rooted in the degree of contractual freedom these structures permit, an attribute with direct practical value for foreign investors.

Under French law, the SAS has no mandatory board structure. Shareholders define governance rules in the statuts (articles of association), covering voting thresholds, decision-making authority, and transfer conditions. This means a foreign founder can design an operating structure that fits their group hierarchy rather than conforming to a rigid statutory default.

For a solo investor, the SASU allows a single natural or legal person to hold all shares, making it compatible with wholly-owned subsidiary arrangements without requiring a local co-shareholder.

Keep these points in mind:

- The statuts must designate at least one président; no minimum capital requirement applies

- A foreign legal entity can serve as sole shareholder of a SASU

- Major decisions not reserved to the shareholder can be delegated by statute to appointed officers

- Share transfer restrictions must be explicitly drafted into the statuts to be enforceable

A foreign corporation can act as the sole shareholder and président of a SASU incorporated in Réunion, without any resident director requirement under current French law.

Access to French and European Funding Programs

Réunion's status as a French overseas department and an EU outermost region gives incorporated entities direct access to European funding programs that are structurally unavailable to companies based in non-EU territories. This access is governed by the entity's legal registration within the French Republic, not by special application or bilateral arrangement.

EU Structural Funds and the ERDF Allocation

As a designated outermost region under Article 349 of the Treaty on the Functioning of the European Union, the island receives a disproportionately higher allocation of European Regional Development Fund (ERDF) financing compared to mainland EU regions. This higher per-capita allocation exists specifically to offset structural disadvantages, and your business, if operating in eligible sectors, can access co-financed grants for investment, innovation, and capacity development. Eligibility is assessed against operational programs managed through the Préfecture de La Réunion and the Conseil Régional, which administer fund distribution under the partnership agreement between France and the European Commission.

France's POSEI Program and Additional National Mechanisms

Beyond EU cohesion instruments, companies operating in agriculture-adjacent or import-substitution sectors may qualify under POSEI, a program distinct from the Common Agricultural Policy mainstream and tailored specifically for outermost regions. The French state also layers additional support through FEDER-funded regional schemes and FEADER for rural development activities. These funding channels compound: a firm accessing ERDF grants is not automatically excluded from national co-financing mechanisms, which means the total public support ceiling can be meaningfully higher than what a comparable mainland French entity would receive.

Maximize Funding Access Through Your Réunion Incorporation

Understand which EU and French funding programs your business structure qualifies for, and how to position your entity for maximum eligibility from the outset.

Strong Infrastructure and Skilled Workforce

Réunion skilled workforce advantages for business are grounded in the island's full integration into the French national education system. Graduates from local institutions hold qualifications governed by the same standards applied in metropolitan France, meaning your firm can hire locally without adjusting for credential gaps or qualification equivalency issues common in other emerging-market locations.

- The island's universities and vocational training centers operate under the French Ministère de l'Éducation Nationale framework, producing graduates in engineering, business administration, IT, and health sciences whose diplomas carry direct recognition across all EU member states.

- French labor law applies in full, so employment contracts, collective agreements, and dispute resolution procedures follow the same Code du Travail provisions used in mainland France, giving foreign firms a predictable legal structure for workforce management.

- Réunion infrastructure benefits for foreign investors include a fiber-optic network connecting the island to international submarine cable systems, supporting data-intensive operations.

- Port Réunion and Roland Garros International Airport provide commercial freight access to Indian Ocean trade routes, which reduces logistics dependency on a single transit point.

- Public utilities, road networks, and telecommunications are maintained under French territorial investment standards, so operational disruptions from infrastructure deficits are less frequent than in many comparable island jurisdictions.

Strategic Location Between Africa and Asia

Réunion sits in the southwestern Indian Ocean, approximately 800 km east of Madagascar and 170 km southwest of Mauritius. This position places your business within a time zone (UTC+4) that overlaps with both East African trading hours and the latter part of Asian business days, reducing the communication lag that typically affects companies operating across multiple continents.

As a French overseas department, the island functions under EU trade frameworks, including preferential agreements that extend to African, Caribbean, and Pacific (ACP) countries. A firm registered here can engage East African markets, such as COMESA member states, while retaining the regulatory standing of an EU-established entity.

- Flight connections run through Roland Garros Airport to major African hubs including Johannesburg, Nairobi, and Antananarivo, as well as onward connections to Asian cities via Mauritius.

- The Port of La Réunion serves as a transit point for goods moving between the African continent and Asian supply chains.

A logistics or distribution company incorporated in Réunion and supplying clients across three East African markets could count those export revenues toward French overseas tax base calculations, potentially qualifying for the reduced rate provisions under Article 217 bis of the French General Tax Code (Code Général des Impôts).

Social Security Coverage Under French System

French social security coverage benefits in Réunion derive directly from the metropolitan French system, administered under the Code de la Sécurité Sociale. Employees on the island are enrolled in the same national scheme covering health insurance, retirement pensions, workplace accident compensation, and family allowances as workers in mainland France.

For a foreign business owner, this structure removes a significant operational variable. You are not managing a fragmented or untested local protection regime; your employees receive coverage backed by one of the most established social insurance frameworks in the world.

Réunion employee social protection advantages extend to employers as well. Contribution rates are set nationally, meaning your payroll compliance obligations follow a predictable, codified schedule rather than locally negotiated terms.

- Health coverage is administered through the Caisse Générale de Sécurité Sociale (CGSS), the island's dedicated social security body.

- Retirement contributions feed into the national CNAV (Caisse Nationale d'Assurance Vieillesse) system.

- Workplace accident and occupational illness coverage follows the same tariff rules applied across French territory.

The consistency of this framework means workforce management, employment contracts, and benefit obligations can be standardized if you operate across multiple French territories.

Employer contribution rates in Réunion may differ slightly from mainland France due to applicable overseas exemption schemes under the LODEOM law; verify current CGSS schedules before finalizing payroll projections.

Euro Currency Eliminates Exchange Rate Risk

Réunion euro currency business advantages are concrete and structural. As a French overseas department, the island uses the euro as its official currency under the same legal and monetary framework that governs metropolitan France and the broader eurozone. For a foreign business owner, this means that transactions invoiced, settled, or reported in euros carry no conversion exposure relative to other eurozone counterparties.

No Currency Conversion Between Réunion and the EU

Any business incorporated on the island operates within the same currency zone as France, Germany, the Netherlands, and 17 other EU member states. Payments to European suppliers, receipts from European clients, and intercompany transfers within an EU group all occur in a single currency. The elimination of conversion costs and hedging requirements on these flows is a direct, quantifiable reduction in operating overhead.

Monetary Policy Governed by the European Central Bank

The euro's monetary policy is set by the European Central Bank under the Treaty on the Functioning of the European Union. Your company does not depend on a small-island central bank or a currency whose value is subject to local political or economic pressures. That stability is legally anchored at the treaty level, not by administrative discretion.

Practical Implications for Multi-Currency Operations

For firms that also operate in African or Indian Ocean markets, the euro functions as a stable base currency for:

- Benchmarking contracts denominated in volatile regional currencies

- Holding working capital without local currency depreciation risk

- Simplifying consolidated financial reporting across EU and non-EU subsidiaries

Why Réunion Stands Out Against Comparable Jurisdictions

Comparing Réunion against other Indian Ocean jurisdictions reveals a structural divide that straightforward cost comparisons tend to obscure. Mauritius and the Seychelles are frequently cited alternatives for regional incorporation, and both offer low nominal tax rates and flexible holding structures. What they do not offer is full integration into EU institutional and legal architecture. For a foreign business owner, that distinction carries direct operational consequences: access to EU procurement, CE marking, GDPR compliance recognition, and treaty protections that neither Mauritius nor the Seychelles can replicate by design.

Mayotte, the other French overseas collectivity in the Indian Ocean, shares some of the same legal heritage but operates under a transitional regulatory framework and lacks the same depth of economic infrastructure. Against these peers, the Réunion vs comparable jurisdictions incorporation advantages argument rests less on tax figures and more on what the regulatory environment unlocks at a practical level, including legal certainty under the French Commercial Code, euro-denominated contracts, and enforceable EU-standard dispute resolution. The Code de commerce governs entity formation directly, with no parallel offshore legal track that creates ambiguity for counterparties.

| Parameter | Réunion | Mauritius | Seychelles |

|---|---|---|---|

| EU Single Market Access | Full (as EU outermost region) | None | None |

| Governing Legal Code | French Commercial Code | Mauritius Companies Act 2001 | Companies Act 1972 (amended) |

| Currency | Euro (no exchange risk) | Mauritian Rupee | Seychellois Rupee |

| VAT Framework | French VAT (reduced rates apply locally) | 15% VAT | No VAT on international structures |

| Dispute Resolution | French courts / EU enforcement | ICAC arbitration | Seychelles courts |

| EU Funding Eligibility | Yes (ERDF, ESF+) | No | No |

| Social Security System | French national system | National Pension Fund | Social Security Fund |

Compliance Services for Companies in Réunion

Maintain your legal standing under French and EU regulatory requirements with structured compliance support tailored to Réunion-registered entities.

Conclusion

Réunion presents a coherent case for incorporation that few French overseas territories can match: EU market access, a stable French legal order, and a tax incentive framework specifically calibrated for overseas economic development under the Loi Girardin and related Code général des impôts provisions.

The combination of EU single market membership and the SASU or SAS corporate structures means your business can operate under a familiar, enforceable framework while retaining meaningful governance flexibility. For export-oriented firms, the geographic position between African and Asian markets adds a distribution advantage that purely European registrations cannot replicate.

Whether this structure suits your business depends on your industry, ownership profile, and planned operations. A holding company with passive income has a different calculus than a trading firm targeting Indian Ocean markets. The right formation decision follows from those specifics.

For businesses that do align with what this territory offers, the formal next step is working through the Centre de Formalités des Entreprises process with qualified local or international support to ensure registration, tax election, and ongoing compliance obligations are handled correctly from the outset.

Start Your Réunion Incorporation Journey With Expanship

Expanship supports foreign investors through the full incorporation process in Réunion, covering everything from selecting between a SASU and SAS structure to filing with the Greffe du Tribunal de Commerce and registering with the Centre de Formalités des Entreprises. The tax incentives under the Loi pour le Développement Économique des Outre-Mer, the Euro currency environment, and the access to EU funding programs covered throughout this blog each carry distinct compliance requirements that Expanship's team is equipped to manage on your behalf.

From document preparation to post-incorporation obligations, the service scope includes:

- Preparation and legalization of incorporation documents

- Registered agent and registered office provision

- Filing and liaison with the Greffe du Tribunal de Commerce

- Post-incorporation compliance management, including annual reporting obligations

- Banking introduction assistance for corporate account setup

- Ongoing registered address maintenance as required under French commercial law

To discuss your setup requirements, contact Expanship Réunion directly.

Frequently Asked Questions (FAQ)

Companies operating in Réunion may benefit from tax reduction schemes established under the Loi Girardin, which provides fiscal incentives for investment in French overseas territories. Eligible investments in productive equipment or real estate may qualify for income tax reductions, subject to conditions set by the French tax authority, the Direction Générale des Finances Publiques. The specific rate and eligibility criteria depend on the sector and the nature of the investment.

Registration timelines follow French metropolitan procedures, as the territory falls under the same legal framework. Filing through the Centre de Formalités des Entreprises or the INPI's online guichet unique generally takes between one and two weeks for straightforward incorporations, assuming all required documents are in order. Complex structures or incomplete filings may extend this period.

Yes. Because Réunion holds Outermost Region status under Article 349 of the Treaty on the Functioning of the European Union, businesses established there can access European Structural and Investment Funds, including the ERDF and ESF. These funds are allocated through multi-annual programs managed in coordination with the regional council and the European Commission.

A registered address in Réunion is required for incorporation, as the entity must be domiciled within the territory for SIRET registration and tax purposes. French law does not strictly require a director to be a resident, but having a local representative can facilitate dealings with the Direction des Entreprises, de la Concurrence, de la Consommation, du Travail et de l'Emploi (DIECCTE) and other administrative bodies. Practical compliance obligations often make local representation advisable.

Changes to tax incentives for overseas departments require legislative action at the French national level, typically through the annual Finance Law (Loi de Finances). Historical precedent shows that schemes like Loi Girardin have been amended multiple times, with transitional provisions generally protecting investments made under prior rules. Businesses should monitor annual finance legislation and any guidance issued by the Direction Générale des Finances Publiques to assess the impact of policy changes on existing structures.

Accounts and statutory filings for companies registered in Réunion are denominated in euros, consistent with French accounting standards under the Plan Comptable Général. For businesses transacting in other currencies, standard foreign exchange accounting rules under French GAAP apply, requiring conversion at applicable exchange rates with gains and losses recorded accordingly. There is no separate currency regime or reporting framework specific to the territory.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.