Key Takeaways

- Businesses incorporated in Réunion are subject to the full French Code de commerce and metropolitan regulatory framework, meaning there is no simplified or reduced compliance model available as exists in many other overseas or island jurisdictions.

- URSSAF social charges levied on payroll represent a significant employer cost burden, with combined employer and employee contributions capable of substantially increasing the effective cost of each hire beyond the nominal salary figure.

- Geographic isolation in the Indian Ocean translates directly into elevated logistics, import, and operational costs that mainland French or continental EU competitors do not face at the same scale.

- The requirement that all corporate documentation, filings, and legal instruments be produced in French creates an additional administrative and translation burden for non-francophone foreign investors that does not exist when incorporating in anglophone jurisdictions with comparable market access.

Réunion operates under the full weight of French metropolitan law, making it one of the more heavily regulated incorporation environments among overseas territories globally. As an integral part of France and the European Union, the business and legal framework applied here is not a simplified offshore model — it mirrors the requirements imposed on companies formed in Paris or Lyon.

This article addresses the disadvantages of incorporating in Réunion across several distinct categories, spanning taxation, administrative procedure, market conditions, and geographic constraints.

The relevance of each drawback depends significantly on your business model, intended industry, and whether your firm requires local staffing or operates across borders. A digital services entity faces a different burden than a manufacturing or import-dependent business.

The applicable commercial legislation is codified in the Code de commerce, published on Légifrance, France's official legal database.

Foreign investors — particularly those from outside the EU considering Réunion as a regional base for Indian Ocean or African market access — are most likely to encounter the structural and operational constraints examined here.

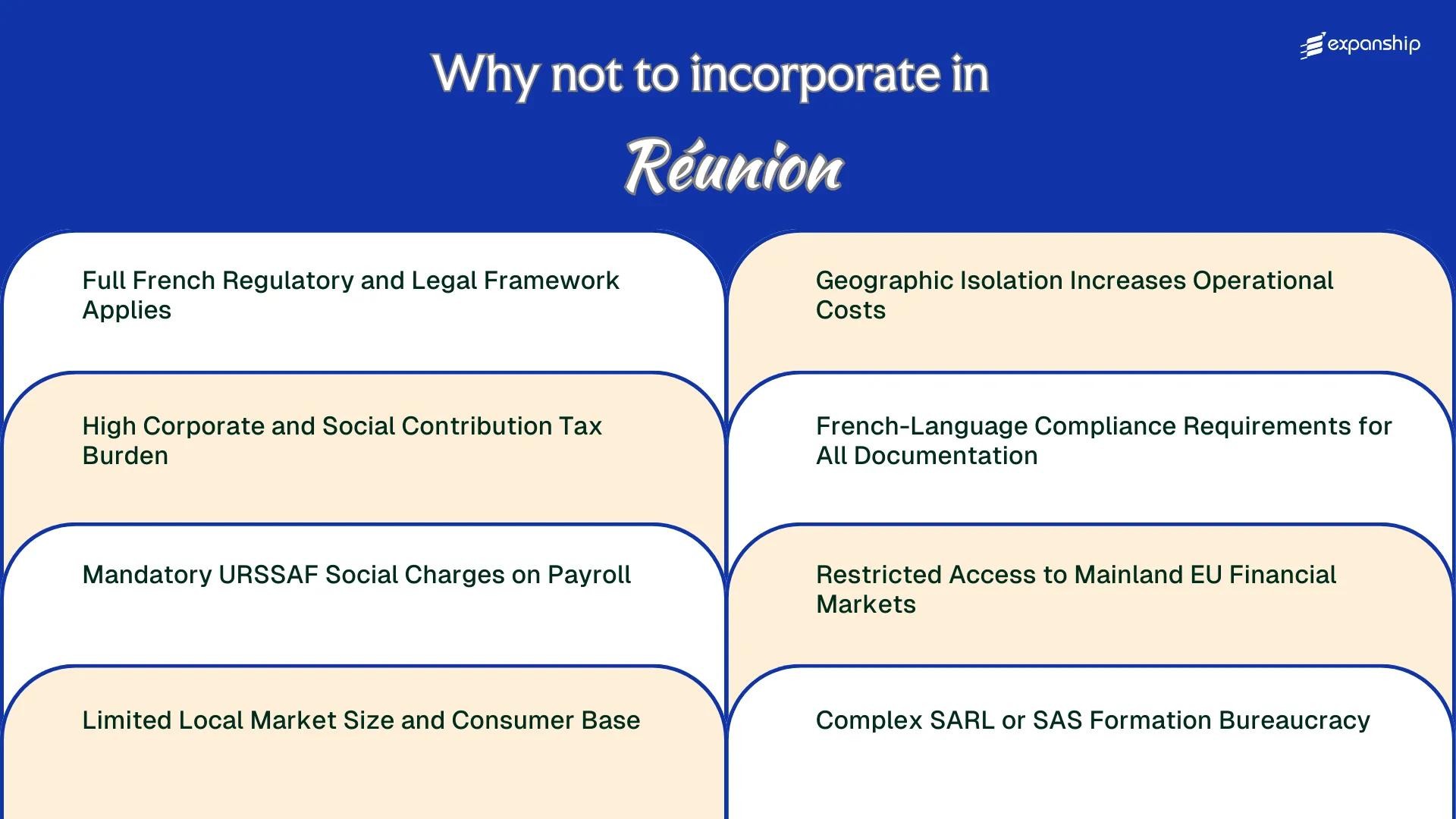

Full French Regulatory and Legal Framework Applies

Réunion operates under the full legal architecture of metropolitan France. Every business registered there is subject to the same regulatory obligations as a firm incorporated in Paris or Lyon, with no territorial carve-outs.

The Scope of French Law in a Remote Jurisdiction

French regulatory restrictions Réunion business owners face are not simplified versions of mainland requirements. The Code de Commerce applies in its entirety, meaning corporate governance obligations, annual reporting to the greffe du tribunal de commerce, and statutory audit thresholds all mirror those enforced in metropolitan France. For a foreign founder without prior exposure to French commercial law, this creates an immediate compliance burden that typically requires local legal counsel from day one.

Why the French Legal Framework Creates Disproportionate Costs Here

The French legal framework challenges in Réunion are compounded by the island's distance from the legal infrastructure that makes compliance manageable on the mainland. Specialist corporate lawyers, certified accountants (experts-comptables), and notaries are less concentrated here than in major French cities, which drives up advisory costs. Code de Commerce compliance in Réunion therefore carries both the complexity of a sophisticated civil law system and the scarcity premium of a remote overseas territory.

A foreign business owner must budget for continuous French-qualified legal support from incorporation onward, as non-compliance with Code de Commerce obligations can result in administrative dissolution or personal liability for company directors.

High Corporate and Social Contribution Tax Burden

The high corporate tax burden in Réunion stems directly from its status as a French overseas department, making the standard French corporate income tax rate applicable. As of recent fiscal years, the standard rate sits at 25% for most companies, applied to net taxable profits under the French General Tax Code (Code général des impôts).

For foreign-owned entities generating profits above established thresholds, this rate applies without the favorable flat-tax structures common in competing jurisdictions.

Beyond corporate income tax, your business faces the French social contribution on corporate profits (Contribution sociale sur les bénéfices, or CSB), levied at 3.3% on the portion of tax exceeding €763,000. This additional layer compounds the effective tax cost for mid-sized and growing firms.

Specific ways this combined tax structure creates operational friction include:

- Profit repatriation to a parent company abroad triggers French withholding tax considerations, reducing net yield on invested capital

- Transfer pricing obligations under French tax law require documented arm's length pricing, generating significant compliance costs for intra-group transactions

- Foreign tax credits may not fully offset Réunion-sourced liabilities depending on the applicable bilateral treaty, leaving residual double taxation exposure

Small companies meeting the PME criteria may access a reduced rate of 15% on the first €42,500 of taxable profit, but this ceiling limits its practical value for any business scaling beyond early-stage revenues.

Company Incorporation in Réunion

Understand the full tax and structural implications before registering your business in Réunion as a French overseas department.

Mandatory URSSAF Social Charges on Payroll

Employers operating in Réunion face URSSAF payroll charges that mirror those applied on the French mainland, with no structural relief for the island's economic context. As an overseas department, the firm is subject to the same social security contribution architecture administered by URSSAF, the national body responsible for collecting employer and employee social charges.

Employer contributions alone typically reach between 40% and 45% of gross salary, covering health insurance, retirement, unemployment, and family allowances. For a foreign business hiring even a small team, this rate substantially increases total employment costs beyond the nominal salary figure.

| Contribution Category | Approximate Employer Rate |

|---|---|

| Health insurance (maladie) | ~7% of gross salary |

| Old-age pension (retraite de base) | ~8.55% up to ceiling |

| Family allowance (allocations familiales) | ~3.45–5.25% of gross salary |

| Unemployment insurance (chômage) | ~4.05% of gross salary |

| Work accident / occupational risk | Variable by sector |

| Total indicative employer burden | ~40–45% of gross salary |

Each payroll cycle requires declaration and remittance through the DSN (Déclaration Sociale Nominative) system, and errors carry financial penalties. Your accounting infrastructure must be configured specifically for French social law, which adds operational overhead from day one.

Partial exemptions exist under the Lodeom scheme for low-wage positions, but mid-to-senior salary bands fall entirely outside that relief and carry the full contribution load.

Limited Local Market Size and Consumer Base

Réunion limited market size risks are structural, not circumstantial. With a population of approximately 900,000 residents on an island of 2,512 square kilometres, the total addressable consumer base is fixed by geography and cannot expand through domestic growth alone.

Per capita GDP sits below the metropolitan French average, which compresses consumer spending capacity across most retail and service categories. A foreign business entering this market faces a ceiling on revenue that no operational efficiency can raise.

Demand concentration in a few urban zones, primarily Saint-Denis and Saint-Pierre, means that businesses serving dispersed populations carry disproportionate distribution costs relative to their actual sales volume. The INSEE Réunion data consistently shows that household purchasing power on the island trails metropolitan France by a measurable margin.

Certain sectors, including financial services and high-value B2B supply chains, face additional constraints because the local corporate ecosystem is limited in scale and depth.

- Foreign firms must account for a consumer base under one million when projecting revenue models

- Sector-specific demand ceilings apply independently of marketing investment or pricing strategy

- Businesses operating B2B models face a restricted pool of qualifying local corporate clients

- Revenue forecasts cannot rely on population growth as a scaling variable given the island's geographic boundaries

Despite being geographically closer to Madagascar than to Paris, all consumer protection and market regulations applied to your business are identical to those enforced in mainland France.

Geographic Isolation Increases Operational Costs

Réunion geographic isolation business costs extend well beyond basic freight expenses, making supply chain reliability a persistent structural problem for any company operating from the island.

Distance From Suppliers and Markets

Located roughly 9,200 kilometres from mainland France in the Indian Ocean, Réunion depends almost entirely on air and sea freight for goods that cannot be sourced locally. Transit times for sea freight from Europe typically run four to six weeks, meaning your inventory cycles are longer and working capital is tied up significantly longer than for firms based in continental Europe.

Cascading Cost Effects on Business Operations

Import dependency means you absorb not just shipping costs but also insurance premiums, port handling fees at Port Réunion, and recurring customs formalities under French customs administration. For time-sensitive inputs, you may have no practical alternative to air freight, which can multiply per-kilogram costs by a factor of eight to ten compared to sea transport. Logistics challenges incorporating in Réunion are therefore not a one-time setup burden but an ongoing operating expense that compresses margins across every business cycle.

Assessing Operational Cost Challenges for Your Réunion Entity

Understand the full cost implications of incorporating and operating in Réunion before committing to a structure.

French-Language Compliance Requirements for All Documentation

French language compliance requirements in Réunion apply to every document your business produces, files, or submits to a public authority, with no official accommodation for English or any other language.

- All statutory filings submitted to the Greffe du Tribunal de Commerce must be drafted in French, meaning foreign founders must either employ qualified translators or retain a local legal professional, adding recurring cost to every filing cycle.

- Contracts, employment agreements, and internal corporate records are subject to the Ordonnance de Villers-Cotterêts principle requiring French as the language of legal validity, so any document drafted solely in another language carries enforceability risk.

- URSSAF and tax authority correspondence, including declarations and responses to administrative notices, must be conducted in French, creating a dependency on intermediaries that slows response times during compliance deadlines.

- No multilingual submission pathway exists within the local commercial registry system, making language barriers a structural operational cost rather than an incidental inconvenience.

Restricted Access to Mainland EU Financial Markets

Réunion restricted EU financial market access is a structural disadvantage that foreign business owners frequently underestimate before incorporation. Although the island is an integral part of France and the EU, its classification as an Outermost Region (OMR) under Article 349 of the Treaty on the Functioning of the European Union creates asymmetries in how financial institutions treat locally registered entities.

Mainland French and broader EU banks often categorize companies incorporated in overseas departments differently from metropolitan entities. This means your firm may face additional due diligence requirements, account opening refusals, or restricted access to standard EU payment infrastructure.

Correspondent banking relationships and certain EU passporting privileges available to firms registered in metropolitan France do not automatically extend to OMR-registered entities without additional qualification steps. For a foreign investor expecting frictionless access to eurozone financial markets, this gap can delay operations and increase setup costs.

A foreign-owned SAS incorporated in Saint-Denis seeking to open a business account with a mainland French bank reports an average processing delay of 6 to 12 weeks, compared to 1 to 3 weeks for a metropolitan French entity, due to enhanced geographic risk classification applied by compliance departments.

Complex SARL or SAS Formation Bureaucracy

SARL SAS formation bureaucracy in Réunion follows the full French commercial code, meaning your incorporation process runs through the same procedural machinery as a metropolitan French company. For foreign founders, this creates immediate friction: documents must be filed with the Greffe du Tribunal de Commerce, capital must be deposited with a licensed French banking institution, and statutes must conform to either the Code de Commerce provisions governing SARLs or SAS structures.

The Centre de Formalités des Entreprises (CFE) coordinates multi-agency registration, but this coordination does not eliminate the sequential nature of the process. Each agency, including the tax authority (Direction Générale des Finances Publiques) and social security bodies, requires separate compliance steps that extend your timeline.

For an SAS specifically, the freedom to draft custom statutes creates a secondary burden. Without a French corporate lawyer familiar with local practice, statute errors can trigger rejection by the Greffe, requiring redrafting and re-filing at additional cost.

Publication of incorporation notices in a legal gazette (Journal d'Annonces Légales) is also mandatory, adding both time and fees.

- Minimum share capital for an SARL is €1, but banking due diligence requirements for non-resident founders often impose practical delays beyond the statutory minimum.

- SAS formations require a statutory auditor (commissaire aux comptes) once certain thresholds are crossed.

Non-EU resident directors or shareholders may face additional identity verification and notarized document requirements under French anti-money laundering regulations, which can significantly extend the Réunion SAS incorporation process beyond standard domestic timelines.

Overcoming These Incorporation Challenges

Overcoming Réunion incorporation challenges begins with understanding that the regulatory environment is French law in its entirety, not a simplified offshore variant.

- Register your entity through the Guichet Unique to consolidate SARL or SAS formation filings across the CFE, INSEE, and RCS simultaneously.

- Appoint a French-speaking legal representative to ensure all statuts, contrats, and official correspondence meet DACS compliance standards from the outset.

- Structure your payroll obligations with URSSAF declarations factored into cash flow projections before hiring, not after.

- Apply for available ZFA (Zone Franche Active) or Outre-mer tax relief schemes through the Direction Générale des Finances Publiques to partially offset the corporate and social contribution burden.

- Establish logistics contracts with suppliers operating Indian Ocean freight corridors to reduce exposure to geographic isolation costs.

These steps address procedural and financial friction points within a system governed by the French Commercial Code. None of them eliminate the underlying cost structures, which remain structurally embedded in the jurisdiction's regulatory framework.

Réunion's Overall Business Viability

Réunion presents a credible incorporation destination for businesses with specific ties to the French regulatory ecosystem or the Indian Ocean region. A realistic Réunion business viability risks assessment, however, shows that the structural disadvantages are significant and consistent rather than incidental.

| Pros | Cons |

|---|---|

| Full access to French and EU legal frameworks, providing a stable, predictable regulatory environment | The complete French regulatory and legal framework applies, including obligations under French commercial and tax law |

| Euro-denominated operations with EU monetary stability | Corporate and social contribution tax burdens are comparable to metropolitan France, with limited island-specific relief |

| French-language documentation standards align with established civil law compliance norms | URSSAF social charges on payroll add substantial mandatory cost to any hiring activity |

| Réunion's status as an EU outermost region provides access to certain EU structural funds | The local consumer base is small, limiting revenue potential from domestic sales |

| Geographic isolation from mainland France and continental markets increases logistics and operational costs | |

| Formation through SARL or SAS structures involves French bureaucratic procedures that are time-intensive for foreign incorporators |

Access to EU frameworks carries real weight for the right entity profile. The constraints on market size, payroll costs, and geographic position remain material factors that any foreign business owner must account for before committing to formation here.

Corporate Compliance Services in Réunion

Manage your ongoing compliance obligations under French commercial law, including annual filings, URSSAF reporting, and statutory requirements applicable to entities registered in Réunion.

Conclusion

Incorporating in Réunion carries a clear set of structural constraints that apply regardless of your sector or business model. The disadvantages incorporating in Réunion summary points to three recurring friction points: the full weight of French metropolitan regulatory obligations, the URSSAF social charge burden on payroll, and the geographic isolation that raises operating costs beyond what comparable EU-adjacent markets would impose. These are not peripheral concerns. For any firm assessing this jurisdiction, understanding the precise scope of these obligations before formation determines whether the structure remains viable at the scale you intend to operate.

Expanship's Support for Your Réunion Expansion

Expanship's support for your Réunion company formation covers the specific compliance obligations that make incorporating here more demanding than in a standard EU member state. From URSSAF payroll registration and SARL or SAS formation filings to French-language documentation requirements and liaising with local authorities, Expanship helps reduce the administrative burden these obligations place on your business.

Our services span the full incorporation and post-incorporation cycle.

- Your company registration and document preparation are handled in accordance with French commercial law requirements applicable in Réunion.

- A registered agent and local office address are provided to satisfy legal domiciliation obligations.

- Government filings and regulatory body liaison are managed on your behalf throughout the process.

- Ongoing compliance management is maintained after your entity is active.

- Banking introduction assistance is provided to help your firm establish a local account.

- Tax registration and liaison with relevant local authorities are coordinated from the outset.

Reach out to Expanship Réunion to discuss your incorporation requirements.

Frequently Asked Questions (FAQ)

URSSAF applies the same payroll contribution framework in Réunion as it does in mainland France, meaning employer social charges typically range between 40% and 45% of gross salary. Some partial exemptions exist under specific overseas employment incentive schemes, but these are conditional on hiring local residents and meeting sector eligibility criteria. Relying on these exemptions without confirming eligibility in advance can create significant retroactive liability.

Failure to meet statutory obligations under French company law — such as filing annual accounts with the Greffe du Tribunal de Commerce or holding required shareholder meetings — can result in fines, forced dissolution, or personal liability for directors. French commercial law does not treat non-residents more leniently; foreign directors carry the same legal exposure as French nationals. Persistent non-compliance can also trigger tax audits by the Direction Générale des Finances Publiques.

With a population of approximately 900,000, the local consumer base is structurally small and cannot sustain most B2C business models at scale without an export strategy. Réunion's geographic position in the Indian Ocean does offer proximity to regional markets such as Madagascar, Mauritius, and the Comoros, but accessing those markets requires separate regulatory and trade arrangements. A business incorporated in Réunion does not automatically gain preferential access to those neighboring jurisdictions.

Shipping goods to or from Réunion involves transoceanic freight, which adds cost, lead time, and logistical complexity that firms in continental Europe do not face. Supply chain disruptions affect the island disproportionately given its dependence on imports for a wide range of inputs. These costs are not offset by any special freight subsidy applicable to all businesses — only certain agricultural and public interest sectors benefit from targeted support mechanisms.

The formation process follows identical French legal requirements under the Code de Commerce, so the baseline complexity is the same as in mainland France. However, the practical burden is compounded in Réunion by the fact that local administrative capacity, notarial services, and specialist legal advisers are less concentrated than in Paris or Lyon. Processing times at the Greffe can therefore extend beyond standard metropolitan benchmarks, particularly for entities with foreign shareholders requiring apostilled documentation.

Access to EU structural funds designated for Réunion — classified as an Outermost Region under Article 349 of the Treaty on the Functioning of the European Union — is primarily channeled through public institutions and approved local operators, not freely available to any incorporated entity. Mainland French capital markets and institutional financing networks are also harder to access from Réunion due to distance, limited local banking infrastructure, and the reduced presence of investment firms on the island. Foreign-owned companies without an established French banking relationship face additional friction when seeking credit facilities or institutional investment.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.