Key Takeaways

- The Private Limited Company is the most frequently registered entity in Sri Lanka, offering limited liability to resident and foreign investors under the Companies Act No. 7 of 2007 with minimal shareholder requirements.

- Sri Lanka's business structures are administered by the Registrar of Companies under the Department of the Registrar of Companies, with foreign investment oversight handled by the Board of Investment of Sri Lanka.

- Foreign firms can establish a presence in Sri Lanka without forming a separate legal entity by registering a Branch Office, Representative Office, or Liaison Office.

- Resident entities in Sri Lanka are taxed on worldwide income under the country's residence-based tax system, while non-resident entities are generally liable only on Sri Lanka-sourced income.

Introduction to Entity Types in Sri Lanka

Sri Lanka is an island nation situated in the Indian Ocean, off the southeastern tip of the Indian subcontinent, with proximity to India and the Maldives. It is an independent sovereign republic and a member of the Commonwealth of Nations. The types of business entities in Sri Lanka are governed primarily by the Registrar of Companies, operating under the Department of the Registrar of Companies, which administers the Companies Act No. 7 of 2007.

The country operates a residence-based tax system with corporate income tax applicable to resident entities on worldwide income, while non-resident entities are generally taxed on Sri Lanka-sourced income only.

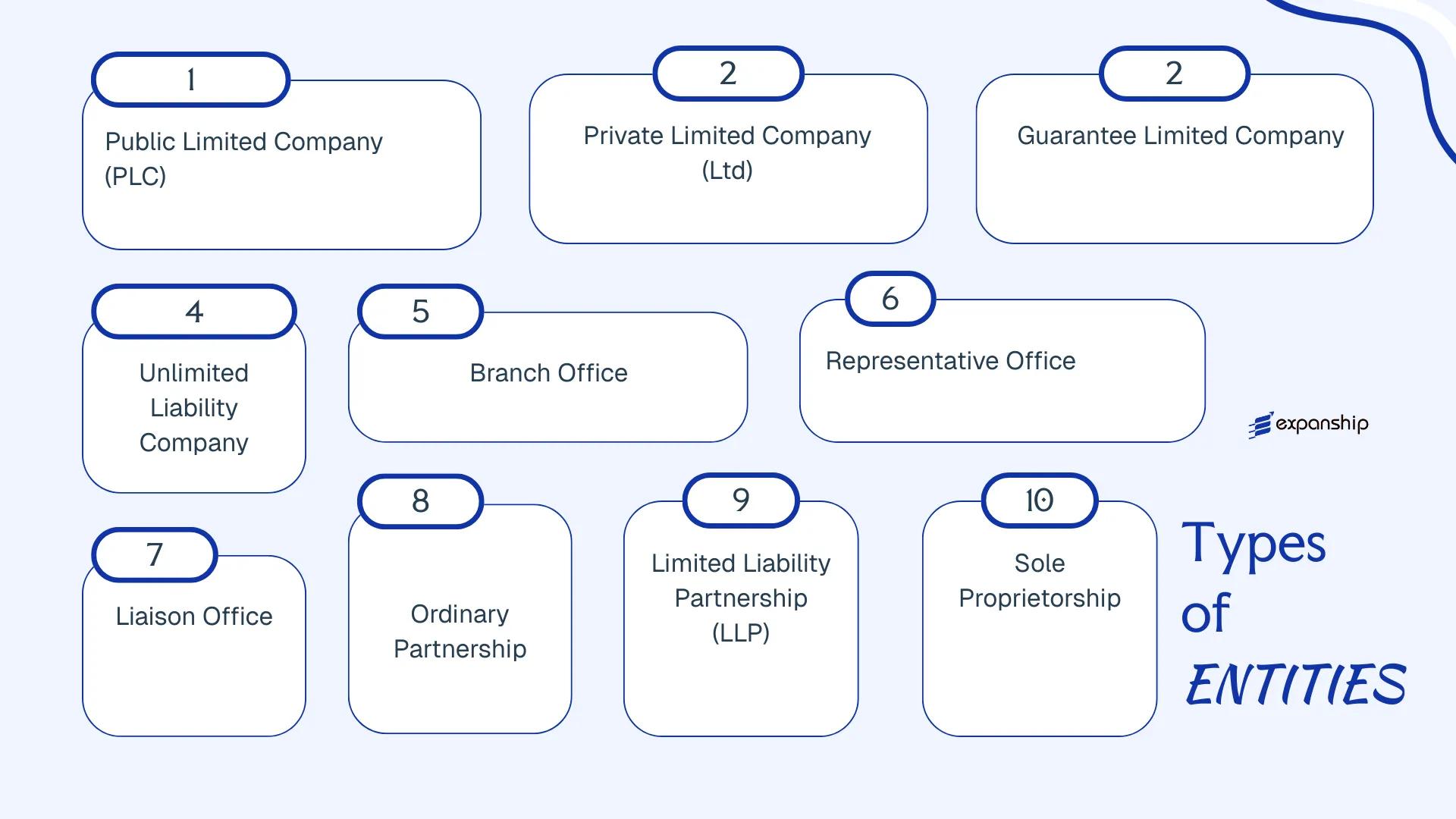

Businesses registering here may do so under several structures: Public Limited Company, Private Limited Company, Guarantee Limited Company, Unlimited Liability Company, Branch Office, Representative Office, Liaison Office, Ordinary Partnership, Limited Liability Partnership, and Sole Proprietorship. Each structure carries distinct legal obligations, liability implications, and regulatory requirements. This article examines each entity type in detail, covering formation requirements, ownership rules, and key compliance considerations.

An Overview of Business Structures in Sri Lanka

Sri Lanka's legal framework recognises several distinct business structures, each governed primarily by the Companies Act No. 7 of 2007 and administered by the Registrar of Companies under the Department of the Registrar of Companies. The Act provides for public and private limited companies, guarantee companies, and unlimited liability companies, while foreign entities may operate through branch, representative, or liaison offices. Each structure carries a different liability profile, ownership arrangement, and regulatory obligation.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Public Limited Company (PLC) | Incorporated company | Limited to shares | Taxable | Permitted | 2 shareholders | Dept. of Registrar of Companies | Companies Act No. 7 of 2007 |

| Private Limited Company (Ltd) | Incorporated company | Limited to shares | Taxable | Permitted | 1 shareholder | Dept. of Registrar of Companies | Companies Act No. 7 of 2007 |

| Guarantee Limited Company | Incorporated company | Limited by guarantee | Taxable / Exempt | Restricted | 1 member | Dept. of Registrar of Companies | Companies Act No. 7 of 2007 |

| Unlimited Liability Company | Incorporated company | Unlimited | Taxable | Permitted | 1 shareholder | Dept. of Registrar of Companies | Companies Act No. 7 of 2007 |

| Branch Office | Extension of foreign entity | Parent company liable | Taxable | Permitted | N/A | Dept. of Registrar of Companies | Companies Act No. 7 of 2007 |

| Representative / Liaison Office | Non-trading presence | Parent company liable | Generally exempt | Not permitted | N/A | Board of Investment / ROC | BOI Act / Companies Act |

| Ordinary Partnership | Unincorporated | Joint and several | Taxable | Permitted | 2 partners | Dept. of Registrar of Companies | Partnership Ordinance |

| Limited Liability Partnership | Incorporated body | Limited to contribution | Taxable | Permitted | 2 partners | Dept. of Registrar of Companies | Partnership Act |

| Sole Proprietorship | Unincorporated | Unlimited personal | Taxable | Permitted | 1 owner | Local authority / ROC | Business Names Ordinance |

Each of these structures is examined in full in the sections below.

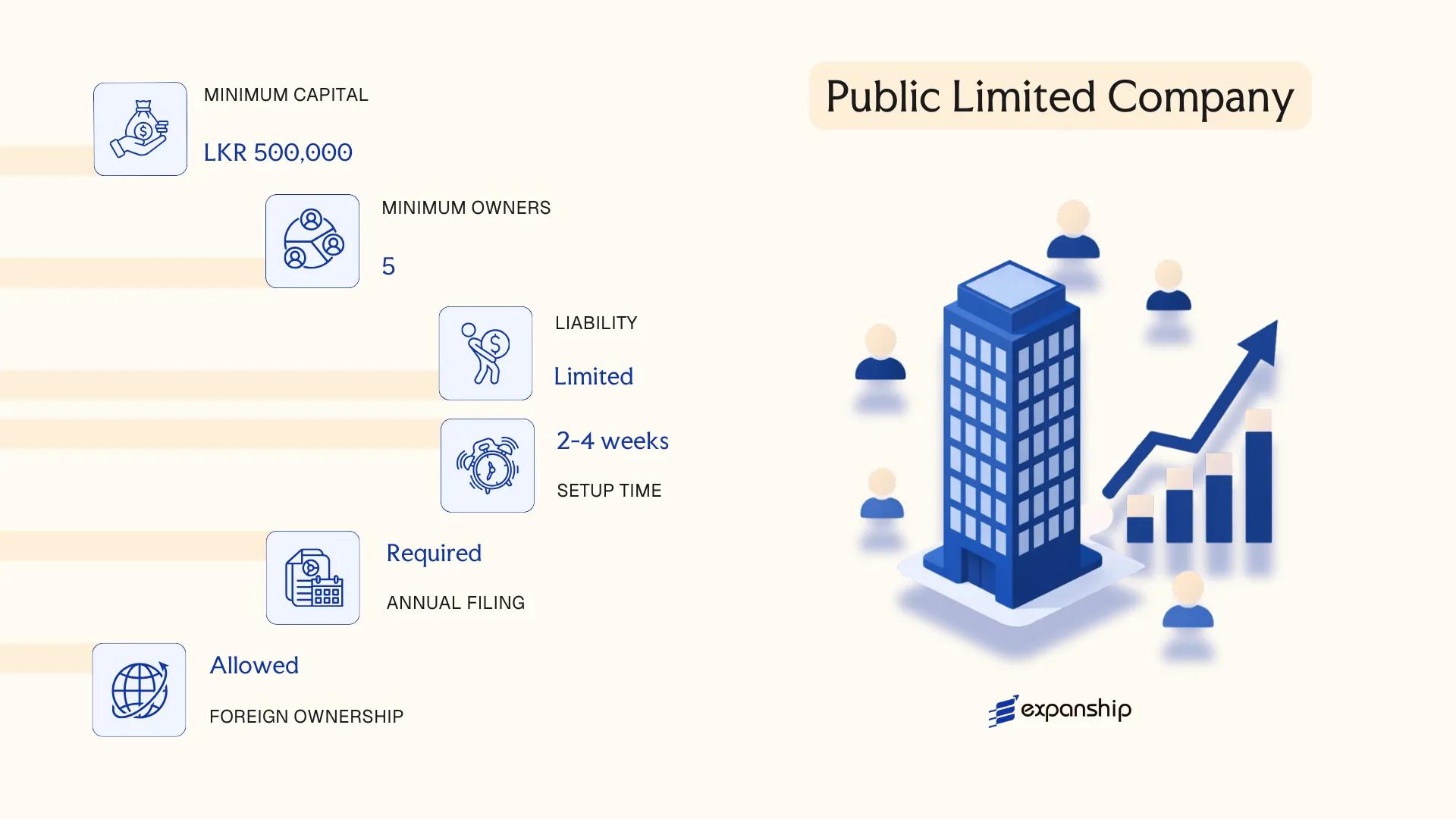

Public Limited Company (PLC) under the Companies Act No. 7 of 2007

A public limited company Sri Lanka recognises as a PLC is governed by the Companies Act No. 7 of 2007, administered by the Registrar of Companies under the Department of the Registrar of Companies. The entity holds a separate legal personality, meaning it can own assets, enter contracts, and incur liabilities in its own name.

Shareholders bear no personal liability beyond their subscribed capital. Unlike a private limited company, a PLC may offer shares to the general public and list on the Colombo Stock Exchange, making it the structure of choice for large-scale fundraising and publicly traded operations.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Public Limited Company | Incorporated under the Companies Act No. 7 of 2007 |

| Members | Shareholders; minimum 2 directors | Minimum 7 shareholders; no maximum cap on shareholders |

| Local Presence | Registered office address in Sri Lanka required | Must maintain a registered office accessible to the Registrar of Companies |

| Capital | LKR; no statutory minimum share capital | Authorised and issued capital must be stated in the Articles of Association |

| Governance | Board of Directors; mandatory Company Secretary | Secretary must be a qualified individual as prescribed under the Act |

| Privacy | Financials and shareholder details are publicly disclosed | Annual reports and audited accounts filed with the Registrar are public record |

Focus Points

- Taxation: Subject to corporate income tax at the standard rate of 30% on profits; VAT applies at 18% on taxable supplies; dividends paid to resident and non-resident shareholders attract withholding tax; stamp duty applies on share transfers.

- Annual Compliance: Must file audited financial statements and an annual return with the Registrar of Companies; failure attracts penalties under the Act.

- Listing Obligations: If listed on the Colombo Stock Exchange, additional disclosure, governance, and reporting obligations apply under SEC regulations.

- Treaty Access: Sri Lanka's double tax treaties may reduce withholding tax on dividends, interest, and royalties paid to foreign shareholders depending on the applicable treaty.

- Conversion: A PLC may be converted to a private limited company provided it no longer meets the criteria for a public company under the Act.

Closing

A PLC suits large enterprises seeking public capital, operating in regulated industries, or planning a stock exchange listing; the structure supports broad ownership but carries significant ongoing compliance and disclosure obligations that make it less practical for closely held or small-scale businesses.

Best suited for large-scale enterprises, joint ventures with public participation, or businesses planning to list on the Colombo Stock Exchange.

Company Incorporation in Sri Lanka

Incorporate your business entity in Sri Lanka with end-to-end support from registration to compliance.

Private Limited Company (Ltd) under the Companies Act No. 7 of 2007

Private Limited Company (Ltd) under the Companies Act No. 7 of 2007

A private limited company Sri Lanka Ltd is governed by the Companies Act No. 7 of 2007, administered by the Registrar General of Companies (RGC) under the Department of the Registrar of Companies. The entity carries separate legal personality, meaning the company exists independently of its shareholders.

Liability is confined to each member's unpaid share capital. This structure suits both domestic operations and foreign investment, as non-resident shareholders may hold equity without restriction under general company law, though sector-specific foreign ownership limits may apply separately.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private Limited Company (Ltd) | Separate legal entity; governed by the Companies Act No. 7 of 2007 |

| Members | Shareholders: min. 1, max. 50 | Shares may not be offered to the public |

| Directors | Min. 1 director required | At least one director must be ordinarily resident in Sri Lanka |

| Local Presence | Registered office address required within Sri Lanka | Must be a physical address; a PO Box is not sufficient |

| Share Capital | No statutory minimum; denominated in LKR | Authorised and issued capital must be stated in the Articles |

| Privacy | Shareholder and director details filed with RGC | Register of members is available for public inspection |

Focus Points

- Taxation: Subject to corporate income tax at the standard rate (currently 30% for most companies, 15% for qualifying sectors); VAT registration required if turnover exceeds the statutory threshold; withholding tax applies to dividends, interest, and royalties paid to non-residents at rates that may be reduced under applicable double tax treaties.

- Annual Compliance: Must file an Annual Return with the RGC and audited financial statements with the Inland Revenue Department; a company secretary must be appointed.

- Treaty Access: Sri Lanka maintains a network of double taxation agreements; a locally incorporated Ltd may access treaty benefits subject to residency and beneficial ownership conditions.

- Conversion: A private limited company may convert to a public limited company under Part IV of the Companies Act No. 7 of 2007, subject to RGC approval and shareholder resolution.

- Restrictions: Shares cannot be transferred freely without Board or shareholder approval per the Articles; public solicitation of investment is prohibited.

Closing

A private limited company is the standard vehicle for trading, holding, and service operations, offering defined liability boundaries without the public disclosure obligations of a listed entity. The resident director requirement is a practical constraint that foreign investors must factor into their setup.

Small to mid-sized foreign or domestic businesses seeking a straightforward incorporated structure with capped liability and no intention of public fundraising.

Guarantee Limited Company

A guarantee limited company in Sri Lanka is incorporated under the Companies Act No. 7 of 2007 and holds a separate legal personality distinct from its members. Liability is limited not by shares but by the amount each member undertakes to contribute to the entity's assets in the event of winding up. This structure is commonly adopted by organisations that operate without a profit motive.

Unlike share-based companies, this entity issues no share capital. Members make a nominal guarantee commitment, which may be as low as one rupee, and the company limited by guarantee Sri Lanka framework permits the entity to accumulate and deploy funds toward its stated objectives without distributing surpluses to members.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Company limited by guarantee | Incorporated under Companies Act No. 7 of 2007; separate legal entity |

| Members | Minimum 2; no statutory maximum | Referred to as members, not shareholders; no shares are issued |

| Governance | Minimum 1 director | Directors manage the company; a company secretary is required |

| Local Presence | Registered office in Sri Lanka | Must maintain a physical registered address within the country |

| Share Capital | None required | Guarantee amount per member typically nominal (e.g., LKR 1–100) |

| Privacy | Member and director details filed with the Registrar of Companies | Public record; limited confidentiality |

Focus Points

- Taxation: Subject to corporate income tax at the prevailing rate on any commercial income earned; VAT registration required if taxable turnover thresholds are met; donation income used for stated objectives may qualify for exemption subject to Inland Revenue Department approval.

- Annual Compliance: Must file annual returns and audited financial statements with the Registrar of Companies; failure to file attracts statutory penalties.

- Economic Substance: No formal economic substance regime applies to this entity type, though operational activity must align with the stated non-commercial objectives.

- Conversion: Conversion to a share-based company is not a standard statutory process; dissolution and re-incorporation under a different structure is the typical route.

- Restrictions: Cannot distribute profits or assets to members during its operation or upon dissolution; any surplus on winding up must be transferred to a similar entity or applied per the constitution.

Closing Paragraph

This Sri Lanka non-profit company structure suits associations, clubs, professional bodies, charities, and religious organisations that require legal personality without a profit-distribution mechanism. The primary advantage is the ability to contract, hold property, and sue in the company's own name; the key limitation is that the entity cannot raise equity capital or return surpluses to its members.

Guarantee company registration in Sri Lanka is most appropriate for non-profit organisations, industry associations, and foundations that require formal legal standing without equity participation.

Unlimited Liability Company

An unlimited liability company Sri Lanka formation follows the same procedural framework as other company types under the Companies Act No. 7 of 2007, administered by the Registrar of Companies. Unlike its limited counterparts, this structure does not cap the personal liability of its members — shareholders remain personally liable for the company's debts and obligations without restriction.

Despite this exposure, the entity retains separate legal personality, meaning it can own assets, enter contracts, and sue or be sued in its own name. The unlimited liability structure is rare in practice but remains a recognised form under the Act.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unlimited Liability Company | Registered under Companies Act No. 7 of 2007 |

| Members | Shareholders; minimum 1, no statutory maximum | Members bear unlimited personal liability for company debts |

| Directors | Minimum 1 director required | At least one director must be ordinarily resident in Sri Lanka |

| Registered Office | Must maintain a registered office in Sri Lanka | Address must be filed with the Registrar of Companies |

| Share Capital | No prescribed minimum capital | Capital structure must be defined in the articles of association |

| Privacy | Shareholder and director details filed on public register | Limited privacy; records accessible through the Registrar |

Focus Points

- Taxation: Subject to standard corporate income tax at 30% (or applicable concessionary rates); VAT registration required if turnover exceeds the threshold; withholding tax applies to dividends, interest, and royalties under prevailing rates.

- Annual Compliance: Must file annual returns and audited financial statements with the Registrar of Companies; same ongoing obligations as a limited company.

- Conversion: An unlimited company may apply to re-register as a limited liability company under the Companies Act, subject to Registrar approval.

- Treaty Access: Qualifies as a Sri Lankan resident entity for double tax treaty purposes, provided it meets substance and residency conditions.

- Restrictions: Not permitted to offer securities to the public; unsuitable for capital-raising structures.

Closing Paragraph

This structure suits closely held businesses where members accept full personal exposure, often for tax planning or specific structuring reasons in professional or family-owned contexts. The absence of a liability cap is its most significant drawback, making it unsuitable where asset protection is a priority.

Best suited for closely held family businesses or professional arrangements where the members have full visibility over liabilities and do not require public fundraising capacity.

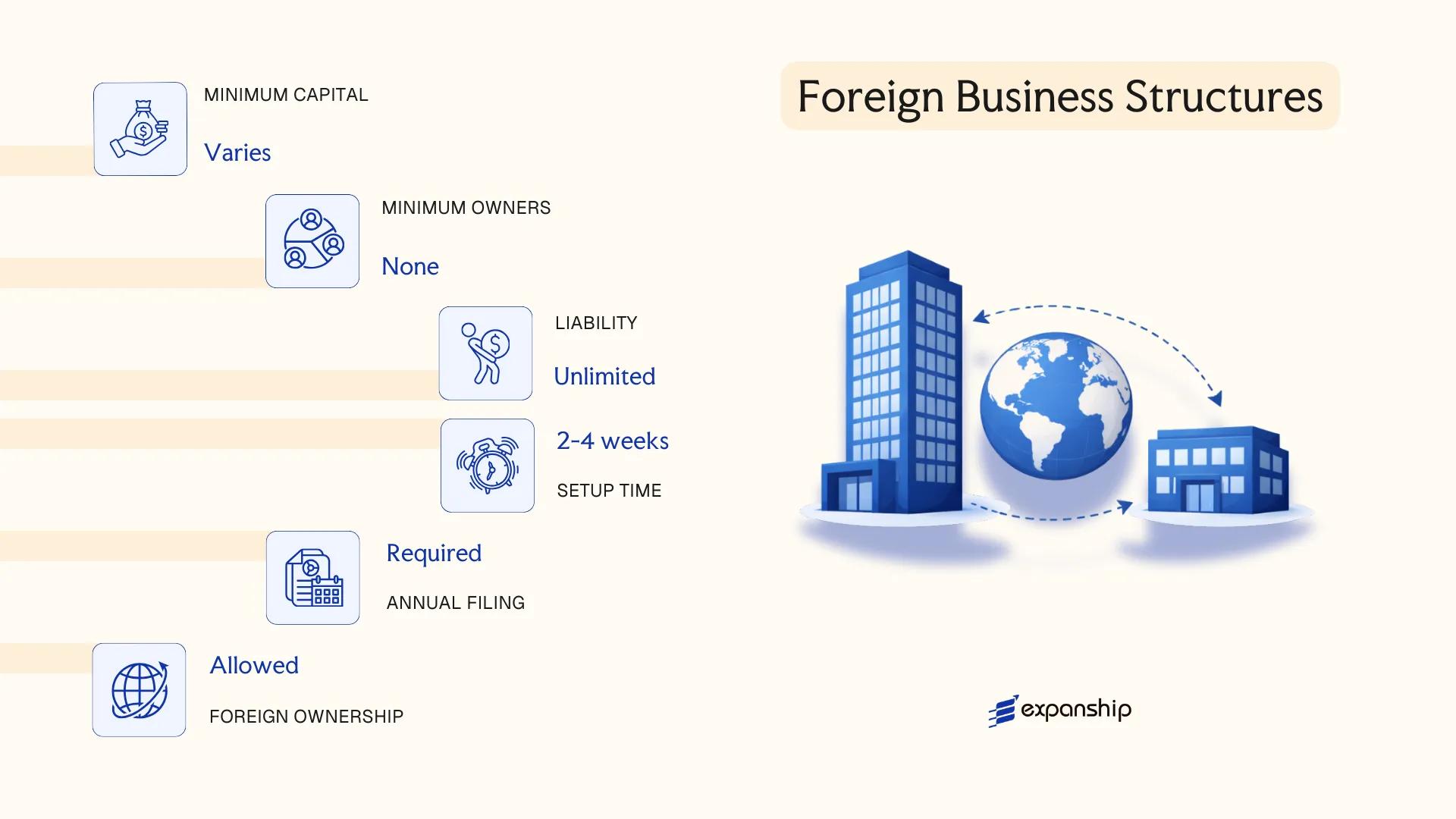

Foreign Business Structures in Sri Lanka [Branch Office, Representative Office, Liaison Office]

Registered under Part IV of the Companies Act No. 7 of 2007, a foreign company branch office in Sri Lanka does not constitute a separate legal entity — the parent company retains full liability for its operations. Foreign firms must register with the Registrar of Companies within one month of establishing a place of business in the country.

Registration requires submitting a certified copy of the parent company's charter, memorandum, articles of association, and particulars of directors and the local authorised agent. The Board of Investment (BOI) may also be involved where the foreign business qualifies for investment incentives or operates within a BOI-designated zone.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Branch of a foreign company (no separate legal personality) | Parent bears full liability |

| Local Representative | Authorised agent resident in Sri Lanka required | Must be named in registration documents |

| Registered Office | Physical address required for service of process | Cannot be a P.O. Box |

| Capital | No statutory minimum; remittances subject to Central Bank approval | Foreign exchange governed by FEMA guidelines |

| Privacy | Parent company details filed publicly with the Registrar of Companies | Limited confidentiality |

| Permitted Activities | Determined by parent's objects and BOI approval where applicable | Trading restrictions may apply by sector |

Focus Points

- Taxation: Branch profits subject to 30% corporate income tax; a branch remittance tax of 14% applies on after-tax profits transferred abroad; VAT registration required if turnover exceeds the statutory threshold; withholding tax applies to dividends, interest, and royalties paid to non-residents.

- Annual Compliance: Audited accounts of the foreign parent, along with local financial statements, must be filed annually with the Registrar of Companies.

- Restrictions: Certain sectors — including banking, insurance, and broadcasting — require separate regulatory approvals beyond standard Companies Act registration.

- Treaty Access: Sri Lanka maintains double tax agreements with over 40 countries; branch eligibility for treaty benefits depends on the specific agreement and residency of the parent.

Sub-Types

Branch Office

A branch conducts active commercial operations and is treated as a taxable presence. It generates revenue directly and is subject to full corporate income tax obligations in Sri Lanka.

Representative Office

A representative office is limited to promotional, market research, and liaison activities on behalf of the parent. It cannot conclude contracts or earn local revenue, and its registration is typically maintained through the BOI or the Registrar of Companies depending on its function.

Liaison Office

Functionally similar to a representative office, a liaison office facilitates communication between the foreign parent and local counterparts without engaging in direct commercial transactions. It carries no independent tax liability on trading income, though registration obligations under the Companies Act still apply.

When to Use This Structure

A foreign branch is typically used by firms testing the local market or serving existing clients from a parent entity's established operations. The primary advantage is the absence of a minimum capital requirement; however, full parental liability exposure and limited structural flexibility are notable drawbacks.

Foreign companies seeking an operational presence without incorporating a separate local entity, particularly where the parent's home jurisdiction has a double tax treaty with Sri Lanka.

Partnerships in Sri Lanka [Ordinary Partnership, Limited Liability Partnership]

A limited liability partnership Sri Lanka framework does not exist as a formally codified structure under current legislation. Partnerships are instead governed by the Civil Law Ordinance (as applicable to general commercial arrangements) and the Partnership Ordinance, which establishes the foundational rules for ordinary partnerships.

Unlike companies incorporated under the Companies Act No. 7 of 2007, a partnership does not carry separate legal personality. Partners bear joint and several liability for the firm's obligations, meaning personal assets remain exposed to business debts.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Ordinary Partnership | No separate legal personality; partners are personally liable |

| Members | Partners; minimum 2, no statutory maximum | Referred to as "partners" under the Partnership Ordinance |

| Local Presence | Principal place of business in Sri Lanka | No statutory registered agent requirement distinct from companies |

| Capital | No minimum capital requirement; LKR contributions by agreement | Capital terms set by the partnership deed |

| Privacy | Partnership deed is not publicly registered with a central registry | Limited public disclosure compared to companies |

Focus Points

- Taxation: Partnerships are generally taxed at the partner level under the Inland Revenue Act No. 24 of 2017; VAT registration applies if turnover thresholds are met; withholding tax obligations may apply on distributions.

- Annual Compliance: No mandatory annual return filing equivalent to companies; tax returns filed through the Inland Revenue Department.

- Restrictions: Foreign nationals face practical constraints on operating as partners in certain regulated sectors.

- Conversion: No codified conversion pathway from a partnership to a private limited company; restructuring requires dissolution and fresh incorporation.

Closing

An ordinary partnership suits small domestic trading businesses or professional arrangements where two or more individuals operate under a shared commercial agreement. The absence of minimum capital requirements offers operational flexibility, though unlimited personal liability remains a significant structural drawback.

Best suited for small-scale domestic ventures between individuals who operate in low-risk sectors and do not require the protection of limited liability.

Sole Proprietorship

Sole proprietorship registration Sri Lanka does not follow a unified national act specifically governing this structure. Instead, registration is handled at the local government level through the relevant Municipal Council, Urban Council, or Pradeshiya Sabha, depending on the business location. There is no separate legal personality — the business and its owner are treated as one and the same under the law.

Because no distinction exists between personal and business assets, the proprietor bears unlimited personal liability for all debts and obligations incurred by the business. Income from the sole proprietorship is assessed under the Inland Revenue Act No. 24 of 2017 as personal income, not as a separate corporate entity.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated individual business | No separate legal personality from the owner |

| Members | Single proprietor | No partners, shareholders, or directors |

| Local Presence | Business registration address required | Obtained through the relevant local authority |

| Capital | No statutory minimum | Funded entirely by the proprietor |

| Liability | Unlimited personal liability | Personal assets are exposed to business creditors |

| Privacy | No public filing of financials | Local authority registration records are not widely published |

Focus Points

- Taxation: Business income is taxed as personal income under the Inland Revenue Act No. 24 of 2017; VAT registration is required if annual turnover exceeds the statutory threshold; no corporate income tax applies.

- Annual Compliance: Business registration must be renewed annually with the relevant local authority; no statutory audit requirement under this structure.

- Conversion: Can be converted to a private limited company under the Companies Act No. 7 of 2007, though this requires a fresh incorporation process.

- Treaty Access: As an unincorporated structure with no separate legal personality, access to Sri Lanka's double tax treaties is generally unavailable.

- Restrictions: Foreign nationals face significant restrictions in operating as sole traders; this structure is generally reserved for Sri Lankan citizens or permanent residents.

Closing

A sole proprietorship suits small-scale, low-risk trading or service activities where the owner operates independently and administrative simplicity is a priority. The absence of statutory audit and minimal registration costs make it accessible, but unlimited personal liability remains a significant structural drawback.

Sri Lankan citizens running small local businesses or freelance operations who require a straightforward setup with minimal ongoing compliance obligations.

How to Choose the Right Entity Type in Sri Lanka

Selecting the wrong structure from the outset creates legal and financial consequences that are difficult to reverse once the entity is registered.

Why Your Entity Choice Matters

The Companies Act No. 7 of 2007 governs most corporate formations, and misalignment between your structure and your intended activity carries concrete risks:

- Registering a foreign branch to conduct local retail or services without meeting the Registrar of Companies' inward investment approval requirements places the entity in breach of the Act, which can result in penalties or striking off.

- Choosing an entity structure that does not qualify under Sri Lanka's double taxation agreements means you cannot claim withholding tax reductions available to qualifying residents under those treaties.

- Forming a private limited company when a sole proprietorship would suffice for a single-person consultancy introduces mandatory statutory obligations — including annual returns and potential audit requirements — that add recurring administrative costs with no operational benefit.

- Selecting an entity without the capacity to demonstrate real substance when the Board of Investment or tax authorities require it triggers compliance failures and potential reassessment of tax residency status.

Key Factors to Consider

- Business Activity: Active trading, passive asset-holding, and regulated sectors such as banking or insurance each require distinct entity structures under Sri Lankan law.

- Ownership Structure: A single founder can operate as a sole proprietor or one-person company, while multi-party ventures point toward a private limited company or partnership.

- Tax Objectives: Your need for treaty access, eligibility for Board of Investment incentives, or standard corporate tax treatment under the Inland Revenue Act No. 24 of 2017 will narrow your options considerably.

- Liability Exposure: The extent to which personal assets must be insulated from business liabilities determines whether an incorporated structure is necessary.

- Substance Capacity: If you cannot maintain a physical office and resident decision-making in the country, this limits which entity types are operationally viable.

- Exit and Continuity: Not all structures permit redomiciliation or conversion; if you anticipate restructuring, confirm at formation whether the chosen entity type supports that process under the Act.

Corporate Compliance Services in Sri Lanka

Maintain statutory obligations for your Sri Lanka entity, including annual returns, registered office requirements, and director filings with the Registrar of Companies.

Conclusion

Selecting the right structure is a foundational decision in any Sri Lanka company incorporation summary. The Private Limited Company remains the most frequently registered entity under the Companies Act No. 7 of 2007, suited to resident and foreign investors seeking limited liability with minimal shareholder requirements. Public Limited Companies serve businesses pursuing capital market access through the Colombo Stock Exchange. Guarantee Limited Companies fit non-profit and membership-based organisations. Unlimited liability entities are uncommon and typically reserved for specific professional arrangements. Branch and representative offices allow foreign firms to establish a presence without forming a separate legal entity.

Administered by the Registrar of Companies and, for foreign investment, the Board of Investment of Sri Lanka, the regulatory framework has been subject to ongoing modernisation. Your firm's liability exposure, ownership structure, and long-term operational intent in the jurisdiction should each factor into the final determination. Expanship's team can assist in working through those specifics.

How Expanship Can Assist You

Expanship company registration Sri Lanka services are built around the actual requirements of the Companies Act No. 7 of 2007 and the registration procedures administered by the Registrar General of Companies. From private limited companies to branch offices and guarantee companies, every entity type covered in this blog involves distinct documentation, filing obligations, and ongoing compliance responsibilities that vary in scope and complexity.

Expanship handles the full cycle of incorporation and post-registration compliance for businesses entering the Sri Lankan market.

- Preparation and legalization of incorporation documents

- Registered agent and registered office provision

- Filing with the Registrar General of Companies

- Post-incorporation compliance management, including annual returns

- Banking introduction assistance for newly incorporated entities

Reach out to Expanship Sri Lanka to discuss which structure suits your business objectives and how we can support your entry into the Sri Lankan market.

Frequently Asked Questions (FAQ)

The Private Limited Company (Ltd), governed by the Companies Act No. 7 of 2007, is the most frequently registered structure. It combines limited liability protection with relatively straightforward incorporation requirements, making it the default choice for both resident entrepreneurs and foreign investors entering the local market.

A Branch Office is an extension of its foreign parent and does not constitute a separate legal entity, meaning the parent retains full liability for its Sri Lankan operations. A Private Limited Company is incorporated as a distinct legal person under the Companies Act No. 7 of 2007, enabling it to contract, own assets, and limit shareholder liability independently. Compliance obligations for a locally incorporated entity generally exceed those of a Branch Office, though the subsidiary structure offers cleaner liability separation.

A Private Limited Company does not require public disclosure of shareholder identity in the same manner as a Public Limited Company (PLC), whose securities and ownership details face broader public scrutiny. Nominee director and shareholder arrangements are legally permissible under Sri Lankan law, allowing an additional layer of privacy for the beneficial owner.

A sole proprietorship requires only one individual. A Private Limited Company can be incorporated with a single shareholder and a single director. Partnerships, by contrast, require a minimum of two partners, making them structurally incompatible with single-person formation.

Foreign nationals may incorporate a Private Limited Company or a Public Limited Company, subject to sector-specific foreign ownership restrictions administered by the Board of Investment of Sri Lanka (BOI) and applicable industry regulators. Branch Offices and Representative Offices are also available to foreign entities already incorporated abroad, allowing operations without establishing a new local legal person.

The Companies Act No. 7 of 2007 provides mechanisms for re-registration, allowing a Private Limited Company to convert to a Public Limited Company and vice versa, subject to meeting the applicable share capital and membership thresholds. Conversion from a partnership or sole proprietorship into a limited liability structure requires a fresh incorporation rather than a statutory re-registration. The Registrar of Companies administers these processes.

No. A sole proprietorship and an ordinary partnership do not possess legal personality distinct from their owner or partners. Companies incorporated under the Companies Act No. 7 of 2007, including Private Limited, Public Limited, Guarantee Limited, and Unlimited Liability Companies, each constitute a separate legal person capable of holding property and entering contracts in their own name.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.