Key Takeaways

- The Sociedad de Responsabilidad Limitada (SL) is Spain's most registered entity type, favored by SMEs for its lower capital threshold and restrictions on share transfers.

- Company formation in Spain operates under a civil law system governed by the Registro Mercantil Central, the Ministry of Justice, and sector-specific supervisory bodies for regulated activities.

- Foreign businesses entering Spain typically establish a branch office rather than a subsidiary when conducting initial market testing.

- Under the Ley de Sociedades de Capital, the chosen legal structure directly determines a company's tax exposure, governance obligations, and exit mechanics.

Introduction to Entity Types in Spain

Spain is a sovereign nation on the Iberian Peninsula in southwestern Europe, bordered by Portugal, France, and Andorra, with additional territory in the Canary Islands, the Balearic Islands, and the autonomous cities of Ceuta and Melilla. Businesses registering here operate under a civil law system, with company formation governed by the Registro Mercantil Central — the central commercial registry — alongside the Ministry of Justice and, for certain regulated activities, sector-specific supervisory bodies.

Corporate taxation in Spain follows a standard resident-based system, with profits subject to national corporate income tax and obligations that vary by entity type and activity.

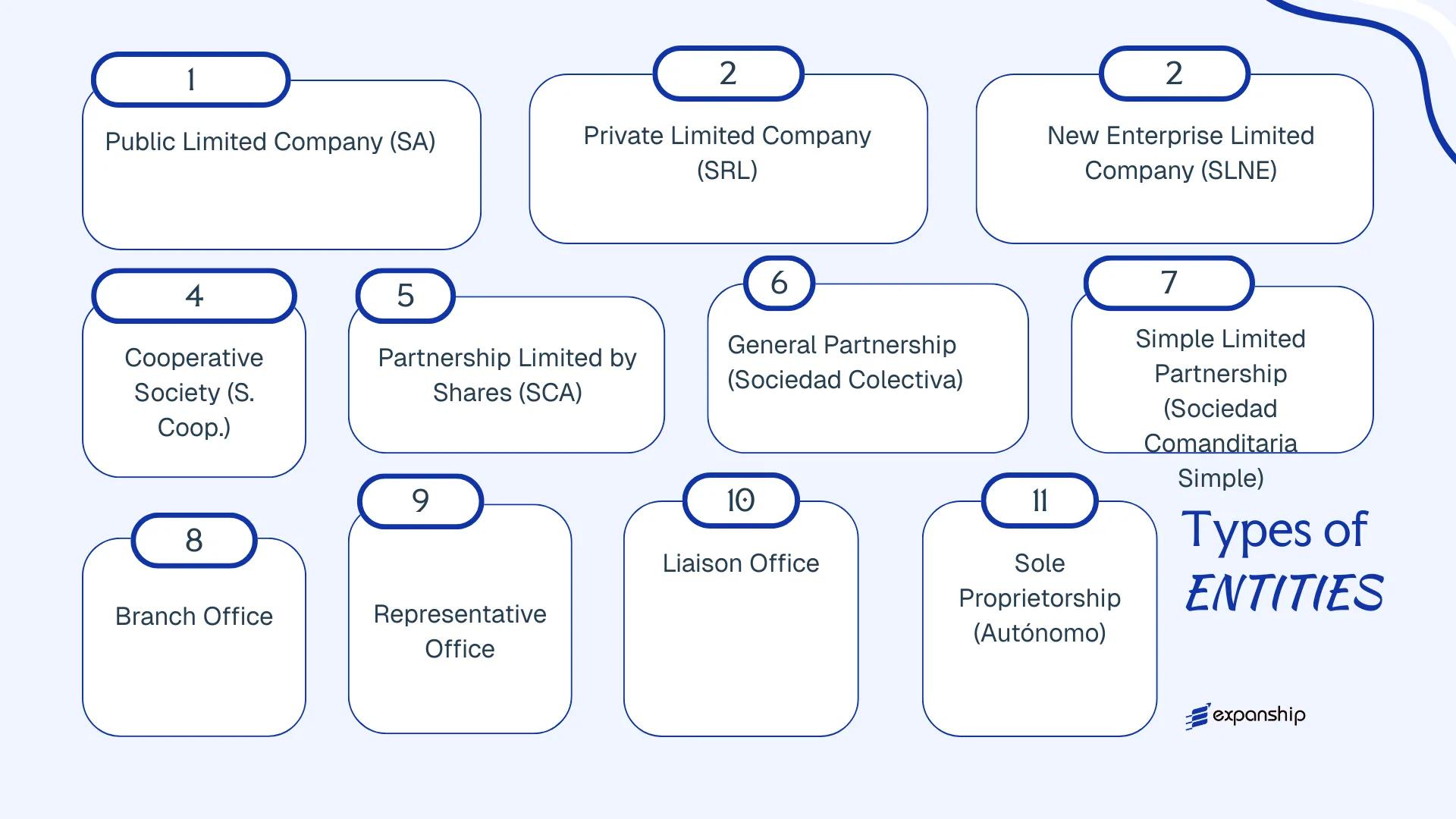

The types of business entities in Spain available to founders and foreign investors span a range of legal corporate forms, from limited liability companies to partnerships and foreign presence structures. These include the Sociedad Anónima (SA), Sociedad de Responsabilidad Limitada (SL), Sociedad Limitada Nueva Empresa (SLNE), Sociedad Cooperativa, Sociedad Comanditaria por Acciones, Sociedad Colectiva, Sociedad Comanditaria Simple, branch offices, representative offices, liaison offices, and the Empresario Individual. Each structure carries distinct implications for liability, governance, and capital requirements, all of which this article examines in detail.

An Overview of Business Structures in Spain

Spanish corporate law recognises multiple entity types, each governed primarily by the Ley de Sociedades de Capital (Royal Legislative Decree 1/2010), which consolidates the rules for capital-based companies, alongside separate legislation covering cooperatives, partnerships, and sole traders. The business structures in Spain overview below captures the full range of legal forms available to domestic and foreign operators. Each entity serves a distinct commercial purpose, ownership structure, and liability profile.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Tax Treatment | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Sociedad Anónima (SA) | Public Limited Company | Limited | Corporate tax liable | Permitted | 1 shareholder | Registro Mercantil | RDL 1/2010 |

| Sociedad de Responsabilidad Limitada (SL) | Private Limited Company | Limited | Corporate tax liable | Permitted | 1 shareholder | Registro Mercantil | RDL 1/2010 |

| Sociedad Limitada Nueva Empresa (SLNE) | Simplified Private Ltd. | Limited | Corporate tax liable | Permitted | 1–5 founders | Registro Mercantil | RDL 1/2010 |

| Sociedad Cooperativa (S. Coop.) | Cooperative Society | Limited | Partially exempt | Permitted | Varies by region | Registro de Cooperativas | Ley 27/1999 |

| Sociedad Comanditaria por Acciones (SCA) | Partnership Ltd. by Shares | Mixed | Corporate tax liable | Permitted | 2+ partners | Registro Mercantil | RDL 1/2010 |

| Sociedad Colectiva | General Partnership | Unlimited | Pass-through | Permitted | 2+ partners | Registro Mercantil | Código de Comercio |

| Sociedad Comanditaria Simple | Limited Partnership | Mixed | Pass-through | Permitted | 2+ partners | Registro Mercantil | Código de Comercio |

| Branch Office | Foreign Entity Extension | Parent liable | Corporate tax liable | Permitted | N/A | Registro Mercantil | RDL 1/2010 |

| Representative Office | Non-trading presence | Parent liable | Generally exempt | Not permitted | N/A | Agencia Tributaria | General tax rules |

| Empresario Individual / Autónomo | Sole Proprietorship | Unlimited | Personal income tax | Permitted | 1 individual | Agencia Tributaria | Código de Comercio |

Each of these structures is examined in full in the sections below.

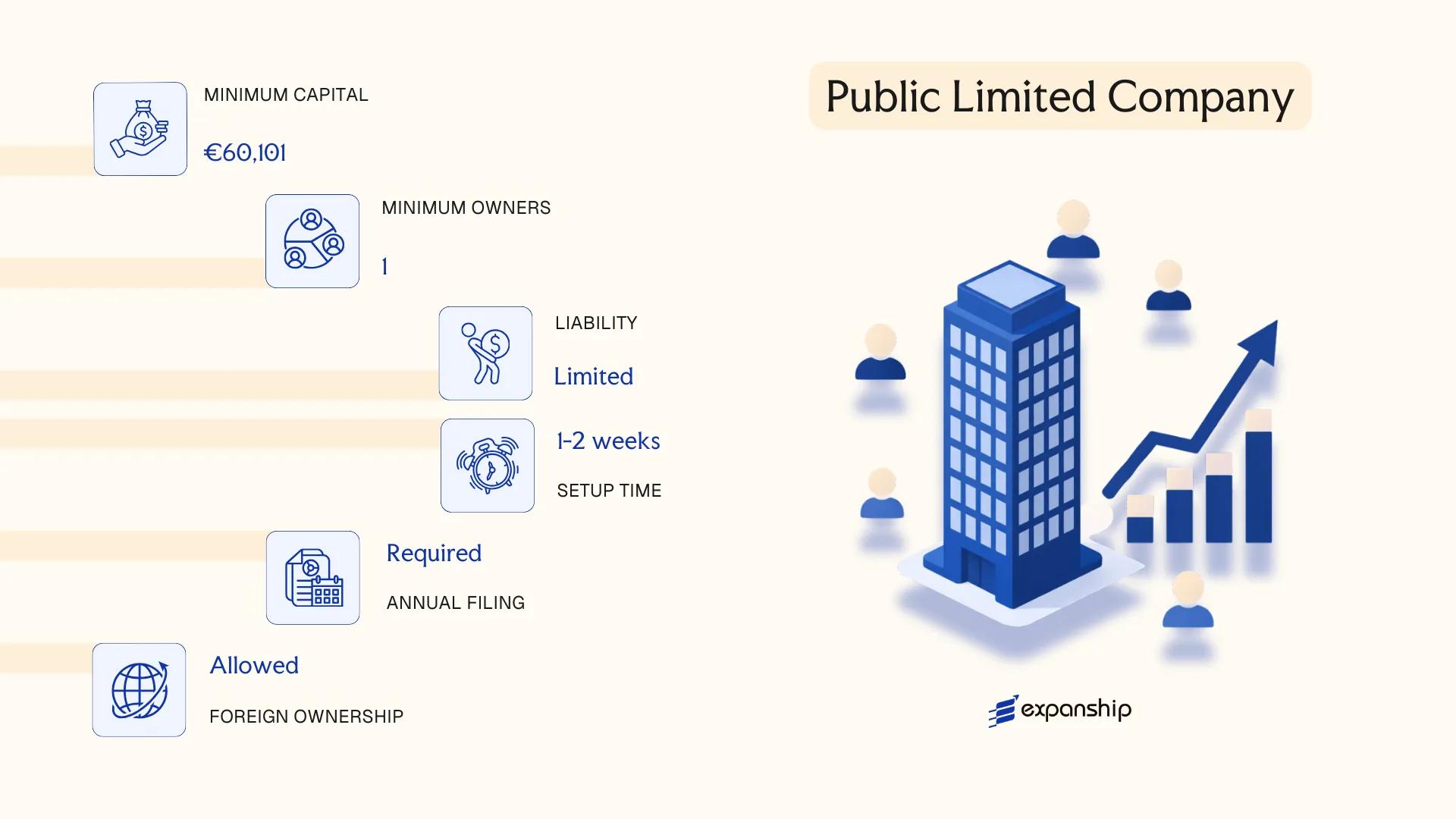

Sociedad Anónima (SA) — Public Limited Company

Governed by the Ley de Sociedades de Capital (Royal Legislative Decree 1/2010), the Sociedad Anónima is Spain's most formally structured corporate vehicle. It carries a separate legal personality, meaning the entity's obligations remain distinct from those of its shareholders.

Capital is divided into publicly transferable shares, which distinguishes the SA from closely held structures. Shareholder liability is limited to the amount subscribed, though the regulatory and disclosure requirements attached to this form reflect its suitability for larger operations and potential public listings.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sociedad Anónima (SA) | Separate legal personality; governed by RDL 1/2010 |

| Members | Shareholders (minimum 1; no maximum) | Single-shareholder SA is permitted; referred to as "Sociedad Anónima Unipersonal" |

| Management | Board of Directors or Sole Administrator | Board required if more than 2 directors; minimum 3 board members |

| Minimum Capital | EUR 60,000 | At least 25% must be paid up at incorporation; remainder within 5 years |

| Local Presence | Registered office (domicilio social) in Spain required | No mandatory local director requirement under general rules |

| Share Transfers | Freely transferable by default | Restrictions may be introduced via articles of association (estatutos) |

| Privacy | Shareholders disclosed in public registry | Financial accounts filed with the Registro Mercantil annually |

Focus Points

- Taxation: Subject to Corporate Income Tax (*Impuesto sobre Sociedades*) at the standard 25% rate; VAT obligations apply to taxable supplies; dividends paid to non-residents may attract withholding tax, reducible under applicable EU directives or bilateral tax treaties.

- Annual Compliance: Audited accounts are mandatory once the entity exceeds two of three thresholds (assets over EUR 2.85M, turnover over EUR 5.7M, more than 50 employees); annual accounts must be filed with the Registro Mercantil within seven months of the financial year-end.

- Treaty Access: As a tax-resident entity, the SA can access Spain's extensive network of double taxation agreements.

- Conversion: An SA may be converted into an SL or other recognised form via a formal restructuring process requiring notarial deed and registry inscription.

- Restrictions: Certain regulated sectors (banking, insurance) impose additional capital or licensing requirements beyond the standard corporate framework.

Closing

The SA suits businesses anticipating external investment, public capital markets activity, or high-volume trading operations where transferable share structures are commercially necessary. The principal drawback is administrative burden — ongoing audit obligations, strict capital maintenance rules, and public disclosure requirements add meaningful compliance costs relative to simpler forms.

The SA is best suited for large enterprises, joint ventures with institutional investors, or businesses planning a future stock exchange listing.

Company Incorporation in Spain

Incorporate your Sociedad Anónima or other Spanish entity with end-to-end support from registry filing to post-incorporation compliance.

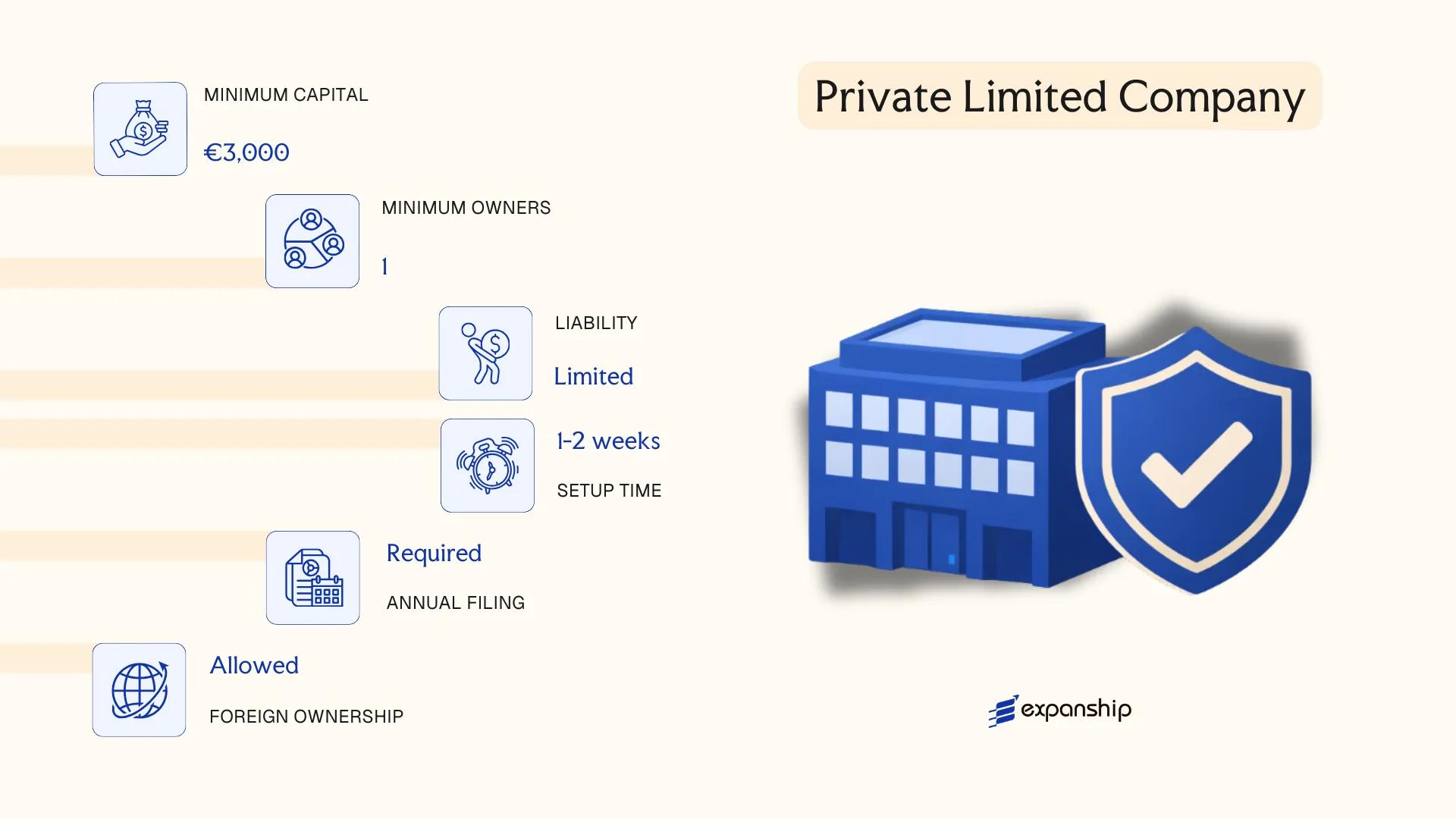

Sociedad de Responsabilidad Limitada (SRL/SL) — Private Limited Company

The Sociedad de Responsabilidad Limitada SL Spain is governed by the Ley de Sociedades de Capital (Royal Legislative Decree 1/2010), which consolidated the prior Ley 2/1995 framework into a unified companies statute. As a separate legal entity, the SL shields its members from personal liability beyond their capital contributions.

Structurally, the SL occupies a middle ground between a sole proprietorship and a public company. Ownership is divided into participaciones (non-transferable quotas rather than freely tradable shares), and transfers to third parties outside the membership are subject to pre-emption rights and, in some cases, member approval.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sociedad de Responsabilidad Limitada (SL / SRL) | Separate legal personality; limited liability |

| Members | Referred to as socios (partners/members); minimum 1, no maximum | A single-member SL is a Sociedad Unipersonal and must be registered as such with the Mercantile Registry |

| Management | Administrador (sole), Administradores solidarios/mancomunados (joint), or Consejo de Administración (board) | Directors need not be shareholders; non-resident directors permitted |

| Capital | Minimum EUR 3,000; fully subscribed and paid-up at incorporation | Held in participaciones; no public offering permitted |

| Local Presence | Registered office (domicilio social) in Spain required | Must be a real, operational address; a registered agent address may satisfy this |

| Privacy | Shareholder identity filed with the Mercantile Registry; publicly searchable | Beneficial ownership reported to the Central Registry of Beneficial Owners (Registro de Titularidades Reales) |

Focus Points

- Taxation: Subject to Impuesto sobre Sociedades (corporate income tax) at 25% standard rate (15% for newly formed entities in the first two profitable years); VAT (IVA) applies to taxable supplies; dividends and interest paid abroad attract withholding tax, reducible under applicable tax treaties; no stamp duty on capital contributions since 2010.

- Annual Compliance: Annual accounts filed with the Mercantile Registry; statutory audit required if two of three thresholds (assets, turnover, employees) are exceeded for two consecutive years.

- Economic Substance: No formal substance test, but tax residency and sede de dirección efectiva (place of effective management) determine treaty access and CFC exposure.

- Conversion: An SL may convert to a Sociedad Anónima (SA) or other recognised form under Articles 3–21 of the Ley de Sociedades de Capital without dissolving.

- Transfer Restrictions: Quota transfers to non-members require prior member consent per the articles; freely negotiated transfer restrictions can be embedded in the estatutos sociales.

Sub-Types

Sociedad Limitada de Formación Sucesiva (SLFS)

Introduced by Law 14/2013, the SLFS allows incorporation with capital below EUR 3,000, down to EUR 1. Until share capital reaches EUR 3,000, the entity faces restrictions on profit distribution and statutory reserve allocation to protect creditors.

Sociedad Unipersonal de Responsabilidad Limitada

A single-member variant of the standard SL. The sole-member status must be registered in the Mercantile Registry within three months of establishment; contracts between the sole member and the company require written form and disclosure in the annual accounts.

The SL is widely used for trading subsidiaries, holding structures, and SME operations where closely held ownership and transfer control matter. Capital requirements are low relative to the SA, but the restriction on freely transferable quotas limits its suitability for businesses anticipating multiple investment rounds or broad equity distribution.

The SL suits small-to-medium enterprises, family-owned businesses, and foreign subsidiaries requiring a straightforward corporate structure with contained compliance costs.

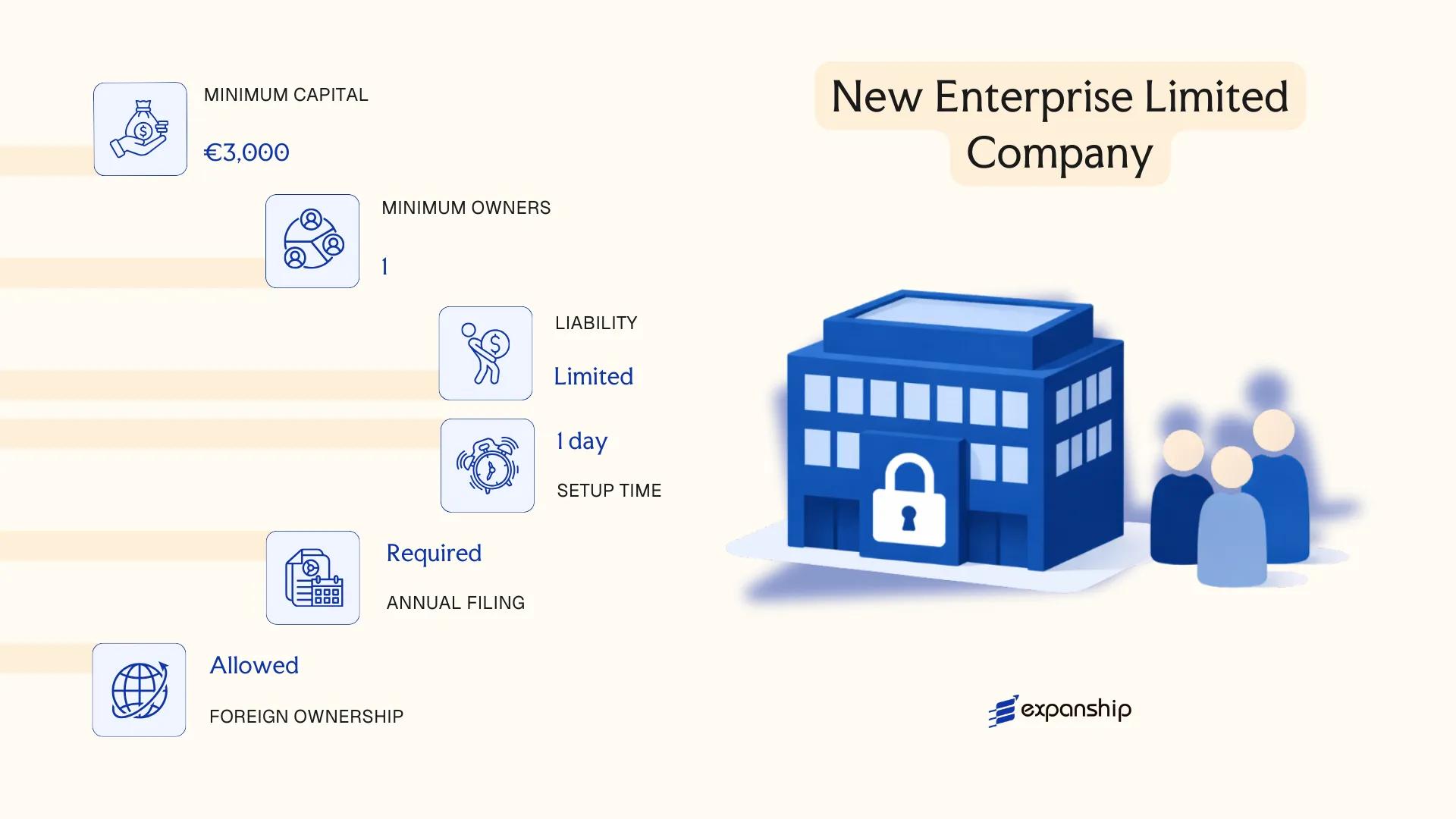

Sociedad Limitada Nueva Empresa (SLNE) — New Enterprise Limited Company

The Sociedad Limitada Nueva Empresa (SLNE Spain) is a simplified variant of the standard SL, introduced through Law 7/2003 to reduce incorporation timelines and administrative friction for small business founders. It carries full separate legal personality and grants shareholders limited liability capped at their capital contributions.

Structurally, the SLNE follows the same foundational rules as a standard SL under the Ley de Sociedades de Capital, but layers on procedural shortcuts designed specifically for fast incorporation in Spain through the Centro de Información y Red de Creación de Empresas (CIRCE) system.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sociedad Limitada Nueva Empresa | Governed by Law 7/2003 and the Ley de Sociedades de Capital |

| Members | Shareholders (socios); max 5 at founding | Only natural persons permitted as founding shareholders |

| Capital | EUR 3,000 minimum; EUR 120,000 maximum | Must be fully paid up at incorporation |

| Registered Office | Required in Spain | Must be maintained throughout the entity's life |

| Corporate Name | Must include founder's name and a numeric code | Name format is prescribed by statute |

| Privacy | Shareholders listed in public registry | Beneficial ownership registered with the Registro Mercantil |

Focus Points

- Taxation: Subject to corporate income tax at 15% for the first two taxable periods with positive income (new entity rate), then 25%; VAT obligations apply from the first taxable supply; no specific withholding tax exemptions beyond standard SL rules.

- Annual Compliance: Annual accounts must be filed with the Registro Mercantil; a statutory audit is generally not required below the standard SL thresholds.

- Conversion: An SLNE can be converted into a standard SL by shareholder resolution without dissolution, making it a transitional structure for growing firms.

- Restrictions: Founding shareholders must be natural persons; legal entities cannot participate at formation.

- Economic Substance: No special substance requirements beyond maintaining a registered office and conducting genuine commercial activity.

Closing Paragraph

The SLNE suits early-stage founders who need a legally recognised entity quickly, particularly sole founders or small teams seeking fast incorporation in Spain without the capital burden of an SA. Its shareholder cap and name format restrictions, however, limit scalability once the business grows or requires institutional investors.

Early-stage individual entrepreneurs or small founding teams of up to five natural persons who need a low-capital, rapid-incorporation structure with a clear path to convert into a full SL later.

Sociedad Cooperativa (S. Coop.) — Cooperative Society

Sociedad Cooperativa Spain registration follows a dual legislative framework: state-level cooperatives are governed by Ley 27/1999, de 16 de julio, de Cooperativas, while autonomous communities such as Catalonia, the Basque Country, and Andalusia maintain their own cooperative laws that may supersede the national statute. The entity carries full legal personality upon registration in the Registro de Cooperativas.

Structured around member participation rather than capital contribution, a cooperative distributes economic activity and surplus among its members. Liability is generally limited to each member's subscribed contribution, though statutes may provide otherwise.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sociedad Cooperativa (S. Coop.) | Separate legal personality; member-driven structure |

| Members | Referred to as socios; minimum 3 founding members | No statutory maximum; class distinctions (ordinary vs. associate socios) permitted |

| Governing Body | Consejo Rector (Board) + Asamblea General | Asamblea General holds supreme authority |

| Capital | No fixed national minimum; set by statutes | Capital is variable by nature; mandatory Reserve Fund (Fondo de Reserva Obligatorio) required |

| Local Presence | Registered office (domicilio social) required in Spain | Must correspond to actual principal activity or administration |

| Privacy | Member register not publicly searchable | Statutes and Consejo Rector composition filed with Registro de Cooperativas |

Focus Points

- Taxation: Subject to corporate income tax (Impuesto sobre Sociedades) at a reduced rate of 20% for fiscally protected cooperatives; standard VAT (IVA) applies; surplus distributions (retornos cooperativos) receive preferential tax treatment compared to dividends.

- Annual Compliance: Annual accounts filed with the Registro de Cooperativas; mandatory audit thresholds apply; Asamblea General must convene within six months of year-end.

- Economic Substance: Activity must genuinely reflect the cooperative's mutual purpose; regulatory scrutiny increases if commercial operations diverge from member-benefit objectives.

- Conversion: Conversion to a Sociedad Limitada or Sociedad Anónima is permitted under Ley 3/2009 on structural modifications, subject to member approval and creditor notification.

- Restrictions: Non-member third-party operations are permitted but capped; exceeding those thresholds can result in loss of fiscally protected status.

Sub-Types

Cooperativa de Trabajo Asociado (Worker Cooperative)

Members are also the workers; this structure is used by professional collectives and artisan groups where labour contribution, not capital, defines membership.

Cooperativa de Consumidores y Usuarios (Consumer Cooperative)

Organised to supply goods or services to its members at cost; commonly used in retail, housing, and utilities sectors.

Cooperativa de Crédito (Credit Cooperative)

Operates financial services exclusively for members and is subject to additional supervision by the Banco de España alongside standard cooperative legislation.

Cooperativa de Segundo Grado

Formed by two or more cooperatives as member-entities rather than individuals; used to consolidate operations or access shared resources across multiple primary cooperatives. Other recognised sub-types include agricultural cooperatives (Cooperativas Agrarias) and housing cooperatives (Cooperativas de Viviendas).

Closing

A cooperative structure suits businesses built around shared economic activity among members, particularly in sectors such as agriculture, professional services, consumer goods, and worker-owned enterprises. The principal advantage is the preferential corporate tax rate available to fiscally protected cooperatives; the key limitation is administrative complexity, as compliance obligations span both national and regional regulatory frameworks simultaneously.

Best suited for groups of professionals, workers, or producers seeking a democratic governance structure with shared economic participation rather than a conventional investor-driven ownership model.

Sociedad Comanditaria por Acciones (SCA) — Partnership Limited by Shares

The Sociedad Comanditaria por Acciones Spain structure is governed by the Ley de Sociedades de Capital (Royal Legislative Decree 1/2010), the same consolidated text that regulates the SA and SL. It carries separate legal personality and represents a hybrid form: general partners bear unlimited personal liability for company obligations, while limited partners hold transferable shares and are exposed only to the extent of their subscribed capital.

Capital is divided into shares rather than participaciones, which makes transfer mechanics more similar to those of an SA than an SL. At least one general partner must assume management, and that same partner bears unlimited liability — a structural feature that distinguishes this entity from purely capital-based forms.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sociedad Comanditaria por Acciones (SCA) | Hybrid partnership-company with separate legal personality |

| Members | Min. 1 general partner (socio colectivo) + min. 1 limited partner (socio comanditario); no statutory maximum | General partners manage and bear unlimited liability; limited partners hold shares only |

| Capital | Min. €60,000; divided into shares (acciones) | Same minimum as the SA; at least 25% must be paid up at incorporation |

| Local Presence | Registered office in Spain required | No statutory requirement for a resident director, but general partners typically must be accessible |

| Management | Conducted exclusively by general partners | Limited partners cannot manage without forfeiting their limited liability status |

| Privacy | Deed of incorporation filed with the Mercantile Registry (Registro Mercantil) | Names of general partners are publicly disclosed |

Focus Points

- Taxation: Subject to Spanish Corporate Income Tax (Impuesto sobre Sociedades) at the standard 25% rate; VAT obligations apply under standard rules; dividends paid to non-resident partners may be subject to withholding tax, reducible under applicable double tax treaties.

- Annual Compliance: Annual accounts must be prepared, audited where thresholds are met, and filed with the Registro Mercantil; general partners sign off on accounts.

- Treaty Access: As a Spanish-resident legal entity, the SCA can access Spain's double tax treaty network, subject to beneficial ownership and substance conditions.

- Conversion: Can be converted to an SA or SL under the Ley 3/2009 on structural modifications, provided statutory procedures and creditor protection rules are observed.

- Restrictions: Limited partners who participate in management risk losing their liability protection under the Código de Comercio provisions applicable to this structure.

Closing

The SCA suits investment fund structures, family-held enterprises, or arrangements where a controlling partner requires management authority while outside investors hold shares with limited exposure. The transferability of shares offers more flexibility than standard partnership forms, though the unlimited liability borne by general partners remains a significant structural constraint that deters most commercial operators.

Best suited for family business groups or investment vehicles where a defined managing partner accepts unlimited liability in exchange for full operational control, and passive investors require freely transferable share interests.

Partnerships [Sociedad Colectiva, Sociedad Comanditaria Simple]

Both the Sociedad Colectiva and the Sociedad Comanditaria Simple are governed by the Spanish Commercial Code (Código de Comercio) of 1885, which remains the foundational legislation for these structures. Each form carries separate legal personality upon registration with the Mercantile Registry (Registro Mercantil).

Sociedad Colectiva and Comanditaria Simple Spain represent the oldest partnership forms under Spanish commercial law. Unlike capital companies, both structures impose unlimited personal liability on at least one category of partner, making them structurally distinct from the SL or SA.

Key Characteristics

| Requirement | Sociedad Colectiva | Sociedad Comanditaria Simple |

|---|---|---|

| Legal Form | General Partnership | Simple Limited Partnership |

| Members | Partners (socios colectivos), minimum 2, no maximum; all bear unlimited liability | General partners (socios colectivos) with unlimited liability + limited partners (socios comanditarios) with liability capped at their contribution; minimum 2 total |

| Minimum Capital | No statutory minimum | No statutory minimum |

| Local Presence | Registered office in Spain required; no mandatory resident director rule | Registered office in Spain required |

| Management | All general partners manage collectively unless the partnership deed delegates otherwise | Only general partners may manage; limited partners are excluded from management |

| Privacy | Partnership deed (escritura pública) filed publicly at the Mercantile Registry | Same public filing requirement applies |

Focus Points

- Taxation: Both structures are fiscally transparent under Spain's Ley del Impuesto sobre la Renta de No Residentes and Ley 35/2006; income passes through to partners and is taxed at the partner level rather than at the entity level, though withholding obligations may apply to non-resident partners.

- Annual Compliance: Annual accounts must be deposited at the Mercantile Registry; neither form benefits from simplified reporting regimes available to micro-entities under the SL framework.

- Treaty Access: Pass-through treatment may complicate access to Spain's tax treaty network, as treaty eligibility depends on the partner's own residency status.

- Conversion: Either structure can be converted into a capital company (sociedad de capital) through a formal deed of transformation filed with the Mercantile Registry, subject to creditor notification requirements.

Sub-Types

Sociedad Colectiva

All partners hold equal management rights and bear joint, unlimited, and personal liability for partnership debts. This form is typically used by professional firms or family businesses where all participants actively manage operations.

Sociedad Comanditaria Simple

General partners retain unlimited liability and management control, while limited partners contribute capital without participating in management. Their liability is capped at their agreed contribution, offering a degree of investor protection absent in the Colectiva.

Closing

These structures suit small, closely held operations where partners prioritise operational control and accept personal liability exposure. The primary advantage is structural simplicity with no minimum capital threshold; the clear limitation is the unlimited liability borne by general partners, which creates significant personal financial risk.

Family businesses or professional partnerships with a small number of trusted principals who are prepared to assume personal liability for business obligations.

Foreign Presence Options [Branch Office, Representative Office, Liaison Office]

A foreign company branch office Spain setup is governed primarily by Royal Legislative Decree 1/2010 (the Companies Act, Ley de Sociedades de Capital) and supplemented by the Commercial Code. Unlike a subsidiary, a branch (sucursal) does not constitute a separate legal entity — it remains an extension of the parent company, which bears full liability for its obligations.

Registration is handled through the Mercantile Registry (Registro Mercantil), and the branch must appoint a resident representative with sufficient powers of attorney. Representative offices and liaison offices operate under a narrower legal footing, restricted to promotional or coordination activities without generating taxable income in Spain.

Key Characteristics

| Requirement | Branch (Sucursal) | Representative / Liaison Office |

|---|---|---|

| Legal Personality | None — extension of parent | None — extension of parent |

| Commercial Activity | Permitted | Not permitted |

| Registration Body | Mercantile Registry | Tax Agency (AEAT) registration only |

| Local Representative | Mandatory (resident, notarised power of attorney) | Recommended |

| Capital Requirement | None | None |

| Tax Registration | Required (NIF assigned) | Required if staff present |

| Privacy | Parent company details publicly filed | Limited public disclosure |

Focus Points

- Taxation: Branches are subject to Corporate Income Tax (Impuesto sobre Sociedades) at 25% on Spanish-sourced profits; a branch profit remittance tax may apply under certain tax treaties, though EU parent companies often qualify for exemption. VAT registration is required for taxable supplies.

- Substance: A branch must maintain a fixed place of business and an appointed representative; liaison offices must not conduct revenue-generating activity or their status is reclassified.

- Annual Compliance: Branches must file annual accounts derived from the parent's financials with the Mercantile Registry and submit Spanish corporate tax returns independently.

- Treaty Access: Access to Spain's tax treaty network depends on the parent company's jurisdiction of residence, not the branch itself.

- Restrictions: Liaison and representative offices cannot sign commercial contracts, invoice clients, or remit profits — activities that would require conversion to a branch or subsidiary.

Closing Paragraph

A branch suits foreign firms testing the Spanish market or executing specific contracts without establishing a fully autonomous local entity, though the parent's unlimited exposure to Spanish liabilities is a significant structural drawback.

Best suited for established foreign companies with existing operations seeking a direct commercial presence in Spain without the overhead of incorporating a separate legal entity.

Empresario Individual / Autónomo — Sole Proprietorship

Autónomo sole trader registration Spain falls under no single codifying statute; instead, the legal framework draws from the Estatuto del Trabajo Autónomo (Law 20/2007) and general provisions of the Spanish Commercial Code. Unlike corporate structures, the empresario individual carries no separate legal personality — the individual and the business are legally the same person, meaning personal assets are directly exposed to business liabilities.

Registration is handled through the Agencia Tributaria (AEAT) for tax purposes and the Tesorería General de la Seguridad Social (TGSS) for mandatory social security enrolment under the RETA (Régimen Especial de Trabajadores Autónomos). Both registrations are required before commencing any commercial activity.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sole Proprietorship (no separate legal entity) | Individual and business are legally indistinguishable |

| Member Type | Proprietor | Single natural person only; no corporate sole traders |

| Local Presence | Spanish fiscal address required | Must be a physical address; a P.O. box does not qualify |

| Capital | No minimum capital requirement | No paid-up capital obligation at incorporation |

| Liability | Unlimited personal liability | Personal assets, including jointly owned property, may be at risk |

| Privacy | Name appears publicly in tax and commercial registrations | No anonymity available to the proprietor |

Focus Points

- Taxation: Subject to personal income tax (IRPF) on net business income at progressive rates up to 47%; VAT (IVA) registration and quarterly filing apply to most activities; no corporate tax applies.

- Social Security: Mandatory RETA contributions are compulsory from the first day of activity, with monthly flat-rate schemes available to new registrants for up to 24 months.

- Annual Compliance: Quarterly IRPF and IVA declarations, plus an annual income tax return filed with AEAT; no requirement to file accounts at the Mercantile Registry.

- Conversion: Can convert to an SL by transferring business assets, though the process requires a notarial deed and tax assessment of transferred assets.

- Restrictions: Cannot issue shares, bring in equity partners, or limit personal liability without restructuring into a separate legal entity.

Closing Paragraph

This structure suits freelancers, sole consultants, and small traders who operate without co-owners and keep overheads low. The absence of minimum capital and simplified accounting obligations reduce administrative burden, but unlimited personal liability remains the structure's defining constraint for any business carrying meaningful financial risk.

Best suited for individual professionals and sole traders operating low-risk activities who do not require liability protection or external investment.

How to Choose the Right Entity Type in Spain

Knowing how to choose a company type in Spain before you register prevents structural problems that are difficult and costly to correct after incorporation.

Why Your Entity Choice Matters

The structure you select has binding legal and financial consequences from the moment of registration.

- Forming a Sociedad Anónima when your business qualifies as a small enterprise triggers mandatory annual audit requirements under the Ley de Sociedades de Capital (Real Decreto Legislativo 1/2010), adding accounting costs that a Sociedad Limitada would not incur.

- Registering a foreign branch rather than an independent subsidiary means the parent company retains unlimited liability for the branch's obligations under Spanish commercial law.

- Selecting an entity ineligible for Spain's tax treaty network prevents your business from claiming reduced withholding rates on dividends, interest, or royalties paid to non-resident counterparties.

- Choosing a structure without adequate substance capacity when economic substance rules apply exposes your firm to reporting failures and potential sanctions under anti-avoidance provisions.

Key Factors to Consider

- Business Activity: Active trading, passive asset-holding, and regulated sectors each point toward a different entity — financial intermediaries face additional authorisation requirements from the Comisión Nacional del Mercado de Valores (CNMV).

- Ownership Structure: A single-founder consultancy has no functional need for the governance mechanisms required of a multi-shareholder SA.

- Tax Objectives: Your eligibility for the patent box regime, the Beckham Law provisions for inbound executives, or treaty benefits depends on which entity type you register.

- Liability Exposure: Unlimited personal liability under a Sociedad Colectiva is structurally incompatible with high-risk commercial operations.

- Exit Strategy: Not all entity types in Spain permit redomiciliation or cross-border conversion; verify this before formation if future restructuring is foreseeable.

- Substance Capacity: If you cannot maintain a genuine operational presence, choose a structure with lower substance thresholds to avoid compliance failures.

Compliance Services for Companies in Spain

Ongoing compliance support for Spanish entities, including annual filings, accounting obligations, and regulatory reporting.

Conclusion

Spain offers one of the more clearly delineated menus of legal structures in the EU, and completing a setting up a company in Spain guide requires understanding how each form maps to a specific ownership profile and commercial purpose. The Sociedad de Responsabilidad Limitada is the most registered entity type, favored by small and medium-sized businesses for its lower capital threshold and transfer restrictions. The Sociedad Anónima suits publicly listed or large-capital ventures; the SLNE serves first-time founders seeking an accelerated registration path. Cooperatives function where member-owned governance takes priority. Partnerships carry unlimited liability and are rare in practice. Foreign groups typically enter through a branch rather than a subsidiary when testing the market.

Registered with the Mercantile Registry and governed under the Ley de Sociedades de Capital, your chosen structure determines tax exposure, governance obligations, and exit mechanics. Spain continues to expand its tax treaty network, which affects holding and financing structures over time. Expanship works through each of these variables with you directly.

How Expanship Can Assist You

Expanship's company formation services Spain cover every entity type discussed in this guide — from registering a Sociedad de Responsabilidad Limitada (SL) with the Registro Mercantil Central to obtaining a tax identification number (NIF) for a branch office through the Agencia Tributaria. Your chosen structure determines which filings, timelines, and capital requirements apply, and Expanship handles that process with jurisdiction-specific precision.

From initial document preparation to ongoing post-incorporation obligations, our Spain business setup assistance covers:

- Document preparation, notarization, and legalization

- Registered agent and registered office provision

- Filing with the Registro Mercantil and liaison with Spanish authorities

- Tax registration and social security enrollment coordination

- Post-incorporation compliance management, including annual accounts and corporate book maintenance

- Banking introduction assistance for corporate account opening in Spain

Get in touch with Expanship Spain to discuss which structure fits your business objectives.

Frequently Asked Questions (FAQ)

The Sociedad de Responsabilidad Limitada (SL) is the most frequently incorporated entity in Spain. Its lower minimum capital requirement of EUR 3,000 and simplified governance structure make it accessible to small and mid-sized businesses alike.

Both structures offer limited liability, but they differ considerably in compliance burden and capital requirements. An SA requires EUR 60,000 in share capital and is subject to more rigorous auditing obligations, while an SL prohibits the free transfer of shares without member consent. For foreign investors focused on closely held operations, the SL typically entails lower administrative overhead.

Among Spanish entities, the SL provides relatively more discretion, as shareholder details are filed with the Registro Mercantil but are not prominently publicised. Nominee shareholder arrangements are legally permissible under Spanish law, though beneficial ownership must still be disclosed to authorities under anti-money laundering regulations transposed from EU Directive 2018/843.

No. A Sociedad Colectiva and Sociedad Comanditaria Simple each require at least two partners by definition. The SL and SA, by contrast, can each be formed by a sole founder, resulting in a Sociedad Unipersonal, which must be noted in the Registro Mercantil.

Non-residents may incorporate an SL, SA, or branch office without holding Spanish residency. A foreigner must obtain a Número de Identificación de Extranjero (NIE) before executing the public deed of incorporation before a Spanish notary. Operating as an Autónomo, however, generally requires residency or a valid work permit.

Spanish corporate law, governed primarily by the Ley de Modificaciones Estructurales de las Sociedades Mercantiles (Law 3/2009), permits structural transformations including conversion of an SL into an SA and vice versa. The process requires notarial deed, shareholder approval, and registration with the Registro Mercantil. Conversion from a cooperative or partnership into a capital company follows a distinct procedural path under the same statute.

Not all. The SL, SA, SLNE, SCA, and Sociedad Cooperativa each hold separate legal personality distinct from their members. Sociedad Colectiva partners, by contrast, bear unlimited personal liability, and the firm does not fully shield personal assets from business creditors.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.