Key Takeaways

- Under the Swiss Code of Obligations, forming an Aktiengesellschaft (AG) requires a minimum paid-in capital of CHF 100,000, creating an immediate liquidity burden before a single transaction is executed.

- Foreign-owned entities must secure at least one Swiss-resident director with signatory authority, a structural requirement that adds ongoing recruitment and governance costs for non-resident founders.

- Businesses operating in financial services face a dual compliance layer, satisfying both Swiss Anti-Money Laundering Act (AMLA) obligations and direct FINMA oversight, which demands dedicated legal and compliance resources from the outset.

- Switzerland's corporate and regulatory documentation spans four official languages — German, French, Italian, and Romansh — across cantonal and federal jurisdictions, meaning legal and administrative costs are systematically higher than in single-language regulatory environments.

Switzerland operates under one of the more heavily regulated corporate frameworks in continental Europe, governed primarily by the Swiss Code of Obligations. For foreign investors evaluating the disadvantages of incorporating in Switzerland, that regulatory density translates into concrete operational and financial friction across several distinct categories.

The challenges covered in this article span capital requirements, director residency rules, compliance obligations, and sector-specific oversight, among others. Not all of these will apply equally to every business — a sole-activity holding entity faces a materially different burden than a fintech firm or a staffed subsidiary.

This article is most relevant to non-resident founders, foreign-owned enterprises, and international entrepreneurs planning to establish an operational presence or registered entity in the country for the first time.

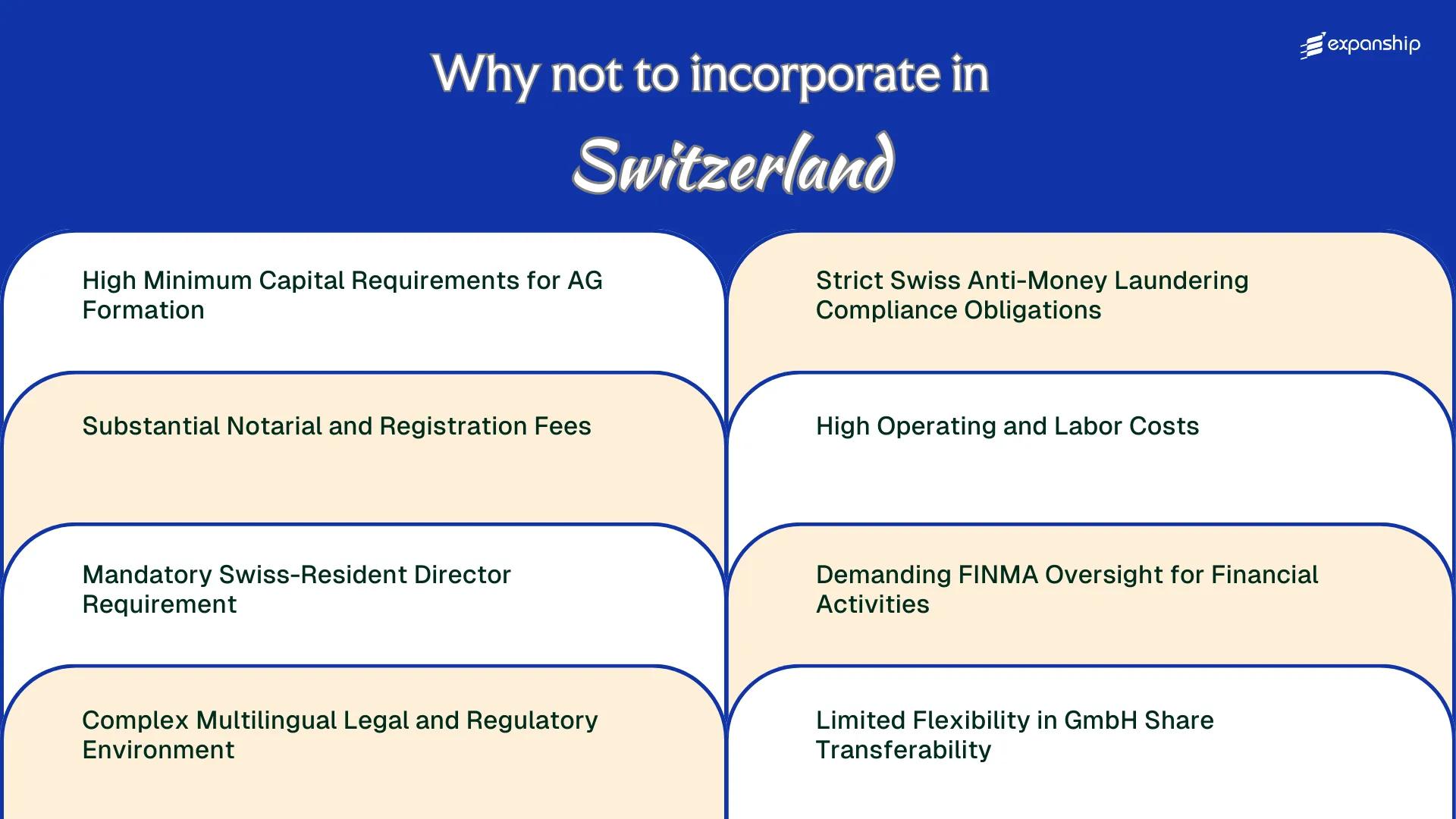

High Minimum Capital Requirements for AG Formation

Forming an Aktiengesellschaft (AG) requires a minimum share capital of CHF 100,000, of which at least CHF 50,000 must be paid up before registration. Switzerland AG minimum capital requirements place an immediate financial threshold on incorporation that most comparable European jurisdictions do not impose.

Capital Lock-Up at the Point of Entry

Under the Swiss Code of Obligations (Art. 621 et seq.), the paid-up portion must be deposited in a blocked bank account prior to registration with the Commercial Register. That capital remains inaccessible until incorporation is completed, which can take several weeks, effectively freezing working capital your business may need during the setup phase.

Structural Implications for Foreign Investors

For foreign founders without an established Swiss banking relationship, opening a capital deposit account presents its own friction, as Swiss banks apply enhanced due diligence to non-resident applicants. A CHF 100,000 floor is substantially higher than the EUR 1 minimum share capital available under several EU member state frameworks, making the AG a structurally expensive entry point.

The full CHF 100,000 capital requirement must be committed before your business can legally operate, creating a cash-flow constraint that precedes any revenue generation in the Swiss market.

Substantial Notarial and Registration Fees

Swiss company registration fees represent a meaningful upfront cost that distinguishes incorporation here from many other European jurisdictions. Both the Aktiengesellschaft (AG) and the Gesellschaft mit beschränkter Haftung (GmbH) require a public notarial deed for their formation, meaning a Swiss-licensed notary must authenticate the founding documents before the entity can be entered into the Handelsregister (Commercial Register).

Notarial fees are set by cantonal tariff regulations, so costs vary depending on where you incorporate. In cantons such as Zurich or Geneva, notarial fees alone can reach several thousand Swiss francs, before Commercial Register filing fees are added on top.

For a foreign business owner, this structure creates friction at multiple points:

- You must coordinate with a cantonal notary before the firm has any legal existence, adding scheduling delays to a process you cannot manage remotely.

- Notarial fees are non-refundable if the incorporation fails or is abandoned, creating a sunk cost with no recourse.

- Canton-specific fee schedules make cost forecasting difficult when comparing registration locations.

- Translation requirements for foreign-language documents generate additional certified translation costs.

The Federal Act on the Commercial Register (HREGV) governs registration procedures, but fee authority remains decentralized at the cantonal level, which prevents any standardized cost structure across the country.

Company Incorporation in Switzerland

Understand the full cost structure and procedural requirements before incorporating a Swiss entity.

Mandatory Swiss-Resident Director Requirement

Under Switzerland's Code of Obligations, an Aktiengesellschaft (AG) must have at least one director authorized to represent the company who is both domiciled in Switzerland and holds Swiss residency. The Switzerland resident director requirement applies regardless of where the beneficial owners are based, making it a structural constraint rather than an administrative formality.

For a foreign founder without local connections, sourcing a qualified resident director means engaging a professional nominee service, which typically carries an annual cost ranging from CHF 3,000 to CHF 12,000 or more depending on the service provider and scope of responsibilities assumed. This is an unavoidable recurring expense, not a one-time setup cost.

| Requirement | Threshold / Condition | Practical Burden |

|---|---|---|

| Minimum resident directors | At least 1 with signatory rights | Cannot be waived regardless of ownership structure |

| Nominee director annual fee | CHF 3,000 to CHF 12,000+ | Recurring cost with no equivalent in many other jurisdictions |

| Director domicile condition | Must be domiciled in Switzerland | Foreign nationals without Swiss residency cannot fulfill this role |

| Personal liability exposure | Director bears legal responsibility | Qualified nominees may impose restrictive conduct conditions |

Nominee directors commonly impose governance restrictions, requiring advance approval before executing contracts or opening bank accounts. This can slow operational decisions in ways that undermine the firm's agility.

Beyond cost, the mandatory Swiss domicile director requirement creates a dependency on a third party who carries legal liability and may limit the scope of authority they are willing to exercise on your behalf.

Complex Multilingual Legal and Regulatory Environment

Switzerland's multilingual regulatory challenges create a structural complexity that is uncommon among comparable European jurisdictions. The Confederation operates across four official languages — German, French, Italian, and Romansh — and the language of your cantonal registration directly determines which legal texts, official correspondence, and court proceedings apply to your entity. For a foreign business owner, this means engaging with Swiss legal language complexity at a level that goes beyond simple translation.

Federal legislation such as the Code of Obligations (OR) is published in German, French, and Italian, all three versions carrying equal legal authority. Discrepancies in legal terminology across versions are not hypothetical — they have produced interpretive disputes that required judicial resolution. Your compliance documentation, articles of association, and board resolutions must align with the language norms of the registering canton.

Cantonal law adds another layer. Zurich operates under German-language cantonal statutes, while Geneva and Vaud apply French-language frameworks, and Ticino applies Italian ones. Each canton also has its own commercial registry procedures, reinforcing the German French Italian compliance difficulties that foreign firms consistently encounter.

- Official correspondence from cantonal authorities arrives in the canton's official language only

- Articles of association must be drafted in the language accepted by the relevant cantonal registry

- All notarial acts are conducted and recorded in the cantonal language

- Federal and cantonal legal texts may diverge in terminology, requiring independent legal review in each applicable language

All three linguistic versions of the Code of Obligations carry identical legal weight, meaning a court can apply whichever version produces the outcome most consistent with legislative intent.

Strict Swiss Anti-Money Laundering Compliance Obligations

Swiss anti-money laundering compliance obligations impose a significant structural burden on foreign businesses, well before any revenue is generated. The Anti-Money Laundering Act (AMLA) establishes a framework that extends far beyond financial institutions, capturing a wide range of commercial activities under mandatory due diligence requirements.

Scope of Obligations Under the AMLA

If your business qualifies as a financial intermediary under the AMLA, which can include trust service providers, asset managers, and certain payment-related activities, registration with a Self-Regulatory Organization (SRO) or direct FINMA supervision is mandatory. Non-compliance carries criminal liability, not merely administrative penalties, making this a high-stakes obligation for newly incorporated entities still building their compliance infrastructure.

Practical Cost for Foreign Operators

SRO membership fees, ongoing compliance documentation, and the obligation to appoint a locally qualified compliance officer translate into recurring costs that many foreign founders underestimate at the incorporation stage. The Switzerland AMLA restrictions for companies also require systematic client identification, beneficial ownership verification, and transaction monitoring, each demanding dedicated internal processes or expensive third-party compliance mandates. Businesses outside the financial intermediary definition still face AML-related obligations under the Code of Obligations when handling certain cash transactions above CHF 100,000.

Support for Meeting Swiss Compliance Requirements

Understand the full scope of AML obligations before incorporating in Switzerland, and get guidance on what your business structure will trigger under the AMLA.

High Operating and Labor Costs

High operating costs in Switzerland represent one of the most consistent financial pressures for foreign-incorporated businesses, extending well beyond the formation phase into every year of ongoing operations.

- Swiss gross salaries are among the highest in Europe, with average annual compensation across sectors frequently exceeding CHF 80,000, which directly inflates your fixed payroll base regardless of company size.

- Employer social security contributions under the Bundesgesetz über die Alters- und Hinterlassenenversicherung (AHVG) and related federal insurance laws add approximately 12–13% on top of gross salary, increasing your true labor cost per employee beyond the headline wage figure.

- Mandatory contributions to the occupational pension system (BVG/LPP) impose additional employer obligations that vary by salary band, creating layered payroll costs that require dedicated HR or payroll administration to manage correctly.

- Commercial office rents in Zurich and Geneva consistently rank among the highest in continental Europe, placing upward pressure on your overhead from the moment you establish a physical presence.

- Swiss value-added tax (MWST/TVA) at 8.1% applies to most taxable supplies, and registration is mandatory once your global turnover exceeds CHF 100,000, adding compliance costs for smaller foreign entities.

Demanding FINMA Oversight for Financial Activities

FINMA oversight challenges in Switzerland are most acutely felt by foreign businesses operating in financial services, asset management, or fintech. The Financial Market Supervisory Authority (FINMA) regulates banks, insurance firms, securities dealers, and collective investment schemes under a framework that demands significant pre-authorization before any regulated activity can begin.

Obtaining a FINMA license is not a procedural formality. Depending on the license category, your firm must demonstrate minimum capital adequacy, fit-and-proper governance structures, and ongoing reporting obligations under the Financial Institutions Act (FinIA) and the Banking Act (BankG).

The Swiss financial regulator's restrictions on businesses extend to activities that may be lightly regulated elsewhere. Holding client assets or providing portfolio management without authorization exposes a firm to criminal liability, not just administrative penalties.

- Fintech firms with a banking license exemption face a CHF 100 million deposit cap under the FinIO

- Securities firms must maintain minimum capital of CHF 1.5 million at authorization

- Ongoing FINMA supervision includes annual audit requirements by recognized audit firms

A foreign-owned asset management startup seeking a FINMA portfolio manager license under FinIA must budget for legal structuring costs, a minimum equity base, and recurring third-party audit fees, which can collectively exceed CHF 200,000 in the first operating year before generating any client revenue.

Limited Flexibility in GmbH Share Transferability

Switzerland GmbH share transferability restrictions stem directly from the Swiss Code of Obligations (OR), which governs how ownership interests in a Gesellschaft mit beschränkter Haftung can change hands. Unlike shares in an AG, GmbH shares cannot be transferred through a simple written agreement. Every transfer requires a publicly authenticated deed executed before a notary, making even routine ownership changes procedurally heavy.

That notarial requirement is not merely a formality. For foreign investors managing cross-border restructurings or secondary sales on compressed timelines, the mandatory authentication process introduces delays and additional costs that are structurally unavoidable.

Beyond procedure, the OR also allows a GmbH's articles of association to include consent clauses, giving existing shareholders the right to refuse an incoming transferee without needing to justify the refusal. A foreign acquirer can complete notarization only to find the transfer blocked at the shareholder approval stage.

Swiss GmbH share transfer limitations also affect exit planning. Private equity structures or venture-backed entities that expect frequent cap table changes often find the GmbH form operationally misaligned with those needs.

Even when a GmbH's articles of association contain no explicit consent clause, the statutory default under the OR still permits shareholders to reject a transfer, meaning foreign buyers have no guaranteed right of entry regardless of the purchase price agreed.

Overcoming Switzerland's Incorporation Challenges

Overcoming Switzerland's Incorporation Challenges

Overcoming Switzerland incorporation challenges requires structural preparation before formation, not reactive adjustments after registration. The regulatory framework is consistent and well-documented, which means most obstacles are foreseeable.

- Satisfy the CHF 100,000 minimum paid-in capital threshold for an AG by confirming funds are deposited in a blocked Swiss bank account prior to notarial deed execution.

- Appoint at least one Swiss-resident director with sole signatory authority to meet the residency requirement under the Code of Obligations.

- Engage a certified anti-money laundering officer or affiliate with a self-regulatory organisation recognised under the Anti-Money Laundering Act (AMLA) to fulfil due diligence obligations.

- Register the entity in the applicable cantonal commercial register through the Federal Commercial Registry to formalise legal existence.

- Assess whether your business activities trigger FINMA licensing requirements before commencing operations.

Solutions to Swiss company formation drawbacks are grounded in federal statute, cantonal procedure, and industry-specific ordinances. Managing Swiss regulatory compliance difficulties is an ongoing obligation, not a one-time formation task.

Switzerland's Value as a Business Destination

Switzerland remains a credible incorporation destination despite the drawbacks documented in this blog. The costs, compliance obligations, and structural constraints are real, but they exist within a jurisdiction that offers political stability, a well-functioning legal system, and a strong international reputation — factors that carry measurable weight for certain business profiles.

| Pros | Cons |

|---|---|

| Switzerland's bilateral treaties and OECD standing support legitimate international tax planning | Minimum share capital for an AG is CHF 100,000, with at least CHF 50,000 paid up at incorporation |

| The Swiss legal system operates predictably under codified federal law, including the Code of Obligations | Notarial deed requirements and commercial register fees add material upfront incorporation costs |

| Access to a highly skilled, multilingual workforce supports operations across sectors | At least one director with signatory authority must be resident in Switzerland |

| The Swiss franc's stability reduces currency risk for businesses holding assets in the jurisdiction | GmbH shares require notarised transfer agreements, limiting ownership flexibility |

| Switzerland's reputation can enhance credibility with institutional counterparties and banks | FINMA oversight applies broadly to financial activities, with demanding licensing and reporting requirements |

For foreign owners, the decision turns less on whether the disadvantages exist and more on whether the business model can absorb them. Regulatory costs that are prohibitive for a small trading entity may be immaterial for a holding structure or an IP-licensing vehicle.

Compliance Services for Companies in Switzerland

Meet your ongoing Swiss compliance obligations, from commercial register filings and annual reporting to AML obligations under the GwG.

Conclusion

The cons of Swiss company incorporation summary are well-documented: high costs, structural constraints, and compliance obligations that require sustained attention. Minimum capital thresholds for the AG, the resident director requirement under the Code of Obligations, and FINMA's oversight for any financially regulated activity each carry meaningful administrative and financial weight. These are structural features of the Swiss legal framework, not incidental friction. For businesses where the jurisdiction's stability and treaty network justify the entry costs, those structural demands still require deliberate planning and qualified local support to manage over time.

Expanship's Support for Your Swiss Expansion

Expanship's Switzerland company formation support services are built around the specific demands this jurisdiction places on foreign businesses. From coordinating with FINMA-regulated intermediaries to managing AML compliance documentation under the GwG framework, the firm helps reduce the administrative weight these obligations create. Expanship does not change what Swiss law requires; it handles the operational steps involved in meeting those requirements.

Beyond incorporation, the firm's services cover the full setup and maintenance cycle for your Swiss entity.

- Preparing and filing constitutional documents for AG or GmbH registration with the commercial register.

- Providing a registered office address and acting as your local registered agent.

- Coordinating government filings and liaising directly with relevant authorities on your behalf.

- Managing ongoing compliance obligations after your company is established.

- Facilitating introductions to Swiss banking institutions suited to your business profile.

- Handling tax registration and correspondence with cantonal and federal revenue authorities.

Reach out to Expanship Switzerland to discuss your incorporation requirements.

Frequently Asked Questions (FAQ)

It is one of the highest statutory minimums in Europe. While a UK limited company requires just £1 in share capital and a German GmbH requires €25,000, a Swiss AG requires CHF 100,000, with at least CHF 50,000 paid up at incorporation. For early-stage businesses or startups testing the Swiss market, this capital is locked into the entity from day one and cannot be redirected to operational costs without triggering legal restrictions under the Swiss Code of Obligations.

Yes, it applies to both entity types. Under the Swiss Code of Obligations, at least one director or managing officer with signatory authority must be resident in Switzerland. This applies regardless of whether your business is structured as an Aktiengesellschaft or a Gesellschaft mit beschränkter Haftung, and it cannot be waived by shareholder agreement or articles of association.

Breaching the Anti-Money Laundering Act (AMLA) in Switzerland can result in criminal prosecution, fines, and mandatory reporting obligations imposed by the Financial Intelligence Unit (MROS). For financial intermediaries, non-compliance can also trigger regulatory sanctions from FINMA, including licence revocation. The consequences are not limited to financial penalties — reputational damage and criminal liability for directors are both realistic outcomes.

Notarial fees alone for an AG formation typically range from CHF 1,500 to CHF 3,000, depending on the canton, and registration with the Commercial Registry adds further costs. When combined with mandatory publication in the Swiss Official Gazette of Commerce and legal drafting fees, total formation costs can exceed CHF 5,000 before any operational expenses are incurred. These figures vary by canton, as notarial fee scales are not uniformly set at the federal level.

It is a material constraint for any firm planning to raise equity from third parties. GmbH share transfers require a public deed executed before a notary, and the articles of association can impose additional approval rights on existing shareholders, effectively giving them veto power over new investors. This makes the GmbH structurally unsuitable for businesses that anticipate multiple funding rounds or broad investor participation.

FINMA oversight applies specifically to entities conducting regulated financial activities, including banking, insurance, securities dealing, and collective investment scheme management. A standard trading or consulting company incorporated in Switzerland is not subject to FINMA licensing. However, the threshold for triggering regulatory classification is interpreted strictly, and activities that resemble financial intermediation — even incidentally — can draw FINMA scrutiny under the Financial Institutions Act (FinIA) or the Banking Act.

Incorporating in a German-, French-, or Italian-speaking canton reduces the number of official languages your entity operates in, but it does not eliminate multilingual exposure entirely. Federal legislation, including the Code of Obligations and the Swiss Civil Code, is published in all three official languages, and discrepancies between language versions can affect legal interpretation. If your business operates across cantonal borders or engages with federal authorities, documentation requirements will frequently extend beyond your canton's primary language.

Swiss labor costs are among the highest in the world, not just in Europe. Average gross salaries are substantially above those in Germany, France, or Austria, and employer social security contributions — covering AHV, IV, and other mandatory schemes — add approximately 12 to 15 percent on top of gross wages. Smaller businesses feel this disproportionately because they cannot distribute overhead across a large headcount, making Switzerland a structurally expensive base for labor-intensive operations at any stage of growth.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.