Key Takeaways

- Switzerland's combined federal and cantonal corporate tax regime, with effective rates that can fall significantly below the OECD average depending on the canton chosen, allows internationally structured businesses to reduce their overall tax burden in a legally transparent framework.

- With over 100 double taxation treaties in force, Swiss-incorporated entities can substantially reduce withholding tax exposure on dividends, royalties, and interest flows across a wider network of counterparty jurisdictions than most competing European locations offer.

- Intellectual property assets held through a Swiss entity benefit from protections grounded in the Swiss Code of Obligations and federal patent law, giving technology and life sciences companies a durable legal basis for cross-border IP structuring.

- Because Switzerland is not an EU member state, companies incorporated there retain access to European markets without being subject to EU regulatory directives — a structural advantage that has remained intact regardless of broader shifts in EU trade and compliance policy.

The benefits of incorporating in Switzerland draw interest from businesses across sectors, from financial services firms to technology companies establishing European operations. Situated in Central Europe and bordered by Germany, France, Italy, and Austria, Switzerland is a sovereign federal republic — not an EU member state — governed under a stable constitutional framework that has remained largely unchanged for decades.

Company registration falls under the authority of the Swiss Commercial Registry, administered at the cantonal level and coordinated federally through the Federal Office of Justice. Foreign businesses most commonly incorporate through an Aktiengesellschaft (AG). The country operates a low-tax regime shaped by both federal rates and significant cantonal variation, with a broad treaty network that reduces withholding burdens on cross-border income.

Foreign ownership of Swiss companies faces no general statutory restrictions, and the country consistently attracts significant foreign direct investment across its major cantons. Your business can hold 100% of a Swiss entity without requiring a local partner in most sectors.

This article examines the principal advantages that Swiss company formation offers to internationally operating businesses.

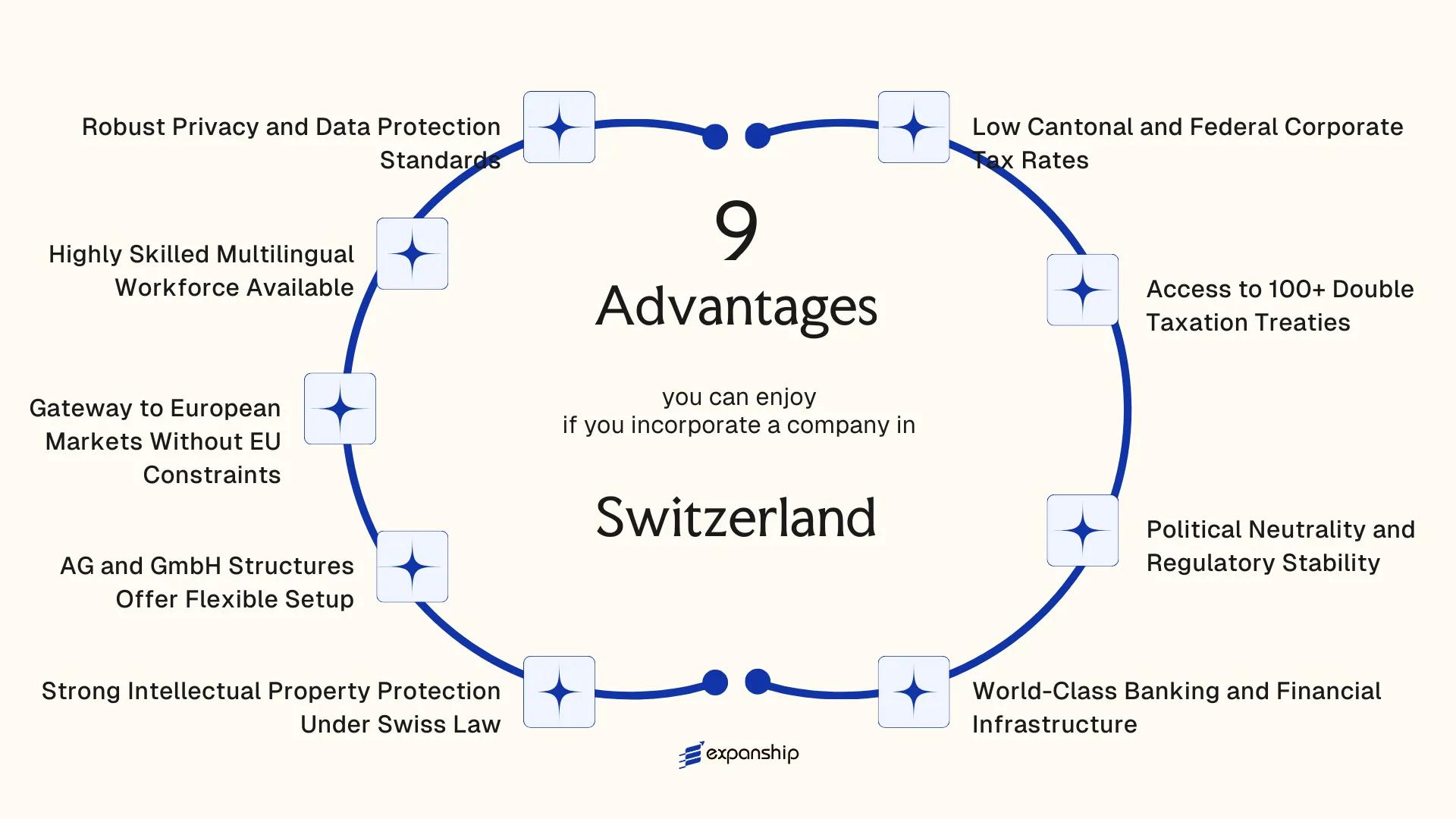

Low Cantonal and Federal Corporate Tax Rates

Low corporate tax rates in Switzerland result from a two-tier system where federal and cantonal taxes are levied separately, giving businesses meaningful control over their effective rate based on where they register.

How the Rate Structure Works in Practice

The federal corporate income tax rate is a flat 8.5% on profit after tax, which translates to roughly 7.83% on pre-tax profit. Cantons then apply their own rates on top, and the combined effective rate varies significantly by location — Zug, Nidwalden, and Appenzell Ausserrhoden consistently post combined rates between 11.9% and 13%, well below the OECD average of approximately 23%.

Choosing your canton of domicile is therefore a direct tax decision. A holding company registered in Zug operates under a materially lower burden than the same entity would face in most Western European jurisdictions.

What This Means for After-Tax Retained Earnings

Federal and cantonal tax benefits in Switzerland compound when a firm retains earnings for reinvestment. At an effective combined rate below 13%, a foreign-owned entity retains a substantially larger share of profit per franc earned compared to incorporation in Germany or France, where rates exceed 25%.

Swiss cantonal tax advantages are anchored in cantonal tax laws (Steuergesetze), which each canton enacts independently within bounds set by the Federal Tax Harmonisation Act (StHG).

Your effective corporate tax rate in Switzerland is partly a location choice — registering in a low-rate canton like Zug or Nidwalden can reduce your combined tax burden to under 12%.

Access to 100+ Double Taxation Treaties

Switzerland has concluded over 100 double taxation agreements, making its treaty network one of the most extensive among non-EU jurisdictions. For foreign investors, the practical consequence is direct: dividends, interest, and royalties paid across borders are subject to reduced withholding tax rates rather than the full statutory rates that would otherwise apply. Under many of these agreements, withholding tax on dividends can fall to 0–5% for qualifying corporate shareholders, compared to Switzerland's standard 35% withholding tax rate under the Verrechnungssteuer.

The treaties follow the OECD Model Tax Convention and typically include provisions on permanent establishment, meaning your business structure determines where profits are taxed. Treaty partners span major economies across Asia, the Americas, the Middle East, and Europe.

Several features make the treaty framework practical for foreign-owned entities:

- Treaty access requires genuine economic substance, which discourages shell structures and strengthens the credibility of treaty claims with counterpart tax authorities

- The Federal Tax Administration publishes official treaty texts and applicable rates, giving your tax advisors a reliable, transparent reference point

- Many treaties include mutual agreement procedures, providing a formal channel to resolve cross-border disputes without litigation

Entities incorporated under Swiss law, whether an AG or GmbH, can access these treaties provided they meet the residency and substance requirements outlined in the applicable agreement.

Incorporate a Company in Switzerland

Set up a Swiss AG or GmbH and access Switzerland's treaty network through a properly structured, compliant entity.

Political Neutrality and Regulatory Stability

Switzerland political stability for businesses is grounded in a constitutional structure that has remained fundamentally unchanged since 1848. The Federal Constitution distributes authority across the Confederation, 26 cantons, and municipalities, creating a layered system of governance where no single political actor can unilaterally alter commercial law or tax policy. For a foreign business owner, this means the rules under which your entity was incorporated are unlikely to shift dramatically with any single election cycle.

The country's long-standing neutrality under international law, codified through a combination of treaty obligations and domestic statute, insulates it from the geopolitical disruptions that frequently trigger regulatory overhauls in neighboring states. Sanctions regimes, trade bloc tensions, and diplomatic disputes that periodically destabilize business environments elsewhere have historically had limited domestic legal consequences here.

| Feature | Detail |

|---|---|

| Constitutional foundation | Federal Constitution of 1848, last fully revised in 1999 |

| Legislative process | Mandatory referendum rights allow public checks on major legal changes |

| Regulatory oversight body | Swiss Financial Market Supervisory Authority (FINMA) for financial entities |

| Legal system | Civil law tradition with high codification and predictability |

Regulatory changes affecting companies follow a structured consultation process called the Vernehmlassung, during which proposed legislation is circulated to cantons, political parties, and industry groups before parliamentary debate. This procedure extends the timeline for legal changes, giving your business advance notice and time to adapt before new rules take effect.

World-Class Banking and Financial Infrastructure

Switzerland banking infrastructure advantages are well established among corporate practitioners, largely because the country's financial system operates under a framework that foreign businesses can access with relative directness after incorporation.

The Swiss Financial Market Supervisory Authority (FINMA) oversees banks, insurance firms, and financial intermediaries under the Banking Act (SR 952.0). For your business, this means accounts are held at institutions subject to one of the more exacting supervisory regimes globally, reducing counterparty risk on routine treasury operations.

Multi-currency accounts, trade finance facilities, and correspondent banking networks are available to incorporated entities through major institutions such as UBS and Julius Baer, as well as cantonal banks like Zürcher Kantonalbank. Access to these services gives foreign-owned firms a credible financial address that facilitates cross-border transactions across Asia, the Americas, and the Gulf.

Swiss payment infrastructure runs through the SIX Group, which operates the Swiss Interbank Clearing system. Settlement times and transaction reliability matter to businesses managing multi-jurisdictional cash flow.

Keep the following in mind:

- Corporate account opening requires substance documentation; nominee-only structures face scrutiny

- FINMA's Anti-Money Laundering Act (AMLA) mandates beneficial ownership disclosure

- Cantonal banks may offer preferential terms to locally registered firms with physical presence

- Account opening timelines vary significantly by institution and client complexity

Cantonal banks, which are partially government-guaranteed, can serve as primary banking partners for foreign-owned Swiss entities, an option many international founders overlook in favour of global private banks.

Strong Intellectual Property Protection Under Swiss Law

Switzerland intellectual property protection benefits stem from a legal framework that treats IP as a registrable, enforceable, and transferable asset class with meaningful legal standing. For a foreign business holding patents, trademarks, or copyrights, this matters because your rights are not merely recognized on paper — they are actionable through well-established civil and criminal enforcement mechanisms.

Statutory Foundation and the Role of the IGE/IPI

The Federal Institute of Intellectual Property (IGE/IPI) administers trademark and patent registrations under the Federal Act on Trade Marks and Indications of Source (MSchG) and the Federal Patents Act (PatG). Both statutes provide clear grounds for infringement claims, injunctive relief, and damages. Unlike jurisdictions where enforcement depends heavily on administrative discretion, Swiss courts handle IP disputes with predictability — a material advantage for foreign firms whose assets cross multiple legal systems.

Switzerland is also party to the European Patent Convention (EPC), meaning a European patent granted through the EPO extends protection to Swiss territory without a separate national filing. This reduces administrative overhead for businesses seeking broad European coverage from a single holding entity.

Tax Treatment of IP Income

IP income held through a Swiss entity can qualify for cantonal IP box regimes, which tax qualifying net income from patents and comparable rights at reduced effective rates. These regimes were introduced in line with the OECD's modified nexus approach, applied following the 2020 cantonal tax reforms under STAF (Federal Act on Tax Reform and AHV Financing). Eligibility is conditioned on a nexus between R&D expenditure and the income-generating IP, which means the relief is substantive rather than purely structural.

Maximize Your IP Benefits in Switzerland

Speak with an Expanship specialist about structuring your intellectual property holdings through a Swiss entity to align with cantonal IP box regimes and Swiss federal IP law.

AG and GmbH Structures Offer Flexible Setup

Switzerland offers two primary corporate vehicles: the Aktiengesellschaft (AG) and the Gesellschaft mit beschränkter Haftung (GmbH). The Switzerland AG and GmbH structure benefits differ in meaningful ways, giving foreign investors genuine options rather than a one-size-fits-all framework.

- The AG requires a minimum share capital of CHF 100,000, of which at least 50% must be paid up at incorporation. Shares can be structured as bearer or registered, and the entity suits businesses anticipating institutional investment or eventual public listing.

- The GmbH carries a lower capital threshold of CHF 20,000, fully paid up at formation. Ownership is recorded in a share register and the articles of association, which limits anonymous transfers and gives founders direct visibility over who holds equity at all times.

- Both structures cap shareholder liability at their respective capital contributions under the Swiss Code of Obligations (OR). For a foreign investor, this means personal assets remain separated from business liabilities without requiring complex holding arrangements.

- Neither form mandates a Swiss-resident shareholder, though at least one director with signatory authority must be domiciled in Switzerland. This preserves foreign ownership while satisfying local governance requirements under the OR.

- Conversion between the two forms is possible under Swiss law, allowing a business that starts as a GmbH to migrate to an AG structure as operational scale increases.

Gateway to European Markets Without EU Constraints

Switzerland's gateway to European markets benefits stem from a legal architecture that gives your business access to EU member state markets without subjecting it to EU regulatory oversight. Through 120+ bilateral agreements with the EU, including the 1999 Bilateral Agreements I covering the free movement of goods, persons, and services across key sectors, a Swiss-registered firm can operate across European borders under negotiated terms rather than full EU membership conditions.

This distinction has direct commercial value. Your entity avoids EU directives on state aid, competition enforcement by the European Commission, and mandatory alignment with regulations such as the EU Corporate Sustainability Reporting Directive (CSRD), while still maintaining structured market access.

- Mutual recognition agreements with EU member states reduce technical barriers for Swiss exporters in specific product categories

- The Agreement on Technical Barriers to Trade allows Swiss-certified products to enter EU markets without re-testing in many regulated sectors

- Swiss firms are not subject to EU VAT harmonization rules, allowing separate domestic VAT structuring under the Swiss VAT Act

A firm exporting medical devices from Zurich to Germany can use Swiss product certification under the bilateral Mutual Recognition Agreement (MRA) for regulatory approval equivalence, bypassing the need for a separate EU conformity assessment in many device categories. This removes a compliance layer that applies to non-Swiss, non-EU manufacturers selling into the same market.

Highly Skilled Multilingual Workforce Available

The Switzerland skilled multilingual workforce advantages begin with geography and constitutional structure. Four national languages — German, French, Italian, and Romansh — are recognized under the Federal Constitution, producing a domestic talent pool that operates fluently across cultural and linguistic contexts without additional training investment.

For a foreign firm establishing operations here, this has direct operational value:

- Client communication across German-speaking Europe, France, and Italy can be handled by locally hired staff

- Multilingual documentation and contract management rarely requires external translation services

- Your business can serve diverse international markets from a single office location

Education underpins much of this. The Swiss Federal Institute of Technology (ETH Zurich) and EPFL in Lausanne consistently produce graduates in engineering, finance, and life sciences, feeding directly into the local employment market. Hiring locally often means accessing candidates with internationally recognized qualifications without relocation costs.

The bilateral agreements between Switzerland and the EU under the Agreement on the Free Movement of Persons also expand the available talent base, allowing firms to recruit from across EU and EFTA member states under structured terms.

Work permit quotas and cantonal authorization requirements still apply to non-EU/EFTA nationals, which affects hiring timelines for roles filled outside the free movement framework.

Robust Privacy and Data Protection Standards

Switzerland data protection standards benefits extend well beyond territorial borders, giving incorporated entities a defensible legal position when handling personal data across multiple markets.

The nDSG Framework and What It Requires

The revised Federal Act on Data Protection (nDSG), which entered force on 1 September 2023, aligns Swiss data protection law with principles found in the EU's GDPR while remaining a distinct national regime. For your business, this matters because Swiss law is not subject to EU institutional oversight, yet the European Commission has granted Switzerland an adequacy decision, allowing personal data to flow freely from EU member states without additional transfer mechanisms. A single legal framework can therefore govern data operations on both sides of the border.

Separation from EU Jurisdiction as a Structural Advantage

Because Switzerland sits outside the EU, your entity is not directly subject to the European Data Protection Board or national supervisory authorities within EU member states. The Federal Data Protection and Information Commissioner (FDPIC) acts as the domestic supervisory authority, operating under Swiss administrative law rather than EU enforcement architecture. This jurisdictional separation limits your regulatory exposure to a single, clearly defined authority.

Obligations That Signal Trustworthiness to Clients

Under the nDSG, controllers must maintain records of processing activities, conduct data protection impact assessments for high-risk processing, and appoint a representative in certain cross-border contexts. Meeting these requirements positions your firm credibly with enterprise clients in regulated sectors, such as finance and healthcare, who conduct supplier due diligence as standard practice.

- Adequacy decision covers data transfers from all EU/EEA member states

- FDPIC publishes binding guidance and can initiate investigations independently

- Criminal penalties under nDSG attach to individuals, not solely to legal entities

Why Switzerland Stands Apart from Competing Jurisdictions

Comparing Switzerland against competing jurisdictions reveals a distinct profile. The jurisdictions most relevant to this comparison are Luxembourg, the Netherlands, and Ireland — all of which attract international holding companies, IP structures, and regional headquarters from outside Europe. Readers evaluating Switzerland vs competing jurisdictions for incorporation are typically also weighing these three, given their similar positioning as stable, treaty-networked EU or European hubs targeting the same investor profiles.

What the comparison surfaces is less about headline tax rates and more about structural reliability. EU membership creates a dependency on harmonisation directives that Switzerland, operating under bilateral agreements rather than supranational law, is not subject to. The OECD Pillar Two minimum tax framework has narrowed rate differentials across these jurisdictions, which shifts the competitive calculus toward treaty depth, legal certainty, and institutional consistency — areas where the Swiss framework has remained largely unchanged across political cycles.

| Parameter | Switzerland | Luxembourg | Netherlands | Ireland |

|---|---|---|---|---|

| Standard Corporate Tax Rate | ~14.9%–19.7% (cantonal variance) | 17% | 25.8% | 12.5% |

| Double Tax Treaties | 100+ | 80+ | 100+ | 75+ |

| EU Member | No (bilateral agreements) | Yes | Yes | Yes |

| Legal System | Swiss Code of Obligations | Civil law (EU-influenced) | Civil law (EU-influenced) | Common law |

| Political Neutrality | Constitutionally enshrined | EU-aligned | EU-aligned | EU-aligned |

| FATF Compliance | Full member | Full member | Full member | Full member |

| IP Regime | Patent box, federal protection | IP box regime | Innovation box | Knowledge Development Box |

Compliance Services for Swiss Companies

Ongoing compliance support for Swiss AG and GmbH entities, covering annual filings, statutory obligations, and regulatory reporting under Swiss law.

Conclusion

Switzerland combines treaty-backed tax efficiency, structural flexibility under Swiss corporate law, and a political environment that has remained stable for generations. Taken together, these features create conditions that are genuinely difficult to replicate elsewhere. The benefits of incorporating in Switzerland are most evident when you consider the interaction between low cantonal tax rates, access to over 100 double taxation agreements, and the legal durability offered by entities such as the AG and GmbH under the Swiss Code of Obligations.

That said, the advantages of Swiss company registration are not uniform across every use case. A holding structure optimising for treaty access will extract different value from the jurisdiction than a life sciences firm prioritising IP protection under Swiss patent law, or a financial services business seeking FINMA-regulated credibility.

What Switzerland offers, at its core, is a jurisdiction where legal frameworks, tax policy, and institutional infrastructure have remained coherent and predictable over time. Your specific industry, ownership structure, and operational footprint will determine how fully those conditions translate into commercial advantage. Establishing a clear understanding of those variables is the necessary first step before any formation decision is made.

Start Your Swiss Company with Expanship Today

Expanship handles the formation and ongoing compliance of Swiss entities, including the AG (Aktiengesellschaft) and GmbH (Gesellschaft mit beschränkter Haftung), working within the registration requirements set by the Swiss Federal Commercial Registry (Handelsregisteramt). The services covered in this blog, from cantonal tax positioning to intellectual property holding structures and banking access, each carry specific procedural and documentary requirements that need to be addressed at the point of incorporation and maintained thereafter.

To support your business from setup through ongoing operation, Expanship's Switzerland company formation services cover the following:

- Preparation and notarization of incorporation documents in accordance with Swiss Code of Obligations requirements

- Provision of a registered address and resident agent where required by cantonal rules

- Filing and liaison with the cantonal Handelsregisteramt for entity registration

- Post-incorporation compliance management, including annual reporting obligations

- Document legalization and apostille coordination for cross-border use

- Banking introduction assistance with Swiss financial institutions

When you are ready to move forward, Expanship Switzerland can be contacted directly to discuss your formation requirements.

Frequently Asked Questions (FAQ)

Yes, foreign nationals can incorporate a Swiss AG or GmbH without residing in Switzerland. However, at least one director with signatory authority must be domiciled in Switzerland, which is a requirement under the Swiss Code of Obligations. This condition is commonly met by appointing a local nominee director or a Swiss-based corporate service provider.

The effective combined federal and cantonal corporate tax rate varies by canton, ranging from approximately 11.9% in Zug to around 21% in less competitive cantons. The federal rate sits at a flat 8.5% on profit after tax, with cantonal and communal taxes applied on top. Choosing the right canton at the time of incorporation can materially affect your firm's annual tax burden.

Switzerland maintains over 100 double taxation agreements, administered under the authority of the State Secretariat for International Finance (SIF). These treaties reduce or eliminate withholding taxes on dividends, interest, and royalties paid across borders. The specific rates and conditions vary by treaty partner, so the applicable agreement should be reviewed before structuring cross-border payments.

The Swiss IP box regime, introduced through the Federal Act on Tax Reform and AHV Financing (TRAF) in 2020, applies to qualifying income derived from patents and comparable rights. Trademarks, copyrights, and domain names are generally excluded from the preferential treatment. Cantons implement the regime individually, so the precise qualifying criteria and relief rates differ depending on where your entity is registered.

Incorporation timelines depend on the cantonal commercial register, but most formations are completed within one to three weeks from the date all required documents are submitted. The process involves notarisation of the articles of association, payment of the minimum share capital, and registration with the relevant cantonal Commercial Register Office. Delays typically arise from incomplete documentation or identity verification requirements.

Switzerland is not a member of the European Union and conducts its trade relationship with the EU through a series of bilateral agreements rather than a single accession treaty. This structure gives businesses incorporated there access to key European markets without being subject to EU regulatory directives, VAT harmonisation rules, or the jurisdiction of the Court of Justice of the EU. The trade-off is that passporting rights available to EU-incorporated entities do not automatically extend to Swiss companies.

Swiss-incorporated companies handling personal data are subject to the revised Federal Act on Data Protection (revFADP), which came into force on 1 September 2023. The Federal Data Protection and Information Commissioner (FDPIC) is the supervisory authority responsible for enforcement. Companies processing data of EU residents may also fall within the scope of the GDPR, depending on their activities, creating a dual compliance obligation.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.