Key Takeaways

- Swiss company formation is governed primarily by the Swiss Code of Obligations (OR), with registration administered at the cantonal level through the Commercial Register (Handelsregister) and indexed federally via the Swiss Federal Office of Justice.

- The GmbH is the most commonly registered entity among new formations in Switzerland, suited to closely held private businesses with defined ownership structures.

- Effective corporate tax burden in Switzerland is highly location-dependent due to a territorial-leaning regime with rates that vary by canton.

- Among the available structures — which include the AG, GmbH, KmAG, Kollektivgesellschaft, Kommanditgesellschaft, Genossenschaft, Einzelunternehmen, and foreign presence forms — each carries distinct requirements around capital, liability, governance, and registration obligations.

Introduction to Entity Types in Switzerland

Switzerland is a landlocked federal republic in central Europe, bordered by Germany, Austria, Liechtenstein, Italy, and France. Company registration is administered at the cantonal level, with the Commercial Register (Handelsregister) serving as the federal index of all registered entities — each canton maintains its own register, and entries feed into the national system operated by the Swiss Federal Office of Justice.

The country applies a territorial-leaning tax regime with rates that vary by canton, making the effective corporate tax burden highly location-dependent.

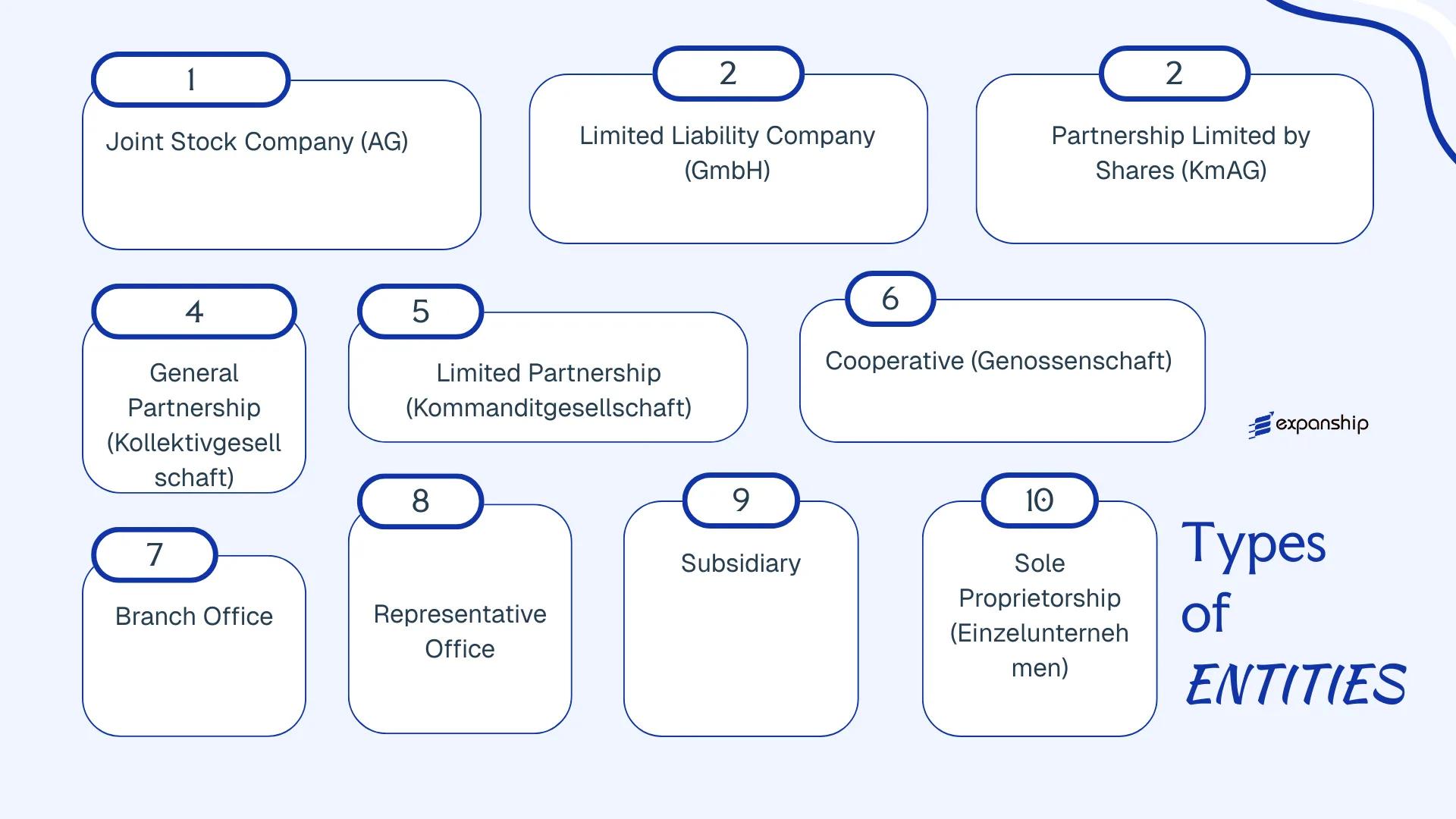

Swiss law, principally governed by the Swiss Code of Obligations (OR), recognises several distinct legal entity types available to residents and foreign investors alike:

- Aktiengesellschaft (AG)

- Gesellschaft mit beschränkter Haftung (GmbH)

- Kommanditaktiengesellschaft (KmAG)

- Kollektivgesellschaft

- Kommanditgesellschaft

- Genossenschaft

- Einzelunternehmen

- Branch Office

- Representative Office

Each form carries specific requirements around capital, liability, governance, and registration obligations. The sections that follow examine each structure in detail to help you determine which fits your business objectives and operational profile.

An Overview of Business Structures in Switzerland

Swiss company law recognises several distinct legal forms, each governed primarily by the Swiss Code of Obligations (Obligationenrecht), which entered into force in 1912 and has been amended substantially over time, including major reforms to share company law effective January 2023. The Swiss Civil Code (Zivilgesetzbuch) provides the framework for cooperative and association structures. Each legal form carries different implications for liability, governance, taxation, and the profile of members or shareholders it accommodates.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Aktiengesellschaft (AG) | Corporation | Limited to share capital | Taxed | Yes | 1 shareholder | Commercial Registry (Handelsregisteramt) | Code of Obligations |

| Gesellschaft mit beschränkter Haftung (GmbH) | LLC | Limited to quota capital | Taxed | Yes | 1 member | Commercial Registry | Code of Obligations |

| Kommanditaktiengesellschaft (KmAG) | Hybrid partnership/corp | Mixed: limited and unlimited | Taxed | Yes | 1 general + 1 limited partner | Commercial Registry | Code of Obligations |

| Kollektivgesellschaft | General partnership | Unlimited, joint and several | Taxed (pass-through) | Yes | Min. 2 partners | Commercial Registry | Code of Obligations |

| Kommanditgesellschaft | Limited partnership | Mixed: limited and unlimited | Taxed (pass-through) | Yes | Min. 2 partners | Commercial Registry | Code of Obligations |

| Genossenschaft | Cooperative | Limited | Taxed | Yes | Min. 3 members | Commercial Registry | Civil Code / CO |

| Branch Office | Foreign branch | Parent bears liability | Taxed on Swiss income | Yes | N/A | Commercial Registry | Code of Obligations |

| Representative Office | Non-trading presence | Parent bears liability | Generally exempt | No | N/A | Cantonal authorities | Cantonal law |

| Einzelunternehmen | Sole proprietorship | Unlimited, personal | Taxed (personal income) | Yes | 1 individual | Commercial Registry (if CHF 100k+ revenue) | Code of Obligations |

Each of these structures is examined in full in the sections below.

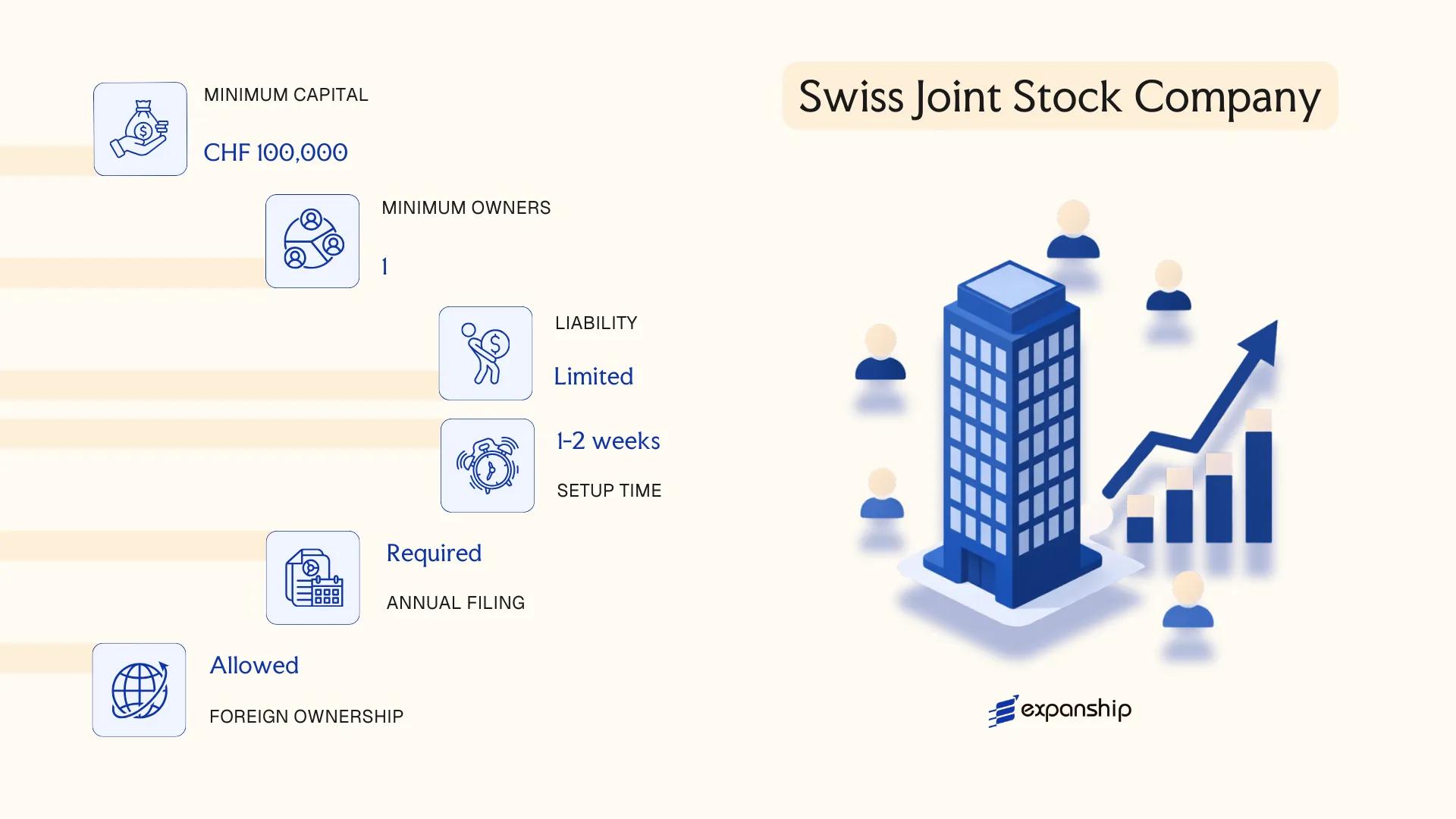

Aktiengesellschaft (AG) – Swiss Joint Stock Company

Aktiengesellschaft AG Switzerland formation is governed primarily by the Swiss Code of Obligations (Obligationenrecht), specifically Articles 620–763, most recently revised through the major corporate law reform that took effect on 1 January 2023. The AG carries full separate legal personality from the moment of registration in the Commercial Register (Handelsregister).

Liability of shareholders is strictly limited to their capital contribution. The structure accommodates both closely held family businesses and publicly listed corporations, making it the predominant vehicle for larger commercial operations.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Aktiengesellschaft (AG) | Separate legal personality; governed by CO Arts. 620–763 |

| Members | Shareholders (min. 1, no maximum); Board of Directors (min. 1 member); statutory auditor required above certain thresholds | Single founder permitted; board members must include at least one Swiss-resident signatory |

| Local Presence | Registered office in Switzerland; at least one board member domiciled in Switzerland with signatory authority | No requirement for a resident shareholder |

| Share Capital | Min. CHF 100,000; at least 50% (CHF 50,000) paid up at incorporation | Shares have a minimum nominal value of CHF 0.01 since the 2023 reform |

| Share Types | Registered shares (Namenaktien), bearer shares (Inhaberaktien) | Bearer shares now require intermediated securities holding; effectively restricts anonymous ownership |

| Privacy | Shareholders not publicly disclosed in the Handelsregister; beneficial owners reported to a private share register | UBO disclosure required internally; FATF-compliant regime |

Focus Points

- Taxation: Corporate income is taxed at the federal level at a flat 8.5% on profit after tax (effective ~7.83%), plus cantonal and communal taxes, bringing the combined effective rate to roughly 12–22% depending on canton; VAT applies at 8.1% standard rate; withholding tax of 35% applies to dividends, partially or fully refundable under applicable double tax treaties; a 1% issuance stamp duty applies on share capital contributions above CHF 1 million. See Swiss Federal Tax Administration for current rates.

- Treaty Access: Switzerland maintains one of the world's broadest DTT networks (100+ treaties); AG entities qualify for treaty benefits subject to substance and anti-abuse requirements.

- Annual Compliance: Mandatory annual general meeting (AGM); statutory financial statements required; audit obligation depends on company size (ordinary audit for large companies, limited audit for smaller ones, opting-out available for very small firms).

- Economic Substance: No formal substance scoring regime, but treaty benefits and cantonal tax rulings increasingly require demonstrable local management and operational activity.

- Conversion: An AG may be converted into a GmbH or other recognised Swiss legal form under the Swiss Merger Act (Fusionsgesetz) without liquidation.

Closing

The AG suits holding structures, group headquarters, IP-holding entities, and businesses seeking access to Swiss capital markets or institutional investors. Its main advantage is the established credibility and structural flexibility it offers; the primary limitation is the CHF 100,000 minimum capital requirement and comparatively heavier administrative obligations relative to the GmbH.

The AG is most appropriate for medium-to-large enterprises, holding companies, and any business that anticipates external investment, a future public listing, or complex multi-shareholder ownership arrangements.

Company Incorporation in Switzerland

Incorporate an Aktiengesellschaft (AG) or other Swiss entity with end-to-end support from registration through post-incorporation compliance.

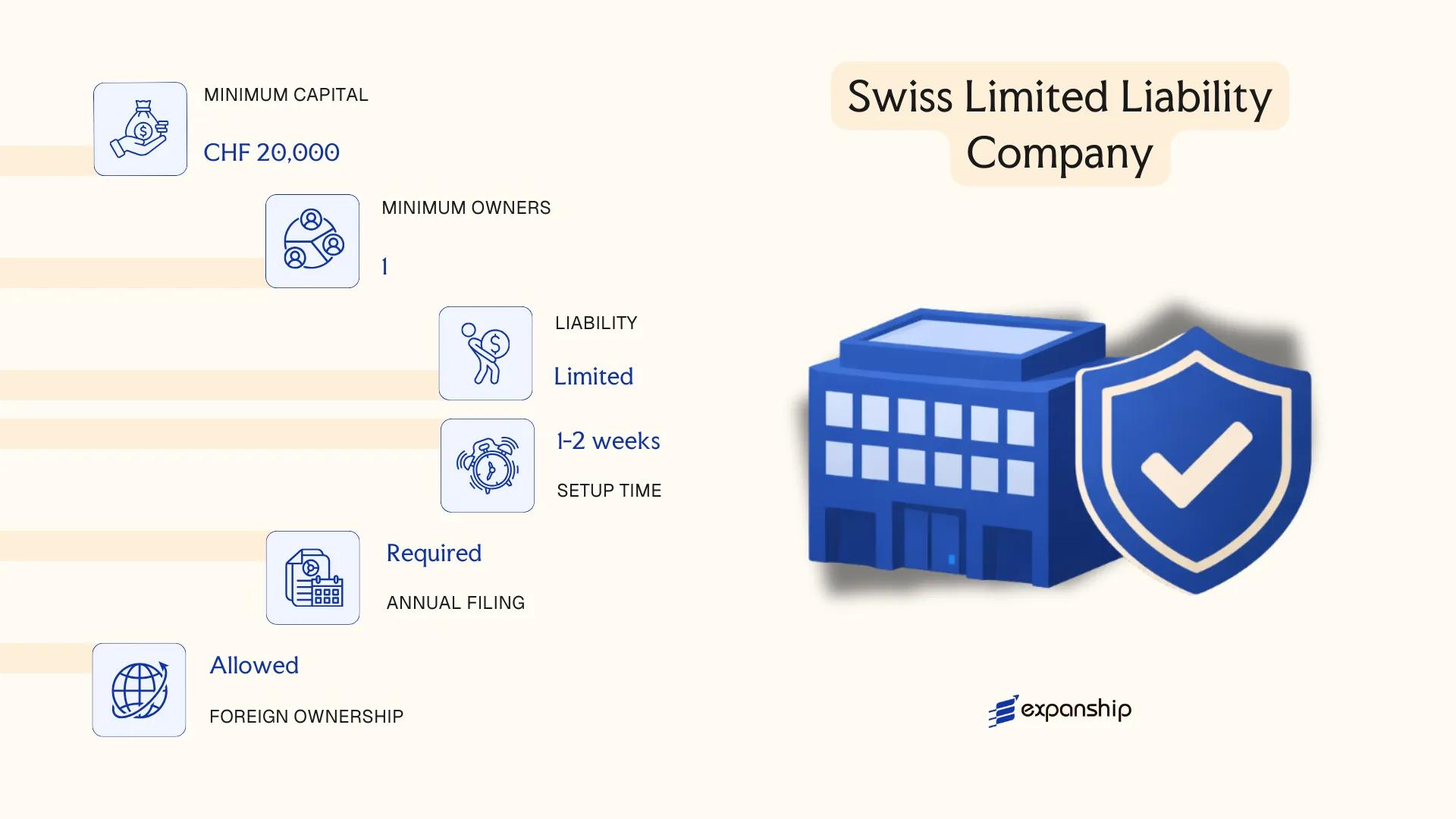

Gesellschaft mit beschränkter Haftung (GmbH) – Swiss Limited Liability Company

The GmbH Switzerland limited liability company is governed by the Swiss Code of Obligations (Obligationenrecht), specifically Articles 772–827, most recently revised under the Swiss company law reform effective January 2023. It carries separate legal personality, meaning the entity's obligations are distinct from those of its members.

Structurally, the Gesellschaft mit beschränkter Haftung Switzerland sits between a sole proprietorship and a full joint stock company. Member liability is capped at their capital contribution, and the entity is frequently chosen by small to mid-sized businesses seeking a formal structure without the higher capital requirements of an AG.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | GmbH (Gesellschaft mit beschränkter Haftung) | Registered with the relevant cantonal Commercial Registry (Handelsregisteramt) |

| Members | 1–unlimited quota holders (Gesellschafter); 1+ Managing Director (Geschäftsführer) | At least one Managing Director must be a Swiss resident |

| Capital | CHF 20,000 minimum share capital; fully paid-up at formation | Divided into quotas (Stammanteile) of at least CHF 100 each |

| Local Presence | Registered office in Switzerland required | A Managing Director resident in Switzerland satisfies the local presence requirement |

| Privacy | Quota holders and managers are listed in the public Commercial Registry | No beneficial ownership register exists at federal level; FINMA rules apply in regulated sectors |

Focus Points

- Taxation: Subject to cantonal and federal corporate income tax (effective combined rates typically range from approximately 11.9% to 21.6% depending on canton); VAT registration required once annual turnover exceeds CHF 100,000; withholding tax of 35% applies to dividend distributions; stamp duty (Emissionsabgabe) of 1% applies to equity contributions above CHF 1 million.

- Annual Compliance: Annual general meeting required; auditor appointment is mandatory only above certain size thresholds (opting out is permitted for smaller entities under Art. 727a CO).

- Economic Substance: No specific substance regime, but Swiss tax residency requires effective management and control to be exercised within Switzerland.

- Treaty Access: Qualifies for benefits under Switzerland's extensive double tax treaty network, subject to applicable anti-abuse provisions.

- Conversion: A GmbH may be converted into an AG under the Swiss Merger Act (Fusionsgesetz) without triggering a full liquidation.

A GmbH suits operating businesses, holding structures, and family-owned enterprises where control should remain closely held among a defined group of quota holders. The mandatory public disclosure of members in the Commercial Registry limits the privacy available to owners.

Swiss GmbH incorporation requirements make this structure most practical for small to medium-sized businesses and owner-managed operations where concentrated ownership and lower setup capital are priorities.

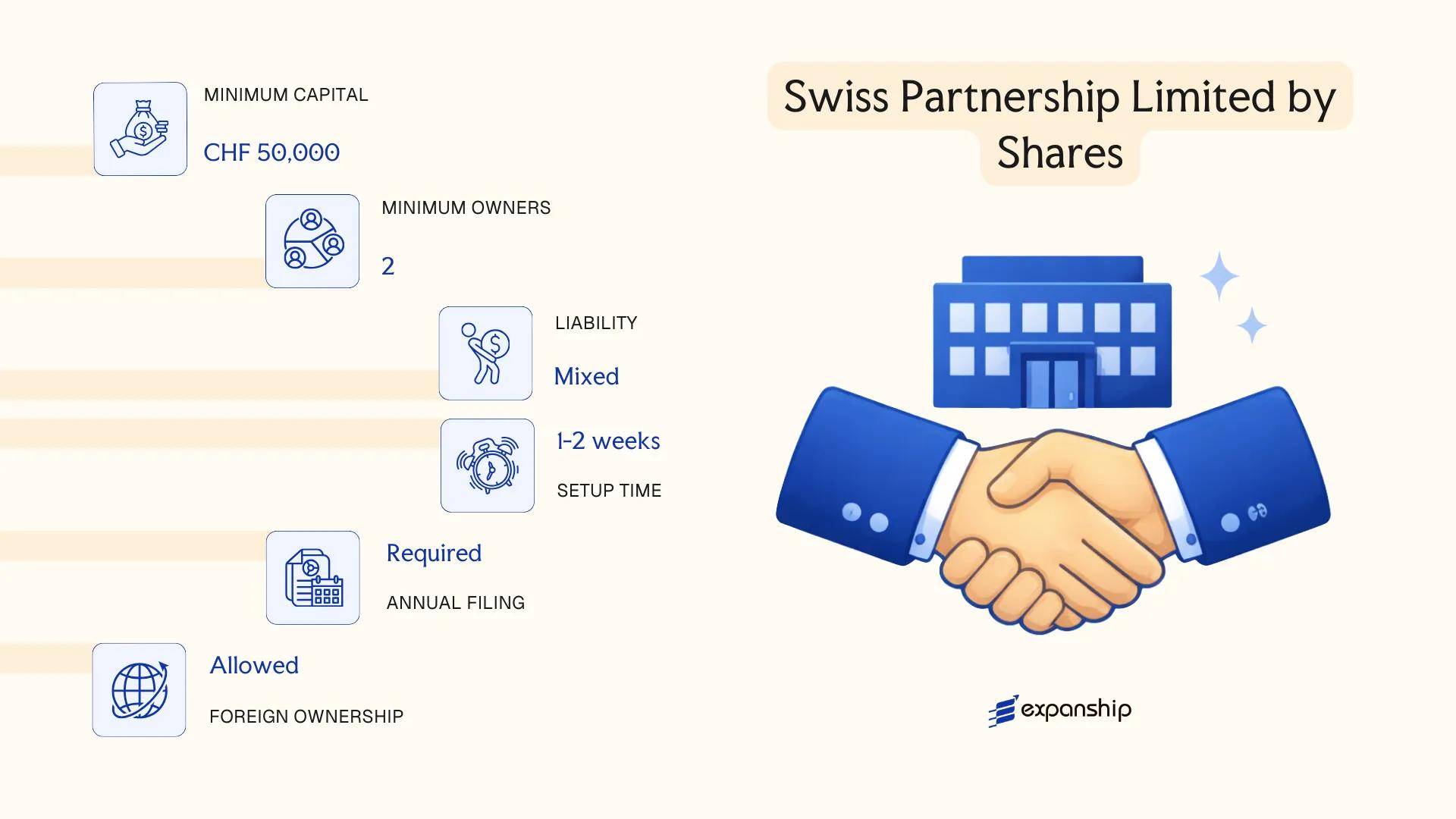

Kommanditaktiengesellschaft (KmAG) – Swiss Partnership Limited by Shares

The KmAG Switzerland partnership limited by shares is codified under Articles 764–771 of the Swiss Code of Obligations (OR). It is a hybrid structure: a corporate entity with full legal personality that combines the liability mechanics of a partnership with the share capital framework of an Aktiengesellschaft.

At least one general partner bears unlimited personal liability for the firm's obligations, while shareholders contribute capital and carry liability only up to their subscribed shares. This dual-track liability model makes the Kommanditaktiengesellschaft Switzerland a structurally complex entity, rarely used in commercial practice.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Kommanditaktiengesellschaft (KmAG) | Separate legal personality under OR Art. 764 |

| Members | At least 1 general partner (unlimited liability) + shareholders (no minimum number) | General partners must be natural persons |

| Capital | CHF 100,000 minimum share capital; fully subscribed at formation | Same threshold as the AG |

| Local Presence | Registered office in Switzerland required | No separate registered agent requirement under OR |

| Privacy | Shareholders not publicly disclosed; general partners appear in the Commercial Register | Commercial Register entry is mandatory |

Focus Points

- Taxation: Subject to federal corporate income tax (8.5% on profit), cantonal/communal taxes, Swiss VAT (if turnover exceeds CHF 100,000), withholding tax of 35% on dividends, and issuance stamp duty of 1% on share capital above CHF 1 million.

- Annual Compliance: Must file audited accounts; audit requirement depends on size thresholds under OR Art. 727.

- Treaty Access: Qualifies as a Swiss-resident entity for double tax treaty purposes, provided sufficient economic substance is maintained.

- Conversion: Can be converted into an AG or GmbH under the Swiss Merger Act (FusG) of 2004.

- Restrictions: General partners cannot simultaneously be shareholders in the same KmAG under OR Art. 765.

Closing Paragraph

The Swiss KmAG structure explained under the OR suits scenarios where founding partners wish to retain direct management control through unlimited-liability positions while raising equity capital from passive investors. Its principal drawback is that at least one individual must accept unlimited personal exposure, which significantly limits its appeal compared to fully limited-liability structures.

The KmAG is best suited for family-controlled businesses or founder-led ventures where one principal is prepared to assume unlimited liability while bringing in external share capital.

Partnerships in Switzerland [Kollektivgesellschaft, Kommanditgesellschaft]

Both the Kollektivgesellschaft and Kommanditgesellschaft Switzerland partnership forms are governed by the Swiss Code of Obligations (Obligationenrecht), specifically Articles 552–619. Neither structure carries separate legal personality under Swiss law, meaning partners bear direct liability for the firm's obligations.

Registration with the Commercial Register (Handelsregister) is mandatory once annual revenue exceeds CHF 100,000, though voluntary registration is permitted below that threshold. Upon registration, the partnership acquires the capacity to sue and be sued in its own name, a functional — though not legal — distinction from the partners themselves.

Key Characteristics

| Requirement | Kollektivgesellschaft | Kommanditgesellschaft |

|---|---|---|

| Legal Form | General partnership; no separate legal personality | Limited partnership; no separate legal personality |

| Members | Partners (Gesellschafter); minimum 2, no maximum; all natural persons | At least 1 general partner (Komplementär) + 1 limited partner (Kommanditär); limited partners may be legal entities |

| Liability | All partners: unlimited, joint and several | General partner: unlimited; limited partner: capped at registered contribution |

| Local Presence | Registered office in Switzerland required | Registered office in Switzerland required |

| Capital | No statutory minimum; contributions defined by partnership agreement | No statutory minimum; limited partner's contribution (Kommanditeinlage) must be registered |

| Privacy | Partner names disclosed in the Commercial Register | General and limited partner names publicly disclosed |

Focus Points

- Taxation: Partnerships are fiscally transparent — profits are attributed directly to partners and taxed at the individual level under cantonal and federal income tax; no entity-level corporate income tax applies; VAT registration is required once turnover exceeds CHF 100,000.

- Annual Compliance: No mandatory audit requirement; financial statements are not required to be filed publicly, but accounting records must be maintained in accordance with the Code of Obligations.

- Treaty Access: Because partnerships lack separate legal personality, access to Swiss double tax treaties is not available at the entity level; treaty benefits depend on the individual partner's residence.

- Conversion: A Kollektivgesellschaft can be converted into a Kommanditgesellschaft or a capital company (AG or GmbH) under Swiss transformation law (Fusionsgesetz).

Sub-Types

Kollektivgesellschaft (General Partnership)

All partners hold unlimited personal liability and are restricted to natural persons. The structure is typically used by professional service firms or family businesses where active management is shared equally among all partners.

Kommanditgesellschaft (Limited Partnership)

The distinguishing feature is the separation between the general partner, who manages the business and holds unlimited liability, and one or more limited partners whose exposure is confined to their registered capital contribution. This form suits arrangements where passive investors participate alongside an active managing partner.

Closing

Both structures are suited to smaller, closely held businesses or professional practices where simplified administration outweighs the need for limited liability. The absence of a minimum capital requirement reduces the barrier to formation, though unlimited personal liability for at least one partner remains a material exposure in both forms.

These structures are best suited for two or more individuals, typically in professional services or family-run businesses, who prefer low administrative overhead and are prepared to accept personal liability for the partnership's obligations.

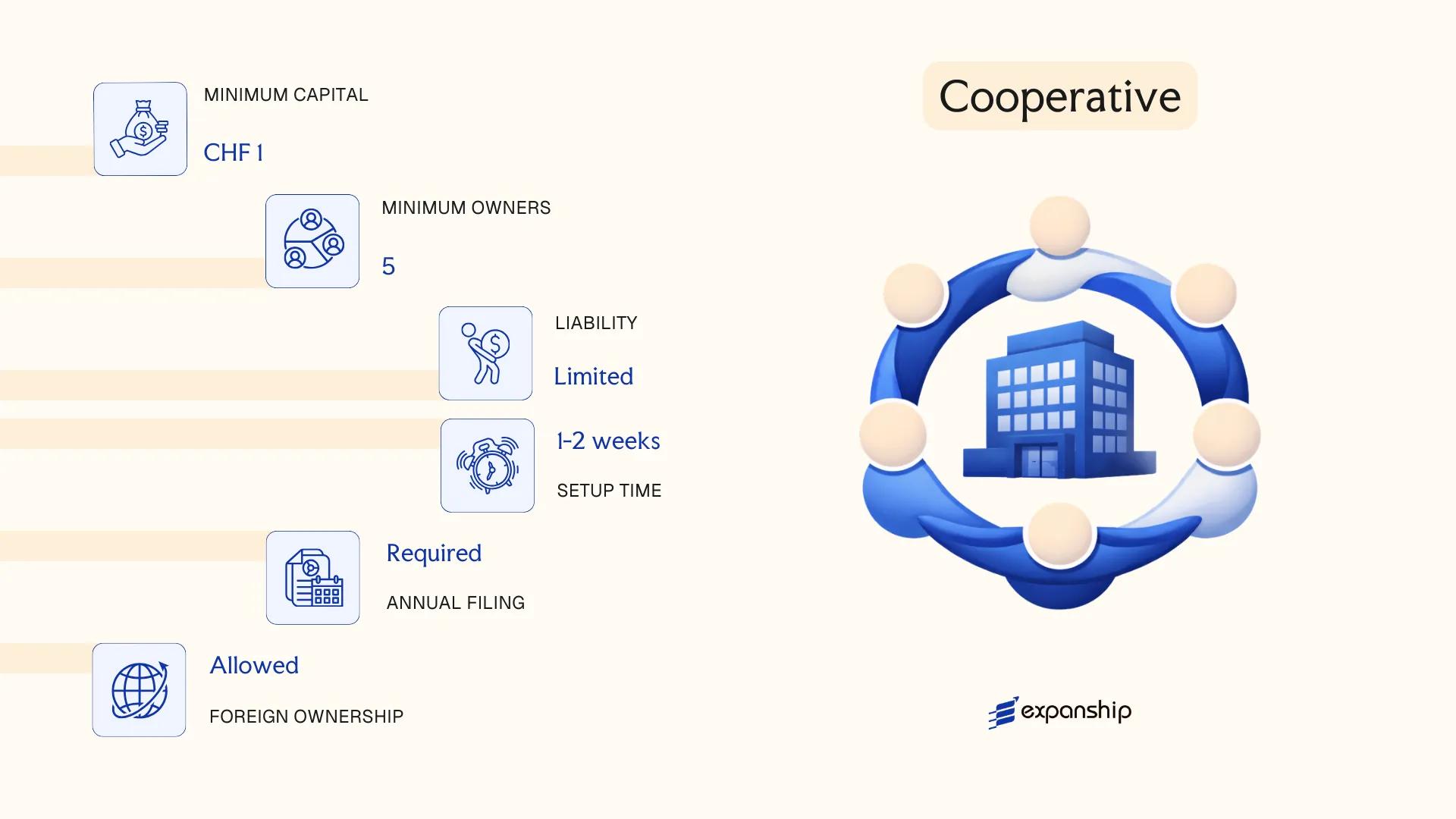

Cooperative (Genossenschaft)

Governed by Articles 828–926 of the Swiss Code of Obligations (1911), the Genossenschaft cooperative Switzerland registration process results in a distinct legal entity with separate legal personality. Unlike capital-based structures, it is organised around members rather than shares, making it structurally suited to collective economic activity, mutual aid, or shared service provision.

Liability is generally limited to the cooperative's own assets unless the statutes expressly provide for supplementary member liability. Membership is variable by design — the entity can admit or lose members without triggering a formal capital restructuring.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Cooperative (Genossenschaft) | Separate legal personality; governed by CO Arts. 828–926 |

| Members | Referred to as members (Mitglieder); minimum 7 at formation | No statutory maximum; membership is open and variable |

| Governing Bodies | General Assembly, Board of Directors, Auditors | Board must have at least 3 members drawn from membership |

| Local Presence | Registered office in Switzerland required | No mandatory resident director, but domicile address is obligatory |

| Capital | No minimum capital required | Statutes may define member contributions (Anteilscheine) |

| Privacy | Member register not publicly disclosed | Board members are listed in the Commercial Register |

Focus Points

- Taxation: Subject to federal corporate income tax (8.5% on profit), cantonal/communal taxes, VAT if turnover exceeds CHF 100,000, and withholding tax of 35% on distributed surpluses qualifying as income.

- Annual Compliance: Annual general assembly required; financial statements must be prepared, with mandatory audit depending on size thresholds under CO Art. 727.

- Treaty Access: Qualifies as a Swiss resident entity and can access Switzerland's tax treaty network, subject to beneficial ownership requirements.

- Conversion: Conversion to another legal form (e.g., AG or GmbH) is possible under Swiss transformation law (Fusionsgesetz, 2004) but requires member approval and regulatory filing.

- Restrictions: Cannot issue shares to outside investors; capital-raising options are structurally limited compared to joint-stock entities.

Cooperatives are most commonly used for agricultural organisations, housing associations, financial institutions (including cantonal banks), and consumer groups. The variable membership structure offers genuine operational flexibility, but the absence of tradeable equity makes external investment difficult to attract.

The Genossenschaft is most appropriate for member-driven organisations pursuing a shared economic purpose rather than external investor returns.

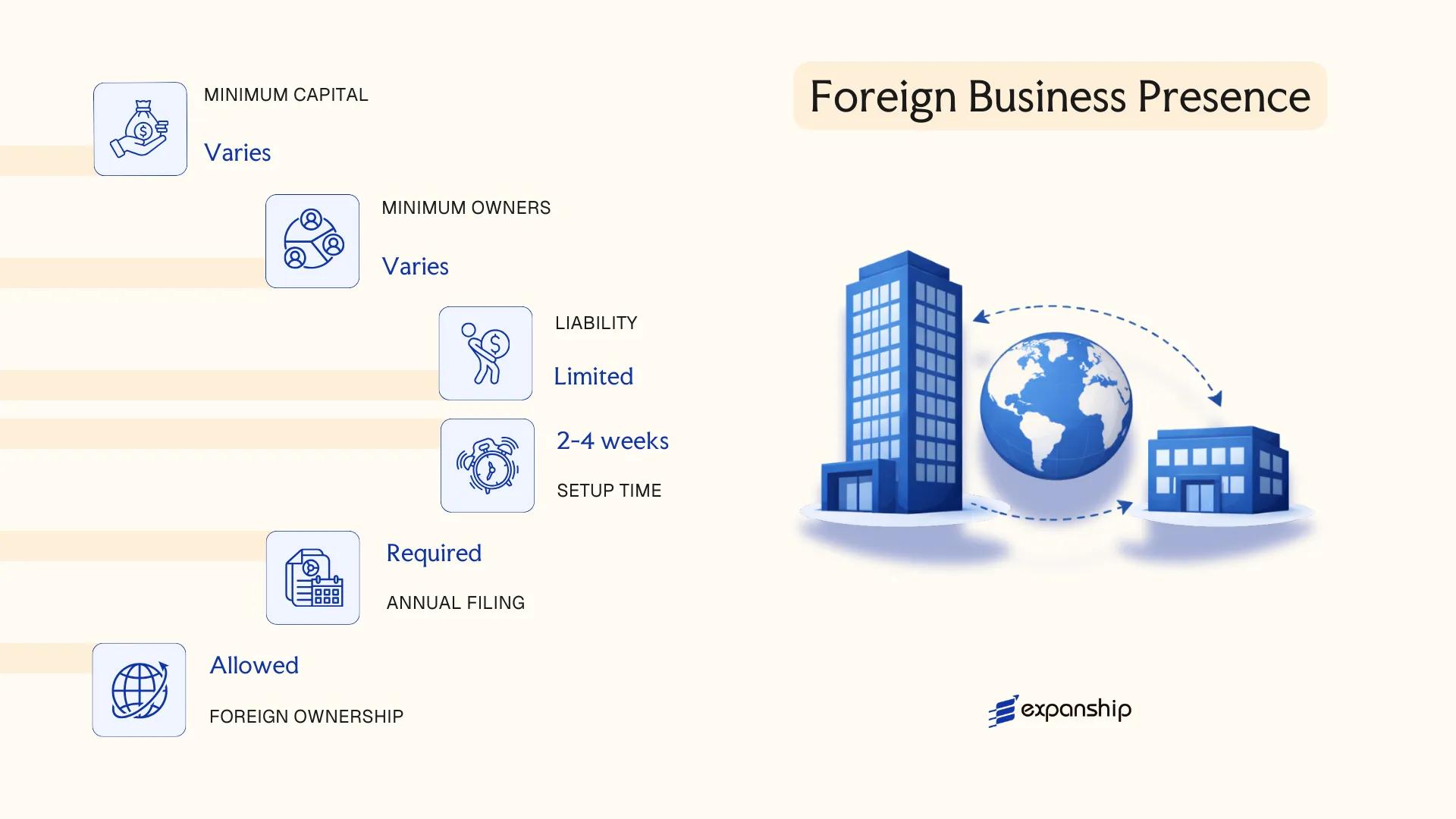

Foreign Business Presence in Switzerland [Branch Office, Representative Office, Subsidiary]

Registering a foreign company branch office Switzerland falls under the Swiss Code of Obligations (OR), which governs commercial registrations through the cantonal Commercial Register offices and the Federal Commercial Registry Office (EHRA). A branch office has no separate legal personality — it remains an extension of the parent company and carries the parent's liability. A subsidiary, by contrast, is incorporated as a distinct Swiss legal entity, typically as an AG or GmbH, and bears liability independently of its foreign parent.

Choosing between these structures affects tax exposure, liability, and administrative obligations. A representative office occupies a more limited position: it cannot conduct direct commercial activity or conclude contracts on behalf of the parent, restricting it primarily to market research and liaison functions.

Key Characteristics

| Requirement | Branch | Representative Office | Subsidiary |

|---|---|---|---|

| Legal Form | Extension of foreign parent | Informal presence; no separate registration required | Separate Swiss legal entity (AG or GmbH) |

| Legal Personality | None | None | Yes |

| Local Representative | Mandatory Swiss-resident authorised signatory | Not formally required | Board director with Swiss residency (AG) |

| Registered Address | Required in Switzerland | Required in Switzerland | Required in Switzerland |

| Capital Requirement | None (parent's capital applies) | None | CHF 100,000 (AG) / CHF 20,000 (GmbH) |

| Liability | Parent bears full liability | Parent bears full liability | Limited to subsidiary's own assets |

Focus Points

- Taxation: Branches are taxed on Swiss-sourced profits at cantonal and federal corporate income tax rates; withholding tax of 35% applies to dividends paid by subsidiaries; VAT registration is required at CHF 100,000 annual turnover; stamp duty applies to subsidiary equity contributions exceeding CHF 1 million.

- Treaty Access: Subsidiaries incorporated as Swiss entities generally qualify for Switzerland's double tax treaty network; branches may face limitations depending on treaty provisions and the parent's jurisdiction.

- Economic Substance: Branches must demonstrate genuine operational activity in Switzerland; purely nominal registrations without local activity attract scrutiny from cantonal tax authorities.

- Annual Compliance: Branches must file audited financial statements of the parent alongside local accounts; subsidiaries follow standard Swiss statutory reporting obligations.

- Conversion: A branch can be converted into a subsidiary, though the process requires re-registration as a new legal entity rather than a structural transformation under a single filing.

Sub-Types

Branch Office

A branch (Zweigniederlassung) must be registered in the cantonal Commercial Register where it operates and appoint at least one Swiss-resident authorised signatory with sole signing authority. It is commonly used by foreign firms entering the market before committing to full local incorporation.

Representative Office

No formal registration with the Commercial Register is required, but the office must not engage in revenue-generating activity. Foreign firms typically use this structure for preliminary market assessment or to support an existing client relationship managed from abroad.

Subsidiary

Incorporated as a standalone Swiss company under the OR, the subsidiary offers the clearest structural separation from the parent and full access to Switzerland's treaty network. It is the preferred form for firms with long-term operational or holding objectives.

A subsidiary suits foreign firms seeking full operational independence and treaty benefits, while a branch provides a lower-cost entry point with simpler setup but exposes the parent to direct liability. The representative office is functionally limited and appropriate only for non-commercial activities.

Foreign firms planning active Swiss operations or IP holding structures are best served by a subsidiary incorporated as an AG or GmbH, given the liability separation and access to Switzerland's double tax treaty network.

Sole Proprietorship (Einzelunternehmen)

The Einzelunternehmen sole proprietorship Switzerland represents the simplest business structure available under Swiss law. Governed primarily by the Swiss Code of Obligations (Obligationenrecht), it carries no separate legal personality — the owner and the business are one and the same entity in the eyes of the law.

Unlike capital companies, this form requires no minimum capital contribution and no formal deed of incorporation. Registration with the Commercial Register (Handelsregister) becomes mandatory once annual revenue exceeds CHF 100,000, though voluntary registration is permitted below that threshold.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sole Proprietorship | No separate legal personality; owner bears full personal liability |

| Owner | Single individual (proprietor) | Only natural persons may establish this form; corporations may not |

| Liability | Unlimited personal liability | All personal assets are exposed to business creditors |

| Local Presence | Swiss residential address required | Owner must be resident in Switzerland |

| Capital | No minimum capital | No paid-up or authorised capital requirement |

| Registration | Mandatory above CHF 100,000 annual revenue | Voluntary registration available below this threshold |

Focus Points

- Taxation: Subject to personal income tax at cantonal and federal levels on business profits; VAT registration required once turnover exceeds CHF 100,000; no separate corporate tax applies; no withholding tax on profit distributions since profits flow directly to the owner.

- Social Security: The proprietor must register with the relevant cantonal AHV compensation office and pay contributions as a self-employed person.

- Conversion: Can be converted into a GmbH or AG, though conversion triggers a formal reorganisation process under the Swiss Merger Act (Fusionsgesetz).

- Restrictions: Only one individual may own the business; the form cannot be used for activities requiring a licensed corporate entity.

Closing Paragraph

The Einzelunternehmen suits freelancers, consultants, and sole traders operating in a single canton with modest revenue and limited third-party liability exposure. Its principal advantage is administrative simplicity; the central limitation is unrestricted personal liability for all business debts.

Self-employed professionals and sole traders already resident in Switzerland who require a low-cost, low-formality structure for individual commercial activity.

How to Choose the Right Entity Type in Switzerland

Selecting the wrong legal form creates concrete, often costly consequences that are difficult to reverse once the entity is registered.

Why Your Entity Choice Matters

- Choosing a tax-exempt cooperative or foundation structure when you need access to Switzerland's double taxation agreement network means withholding tax reductions under those treaties may be unavailable to your business.

- Forming an AG when a single-person consultancy is the intended activity triggers mandatory audit thresholds and associated costs that serve no operational purpose.

- Selecting a structure without adequate local substance when Swiss tax authorities apply the substance-over-form doctrine can result in the entity being reclassified for tax purposes, with back assessments and penalties attached.

- Incorporating a commercial entity when the underlying need is asset protection or succession planning locks the structure into annual general meeting obligations and shareholder disclosure requirements that a foundation would not carry.

Key Factors to Consider

- Business Activity: Active trading, passive asset holding, and regulated sectors such as banking or collective investment schemes each require distinct legal forms under the Code of Obligations and relevant supervisory frameworks.

- Ownership and Management: Single-owner operations favour the GmbH or Einzelunternehmen, while multi-investor arrangements may require the board governance structure of an AG.

- Tax Objectives: Your need for full cantonal tax exemption, participation relief, or treaty access determines which entity and domicile canton to select.

- Substance Capacity: If you cannot maintain genuine management and staff locally, structures with lower substance thresholds warrant consideration.

- Exit Strategy: Not all Swiss entity types permit redomiciliation or conversion without dissolution; confirm this before formation.

Compliance Services for Companies in Switzerland

Conclusion

Switzerland offers a defined set of legal structures, each calibrated to distinct ownership profiles and operational purposes. This Switzerland company formation conclusion guide reflects a framework governed primarily by the Swiss Code of Obligations and overseen at the cantonal level by the Commercial Registry offices.

The AG suits publicly tradeable or investor-backed ventures; the GmbH serves closely held private businesses with defined ownership. Partnerships carry unlimited liability and fit smaller professional arrangements. The KmAG remains a specialist structure, rarely used in practice. Cooperatives serve member-driven economic activity, and the Einzelunternehmen functions for sole operators at low initial cost.

The GmbH is the most commonly registered entity among new formations. Regulatory direction continues toward increased transparency, with Switzerland progressively aligning its reporting standards with OECD frameworks. Selecting the appropriate structure is a decision with lasting legal and fiscal consequences — one that merits careful, jurisdiction-specific analysis before registration proceeds.

How Expanship Can Assist You

Expanship's Switzerland incorporation services cover the full formation process for every entity type discussed in this guide, from the AG and GmbH to branch registrations filed with the relevant cantonal Commercial Register (Handelsregister). Our team works directly with SECO and cantonal registry offices to ensure your filings meet current requirements under the Swiss Code of Obligations.

From document preparation to post-incorporation compliance, our Switzerland company registration assistance covers the practical steps that follow a formation decision:

- Drafting and notarization of articles of incorporation and founding documents

- Registered address and agent provision across Swiss cantons

- Filing coordination with the cantonal Handelsregister

- Share capital deposit and attestation support

- Post-incorporation compliance management, including annual obligations

- Banking introduction assistance for corporate account opening

Get in touch with Expanship Switzerland to discuss your specific situation and the right structure for your business.

Frequently Asked Questions (FAQ)

The Aktiengesellschaft (AG) is the most widely registered corporate form. Its transferable shares, established governance framework under the Swiss Code of Obligations, and broad acceptance among institutional counterparties make it the default choice for mid-to-large enterprises.

Both are capital-based entities with limited liability, but the AG requires a minimum share capital of CHF 100,000 compared to CHF 20,000 for a GmbH. Shareholders of an AG are not listed in the Commercial Register, whereas GmbH members and their capital contributions are publicly disclosed, resulting in a lower privacy threshold for the GmbH.

The AG offers greater ownership privacy, as shareholder identities are not entered in the Commercial Register. Bearer shares were abolished under the 2019 amendments to the Code of Obligations, so registered shares are now mandatory, but these remain outside public disclosure. Nominee shareholding arrangements are legally permissible.

A sole proprietorship (Einzelunternehmen) and an AG can each be formed by one individual. A GmbH also permits a single member. Kollektivgesellschaft and Kommanditgesellschaft partnerships each require at least two partners by statutory definition.

Foreigners may form an AG, GmbH, or branch office without restrictions on share ownership. However, at least one director with signatory authority must be domiciled in Switzerland, regardless of entity type, per the requirements administered through the relevant cantonal Commercial Registry (Handelsregisteramt).

Structural conversions are governed by the Swiss Merger Act (Fusionsgesetz), which permits transformation between certain entity types, including conversion of a GmbH into an AG and vice versa. The process requires notarial involvement, creditor notification periods, and re-registration with the Commercial Register.

No. The Kollektivgesellschaft and Kommanditgesellschaft are not separate legal persons; partners bear personal liability for obligations of the firm. The AG, GmbH, KmAG, Genossenschaft, and registered branches of foreign companies each hold distinct legal standing under Swiss civil law.

The Einzelunternehmen carries the lightest compliance burden, with no mandatory audit, no board requirements, and simplified accounting obligations for firms below the statutory thresholds set under the Code of Obligations. Registration with the Commercial Register only becomes compulsory once annual revenue exceeds CHF 100,000.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.