Key Takeaways

- Bermuda's exempted companies are governed by the Companies Act 1981, which imposes ongoing compliance obligations — including mandatory local registered office maintenance — that add recurring costs regardless of whether the company conducts any active business.

- Foreign-owned structures face limited access to double tax treaties, reducing Bermuda's utility for businesses that rely on treaty networks to manage withholding tax exposure across multiple jurisdictions.

- Economic substance requirements force certain Bermuda-registered entities to demonstrate genuine local activity, creating operational and staffing burdens that can be difficult to satisfy given the island's limited local talent pool and elevated cost base.

- Banking access presents a practical obstacle, as Bermuda's international reputation as an offshore centre leads many correspondent banks to apply heightened due diligence to Bermuda-incorporated entities, slowing account opening and increasing compliance scrutiny.

Bermuda operates under a well-established and heavily regulated corporate framework, overseen primarily by the Registrar of Companies and the Bermuda Monetary Authority. The Companies Act 1981 remains the primary legislation governing company formation and ongoing compliance obligations.

The disadvantages of incorporating in Bermuda span cost structures, regulatory requirements, banking access, and operational constraints — each examined separately in this article.

Not every drawback applies equally across all structures. A holding company with no local operations faces a different compliance burden than an insurance entity or a fund vehicle requiring BMA licensing.

This article is most relevant to foreign investors and business owners considering an exempted company — the structure most commonly used by non-residents — who need a realistic picture of the Bermuda company formation drawbacks before committing to the jurisdiction.

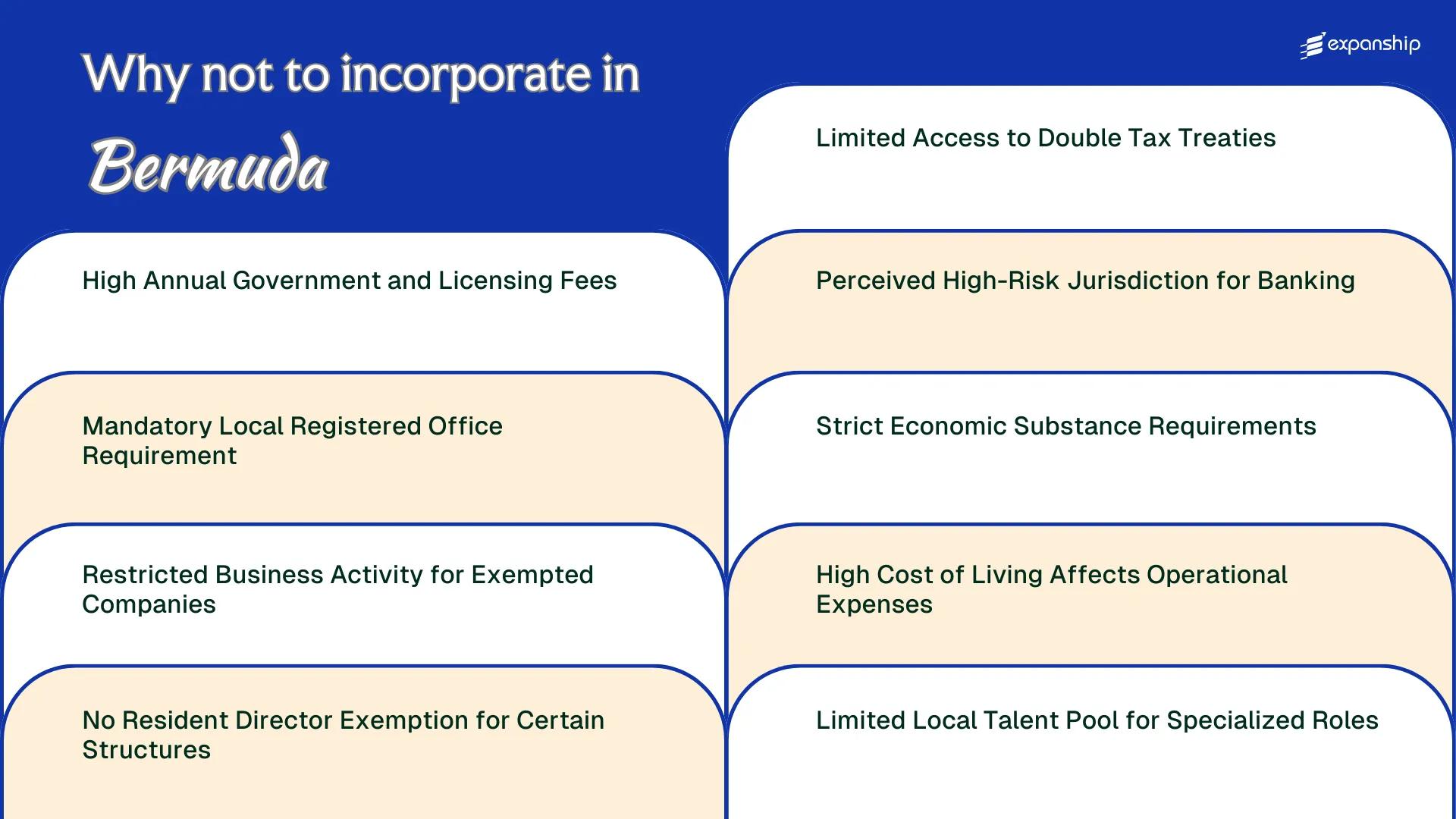

High Annual Government and Licensing Fees

Bermuda annual government fees drawbacks are a recurring concern for foreign incorporators, particularly those operating through exempted companies. The cost structure goes beyond initial registration and creates predictable annual pressure on your operating budget.

Annual Government Fees for Exempted Companies

Under the Companies Act 1981, exempted companies pay annual government fees scaled to their authorised share capital. A company with authorised capital up to $12,000 pays a baseline fee, but as capital increases, the fee scales upward significantly, reaching into the tens of thousands of dollars for larger capital structures. This tiered model means that entities capitalised to attract investor confidence can face disproportionately high Bermuda company registration fees simply for maintaining their legal standing.

Licensing and Regulatory Fees Add Further Cost

Regulated entities face an additional layer of charges through the Bermuda Monetary Authority, which imposes annual licensing fees that vary by licence category and business volume. A Class E insurer, for example, faces fees that can exceed $100,000 annually. For a foreign business owner running a holding or investment structure, these costs apply regardless of whether the company generates active revenue in a given year.

Annual government and licensing fees in Bermuda accrue whether or not your company is operationally active, meaning a dormant or pre-revenue entity still carries a substantial fixed compliance cost each year.

Mandatory Local Registered Office Requirement

Every company incorporated under the Companies Act 1981 must maintain a registered office in Bermuda at all times. This is not a procedural formality — it is a statutory obligation that requires your business to engage a locally licensed corporate service provider, generating a recurring cost that exists regardless of whether your company trades or generates revenue.

Unlike some jurisdictions where a postal address satisfies the requirement, Bermuda demands a functioning registered office address serviced by an authorised entity. For a foreign business owner with no physical presence on the island, this means an unavoidable dependency on third-party providers.

This dependency creates several layers of operational friction:

- Annual service fees for registered office providers add a fixed cost that compounds against the already elevated government fees your entity must pay

- Switching providers requires formal notification to the Registrar of Companies, creating administrative delays during periods of restructuring

- Service providers set their own fee schedules, so your costs can increase at renewal with limited alternatives given the small pool of licensed operators on the island

- Any lapse in the registered office arrangement — even briefly — places the company in breach of the Companies Act 1981, exposing it to regulatory action

The obligation applies to all company types, including exempted companies, which are the structure most foreign investors use.

Company Incorporation in Bermuda

Understand the full compliance obligations before incorporating in Bermuda, including registered office requirements and ongoing maintenance costs.

Restricted Business Activity for Exempted Companies

Under the Bermuda Companies Act 1981, an exempted company is explicitly prohibited from conducting business within Bermuda, except in specific, narrow circumstances. This is the foundational Bermuda exempted company business restriction that many foreign founders underestimate when structuring their operations.

The practical consequence is significant. Your entity cannot solicit local clients, employ staff to serve a Bermudian customer base, or enter contracts directed at the domestic market without breaching its exempted status.

| Activity | Permitted for Exempted Company | Restriction Severity |

|---|---|---|

| Conducting business with Bermuda residents | No | Absolute prohibition |

| Owning local real estate for operations | Restricted | Requires separate consent |

| Employing Bermudians for local sales | No | Prohibited without license |

| Dealing with other exempted companies | Yes (limited) | Conditional only |

| International business transactions | Yes | Core permitted purpose |

Exempted companies may only interact with the local economy through a defined list of permitted dealings, such as contracting with other exempted entities or using professional services locally. Any activity outside that list requires a separate license or consent from the Bermuda Monetary Authority, adding regulatory friction and cost.

For businesses that evolve over time, this creates a structural constraint. If your firm develops a product or service with Bermudian market potential, the exempted structure cannot simply be adapted. A separate licensing regime or entity would be required, which means duplicate compliance obligations and additional government fees.

No Resident Director Exemption for Certain Structures

Under the Companies Act 1981, exempted companies, which are the most commonly used structure by foreign investors, are required to have at least one director who is a natural person. No statutory exemption permits a fully corporate board for this structure.

This creates a direct compliance cost. You must either appoint a qualified local director or engage a professional nominee director service, both of which carry ongoing fees and contractual obligations.

Unlike some offshore jurisdictions that permit entirely nominee or corporate director arrangements without residency conditions, Bermuda imposes this requirement on exempted companies without a carve-out based on company size, ownership structure, or activity type.

The Bermuda Monetary Authority and the Registrar of Companies both maintain oversight of corporate governance standards, meaning non-compliance is not a low-risk oversight. Failures in director appointment obligations can affect a company's good standing status.

- At least one director must be a natural person under the Companies Act 1981

- No size-based or activity-based exemption removes this requirement for exempted companies

- Professional nominee director arrangements must be formally documented and maintained

- Director details must be accurately filed and kept current with the Registrar of Companies

- Non-compliance with director requirements can affect the company's good standing certificate

Bermuda does not require that the mandatory natural person director be a Bermuda resident, but finding a willing, qualified non-resident director willing to accept fiduciary liability for a Bermuda exempted company is often harder and more expensive than founders expect.

Limited Access to Double Tax Treaties

Bermuda double tax treaty limitations present a structural gap that most incorporated entities cannot work around through planning alone. The island operates outside the major bilateral tax treaty networks entirely.

The Scope of the Gap

Bermuda has not entered into comprehensive double taxation agreements with major economies such as the United States, the United Kingdom, or EU member states. Your business income may therefore be taxed in the source country without any treaty-based relief mechanism to reduce or eliminate that liability.

The limited tax agreements Bermuda companies can rely on are restricted to a narrow set of Tax Information Exchange Agreements (TIEAs) and a handful of arrangements under the OECD framework, none of which provide the dividend withholding or royalty relief that a full DTA would offer. For a firm routing cross-border income through a Bermuda entity, this translates into higher effective tax costs in counterparty jurisdictions.

Practical Consequences for Foreign Investors

Bermuda tax treaty risks become particularly acute for businesses earning passive income from foreign subsidiaries, since withholding taxes applied at source remain unreduced. Jurisdictions such as the Netherlands or Singapore, by contrast, maintain treaty networks spanning 90 or more countries, offering negotiated withholding rates that a Bermuda-registered entity simply cannot access.

Assessing Treaty Exposure for Your Bermuda Entity

Understand how the absence of double tax treaties affects your cross-border income structure and what this means for your specific business model.

Perceived High-Risk Jurisdiction for Banking

Bermuda's status as a perceived high-risk jurisdiction for banking creates real friction when opening and maintaining corporate accounts. Many international banks apply enhanced due diligence to entities incorporated there, which translates directly into delays, additional documentation demands, and outright rejections.

- Correspondent banks in the US and EU frequently flag Bermuda-registered entities during compliance screening, forcing your business to justify its structure before basic account functions are approved.

- The Financial Action Task Force (FATF) and EU AML frameworks treat offshore incorporation jurisdictions with zero corporate tax as elevated-risk categories, triggering mandatory enhanced due diligence reviews for your entity.

- Bermuda offshore banking restrictions mean that even locally licensed banks may require extensive beneficial ownership documentation under the Proceeds of Crime Act 1997 before onboarding a new corporate client.

- Payment processors and fintech platforms frequently apply the same risk classification as traditional banks, limiting your firm's access to merchant accounts and digital payment infrastructure.

- Exempted companies with no local business activity face the steepest scrutiny, as the absence of Bermuda-sourced revenue signals to compliance officers that the structure exists primarily for tax positioning.

Strict Economic Substance Requirements

Bermuda economic substance requirements risks are among the most operationally demanding compliance obligations facing foreign business owners under the Economic Substance Act 2018. Entities engaged in "relevant activities" — including holding company business, intellectual property business, and finance and leasing — must demonstrate genuine core income-generating activity on the island.

That requirement has direct cost implications. Your entity must maintain adequate physical presence, employ qualified personnel locally, and incur operational expenditure proportionate to the level of activity conducted in the jurisdiction.

The Bermuda Economic Substance Act challenges are especially acute for holding structures or IP-holding companies, where the substance threshold is high relative to the passive nature of the activity. Failure to satisfy the test exposes the entity to escalating financial penalties under the Act and potential disclosure to foreign tax authorities.

The Registrar of Companies is the primary enforcement body and has authority to assess compliance annually. Even a well-structured entity can fall short if local staffing or spending levels do not meet the standard applied in a given year.

A foreign-owned IP holding company with two part-time local contractors and no dedicated office lease could face a first-year penalty of up to BD$250,000 under the Economic Substance Act 2018 for failing to meet the adequate people and premises threshold — a cost that exceeds annual fees in most comparable low-tax jurisdictions.

High Cost of Living Affects Operational Expenses

Bermuda high cost of living business drawbacks are not incidental — they are structural. The island's geographic isolation means virtually all consumer goods, construction materials, and office supplies are imported, and import duties under the Customs Tariff Act compound those base costs before goods even reach your supplier's shelf.

Office rents in Hamilton, the primary commercial district, consistently rank among the highest in the Atlantic region. For a foreign-owned exempted company requiring physical space or local administrative staff, that cost is unavoidable rather than discretionary.

Salary expectations among local professionals reflect the broader cost environment. Hiring even administrative or paralegal support locally can cost significantly more than equivalent roles in comparable offshore centers such as the Cayman Islands or the Channel Islands.

- Imported office equipment and supplies carry layered customs duties

- Local vendor and contractor rates reflect elevated consumer prices island-wide

- Expatriate staff packages typically include housing allowances, which inflates your payroll overhead beyond base salaries alone

These expenses accumulate even for entities with minimal physical operations, since maintaining a registered presence still requires locally sourced services.

Even an exempted company with no local employees will incur above-average costs for registered office services, local compliance agents, and government-mandated filings, none of which are priced in line with lower-cost offshore jurisdictions.

Limited Local Talent Pool for Specialized Roles

Bermuda's population sits at roughly 64,000 people, making it one of the smallest jurisdictions by resident workforce in the Atlantic. For foreign firms requiring specialists in areas such as actuarial science, fintech development, or advanced legal compliance, the Bermuda limited local talent pool risks become an immediate operational constraint.

Sourcing talent externally means working through the work permit system administered by the Department of Immigration under the Immigration and Protection Act 1956. Each permit is role-specific and term-limited, adding both administrative overhead and renewal uncertainty that can disrupt continuity for senior hires.

Hiring difficulties Bermuda companies face are compounded by the Bermudianization policy, which requires employers to demonstrate that no qualified local candidate was available before a permit is granted. This process delays onboarding timelines in ways that would not occur in larger jurisdictions with open labour markets.

Workforce restrictions present a direct cost implication as well. Competitive expatriate compensation packages, housing allowances, and relocation costs are standard expectations for foreign hires, all of which feed into the firm's fixed operational expenses.

Overcoming Bermuda Incorporation Challenges

Overcoming Bermuda incorporation challenges requires structural planning before formation, not reactive adjustments after registration. The fee burdens, substance obligations, and banking friction covered in this blog each respond to specific structural decisions made at the outset.

- Engage a licensed local registered agent in Bermuda to satisfy the mandatory registered office requirement under the Companies Act 1981.

- Pre-qualify your exempted company's intended activities against the permitted scope to avoid post-registration restrictions on local business operations.

- Assess economic substance compliance requirements under the Economic Substance Act 2018 before selecting your entity's jurisdiction of management.

- Open banking relationships early, using a clean corporate structure that clearly documents beneficial ownership to address correspondent banking concerns.

- Budget for annual government fees and escalating operational costs during the pre-incorporation financial modelling phase.

These steps operate within a framework overseen by the Registrar of Companies. Addressing compliance gaps after incorporation is significantly more resource-intensive than building a compliant structure from the start.

Bermuda Still a Viable Jurisdiction

The drawbacks covered throughout this blog are real and carry material cost and compliance implications. That said, Bermuda jurisdiction viability despite drawbacks holds up when assessed against the full picture — the island's political stability, absence of corporate income tax, and well-established legal framework under the Companies Act 1981 continue to attract holding companies, reinsurers, and international business structures.

| Pros | Cons |

|---|---|

| No corporate income tax, capital gains tax, or withholding tax under Bermuda law | Annual government fees are among the highest in the offshore world, scaling with authorised share capital |

| The Companies Act 1981 provides a mature, English-based legal framework with strong creditor and shareholder protections | Exempted companies are barred from conducting business within Bermuda, limiting operational flexibility |

| Bermuda's regulatory reputation supports credibility with institutional counterparties | Access to double tax treaties is extremely limited, creating exposure for cross-border income flows |

| The Bermuda Monetary Authority is a recognised, well-resourced financial regulator | Economic substance requirements under the Economic Substance Act 2018 impose ongoing compliance obligations |

| No requirement for local shareholders in an exempted company structure | A restricted local talent pool drives up the cost of hiring qualified personnel on the island |

Banking access remains a practical friction point, and the cost of maintaining physical or functional presence is substantial relative to many competing jurisdictions.

Compliance Services for Companies in Bermuda

Understand the ongoing compliance obligations for Bermuda exempted companies, including economic substance filings, annual government fee submissions, and registered office requirements under the Companies Act 1981.

Conclusion

Bermuda incorporation drawbacks summary points to a jurisdiction that carries genuine structural costs: high government fees, restrictive economic substance obligations under the Economic Substance Act 2018, and limited access to double tax treaties create real friction for certain business models. Banking access remains a persistent operational challenge. These are not theoretical risks. Firms that have mapped out their compliance requirements and cost projections against the regulatory framework administered by the Registrar of Companies are better positioned to manage what the jurisdiction actually demands.

Expanship's Bermuda Incorporation Support

From the annual government fees set by the Registrar of Companies to Bermuda's economic substance obligations, the compliance burden on an exempted company adds up quickly. Expanship's Bermuda incorporation support services help your business manage these requirements methodically, reducing the administrative weight without overstating what professional assistance can change about the jurisdiction itself.

Our team supports clients across the full formation and post-registration process. Services include:

- Preparing and filing company registration documents with the Registrar of Companies

- Providing a compliant registered agent and local office address in Bermuda

- Handling government submissions and liaising with relevant regulatory authorities on your behalf

- Managing ongoing compliance obligations after your entity is operational

- Facilitating introductions to banking institutions familiar with Bermuda-incorporated structures

- Coordinating tax registration and correspondence with local authorities as required

Reach out to Expanship Bermuda to discuss your incorporation requirements directly.

Frequently Asked Questions (FAQ)

The restriction applies specifically to exempted companies under the Companies Act 1981, which prohibits these entities from conducting business within Bermuda except in limited circumstances permitted by the Act or under a specific licence. The exemption was designed for internationally focused businesses, so the restriction is structural rather than incidental. If your intended operations involve local Bermudian customers or suppliers in a direct commercial relationship, an exempted company structure may be legally insufficient without additional authorisation.

Under the Economic Substance Act 2018, first-instance non-compliance can attract a penalty of up to BD$250,000, with higher penalties for continued failure. The Bermuda Registrar also has authority to share non-compliance information with foreign tax authorities in the jurisdictions where beneficial owners are resident. That reporting mechanism creates potential tax exposure in your home country beyond the direct Bermudian penalty.

Annual government fees for an exempted company in Bermuda are calculated based on the company's authorised share capital, and for mid-to-large-capitalised entities these fees can exceed BD$30,000 per year. Unlike many competing offshore jurisdictions, Bermuda does not offer a flat low-cost fee structure for high-capital entities. When combined with mandatory registered office fees payable to a licensed service provider, the annual fixed cost base is considerably higher than jurisdictions such as the Cayman Islands or BVI.

Bermuda faces comparable correspondent banking challenges to other offshore financial centres, but its position on various international watchlists and its association with reinsurance and high-net-worth structures draws additional scrutiny from compliance departments at major international banks. Opening a corporate bank account for a newly incorporated Bermuda entity without a substantive operational footprint or established institutional relationships is genuinely difficult. Some entities wait several months before securing a functional banking relationship, which delays operational launch.

Maintaining a registered office in Bermuda through a licensed service provider is a statutory requirement under the Companies Act 1981, not an optional administrative step. If this requirement lapses, the Registrar of Companies can initiate proceedings to strike the company off the register, which voids its legal standing and can create significant downstream issues for any contracts, licences, or regulatory approvals the entity holds. Reinstatement is possible but involves additional fees and filings that disrupt business continuity.

The limitation cannot be avoided through the Bermuda entity itself, since Bermuda has not entered into a broad network of double tax treaties and the OECD's BEPS framework restricts the use of conduit arrangements designed to access treaty benefits through a non-treaty jurisdiction. If your business requires treaty protection for dividend flows, royalties, or interest payments, the Bermuda entity will not provide that benefit directly. Structuring a holding layer in a jurisdiction with an applicable treaty may address the gap, but it adds structural complexity and cost.

The constraint is most acute for entities that must demonstrate genuine economic substance, since the Economic Substance Act 2018 requires that qualified employees and management be physically present in Bermuda for relevant activities. For pure holding structures with minimal activity, the talent pool issue is less operationally significant, though finding and retaining local directors or officers with relevant sector expertise remains a real challenge. The cost of relocating specialised staff from abroad is compounded by Bermuda's high cost of living, which directly inflates salary expectations.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.