Key Takeaways

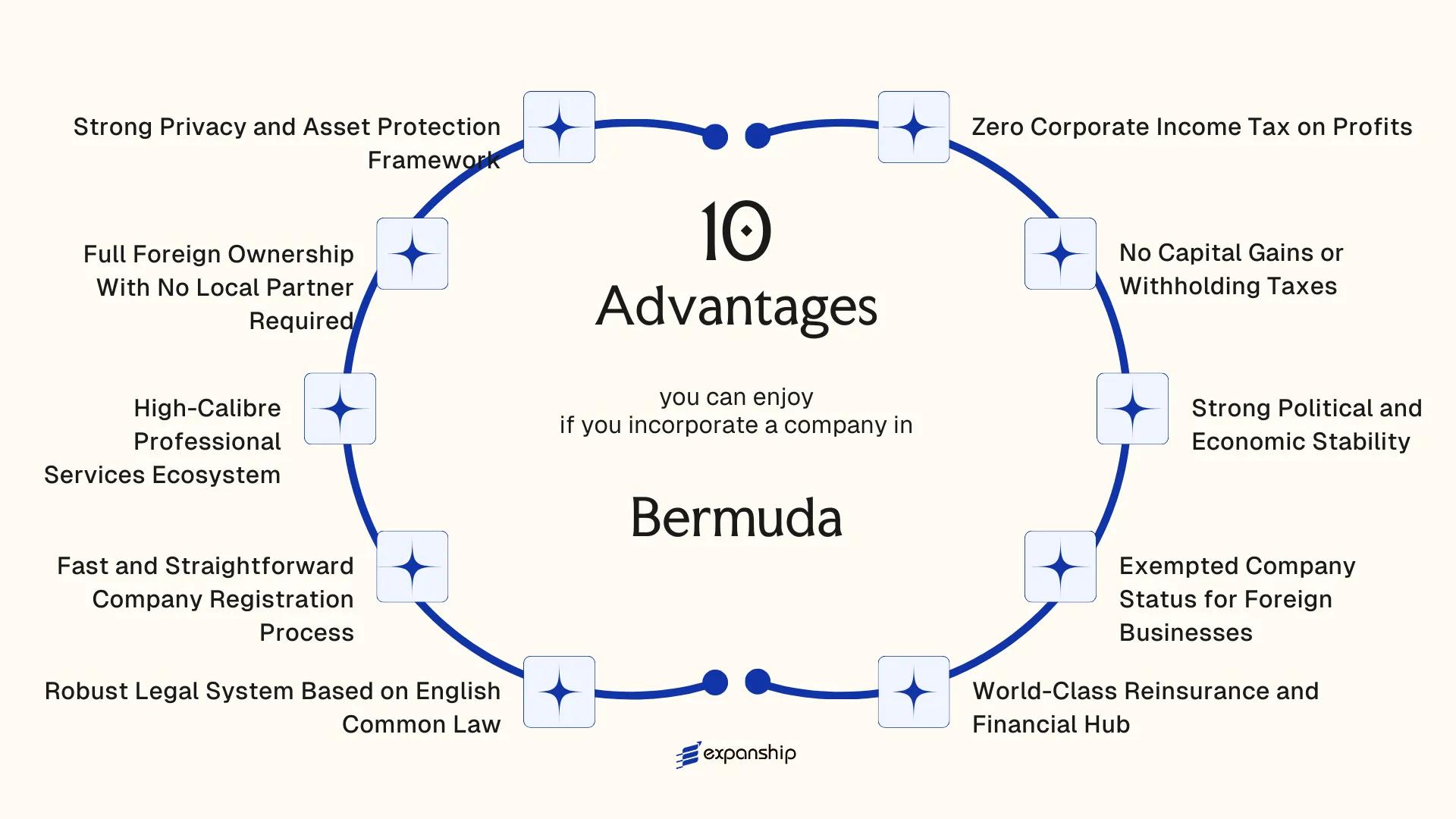

- Exempted companies incorporated in Bermuda pay zero corporate income tax, capital gains tax, or withholding tax, and those protections are legally formalised under the Exempted Undertakings Tax Protection Act — reducing the risk that future legislative changes will erode the tax position.

- Foreign investors can hold 100% ownership of a Bermuda exempted company without a local partner or resident shareholder, removing a structural constraint that increases cost and complexity in many competing jurisdictions.

- Bermuda's concentration of reinsurance carriers, captive managers, and fund administrators means that businesses in those sectors gain access to a specialist counterparty ecosystem that is commercially difficult to replicate elsewhere.

- Because the jurisdiction's legal system is grounded in English common law and its courts carry a documented track record on commercial disputes, contractual and corporate matters can be resolved within a familiar, predictable framework.

Bermuda is a self-governing British Overseas Territory situated in the North Atlantic Ocean, approximately 1,070 kilometres east of North Carolina. Company registration falls under the oversight of the Registrar of Companies, the statutory authority responsible for incorporating and maintaining records of all legal entities on the island. Foreign businesses most commonly establish a presence through an exempted company.

The territory operates a zero-tax regime, imposing no corporate income tax, capital gains tax, or withholding tax on companies incorporated there. Foreign ownership is broadly welcomed, and no local partner or resident shareholder is required to form a business entity — a policy that has attracted substantial foreign direct investment across multiple sectors. This article covers the principal benefits of incorporating in Bermuda for international businesses evaluating the jurisdiction as part of their corporate structure.

Zero Corporate Income Tax on Profits

Bermuda imposes no corporate income tax on profits earned by companies incorporated there. This makes the Bermuda zero corporate income tax benefit directly material to your bottom line, not just a headline figure.

What the Law Actually Provides

Under the Exempted Undertakings Tax Protection Act 1966, an exempted company can apply for a tax assurance certificate guaranteeing that no future profits tax, income tax, or capital gains tax will be imposed until at least 2035. That guarantee is statutory, not discretionary, which means your entity's tax position is not subject to annual policy shifts.

Why This Matters for Foreign-Owned Structures

Profits generated by a Bermuda-incorporated business remain fully intact without reduction at the corporate level. For context, the OECD average corporate tax rate sits above 21%, so the structural difference between operating through a Bermuda exempted company and a standard onshore jurisdiction is immediately quantifiable.

Eligibility for the tax assurance is limited to exempted companies and certain other qualifying entities, so confirming the correct structure at incorporation is necessary for the protection to apply.

Your company's retained earnings are not eroded by corporate-level taxation, allowing full reinvestment or distribution without a mandatory tax haircut at source.

No Capital Gains or Withholding Taxes

Bermuda imposes no capital gains tax on the disposal of shares, securities, or other assets held by exempted companies. This applies regardless of where the underlying assets are located or where the gains arise. For investors and shareholders, the practical effect is that returns generated through asset sales or portfolio exits are not reduced at the corporate level by a gains-based charge.

Dividend distributions, interest payments, and royalties paid from an exempted company to non-resident shareholders carry no withholding tax obligation. No deduction is made at source before funds leave the jurisdiction. This structural feature is particularly relevant for holding structures where regular income distributions form part of the business model.

The legal basis for this treatment is the Exempted Undertakings Tax Protection Act 1966, under which the Bermuda government provides eligible companies with a formal assurance against the imposition of taxes on profits, income, or capital gains until 2035.

What this means in practice for your business:

- Gains on exits or asset disposals are not taxed at the entity level before distribution

- No withholding mechanism reduces dividend flows to foreign shareholders

- The 2035 tax assurance provides long-term planning certainty without annual re-application

- There is no minimum holding period required to qualify for these protections under current law

Incorporate a Company in Bermuda

Set up an exempted company in Bermuda and access its zero capital gains and withholding tax framework.

Strong Political and Economic Stability

Bermuda political stability for businesses is not incidental — it is constitutionally structured. As a British Overseas Territory, the island operates under a system of internal self-government established by the Bermuda Constitution Order 1968, while the United Kingdom retains responsibility for defence and foreign affairs. This arrangement has produced over five decades of uninterrupted political continuity, with no sovereign risk, no currency crisis, and no abrupt regulatory overhaul affecting foreign-held entities.

The Bermuda dollar is pegged at parity to the US dollar, a fixed-rate arrangement that has been maintained since 1970. For foreign business owners, this eliminates currency conversion uncertainty when managing USD-denominated transactions, which is particularly relevant in reinsurance and capital markets activity.

| Indicator | Detail |

|---|---|

| Constitutional Framework | Bermuda Constitution Order 1968 |

| Currency Peg | BMD : USD at 1:1 since 1970 |

| Sovereign Oversight | UK responsible for defence and foreign affairs |

| Regulatory Consistency | No history of sudden corporate law reversal |

The Bermuda Monetary Authority, established under the Bermuda Monetary Authority Act 1969, acts as the territory's integrated financial regulator. Its mandate covers banking, insurance, and investment business, giving foreign firms a single, consistent point of regulatory oversight rather than fragmented supervision across multiple agencies. That structural clarity reduces compliance uncertainty for businesses operating across financial service categories.

Exempted Company Status for Foreign Businesses

Under the Companies Act 1981, an exempted company is a distinct corporate structure designed specifically for foreign-owned businesses that operate outside Bermuda. The entity is legally incorporated locally but exempted from the general requirement that at least 60% of its shares be held by Bermudans. This single structural distinction is the foundation of most Bermuda exempted company benefits for foreigners.

Because an exempted company is not permitted to trade within the local Bermuda market, the government treats it as a foreign-facing vehicle. In exchange for this restriction, the entity gains access to statutory protections and tax concessions that domestic companies do not receive in the same form.

The Registrar of Companies, operating under the Ministry of Finance, administers exempted entity registration. Your business does not need a local partner, and 100% foreign shareholding is permitted from the outset.

Keep the following in mind while maintaining exempted status:

- The company must not carry on business with residents of Bermuda except as permitted under the Act

- A licensed resident representative agent is required at all times

- Annual government fees apply and vary by authorised share capital

- Any change in business activity may require a fresh assessment of compliance with exempted status conditions

- Trading locally without authorisation can result in loss of exempted status

An exempted company can obtain a statutory guarantee from the Bermuda government that no future profits or income tax legislation will apply to it for up to 30 years, under section 164 of the Companies Act 1981.

World-Class Reinsurance and Financial Hub

Bermuda's position as a global reinsurance capital is not accidental. The island hosts over 40 of the world's largest reinsurers and insurance groups, a concentration that developed following major catastrophe events in the 1990s and accelerated after Hurricane Andrew in 1992 and again post-9/11. That density of capital creates a self-reinforcing environment where risk modeling expertise, specialist legal counsel, and deep pools of reinsurance capacity exist in close proximity. For businesses seeking Bermuda reinsurance hub advantages, this ecosystem translates directly into access to counterparties, capital structures, and industry knowledge that few jurisdictions can replicate at scale.

Regulatory Architecture Built for Insurance Structures

The Bermuda Monetary Authority (BMA) regulates all insurance and reinsurance entities under the Insurance Act 1978. The BMA's Class system, ranging from Class 1 through Class E for long-term insurers, provides tiered regulatory treatment that allows captives, special purpose insurers, and commercial reinsurers to operate under frameworks calibrated to their risk profile. Solvency II equivalence, granted by the European Commission, means reinsurance contracts placed through Bermuda-based entities receive equivalent treatment in EU member state balance sheets, a material operational advantage for firms with European cedants.

Structured Access to Global Capital Markets

Bermuda's Insurance-Linked Securities (ILS) market is among the largest in the world, with catastrophe bond issuance regularly channeled through Bermuda-domiciled special purpose insurers. Your business can access institutional capital through structures that are legally recognized across major financial markets. The Bermuda Stock Exchange (BSX) provides a regulated listing venue for ILS instruments, enabling secondary market liquidity.

Structure Your Bermuda Insurance or Reinsurance Entity Correctly

Speak with our team about the regulatory classifications, BMA requirements, and corporate structures available for reinsurance and financial service businesses incorporated in Bermuda.

Robust Legal System Based on English Common Law

Bermuda English common law business advantages extend well beyond reputation. The legal system is directly rooted in English common law, meaning courts apply established principles of contract, tort, and equity that are familiar to legal counsel across the UK, Commonwealth countries, and many international financial centres. That familiarity reduces legal uncertainty for foreign investors structuring cross-border transactions or enforcing agreements.

- The Companies Act 1981 governs exempted companies and provides a codified statutory framework built on common law foundations, giving your entity a predictable legal basis from the moment of incorporation.

- Bermuda's Supreme Court and Court of Appeal follow English precedent where local statute does not provide otherwise, so legal outcomes are generally consistent with those in other common law jurisdictions rather than relying on untested domestic rulings.

- Commercial disputes can be resolved through arbitration under the Arbitration Act 1986, and the island has also developed institutional expertise in insurance and reinsurance litigation, meaning specialised disputes are handled by courts with direct sectoral experience.

- Contracts governed by Bermudian law are routinely enforced by courts with no requirement for a local party, which matters when structuring shareholder agreements or intercompany arrangements between foreign entities.

- Judicial independence is constitutionally protected, and the Judicial Committee of the Privy Council in London serves as the final court of appeal, providing an additional layer of oversight outside the jurisdiction itself.

Fast and Straightforward Company Registration Process

Bermuda fast company registration advantages are rooted in statute. Under the Companies Act 1981, an exempted company can be incorporated once the Registrar of Companies receives the memorandum of association, supporting documents, and the prescribed fee. No pre-approval from a government ministry is required for most standard structures.

Processing times are measured in days, not weeks. For foreign founders, this means a legally constituted entity can be operational quickly, reducing the window between the incorporation decision and actual business activity.

The Registrar of Companies maintains a public register and issues a certificate of incorporation upon successful filing. That certificate carries immediate legal effect, allowing your business to open bank accounts, enter contracts, and conduct international transactions without a waiting period tied to bureaucratic sequencing.

Registered local representatives, known as resident representatives, handle the filing on behalf of foreign applicants, so physical presence in the jurisdiction is not required at any stage of formation.

A hypothetical scenario: A fund manager based in Singapore decides to incorporate an exempted company in Bermuda. From the date documents are submitted to a licensed registered agent through to certificate issuance, the process can be completed within five to seven business days, allowing the entity to be in place before the manager's first investor close.

High-Calibre Professional Services Ecosystem

Bermuda's professional services ecosystem benefits foreign business owners in a direct, structural way: the jurisdiction has spent decades building specialist expertise around insurance, reinsurance, fund administration, and cross-border capital structures. That concentration means the legal, accounting, and advisory firms based here work routinely with international clients on complex transactions, not as an exception but as standard practice.

Law firms operating on the island are well-versed in the Companies Act 1981 and the regulatory requirements of the Bermuda Monetary Authority (BMA). Your advisors are not interpreting offshore frameworks from a distance; they operate within them daily.

The depth of local expertise translates into practical advantages:

- Actuarial, legal, and audit firms with direct BMA familiarity reduce compliance friction for regulated entities.

- Corporate service providers understand exempted company structuring under the Companies Act 1981 without requiring extensive external counsel to interpret local rules.

- Fund administrators experienced with the Investment Business Act 2003 can support your entity from formation through ongoing regulatory reporting.

This concentration of specialised professionals shortens transaction timelines and reduces the risk of compliance gaps that arise when advisors lack jurisdiction-specific experience.

The quality and cost of professional services vary significantly between firms; engaging advisors with direct BMA regulatory experience is particularly important for licensed or regulated entities.

Full Foreign Ownership With No Local Partner Required

One of the more structurally significant Bermuda full foreign ownership benefits is that foreign nationals can hold 100% of an exempted company without bringing in a local Bermudian shareholder, director, or partner. This removes a constraint that exists in many jurisdictions, where equity dilution or shared control with a resident party is a legal precondition for doing business.

Under the Companies Act 1981, an exempted company is by definition intended to conduct business outside Bermuda. Because the business of the entity is oriented externally, the Bermuda no local partner requirement advantage is built directly into the legislation rather than granted through a special dispensation or license category.

This matters for capital control and governance. You retain full voting rights, full profit entitlement, and the authority to appoint directors and officers without negotiating those terms with a mandated local party. In jurisdictions that impose local ownership requirements, foreign investors routinely face disputes over distributions, strategic decisions, and exit terms.

The conditions that do apply are worth understanding:

- An exempted company must appoint a local registered agent and maintain a registered office in the jurisdiction.

- At least one officer or a registered representative must maintain a presence, though this does not require equity participation.

- The firm cannot conduct most categories of local business with Bermuda residents without additional licensing.

The Bermuda 100 percent foreign ownership exempted company structure is codified in law, not dependent on executive discretion, which means it is not subject to change through policy shifts or administrative reinterpretation.

Strong Privacy and Asset Protection Framework

Bermuda asset protection benefits for businesses rest on a legal structure that distinguishes between information required by regulators and information made available to the public. The Register of Companies, maintained under the Companies Act 1981, does not make beneficial ownership details publicly accessible. For a foreign investor, this means your identity as an owner is not exposed to competitors, litigants, or unsolicited third parties through open public records.

Exempted companies are not required to file annual financial statements with any public registry. Audited accounts may be required internally or by specific regulatory licences, but general financial disclosure to the public is not mandated under the standard exempted company regime. The practical effect is that your company's revenue, assets, and operational data remain outside the public domain.

Asset protection under Bermudian law is reinforced by the jurisdiction's creditor protection provisions and the formal separation between a company and its shareholders. Trusts formed under the Trustee Act 1975 offer an additional structural layer, allowing assets to be held in a manner that creates legal distance from personal liability exposure.

Key privacy and protection features under the current framework include:

- Beneficial ownership information is reported to the Bermuda Monetary Authority but is not publicly searchable

- No public filing of financial statements for standard exempted companies

- Trusts governed by the Trustee Act 1975 provide a separate legal vehicle for holding assets

- The Companies Act 1981 restricts the circumstances under which company records must be disclosed externally

Why Bermuda Stands Out Among Offshore Jurisdictions

The jurisdictions most relevant to compare against are the Cayman Islands, British Virgin Islands (BVI), and Delaware (US). These three are consistently evaluated alongside Bermuda by international investors and financial services businesses seeking offshore or low-tax structures. Cayman and BVI compete directly on tax neutrality and exempted company frameworks, while Delaware attracts incorporation activity through legal predictability and cost, making it a realistic alternative for businesses weighing onshore versus offshore structures.

What the comparison reveals is that Bermuda's tax exemption guarantee under the Exempted Undertakings Tax Protection Act, combined with its established position as the global reinsurance capital and its English common law judiciary, creates a profile that differs meaningfully from jurisdictions offering similar tax outcomes. The distinction lies in regulatory depth and sector-specific infrastructure rather than tax rates alone.

| Parameter | Bermuda | Cayman Islands | British Virgin Islands | Delaware (USA) |

|---|---|---|---|---|

| Corporate Income Tax | 0% (statutory exemption until 2035) | 0% | 0% | 8.7% state corporate tax |

| Capital Gains Tax | None | None | None | None at state level |

| Foreign Ownership | 100% permitted | 100% permitted | 100% permitted | 100% permitted |

| Legal System | English common law | English common law | English common law | US common law |

| Reinsurance / Insurance Hub | Yes, globally dominant | Developing | Limited | Limited |

| Privacy of Beneficial Owners | Regulated under AML framework | Regulated under AML framework | Central register (restricted access) | Disclosure requirements increasing |

| Statutory Tax Guarantee Period | Until 31 March 2035 | No equivalent guarantee | No equivalent guarantee | Not applicable |

| OECD BEPS Compliance | Yes | Yes | Yes | Yes |

Compliance Services for Companies in Bermuda

Maintain good standing in Bermuda with ongoing compliance support, including economic substance filings, annual government fees, and regulatory reporting.

Conclusion

Bermuda's case as an incorporation destination rests on a combination of structural features that are difficult to find together in a single jurisdiction. The permanent tax assurance provided under the Exempted Undertakings Tax Protection Act, the absence of exchange controls on exempted companies, and the depth of the professional services sector create conditions that directly reduce cost, complexity, and operational friction for foreign-owned businesses.

Not every structure benefits equally. A firm with passive holding activities will find different advantages than one operating within the reinsurance or fund administration sector, where proximity to a concentrated cluster of specialist counterparties carries real commercial weight.

The question for your business is whether these structural features align with your specific ownership model, industry, and long-term goals. Where they do, the foundation is legally sound, administratively accessible, and supported by a court system with a well-documented track record on commercial matters. Determining how that foundation applies to your particular situation is the natural next step.

Start Your Bermuda Company With Expanship Today

When you start a Bermuda company with Expanship, you work with a team that understands the specific obligations and structural requirements that govern exempted companies under the Companies Act 1981. From initial name reservation through the Registrar of Companies to maintaining statutory records in good standing, each stage of the process is managed with direct reference to local regulatory requirements.

Expanship's services cover the full scope of what a foreign business owner requires to establish and maintain a compliant entity:

- Preparation and legalization of incorporation documents

- Registered agent and registered office provision in Bermuda

- Filing coordination and liaison with the Registrar of Companies

- Post-incorporation compliance management, including annual government fees and statutory filings

- Banking introduction assistance with local and international financial institutions

Expanship does not provide legal advice, but works alongside qualified local counsel where the transaction structure or regulatory requirements call for it. This distinction matters for foreign founders who need accurate guidance on the Bermuda Monetary Authority's requirements for licensed activities, or on economic substance obligations that may apply depending on the nature of the business.

Reach out to Expanship Bermuda to discuss your incorporation requirements.

Frequently Asked Questions (FAQ)

Bermuda does not impose corporate income tax on company profits. The government has historically operated without a corporate tax regime, and exempted companies may additionally apply for a tax assurance certificate under the Exempted Undertakings Tax Protection Act 1966, which can guarantee exemption from any future profits or income tax until 2035. This certificate does not protect against the global minimum tax rules introduced under the OECD Pillar Two framework, which may apply to large multinational groups meeting the revenue threshold.

Incorporation can be completed within one to three business days once the Registrar of Companies receives a complete application, including the memorandum of association and requisite supporting documents. Expedited processing is available for an additional government fee. The timeline assumes all due diligence documentation for beneficial owners meets the requirements set by the Bermuda Monetary Authority.

Exempted companies are not required to file financial statements on a public register, which preserves a degree of financial confidentiality. However, they must maintain proper accounting records and, depending on size and structure, may be subject to audit requirements under the Companies Act 1981. Certain regulated entities, particularly those licensed by the Bermuda Monetary Authority, face additional disclosure obligations specific to their licensing class.

Bermuda is a member of the OECD's Global Forum on Transparency and Exchange of Information and participates in the Common Reporting Standard for automatic exchange of financial account information. The jurisdiction has also enacted the Proceeds of Crime Act 1997 and related regulations to align its anti-money laundering framework with Financial Action Task Force recommendations. These commitments mean the jurisdiction is not listed on major international blacklists, though businesses should confirm current status with relevant EU and FATF listings at the time of structuring.

A registered office in Bermuda is mandatory and must be maintained through a licensed service provider, as exempted companies cannot self-register a registered address without the appropriate licence. At least one director is required, and while there is no statutory requirement that the director be a Bermudian resident, many corporate governance arrangements and some regulated structures do benefit from local directorship to satisfy substance considerations. Bermuda has enacted economic substance legislation that may impose additional requirements depending on the business activity conducted.

Bermudian law is grounded in English common law, and the courts regularly apply precedents from English and other Commonwealth jurisdictions where local case law is absent. The Supreme Court of Bermuda handles commercial disputes, and the jurisdiction has an established track record in complex insurance and financial litigation. Parties to contracts governed by Bermudian law can generally expect a predictable legal framework, and international arbitration clauses are also recognised and enforceable.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.