Key Takeaways

- Bermuda's zero-tax posture — no corporate income tax, capital gains tax, or withholding tax on dividends — is the primary driver behind the jurisdiction's tiered entity structure, which ranges from Exempted Companies to Segregated Accounts Companies.

- The Exempted Company is the most widely registered vehicle in Bermuda, designed specifically for non-resident investors conducting international business under the Companies Act 1981.

- Segregated Accounts Companies provide statutory cell separation, making them the preferred structure for insurers and fund managers requiring legal isolation between pools of assets and liabilities.

- Regulatory oversight by the Bermuda Monetary Authority has intensified across financial services sectors, with increasing requirements around substance, transparency, and beneficial ownership disclosure.

Introduction to Entity Types in Bermuda

Bermuda is a British Overseas Territory situated in the North Atlantic Ocean, approximately 1,070 kilometres east of North Carolina. It operates as a self-governing territory with its own legal and regulatory framework, distinct from UK domestic law.

Company registration falls under the jurisdiction of the Registrar of Companies, which operates within Bermuda's Ministry of Finance. The Companies Act 1981 remains the primary statute governing corporate formation and ongoing compliance obligations for most business structures.

The territory imposes no corporate income tax, no capital gains tax, and no withholding tax on dividends — a posture that has shaped the types of structures available to both resident and non-resident businesses.

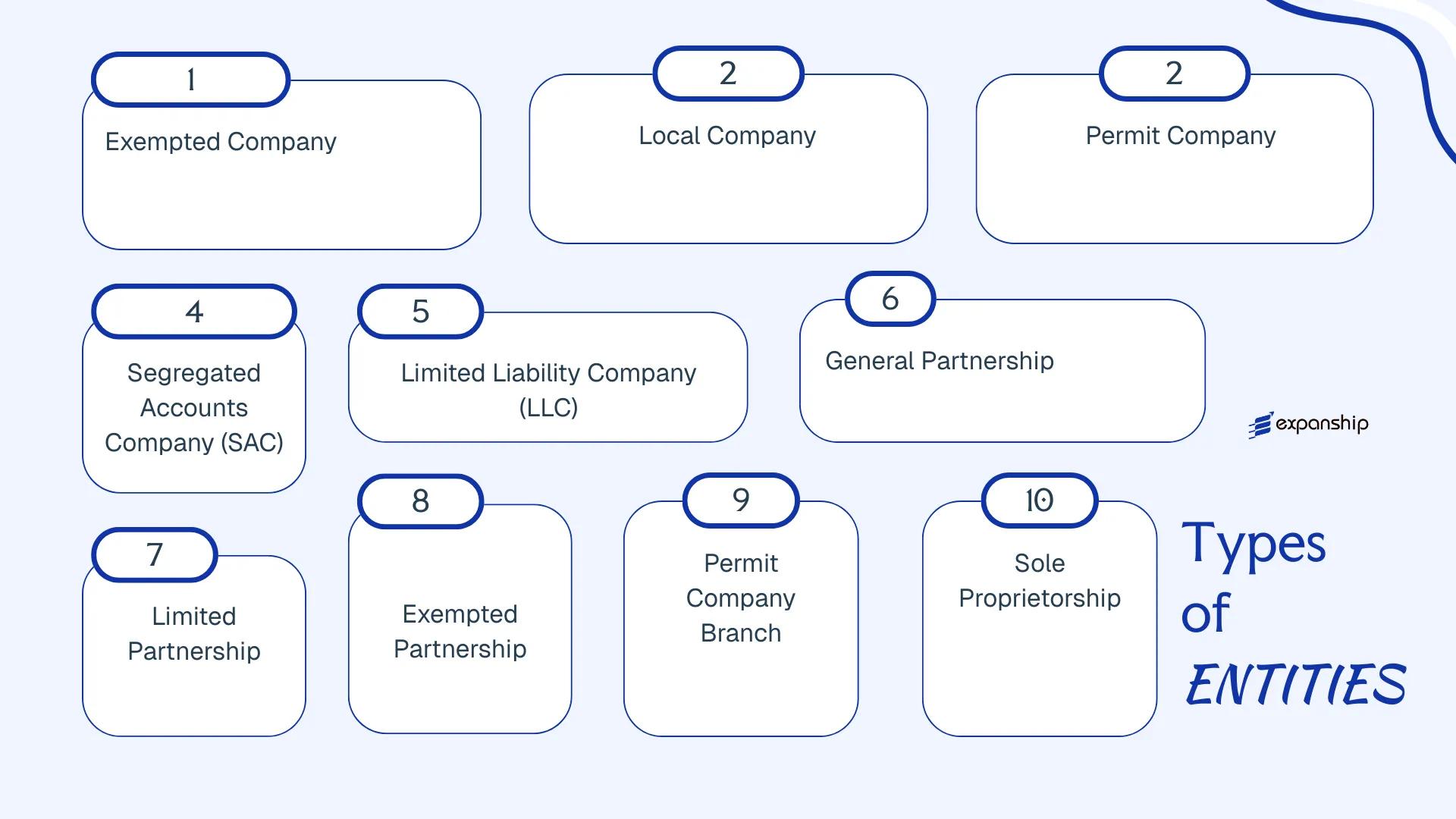

The main types of business entities in Bermuda include the Exempted Company, Local Company, Permit Company, Segregated Accounts Company, Limited Liability Company, General Partnership, Limited Partnership, Exempted Partnership, Overseas Partnership, and Sole Proprietorship. Each structure carries distinct eligibility criteria, ownership restrictions, and regulatory requirements.

This article examines each entity type in detail, covering formation requirements, permitted activities, and the practical considerations relevant to your business.

An Overview of Business Structures in Bermuda

Bermuda's company law framework offers several distinct business structures, each governed primarily by the Companies Act 1981 and supported by subsidiary legislation including the Limited Liability Company Act 2016 and the Partnership Act 1902. The Registrar of Companies, operating under the Bermuda Monetary Authority (BMA) for regulated entities, oversees formation and ongoing compliance across these structures. Each entity type carries different implications for ownership, liability, taxation, and permitted activities.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Exempted Company | Corporate | Limited | Exempt | Not permitted | 1 shareholder | Registrar of Companies | Companies Act 1981 |

| Local Company | Corporate | Limited | Taxed locally | Permitted | 1 shareholder | Registrar of Companies | Companies Act 1981 |

| Permit Company | Corporate (foreign) | Limited | Depends on origin | Permitted (with permit) | N/A (existing foreign entity) | Registrar of Companies | Companies Act 1981 |

| Segregated Accounts Company | Corporate | Segregated per cell | Exempt | Not permitted | 1 shareholder | BMA (if regulated) | Segregated Accounts Companies Act 2000 |

| Limited Liability Company | Hybrid | Limited | Exempt | Not permitted | 1 member | Registrar of Companies | LLC Act 2016 |

| General Partnership | Unincorporated | Unlimited | Pass-through | Permitted | 2 partners | Registrar of Companies | Partnership Act 1902 |

| Limited Partnership | Unincorporated | Mixed | Pass-through | Restricted | 1 GP + 1 LP | Registrar of Companies | Limited Partnership Act 1883 |

| Exempted Partnership | Unincorporated | Mixed | Exempt | Not permitted | 1 GP + 1 LP | Registrar of Companies | Exempted Partnerships Act 1992 |

| Overseas Company | Branch (foreign) | Unlimited (parent) | Depends on parent | Permitted (with registration) | N/A | Registrar of Companies | Companies Act 1981 |

| Sole Proprietorship | Unincorporated | Unlimited | Personal income | Permitted | 1 individual | Registrar of Companies | Business Names Act 1984 |

Each of these structures is examined in full in the sections below.

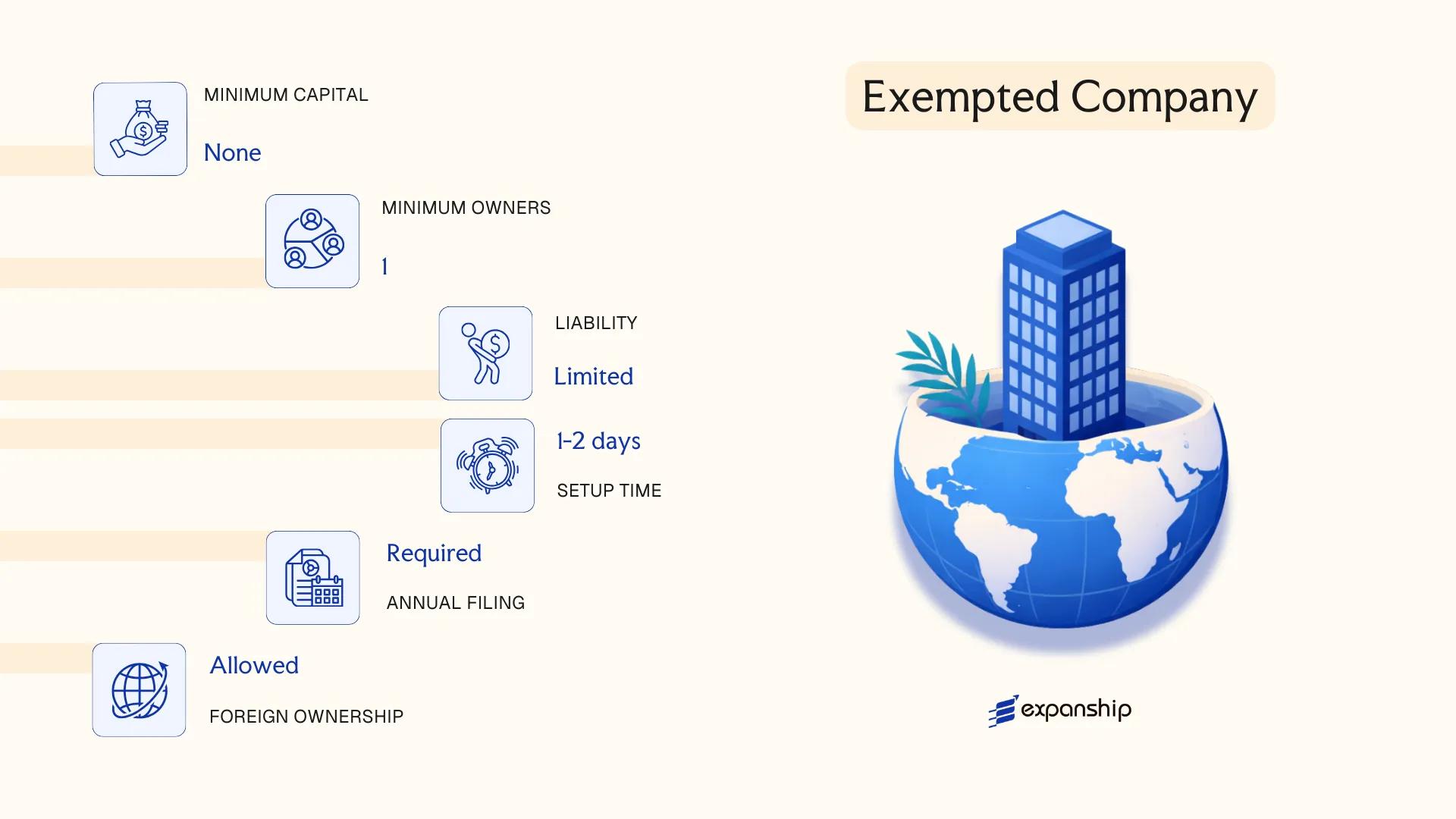

Exempted Company

Bermuda exempted company formation is governed by the Companies Act 1981, which establishes the exempted company as a separate legal entity distinct from its shareholders. The defining characteristic of this structure is that it is "exempted" from the requirement that a majority of its shares be held by Bermudian residents — making it the standard vehicle for foreign-owned business operations conducted primarily outside the island.

Shareholders benefit from limited liability, meaning personal assets are protected from company debts. Incorporation is administered through the Registrar of Companies, and all applications require the involvement of a licensed local service provider.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Limited liability company (corporate) | Separate legal personality from shareholders |

| Members & Directors | Min. 1 shareholder; min. 1 director (individual or corporate) | No maximum; corporate directors permitted |

| Local Presence | Registered office in Bermuda; licensed resident representative required | Physical address, not a PO box |

| Share Capital | No statutory minimum; typically denominated in USD | Par value or no-par-value shares permitted |

| Privacy | Shareholder register not publicly accessible | Director details filed with Registrar but limited public disclosure |

| Restrictions | Cannot carry on business with Bermuda residents without a licence | Restricted to business conducted outside Bermuda |

Focus Points

- Taxation: Exempt from corporate income tax, withholding tax, capital gains tax, and stamp duty on share transfers; the government issues tax assurance certificates valid until 2035.

- Economic Substance: Companies in relevant sectors (banking, insurance, fund management, IP holding, etc.) must satisfy economic substance requirements under the Economic Substance Act 2018.

- Annual Compliance: Annual government fee payable; annual return and financial statements required; audited accounts may be required depending on size.

- Treaty Access: Bermuda has no broad tax treaty network; exempted companies do not access treaty benefits in the conventional sense.

- Conversion: An exempted company may convert to a local company or re-register as a foreign entity in another jurisdiction, subject to Registrar approval.

Sub-Types

Exempted Company Limited by Guarantee

Shareholders have no share capital obligation; liability is limited to a predetermined guarantee amount. Typically used for non-profit associations, foundations, or industry bodies operating across borders.

Exempted Company with Limited Duration

The company's existence is fixed for a defined period not exceeding 50 years, as specified in its memorandum of association. Used in project finance, joint ventures, or fund structures requiring a defined wind-down date.

Exempted Unlimited Liability Company

Shareholders bear unlimited liability for the company's obligations. Occasionally used where a parent entity requires unlimited liability treatment for consolidated accounting purposes in its home jurisdiction.

Common Uses and Considerations

Exempted companies are widely used as holding vehicles, IP-owning entities, captive insurers, and investment fund structures. The absence of corporate income tax is a material structural advantage, though the economic substance requirements impose genuine operational obligations on entities in designated sectors.

Businesses owned and operated by non-Bermudian interests seeking a tax-neutral corporate vehicle for international holding, investment, or IP structures.

Company Incorporation in Bermuda

Register an exempted company in Bermuda with end-to-end support from licensed local representatives.

Local Company

Bermuda local company registration falls under the Companies Act 1981, the same legislation that governs exempted companies, though the operational and ownership constraints differ substantially. A local company is incorporated as a separate legal entity, carrying limited liability for its shareholders, and is designed primarily to conduct business within the island's domestic economy.

Unlike exempted companies, which are restricted from local trading, local entities are permitted to engage in commerce directly with Bermuda residents and businesses. Ownership, however, is subject to the Bermuda Immigration and Protection Act 1956, which generally requires that at least 60% of the equity be held by Bermudians or entities that qualify under local ownership definitions.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Limited liability company with separate legal personality | Incorporated under the Companies Act 1981 |

| Governed By | Bermuda Registrar of Companies | Filing and compliance oversight |

| Shareholders | Minimum 1; no statutory maximum | At least 60% Bermudian ownership required under the Immigration and Protection Act 1956 |

| Directors | Minimum 1; majority must be Bermudian resident | Local director requirement strictly enforced |

| Registered Office | Required in Bermuda | Must maintain a physical registered address on the island |

| Share Capital | No mandatory minimum; typically denominated in USD | Par value or no-par-value shares permitted |

| Privacy | Shareholder register is not fully public | Director information filed with the Registrar |

Focus Points

- Taxation: Local companies are subject to no corporate income tax, capital gains tax, or withholding tax; stamp duty may apply to certain instruments and property transactions.

- Economic Substance: Local companies engaged in relevant activities must satisfy Bermuda's Economic Substance Act 2018 requirements, including adequate local expenditure and management.

- Annual Compliance: Annual government fees are payable to the Registrar of Companies; financial statements and annual returns must be maintained and filed as required.

- Restrictions: Foreign ownership is capped at 40%, limiting the entity's suitability for fully foreign-owned operations; a licence may be required for certain regulated industries.

- Conversion: A local company may apply to re-register as an exempted company, subject to approval by the Minister responsible under the Companies Act 1981.

Closing

A local company suits businesses targeting the domestic Bermudian market, particularly in retail, professional services, or construction, where direct engagement with residents is commercially necessary. The requirement for majority Bermudian ownership is the defining constraint for any foreign investor considering this structure.

Local companies are best suited for Bermudian entrepreneurs or joint ventures where a qualifying local partner holds the majority stake and the business operates primarily within the island's domestic market.

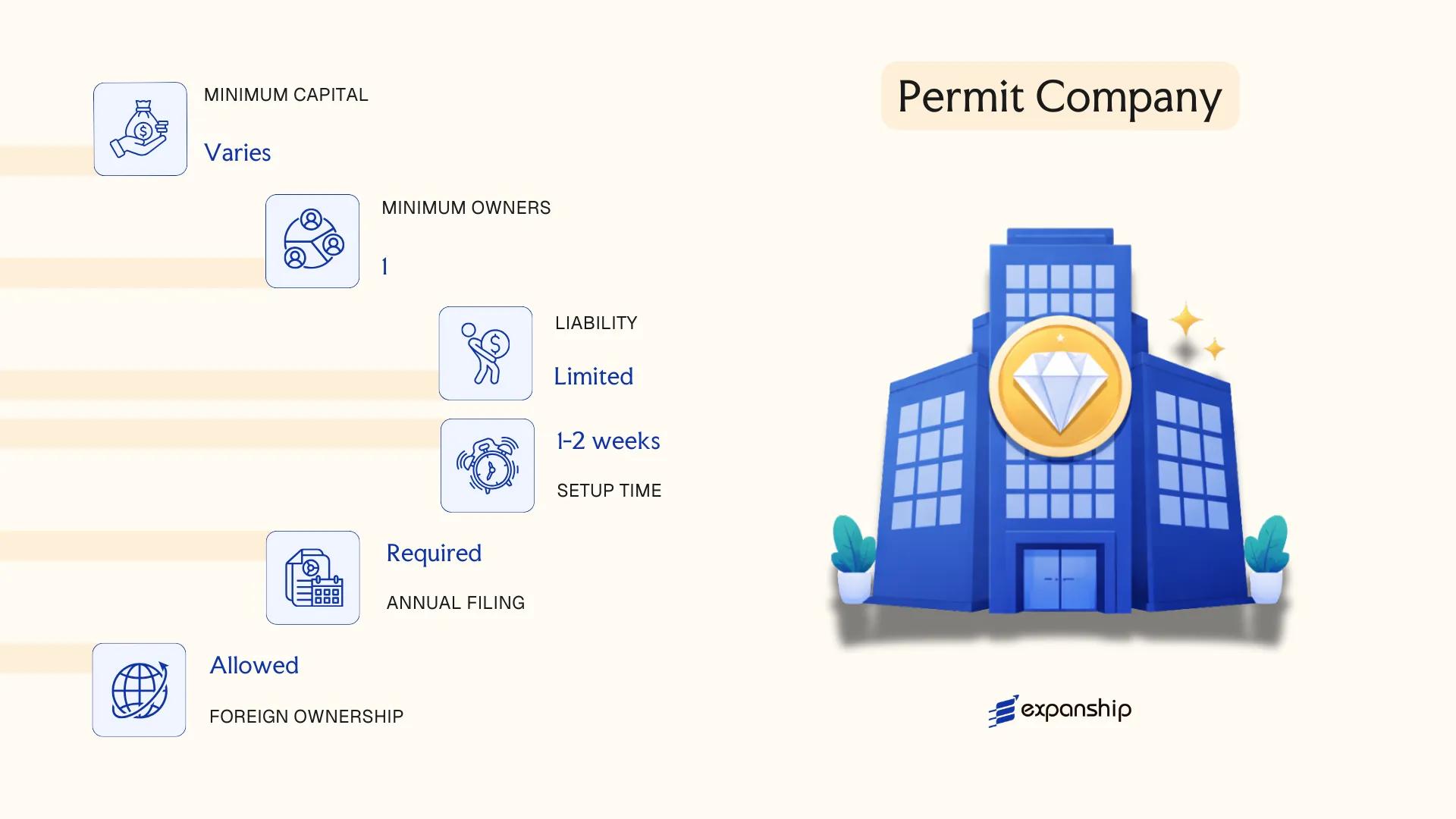

Permit Company

A Bermuda permit company structure applies to a foreign-incorporated company that wishes to carry on business within Bermuda without reincorporating locally. Governed by the Companies Act 1981, specifically Part IX, this vehicle allows an overseas company to obtain a permit from the Minister of Finance, granting it the legal authority to operate in the jurisdiction while retaining its original corporate identity and domicile.

The entity does not acquire a new legal personality through the permit process; it continues to exist as a company incorporated elsewhere. Liability remains governed by the law of its home jurisdiction, and Bermuda exercises regulatory oversight over local operations only.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Foreign company operating under a local permit | Retains legal personality of home jurisdiction |

| Governing Authority | Minister of Finance under Companies Act 1981, Part IX | Application submitted through the Bermuda Monetary Authority in practice |

| Local Presence | Registered office in Bermuda; local representative required | Representative must be a resident individual or authorised firm |

| Members / Directors | Determined by home jurisdiction law | Bermuda imposes no separate member or director minimums |

| Capital | No separate capital requirement imposed by Bermuda | Home jurisdiction capital rules apply |

| Privacy | Permit holder details are on public record with the Registrar of Companies | Financial accounts not publicly disclosed |

Focus Points

- Taxation: No corporate income tax, withholding tax, or VAT applies; a fixed annual government fee is payable in lieu of tax.

- Economic Substance: Depending on the activities conducted locally, substance requirements under the Economic Substance Act 2018 may apply.

- Annual Compliance: Annual renewal of the permit is required, along with filing of the annual return and payment of the government fee.

- Restrictions: Permitted activities are limited to those specified in the permit; any expansion of scope requires a separate application to the Minister.

- Conversion: A permit company cannot convert directly into a Bermuda exempted or local company without first dissolving or reincorporating under Bermuda law.

A permit company is used primarily by foreign firms that need a temporary or project-specific operational presence without committing to full reincorporation. The principal advantage is continuity of the original corporate structure; the key limitation is that permitted activities are strictly bounded by the terms of the permit, leaving little operational flexibility without further regulatory approval.

Foreign companies seeking a defined, short-term operational footprint in Bermuda without restructuring their existing corporate entity.

Segregated Accounts Company (SAC)

A Bermuda segregated accounts company SAC is governed by the Segregated Accounts Companies Act 2000, making Bermuda one of the earlier jurisdictions to legislate this structure formally. Each segregated account within the entity holds assets and liabilities that are legally ring-fenced from those of other accounts and from the general account of the company itself.

The SAC retains a single legal personality — it is one company, not multiple entities. Despite this, the statutory segregation means that creditors of one account cannot access the assets of another, a protection enforced by law rather than by contract alone.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Segregated Accounts Company (statutory) | Single legal entity with account-level asset segregation under the SAC Act 2000 |

| Governing Body | Board of Directors | Minimum one director; corporate directors permitted |

| Members | Shareholders | No statutory minimum share capital prescribed for most SACs |

| Local Presence | Registered Office in Bermuda; licensed Registered Agent required | Bermuda Monetary Authority (BMA) oversight applies |

| Capital | Bermuda Dollar or any foreign currency | Capital requirements vary by account purpose; insurance-linked SACs face BMA solvency requirements |

| Privacy | Shareholder register not publicly accessible | Beneficial ownership held with authorities under AML frameworks |

Focus Points

- Taxation: No corporate income tax, withholding tax, capital gains tax, or VAT applies; stamp duty may arise on certain instruments.

- Regulatory oversight: Insurance-linked SACs require BMA licensing; the BMA supervises account-level solvency and conduct.

- Economic substance: Holding or finance SACs may be subject to substance obligations under the Economic Substance Act 2018.

- Annual compliance: Annual general meetings, financial statements, and BMA filings apply depending on the SAC's licensed category.

- Restrictions: SAC accounts cannot be used to obscure cross-account liabilities; statutory rules govern when account assets may be used to meet general company obligations.

Closing

SACs are used predominantly as insurance captives, investment fund vehicles, and structured finance platforms where strict liability separation between portfolios or business lines is operationally necessary. The statutory ring-fencing provides stronger creditor protection than contractual segregation alone, though administering multiple accounts within one entity adds regulatory and operational complexity.

The SAC structure suits insurance managers, fund administrators, and financial institutions that require legally enforceable separation of multiple risk pools or asset classes within a single corporate entity.

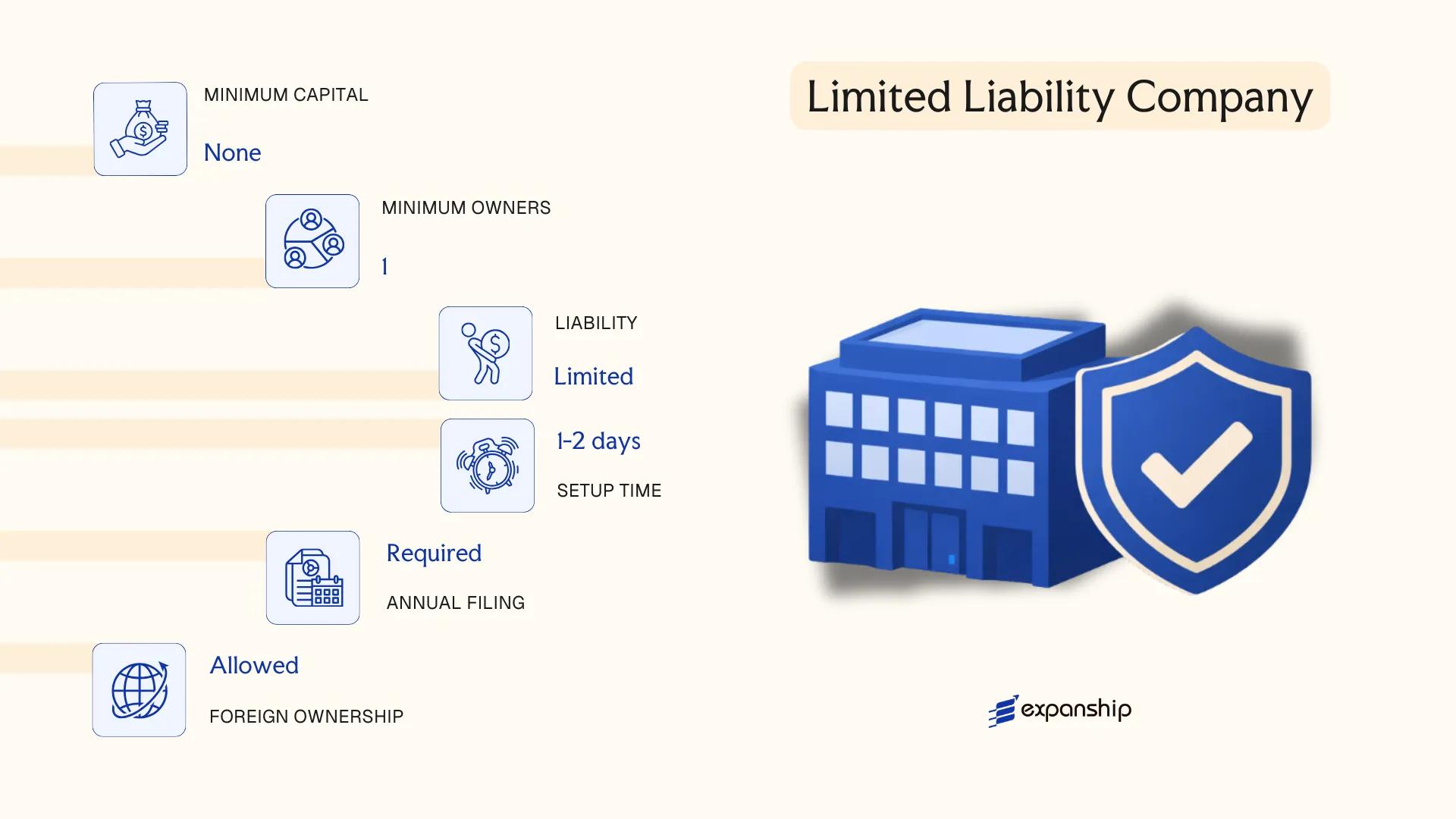

Limited Liability Company (LLC)

Introduced under the Limited Liability Company Act 2016, the Bermuda limited liability company LLC is a relatively recent addition to the jurisdiction's corporate toolkit. Structurally, it is a hybrid entity that combines the limited liability protection of a company with the contractual flexibility associated with a partnership.

Unlike a traditional exempted company, the LLC does not issue shares. Ownership is expressed through membership interests, and governance is primarily governed by an LLC agreement, which allows significant flexibility in allocating economic rights and management responsibilities among members.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Separate legal entity | Governed by the Limited Liability Company Act 2016 |

| Members | Referred to as Members; minimum 1, no maximum | Members may manage directly or appoint a Manager |

| Management | Manager-managed or member-managed | Defined by the LLC agreement |

| Local Presence | Registered office in Bermuda; registered agent required | Must be maintained at all times |

| Capital | No minimum capital requirement; contributions in agreed form | Capital structure defined in the LLC agreement |

| Privacy | Member details not publicly filed | LLC agreement is a private document |

Focus Points

- Taxation: No corporate income tax, withholding tax, capital gains tax, or VAT; a 0% tax assurance certificate may be obtained under the Exempted Undertakings Tax Protection Act 1966.

- Economic Substance: Subject to economic substance obligations under the Economic Substance Act 2018 if engaged in a relevant activity.

- Annual Compliance: Annual government fees apply; the LLC must maintain a registered office and file annual returns confirming continued compliance.

- Treaty Access: Bermuda has no broad tax treaty network; LLCs do not benefit from double tax agreements.

- Conversion: The Act permits conversion of an existing company or partnership into an LLC, subject to statutory requirements.

Closing

The LLC structure suits investment funds, joint ventures, and holding arrangements where flexible profit allocation and bespoke governance are priorities. The LLC agreement provides contractual freedom that a standard company constitution does not, though the relative novelty of the form means there is less judicial precedent interpreting it compared to the exempted company.

Sophisticated investors and fund managers seeking a flexible, contractually-driven structure with limited liability, particularly for private equity, venture, or co-investment vehicles.

Partnerships [General Partnership, Limited Partnership, Exempted Partnership, Overseas Partnership]

Bermuda exempted partnership registration is governed primarily by the Exempted Partnerships Act 1992, while other partnership forms fall under the Partnership Act 1902 and the Limited Partnership Act 1883. These statutes create distinct legal frameworks depending on the structure chosen, with key differences in liability exposure, partner composition, and permitted business activity.

Partnerships in Bermuda do not generally possess separate legal personality as a matter of common law, meaning the partnership itself is not distinct from its partners for liability purposes. The exempted partnership is the most commonly used structure for international business and fund vehicles, as it permits non-resident partners and is expressly prohibited from carrying on business within the jurisdiction.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Contractual arrangement; generally no separate legal personality | Exempted partnerships may elect legal personality under the 1992 Act |

| Members | General Partner(s) and/or Limited Partner(s); no statutory maximum | At least one general partner required; limited partners have restricted management rights |

| Local Presence | Registered office in Bermuda; registered representative required | Exempted partnerships must maintain a registered office with a licensed firm |

| Capital | No minimum capital requirement; no prescribed currency | Capital contributions are governed by the partnership agreement |

| Privacy | Partnership agreements are not publicly filed | Register of partners is maintained but not open to public inspection |

Focus Points

- Taxation: Partnerships are fiscally transparent; no corporate income tax, withholding tax, VAT, or capital gains tax applies at the entity level, with income attributed directly to partners.

- Economic Substance: General partnerships conducting relevant activities may be subject to economic substance obligations under the Economic Substance Act 2018.

- Annual Compliance: Exempted partnerships must file an annual declaration confirming that partners remain predominantly non-Bermudian; a government annual fee applies.

- Conversion: An exempted partnership may apply to be registered as an exempted limited partnership or convert to an exempted company under prescribed statutory procedures.

- Treaty Access: Bermuda has no broad tax treaty network, so partners should assess treaty benefits at their own jurisdictional level.

Sub-Types

General Partnership

Formed under the Partnership Act 1902, all partners bear unlimited joint and several liability. This structure is rarely used for commercial purposes given the absence of liability protection.

Limited Partnership

Governed by the Limited Partnership Act 1883, this structure introduces one or more limited partners whose liability is capped at their agreed capital contribution, provided they do not participate in management.

Exempted Partnership

Established under the Exempted Partnerships Act 1992, this form is restricted to partners who are predominantly non-Bermudian and cannot conduct business locally. It is the standard vehicle for international private equity funds and investment structures.

Overseas Partnership

An overseas partnership is a foreign partnership registered to conduct business in Bermuda under a permit. It retains its original legal character from the jurisdiction of formation and does not reincorporate locally.

Closing Paragraph

Partnership structures are most commonly used for private equity funds, hedge fund vehicles, joint ventures, and asset-holding arrangements where pass-through taxation is a structural priority. The exempted partnership offers significant flexibility in agreement-based governance, though the absence of separate legal personality in the default form can complicate contracting and enforcement in certain cross-border contexts.

Exempted partnerships are best suited for fund managers, institutional investors, and joint venture parties seeking a tax-transparent, agreement-driven structure for cross-border investment or asset-holding purposes.

Overseas and Foreign Vehicles [Permit Company Branch, Overseas Company Registration]

Overseas company registration in Bermuda is governed by the Companies Act 1981, which sets out the requirements for foreign entities seeking to operate or establish a presence on the island. A foreign corporation does not form a new legal entity by registering locally — it remains subject to the laws of its home jurisdiction and retains its original legal personality.

Registration under the Act does not confer Bermudian residency status on the foreign entity, nor does it create a separate subsidiary structure. The registered presence functions as an extension of the parent company, with liability flowing back to that parent.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Branch of a foreign company | No separate legal personality; parent company remains liable |

| Governing Legislation | Companies Act 1981 | Part XII covers overseas companies |

| Local Representatives | Minimum one resident representative required | Must be ordinarily resident in Bermuda |

| Registered Office | Physical registered office required | Must be maintained at all times |

| Capital | No separate capital requirement | Parent company's capital structure applies |

| Privacy | Parent company details filed with the Registrar of Companies | Public record in home jurisdiction may apply |

Focus Points

- Taxation: Bermuda imposes no corporate income tax, withholding tax, capital gains tax, or VAT on branch operations; the parent entity's home jurisdiction tax position governs.

- Economic Substance: Branches conducting relevant activities must satisfy the Economic Substance Act 2018 requirements, including demonstrating adequate local activity.

- Annual Compliance: Annual filing and payment of government fees to the Registrar of Companies are required to maintain active status.

- Treaty Access: Bermuda has no broad tax treaty network; treaty benefits, if any, depend entirely on the parent company's jurisdiction of incorporation.

- Restrictions: A branch cannot conduct local business without a permit; activity is generally restricted to the scope authorised under the original registration.

Sub-Types

Permit Company Branch

A foreign company granted a permit under the Companies Act 1981 may carry on business in Bermuda within the scope defined by that permit. The Bermuda permit company branch setup process requires application to the Minister of Finance, and the permit specifies the permitted activities, distinguishing it from an unrestricted overseas registration.

Overseas Company Registration

A foreign company registering as an overseas vehicle without a permit is typically recognised for administrative or holding purposes rather than active local trading. Registering an overseas vehicle in Bermuda in this form is used where the entity needs a local presence for regulatory or operational reasons but does not require a permit to conduct its core business activities on the island.

When to Use This Structure

A foreign company branch is suited to multinationals that need an operational footprint without establishing a separate subsidiary, though the absence of limited liability ring-fencing at the branch level is a material structural drawback.

Foreign corporations requiring a local operational or administrative presence in Bermuda without incorporating a separate entity.

Sole Proprietorship

A sole proprietorship in Bermuda is the simplest form of business operation available to individuals. Unlike incorporated entities, it carries no separate legal personality — you and the business are legally the same person, meaning personal assets are fully exposed to business liabilities. Registration is governed under the Registration of Business Names Act 1974, which requires any individual trading under a name other than their own to register that name with the Registrar of Companies.

Registration does not create a distinct legal entity. You remain personally liable for all debts and obligations incurred in the course of trading.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated business | No separate legal personality from the owner |

| Proprietor | Single individual | One owner only; no partners or shareholders |

| Local Presence | Registered business name (if trading under a trade name) | Filed with the Registrar of Companies under the 1974 Act |

| Liability | Unlimited personal liability | Personal assets are at risk for business debts |

| Capital | No minimum requirement | No statutory capital threshold |

| Privacy | Business name is publicly registered | Owner's identity linked to the registered name |

Focus Points

- Taxation: No corporate income tax, capital gains tax, withholding tax, or VAT applies; income is treated as personal earnings, though work permit and payroll tax obligations may apply depending on employment arrangements.

- Work Permit Requirement: Non-Bermudian individuals must hold a valid work permit issued by the Department of Immigration before operating a sole proprietorship.

- Annual Compliance: Annual renewal of the registered business name may be required; no audited accounts are mandated.

- Economic Substance: Sole proprietorships are not subject to the Economic Substance Act 2018, which applies to registered entities.

- Conversion: There is no formal statutory conversion mechanism; transitioning to a company requires incorporating a new entity separately.

Closing Paragraph

A sole proprietorship suits individuals providing services or running small local operations where administrative simplicity outweighs the need for liability protection. The absence of incorporation formalities reduces setup costs, but unlimited personal liability is a significant structural constraint for any business carrying financial or legal risk.

Local individual traders or self-employed professionals operating low-risk service businesses who require minimal administrative overhead.

How to Choose the Right Entity Type in Bermuda

Selecting the wrong structure carries concrete legal and financial consequences — knowing how to choose a business entity in Bermuda before incorporating can prevent costly corrections later.

Why Your Entity Choice Matters

- Registering an exempted company while intending to trade locally means operating in breach of the Companies Act 1981, which can result in penalties or striking off.

- Choosing a tax-exempt structure when your business requires access to double taxation treaties means relief on withholding taxes in counterpart jurisdictions will not be available to you.

- Selecting an entity without the capacity to demonstrate local substance when substance requirements apply can trigger reporting failures and regulatory fines under the Economic Substance Act 2018.

- Forming a standard company when a trust or partnership would better serve asset protection or succession objectives locks your business into annual shareholder obligations that would not otherwise apply.

Key Factors to Consider

- Business Activity: Passive asset-holding, active trading, and regulated activities such as insurance or fund management each point toward a distinct structure under Bermuda law.

- Local vs. Offshore Operations: Entities intending to deal with Bermuda residents require a local company or permit, while those operating exclusively outside the jurisdiction may qualify as exempted.

- Ownership and Management: Multi-party ownership with flexible governance favours an LLC or partnership, whereas a company structure suits those needing a formal board.

- Substance Capacity: If maintaining local employees and decision-making in Bermuda is not feasible, the entity type chosen must align with applicable substance thresholds under the Economic Substance Act 2018.

- Exit Strategy: Not all structures permit redomiciliation or conversion — confirm continuance provisions under the Companies Act 1981 before committing to a form.

- Privacy Requirements: Director and shareholder disclosure obligations vary by entity type; nominee arrangements may be necessary where confidentiality is a priority.

Corporate Compliance Services in Bermuda

Maintain good standing and meet ongoing regulatory obligations for your Bermuda entity.

Conclusion

Bermuda company incorporation summary reflects a deliberately tiered system, where each structure serves a distinct commercial purpose under the Companies Act 1981 and its associated legislation. The Exempted Company remains the most registered vehicle, favored by non-resident investors for its tax-neutral profile and unrestricted international business activity. Segregated Accounts Companies suit insurers and fund managers requiring statutory cell separation. The LLC offers contractual flexibility for joint ventures, while the Limited Partnership remains the standard choice for private equity structures. Local Companies and Permit Companies serve businesses with a direct operational presence on the island.

Regulatory oversight through the Bermuda Monetary Authority continues to tighten across financial services sectors, aligning the jurisdiction with international standards on substance, transparency, and beneficial ownership. For your business, the right structure depends on the commercial function the entity needs to perform. Expanship's team works through each of these formation pathways directly.

How Expanship Can Assist You

As a corporate services provider Bermuda businesses and international investors rely on, Expanship works directly with the structures discussed throughout this guide — from Exempted Companies and Segregated Accounts Companies to Exempted Partnerships and LLCs. Every formation and maintenance obligation runs through the Registrar of Companies in Hamilton, and our team manages that relationship on your behalf.

Expanship's scope covers each stage of your entity's lifecycle in Bermuda:

- Document preparation, notarization, and legalization

- Registered agent and registered office provision

- Filing and liaison with the Registrar of Companies

- Annual return and compliance calendar management

- Economic substance monitoring where applicable

- Banking introduction and account opening support

Ready to move forward? Reach out to Expanship Bermuda to discuss your specific structure and timeline.

Frequently Asked Questions (FAQ)

The Exempted Company is the most frequently registered structure, primarily because it permits 100% foreign ownership and carries no corporate income tax obligation. Its flexibility across holding, trading, and finance functions makes it the default choice for international business.

An Exempted Company cannot conduct business within Bermuda except as permitted by its licence, whereas a Local Company is authorised to trade domestically. Local Companies are subject to the same tax-neutral environment but face greater ownership restrictions under the Companies Act 1981. Compliance requirements are broadly similar, though Exempted Companies have additional obligations tied to their economic substance declarations.

The Exempted Company and the Exempted Limited Partnership both offer meaningful confidentiality, as beneficial ownership information is held by the registered agent and not published on a public register. Nominee services are available, though disclosure obligations under the Proceeds of Crime Act 1997 and economic substance frameworks still apply. Share registers are not publicly accessible.

A sole individual can form an Exempted Company, as the Companies Act 1981 permits a single shareholder and a minimum of one director. Partnerships, whether general or limited, require at least two partners under their respective statutory frameworks. A Segregated Accounts Company also requires a duly licensed sponsor, making sole formation impractical without additional parties.

Foreigners may incorporate an Exempted Company, an Exempted Limited Partnership, a Segregated Accounts Company, or register as an Overseas Company without restriction on nationality. The Bermuda Monetary Authority must licence certain regulated activities regardless of the incorporator's origin. Local Companies, by contrast, require at least 60% Bermudian ownership under standard regulations.

Bermuda's Companies Act 1981 allows a company to re-register or convert under certain conditions, including conversion between company forms. Continuation from a foreign jurisdiction into Bermuda is also permitted, subject to BMA approval where regulated activities are involved. Not all conversions are available as of right; some require court approval or ministerial consent.

The Exempted Limited Partnership carries comparatively lighter statutory requirements than corporate structures, with no mandatory audit requirement absent a specific regulatory condition. However, all entities must maintain registered offices through a licensed service provider and file any required economic substance declarations with the Registrar of Companies.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.