Key Takeaways

- Saint Barthélemy's business entity types are drawn from French commercial law and registered through the Greffe du Tribunal Mixte de Commerce de Basse-Terre, which handles filings as part of the Guadeloupe judicial district.

- The SARL is the most commonly registered entity for small and medium businesses, while the SAS offers greater governance flexibility without the shareholder minimums required by the SA.

- Partnership structures such as the Société en Nom Collectif (SNC) impose unlimited liability on partners, making them unsuitable for founders seeking personal asset protection.

- Despite operating as a French collectivité d'outre-mer, Saint Barthélemy holds a distinct fiscal status that exempts it from most metropolitan French taxes, which remains a defining consideration for corporate planning.

Introduction to Entity Types in Saint Barthélemy

Saint Barthélemy is a French collectivity located in the northeastern Caribbean Sea, situated in the Leeward Islands approximately 35 kilometres southeast of Saint Martin. Governed under French law as an overseas collectivity (collectivité d'outre-mer) since 2007, the territory operates within the French legal framework while holding a distinct fiscal status that exempts it from most metropolitan French taxes.

Business registration and oversight fall under the jurisdiction of the Greffe du Tribunal Mixte de Commerce de Basse-Terre, the commercial court registry that handles company filings for Saint Barthélemy as part of the Guadeloupe judicial district.

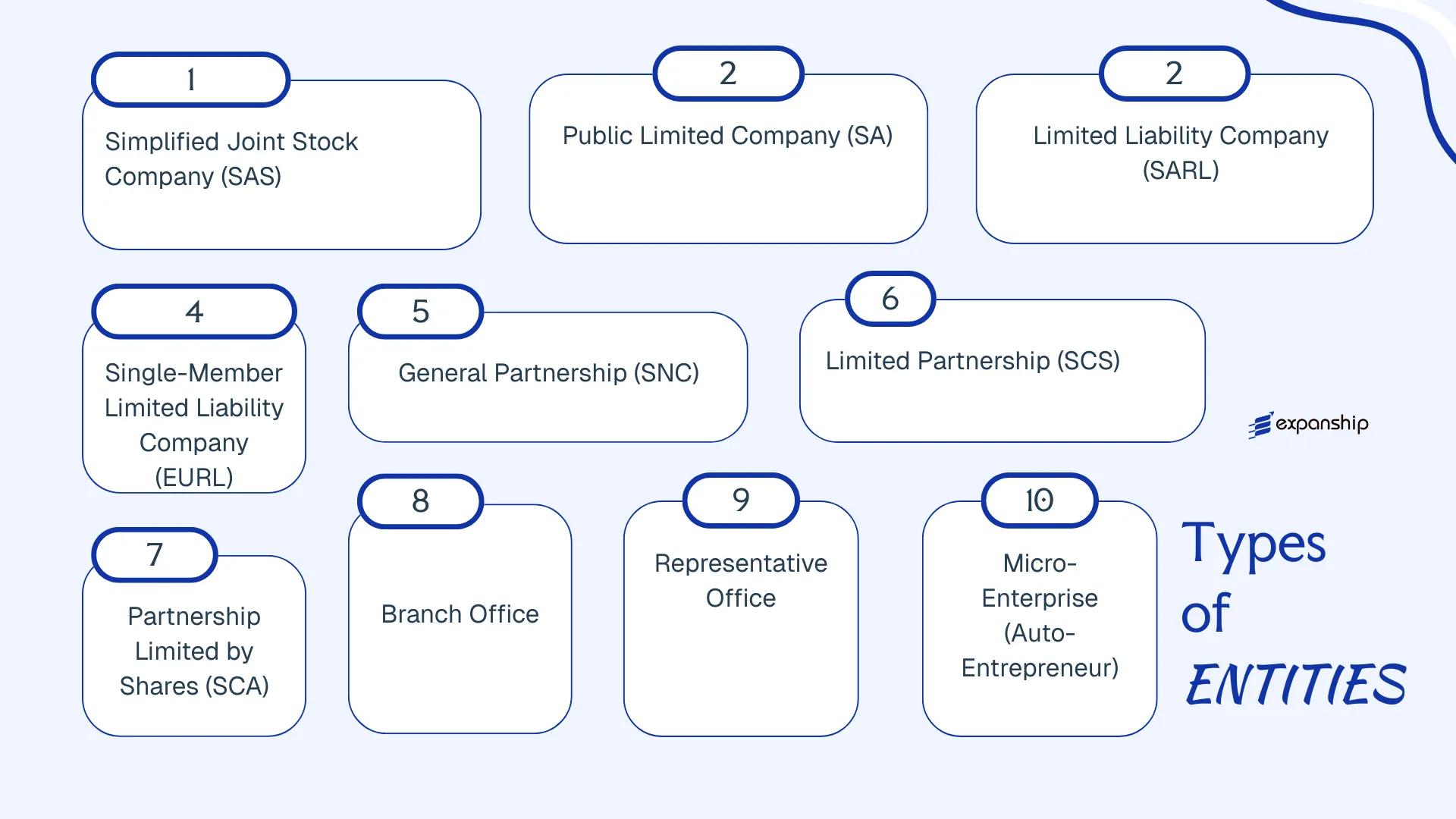

The territory's business entity types Saint Barthélemy incorporators can access are drawn from French commercial law. Available structures include the Société par Actions Simplifiée (SAS), Société Anonyme (SA), Société à Responsabilité Limitée (SARL), Entreprise Unipersonnelle à Responsabilité Limitée (EURL), Société en Nom Collectif (SNC), Société en Commandite Simple (SCS), Société en Commandite par Actions (SCA), branch offices, representative offices, and the Auto-Entrepreneur micro-enterprise regime.

Each of these Saint Barth company structures carries distinct requirements around capital, governance, liability, and registration — all examined in the sections that follow.

An Overview of Business Structures in Saint Barthélemy

French corporate law governs the full range of Saint Barthélemy corporate entities available for registration on the island, principally through the French Code de Commerce as applied within the collectivity's legal framework. Several distinct legal forms exist, from single-member limited liability companies to publicly traded structures and foreign branch registrations. Each form carries different implications for liability, governance, and taxation.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| SAS | Share company | Limited | Taxable | Yes | 1 shareholder | Greffe du Tribunal | Code de Commerce |

| SA | Share company | Limited | Taxable | Yes | 2 shareholders | Greffe du Tribunal | Code de Commerce |

| SARL | Limited liability | Limited | Taxable | Yes | 1–100 members | Greffe du Tribunal | Code de Commerce |

| EURL | Single-member LLC | Limited | Taxable / Pass-through | Yes | 1 member | Greffe du Tribunal | Code de Commerce |

| SNC | General partnership | Unlimited | Pass-through | Yes | 2+ partners | Greffe du Tribunal | Code de Commerce |

| SCS | Limited partnership | Mixed | Pass-through | Yes | 2+ partners | Greffe du Tribunal | Code de Commerce |

| SCA | Partnership-share hybrid | Mixed | Taxable | Yes | 4+ members | Greffe du Tribunal | Code de Commerce |

| Branch Office | Foreign extension | Parent liability | Taxable | Yes | Parent company | Greffe du Tribunal | Code de Commerce |

| Representative Office | Non-trading entity | Parent liability | Generally exempt | No | Parent company | Local authorities | French regulations |

| Auto-Entrepreneur | Sole trader | Unlimited | Micro-tax regime | Yes | 1 individual | URSSAF / CFE | Code de Commerce |

Each of these structures is examined in full in the sections below.

Société par Actions Simplifiée (SAS)

The SAS company Saint Barthélemy operates under French corporate law — specifically the provisions of the Code de commerce as amended by the law of 3 January 1994, which introduced this structure into the French legal order. As an overseas collectivity of France, Saint Barthélemy applies metropolitan French commercial legislation, giving the SAS full legal personality separate from its shareholders and limiting member liability to their capital contributions.

Structurally, the Société par Actions Simplifiée Saint Barth sits between a private limited company and a public one, offering considerable contractual freedom in how governance is arranged. The statuts (articles of association) can be drafted with significant flexibility, making internal governance arrangements highly customisable compared to more rigid French entity forms.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Société par Actions Simplifiée (SAS) | Separate legal personality; governed by French Code de commerce |

| Members | Shareholders (associés): minimum 1, no maximum | Single-shareholder variant is the SASU |

| Management | President (Président): minimum 1, no nationality restriction | Can be an individual or legal entity |

| Local Presence | Registered office (siège social) in Saint Barthélemy required | No statutory requirement for a local resident director |

| Share Capital | No statutory minimum; denominated in EUR | Capital must be fully defined in the statuts |

| Privacy | Shareholder register not publicly disclosed | Beneficial ownership reported to French financial authorities |

Focus Points

- Taxation: Saint Barthélemy has its own local tax regime distinct from metropolitan France; the territory levies no VAT and applies a local income tax, though corporate tax treatment depends on the entity's activity and residency status — mainland French corporate tax rules may apply where the entity is managed from France.

- Annual Compliance: Annual accounts must be filed; a statutory auditor (commissaire aux comptes) is mandatory once certain size thresholds are met.

- Economic Substance: No formal economic substance regime equivalent to those in British overseas territories applies, but tax residency claims must reflect genuine local management and control.

- Conversion: An SAS may be converted into an SA or SARL by shareholder resolution, subject to compliance with the relevant capital and membership requirements of the target form.

- Restrictions: SAS shares cannot be listed on a regulated stock exchange; public offerings of securities are prohibited.

Closing

SAS incorporation Saint Barthélemy suits holding structures, joint ventures, and businesses requiring bespoke shareholder arrangements, with its primary advantage being contractual freedom in governance. The main limitation is the administrative complexity of drafting sound statuts, which typically requires qualified legal counsel.

This entity is best suited for investors or groups establishing holding companies or multi-party ventures who require flexible shareholder arrangements under a recognised French legal framework.

Company Incorporation in Saint Barthélemy

Incorporate an SAS or other entity type in Saint Barthélemy with end-to-end support from Expanship.

Société Anonyme (SA)

The Société Anonyme Saint Barthélemy SA is governed by French corporate law, specifically the provisions of the Code de commerce, which Saint Barthélemy applies as part of its legal alignment with French commercial legislation. As a collectivité d'outremer, the territory does not maintain a separate commercial code, so French statutory rules on the SA structure apply directly.

Structured as a public limited company, the SA carries full separate legal personality and offers shareholders limited liability. It is suited to larger operations or those planning to raise capital from multiple investors, given its capacity to issue shares to the public under regulated conditions.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Société Anonyme (SA) | Separate legal personality under French commercial law |

| Members | Shareholders (min. 2; min. 7 if publicly listed) | No statutory maximum |

| Governance | Board of Directors (min. 3, max. 18) or Directoire with Supervisory Board | Two structural models available under French law |

| Local Presence | Registered office in Saint Barthélemy required | No statutory requirement for a local resident director |

| Share Capital | Minimum EUR 37,000 (non-listed); EUR 225,000 (listed) | At least half must be paid up on incorporation |

| Privacy | Shareholder identity disclosed in public filings | Limited privacy compared to simpler structures |

Focus Points

- Taxation: Saint Barthélemy does not levy corporate income tax, personal income tax, or VAT on locally sourced activities; French tax obligations may apply to non-resident shareholders depending on treaty status.

- Annual Compliance: Statutory auditors (commissaires aux comptes) are mandatory; annual accounts must be filed with the Greffe du Tribunal de Commerce.

- Economic Substance: No formal substance legislation mirrors the EU framework here, but commercial reality and French tax residency rules govern where decisions are treated as made.

- Treaty Access: Access to French tax treaties is not automatic for entities incorporated in Saint Barthélemy; treaty eligibility depends on tax residence determination.

- Conversion: An SA may be converted into an SAS under French law without dissolution, subject to shareholder resolution and updated statuts.

Closing

The SA structure is suited to established businesses, joint ventures with multiple institutional shareholders, or operations requiring external capital investment. Its principal advantage is the capacity to issue publicly traded shares; the mandatory auditor requirement and higher minimum capital threshold, however, make it administratively heavier than most other entity forms available in the territory.

Best suited for larger enterprises or joint ventures requiring a formal governance structure and the ability to raise capital from multiple investors.

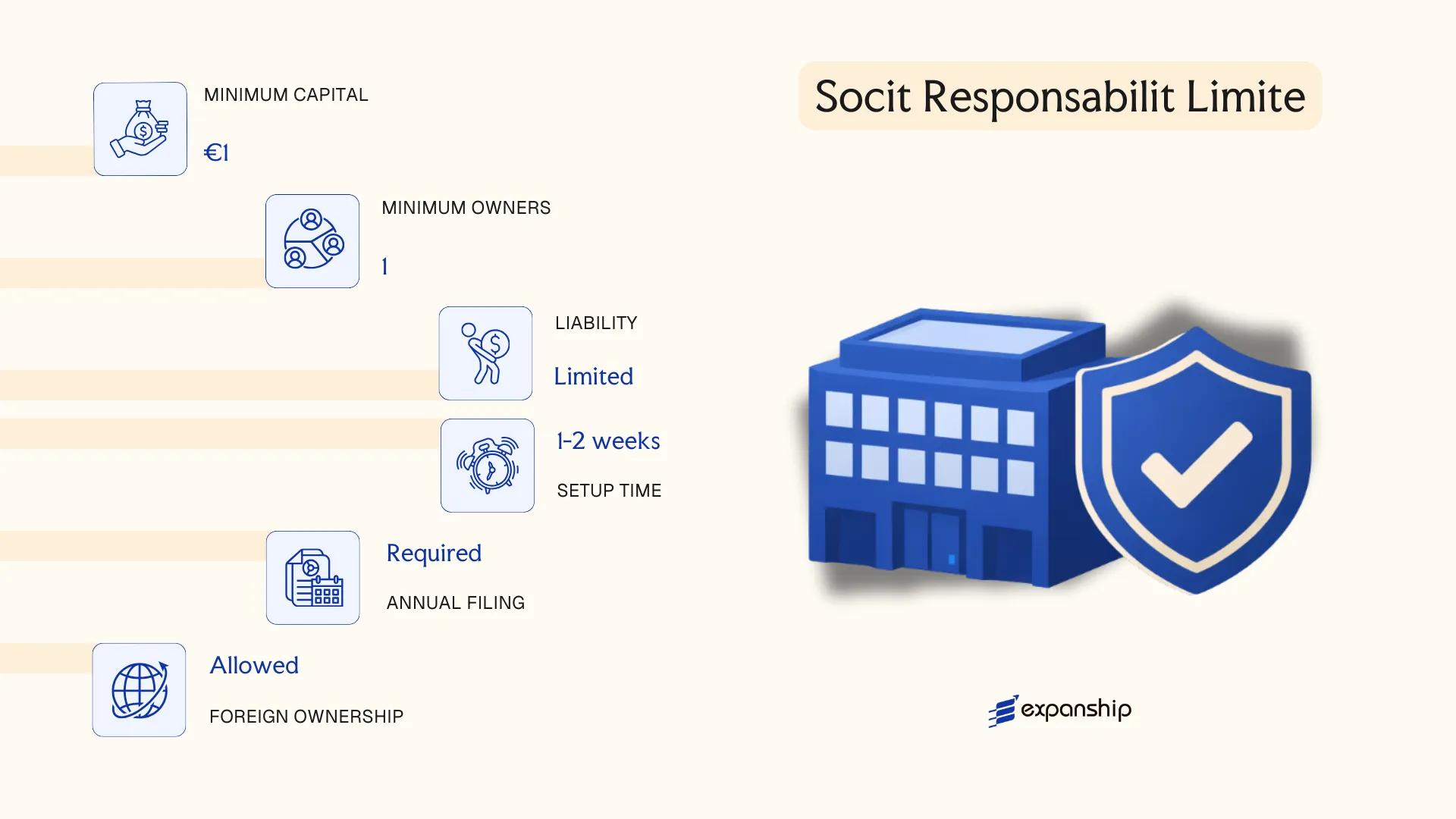

Société à Responsabilité Limitée (SARL)

SARL formation Saint Barthélemy follows the French corporate framework that applies across the collectivity, specifically the provisions of the French Code de Commerce. Introduced in its modern form through legislation that has been updated progressively under French law, the SARL is a hybrid structure combining limited liability protection with the operational flexibility typically associated with smaller, closely held businesses.

As a distinct legal entity, the SARL holds rights and obligations separate from its associates. Liability of each associate is capped at the amount of their capital contribution, shielding personal assets from business debts.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Société à Responsabilité Limitée | Separate legal personality; limited liability entity |

| Members | Associates (associés); 1–100 | Single-member variant is the EURL |

| Management | One or more gérants (managers) | Need not be an associate; natural persons only |

| Local Presence | Registered office required in Saint Barthélemy | No statutory requirement for a local resident gérant |

| Share Capital | No statutory minimum under current French law | Capital divided into parts sociales; not freely transferable |

| Privacy | Associates listed in public registration filings | Beneficial ownership disclosure required under French AML rules |

Focus Points

- Taxation: The SARL is subject to French corporate income tax (Impôt sur les Sociétés); Saint Barthélemy's autonomous tax regime means local territorial rules may apply to qualifying income, with no local VAT — French TVA does not apply in the collectivity.

- Annual Compliance: Annual accounts must be filed with the Registre du Commerce et des Sociétés (RCS); statutory audit requirements apply only beyond defined size thresholds.

- Transfer Restrictions: Parts sociales transfers to third parties require approval from associates representing at least half of the share capital.

- Conversion: An SARL may convert to an SAS or SA, subject to compliance with the procedural requirements of the Code de Commerce.

- Treaty Access: Access to French tax treaties is not automatic for Saint Barthélemy-registered entities, given the collectivity's status as an Overseas Collectivity outside the EU fiscal territory.

Closing

The SARL suits trading operations, family-held businesses, and local service firms where ownership control and liability separation are both priorities. Its principal advantage is the simplicity of governance relative to an SA; the main limitation is the restriction on transferring ownership interests, which can complicate equity restructuring or external investment rounds.

Best suited for small to mid-sized businesses with a defined group of associates who require limited liability without the administrative weight of a full public company structure.

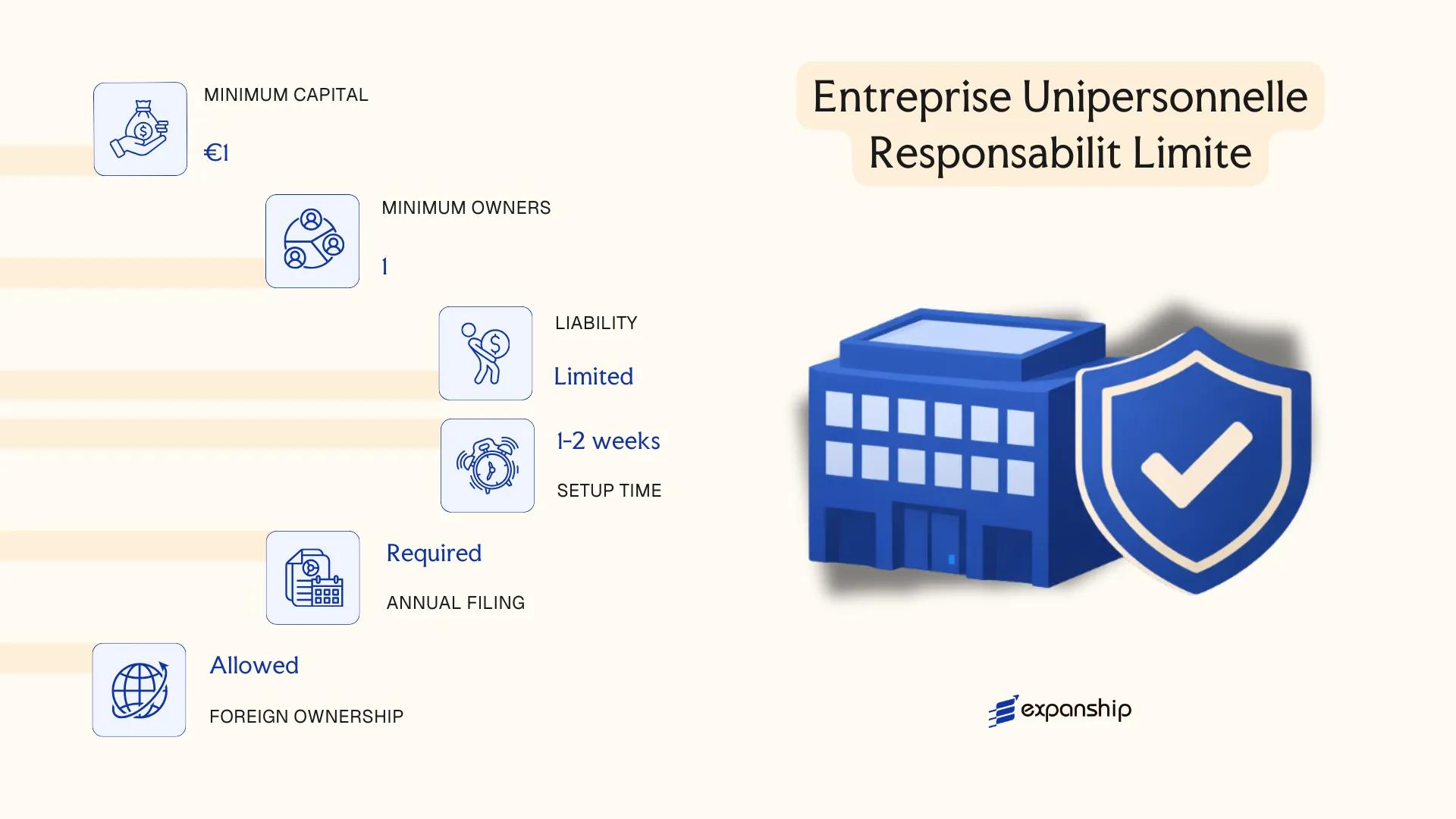

Entreprise Unipersonnelle à Responsabilité Limitée (EURL)

The EURL single member company Saint Barthélemy is the single-shareholder variant of the SARL, governed by the same French commercial law framework applicable through the island's collectivity status. As a distinct legal entity, it carries separate legal personality, meaning the sole shareholder's personal assets remain protected from the company's liabilities.

Structurally, the Entreprise Unipersonnelle à Responsabilité Limitée Saint Barth sits between a sole proprietorship and a multi-member limited liability company. The single shareholder may also serve as the gérant (manager), consolidating ownership and management within one individual.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Single-member limited liability company | Variant of SARL; converts to SARL if a second member joins |

| Members | 1 sole shareholder (associé unique) | Individual or legal entity; shareholder may act as gérant |

| Management | Gérant (manager) | Appointed by the sole shareholder; may be the shareholder themselves |

| Local Presence | Registered office required in Saint Barthélemy | No mandatory local agent under current rules |

| Capital | No statutory minimum (€1 minimum in practice) | Defined in articles of association; must be fully subscribed |

| Privacy | Shareholder identity disclosed in public filings | Accounts filed with the Registre du Commerce et des Sociétés |

Focus Points

- Taxation: Subject to French income tax (IR) by default for individual shareholders, with an option to elect corporate tax (IS); no local corporate income tax applies in Saint Barthélemy, and no VAT is levied on the island.

- Annual compliance: Annual accounts must be filed with the Registre du Commerce et des Sociétés (RCS); general meetings are replaced by sole shareholder resolutions recorded in writing.

- Conversion: Automatic conversion to a standard SARL occurs upon the admission of a second member, requiring updated articles and RCS notification.

- Restrictions: The EURL cannot issue shares to the public or list on a stock exchange.

- Treaty access: Access to French tax treaties may be available depending on the specific treaty's territorial scope and the shareholder's residency.

Closing

The EURL suits sole founders or individual entrepreneurs seeking limited liability for a trading, consulting, or holding activity without the overhead of a multi-member structure. The primary constraint is scalability — bringing in additional shareholders triggers mandatory conversion to a SARL.

Individual entrepreneurs or sole investors who require liability protection and anticipate operating as a single-owner business for the foreseeable future.

Partnership Structures [Société en Nom Collectif (SNC), Société en Commandite Simple (SCS), Société en Commandite par Actions (SCA)]

Partnership structures in Saint Barthélemy follow French commercial law, specifically the Code de Commerce, which Saint Barth applies as part of its legislative alignment with France despite its status as a French overseas collectivity. Each of the three forms — the Société en Nom Collectif (SNC), Société en Commandite Simple (SCS), and Société en Commandite par Actions (SCA) — carries distinct liability profiles and governance mechanisms.

All three structures are registered with the Registre du Commerce et des Sociétés (RCS) and possess separate legal personality upon incorporation.

Key Characteristics

| Requirement | SNC | SCS | SCA |

|---|---|---|---|

| Legal Form | General partnership | Limited partnership | Partnership limited by shares |

| Members | 2+ associés (all general partners) | 1+ general partner (commandité) + 1+ limited partner (commanditaire) | 1+ general partner (commandité) + 3+ shareholder-limited partners (commanditaires) |

| Liability | Unlimited, joint and several for all partners | Unlimited for general partners; limited to contribution for limited partners | Unlimited for general partners; limited to share value for limited partners |

| Capital | No statutory minimum | No statutory minimum | Minimum €37,000 (aligned with French SA threshold) |

| Local Presence | Registered office in Saint Barthélemy required | Registered office required | Registered office required |

| Privacy | Partners disclosed in RCS filings | Partners disclosed in RCS filings | Shareholder register maintained; general partners publicly disclosed |

Focus Points

- Taxation: No corporate income tax, no VAT, and no withholding tax apply in Saint Barthélemy; SNCs are fiscally transparent by default, with profits taxed at partner level, while SCS and SCA taxation follows the partner's applicable regime.

- Annual Compliance: Annual accounts must be filed with the RCS; SNCs and SCS partnerships below certain thresholds may benefit from simplified reporting.

- Economic Substance: No formal economic substance legislation mirrors that of some offshore jurisdictions; standard French commercial activity requirements apply.

- Treaty Access: Access to France's tax treaty network is not automatically extended to Saint Barthélemy, given its exclusion from EU VAT territory and specific fiscal status.

- Conversion: An SNC may be converted to an SARL or SAS subject to partner consent and compliance with Code de Commerce conversion procedures.

Sub-Types

Société en Nom Collectif (SNC)

All partners hold unlimited joint and several liability, making this structure uncommon for passive investors. It is typically used by professional firms or family businesses where partners are actively involved in management.

Société en Commandite Simple (SCS)

The SCS separates active general partners from passive limited partners, whose liability does not exceed their agreed contribution. This form suits structures where a managing partner operates alongside silent capital contributors.

Société en Commandite par Actions (SCA)

The SCA combines partnership governance with a share-based capital structure, making it suitable for larger enterprises or holding arrangements requiring transferable equity while retaining a managing general partner with control. The minimum capital requirement of €37,000 distinguishes it from the other two forms.

Closing

Partnership structures in Saint Barthélemy are used primarily for family businesses, professional services, and holding arrangements where the parties have a pre-existing relationship and defined roles. The absence of local corporate taxation is an advantage, but unlimited liability exposure for general partners in the SNC and SCS remains a material drawback for most commercial ventures.

These structures are best suited for closely held businesses, professional partnerships, or holding entities where partners accept defined liability roles and seek fiscal transparency.

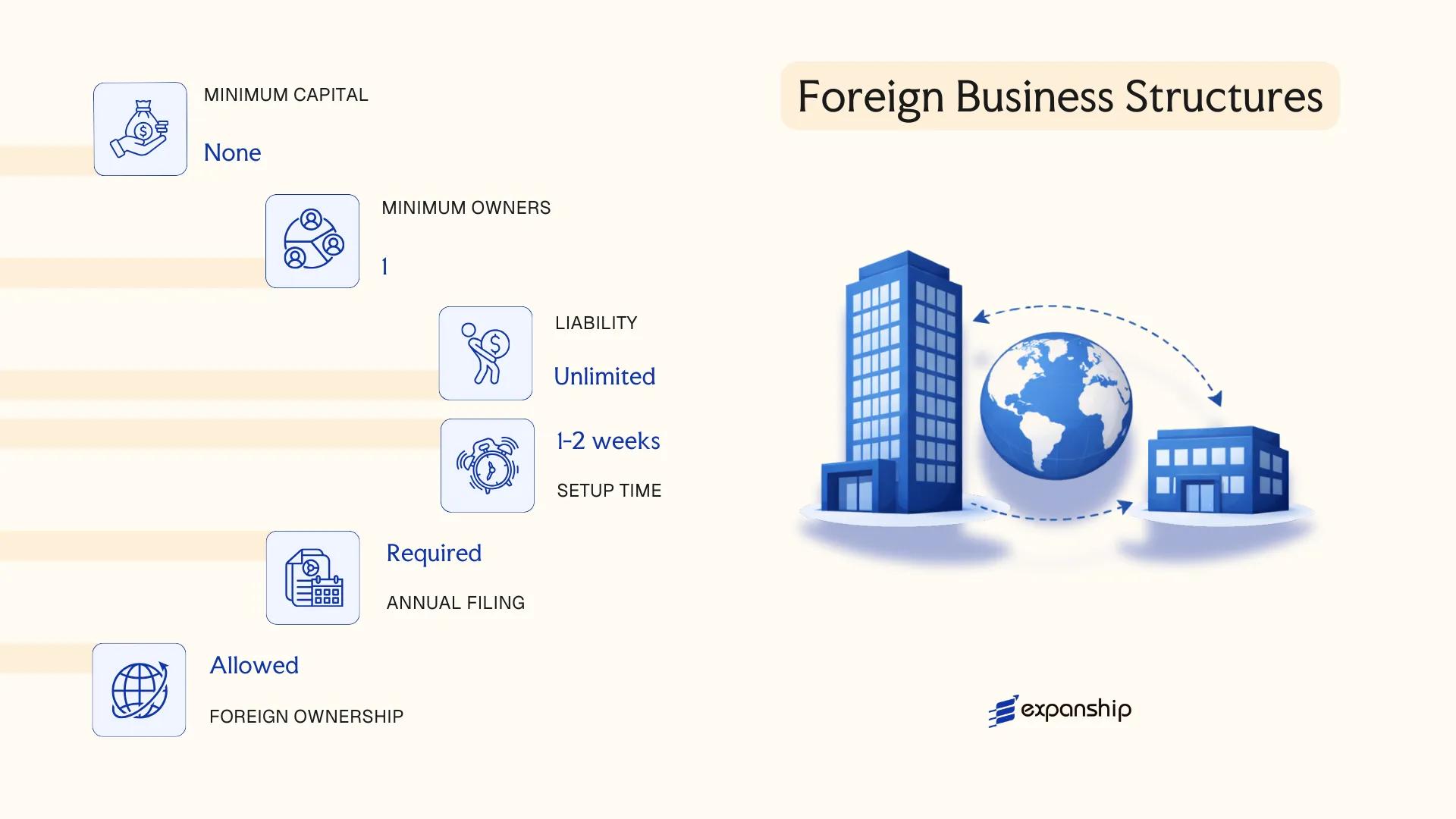

Foreign Business Structures [Branch Office, Representative Office]

Establishing a foreign branch office in Saint Barthélemy follows the French legal framework, as the territory operates under French law with certain local adaptations administered through the Collectivité de Saint-Barthélemy. A branch office is not a separate legal entity; it remains an extension of the parent company, which bears full liability for the branch's obligations.

Registration is handled through the Centre de Formalités des Entreprises (CFE) and requires filing with the Registre du Commerce et des Sociétés (RCS). The parent company must appoint a local representative and provide certified constitutional documents, translated into French where necessary.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Branch: extension of parent; Representative Office: non-trading presence | Neither holds separate legal personality |

| Representative | Appointed individual resident or legally authorised in France/Saint Barthélemy | Mandatory for both structures |

| Local Presence | Registered address required; registered with RCS | Physical office address needed for branch |

| Capital | No minimum capital requirement | Parent company's capital remains relevant for liability |

| Liability | Parent company bears full liability | No liability ring-fencing at branch level |

| Privacy | Parent company details disclosed in public registry | Beneficial ownership follows French transparency rules |

Focus Points

- Taxation: Branches are subject to French corporate tax rules applicable in Saint Barthélemy; no local income tax applies, but French VAT and withholding tax provisions may apply depending on activity.

- Economic Substance: The branch must reflect genuine operations tied to the parent's declared activities.

- Annual Compliance: Accounts must align with the parent's financial statements; annual filings with the RCS are required.

- Treaty Access: Access to French tax treaties depends on the parent company's residence jurisdiction and treaty provisions.

- Restrictions: Representative offices are prohibited from generating revenue or conducting direct commercial transactions.

Sub-Types

Branch Office

A branch office can conduct full commercial operations on behalf of the parent entity and is treated as a taxable presence. It suits foreign firms seeking operational activity without incorporating a separate local company.

Representative Office

A representative office is restricted to promotional, liaison, and market research activities. No revenue-generating transactions are permitted, making it appropriate for firms assessing the local market before committing to full incorporation.

Closing

Foreign firms with existing French-law entities or those operating across French territories frequently use the branch structure for operational continuity, though the absence of liability separation is a material drawback for risk-sensitive businesses.

Best suited for established foreign companies with existing French corporate structures seeking operational presence without full local incorporation.

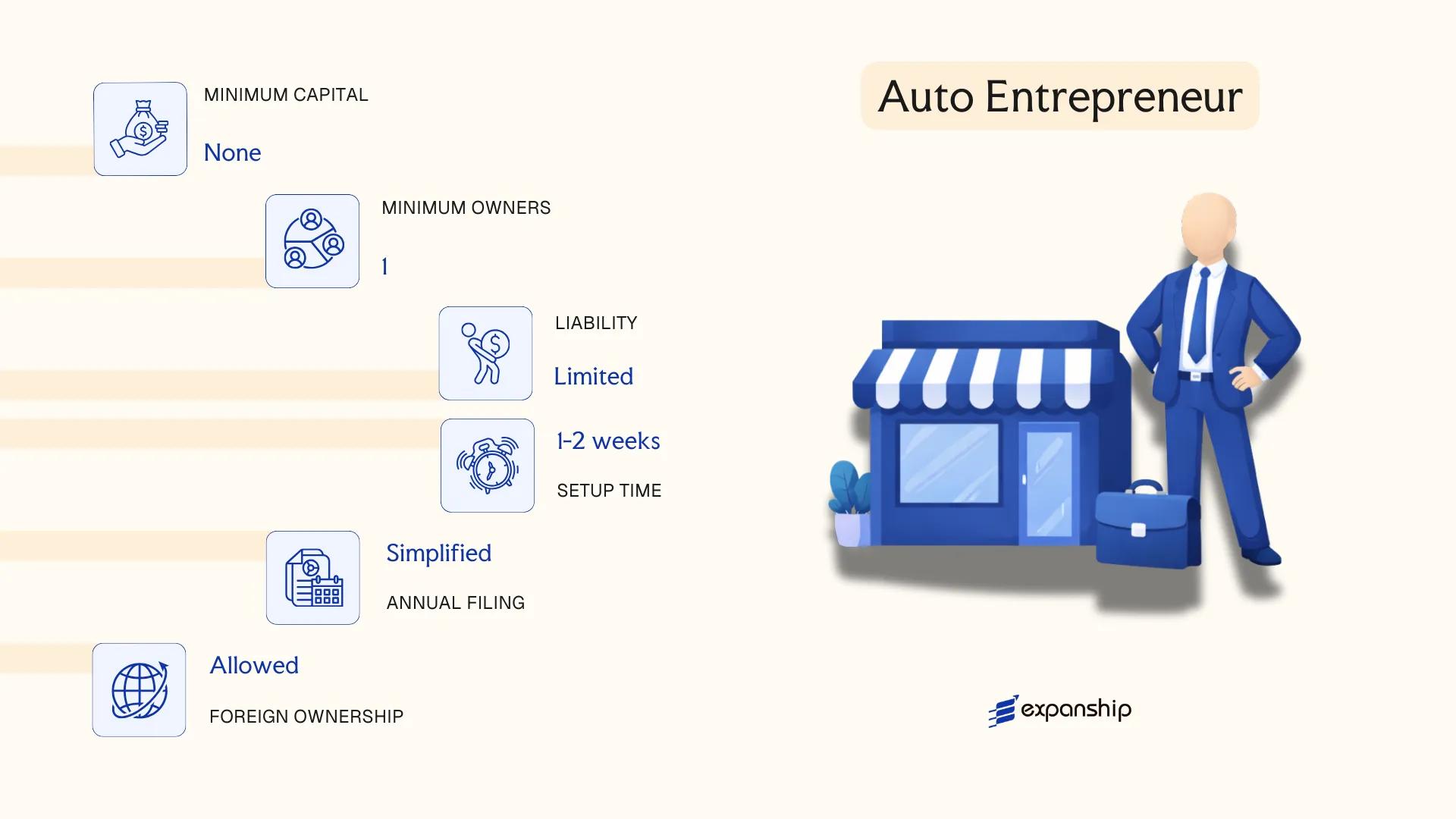

Auto-Entrepreneur (Micro-Enterprise)

The auto-entrepreneur regime in Saint Barthélemy operates under French national legislation, specifically the Loi de modernisation de l'économie (LME) of 2008, which introduced this simplified sole trader status across French territories. As a collectivité d'outremer, Saint Barth applies this framework directly. The auto-entrepreneur carries no separate legal personality — the individual and the business are legally the same entity, meaning personal assets are not shielded from professional liabilities.

Registration for this micro-enterprise status is handled through the Centre de Formalités des Entreprises (CFE), and the process is straightforward by design, with no minimum capital requirement.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sole proprietorship (micro-enterprise) | No legal separation between owner and business |

| Members | Single proprietor | One individual only; no partners or shareholders |

| Local Presence | Registered business address required | No mandatory registered agent |

| Capital | No minimum | No capital injection required at formation |

| Revenue Ceiling | Annual turnover thresholds apply | Set under French tax code; separate limits for services and goods |

| Privacy | Owner's name publicly linked to the business | No anonymity available |

Focus Points

- Taxation: Subject to the micro-fiscal regime with flat-rate income tax and social charges applied to gross turnover; no corporate tax, VAT only applies above specific thresholds.

- Annual Compliance: Periodic turnover declarations to the tax authority; no statutory audit required.

- Conversion: Can convert to a full commercial structure (such as EURL or SASU) if revenue growth exceeds threshold limits.

- Restrictions: Cannot be used for certain regulated professions or activities requiring a commercial company structure.

Closing

This status suits independent contractors, freelancers, and micro-scale traders seeking a low-cost, low-administration entry point into commercial activity. The primary limitation is the absence of liability protection, exposing the proprietor's personal assets to business debts.

Best suited for individual service providers or tradespeople testing a new activity with limited startup costs and modest projected revenues.

How to Choose the Right Entity Type in Saint Barthélemy

Choosing the right company structure in Saint Barthélemy is not a formality — the entity you register determines your tax position, liability exposure, compliance burden, and operational capacity from day one.

Why Your Entity Choice Matters

- Selecting an entity without substance capacity when local substance rules apply can trigger reporting failures and associated financial penalties.

- Choosing a tax-exempt structure when you need access to France's tax treaty network means withholding tax reductions available under those treaties cannot be claimed.

- Forming a share-capital company when a foundation or trust would better serve asset protection locks your structure into annual shareholder obligations that are unnecessary for passive holding purposes.

- Registering an entity type that requires audited financial statements for a single-person consultancy introduces recurring costs with no corresponding compliance benefit.

Key Factors to Consider

- Business Activity: Active trading, passive asset holding, and regulated sectors each point to different structures under French commercial law as applied in the territory.

- Ownership and Management: Single-owner operations align with the EURL, while multi-party arrangements with governance requirements favour the SAS or SA.

- Tax Objectives: Your eligibility for Saint Barthélemy's local tax regime depends on the entity type and the nature of the income generated.

- Substance Capacity: If you cannot realistically maintain staff and decision-making locally, the entity type must reflect that operational reality.

- Privacy Requirements: Public disclosure obligations vary across structures; nominee arrangements may be required where confidentiality is a priority.

- Exit Strategy: Not all entity types permit redomiciliation or conversion — verify this before formation if restructuring is foreseeable.

The primary legislation governing commercial entities in the territory is the French Commercial Code (*Code de commerce*), which applies in Saint Barthélemy by extension.

Compliance Services for Companies in Saint Barthélemy

Maintain good standing with ongoing compliance support tailored to your entity type and obligations under applicable French commercial law.

Conclusion

Incorporating a company in Saint Barthélemy requires selecting a structure that aligns with your operational scope, ownership preferences, and liability considerations. The SAS suits founders who want governance flexibility without the shareholder minimums of an SA. The SA fits larger ventures requiring public capital-raising capacity. The SARL remains the most commonly registered entity for small and medium businesses, while the EURL serves single founders who need limited liability without a partner. Partnership structures like the SNC carry unlimited liability, making them appropriate only where partners accept that exposure. Branch and representative offices serve foreign firms testing the market before committing to a local entity.

Governed under French commercial law through the Collectivité of Saint-Barthélemy, the jurisdiction's regulatory framework continues to reflect metropolitan French norms, with its territorial tax status remaining a defining characteristic for corporate planning purposes. Expanship's team can help you determine which structure fits your specific situation.

How Expanship Can Assist You

Expanship company formation Saint Barthélemy services are built around the specific structures this jurisdiction offers — from the SAS and SARL to the auto-entrepreneur regime — and the compliance requirements tied to each. Saint Barthélemy operates under French corporate law while maintaining its distinct territorial tax status, and filings run through the Greffe du Tribunal de Commerce de Basse-Terre as the competent registrar. Our team works directly within that framework on your behalf.

From initial document preparation to post-incorporation obligations, Expanship covers the full operational setup:

- Corporate document preparation and notarization

- Registered agent and registered office provision in Saint Barthélemy

- Filing coordination with the Greffe du Tribunal de Commerce de Basse-Terre

- Ongoing compliance and annual obligation management

- Banking introduction assistance for your entity

Contact Expanship Saint Barthélemy to discuss your incorporation requirements with our corporate services team.

Frequently Asked Questions (FAQ)

The Société à Responsabilité Limitée (SARL) is the most frequently registered structure. Its combination of limited liability, a single-shareholder variant (EURL), and relatively low capital requirements makes it the default choice for small to mid-sized businesses.

Both structures offer limited liability and can be formed with a single euro of share capital, but their governance frameworks diverge significantly. The SAS allows shareholders to define management rules contractually through the company's statuts, whereas the SARL operates under a more prescriptive statutory regime. For foreign investors seeking flexibility in shareholder agreements, the SAS is generally more accommodating.

The SAS offers comparatively greater confidentiality because its shareholder agreements and internal governance documents are not filed in the public register. Beneficial ownership information is reported to the Registre des Bénéficiaires Effectifs, but detailed share transfer conditions remain private. Nominee arrangements are legally permissible in France and its collectivities, though they carry fiduciary and disclosure obligations.

No. The EURL and the unipersonal SAS can each be formed by one person. The SARL requires at least two associés unless structured as an EURL. Partnership forms such as the SNC and SCS require a minimum of two partners, and the SA requires at least two shareholders in its standard configuration.

Yes. As a French collectivity, Saint Barthélemy applies French corporate law, which does not restrict company formation based on the nationality of shareholders or directors. Foreign nationals can establish an SAS, SARL, or SA without a local partner. A registered address within the territory is required, and non-EU directors conducting management activities may need to verify their residency or work authorization status under French regulations.

French corporate law, applicable in Saint Barthélemy, permits transformation between entity types. A SARL can be converted into an SAS, and an SAS can be converted into an SA, subject to shareholder approval and compliance with the relevant capital and governance thresholds. The transformation does not create a new legal entity; the original firm retains its legal personality, contracts, and registration history.

The SAS, SA, SARL, EURL, SCS, and SCA all hold distinct legal personality upon registration with the Greffe du Tribunal de Commerce. The SNC also holds legal personality. The Auto-Entrepreneur regime, by contrast, does not create a separate legal entity; the individual and the business remain legally unified, which exposes personal assets to professional liabilities.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.